Summary

- 121 SAS is an active French company with a Paris registered office and operating locations around Montpellier. Its legal purpose was broadened in 2025 to telecom-network operation, server and data hosting, equipment sales and related advice. It presents a broad fibre, satellite, mobile, private-cloud and integration offer, but public evidence does not establish owned national fibre, data-centre ownership, customer numbers or current revenue.

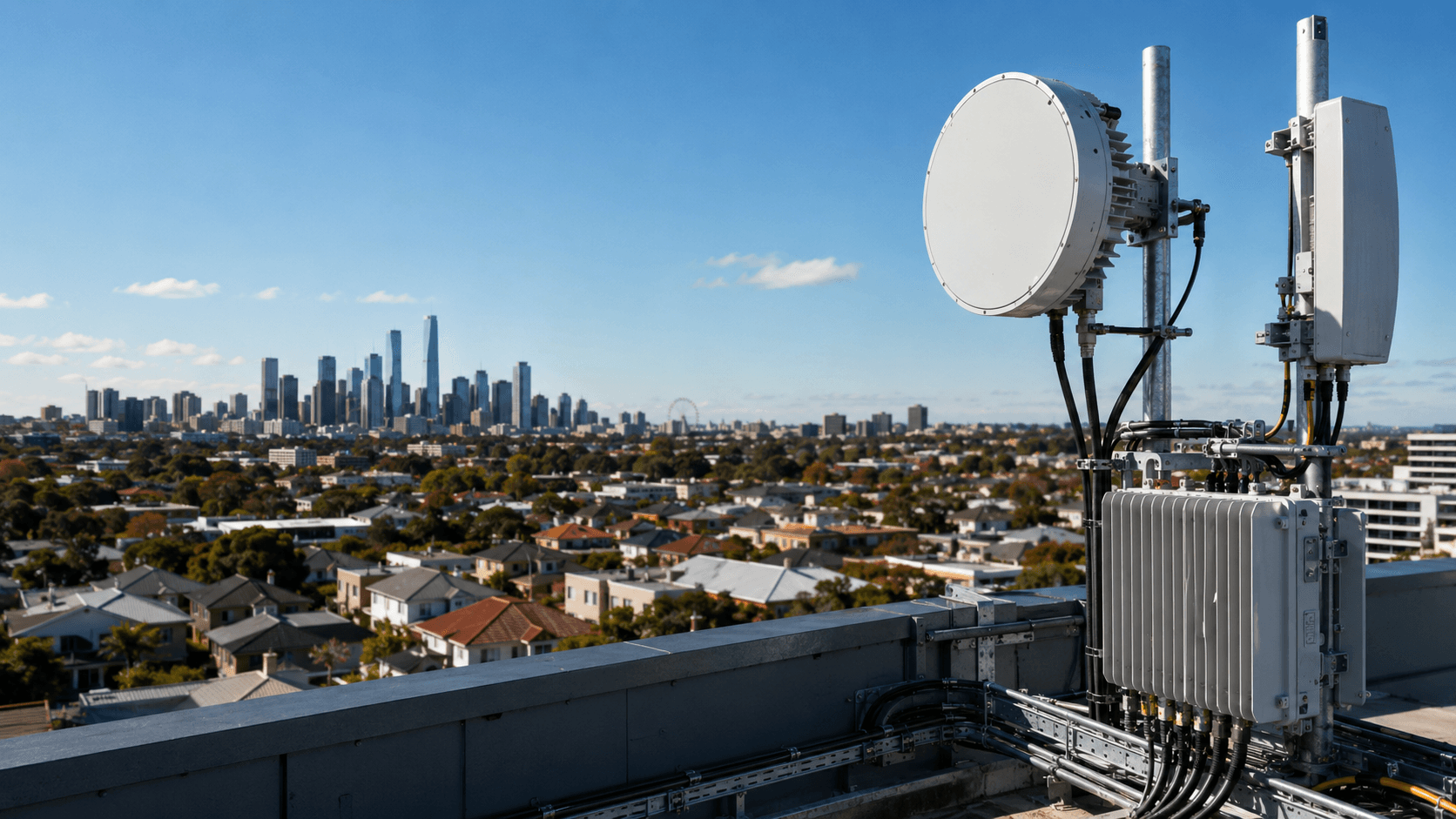

- The network footprint is real but modest and transitional. AS214877 originated one IPv4 /24 and no IPv6 on 10 July 2026, with Cogent and Zayo observed as neighbours. An older provider-independent /24 assigned to 121 remained originated through OC3 Network's AS8921 and served 121's own web and mail systems. Those records show operational capability and supplier plurality, not proven physical route diversity or independence.

- Historical accounts are too old to validate the present strategy. The pre-expansion company generated EUR255,734 of revenue and EUR46,893 of net profit in 2022, while the smaller business absorbed in 2024 generated EUR100,700 and lost EUR20,028. Later accounts are confidential. The investment case turns on undisclosed facts: recurring revenue, gross margin after wholesale access and colocation, renewal rates, top-customer exposure, response staffing, maintenance capital, service credits and whether apparently separate links share ducts, buildings or suppliers.

Independence is valuable only when somebody pays for it

There is a sensible commercial instinct behind 121's move toward operator status. A pure reseller buys a connection from a larger carrier, adds account management and passes most of the economics upstream. Its customer may value one invoice and one person to call, but the reseller controls neither the fault domain nor the restoration queue. When a circuit fails, its margin can disappear into support hours and service credits while the underlying carrier decides when the line returns.

Owning more control can improve that bargain. A provider with its own routing policy can move traffic between upstream networks. One that controls optical equipment can light more capacity without replacing the physical strand. A provider present in several data centres can place workloads and backup copies in different facilities. An engineering team that designs the customer's local network can make the access line, firewall, Wi-Fi, cloud and recovery plan work as one service. Each added layer creates an opportunity to charge for continuity rather than merely bandwidth.

The opportunity is especially relevant as French business connectivity shifts to fibre. Arcep's 2026 enterprise study found that 85% of internet-connected businesses with fewer than 50 employees had at least one fibre offer, rising to 88% among businesses with 50 to 499 employees and 99% among those with 500 to 4,999. Basic fibre is no longer scarce enough to sustain a large premium by itself. The sellable difference lies in guaranteed restoration, diverse backup, security, application continuity and a supplier that accepts responsibility when several components interact.

That is the demand 121 is addressing. Its current public offer combines dedicated and dark fibre, satellite, 4G or 5G connectivity, VPNs, private cloud, hosting, monitoring, maintenance and network integration. It says it can supply dark-fibre capacity from 10 to 800Gbps, integrate satellite service for remote locations or backup, and configure automatic failover between access types. This is not the catalogue of a household broadband seller. It is an enterprise proposition for customers whose cost of disconnection is higher than the monthly price of a commodity line.

The hard part is that control is never absolute. Dark fibre still runs through somebody's duct. A router still sits in somebody's facility and uses somebody's power. Internet traffic still leaves through upstream carriers. Satellite backup depends on a separate global network. Private cloud uses servers that age, licences that renew and technicians who must respond. The customer can buy the appearance of one accountable provider, but 121 has to pay every contributor beneath that appearance.

The core economic question is therefore not whether redundancy has value. It plainly does. It is whether 121 can retain enough of that value after wholesale access, colocation, equipment, field work and support. A network that costs twice as much to build and operate but commands only a modest premium is not independent in an economic sense. It is an expensive resale platform.

The legal company has changed faster than its disclosed accounts

The corporate identity is clear. France's public company-search service identifies SIREN 840 658 082 as the active company 121, with the sigle CERF, legal form SAS, a registered office at 10 rue de la Bourse in Paris and three open establishments. It classifies the principal activity as data processing, hosting and related activities. The same legal identifier appears in 121's RIPE organisation record, joining the commercial company to the network registration without making the registration the company itself.

The operating geography is less Paris-centred than the registered office suggests. The government record lists active establishments at 24 Cours Gambetta in Montpellier and at a business zone in Claret, north of the city. The company contact page directs customers to the Montpellier address. The Paris office is commercially useful for national sales and legal presence, but the public record does not disclose staff by site, a network operations centre, warehouse capacity or field-team coverage.

The name also conceals a recent strategic rewrite. The business began in 2018 as Compagnie Europeenne pour le Reseau et la Fibre, with network construction, exploitation and project support in its purpose. Public notices presented by Pappers show that in May 2025 it expanded the purpose to operating and renting telecom networks in Europe, hosting servers or data, selling and renting network and computing equipment, and advising on telecom and internet projects. Its statistical classification was subsequently updated to hosting and related activities.

That matters because the latest visible financial series belongs to the earlier business. In 2022, before the present operator proposition was fully assembled, the company reported EUR255,734 of revenue, EUR108,000 of EBITDA and EUR46,893 of net profit. Revenue had risen from EUR142,080 in 2020 and EUR206,233 in 2021. Net margin in 2022 was 18.3%, while cash was EUR94,500, financial debt EUR88,200 and equity EUR112,000. Those are healthy ratios for a small services company. They do not prove that a capital- and support-intensive network offer earns the same return.

The present business also contains another lineage. In January 2024, the company absorbed 121 Digital Group, a consultancy whose registered purpose covered network projects and digital services. The published merger terms valued the absorbed assets at EUR314,979, liabilities at EUR214,979 and net contribution at EUR100,000. The merger took accounting and tax effect from 1 January 2023, and the absorbed company was dissolved without liquidation.

The absorbed operation was not a large growth engine in its last disclosed year. 121 Digital Group's accounts presentation reports 2022 revenue of EUR100,700, EBITDA of EUR43,600 and a net loss of EUR20,028. It carried EUR187,000 of financial debt against EUR95,000 of equity, and its reported customer-payment period was 223 days. The merger could still make strategic sense by consolidating brand, customer relationships and network know-how. But the numbers warn against describing the combination as scale. Combined 2022 revenue of the two legal companies was roughly EUR356,000, before eliminating any transactions between them, and before the later operator build-out.

Current capital is EUR50,000. In 2025, a newly formed holding company, Scultore & Associes, became president of 121. Its registry presentation says the holding company's capital increased from EUR1,000 to EUR293,800 through a contribution in kind. That is evidence of corporate reorganisation, not evidence of EUR292,800 of new cash available for routers, fibre or payroll.

The public financial gap is consequently large. Accounts for 2023 and 2024 were filed under confidentiality, and no segment data show connectivity revenue, hosting revenue, recurring contracts, capital spending or operating cash. The government's latest available employee-size band is one to two people for 2023, before the recent expansion. Contractors, related companies and outsourced support may extend capacity, so that band is not a current headcount. It does, however, put the burden on 121 to show how a broad 24-hour reliability promise is staffed and financed.

Four revenue engines have to share one cost base

121's offer can be understood as four revenue engines. The first is connectivity. A business pays for dedicated fibre, dark fibre, an internet circuit, a private inter-site link or a combination of fibre and wireless backup. Contracts are likely to include installation, a recurring access charge, bandwidth, equipment rental and optional restoration commitments. None of 121's public pages gives a tariff, contract duration or service-credit schedule, so this remains a quote-led business.

The second engine is hosting and private cloud. 121 says it can place customer clusters in French Tier III data centres, provide private-cloud environments, replication, immutable backup and housing. This can create recurring monthly revenue and higher switching costs than a circuit alone. It can also turn an access customer into a wider account: the customer connects sites to workloads hosted by the same provider and pays for backup, storage, security and administration around them.

The third engine is integration. The company offers audit, network architecture, deployment of switches, firewalls and Wi-Fi, LAN and WAN segmentation, VPN configuration, monitoring and maintenance. Project work can provide upfront cash and expose 121 to a customer's broader technology budget. It can also become bespoke labour that does not scale. A design that is reused across similar multi-site customers has attractive economics. A one-off design with unusual hardware and permanent support obligations can consume its initial margin over years.

The fourth engine is accountability. This is not a separate technical product, but it is the reason the first three can command a premium. The customer buys one supplier to diagnose whether a problem sits in the local network, the access circuit, routing, hosting or security. A small local provider can make that valuable by giving the customer an experienced person quickly. It destroys the value if every incident produces a chain of referrals to unnamed subcontractors.

The mix matters more than headline revenue. Connectivity resale can generate high turnover with low gross margin. Hardware projects can make revenue jump while most of the invoice passes to vendors. Hosting can have strong contribution after a server or rack is filled, but poor returns while capacity is empty. Consulting can be asset-light but constrained by billable hours. Management needs contribution margin by product, not a single revenue-growth number, to know whether network control creates value.

The ideal account uses all four engines. A regional group with five sites buys primary fibre, a physically different backup, a managed firewall, private connectivity to hosted workloads, replication and on-call support. Installation revenue pays some acquisition cost, while recurring service pays for the shared network and support team. The customer is less likely to switch because the replacement must reproduce an architecture, not just undercut one line item.

The weak account buys a single resold circuit after a price comparison. 121 carries sales, billing and first-line support while the upstream keeps most of the access economics. If the customer leaves after the minimum term, there is little installed value to recover. The distinction between those two accounts is the difference between a regional operator and a sales wrapper.

Public prices show how difficult the middle market is

121 does not disclose prices, which prevents direct unit-economic analysis. The surrounding market still sets useful boundaries. At the low end, Free Pro's published tariff prices its fibre service at EUR39.99 per month for the first 12 months and EUR49.99 thereafter, with a 4G modem and SIM for business continuity. That is not a substitute for dark fibre or a bespoke multi-site network, but it anchors what a small office can buy before paying for engineered resilience.

Satellite backup is also becoming a visible commodity input. Starlink's French business plans listed Local Priority packages from EUR33 a month for 50GB to EUR318 for 2TB on the observation date, with extra priority data sold in blocks. A buyer can purchase the terminal and subscription directly. 121 must therefore earn its satellite margin through site survey, installation, failover design, monitoring and support, not by treating satellite access itself as scarce.

Dedicated hosting faces similar pressure. Scaleway's Dedibox range advertised entry servers from EUR4.74 a month with a 12-month commitment and said it manages more than 100,000 servers across France and the Netherlands. A small provider cannot win a bare-server price war against that utilisation and purchasing scale. It must sell migration, private design, data location, human support and continuity across connectivity and hosting.

At the higher end, dedicated-fibre competitors already package reliability. Celeste advertises a four-hour restoration guarantee, 4G backup, access to more than 35 data centres, 11 regional offices and more than 13,000 kilometres of its own French fibre network. Its separate availability page states a 99.99% commitment for dedicated fibre. Orange Business and other national carriers can bundle mobile, voice, security, cloud and nationwide field support. The realistic competitor is not only another small operator. It is the customer's incumbent carrier plus a cloud account and an integrator.

121 can still occupy a valuable middle position. A national carrier may be too procedural for a complex regional customer. A hyperscale cloud platform will not survey a warehouse, install diverse access and take responsibility for the local firewall. A low-cost fibre product may offer backup but not prove physical diversity. The middle position works when 121 can assemble large suppliers into a service that is faster to buy and easier to operate than the alternatives.

Price discipline is crucial. A bespoke quote can hide value-destroying concessions: waived installation, free equipment, unlimited support or an availability promise with weak exclusions. A small provider often wins by saying yes where a large carrier says no. Every exceptional term must be costed over the contract life. Otherwise revenue growth simply accumulates obligations.

A sensible pricing unit would separate at least five items: access and capacity; customer-premises equipment; installation and construction; monitoring and response; and genuine diversity. It should also charge differently for office-hours repair, 24-hour restoration and active-active continuity. A customer that wants two access technologies, two data centres and a named response target is asking 121 to reserve resources. The contract has to pay for those resources even when no incident occurs.

The reliability claim needs a denominator

121's homepage reports 99.987% availability for its dark-fibre network in 2025. Taken literally across a full year, 0.013% downtime equals about 68 minutes. That is a useful operating claim, but it lacks the information needed to price or compare it. The page does not identify the number of circuits, whether the measure is customer-weighted, whether planned maintenance is excluded, what counts as unavailable or whether the figure was independently verified.

The date also requires care. RIPEstat's routing record first observed 121's own AS announcing a route on 10 February 2026. The claimed 2025 result therefore cannot be read as the uptime of AS214877. It may describe fibre services delivered through other networks or a different service layer. That can be legitimate, but the distinction should be explicit.

Reliability has at least four denominators. Circuit availability asks whether a specific access line is up. Network availability asks whether the provider's core can carry traffic. Service availability asks whether the customer's application is reachable. Business continuity asks whether the customer can still operate. A perfect core does not help if both local fibre paths share one street chamber. A satellite terminal does not provide continuity if failover is untested or critical applications reject the changed path. Two servers do not provide resilience if they share one power domain.

The upstream supplier's commitment does not automatically become 121's end-to-end commitment. Cogent's IP Transit page advertises 100% network availability, 99.9% packet delivery, fault notification within 15 minutes and round-the-clock support. Those terms concern Cogent's defined network and exclusions. They do not cover 121's access tail, customer equipment, another carrier, the data-centre cross-connect or 121's own response process.

Service credits create another economic asymmetry. A carrier may credit only a small portion of its monthly fee after a qualifying outage. 121's business customer may claim a larger loss, demand engineering attention or leave at renewal. The wholesale credit rarely pays for the retail relationship damage. The margin on reliable months has to fund the rare bad month.

This is why physical diversity is a product, not a diagram. 121 needs to know conduit routes, building entries, splice points, carrier handoff locations, power sources and operational ownership. Fibre from two commercial suppliers can share the same civil infrastructure. Fibre plus 5G can share a regional power failure. Two upstream BGP sessions can terminate in one router. Satellite provides a different path but adds sky visibility, terminal power and capacity constraints.

The best evidence would be a measured service record tied to contract definitions: incident count, customer minutes lost, mean time to acknowledge, mean time to restore, change failure rate and failover-test results. Without it, 99.987% is a marketing statistic rather than a basis for valuing the network.

The network records show a transition, not full independence

121 became a RIPE member and local internet registry in May 2024. Its RIPE aut-num record shows AS214877 assigned on 17 May 2024. The registered routing policy names Cogent's AS174 and Orange's AS3215. On 10 July 2026, however, RIPEstat observed two neighbours: Cogent and Zayo's AS6461. The difference may reflect a changed supplier, an incomplete registry update or a private connection not visible to route collectors. It is evidence that a contract or registry line should not be mistaken for a live topology.

The active footprint was one IPv4 /24, or 256 addresses, and no IPv6 announcement. RIPEstat saw that route from all 327 full-feed IPv4 peers in its snapshot, so the route had broad visibility. It observed no downstream networks. The footprint is enough to run services and exercise routing choice. It is not evidence of a national access network, large hosting estate or substantial customer traffic.

The address source further qualifies independence. ARIN's public registration returns the encompassing 38.0.0.0/8 as a direct Cogent allocation rather than a separately registered 121 block. 121 originates 38.110.198.0/24 through its own AS, but the address space remains connected to a supplier's allocation. If the Cogent relationship changes, portability depends on contractual and registry arrangements that are not public.

Route-origin security was incomplete at the observation point. RIPEstat's RPKI validator returned unknown and no validating authorisation for the route. Unknown does not mean invalid, hijacked or unavailable. It means the public cryptographic system did not provide a matching authorisation that networks could use to validate this origin. For an operator selling security and reliability, creating and monitoring a valid authorisation would remove avoidable ambiguity if the address holder permits it.

The older resource footprint is more revealing. A RIPE database search identifies 194.0.176.0/24 as provider-independent space assigned to 121's RIPE organisation. The record dates to 2007 and is maintained by both 121 and OC3 Network maintainers. Yet RIPEstat network information placed the block behind OC3 Network's AS8921, not AS214877. Public DNS on 10 July put 121's website and its mail gateways in that older block, with no IPv6 address returned for the web host.

This produces a coherent but unfinished picture. 121 has longstanding address and hosting continuity associated with the Montpellier ecosystem. It has added its own AS and a new route with two observed upstreams. Its visible services have not all moved to the new routing domain, and the new domain does not yet advertise IPv6. The strategy may be staged deliberately. It may also reflect dependence on an older provider relationship while the new network matures.

No public PeeringDB entry was found for AS214877 on the observation date. That is not a service defect. Many small enterprise networks buy transit without public peering. It does mean there is no operator-maintained public evidence of exchange ports, facilities, traffic range or peering policy to support a broader interconnection claim.

The company's statement that it keeps three operators interconnected may refer to access suppliers, private links, data-centre options or a layer not visible in BGP. Public routing showed two live neighbours for the new AS. Registered policy named a different second supplier. A customer buying diversity should ask for a circuit-level design and failure-domain attestation rather than counting logos or autonomous-system records.

Suppliers carry much of the service even when 121 carries the promise

Cogent and Zayo are the visible upstream paths for AS214877. Orange remains in the registered policy. These large carriers provide reach that 121 cannot economically reproduce. They also create supplier concentration. A price increase, contract dispute, port move or policy change can affect 121's margin or routing. Buying from two carriers limits outage risk, but it doubles some fixed costs and does not guarantee separate physical routes.

The data-centre layer is similar. 121 displays Etix among its strategic-partner logos and says it hosts private cloud in high-grade French facilities. Etix Montpellier advertises 100 racks, 300kW of IT capacity and more than 15 available network providers. That local carrier-neutral facility is a plausible platform for a regional operator and a realistic substitute for customers that can manage colocation directly. The public evidence does not specify which Etix site or capacity 121 uses, whether it has reserved racks, or whether customer replicas sit in independent facilities.

Colocation converts capital expenditure into a recurring supplier bill. That can be efficient for a small operator: the landlord finances power systems, cooling, physical security and building maintenance. It also narrows 121's margin. A customer pays 121 for cloud or housing; 121 pays for rack space, power, cross-connects and remote hands before funding its own servers, software and support. Empty reserved capacity is expensive, while capacity bought only after a sale can be slow to deliver.

Equipment suppliers matter as well. The homepage displays Cisco, but no public bill of materials or vendor agreement was found. Switching, routing, firewall and wireless equipment have replacement cycles, licence renewals and spare requirements. Extending hardware life protects short-term cash and raises failure and security risk. Refreshing too early consumes capital before old equipment has earned its return.

Starlink is a useful backup supplier because it changes the physical path. It is not an owned satellite network. The current French tariff includes finite priority-data allowances, and Starlink says service requires a clear view of the sky. 121 can add value through installation and managed failover, but capacity, terms and the space segment remain outside its control. The geopolitical label also matters: a French private-cloud proposition can still depend on a US satellite provider and US network vendors. Customers should distinguish data location, legal control, software origin and operational dependency rather than accepting one broad sovereignty claim.

The older relationship with OC3 deserves particular diligence. OC3 is an established Montpellier hosting provider that says it owns a local data centre. RIPE records place 121's older address block inside OC3's routing domain, and 121's public-facing systems still use that block. Registry histories also show overlapping past leadership. A public legal-data listing records a commercial-court matter in Montpellier dated 23 April 2026 in which 121 is claimant and OC3 is defendant. The public listing does not disclose the claim, evidence or result, so no conclusion about wrongdoing or liability is justified.

Economically, the existence of the matter is enough to identify a question. What services, equipment, addresses, customer contracts or operational responsibilities pass between the two companies, and under what terms? If the relationship is stable, the older network can be a useful bridge. If it is contested, migration cost and service continuity become more important. The answer cannot be inferred from the docket.

A small provider's largest cost may be readiness

Transit, fibre and rack space are visible invoices. Readiness is the less visible burden. A provider selling continuity needs someone able to diagnose a fault at night, contact the right carrier, reach a customer site, replace failed equipment and communicate clearly. The team must train and rehearse even when nothing breaks. That standby capacity is not free simply because it is idle.

121's contact page lists commercial and technical support from 9am to 5pm on weekdays, while other public copy refers to on-call or continuous response. Those statements can coexist if round-the-clock help is contractual and office support is general. Buyers need the exact escalation model: who answers outside normal hours, whether that person can make routing changes, where spares are held and which regions have field coverage.

With a small disclosed historical employee band, key-person risk is material until shown otherwise. A handful of engineers can deliver excellent service to a concentrated customer base. They can also become the bottleneck when two incidents occur, one person leaves or a complex project overlaps with maintenance. Outsourcing expands coverage but introduces handoffs and supplier margin. The staffing model has to match the service promise, not the average day.

Working capital is another readiness cost. Fibre construction and equipment may be paid before customer acceptance. Suppliers may require deposits or annual licences. A large customer may pay in 45 or 60 days. The absorbed 121 Digital Group's 223-day customer-payment measure in 2022 shows how quickly a small balance sheet can become tied up, although that old figure should not be assigned to today's contracts. Upfront installation charges, credit checks and milestone billing are not administrative details; they determine whether growth consumes or releases cash.

Maintenance capital must also be separated from expansion. A new router that adds customers is growth capital. A replacement for an ageing router preserves the existing revenue base. The same distinction applies to optics, batteries, servers and firewall licences. EBITDA can look strong while the network is young, then disappoint when several replacement cycles arrive together.

Compliance turns readiness into documentation. French communications law sets conditions around network continuity, quality, security and significant-incident notification for covered operators. Arcep notes that the former prior declaration requirement was removed in 2021, so the absence of a public declaration should not be treated as absence of operator status. The applicable obligations depend on the services actually provided, not the marketing label.

Hosting adds data-protection duties. CNIL guidance tells customers to require sufficient security guarantees, defined incident obligations, auditability, encryption, access control and clear subprocessor chains. A data-centre certification does not automatically certify 121's managed layer. A hardware vendor's security features do not document 121's procedures. Each layer needs a defined owner and evidence.

The EU Data Act adds commercial pressure. The European Commission explains that cloud contracts must support switching and that switching charges, including data-egress charges, are to be removed from 12 January 2027. Easier exit can reduce customer fear and help a local provider win migrations. It also weakens lock-in as a substitute for service quality. Retention will have to come from performance and support.

Customer concentration is the hidden balance-sheet risk

The public record provides only fragments of customer evidence. Groupe GRIM's data-protection page identifies 121 as the host of its web service at the Montpellier address. A 2024 Classic Racing publication says it was hosted by 121. These independent references support the existence of delivered hosting work. They do not reveal contract value, current status, margin, service scope or the number of other customers.

At the historical revenue scale, one medium-sized network or hosting contract could dominate the company. Concentration cuts both ways. A large account can fund a router, rack or field engineer that later serves more customers. It can also dictate custom terms, delay payment and remove a large share of contribution at renewal. The useful measure is not only top-customer revenue but top-customer gross profit, receivables and dedicated assets.

Market dependence is also regional. Montpellier and the wider south of France offer a credible niche: local enterprises, health and research organisations, tourism groups, industrial sites and professional services that value nearby support and French hosting. Etix's local facility and OC3's longstanding presence prove there is an infrastructure market. They also prove that 121 is not alone.

The customer alternative set is broad. A small site can buy Free Pro with mobile backup. A demanding enterprise can buy dedicated fibre with a four-hour restoration target from Celeste or a national carrier. A technically capable buyer can colocate directly at Etix and buy transit. A cloud-first customer can use OVHcloud or Scaleway and purchase connectivity separately. A remote site can buy Starlink directly. A managed-service provider can integrate those components without operating its own AS.

121's defensible customer is therefore neither the most price-sensitive buyer nor the largest multinational requiring a vast audited footprint. It is a customer complex enough to value integration but small enough to value direct access to senior engineers. That niche can be profitable, but its size is not disclosed and its sales cycle may be long.

The company should resist confusing contracted bandwidth with customer value. A 100Gbps or 800Gbps optical capability sounds impressive, but unused capacity does not pay invoices. Many SME workloads need far less throughput and much more reliable recovery. Selling the correct smaller circuit with tested backup can create more value than oversizing the primary link.

Public signals point to an active transition, with evidence still thin

The unofficial market signal is not a wave of customer praise or complaint. It is the pattern of recent change. The legal purpose broadened in 2025. The new AS began appearing in global routing in February 2026. The website was substantially refreshed in July 2026. A public professional profile for Raoul Scultore identifies 121 SAS, while registry records place Scultore & Associes as corporate president. Together these signals suggest active commercial repositioning.

They do not establish scale. The website contains ambitious claims about fibre speeds, private cloud, three interconnected operators, broad data-centre presence and 2025 availability. Public routing shows one route and two observed neighbours. Public accounts stop before the expansion. Independent customer references are sparse. No public capacity, customer, order-book or certification schedule closes the gap.

The OC3 overlap is similarly a signal, not a conclusion. Older websites and documents connected 121 Digital Media with OC3 hosting. Current DNS and RIPE records still show technical coexistence. A public court listing shows a dispute without details. It would be irresponsible to turn those fragments into a story of conflict or separation. It would be equally weak to ignore them when assessing operational dependencies.

This is the appropriate use of informal and incomplete evidence: formulate questions, do not manufacture answers. Customers and creditors should ask for current references, audited service reports, network diagrams under confidentiality, insurance, supplier terms and current financial statements. Until those are available, confidence should remain proportional to the evidence.

What would prove the reliability strategy works

The first decisive fact would be current recurring revenue. 121 should disclose, at least privately to serious counterparties, annual recurring connectivity and hosting revenue, project revenue, gross margin by line and renewal rates. Growth in low-margin pass-through hardware is less valuable than stable contribution from monitored circuits and managed hosting.

The second would be cash conversion. Operating cash after receivables, supplier prepayments and maintenance capital should remain positive as the network grows. A profitable income statement financed by longer supplier terms or unpaid customer balances would not prove the model. Nor would capitalised equipment without contracted utilisation.

The third would be customer diversity. No single account should be able to strand a large share of network capacity or support cost. Disclosure of the top five customers' share of revenue and gross profit, contract duration, cancellation rights and overdue balances would materially improve the judgment.

The fourth would be a tested resilience map. Customers need evidence that primary and backup paths differ by carrier, duct, building entry, power and device. They need failover test dates, restoration targets and service-credit terms. For cloud, they need facility locations, replication distance, recovery-point and recovery-time commitments, backup immutability tests and subprocessor lists.

The fifth would be network maturity. A valid route-origin authorisation, IPv6 deployment, updated public routing policy and facility or interconnection disclosures would not create profit by themselves. They would show that the control plane is catching up with the commercial promise. Evidence of traffic growth and capacity headroom would show whether the AS is becoming an operating platform rather than remaining a credential.

The sixth would be a documented operating team. Named roles, round-the-clock escalation coverage, field-service arrangements, spare inventory, training and key-person succession matter more than a generic support claim. Employee retention and incident load would show whether local accountability is scalable.

The seventh would be clarity around OC3 and other suppliers. A stable long-term arrangement may be entirely rational. A completed migration may be equally rational. What matters is that customer continuity, address control, equipment ownership and contractual rights are understood and not dependent on unresolved assumptions.

Evidence in the opposite direction would change the view quickly: persistent discounting, weak renewal, a large overdue customer balance, common-path failures marketed as diversity, repeated use of service exclusions, staff concentration, delayed equipment refresh or a supplier dispute affecting customer systems. Any one of those can turn the reliability premium into a liability.

The verdict is an option on execution, not proof of scale

121 has moved beyond a paper claim to network activity. It is a recognised French company, a RIPE member, the operator of a visible autonomous system and the holder of longstanding address resources. Its offer is commercially coherent: combine fibre, wireless backup, private hosting and integration so a regional customer buys one accountable service rather than coordinating several suppliers.

The resources do not yet prove the economics. One visible route, no advertised IPv6, two observed upstreams, an older service block still routed through another operator and confidential current accounts describe a platform in transition. The last public financial base was small. The current offer can succeed only if the company sells enough recurring, high-contribution service to fund wholesale connectivity, colocation, hardware renewal and genuine response capacity.

Who pays is clear: regional businesses whose operations depend on connectivity and which cannot or do not want to integrate carriers, cloud and recovery themselves. Who benefits is also clear: customers gain one accountable architecture, and 121 retains more value than a pure reseller if it controls design and support. Who carries the downside is less evenly distributed. 121 carries supplier contracts, readiness cost and first-line blame; customers carry the operational loss if the redundancy is not real; upstream carriers and landlords usually limit their exposure through defined service credits.

The practical judgment is neutral with a constructive bias. 121 has assembled credible ingredients and a reason to exist between commodity access and national-carrier bureaucracy. It has not publicly demonstrated the utilisation, cash flow, diversity or staffing that would show those ingredients create durable value. The next stage is not another broad capability claim. It is evidence that customers pay for independence at a price higher than independence costs.