Summary

- Globe Development GmbH has more public evidence of a real infrastructure operator than many small hosting names: it lists a Münster data centre, colocation, virtual servers, mail, domains, RIPE membership, DE-CIX presence, AS12470, IPv4 and IPv6 resources, and a public claim of high availability. That supports operational substance, but not necessarily economic scale.

- The investment case is constrained by missing public revenue, customer mix and churn evidence. Globe's visible prices start very low in mail, web hosting and entry colocation, while the high-cost reliability stack depends on enough business customers buying higher-value redundancy, connectivity and managed support.

- The most important uncertainty is customer density. Globe's own references page claims more than 10,000 customers, but the examples are mostly unnamed and the public record does not show how many buy high-availability services rather than low-ARPU domains, mailboxes or basic web packages.

- The judgement is cautious: Globe appears strategically coherent as a local continuity provider, but reliability may not pay unless it can keep premium customers, pass through power and repair costs, maintain upstream diversity, and avoid being pushed into price competition with national fibre operators, hyperscale cloud and mass-market hosting platforms.

The outage a buyer is paying to avoid

The customer Globe wants is not buying bandwidth as a commodity. The customer is buying the avoidance of a business interruption. Globe's public site frames the offer around availability, secure access, backup, mirrored storage and the extension of a customer's server room into a managed platform. In plain economic terms, Globe is trying to convert downtime risk into recurring service revenue.

That is a rational offer. A small or medium-sized company can tolerate many kinds of IT inconvenience, but it cannot comfortably tolerate the loss of online ordering, external mail, customer-service data, accounting access, a hosted CRM system or the VPN path into shared records. The damage from an outage often arrives as staff idle time, missed orders, emergency contractor work, customer apology cost and management distraction rather than as a single invoice.

A local operator that can bundle hosting, connectivity, backup and support has a commercial opening if it can make the customer believe that the avoided failure is worth the monthly bill.

Globe's message is direct. Its home page says 99 percent is not enough and highlights personal advice, 99.99 percent availability, individual solutions, daily data backup, 30 days of retained backup and business liability insurance. Its high-availability page explains the problem as a set of connected failure points: network access, data centre, server and storage availability must all work together. The company says it has worked for years to design a platform with sustained availability above 99.99 percent, and it contrasts that with the lower reliability of a single server.

That promise creates the core trade-off. A reliability provider must spend before the customer's failure happens. It needs spare capacity, duplicated paths, backup storage, monitoring, support staff, replacement equipment, contracts with upstream networks, physical security, cooling, electricity resilience and procedures that do not look valuable until something breaks. The customer, meanwhile, compares the monthly price against a cheaper server, a standard fibre line, a public cloud instance, a low-cost mailbox bundle or a national operator's business broadband package.

The economics therefore turn on willingness to pay, not just technical capability. Globe can be technically useful and still face a weak return if too many customers treat high availability as an insurance policy they admire but do not buy. The company can also hold a defensible niche if a sufficient slice of Münster-area businesses value a nearby operator that can explain, install and troubleshoot a continuity stack without forcing them into a distant platform or a long national-carrier process.

Globe is a Münster infrastructure operator, not just a reseller

The public identity evidence is consistent. Globe Development GmbH lists its address at Königsberger Strasse 260 in Münster, gives Martin Stein as managing director, states HRB 5523 at the Münster court, and publishes German VAT identification DE203230688. The same Münster address appears in RIPE NCC's public member listing and in the eco Association of the Internet Industry member directory. Its contact page separates general inquiries, technical support, billing and sales addresses, which is a small but useful signal of an operating service business rather than a placeholder shell.

The operating boundary is also visible. Globe describes itself as a specialist in highly available hosting and says it provides a platform covering internet access, internet feed-in, data storage, internet security and cloud. Its services page says it has advised on business use of internet technologies since 1993 and provides its own comprehensive infrastructure from Münster. The company offers colocation, a data centre, hosted or virtual servers, mail packages, web packages, domains, radio links and security modules.

Those public pages may not disclose revenue or staffing, but they do show a product set that sits in the regional ISP and hosting category rather than in pure consulting.

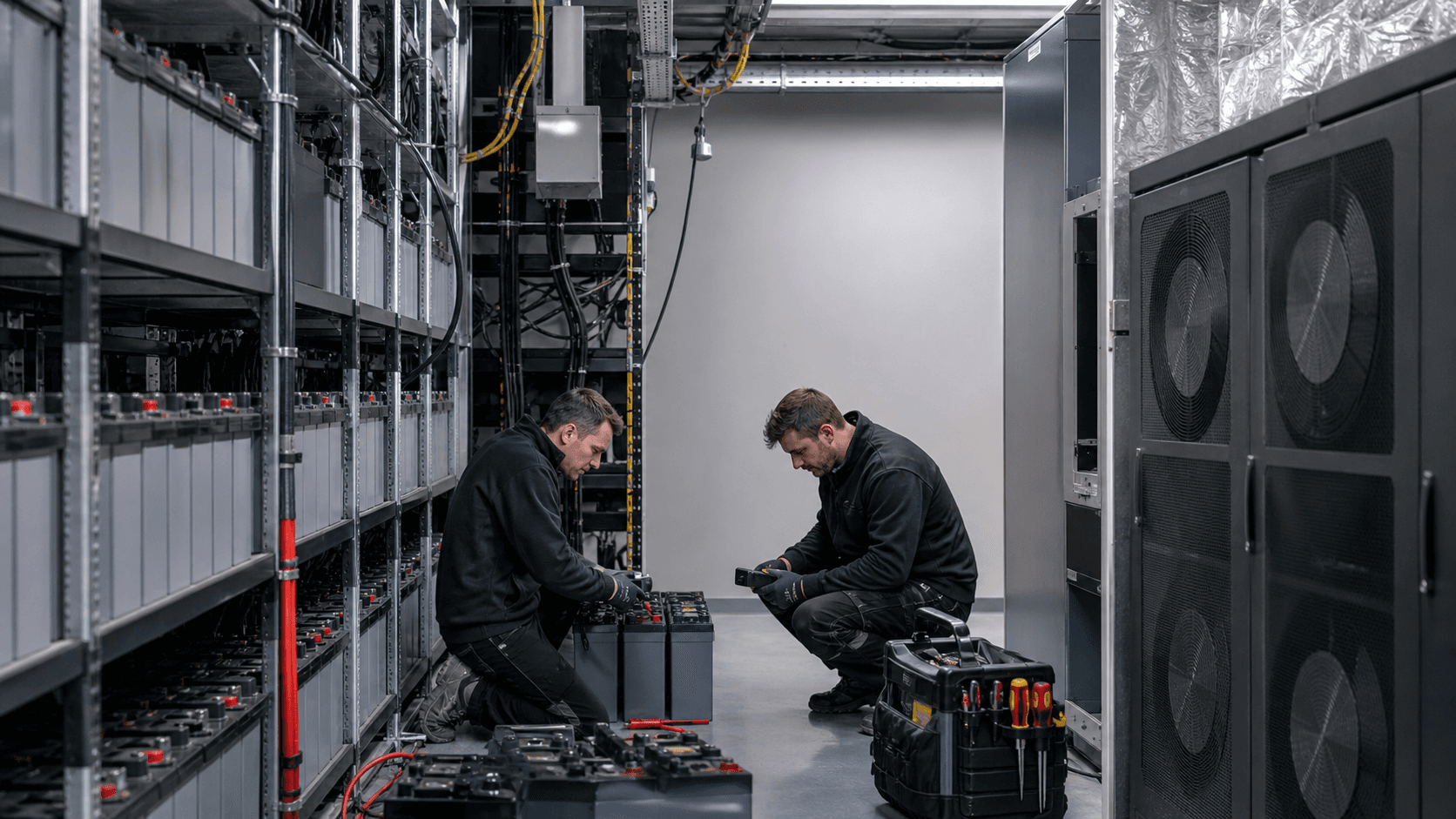

The data centre claim is central to the boundary. Globe says it operates a modern data centre with room for up to 4,000 servers. It describes UPS systems, emergency generators, cooling, fire protection, access control, around-the-clock monitoring, firewall clustering, daily backups, 30-day retention, customer servers connected on gigabit ports, and a mirrored site. It also says the data centre uses modern routing and has redundant internet links through connectivity partners including DE-CIX, Telekom, Cogent, Versatel and Open Carrier, with uplink bandwidth above 20 Gbit/s.

This is more than a storefront for somebody else's hosting panel. The combination of RIPE membership, ASN visibility, public peering records and a claimed local data centre suggests Globe controls meaningful pieces of its network and facility stack. That matters for reliability because accountability becomes clearer: the company is not only reselling a mailbox or a virtual private server; it is positioning itself as the operator responsible for the customer's path from local access to hosted application.

But the same boundary also limits the scale story. Globe's public materials are local and bespoke in tone. They emphasize Münster, personal advice, short contractual commitment and customer-specific solutions. That can be attractive to the Mittelstand, but it is not the language of a national cloud platform, a hyperscale data-centre campus, or a fibre overbuilder with mass household penetration. The company looks like a regional continuity operator with some carrier-grade tools, not a carrier whose economics are protected by national access scale.

The business model sells control, locality and flexibility

Globe's business model has three visible pillars: local infrastructure, managed reliability and flexible commercial terms. The colocation pages monetize physical rack space and power. The high-availability pages monetize virtual machines, SAN storage, data mirroring, load balancing, firewalling, VPN and backup. The radio-link pages monetize local access into Globe's data centre and then onward to the internet. The domain, mail and web-hosting pages add lower-priced recurring services around the same customer relationship.

The strongest part of the offer is control. Globe tells customers that some data is better kept locally than in a generic cloud, but that certain servers need broadband internet access and a higher level of resilience than the customer's own server room can easily provide. Its solution is to extend the customer's server environment into a managed platform. That speaks directly to SMEs that have not fully migrated to hyperscale cloud, still value physical or jurisdictional proximity, and need continuity without building duplicate infrastructure themselves.

The second part is locality. The company says its radio network in Münster offers stable, low-latency, weather-independent gigabit radio links as an alternative to fibre lines. The offer includes an internal route to Globe's data centre, so customers can reach server, storage or backup services without going across the public internet, and also a symmetrical internet uplink in the booked bandwidth. For a customer near Globe's network nodes, the proposition is not only hosting; it is a local access and continuity design.

The third part is flexibility. Globe says it does not impose forced contract terms in the offered products. The terms page says contracts have a minimum term of one month unless the contract says otherwise, with cancellation rules stated in the contract and at least 14 days to month-end. The radio-link page says installation is simple when line of sight exists, that setup fees are not charged, and that products are delivered without forced term commitment. That is commercially appealing for small firms that dislike long telecom commitments.

Flexibility, however, cuts both ways. It lowers buyer resistance, but it also weakens revenue visibility. A national network operator can often rely on long contract durations, bundled mobile/fixed accounts and a large existing base. A small regional provider offering short commitments must earn retention through service quality, not contract lock-in. That makes the cost of support and responsiveness part of the product margin. If the service is excellent, churn may be low. If customers move to bundled fibre, Microsoft 365, a cloud platform, or a national operator's managed package, short terms make the revenue easier to lose.

The model is coherent if the customer relationship expands. A business that starts with domains and mail can add hosting, then backup, then a secure access path, then colocation or a redundant radio/fibre design. But public prices make the entry-level products look thin. Mail packages start from EUR 1.90 per month plus VAT, web hosting from EUR 2.90, one rack unit colocation from EUR 39 plus VAT and a full rack from EUR 390 plus VAT, with power and cooling charged separately at 29 cents per kWh plus VAT on the published colocation pages.

These visible prices are not enough by themselves to support a high-availability infrastructure story; the upside must come from customers buying larger bundles, managed work and premium continuity.

Network evidence supports competence, not scale

The network evidence is useful because it is harder to dress up than marketing copy. Globe appears in RIPE NCC's member directory with service area Germany. RIPE database material and third-party BGP tools identify Globe Development GmbH with AS12470 and organization ORG-GGIG1-RIPE. PeeringDB lists GLOBE Development GmbH with AS12470, the AS-GLOBENET name, RIPE::AS-GLOBENET, network type NSP, regional scope, open general peering policy, no ratio requirement and no contract requirement.

The route evidence shows a real resource footprint. BGP tools list originated IPv4 prefixes including 194.59.213.0/24, 212.124.32.0/19 and 217.25.64.0/20, plus IPv6 prefix 2a00:1050::/32. BGP.tools currently counts three upstream carriers and more than 200 peers, while PeeringDB shows 100 IPv4 prefixes and 100 IPv6 prefixes as self-reported prefix limits. Hurricane Electric's BGP toolkit also lists the main originated prefixes. IPinfo and IPIP identify AS12470 as a German network associated with Globe Development GmbH, with IPinfo showing ranges including 212.124.32.0/19, 217.25.64.0/20 and 194.59.213.0/24.

The interconnection evidence is also material. PeeringDB lists Globe at DE-CIX Frankfurt and DE-CIX Düsseldorf with operational 10G public peering entries, IPv4 and IPv6 addresses, and route-server participation. BGP.tools likewise lists DE-CIX Frankfurt and Düsseldorf entries. DE-CIX's own connected-network page for Frankfurt includes GLOBE Development GmbH, AS-GLOBENET, open policy and active status, while BGP exchange pages show AS12470 at Frankfurt and Düsseldorf. RIPE's Routing Information Service peer list shows AS12470 as an up peer at 80.81.194.230 and 2001:7f8::30b6:0:1.

This evidence supports technical competence. A company with its own ASN, RIPE membership, routed prefixes, exchange connections and upstream diversity is better placed to discuss BGP failover and redundant access than a simple web host. Globe's own high-availability page talks about customers using their own autonomous system and BGP-capable routers to support redundant connectivity. That is consistent with the public network footprint.

The limitation is scale. A few prefixes, two public exchange points and three listed upstreams are meaningful, but they are not enough to imply a large national customer base or high traffic volume. PeeringDB does not disclose Globe's traffic level. BGP.tools peers can include route-server peers and do not automatically translate into high revenue. The presence of an ASN tells us Globe can operate a network; it does not tell us how many customers pay enough to cover the cost of keeping the network resilient.

For the economic question, the network record should be read as a floor, not a ceiling. It confirms that Globe is not merely a brand pasted over rented hosting. It does not prove that reliability pays. The proof would be sustained revenue per customer, low churn, utilization of the claimed data-centre capacity, and a customer base large enough to spread replacement, power, staffing and compliance costs across more than a handful of critical accounts.

Pricing shows a low entry point and a hard upsell

The most uncomfortable evidence for Globe's profitability is the visible pricing. Low posted prices are useful for customer acquisition, but they can anchor buyer expectations below the true cost of reliability. A EUR 1.90 monthly mail package, EUR 2.90 web package, EUR 39 one-unit colocation product and EUR 390 full rack product are not economically equivalent to a high-touch continuity service. They are feeder products unless the customer buys more.

Mail illustrates the issue. The Basic package includes 10 POP3/IMAP accounts, 1 GB of mail storage, 10 GB monthly transfer, spam and virus filtering, autoresponder, 100 aliases, FTP access, subdomains, daily backup and free email support for EUR 1.90 per month plus VAT. The Business package lists 100 accounts, 5 GB storage, flat traffic, filtering, add-on domains, 2,000 aliases, FTP access, subdomains, daily backup and email/telephone support for EUR 9.90 plus VAT. The Premium package lists 300 accounts, 10 GB storage, flat traffic and unlimited aliases, FTP accesses and subdomains for EUR 19.90 plus VAT.

Those packages may be old, and the site footer says copyright 2019, so the prices should be treated as currently visible public pricing rather than necessarily newly revised offers. Even with that caveat, they show the margin challenge. Mailboxes with support, filtering and daily backup at low monthly prices depend on automation, shared infrastructure and low service burden. A few support calls can consume the contribution from many cheap accounts. The customer's value is high, but the posted price is low.

Colocation looks more plausible, but still has density risk. One rack unit at EUR 39 per month plus VAT includes a 100 Mbit connection to the router, high-speed access to external internet links, a climate-controlled server room, traffic flat rate, one IP address with reverse delegation, extra IP addresses by need, 24-hour server monitoring with email notification, and 100 GB backup space.

Full rack pricing at EUR 390 per month plus VAT includes 40 rack units, 1,000 Mbit router connection, carrier-neutral access over other providers, traffic, UPS-secured power, redundant A/B power supply, diesel generator, climate control, raised floor, video monitoring and IP addresses under RIPE rules. Power and cooling are billed separately at 29 cents per kWh plus VAT.

The rack product moves closer to the reliability economics because power is passed through and the customer pays for scarce facility space. Yet full-rack pricing in a regional data centre still competes with national colocation providers, cloud substitution and the customer's own server-room economics. Globe's differentiator has to be the combination of local support, connectivity, backup and access design, not only the rack. If buyers strip the offer down to cheap space and cheap transit, the economics worsen.

The price architecture therefore implies an upsell requirement. Globe needs customers to buy premium continuity: mirrored data, managed virtual machines, secure access, load balancing, firewalling, VPN, redundant connection paths and hands-on support. Its site says individual SLAs are available on mail packages and that virtual machines can be booked in units with CPU, RAM, SAN storage, data mirroring, backup, firewall, web cache, load balancer and VPN modules. That is where the economic value should sit. The public record, however, does not quantify how many customers buy those higher-value modules.

Reliability raises the cost base before it raises density

Reliability is expensive because it multiplies assets. A single server becomes a virtualized cluster. A local disk becomes a SAN, then a second mirrored SAN, then a daily backup cycle with multiple generations. One router path becomes two access paths, two routers and two switches. A cheap internet line becomes upstream diversity, peering, monitoring and route policy. A simple hosting account becomes backup retention, support commitments and documented handling of faults.

Globe's own pages make that cost structure visible. The high-availability page says effective availability is the product of network access, data centre, servers and storage. The data-centre page lists UPS, emergency generators, cooling, fire protection, access control, monitoring, firewall cluster, gigabit customer ports, daily backups, 30-day retention and site mirroring. The redundant-connection page says high availability requires two paths with different routing into Globe's network, which can be two radio links to different nodes or a combination of fibre and radio.

Those are not marketing ornaments; they are cost drivers. UPS batteries age. Diesel generators require testing and fuel management. Fire systems, access control and monitoring need maintenance. SAN hardware and backup storage must be replaced before failure. Routing equipment must be patched and eventually refreshed. Wireless gear on roofs has installation, alignment, access and weather-exposure costs even if the service is designed to be stable. Staff must be available when the customer reports the outage that the product is meant to avoid.

The data-centre power line is especially important. Globe's colocation pages separately charge for power and climate at 29 cents per kWh plus VAT. That pass-through helps protect margin, but it also exposes customers to the economics of energy-intensive infrastructure. In a period when data centres across Europe face power-price volatility, grid constraints and efficiency expectations, a regional operator has less purchasing leverage than the largest cloud and colocation groups. The more Globe sells reliability, the more it must pay attention to power resilience and energy efficiency.

The operating challenge is utilization. A data centre with room for up to 4,000 servers is valuable only if enough of the space, power, connectivity and support capacity is used by paying customers. Underutilized redundancy is a drag. Overutilized redundancy is a risk. Globe must keep enough spare capacity to make the reliability promise credible without letting unused assets consume the margin from low-price products. That balance is hard for every regional infrastructure operator.

The cost base also recurs in repair cycles. The article's title question turns on recurring repair costs because telecom and hosting systems do not stay fixed once installed. Cables are moved. Roof access changes. Batteries expire. Customers request upgrades. Vendors end support. Security rules change. A small provider can manage this well if it has disciplined operations and loyal customers. It can also be squeezed if each customer expects bespoke attention while paying commodity prices.

Suppliers and exchanges reduce risk while preserving dependence

Globe's network evidence shows sensible supplier diversification. BGP.tools identifies upstreams including Cogent Communications, GTT Communications and Deutsche Telekom. Globe's own data-centre page lists connectivity partners including DE-CIX, Telekom, Cogent, Versatel and Open Carrier. PeeringDB and DE-CIX records show the company present at Frankfurt and Düsseldorf. This mix reduces the risk that one supplier failure cuts off every customer path.

Exchange presence is economically useful. Public peering can improve performance and reduce reliance on paid transit for reachable networks. DE-CIX Frankfurt is one of the world's most important interconnection hubs, and Düsseldorf offers a regional option closer to Globe's home market. An open peering policy and route-server participation help a smaller network reach many counterparties without negotiating bilateral sessions with each one.

But diversification does not eliminate dependence. Globe still depends on access to upstream carriers, exchange platforms, data-centre power, equipment vendors, software vendors, domain registries and radio-site availability. Its high-availability platform mentions VMware and EMC/HP in the about page. Its secure-access page refers to FortiToken and a Radius server. The website's domain page says Globe is a DENIC registrar and can book many domains, but domain services remain connected to registry and registrar rules. RIPE membership gives resource-management standing, but IP address use remains governed by RIPE policy.

The supplier question matters because regional providers often compete on responsiveness while depending on large suppliers for the hardest infrastructure layers. If an upstream carrier changes pricing, an exchange port needs upgrade, a software licensing model changes, or a hardware platform reaches end of life, Globe cannot pass every cost to customers without risking churn. It can blunt the risk by using multiple paths and by charging for power, managed modules and bespoke support. It cannot make the cost stack disappear.

The same is true for wireless access. Globe's radio-link product is positioned as a stable, weather-independent alternative to fibre and a quick installation route where line of sight is available. That can be a genuine advantage in a city where civil works delay fibre delivery. Yet radio depends on roof access, line-of-sight geometry, equipment placement and local spectrum conditions. It is a valuable regional tool, not a universal substitute for dense fibre footprint.

Customer concentration is the unseen variable

Globe's references page claims more than 10,000 customers and says many are Mittelstand businesses.

It then lists examples without naming most customers: a US large company using colocation and European server/network monitoring; a food wholesaler using highly available internet uplink from fibre and radio with automatic switching and availability above 99.9 percent; a Swiss company running CRM applications on the high-availability platform; an electrical wholesaler using hardware-token secure access; a Japanese telephone group booking radio links for VPN connections; software houses and system houses using the platform for shop solutions, backup and virtual phone systems.

This is helpful but incomplete evidence. The examples are credible in the sense that they map closely to Globe's product set. They show the type of customer pain the company is trying to solve. They also support the idea that Globe's value is not only access or hosting, but continuity for business applications. However, the public page does not name the accounts, date the references, disclose contract size, disclose churn, or distinguish between high-value managed customers and low-value domain or mailbox customers.

That distinction is decisive. A claim of more than 10,000 customers can sound large, but a hosting and domain provider can accumulate many small accounts. The economic value of 10,000 low-price mailboxes, web packages or domains is very different from 10,000 businesses buying redundant access and managed high-availability infrastructure. If a large share of the base is low ARPU, Globe needs the support load to be low and the upsell conversion flow to be strong. If a small share of the base is high ARPU, Globe faces concentration risk if a few large continuity customers leave.

The references also show a geographic and segment concentration question. Globe's strongest operating story is Münster and the surrounding business market. Locality helps with trust, installation and service, but it caps density. A radio network only serves customers within feasible reach. A local data-centre relationship is strongest for companies that value proximity. Customers outside that circle have more alternatives and less reason to prefer a Münster operator unless the price or service is exceptional.

There is also a customer maturity issue. Globe's materials speak to firms that still operate servers, storage and applications close to their own environment. That remains a real market. Many German SMEs are cautious about cloud migration, have legacy applications, and value personal support. But the direction of travel for email, collaboration, CRM and hosting has been toward platform software, managed cloud and SaaS. The customers most willing to pay for local continuity may be valuable, but they are not necessarily the fastest-growing portion of the market.

The public evidence therefore supports a narrow conclusion: Globe has customer-market fit for business continuity use cases, but the margin cannot be inferred from the customer count. The key missing variable is the revenue distribution across the base. Without that, reliability may be either a profitable premium niche or a costly promise subsidized by thin commodity services.

Competition makes reliability a threshold, not a moat

The German telecom market is large, competitive and capital-intensive. Bundesnetzagentur's 2025 report says active fibre connections rose from 5.3 million at the end of 2024 to 6.4 million at the end of 2025, while fibre's share of active fixed broadband connections increased from 13.7 percent to 16.5 percent. The 2024 annual report estimated German telecom external revenue at EUR 61.1 billion, with fixed networks accounting for slightly more than half of the market and competitors still holding a majority of external revenue even as Deutsche Telekom gained share.

For Globe, the headline is not that Germany lacks demand. Demand exists. The problem is that the market contains many substitutes. A business customer can buy fibre or broadband from large network operators, colocation from national data-centre providers, public cloud from hyperscalers, email from global software platforms, domains from specialist registrars, and managed IT from regional system houses. Many of these substitutes bundle reliability into the base expectation rather than selling it as a separate narrative.

VATM's 2025 market analysis argues that competitors continue to drive much of Germany's digital infrastructure investment and that competition provides almost 62 percent of fibre-to-the-home connections. BREKO's 2024 market analysis says fibre expansion reached 43.2 percent by mid-2024 and that Deutsche Telekom's competitors accounted for the majority of homes passed, homes connected and homes activated. These facts show a market where non-incumbent operators can matter. They also show that regional operators are not competing in a quiet niche.

The substitution threat is strongest at the low end. Globe's mail and web-hosting prices compete with automated platforms that have massive scale. Its domain prices compete with large registrars. Its virtual-server offer competes with cloud instances and specialized hosting providers. Its connectivity offer competes with fibre providers and business broadband bundles. Reliability becomes a threshold requirement: every serious provider claims uptime, backup, monitoring and support. Globe must make the reliability feel specific, local and accountable enough to justify choosing it.

The strongest competitive defense is bundled local continuity. A hyperscale cloud can deliver global scale, but it cannot install a Münster roof antenna, combine it with a local data-centre path, route a customer's autonomous system, and have a local support conversation in the same way. A national carrier can provide access, but may not care about the customer's hosted application. A system house can manage applications, but may not own the network. Globe's strategic logic is to sit between those layers.

That position is defensible only if the customer values the bundle. If customers separate the bundle into cheapest domain, cheapest email, cheapest cloud server and cheapest fibre line, Globe loses the economic argument. If customers price the avoided outage and prefer one accountable regional operator, Globe has a reason to exist.

Regulation and security add operating load

Globe operates in Germany, a market with mature telecom, data protection, network-security and consumer-protection expectations. RIPE membership and public number-resource operations bring registry obligations. Domain registration connects the company to DENIC and other registry rules. Hosting and managed services involve data protection, security, abuse handling and customer communications. The company's terms require customers to use services properly, follow legal rules, report faults, maintain data security principles and reimburse expenses where faults arise from the customer's area of responsibility.

Bundesnetzagentur's annual reporting shows a market where bandwidth demand and fibre adoption are rising, but also where regulators closely watch telecom development, broadband performance and market structure. Its net-neutrality reporting separately documents ongoing monitoring of open-internet obligations. A regional provider does not carry the same public-profile burden as the largest national operators, but it still operates under a regulatory environment where network performance, transparency, data security and lawful handling of customer services matter.

Security is both a cost and a selling point. Globe's pages refer to firewall clustering, VPN, token authentication, spam and virus filtering, secure access to data, isolated internal traffic to hosted servers and data backup. These features let Globe sell risk reduction. They also require ongoing maintenance. Security systems must be patched, monitored, renewed and explained. Abuse reports must be handled. Customer misconfiguration can create support cost. Data retention and backup expectations must be managed carefully so that customers understand what is protected and what is their responsibility.

Operational risk is not only cyber risk. Physical systems fail. Roof access can be delayed. Fibre routes can be cut. Cooling can break. Power systems can degrade. Backup restores can take longer than the customer expects. A high-availability claim gives the customer a reason to buy, but it also raises the reputational cost of failure. If Globe's differentiation is reliability, failures are not just incidents; they strike at the product's economic rationale.

Geopolitical risk is lower than for operators exposed to sanctioned jurisdictions or politically sensitive international backbones, but vendor, routing and energy dependencies remain. Cogent, GTT, Deutsche Telekom, DE-CIX and equipment vendors are commercial dependencies rather than geopolitical red flags. The bigger issue is resilience to supplier pricing, software licensing, and European infrastructure-cost pressures. Small operators are often disciplined because they must be; they are also vulnerable because they have less leverage.

Market signals point to a real but narrow franchise

Unofficial market signals should be handled carefully. There is no public evidence in the reviewed sources of a major scandal, sanction problem or obvious identity confusion around Globe Development GmbH. Third-party directories such as eco, WLW, Creditreform snippets, IPinfo, IPIP, BGP.tools and Hurricane Electric consistently point to the same Münster company and AS12470 context. Those signals support identity and operating continuity, but they do not provide audited financial performance.

The strongest positive signal is consistency over time. Globe says it has advised on business use of internet technologies since 1993. BGP.tools shows AS12470 registered in 2002 and active under RIPE, while the RIPE organization record was created in 2004. The website shows a product set that has not chased every fashion: colocation, high availability, domains, mail, backup, radio links and secure access. That stability is valuable in infrastructure markets where customers often prefer a provider that survives.

The strongest negative signal is dated public presentation. Many product pages carry a 2019 copyright footer and describe VMware, EMC/HP, FortiToken and specific prices in a style that may reflect an older market moment. A dated site does not mean the infrastructure is dated; many regional B2B operators underinvest in marketing while keeping operations stable. But dated public materials make it harder for a new buyer or analyst to see whether the price book, technology stack, security posture and customer examples are current.

Another signal is the absence of disclosed financials in the reviewed public material. There are registry and business-directory entries, but no public revenue, EBITDA, customer churn, rack utilization, ARPU, support headcount, capex or traffic revenue mix in the accessible sources used here. That absence is normal for a private German GmbH of this type, but it leaves the economic judgment dependent on inference from products and network evidence.

The result is a narrow-franchise assessment. Globe appears real, operational and specialized. It likely has a defensible role for local businesses that need a practical continuity partner. It does not present public evidence of national scale, high growth, unique technology or a pricing umbrella strong enough to make reliability automatically profitable. The franchise may be good because it is local and specific; it may be limited for exactly the same reason.

What would change the judgment

The bullish case would strengthen if Globe disclosed or could demonstrate four things. First, a meaningful share of revenue from high-availability services rather than low-price mail, domains and web hosting. Second, strong utilization of its data-centre capacity and radio network without excessive fault or repair cost. Third, multi-year retention among business continuity customers despite short or flexible contracts. Fourth, clear evidence that customers buy Globe for integrated reliability rather than buying isolated commodity services.

Named customer proof would help. The references page is useful, but anonymous examples do not show current contract strength. Case studies showing a redundant access design, recovery performance, contractual scope and measurable business benefit would make the reliability proposition more tangible. So would updated public pricing for high-availability modules, transparent SLA options and current technical descriptions of the platform.

Network evidence could also change the view. More visible upstream diversity, higher disclosed traffic levels, additional exchange locations, strong RPKI hygiene, visible route-security practice and current peering data would support the claim that Globe's network role is deepening. Conversely, shrinking prefixes, stale peering records, loss of exchange presence or visible routing-security gaps would weaken the infrastructure argument.

The bear case would strengthen if the visible low-price products dominate revenue, if high-availability demand is occasional rather than recurring, if large customers are few, or if the local radio/fibre footprint is too small to create density. It would also strengthen if power, equipment and software costs rise faster than Globe can reprice, or if national operators and cloud platforms make bundled continuity cheap enough that Globe's local advantage becomes sentimental rather than economic.

The current conclusion is therefore measured. Globe Development GmbH has enough public evidence to be treated as a genuine regional infrastructure and business-continuity provider. Its reliability proposition is economically sensible because customers do fear costly outages. But reliability does not pay just because the engineering is real. It pays only when customers value the avoided failure more than the operator's recurring cost to prevent it. On the public evidence, Globe's technical case is stronger than its disclosed economic case, and the missing price, revenue and customer-mix evidence belongs at the centre of the conclusion.