Summary

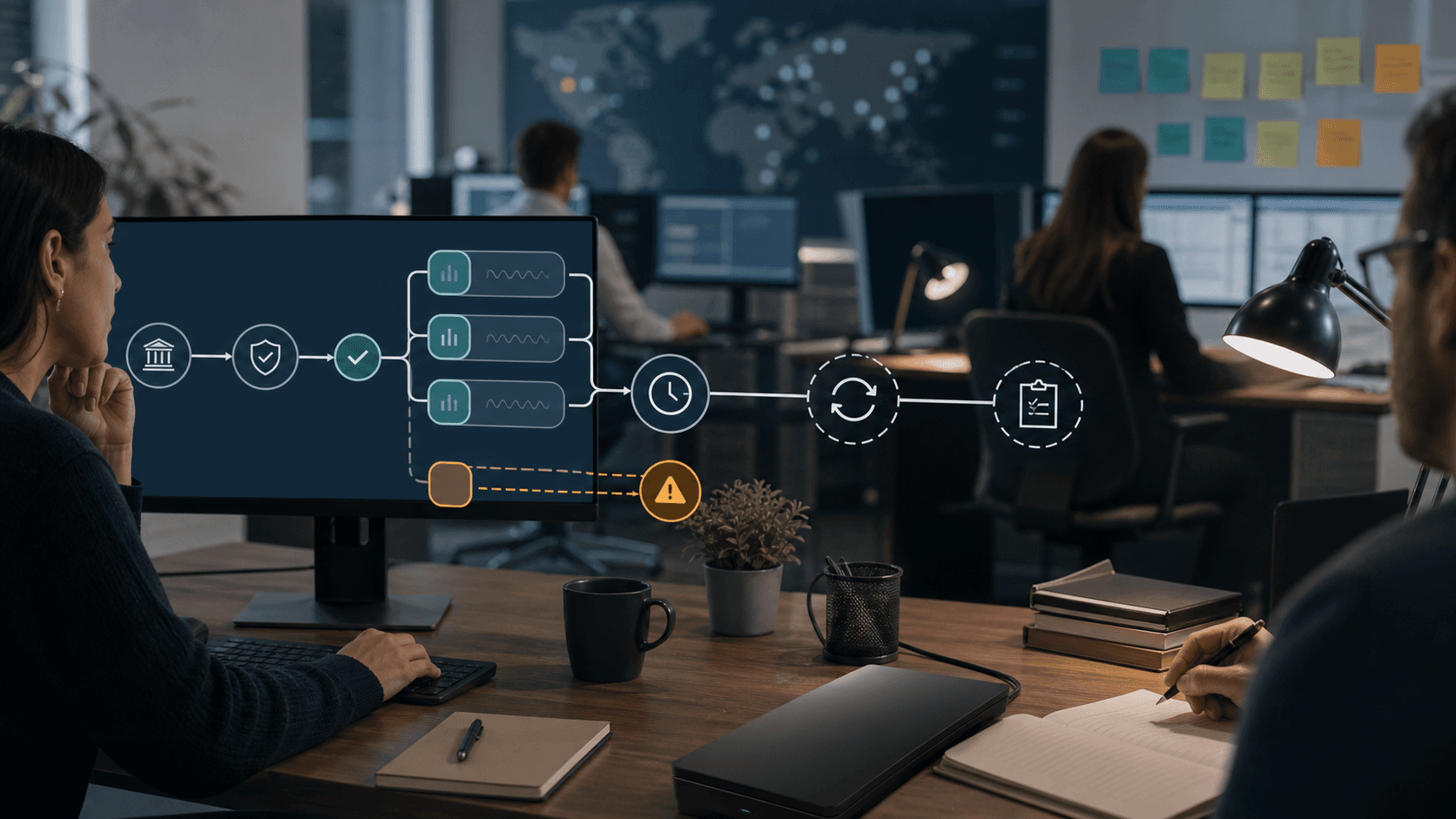

- Plaid's core automation is not simply "connect a bank account." It is the conversion of a user's permission, institution login, account selection, and continuing access state into a signal that an app can use for onboarding, account verification, transaction insight, ACH risk, or money movement.

- The signal is strongest when the application treats Link, Auth, Transactions, Identity, Signal, Transfer, webhooks, dashboard evidence, and error handling as an operating system for financial-data workflows, not as a one-time API call.

- The public evidence supports Plaid as a broad, mature connectivity layer, but it does not provide an independent cross-institution benchmark for link success, freshness, cost, or return-rate outcomes. Vendor metrics and customer stories should be read as directional, not universal.

- The commercial case is best where faster onboarding, lower card-network dependence, account validation, fraud review, and richer financial context exceed the costs of consent maintenance, support escalation, compliance review, fallback handling, and platform dependence.

The bank-link signal is the product that matters

Plaid's public identity is easy to compress: it lets apps connect to users' financial accounts. That compression is useful for consumers, but it is incomplete for operators. A bank-link platform is not valuable because a user sees a familiar interface. It is valuable when the resulting signal can survive the routine mess of financial services: a bank changes its login flow, a user revokes permission, an OAuth token expires, a transactions feed is stale, a lender needs ownership confidence, a payment team needs account validation, or an ACH risk model says the debit is too likely to return.

The core task behind Plaid is therefore an accepted signal task. A user gives permission, chooses an institution, authenticates, and selects accounts. Plaid turns that chain into an Item, an access token, product-specific data, webhooks, request identifiers, institution-health signals, and dashboard logs. The app then decides what the signal is good for. In a budgeting app, it may be good enough to show a transaction list with a visible freshness note. In a lender's workflow, it may support cash-flow review but still require adverse-action and compliance logic outside Plaid.

In a payment flow, it may validate that an account can be used, but it does not remove the need to manage ACH authorization, return exposure, identity mismatch, and customer support.

This is why Plaid should not be judged by API breadth alone. Plaid's developer documentation spans Auth, Balance, Signal, Identity, Transfer, Transactions, Investments, Liabilities, Enrich, Identity Verification, Monitor, Protect, Assets, Income, Statements, Layer, and other products. Breadth matters because financial workflows rarely stop at one endpoint. A pay-by-bank flow may need account and routing data, balance information, identity comparison, ACH risk scoring, a processor token, transfer monitoring, and exception handling. A lending flow may need transaction history, income evidence, statements, and auditability. A personal-finance app may need recurring refresh, transaction categories, deleted transactions, and user-facing explanations of freshness. The breadth is only useful when the application knows which signal is being accepted and which signal remains uncertain.

The central question is whether Plaid can keep financial-data connections reliable, permissioned, and current enough for repeated account, identity, transaction, and transfer decisions. The public answer is conditional. Plaid has a mature product surface, a large network claim, detailed operational documentation, institution-health tooling, a consumer control portal, and public trust material. But a developer still inherits exception work.

Plaid's own docs describe common errors that can occur even when an integration is correct, including expired credentials or consent, product data that is not ready, unsupported products, missing OAuth permission, institution outages, and rate limits. A system that treats those states as edge cases will disappoint users. A system that treats them as normal operating states has a better chance of extracting value from Plaid.

Plaid automates a permission chain, not a financial decision

Plaid Link is the starting point for most Plaid workflows. According to Plaid's Link documentation, Link is the client-side component that users interact with to connect financial accounts and allow the application to access those accounts through Plaid. The same documentation says Link is mandatory for all Plaid integrations except a small set of products that do not require end-user interaction. It handles login, credential validation, multi-factor authentication, error handling, account selection, confirmation emails, and OAuth handoff where institutions require it.

That is a large automation task. It removes the need for each fintech, bank, lender, payroll app, personal-finance tool, or payment team to build its own institution search, credential flow, OAuth return path, and user consent ceremony. It also standardizes the token exchange pattern. The application creates a Link token, the user completes Link, Link provides a temporary public token, the backend exchanges it for a long-lived access token and Item identifier, and product endpoints use that Item to fetch or evaluate data. Plaid's API reference describes the API as JSON over HTTPS, with request identifiers on responses and separate sandbox and live hosts.

But the user-facing ceremony is not the decision. A linked account does not mean "safe to fund," "identity verified," "cash flow sufficient," "income stable," "customer low risk," or "payment guaranteed." It means a permissioned connection and product response exist under specific conditions. The app has to decide what to do with that response. Plaid's own Auth documentation reinforces the distinction: Auth can retrieve account and routing information for ACH, wire, or equivalent bank-to-bank transfer flows, but Auth must be used with a payment processor unless the customer uses Plaid Transfer. Auth can be combined with Balance, Signal, and Identity, but those combinations still require the application to define risk thresholds, compliance checks, and customer support procedures.

This separation is healthy if operators respect it. It lets Plaid focus on the connectivity layer while customers retain responsibility for the business process. It becomes dangerous when a product team treats account linking as a guarantee. The difference is easiest to see in payments. Account validation can help satisfy operational and compliance needs, but ACH returns can still occur. A risk score can help block or review a debit, but it does not know a merchant's margin, refund policy, risk appetite, customer history, or legal obligations.

A transaction feed can model cash flow, but transactions may be pending, modified, removed, or delayed by an institution.

Plaid's strongest use cases therefore have explicit downstream decisioning. The application asks a narrow question: can this account receive a transfer, does this account appear to belong to the same person, is this transaction history current enough for this feature, is this debit too risky to approve automatically, or should the customer enter a fallback flow? Plaid supplies a structured signal. The operator accepts, rejects, reviews, or asks for more evidence.

Link reliability depends on consent renewal and user return paths

The first operational question is not whether Link can produce a successful first connection. It is whether the connection can be repaired when the real world changes. Plaid's Link overview recommends update mode when an application will access an Item on a recurring basis. Update mode refreshes an Item if it enters an error state, such as after a user changes a password or multi-factor information. The same page warns that duplicate Items can increase bills and confuse users. It also notes that Plaid periodically updates Link, so an app's test suites and business logic should tolerate changes in the user-facing flow.

Those details matter because repeated financial-data access is not a static permission grant. Users forget passwords, banks change flows, OAuth connections expire, phone numbers change, joint account ownership complicates selection, and consumers revoke access from a bank or from a Plaid control surface. Plaid's Items API documentation includes webhooks for Items entering an error state, login repair, new accounts, pending disconnection, pending expiration, user permission revocation, and user account revocation. Those are not rare technical footnotes. They are the shape of the operating problem.

The app has to design for them. A payroll product that uses Plaid to collect direct-deposit account information needs a path for an employee whose bank link expires before payday. A personal-finance app needs to explain stale balances without sounding broken. A lender needs to know whether missing transaction data means the customer has no relevant transactions, the institution is degraded, or the Item requires user action. A pay-by-bank checkout needs to avoid pushing a customer into a dead-end Link loop while a shopping cart timer is running.

The quality of the bank-link signal is therefore partly a product-management discipline. The application needs pre-Link messaging, a clear reason for asking for access, a customer support script, update-mode notices, duplicate-item prevention, and a plan for users who cannot or will not authenticate. Plaid can simplify the ceremony, but it cannot make every consumer trust the app, every bank support the same products, or every institution connection remain healthy.

This is also where privacy and conversion meet. A user who understands what is being shared is more likely to complete the flow, but a user who later feels surprised by data scope becomes a support and trust problem. Plaid's consent and control materials emphasize transparency and revocable permission. That is strategically important. It is also operationally demanding because the app must keep its own copy, retention, and downstream use aligned with what the user reasonably understood at the moment of connection.

Institution coverage is product-specific, not a universal promise

Plaid's homepage says its network spans 12,000 financial institutions across 20 countries, with over one million daily connections and use by one in two banked adults in the United States. These are scale claims from Plaid, not independent measurements in the public record reviewed here. They still point to an important advantage: for many builders, maintaining direct integrations with thousands of institutions would be impractical.

Coverage, however, is not a single number. A financial institution may support Auth but not the exact transaction depth a lender wants. It may support account selection but have degraded Transactions updates. It may have healthy item login but partial support for another product. Plaid's Institutions API documentation directs developers to coverage explorers and institution endpoints, and describes health entities for request types such as Auth, Balance, Identity, Transactions updates, Investments updates, Liabilities updates, and Item logins. The status values include healthy, degraded, and down.

That granularity is the right model. A product manager should not ask, "Does Plaid support this bank?" The better question is, "Does this institution support the product, account type, country, and reliability level needed for this workflow today, and what happens if that support is degraded tomorrow?" A rent-payment application that needs a debitable checking account faces a different coverage question from an expense app that needs merchant names, or a lender that needs two years of transaction history, or a brokerage-transfer flow that needs investment data.

Plaid's Institution status in Link shows another product choice: Link can proactively tell users if an institution connection is not performing well. That is better than failing silently after the user has typed credentials. But it also confirms that institution health is part of the user experience. If a popular bank is degraded, the app may suffer conversion loss even if Plaid's core API is up. The app then needs a fallback: try later, use micro-deposits, upload a statement, select another account, or route the user to support.

The evidence limit is important. Public status and coverage pages do not reveal a complete, independent success-rate distribution across institutions, products, countries, account types, and time windows. A buyer can inspect Plaid's public docs and dashboard tooling, but the real procurement question is empirical: how often do the target customers' top institutions connect, refresh, and recover under this exact workflow? That answer usually requires private implementation data, pilot results, and ongoing monitoring.

Freshness is the hidden boundary around transaction insight

Plaid's Transactions documentation says the product can retrieve up to 24 months of transaction data and stay up to date with webhooks. It lists typical fill rates for selected fields, including 100 percent for amount, date, and description, 97 percent for merchant name where a merchant is applicable, and 95 percent for personal finance category. It also warns that transaction data is not static: users make new transactions, and past transactions can change as institutions process them.

That last point is the operating boundary. A transaction feed is not a final ledger. Pending card authorizations can settle for different amounts. Merchants can be renamed. Categories can change. Institutions can update at different frequencies. Plaid says it checks for updated transactions regularly and that the frequency is typically one or more times a day, depending on the institution. The app can use webhooks and, for eligible customers, on-demand refresh. But "one or more times a day" is not the same as real-time cash certainty.

For personal-finance management, that may be acceptable. A budget app can say a feed was last updated at a given time, show pending transactions clearly, and revise a category later. For underwriting, the timing question becomes more serious. A lender using transaction data to assess cash flow must decide how to treat missing days, pending payroll, account transfers, overdrafts, cash deposits, and changed descriptions. For payment risk, a balance check or risk score may need to be contemporaneous with the payment attempt. A stale transaction feed can be informative without being decisive.

The same issue appears in dashboards and customer service. Plaid's Account Activity documentation says the Dashboard Logs page shows the past 14 days of API activity, including requests, responses, webhooks, and Link events. That is useful for diagnosing recent failures. It does not remove the need for the customer to persist its own audit trail, event history, consent state, support notes, and decision records. A financial application cannot outsource accountability for a user-impacting decision to a third-party dashboard with a limited time window.

The key is to expose freshness as a first-class input. An accepted Plaid signal should include not only the data value but the last successful update, the institution status, the Item error state, the relevant webhook trail, and the confidence needed for the workflow. If a product hides freshness from its own business logic, it risks turning a good connectivity platform into a misleading decision layer.

Account validation and ownership are adjacent, not identical

Plaid Auth is often discussed as instant account verification. Its documentation says Auth can request a user's checking, savings, or cash-management account and routing number, making it easier to initiate credits or debits through ACH, wire, or equivalent networks. The same page says Auth can only be used with debitable checking, savings, or cash-management accounts, and that credit cards cannot receive payments directly through electronic interbank transfers.

This matters because account validation is narrower than identity proof. Nacha's WEB debit rule material says Originators of WEB debit entries must include account validation as part of a commercially reasonable fraud detection system for the first use of an account number or a change to it. Nacha also says the minimum standard is to determine that the account is a legitimate, open account to which ACH entries may be posted. It explicitly distinguishes that minimum from proving account ownership, while noting that some Originators may need more rigorous assessment depending on their risk profile.

Plaid's product structure reflects the same distinction. Auth can provide account and routing information. Identity can retrieve or match owner information on file at the financial institution. Plaid's Identity documentation says /identity/get retrieves names and contact information from the institution, while /identity/match returns match scores against user-provided identity data. It says both endpoints can reduce fraud, improve onboarding, and complement Know Your Customer checks. It also says 97 percent of Items initialized with Auth provide Identity data as well.

The combination is useful, but it still needs business interpretation. A name mismatch can be innocent in a joint account, business account, nickname, marriage-name change, or family account context. A match can still be limited public evidence if the payment risk is high, the transaction amount is large, the account is newly linked, or the customer behavior is suspicious. A valid account can still return because funds are limited public evidence, the consumer disputes the debit, the account is frozen, or the bank applies a restriction.

The prudent operating design is layered. Use Auth to reduce manual entry and validate bank-account details. Use Identity or Identity Match where account ownership matters. Use Balance or Signal where funds and ACH return risk matter. Use KYC tooling where legal identity obligations apply. Use manual review for the cases where automated signals disagree or where the loss severity is too high. Plaid improves the signal stack; it does not collapse account validity, ownership, authorization, and risk into one answer.

Signal turns risk into rules, and rules need owners

Plaid Signal is the clearest example of Plaid moving beyond raw data access into decision support. Plaid's Signal documentation describes Signal as an ACH risk-management product. It says Signal Transaction Scores uses machine learning to assess transaction risk using more than 80 attributes, and that the Signal Platform considers more than 1,000 risk factors. It also says Plaid applies a risk score and then a ruleset turns scores into actions, with business rules managed through the Dashboard. The docs claim ultra-low latency, specifically p95 under two seconds, for transaction evaluations.

That performance claim should be read carefully. It is a Plaid documentation claim, not an independent benchmark in the public evidence reviewed here. It is still strategically important because risk evaluation has to fit inside user-present flows such as account funding or checkout. A fraud score that arrives after the user has left the session may be useful for monitoring, but it is less useful for a real-time approval decision.

The more important point is that Plaid says the customer must configure and tune rulesets to match business risk tolerance. This is exactly right. A score is not a policy. A score needs thresholds, treatment paths, manual-review rules, escalation logic, customer messaging, and feedback from actual returns and disputes. A merchant with low margins and high fraud exposure may block or review more transactions. A payroll app with an established employer relationship may tolerate different risk. A lender may use transaction risk as one input among many.

Signal also has scope limits. Plaid says Signal Transaction Scores can evaluate US domestic ACH transactions, including Standard and Same Day ACH, and cannot evaluate RTP, RfP, debit-card, non-US bank-account, or wire-transfer transactions. For other cases, Plaid points to Balance. That is an important guardrail. A team that reads "payment risk" as a universal payment-risk engine will overextend the product. A team that reads it as ACH return-risk support can fit it into a clearer control framework.

Signal's value therefore depends on a feedback loop. The customer needs to report returns and decisions, measure false positives, examine lost conversion, distinguish limited public evidence-funds risk from unauthorized-return risk, and revise thresholds. The software can score; the operator must supervise. Without that supervision, Signal becomes a black box that may approve transactions a business cannot afford or block customers a business wanted to keep.

Transfer raises both convenience and accountability

Plaid Transfer extends the workflow from connectivity and risk into money movement. Its documentation describes Transfer as a US-only multi-rail payment platform for ACH, RTP, RfP, wire transfer, and FedNow transactions. It presents Transfer as a single Plaid integration for connecting user accounts, making transaction decisions, managing risk, moving money, monitoring transfer activity, and simplifying reconciliation. The same page says Transfer requires an application and approval before integration, though sandbox work can begin while approval is pending.

Transfer may improve the business case where the customer does not want to assemble separate providers for account linking, risk, payment initiation, reconciliation, and monitoring. But it also concentrates dependency. If a product relies on Transfer for funds movement, Plaid is no longer only the account-connectivity layer. It becomes part of the payment operating stack. That raises the bar for incident response, treasury operations, support, reversals, returns, refund handling, authorization records, and reconciliation.

Plaid's billing documentation underlines the point. It says public documentation does not include a price list, that customers see pricing through access requests or sales, and that pricing models differ by product. It describes one-time fees, subscription fees, per-request flat fees, flexible fees, and Transfer-specific fees. It also says subscription-billed products such as Transactions, Liabilities, and Investments can continue to bill while a valid access token exists, even if no API calls are made or calls cannot succeed because an Item is in an error state. For Transfer, it describes Auth fees, Signal or Balance fees, per-transfer fees, and possible operational fees for actions such as ACH returns, incoming wires, or support interventions.

The unit economics therefore cannot be inferred from a product page. Plaid may reduce engineering work and speed onboarding, but the customer still needs a volume model. How many users attempt Link? How many succeed? How many Items add paid products? How many subscription Items remain active but stale? How many Signal calls are made per attempted payment? How many payment failures, reversals, or support events occur? How much conversion is lost to fallback flows? How much card-network cost is avoided by pay-by-bank adoption? The answer will vary sharply by use case.

The best Transfer case is not "Plaid moves money." It is "Plaid reduces the number of moving parts in a payment workflow while preserving enough controls for the operator to understand failures, costs, and customer treatment." That is a much higher bar, but it is the bar that money movement deserves.

Privacy history makes consent quality a hard requirement

Financial-data connectivity lives or dies on user trust. Plaid's public safety and trust material says Plaid uses encrypted APIs, invests in security infrastructure, provides 24/7 monitoring, and lets users manage connections through Plaid Portal. Its Trust Center lists certifications including SOC 2 Type 2, ISO 27001, ISO 27701, TruSight, Doyensec, and AWS Foundational Technical Review. Plaid's legal page says users can use my.plaid.com to manage connections between accounts and apps, while also noting that third-party apps and account providers have their own terms and that Plaid is not responsible for those third parties' acts or omissions.

Those materials are relevant, but they are not the whole trust story. In July 2022, a federal court in the Northern District of California granted final approval to a class-action settlement in In re Plaid Inc. Privacy Litigation. The case resolved allegations about how Plaid collected and disclosed financial data through its interface. A settlement order is not the same as an independent finding on every allegation. It is still a permanent reminder that the consent layer is not cosmetic. In this market, the interface, data scope, retention policy, deletion process, and user explanation are part of the product's risk surface.

Plaid's recent consumer-control article, "How Plaid puts you in control of your financial data", published in March 2026, emphasizes secure connection, control over access, connection management, and data deletion upon request. Plaid's open-finance trust material says more than 150 million consumers have used Plaid to link accounts from over 12,000 institutions and that consent safeguards are anchored in transparency, control, and security. These are Plaid's claims, and they speak to the right issues.

For a Plaid customer, however, trust is shared. A consumer may see Plaid's interface, but the consumer is trying to use another company's app. If that app asks for broad access without a clear reason, stores data longer than users expect, buries deletion instructions, or uses transaction data for a surprising purpose, Plaid's controls cannot fully absorb the trust damage. The operator needs data minimization, retention discipline, user-facing explanations, permission renewal, deletion workflows, and support training.

Consent durability also has a technical dimension. A consumer who revokes access should not be treated as a broken account. They made a choice. The app needs to stop using the stale signal, explain the consequence, and offer a path to reconnect or proceed another way. That is a product and compliance requirement, not merely an error state.

The policy environment favors APIs but does not remove uncertainty

Plaid's market sits inside a broader shift from credential-based aggregation toward API-based, permissioned data access. The CFPB's personal financial data rights page describes Section 1033 as requiring covered entities, subject to CFPB rules, to make transaction data and other information available to consumers. The Federal Register final rule published in 2024 described requirements for covered data to be made available to consumers and authorized third parties in standardized, machine-readable form, with functional requirements around reliability, security, and competition.

The legal path has been unsettled. A June 2026 analysis from Consumer Finance Monitor reported that the CFPB's 2024 Section 1033 rule had been challenged, that enforcement had been enjoined by a federal court in Kentucky, and that appeal activity was stayed while the CFPB pursued modifications. That does not make open finance disappear. It means the exact federal rule timetable and obligations were not settled in the public evidence reviewed here.

Industry standards still matter. The Financial Data Exchange describes itself as an organization dedicated to a common standard for secure and convenient access to permissioned consumer and business financial data. Plaid's own FDX explainer says the standard covers secure authentication and authorization, user-experience guidelines for consent journeys, and endpoints and data structures for specific use cases. Plaid's open finance page positions its infrastructure as FDX-aligned and aimed at giving institutions visibility and control over permissioned connections.

This policy and standards context changes the competitive question. Plaid is not merely competing on developer convenience. It is competing to be a trusted intermediary in a market where banks, fintechs, regulators, standards bodies, and consumers all care about consent, security, reliability, and control. If APIs become more standardized and financial institutions improve direct developer interfaces, some parts of aggregation may commoditize. If implementation remains fragmented and institutions vary in readiness, Plaid's network, tooling, and support layer remain valuable.

The likely outcome is not simple displacement. It is a negotiation over where value sits. Raw account access may become more standardized. App risk review, conversion optimization, data normalization, dashboard visibility, institution-health management, ACH risk, consent renewal, and multi-product workflow support may become more important. Plaid's challenge is to keep moving up that stack without asking customers to trust opaque signals they cannot supervise.

Customer stories show a pattern but not a universal benchmark

Plaid publishes customer stories that show how different organizations use its platform. Varo's customer story says Varo saw a 60 percent lift in card activations for customers who linked accounts through Plaid compared with customers who did not. Alliant Credit Union's story says member complaints fell by 20 to 30 percent after adoption of Plaid-supported open banking APIs. Wethos' story says Wethos launched banking with Unit and Plaid in 41 days and later saw 40 percent month-over-month user growth and higher retention among banking users.

These examples are useful because they show the kinds of benefits Plaid can support: fewer complaints from connectivity problems, faster product launch, stronger activation, and better engagement. They should not be treated as guaranteed outcomes. They are vendor-published case studies with specific products, customers, baseline conditions, and business models. The causality may include other product decisions, marketing, customer mix, prior vendor performance, or broader organizational changes.

The stronger lesson is operational. Plaid tends to create value when the old process is visibly worse: manual bank account entry, micro-deposit delays, broken aggregator connections, support-heavy open banking access, disconnected risk tools, or slow provider assembly. If the incumbent process is already smooth, if the target institutions are poorly supported, if conversion is limited by trust rather than UI, or if payment returns dominate the cost structure, the gain may be smaller.

A buyer should therefore run a use-case-specific evaluation. Rank the institutions customers actually use. Map the exact product coverage required. Measure Link conversion by institution and device. Track update-mode completion. Compare ACH returns before and after Signal or Transfer adoption. Count manual reviews and support contacts. Measure false positives, not only fraud losses. Track billing per active user and per successful decision, not only per API call. Plaid's value is not a generic network number; it is the difference between the old and new workflow under the buyer's actual constraints.

The operating bill includes work Plaid cannot erase

Plaid can reduce integration work, but it does not eliminate operating work. The first category is supervision. Teams need monitors for status, institution health, webhook delivery, failed Link sessions, stale Items, and product-specific errors. Plaid's status page shows system-level status and says institution and Item-level status should be checked through the Dashboard or Institutions API. That means an app cannot rely only on a global uptime badge. A global API can be healthy while a target institution or product flow is degraded.

The second category is integration maintenance. Plaid says Link can change automatically and that SDKs should be kept current. APIs evolve, products change access requirements, OAuth flows vary, and new rails require new operating assumptions. A company with a thin engineering team may save months by adopting Plaid, but it still needs owners for SDK updates, error taxonomy, webhook retries, token storage, data retention, and regression tests around the customer journey.

The third category is review and exception handling. Common Plaid errors are not necessarily Plaid failures. They may represent expired consent, missing OAuth permission, unsupported products, institutions not responding, accounts not found, rate limits, or data not ready. The customer has to decide which errors block the user, which trigger retry, which open a fallback, and which go to support. A live workflow needs a queue for unresolved bank-link issues and a policy for how long a decision can wait.

The fourth category is rollback and fallback. A bank-link feature should have alternatives for users who cannot connect: manual entry, micro-deposits, statement upload, another account, customer support, or delayed completion. Plaid itself supports additional Auth verification methods such as micro-deposits and database verification, but each fallback changes conversion, risk, timing, and support cost. A no-fallback system will look efficient until the first high-volume institution outage or customer segment that cannot complete Link.

The fifth category is unit economics. Plaid's pricing models are product-specific and not fully public. Subscription products can continue charging while valid access tokens exist, and per-request fees can accumulate if a product calls Signal, Balance, Identity Match, refresh endpoints, or other paid endpoints too frequently. Good implementation includes token cleanup, duplicate-item prevention, product initialization discipline, call suppression where data is not needed, and measurement of cost per useful decision. The cheapest integration may be the one that asks for fewer products at Link and adds only what the use case actually needs.

How to judge Plaid in a repeated workflow

The right evaluation framework starts with the accepted signal. For each workflow, define what Plaid must prove and what it cannot prove. For account funding, Plaid may need to confirm a debitable account, retrieve account numbers or create a processor token, check balance or risk, and monitor revocation. For underwriting, it may need to provide transaction history, categories, cash-flow evidence, statements, or income data. For personal-finance management, it may need recurring refresh and comprehensible categories.

For open-finance institution connectivity, it may need FDX-aligned access, app directory visibility, permissions management, and connection-health monitoring.

Then define freshness thresholds. A personal-finance feature can tolerate a different data age than an ACH debit. A loan decision may need the most recent payroll cycle; a monthly budgeting chart can tolerate slower refresh. If the application cannot articulate freshness, it cannot articulate trust.

Next, define exception states. Which error codes require user action? Which require institution retry? Which require support? Which trigger a fallback? Which stop a payment? Which allow an informational warning? The app should make these decisions before launch, not during a support incident.

Then evaluate institution concentration. If 70 percent of users bank at five institutions, the average network claim matters less than the performance of those five. If a customer base includes credit unions, payroll cards, limited-purpose accounts, regional banks, or non-US accounts, coverage must be tested against that population. If a use case depends on a product available only in selected countries or account types, the business should model the excluded users.

Finally, measure business outcomes against full cost. Did onboarding get faster? Did support volume fall? Did payment returns fall? Did fraud losses fall? Did manual review increase? Did conversion drop because users mistrusted data sharing? Did billing grow with stale Items? Did fallback use rise after a bank changed OAuth? Did customers understand data deletion? The answer determines whether Plaid is an infrastructure advantage or merely a convenient integration.

Plaid's defensible value is disciplined intermediation

Plaid's best argument is not that bank linking is effortless. The public evidence does not support that broad claim, and Plaid's own docs make clear that errors, institution health, revocation, freshness, consent expiration, billing choices, and fallback flows all require attention. Plaid's better argument is that it has turned a fragmented, high-risk, institution-by-institution problem into a managed workflow with a large network, standard products, developer documentation, user-facing consent, dashboard evidence, webhooks, security programs, and adjacent risk tools.

That is meaningful infrastructure. For many fintech developers, banks, lenders, payroll apps, payment teams, and personal-finance products, building equivalent coverage and operational tooling alone would be unrealistic. The business case is strongest where Plaid replaces manual entry, reduces onboarding friction, supports account validation, improves data access, gives institutions better connection visibility, or consolidates account linking and payment-readiness signals.

The risks are equally clear. Plaid can become a platform dependency in a sensitive part of the customer journey. Institution gaps can become conversion gaps. Stale data can become misleading data. A score can become an unreviewed decision. A broad consent screen can become a trust problem. A subscription Item can become a recurring cost without recurring value. A vendor case study can become an overfit business plan.

The practical verdict is conditional but positive. Plaid is valuable when the customer treats the accepted bank-link signal as a living signal: permissioned, scoped, monitored, refreshed, challenged, and paired with human or policy review where the stakes justify it. It is weaker when used as a magic translation layer between a user's bank and an app's desired answer. The difference is not cosmetic. It is the difference between faster financial workflows and automated overconfidence.