Summary

- AVIATION REPAIR RESOURCES INC is best read as an aircraft-downtime business, not merely as a repair label: the public record points to a Texas-based Part 145 repair-station surface at

https://www.goarr.com, a related AIR Group parts and inventory surface athttps://avinvres.com, and ARIN network-accountability records that place the named company in Johnson County, Texas. - The paid unit is the avoidance of grounded-aircraft time through certified labor, component repair, parts availability, exchange stock, engineering judgment, tooling, ground-support equipment and digital continuity. The cheaper substitutes are delayed schedules, cannibalized parts, in-house maintenance, a larger MRO group, an OEM service channel, or another regional specialist.

- The strongest public evidence is company and regulatory evidence, especially Aviation Repair Resources' own Part 145 and capability claims, Aviation Inventory Resources' regional-airline parts support claims, FAA repair-station rules, and ARIN RDAP assignments. Public records do not prove revenue, margins, utilization, response times, customer concentration, rework rates or retention.

- The commercial judgment turns on whether a customer values a narrow, experienced, near-DFW repair and parts support team more than scale. That judgment would improve with verified turnaround-time history, shop loading, repair approval scope, inventory depth, airline repeat business and gross margin by service line.

The Downtime Account

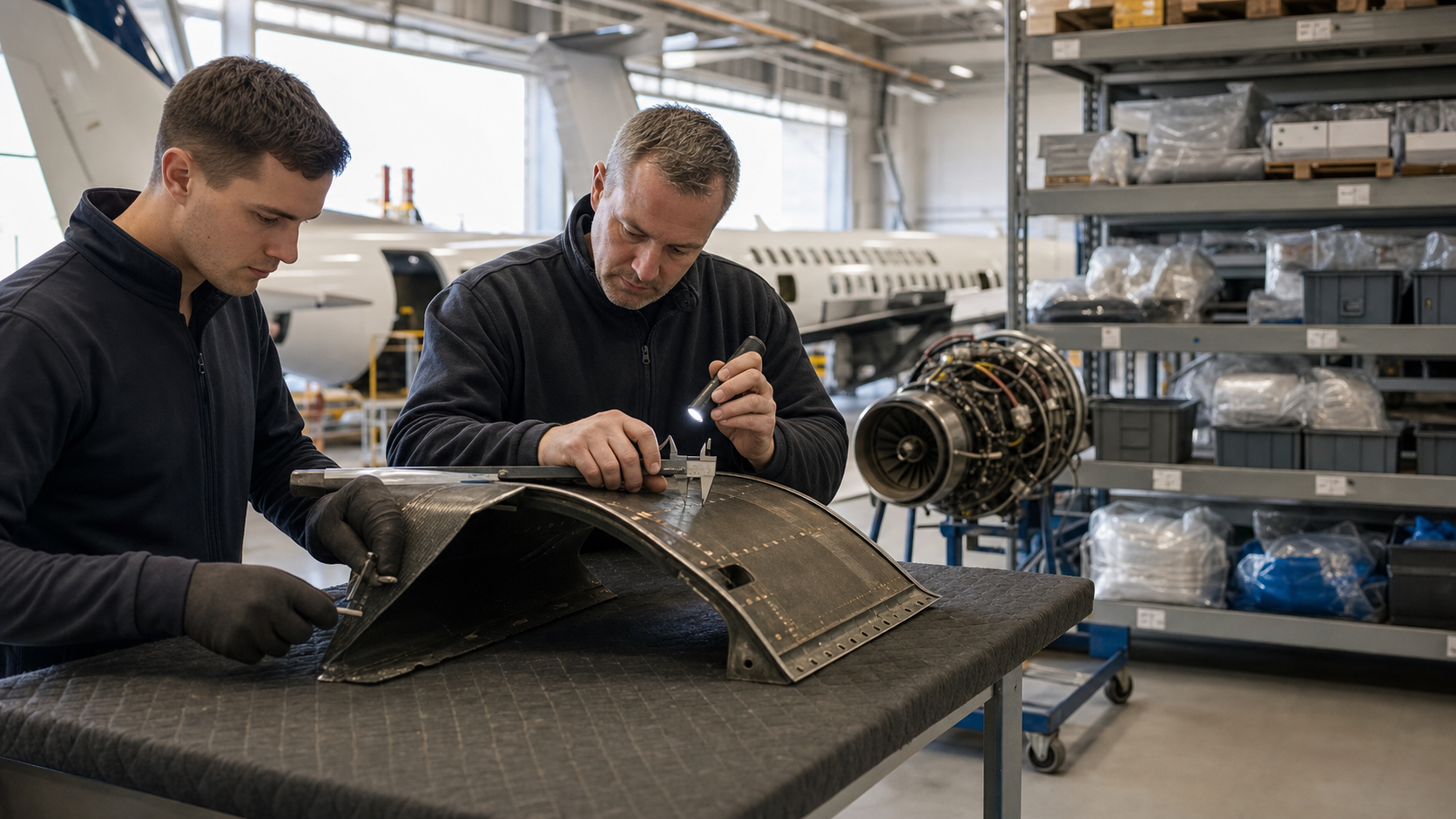

Start with an aircraft that cannot leave the ramp because a structure, engine accessory, interior component, tool, or serviceable replacement is not ready. The operator can wait for an OEM channel, ask an in-house team to work around the problem, remove a part from another aircraft, push the schedule back, or pay a specialist that can repair, source, lease, or exchange the missing unit. In that moment, the purchased unit is not a part alone and not labor alone. It is the recovery of aircraft availability before a technical defect becomes a network, crew, lease, passenger, or customer-retention problem.

AVIATION REPAIR RESOURCES INC appears in the BTW directory at https://btw.media/en/directory/aviation-repair-resources-inc, and the strongest public commercial surface is the Aviation Repair Resources site at https://www.goarr.com. That site presents Aviation Repair Resources, or ARR, as an FAA/EASA certified Part 145 repair station in Alvarado, Texas, founded in 2009, with an operations team that it says carries well over 100 years of experience. A second public surface, https://avinvres.com, presents Aviation Inventory Resources, or AIR, as part of The AIR Group and as a regional-airline parts and support business. The two surfaces link together through the AIR Group section, which matters because the article's economic unit is the aircraft-maintenance, parts-availability and downtime-avoidance account rather than a narrow corporate-title exercise.

By the third paragraph, the account can be priced clearly. The paid unit is time-certain access to certified repair, repair development, serviceable inventory, exchange stock, rental or leased engines and aircraft, technical help, tooling and GSE that keep an aircraft from staying down longer than necessary. The cheaper substitute is a larger maintenance group, an OEM service channel, another regional MRO, a delayed schedule, a cannibalized part or an in-house technical team. The cost driver is qualified labor tied to regulated work, scarce component and engine inventory, shop and hangar capacity near useful logistics nodes, approved data, quality discipline and the working capital locked inside parts. The strongest evidence class is company and regulatory evidence: company capability claims, FAA rules and ARIN network accountability. The missing proof categories that would change the judgment are economics, reliability and retention: revenue and margin by line, verified turnaround and rework history, and repeat-customer durability.

That framing is important because aircraft maintenance is full of language that can sound larger than the public facts. "Repair station" does not automatically prove depth across every aircraft type. "Inventory" does not automatically prove that the right rotable is on the shelf on the day an aircraft is down. "AOG support" does not automatically prove response-time performance. "FAA/EASA certified" does not by itself show the exact ratings, the active capability list, or the commercial mix of work. The public record does, however, show a plausible downtime product: ARR's public site emphasizes airframe component repair, sheet metal, composites, engineering and design services, repair development, tooling, ground-support equipment, and a 20,000 square-foot operation near DFW International Airport. AIR's public site emphasizes regional airline parts, exchanges, outright sales, managed inventory, per-flight-hour and event-driven support, technical assistance and 24/7/365 AOG support from headquarters near DFW.

The commercial question is therefore not whether the company belongs somewhere in aviation maintenance. It does. The question is how to price a smaller, specialized service surface when large operators, OEM channels, airline technical departments and parts marketplaces can all claim some share of the same problem. For a regional operator, the right specialist can be valuable because the aircraft fleet is often old enough to need practical repair judgment and young enough to still have revenue value if downtime is controlled. For a buyer with a larger fleet, scale may matter more: broad hangar capacity, global parts pools, multi-site line support and formal service-level terms can beat a smaller shop's craftsmanship. The article's central judgment sits between those poles.

The best public reading is that Aviation Repair Resources competes for the moments when a customer does not want a generic maintenance answer. It wants an airframe component fixed, a composite or honeycomb repair developed, a tool made, a part obtained, a Saab 340 or regional-aircraft support problem solved, or an engine or aircraft support option evaluated quickly enough to avoid a larger operating loss. That is a paid unit with real economic weight, but it is not fully measurable from open records. Public evidence supports the existence of capabilities and operating context. It does not disclose the private commercial facts that decide whether the unit is consistently profitable.

Identity, Public Surface And Name Risk

The identity evidence is unusually useful because it shows both a public business surface and an infrastructure-accountability surface. ARIN's RDAP search for AVIATION REPAIR RESOURCES INC returns an organization handle, ARR-43, with a Johnson County, Texas address and registration in July 2019 at https://rdap.arin.net/registry/entity/ARR-43. A second ARIN customer handle, C08755253, carries the same organization name and address with a 2022 registration at https://rdap.arin.net/registry/entity/C08755253. Those records are not proof of revenue or aircraft-service scope, but they show that the named company appears in public network-accountability records rather than only in a marketing page.

The public commercial site at https://www.goarr.com uses the Aviation Repair Resources name directly. It says ARR is an FAA/EASA certified Part 145 repair station based in Alvarado, Texas, with a 2009 start date, repair development capability, manufacturing capability, engineering and design services, and practical specialization in sheet metal and composites including metal-to-metal, honeycomb sandwich and solid laminate structures. The page also says the operation is located minutes from DFW International Airport and describes multi-axis CNC production machinery, high-precision measuring and scanning equipment, clean-room capacity for repair and production, a large-format paint booth, high-heat curing and other shop equipment.

The related site at https://avinvres.com uses the Aviation Inventory Resources name and the AIR initials. It says AIR has supported regional airlines around the world for 20 years and offers parts inventory, parts distribution, aircraft and engine sales or leases, tooling and GSE, parts support programs and technical assistance. It also says the business supports Saab 340, ATR42, ATR72, Beechcraft 1900, Cessna Caravan, Embraer ERJ, Bombardier CRJ and more. The site states that AIR is part of The AIR Group and links to ARR's site, so the two surfaces can be analyzed together as a regional-airline support cluster while preserving the fact that the exact legal and operating boundaries are not fully disclosed.

That boundary matters. A repair-station claim and a parts-distribution claim are adjacent, not identical. Repair stations sell qualified work, release discipline and rework risk management. Parts distributors sell availability, traceability, working-capital timing and procurement reach. The ARR and AIR public sites together describe a broader account: repair components when that is the best path, source or exchange parts when repair is slower or uneconomic, make or rent tooling when the physical task is the constraint, and use technical judgment to keep a regional operator from losing aircraft days. Public records do not show which company books which sale, how the group allocates costs, or whether the parts side subsidizes the repair side. Those are private facts.

The name risk should not be treated as fatal. Aviation businesses often operate with trade names, related entities, group brands and legacy domains. The conservative point is simply that public evidence should not collapse every surface into one fully verified operating statement. ARIN shows AVIATION REPAIR RESOURCES INC. The ARR site shows Aviation Repair Resources. The AIR site shows Aviation Inventory Resources and links ARR as a group member. A careful reader can infer a related service ecosystem, not a full legal consolidation. That is enough to analyze the downtime account, and not enough to claim consolidated revenue, margin or customer contracts.

The public directory context also matters because it describes the subject with network-resource evidence while the stronger commercial surface sits in aviation repair and inventory support. That does not mean the company is a network operator in the telecom sense. It means the public evidence includes both digital accountability records and aircraft-support claims. The better business lens is aviation support: an aircraft can be grounded by a missing component, a slow repair, a tooling gap, an inspection bottleneck or a supplier delay. Digital reachability matters because purchase orders, inventory searches, AOG requests, engineering drawings, customer communication and shipment coordination depend on working systems, but network evidence is supporting context rather than the economic center.

In practice, the company is more interesting because it is not a public issuer with clean segment data. Large listed competitors tell investors their revenue, facilities, business lines and risks. A small privately held repair-and-inventory specialist must be judged through indirect public evidence: what it says it does, where it is accountable, what markets it names, what capabilities it publishes, what inventory surfaces are visible, what regulatory obligations apply, and what missing data would change a buyer's decision. That is a harder assessment, but it is also closer to how customers actually choose aviation support suppliers under time pressure.

What The Customer Actually Buys

The customer buys an option on aircraft time. If an aircraft is grounded for a repairable airframe component, the customer needs a shop that can understand the component, apply approved data, make a repair judgment, document the work, and return the article to service without creating a later compliance or reliability problem. If the repair is too slow, the customer may need a rotable exchange or a serviceable part. If no part is readily available, the customer may need technical assistance, a field workaround within approved practice, a temporary lease, a rental engine or a component sourced through a marketplace. The ARR and AIR public surfaces show that the group is trying to sell that combination, not only a single workshop task.

AIR's own service list supports that reading. The site names parts inventory with rotables and expendables, exchanges and outright sales; parts distribution for AIM Altitude and Helios Ice Protection Systems; aircraft and engine sales and leases; tooling and GSE sales, rental and specialty tool stock; parts support programs including AIRcare managed inventory, per-flight-hour and event-driven programs, consignment and rental programs; and technical assistance including on-site maintenance training, on-site or remote support and maintenance-program consulting. That list is visible on https://avinvres.com, and the inventory page at https://avinvres.com/inventory.html says the searchable database is coming soon while directing users to ILSMart and PartsBase.

ARR's public site fills the repair side. It presents material repair capabilities, sheet-metal and composite expertise, engineering and design services, repair development, PMA or owner-fabricated parts manufacturing, tooling and GSE, and a quality claim tied to regional-airline reliability. FAA repair-station rules explain why this is not a casual trade. The FAA's repair-station page at https://www.faa.gov/aircraft/repair directs users to Part 145 certification, repair-station finding tools and airworthiness approval forms. The live eCFR Part 145 text at https://www.ecfr.gov/current/title-14/chapter-I/subchapter-H/part-145 describes certification, ratings, housing, facilities, equipment, materials, data, personnel, manuals, quality control, inspection, capability lists, contract maintenance, recordkeeping and FAA inspections.

That regulatory context turns "repair" into an economic unit with a compliance premium. A customer is not simply buying a technician's hours. It is buying a regulated release path in which the wrong work can create aircraft safety exposure, future rework, insurer questions, lessor disputes, customer complaints and regulatory scrutiny. A smaller shop with the right capability can be valuable precisely because it can move faster than a large queue, but speed is only valuable if the work is defensible. A fast repair that fails documentation or quality standards is not downtime avoidance. It is postponed downtime with added risk.

Parts availability adds the second layer. A rotable or expendable that arrives today can be worth more than a cheaper part that arrives after a missed flight series. AIR's public engine listing at https://avinvres.com/engines.html and its underlying public CSV at https://avinvres.com/assets/article-connect---content-template---air---engines-for-sale---content-template---article-connect-by-musethemes.com.csv.csv show two GE CT7-9B engine listings marked available for sale or rental, with time-since-new, cycles-since-new, time and cycles since last shop visit, limiting items and prior U.S. Part 121 air-carrier operation. The aircraft listing CSV shows no current aircraft available but records prior Saab 340 sales. That is not proof of deep inventory, but it is proof that the public offer includes engines, rental or lease options and regional aircraft disposition history.

The customer also buys search efficiency. The AIR inventory page says users can find inventory on https://www.ilsmart.com/ and https://www.partsbase.com/landing/home. Those marketplaces can be substitutes and complements. A buyer can search marketplaces directly, but a specialist with actual inventory, supplier relationships and technical knowledge can reduce the time between identifying a part and knowing whether it is usable, traceable, economical and fast enough. The margin, if any, lives in that reduction of search and verification cost. Public pages cannot prove that AIR consistently wins that spread, but they do show the business model it is trying to run.

For regional airlines and business aircraft operators, the economic value can be asymmetric. A missing relatively small component can immobilize a much more valuable aircraft and disrupt a much larger revenue schedule. The customer's willingness to pay is therefore not always tied to the part's production cost or the hourly labor cost. It is tied to avoided delay, avoided substitution, avoided passenger disruption, avoided lease penalties, avoided contract failure and avoided reputational damage. Aviation Repair Resources' thesis depends on this asymmetry. The company does not have to be the cheapest engineering label if it is credible in the moments when being first, right and traceable is more valuable than a lower nominal quote.

Why The Unit Is Costly

The downtime-avoidance unit is costly because every layer is constrained. Certified labor is constrained by training, experience, ratings and availability. Parts are constrained by aircraft age, OEM support, aftermarket production approvals, repairability, documentation, traceability and working capital. Shop capacity is constrained by equipment, clean areas, paint and curing capacity, inspection tools and the ability to schedule work without quality shortcuts. Logistics are constrained by proximity to airports, shipping cutoffs, customs when parts cross borders and the need to protect serviceable material. Digital continuity is constrained by inventory systems, network access, customer communication and accurate records.

The labor constraint is visible in public labor data. The U.S. Bureau of Labor Statistics' Occupational Outlook Handbook page at https://www.bls.gov/ooh/installation-maintenance-and-repair/aircraft-and-avionics-equipment-mechanics-and-technicians.htm reports 2024 median pay of $79,140 for aircraft and avionics equipment mechanics and technicians, 160,800 jobs in 2024, 5 percent projected employment growth for 2024 to 2034, and about 13,100 projected annual openings. It also notes that aircraft mechanics and technicians work in hangars, repair stations and airfields, often under stress because they must meet strict safety standards while meeting deadlines. That is the labor market behind the invoice.

The regulatory constraint is equally important. eCFR Part 145 requires repair stations to have appropriate facilities, equipment, materials, data, qualified personnel, manuals, quality-control systems, inspection processes and records. It also restricts privileges and includes FAA inspection rights. That means a smaller repair station cannot simply add capability by hiring a general mechanic and accepting every job. It must have the right rating, scope, data, tools, trained people and quality release path for the work. The capacity customers buy is the intersection of a particular job and the repair station's approved, practical ability to perform it.

The parts constraint appears in the relationship between repair and replacement. If a component is unavailable, repair becomes more valuable. If the repair requires approved data or a developed repair method, engineering judgment becomes more valuable. If the component can be replaced with a PMA part, the economics change again. FAA's Parts Manufacturer Approval page at https://www.faa.gov/aircraft/air_cert/design_approvals/pma explains PMA as a combined design and production approval for modification and replacement articles. ARR's public site says it can create affordable PMA or owner-fabricated parts manufacturing. That is a meaningful claim because it points beyond simple bench work into the supply problem that can keep a regional aircraft down.

The working-capital constraint is less visible but central. Parts inventory ties up cash before a buyer appears. Exchange stock ties up cash while the customer's removed component is repaired, scrapped or returned. Rental engines tie up capital in a high-value asset whose economics depend on utilization, maintenance status, life-limited parts, return conditions and customer credit. A company can advertise inventory, but the investment question is whether it carries enough of the right items at the right economics to command a premium without becoming a warehouse of slow-moving stock. Public pages do not show AIR's inventory age, turns, write-downs, consignment terms or supplier credit.

The shop-capacity constraint is partly visible at ARR. A 20,000 square-foot operation near DFW can be useful because DFW is a major logistics node and because regional operators often value fast shipping and practical access. But 20,000 square feet is not the same as a large airframe MRO campus, and ARR's public language is strongest around components, materials, engineering, tooling and shop equipment rather than heavy airframe hangar lines. That is not a weakness if the business is built around component repair and parts support. It is a weakness only if a customer expects a full substitute for a large maintenance group.

The digital constraint is smaller than the certification constraint, but still relevant. ARIN's https://rdap.arin.net/registry/ip/12.11.49.96 shows a /27 IPv4 assignment named AVIATION15-49-96 associated with ARR-43 and registered in 2019. ARIN's https://rdap.arin.net/registry/ip/12.0.158.72 shows a /29 assignment named AVIATION24-158-72 associated with C08755253 and registered in 2022. These are modest blocks, not telecom-scale assets. Their value is accountability: they show a named organization tied to public network resources, which supports the view that digital ordering, email, inventory access and customer coordination belong in the continuity picture. They do not prove uptime, cybersecurity maturity or transaction volume.

The costliest part of the unit may be trust. A grounded aircraft creates pressure to improvise, but aviation maintenance punishes careless improvisation. A customer paying ARR or AIR wants the job done quickly but also wants traceability, conformity and a supplier that will stand behind the work. Trust is costly because it is accumulated through previous jobs, clean releases, responsive communication, low rework, honest limitations and the ability to say no when work exceeds capability. Public websites can state that trust. Only customer records can prove it.

Evidence The Public Record Can And Cannot Prove

The public record can prove that Aviation Repair Resources has a public repair-station website, that the website states FAA/EASA Part 145 certification, Alvarado location, 2009 inception, regional-airline repair focus, shop equipment and material-repair expertise. It can prove that the related AIR site presents a parts and inventory business serving regional airlines, with named aircraft families, AOG support, inventory categories, technical assistance, support programs, aircraft and engine sale or lease categories, and ASA-100 accreditation. It can prove that ARIN has RDAP records for AVIATION REPAIR RESOURCES INC and two IPv4 assignments. It can prove that FAA rules make repair stations a regulated business and that BLS data show aircraft maintenance labor is skilled, paid above the median for all occupations and projected to keep demand.

The public record cannot prove ARR's active FAA certificate number, rating scope, EASA approval number, current capability list, inspection outcomes, enforcement history, customer names, customer concentration, annual revenue, gross margin, EBITDA, utilization, labor headcount, repair mix, part turns, order fill rate, quote win rate, AOG response speed, on-time return, warranty claims, rework rate, lease-engine utilization or repeat-purchase retention. Some of those facts may exist in customer records, FAA databases, audit files, insurance underwriting, supplier agreements or private management accounts. They are not disclosed in the public pages reviewed for this article.

That division should shape the conclusion. It would be wrong to say that public evidence proves a strong profitable niche. It would also be wrong to dismiss the company because it lacks public issuer-style disclosure. Most small aviation support companies do not publish detailed unit economics. The right conclusion is conditional: the public evidence supports a commercially plausible downtime-avoidance account, and the private value depends on whether ARR/AIR can convert capability claims into measurable turnaround, repeat business and margin.

The official company evidence is more useful than generic market chatter because it names specific capabilities. ARR says it works in sheet metal and composites, including honeycomb and solid laminate structures. It says it supplies engineering and design services and has repair-development experience for airframe components. It says it can design new repairs, create affordable PMA or owner-fabricated parts, and craft new tooling or ground-support equipment. AIR says it supports regional aircraft families, provides parts inventory and distribution, offers support programs and technical assistance, and maintains public engine listings. These statements are specific enough to anchor an economic analysis, even though they remain company claims until independently verified by contract, certificate and customer evidence.

Regulatory evidence is the guardrail. FAA Part 145 shows why a repair-station business is not equivalent to an unregulated workshop. FAA PMA materials show why approved replacement parts can change the repair-versus-replace economics. BLS labor data show why technician scarcity and pay matter. Oliver Wyman's 2025 fleet and MRO forecast at https://www.oliverwyman.com/our-expertise/insights/2025/feb/global-fleet-and-mro-market-forecast-2025-2035.html shows a larger demand backdrop: it estimates the global commercial fleet at just over 29,000 aircraft in 2025, growing to 38,300 by the start of 2035; it says the MRO market is set to reach $119 billion in 2025 and $156 billion by 2035; and it notes North American MRO demand rising from $28 billion to $34 billion by 2035. This does not prove ARR/AIR's revenue, but it supports the sector pressure behind downtime.

Network evidence is the narrowest support. ARIN records show accountability for named IPv4 assignments, but no ASN is attached in the RDAP records reviewed and the blocks are small. A small IP allocation can support enterprise connectivity, inventory systems, email and customer communications, but it cannot prove that the company operates mission-critical infrastructure at scale. For this article's purposes, network evidence matters because an AOG request, inventory quote or repair status update now travels through digital channels. It is not the main business conclusion.

The AIR inventory evidence is useful but bounded. The engine CSV shows two GE CT7-9B listings with life and shop-visit fields and prior U.S. Part 121 operation. The aircraft CSV shows no current aircraft available while recording multiple sold Saab 340 aircraft. That tells a reader that the site has supported real aircraft and engine sale or rental postings, and that the current public aircraft inventory is limited or absent. It does not show whether AIR maintains a private inventory not exposed on the site, whether the CSV is current, whether marketplace listings on ILSMart or PartsBase are active, or whether engine listings are still available.

Public sources therefore support a valuation logic, not a valuation number. If ARR/AIR has strong repeat airline customers, fast turn times, low rework, scarce regional-aircraft expertise, useful engine and rotable access, and disciplined working-capital management, its small scale could be an advantage. If it lacks active inventory, is dependent on a few customers, cannot hire enough technicians, or has thin shop utilization, the same narrowness would become a margin risk. The public record points to the questions; it does not answer them completely.

Revenue Logic And Margin Levers

Revenue in this account likely comes from multiple but related activities: component repair, engineering and repair development, tooling and GSE work, parts sales, parts exchanges, consignment, rentals, managed inventory, technical assistance, training, consulting, aircraft or engine sales, and leases. The public pages do not disclose the mix. That mix matters because each activity has a different margin and risk profile. Repair labor can carry good margin when the shop is loaded and rework is low. Parts sales can generate spread when inventory is scarce and traceable. Exchanges can generate premium pricing when the customer needs speed. Rentals can produce recurring revenue when assets stay utilized. Consignment can reduce capital burden but also reduce margin.

The pricing power starts with avoided aircraft downtime. A buyer paying for a repair or exchange does not compare the quote only with the material cost. It compares the quote with canceled flights, repositioning, crew disruption, replacement aircraft, passenger recovery, customer penalties, lease costs and reputational loss. This is why AOG support can command a premium when credible. AIR's 24/7/365 AOG support claim from headquarters near DFW is valuable if it is backed by actual response capability. Without response-time and fill-rate data, the claim should be treated as a commercial promise rather than a measured outcome.

The second lever is aircraft-type knowledge. AIR names Saab 340, ATR42, ATR72, Beechcraft 1900, Cessna Caravan, Embraer ERJ, Bombardier CRJ and more. These are not all identical markets. Saab 340 support can involve aging regional turboprop economics and scarcity of certain parts. ATR support has a larger global turboprop fleet but depends on OEM and supplier availability. ERJ and CRJ support has its own aftermarket dynamics as airlines retire, part out or continue regional jets. A specialist that knows these platforms can identify whether repair, exchange, used serviceable material, PMA, owner-fabricated parts or delay is the best answer. That platform knowledge can create margin by reducing buyer uncertainty.

The third lever is repair development. ARR says its engineering team has experience in repair development for airframe components and in design and fabrication of parts and tooling. If true and active within approved limits, this can be more valuable than routine repair because the customer may not have a standard low-cost path. Developing a repair can preserve a component that would otherwise be scrapped, avoid OEM replacement cost, reduce lead time and convert engineering judgment into a repeatable solution. The risk is that repair development requires strong documentation, approved data and quality controls. A bad repair method destroys the margin by creating rework, delay and trust damage.

The fourth lever is inventory timing. AIR's parts inventory language includes rotables, expendables, exchanges and outright sales. A rotable exchange lets the customer keep operating while the removed unit enters repair. The margin can come from the exchange fee, the repair spread, the replacement value and customer urgency. But the risk is that the exchange pool requires capital, storage, inspection, traceability and forecast accuracy. An exchange stock that sits idle consumes cash. A missing exchange stock loses the AOG sale. The best businesses in this space know which units fail, which operators need them, and how often a higher price is accepted because delay is worse.

The fifth lever is program revenue. AIRcare managed inventory, per-flight-hour and event-driven programs, consignment and rental programs suggest a move beyond spot parts sales. Program arrangements can stabilize revenue and deepen retention because the supplier becomes part of the operator's maintenance planning. Per-flight-hour pricing converts irregular parts demand into a usage-linked account. Event-driven programs can attach revenue to specific checks or component events. Consignment can widen accessible inventory without buying every part outright. Public records do not show whether AIR has active contracts of this type, but the offer is economically coherent.

The sixth lever is location. ARR and AIR emphasize proximity to DFW. For a shop serving North American regional operators, DFW-area access helps with shipping, customer visits, airline maintenance networks and labor recruitment. Location alone does not create margin, but it reduces friction. In an AOG event, the difference between making the cutoff and missing it can be the difference between a saved day and a canceled operating sequence. A customer may pay a premium to a supplier that combines capability with logistics reliability.

The margin test is therefore simple to state and hard to verify. Aviation Repair Resources is attractive if customers repeatedly pay it to compress downtime and if the company can price that compression above the full cost of qualified labor, inventory, facilities, capital and quality risk. It is weak if quotes are won only on low price, if shop utilization is uneven, if inventory turns slowly, if rework absorbs labor, if larger competitors beat it on scope, or if customers use it only as an emergency supplier without durable retention. Public evidence tells us the revenue logic. Private data decides the margin.

Suppliers, Upstream Dependence And The OEM Channel

The company cannot escape upstream dependence. Aircraft support suppliers depend on OEM data, approved repair data, component manufacturers, distributors, used-serviceable-material markets, engine lessors, teardown supply, specialty vendors, freight carriers, FAA and EASA recognition, and skilled technicians. ARR's own public language points to PMA, owner-fabricated parts, repair development and tooling because the OEM channel is not always the cheapest or fastest answer. But OEM dependence still shapes the economics because some repairs require approved data, some parts are controlled by the OEM or a licensed supplier, and some customers require OEM-backed material or service channels.

FAA Part 145 makes that dependence formal. A certificated repair station must have the equipment, materials and data required for its ratings and work. Capability is not a marketing preference. It is tied to what the station can lawfully and safely do. If a repair depends on a manual revision, approved data or an OEM instruction that the shop does not have, the shop cannot convert customer urgency into revenue without resolving that data issue. If a replacement depends on a part whose trace or certification is weak, the buyer may reject it even if it is physically available. That is why technical records can be as important as the metal itself.

PMA and owner-fabricated parts are possible release valves. FAA's PMA page explains the formal production approval pathway, while owner-fabricated parts occupy a different and narrower maintenance context. ARR's statement that it can create PMA or owner-fabricated parts manufacturing suggests an upstream strategy: when OEM parts are expensive, delayed or scarce, develop an approved or customer-specific alternative. That can be economically powerful for mature regional aircraft. It can also be risky if the buyer, regulator, insurer or lessor is uncomfortable with the basis of the part. The value is highest when the supplier can document the path and make the operator comfortable.

Parts marketplaces are another release valve. AIR points customers to ILSMart and PartsBase, which are widely used aviation parts search platforms. Marketplaces can reduce search time, but they can also commoditize part availability and weaken distributor margin if many sellers show the same unit. AIR's advantage must therefore come from more than being findable on a marketplace. It needs either actual scarce stock, superior traceability, better platform knowledge, faster logistics, repair capability behind the part, or a program relationship that makes the buyer prefer AIR even when another seller appears in search results.

Larger competitors show how scale changes upstream economics. AAR's repair page at https://www.aarcorp.com/en/repair/ says it provides airframe and component MRO services, and AAR's parts page at https://www.aarcorp.com/en/parts/ says it supplies airframe and engine parts with broad inventory, including rotables and used serviceable material. VSE's home page at https://vsecorp.com/ presents the company as a provider of aftermarket distribution and MRO services, with VSE Aviation combining distribution, technical sales, repair, rotable exchange and supply-chain services. These companies can negotiate with suppliers, carry deeper stock and serve more platforms, but they can also be slower or less personal for a narrow urgent case.

Business-aviation competitors show another scale model. Duncan Aviation's site at https://www.duncanaviation.aero/ presents a complete MRO service offering, three U.S. facilities and mobile technical teams. That kind of full-service brand can capture customers who want one large accountable provider across avionics, interiors, paint, engines and airframe. ARR/AIR's likely advantage is narrower: regional airline support, component repair, fast practical problem solving and parts access around aircraft families where a smaller team may know the customer and fleet history. The risk is that customers may prefer the perceived security of a larger provider when the aircraft value, warranty question or lease obligation is high.

Upstream dependence also includes labor supply. A company that advertises engineering, composites, sheet metal, CNC production, clean-room work, inspection equipment and paint capability needs people who can actually use those assets. Hiring in aviation maintenance is not only a wage question. It involves experience, certification, quality culture, retention and supervision. If labor is scarce, a small shop may suffer more because one or two departures can remove a meaningful share of capacity. If a small shop retains experienced people, it can outperform larger operators in specialized work. Public evidence does not tell us which case applies.

The supplier-dependence conclusion is balanced. Aviation Repair Resources appears to position itself as a workaround to OEM and large-MRO friction, not a full replacement for those channels. That can be a good niche: repair what can be repaired, make or source what can be made or sourced, use platform knowledge to avoid unnecessary waiting, and send the customer elsewhere when the scope requires it. It is a bad niche only if the company overpromises capability or lacks access to the data, parts and people needed to make the workaround reliable.

Customers, Market Dependence And Competition

The visible customer target is regional aviation. AIR's public language says it has supported regional airlines around the world for 20 years and names regional aircraft families. ARR's public language says much of its operations leadership comes from the airline industry and that this operator-level experience helps it understand customers. These are valuable claims because regional operators live with a specific economics problem: aircraft are often less valuable than new mainline jets, but downtime can still be expensive because the fleet, route network and spare-aircraft pool are thin. A missing component on a small aircraft can disrupt an entire day of utilization.

Regional aircraft support also creates customer concentration risk. The same specialist knowledge that makes a supplier useful can narrow the customer base. If the company is especially strong on Saab 340, ATR, Beechcraft, Caravan, ERJ or CRJ support, its fortunes depend on how many operators still use those aircraft, how often the relevant parts fail, how much inventory remains in circulation, whether airlines retire or part out fleets, and whether larger providers or OEM channels remain expensive enough to leave room for a specialist. Public pages do not show customer count or concentration, so this risk must be left open.

The substitute set is varied. A customer can send work to a large MRO, use the OEM channel, buy a replacement part, search marketplaces directly, pull a part from a spare aircraft, wait for scheduled maintenance, use an internal engineering team, or accept the delay. That means ARR/AIR must win on some combination of speed, credibility, price, platform fit and relationship. A small supplier does not need to beat every substitute in every case. It needs to be the preferred answer for the cases where the customer values a narrow recovery path.

Large MRO groups compete on breadth and reputation. AAR, VSE and Duncan Aviation show the public face of that competition. AAR is broad across repair and parts. VSE combines aftermarket distribution and MRO. Duncan Aviation sells full-service business-aircraft support. OEM channels compete on factory authority and documentation. Marketplaces compete on visibility and seller count. In-house teams compete on knowledge of the customer's own fleet. Against that field, Aviation Repair Resources' plausible differentiation is hands-on repair development, regional-aircraft familiarity, DFW-area logistics and AIR Group parts linkage.

Competition also includes the customer's decision to do nothing immediately. Delaying a flight or leaving an aircraft out of service can be rational when the aircraft is spare, the component is non-urgent, the part price is too high, or the customer expects a cheaper route to appear. That substitute limits pricing power. AOG pricing can be high only when the aircraft's next revenue use is worth saving and the supplier's answer is credible. If the customer has slack capacity, urgency falls and the quote becomes more price-sensitive.

Unofficial market signals should be used carefully. LinkedIn links on company pages show that ARR and AIR maintain public professional profiles, but social presence does not prove customer satisfaction. Marketplace links show where inventory might be searched, but they do not prove fill rates. The company's own video and image-heavy site design suggests a business that sells practical facility credibility, but visuals are not audit evidence. The useful signal is not hype; it is the way the public surfaces converge around the same support thesis: regional aircraft, repair, parts, engines, tooling, GSE and customer urgency.

Customer dependence would be the biggest fact to change the assessment. A list of recurring regional airline, cargo, charter, leasing or maintenance customers would tell us whether ARR/AIR is embedded in actual fleets or mostly a spot supplier. Retention by fleet type would show whether customers come back after the first urgent recovery. Revenue by top customer would show concentration. Quote win rate would show whether the supplier is chosen for value or used only as a last resort. Public evidence does not provide those facts, so the assessment must preserve uncertainty.

The positive case is that small operators often need exactly this kind of supplier. They may not have the leverage to receive immediate OEM attention, the internal capability to develop a repair, or the spare fleet to absorb downtime. If ARR/AIR can deliver honest, traceable, fast-enough service, it can earn trust that a larger competitor cannot easily displace. The negative case is that small operators are cost-sensitive, and a supplier dependent on urgent jobs may face lumpy demand, credit risk and hard bargaining. The difference between those cases is retention.

Regulation, Operational Risk And Digital Continuity

Regulation is both a barrier and a liability. Part 145 certification can make a repair station more credible because customers know it operates within a defined FAA framework. It also creates ongoing obligations. Facilities, equipment, materials, data, personnel, records, manuals, quality control, inspection and FAA access are not optional. The company must preserve compliance while responding to customer urgency. That combination creates the classic aviation maintenance tension: speed is valuable, but speed cannot come at the expense of traceability, approved practice or release discipline.

The ARR public site says FAA/EASA certified Part 145. That is an important claim because EASA recognition can matter for parts or aircraft tied to European registration, leasing, or operator requirements. However, the public site text reviewed here does not provide certificate numbers or current scope. The reader should treat the statement as a company claim that requires verification through official certificate records before a customer relies on it. In a commercial diligence file, the next step would be to match the claim to FAA repair-station data, certificate number, ratings, limitations and any foreign approval details.

Operational risk begins with rework. If a repaired component returns with a defect, the customer loses the very downtime the supplier was paid to avoid. Rework also consumes shop capacity and trust. The second risk is documentation. A physically sound repair with weak records can still create return-to-service, lease, resale or insurance problems. The third risk is scope drift: accepting work outside the shop's practical or approved capability. The fourth risk is supplier delay. A repair can be complete except for one traceable material, one approval, one specialty tool, one outside process or one freight movement.

Inventory risk is different but related. A parts distributor or exchange provider must know what it owns, what is consigned, what is serviceable, what is repairable, what is life-limited, what documentation is attached, what has demand and what is obsolete. A public listing of CT7-9B engines is useful, but engine economics are complicated by cycles, life-limited parts, shop visit status, program eligibility, return conditions and lessee credit. A part listed as available may have a very different value depending on trace and release paperwork. Customers pay for confidence in that paperwork.

Digital continuity has become a practical operating risk. AOG communications, inventory searches, quote approvals, document exchange, shipping coordination and customer support depend on email, websites, marketplace accounts and sometimes remote access to records. ARIN RDAP records showing public IP assignments for AVIATION REPAIR RESOURCES INC do not prove resilience, but they do make network accountability part of the public record. The RDAP links for ARR-43 and C08755253 show organization records; the IP records show small active assignments. For a downtime business, the question is whether digital systems fail gracefully when the customer is already under time pressure.

Cybersecurity is not visible in the public evidence. The company website uses older static-site technology, and the public pages include links to email, marketplaces, video and professional-network profiles. That is normal for a smaller business, not proof of weakness. The missing facts are domain security, email protection, backup discipline, access controls, incident history, vendor exposure and customer-data handling. Because parts records, quotes, aircraft data and customer contacts can be sensitive, a buyer should treat digital continuity as part of supplier diligence even when the core service is physical.

Geopolitical risk is muted but present. The company is U.S.-based, serves aviation, mentions FAA/EASA certification, uses parts and engine markets, and may support aircraft that operate internationally. Export controls, sanctions, customs, end-use restrictions, foreign repair approvals and bilateral aviation safety arrangements can affect whether a part or repair can move across borders. The public pages say regional airlines around the world, but do not disclose regions, customer countries or export-control procedures. A global customer should verify those controls before relying on the supplier for cross-border support.

The operational-risk conclusion is that the public evidence supports a specialist that lives in a high-trust, high-friction market. That is the source of both value and risk. If quality systems, records, labor retention and digital coordination are strong, the company can sell downtime avoidance at attractive prices. If any of those elements break, the same narrow service unit becomes fragile. Aircraft maintenance is unforgiving because the customer discovers supplier weakness at the worst possible time: when an aircraft is already not earning.

The Facts That Would Change The Judgment

The first economics fact would be revenue by line: component repair, repair development, tooling and GSE, parts sales, exchanges, rentals, managed inventory, technical assistance, aircraft sales and engine leases. Without that split, it is impossible to know whether ARR/AIR is mainly a repair shop, a parts distributor, an exchange supplier, a program manager, or a mixed support platform. Each business deserves a different multiple and risk discount. A repair-heavy company depends on labor productivity and utilization. A parts-heavy company depends on inventory turns and spread. A rental-heavy company depends on asset utilization and return conditions.

The second economics fact would be gross margin by line after rework, freight, credit losses, inventory write-downs and warranty costs. A downtime supplier can show impressive top-line activity while earning thin margin if it buys expensive parts to satisfy urgent customers, absorbs rework, or carries inventory that ages out. It can also earn excellent margin if it owns scarce stock at low basis, repairs parts efficiently, turns exchange pools quickly and prices urgency honestly. Public evidence cannot distinguish those cases.

The third economics fact would be working capital. Parts inventory and engine or aircraft assets consume cash. Consignment and supplier credit can reduce cash burden. Customer deposits and quick payments can improve it. Airlines and operators under stress can create receivables risk. The quality of the business depends on whether capital is locked in slow-moving stock or deployed in parts that repeatedly solve urgent problems. Public pages show categories, not capital efficiency.

The first reliability fact would be verified turnaround time by work type. A repair station's value is not its average turn across easy jobs. It is the distribution: how often does it meet the promised date, how often does it miss because of internal capacity, and how often does it miss because of outside processes or missing parts? A buyer should ask for on-time completion, median and 90th-percentile turnaround, AOG response times and reasons for delay. Those numbers would turn the article's thesis from plausible to measurable.

The second reliability fact would be rework and warranty history. A fast repair with high return rate is a false saving. A slower repair with near-zero rework can be better if the customer has spare capacity. Rework by component family, warranty cost, nonconformance history, audit findings and customer complaints would show whether quality discipline supports the public claims. FAA inspection outcomes and any enforcement history would also matter.

The third reliability fact would be inventory fill rate. AIR's parts model depends on whether it can actually supply the needed unit when the customer calls. The right metric is not website count. It is AOG request response, quote conversion, fill rate, part trace acceptance, shipment speed and substitutions. Marketplace visibility can help, but a buyer wants to know whether AIR has the item, can prove it, can ship it and can stand behind it.

The first retention fact would be repeat customer share. The ARR site says success is gauged by customers that continually come back for support day in and day out. That is the right metric. Repeat revenue would prove that customers value the service after experiencing it. One-off emergency wins are useful but fragile. A recurring program or repeat repair relationship is stronger because it shows trust.

The second retention fact would be customer concentration. A small aviation support supplier can look stable if two or three airlines or leasing customers are active. It can be vulnerable if one fleet retirement or procurement change removes a large share of revenue. Customer count, top-five concentration and contract duration would change the risk judgment more than another generic capability statement.

The third retention fact would be platform durability. If the company's best knowledge is tied to aging aircraft families, retirements can create both risk and opportunity. Retirements increase teardown supply and parts availability, but they reduce future flight-hour demand. Continued operation of older regional aircraft creates maintenance demand, but only if customers keep flying them and if support economics remain favorable. The best evidence would be customer fleet plans and demand by aircraft family.

The fourth retention fact would be employee retention. In a specialist repair shop, people are the operating memory. A company that retains experienced composite, sheet-metal, engineering, inspection and customer-support people can deliver value beyond written procedures. A company that loses them becomes a set of assets without the same judgment. Public pages cannot show employee churn, training depth or succession.

The final judgment would change most if all three categories improved together: strong margins, strong reliability and strong retention. Any two without the third are incomplete. Strong margin without reliability can fade as customers leave. Strong reliability without margin may be a customer gift rather than a business. Strong retention without margin can hide underpricing. For Aviation Repair Resources, the public evidence is good enough to make the downtime thesis credible. It is not enough to declare the thesis proven.

Bottom Line

AVIATION REPAIR RESOURCES INC matters because aircraft availability is a commercial unit assembled from certified work, parts access, technical judgment, equipment, logistics and continuity. The company is not interesting merely because a directory record names it or because an ARIN record shows network accountability. It is interesting because the public ARR and AIR surfaces describe a practical regional-aircraft support account: repair development, composites and sheet metal, PMA or owner-fabricated alternatives, tooling and GSE, regional parts, exchanges, managed inventory, engine sale or rental and AOG support around a DFW-area base.

That account can be valuable in the aviation maintenance market described by FAA rules, BLS labor data and Oliver Wyman's MRO forecast. Older fleets, aircraft-production constraints, technician demand and parts scarcity all make downtime avoidance more valuable. A small specialist can exploit those frictions if it knows the aircraft, owns or can source the right parts, keeps qualified labor, documents the work and responds faster than large channels. The customer's purchase is not a repair in isolation. It is a shorter interval between defect discovery and aircraft return.

The investment or supplier risk is that public evidence does not show private performance. ARR/AIR could be a useful, trusted niche with repeat regional customers and strong repair economics. It could also be a thin small-business surface with limited inventory, lumpy demand and undisclosed concentration. The difference is not visible from website language alone. The missing facts are straightforward: certificate scope, capability list, customer count, utilization, turnaround performance, rework, inventory turns, margins, program revenue and retention.

The right public conclusion is therefore disciplined but not dismissive. Aviation Repair Resources should be priced as a downtime-avoidance specialist whose value rises when certified labor, repair development, serviceable parts, tooling and regional-aircraft knowledge prevent a grounded aircraft from staying grounded. The cheaper substitute is always available: wait, search marketplaces, use a larger MRO, call the OEM, cannibalize a part, or rely on in-house maintenance. The company earns its premium only when those substitutes cost more in lost aircraft time than the specialist's invoice. Public records make that mechanism visible. Private operating facts decide how often it works.