Summary

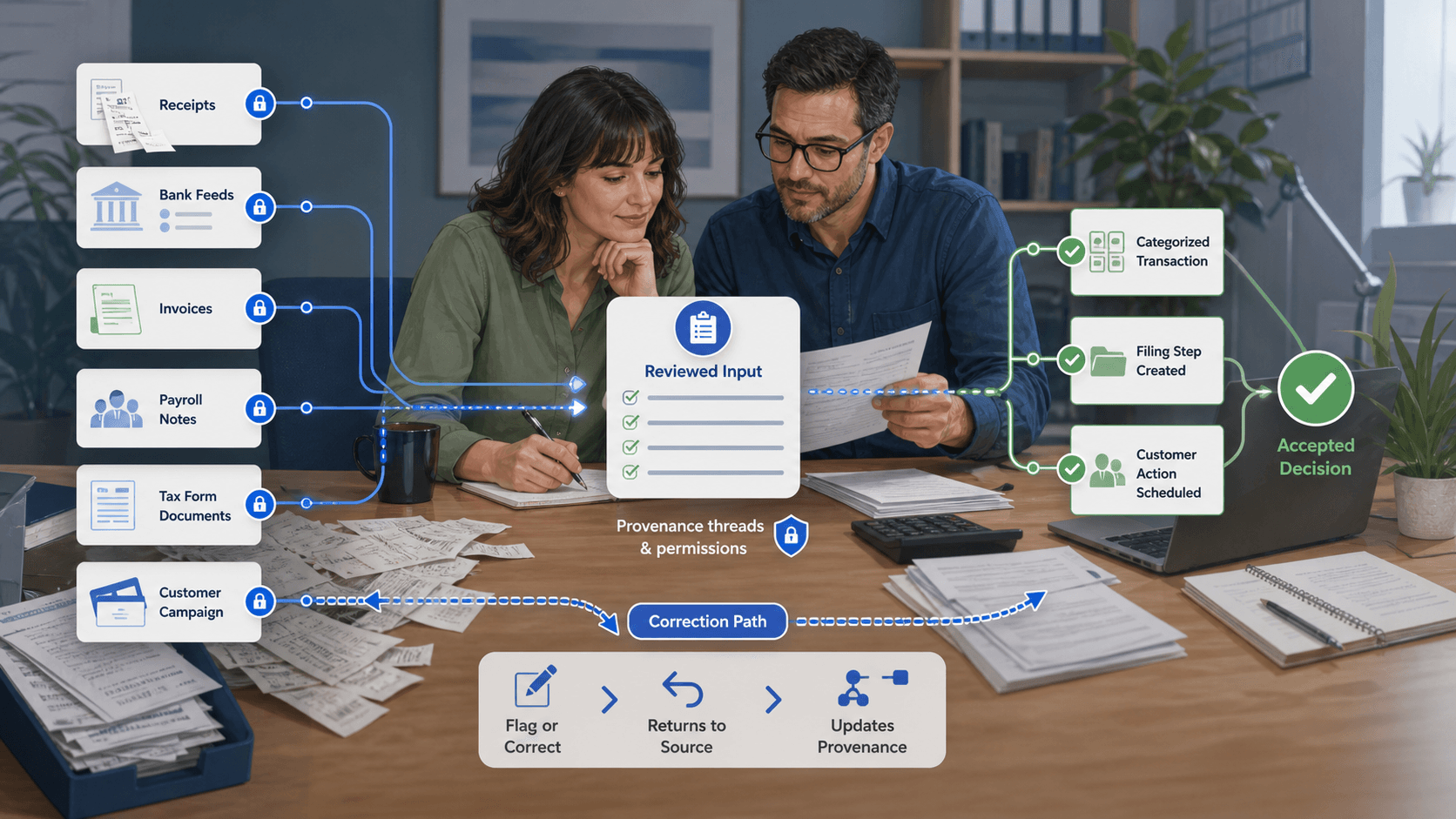

- Intuit Inc. should be judged by the accepted financial workflow decision, not by a polished AI answer. A useful output is a step that a business owner, taxpayer, accountant or marketer can rely on because the source data, rule context, permission state, human review and correction path remain visible.

- The company has a rare distribution advantage because QuickBooks, TurboTax, Credit Karma and Mailchimp already sit near money movement, tax preparation, credit choices, accounting records and customer data. That advantage also raises the cost of error: a wrong category, stale rule, bad sync, misleading eligibility message or overconfident recommendation can transfer work and liability back to the customer.

- Buyers should measure cost per accepted financial step. The numerator includes subscriptions, filing fees, expert help, app integration, bookkeeping cleanup, tax review, support time, correction, compliance work, data-sharing decisions and switching cost. The denominator should include only steps that survive review, audit, correction and operational use.

The answer is not the output

Intuit Inc. is one of the few software companies whose consumer and business products sit directly in front of decisions that carry money, compliance and trust consequences. QuickBooks is where many small and mid-market businesses collect invoices, payments, payroll records, bills, bank feeds and accounting categories. TurboTax is where consumers and small businesses turn messy tax facts into federal and state filing decisions. Credit Karma influences consumer credit, debt and financial-product choices. Mailchimp turns customer data into marketing actions.

Intuit Assist and the company's AI-assisted automation strategy are meant to bring those surfaces together as an AI-driven financial platform.

That breadth changes the normal enterprise-software evaluation. For a generic assistant, a plausible answer may be enough to keep a conversation going. For Intuit, the useful output is not the sentence. It is the accepted step after the sentence: a transaction category that an accountant leaves in the books, a sales-tax treatment that a developer-tested app does not corrupt, a tax checklist that matches the taxpayer's actual documents, an invoice reminder that does not break the customer relationship, a payroll or cash-flow recommendation that a business owner can defend, or a campaign segment that respects consent and customer history.

Intuit's public positioning makes this test unavoidable. Its press room describes the company as a global financial technology platform serving approximately 100 million customers with TurboTax, Credit Karma, QuickBooks and Mailchimp. Its fiscal 2025 Form 10-K describes Global Business Solutions as serving small and mid-market businesses and accounting professionals, with QuickBooks and Intuit Enterprise Suite built around financial management, payroll and time tracking, payment processing, bill pay, checking through a bank partner and financing.

The same filing says the company's business platform vision includes AI automation, AI-enabled human experts and an all-in-one operating surface for running and growing a business.

The scale is not speculative. In fiscal 2025, Intuit reported total net revenue of $18.831 billion, up 16% from fiscal 2024. It reported Global Business Solutions revenue of $11.077 billion, Consumer revenue of $4.870 billion, Credit Karma revenue of $2.263 billion and ProTax revenue of $621 million. In its fiscal third quarter ended April 30, 2026, Intuit reported $8.6 billion of revenue, up 10%, with Consumer revenue of $5.3 billion and Global Business Solutions revenue of $3.3 billion. QuickBooks Online Accounting revenue grew 22% in that quarter, according to the company. These are not side experiments attached to a small AI product.

They are core revenue lines that Intuit is increasingly presenting as an AI-enabled financial operating layer.

That makes the denominator stricter. The question is not whether Intuit can answer "What does this tax form mean?" or "How should I improve cash flow?" The question is whether Intuit can preserve enough evidence, permissioning, rule currency and human review that a user can accept the next step. A financial workflow does not end when a model sounds confident. It ends when the record is right enough to close the books, file the return, get paid, explain the decision, amend it if needed and survive the later question: why did we do that?

Intuit sits between raw records and accountable action

The work Intuit is trying to automate begins before accounting, tax or marketing appears clean. A small business rarely starts with perfect records. It starts with bank transactions, point-of-sale deposits, invoices, expenses, receipts, payroll events, sales-tax obligations, customer contacts, late payments, loan applications and questions from an owner who has time pressure rather than accounting patience. A consumer tax return starts with W-2s, 1099s, prior-year facts, state rules, credits, deductions, health coverage, dependents, investments, side income and fear of making a mistake.

A marketing workflow starts with customers, purchase history, opt-in state, audience segments, campaign timing and the risk of contacting the wrong person in the wrong way.

Intuit's advantage is that it already sits inside those flows. QuickBooks can connect banking, invoicing, bill pay, payroll, payments, accounting reports and third-party apps. TurboTax can turn a taxpayer interview into forms and filing choices. Credit Karma can connect credit profile, offers and financial guidance. Mailchimp can connect audiences, campaigns, automation and reports. Intuit's AI claims therefore start from a real distribution and data position.

They are not a model vendor's general promise to "transform finance." They attach to products where users already place sensitive records and make consequential choices.

The same position creates the central risk. Intuit does not merely help a user compose text. It helps a user make records. If the record is wrong, the correction cost can arrive later, after the customer has forgotten the context. A wrong transaction category can distort profit and loss, tax planning or loan readiness. A stale tax rule can change filing confidence. A missing receipt can make an expense hard to defend. An account-sync failure can make cash look better than it is. A permission mismatch can expose payroll or customer information to the wrong app. A campaign recommendation can use data in a way the marketer cannot justify.

A credit recommendation can be personalized but still commercially conflicted or unsuitable for a user's real constraints.

This is why "AI assistant" is too weak a description. Intuit is building a financial work system with assistants inside it. Its 2023 GenOS release described a proprietary generative AI operating system with custom-trained financial large language models specializing in tax, accounting, marketing, cash flow and personal finance. The same release described GenUX and the ability to invoke actions such as contacting human experts. Its 2025 GenOS release said automated AI experience development combines rich data and AI platform capabilities with proprietary domain-specific LLMs and commercial LLMs.

Its 2025 QuickBooks AI automation release said the features could manage customer leads, track payments, send invoices and reconcile books while collaboration tools let business owners and accountants work together.

Those claims are strategically coherent. They also move Intuit closer to operating responsibility. A generic assistant can retreat to "please verify." A product that sends an invoice reminder, reconciles books, prepares a tax checklist or surfaces a loan option is closer to the workflow. In that setting, the acceptable answer is not "probably correct." It is "correct enough to act on, with the provenance and controls needed to recover if it is not."

QuickBooks is a provenance problem first

QuickBooks is the most concrete test of Intuit's automation thesis because bookkeeping is both repetitive and unforgiving. A bank feed arrives. A payment clears. An invoice is paid. A vendor bill appears. Payroll runs. Sales tax accumulates. A receipt is uploaded. A third-party app updates a customer or item. The system needs to translate these events into a book of record that a business owner, accountant, lender or tax preparer can use.

The obvious automation task is transaction categorization. That is useful, but it is not enough. The accepted output is not the first suggested category. It is a category, matched to the right transaction, source document and chart-of-accounts logic, that survives review by the person responsible for the books. If the system cannot show why the category was chosen, what document supported it, who approved it, and how to reverse it, the work has not disappeared. It has moved into later cleanup.

Public Intuit developer documentation shows why this is an engineering and governance problem rather than just a model problem. QuickBooks Online apps use OAuth 2.0 authorization, access and refresh tokens, realm IDs and user consent. Scopes define what data types an app can access, and users see requested scopes during authorization. Webhooks notify apps when data changes in connected QuickBooks company files, but live and development webhooks are configured separately and notifications can take time.

Change Data Capture lets apps poll for changed entities within a look-back window, but the documented response size limit means high-change systems need careful time windows and retry design. Common-error documentation warns about stale-entity errors, syncToken handling, duplicate document numbers and business validation failures.

These details matter because AI does not remove sync problems. It can hide them. If an app or automation categorizes from stale local data, the answer may look reasonable while the book of record has moved. If a user or third-party app changes a customer, item, bill or invoice after a local system cached it, a later write can collide. If a duplicate document number is created, the problem is not a model hallucination in the usual sense. It is workflow state.

If an API integration relies on CDC alone rather than webhooks, Intuit's publishing guidance recommends limited CDC frequency as a catch-up mechanism and says apps that handle sales tax should verify and thoroughly test transaction tax accuracy.

That is a useful public signal. Intuit's own developer surface assumes developers must maintain state, validate entities, test tax handling, handle stale writes and keep local databases current. A business buyer should apply the same logic to AI automation. If an AI feature suggests reconciliation, payment follow-up or categorization, the buyer should ask what source state it used, whether it saw the latest change, whether an accountant can inspect the trail, and whether the action can be undone without corrupting downstream reports.

QuickBooks has a commercial opportunity because many small businesses do not want to become systems integrators. They want books that are good enough to manage cash, invoice customers, pay staff, comply with taxes and talk to advisors. If Intuit can make the accepted bookkeeping step cheaper, the value is real. But the work being removed is not "typing." It is the cycle of gathering evidence, applying rules, checking exceptions, and maintaining a record that the next person can trust. The numerator includes the subscription, payment and payroll add-ons, app integration, accountant time, cleanup, support, training and correction.

The denominator is only the reviewed step that remains in the books.

TurboTax raises the liability stakes

TurboTax is a different test because the user may not understand the rules well enough to know when the assistant is wrong. A small business owner can often recognize an invoice or receipt. A taxpayer may not know which deduction, credit, schedule, state rule or filing status applies. That makes an AI answer both more valuable and more dangerous.

Intuit's TurboTax support page for Intuit Assist says the product can use AI to understand a tax situation, create a personalized checklist, help after tax data and documents are uploaded, run real-time checks for accuracy, analyze the return for deductions and credits, provide instant answers to tax questions and work alongside tax experts. The TurboTax product page emphasizes CompleteCheck, expert help, return review and guarantees, while also documenting limitations and service conditions. TurboTax Free Edition's public page says it applies to simple Form 1040 returns and that roughly 37% of U.S.

taxpayers qualify, with important exclusions for situations such as itemized deductions, self-employment or gig income, stock or cryptocurrency sales and rental income.

The accepted output in tax is therefore not "an answer about a deduction." It is a filing decision the taxpayer can submit or hand to an expert with confidence. That decision must be grounded in actual taxpayer facts, current tax rules, product eligibility, support limitations and the customer's chosen level of service. If a user starts with Free Edition but later discovers a disqualifying form, the cost is not only a price upgrade. It is lost trust, duplicated data entry, support time and the feeling of being pulled through a funnel.

If AI explains a tax situation but the user's facts are incomplete, the answer may be fluent and still operationally weak.

Public alternatives make the buyer's calculation clearer. The IRS Free File page says eligible taxpayers can prepare and e-file federal returns at no cost through Free File Alliance partners, with an adjusted gross income threshold of $89,000 for 2026 in the retrieved guidance, while also noting possible state-return and eligibility differences. The same IRS page says Free File partners must avoid deceptive online practices and upselling of additional services. Intuit's own Free File notice says it no longer offers the IRS Free File Program delivered by TurboTax.

That does not make TurboTax a bad product; it means TurboTax's commercial promise must be evaluated against a public free-filing baseline and against the cost of expert help or paid tiers.

The regulatory history also matters, even though it should not dominate a technology article. The FTC brought an administrative case over TurboTax "free" advertising, alleging that many consumers could not use the advertised free service. On March 20, 2026, the U.S. Court of Appeals for the Fifth Circuit granted Intuit's petition, vacated the FTC order and remanded after holding that the FTC's administrative adjudication of deceptive-advertising claims violated separation of powers. The legal posture changed, but the product lesson remains: in tax software, eligibility language is part of the workflow.

If users misunderstand what is free, what is covered, what requires expert help, or what facts change the answer, the product has failed before the return is filed.

AI can improve that if it narrows uncertainty early. A good assistant should say, in plain terms, what it knows, what it does not know, which documents are missing, which product path is still eligible, when a human expert should review, and what will happen if facts change. A weak assistant will maximize confidence and defer the correction to the end. The first reduces user burden. The second turns the user into the quality-control layer.

The external AI partnerships widen distribution and sharpen accountability

Intuit's partnerships with OpenAI and Anthropic put the accepted-output question into new interfaces. In November 2025, Intuit announced a multi-year partnership with OpenAI to bring Intuit-powered apps into OpenAI's conversational environment and to deepen Intuit's use of OpenAI frontier models under a $100M+ contract. OpenAI separately confirmed the partnership. Intuit's March 2026 blog said TurboTax, Credit Karma, QuickBooks and Mailchimp apps were live in that external environment for logged-in U.S. users, with examples including tax estimates, credit coaching, QuickBooks reports and Mailchimp campaign strategy.

Intuit said customer data stays within Intuit apps and is not used to train foundation models.

In February 2026, Intuit announced a multi-year partnership with Anthropic. The company said mid-market businesses would be able to build secure, customizable AI automation on Intuit's platform with Anthropic developer tooling, and that Intuit tax, finance, accounting and marketing tools would surface directly inside Anthropic products. In April 2026, Intuit said TurboTax, Credit Karma, QuickBooks, Mailchimp and Intuit Enterprise Suite were available in Claude.

These partnerships are commercially logical. Users increasingly ask financial and business questions in general-purpose AI environments. If Intuit can bring its domain data and product actions into those conversations, it can meet users at the point of need rather than waiting for them to open a separate finance app. A business owner might ask about cash flow in Claude, pull QuickBooks context, draft invoice reminders and review a report. A consumer might ask an OpenAI conversation for tax estimate help and connect TurboTax. A marketer might use Mailchimp inside a conversational workflow to draft a segmented campaign.

The risk is that conversational convenience can blur system boundaries. In finance, a user's trust often attaches to the visible conversation rather than the underlying chain of custody. If a response appears inside an OpenAI or Anthropic conversation, the user needs to know which parts came from Intuit, which came from the external model, which data was shared, what was not shared, whether the answer used live account data, whether it is allowed to initiate an action, and where the audit trail lives.

Intuit's statements that data stays within Intuit apps and that Intuit owns accuracy, compliance, security and privacy of its insights are important. They are also claims that need product-specific controls.

The accepted-output rule helps separate the layers. Model capability is the ability to understand a question and generate useful reasoning or language. Product reliability is the ability to retrieve the right Intuit data, apply the right product rules, preserve permissions, expose caveats and complete or hand off the right action. Customer outcome is whether the user made a better, cheaper, faster or safer financial decision. A partnership can improve the first layer and distribution without proving the second or third.

Buyers should not treat availability inside a conversational AI surface as evidence that a tax, credit, accounting or marketing action is accepted.

The practical test is simple: ask what happens after the answer. Can the user see the reference? Can the user decline the suggested action? Is a human expert available for the riskier step? Can the user revoke the connection? Does the record show that an external AI surface was involved? Does the data remain governed by the same privacy choices? Can the output be reproduced or explained later? If those questions cannot be answered, the convenience layer has outrun the control layer.

Mailchimp and Credit Karma extend the financial graph

Mailchimp can look like a separate marketing product, but inside Intuit it matters because small-business finance does not end at the ledger. A business wants customers, revenue, payment, cash-flow visibility and repeat purchases. Intuit's acquisition logic was that marketing, customer engagement, payments and accounting could reinforce each other. Mailchimp's public developer API exposes campaign creation, campaign updates, send, schedule, cancellation, classic automation, connected-site and send-checklist surfaces.

Its report endpoints are read-only and cover clicks, opens, subscriber activity, e-commerce data and related campaign analytics. In 2026, Intuit announced Mailchimp Analytics AI and expanded data integrations, saying new AI-powered capabilities automate analysis, deliver conversational insights and support more compliance options for regulated industries.

The accepted output here is not a generated email subject line. It is a campaign action that uses the right audience, consent state, timing, channel, product context and performance evidence. AI can reduce creative and analytical effort, but the risk is not only poor copy. It is using stale or wrongly synced customer data, sending to the wrong segment, over-attributing revenue, ignoring compliance constraints, or optimizing for short-term campaign metrics while damaging trust. If Mailchimp pulls from commerce, accounting or customer history, the marketing action inherits the provenance questions of the financial record.

Mailchimp also provides a cautionary identity and support-control example. In January 2023, Mailchimp disclosed that an unauthorized actor accessed a tool used by customer-facing teams for support and account administration after a social-engineering attack on employees and contractors, and that 133 accounts were affected based on its investigation. Mailchimp stated there was no evidence that the compromise affected Intuit systems or customer data beyond those accounts. The incident is not evidence of a current problem.

It is evidence that customer-support and account-administration tooling is part of the risk surface when a platform handles customer lists and campaign data.

Credit Karma extends the graph in a different direction. Intuit's external AI availability posts describe credit coaching, financial-product shopping, credit-health explanations and cash-flow analysis. That can be useful because consumers often make credit decisions with partial information. But the accepted output is not a friendly explanation of credit factors. It is a recommendation or next step that the user understands as a financial product decision with eligibility, incentives and alternatives.

If an AI surface nudges a consumer toward a credit card, loan or insurance offer, the system needs to separate personalized guidance from monetized marketplace placement. A clear answer still needs caveats.

This is where Intuit's platform breadth is both powerful and uncomfortable. A company that knows bookkeeping, tax, credit, cash flow, payments and marketing can give unusually contextual advice. It can also become the place where many commercial incentives meet the user's sensitive data. The privacy statement matters because it describes platform-level use of personal information across QuickBooks, Mailchimp, TurboTax and Credit Karma, including AI and automated processing, partner sharing, affiliate sharing and choices. A buyer or consumer should not evaluate AI usefulness separately from those data flows.

Personalization is the product, but data-boundary confidence is part of the price.

Auditability is the real AI feature

In regulated or quasi-regulated work, the most important AI feature may be boring: auditability. A business owner needs to know what evidence supported a category or recommendation. An accountant needs to know whether a transaction was changed by a user, an app, an import, an automation or an AI-assisted suggestion. A taxpayer needs to know which document or answer triggered a filing path. A developer needs to know whether a webhook, CDC catch-up or stale entity caused an integration gap. A marketer needs to know which audience, report or consent state informed a campaign.

Auditability is not the same as logging everything. It is the ability to reconstruct the decision at the level the user needs. For a small business, that may mean a receipt attached to an expense, a transaction rule, an accountant note and a record of who approved the category. For a tax return, it may mean the source document, taxpayer answer, tax form, expert review and guarantee boundary. For a developer, it may mean an OAuth scope, API request, response, syncToken and webhook signature. For an AI assistant, it may mean the source data used, model surface, user consent, human review state and final action.

Intuit's public materials contain pieces of this puzzle but not a complete independent audit story. The developer docs show permission and synchronization mechanics. TurboTax pages show expert support, review and guarantee structures. Privacy materials describe choices, automated processing, partner sharing and security safeguards. Responsible-AI governance materials say Intuit is aligning with the NIST AI Risk Management Framework and designing governance to prevent harm. Those are necessary ingredients. They are not enough to prove that a customer can always reconstruct an AI-assisted financial step.

The buyer's test should therefore be operational. Pick a workflow such as invoice collection, expense categorization, tax checklist creation, sales-tax app integration or campaign targeting. For each accepted step, require a reference, rule or recommendation basis, permission evidence, reviewer or approver state, correction path, downstream effect and retention policy.

Then inject ordinary failure: a changed bank transaction, a duplicate invoice number, an inactive customer, a missing receipt, a revoked app permission, a disconnected account, a tax situation that exits free eligibility, a campaign audience that should be excluded, and a user who changes their mind.

If the system makes those exceptions visible and recoverable, AI can lower cost. If the system produces clean language while exceptions become support tickets, the apparent automation is a debt. The distinction will be hard to see in a demo because demos rarely include reversal, amendment, stale data, support escalation or regulator-facing explanation. Those are exactly the moments where financial workflow software earns trust.

What Intuit can replace, and what it cannot

The alternative to Intuit's AI-enabled platform is not one thing. For bookkeeping, the alternatives include manual spreadsheets, accountants using other accounting packages, bank portals, point solutions for receipts or expenses, open-source tools, in-house integrations, rival accounting platforms and doing less frequent financial review. For tax, alternatives include IRS Free File for eligible taxpayers, Free File Fillable Forms, other commercial tax software, a CPA, an enrolled tax professional, a storefront preparer, or not optimizing beyond basic compliance.

For marketing, alternatives include standalone email platforms, customer-data platforms, agency work, manual segmentation and less frequent campaigns. For credit guidance, alternatives include credit bureaus, bank apps, marketplace comparison sites and financial advisors.

Intuit's strongest case is the integrated workflow. A business owner who already uses QuickBooks for invoices, payments and payroll may prefer AI suggestions and expert help inside the same system rather than moving data between tools. A taxpayer who already used TurboTax last year may value prior-year context and document reuse. A marketer who already has Mailchimp audiences may prefer AI campaign strategy tied to existing campaign history. A consumer who uses Credit Karma may value personalized explanations rather than generic credit advice. Integration can reduce switching, re-entry and reconciliation work.

The commercial question is whether those savings exceed the new costs. Subscriptions and filing fees are visible. Expert help, payroll, payments, capital products, app subscriptions, API access, implementation, accountant review, tax support, campaign planning, data cleanup, privacy review and migration are less visible. So is the cost of correcting a wrong accepted step. A business may think it saved time on categorization until an accountant spends hours fixing the chart of accounts. A taxpayer may think AI answered a question until an expert discovers the wrong form path.

A marketer may think campaign creation got faster until deliverability, consent or attribution problems appear.

Lock-in is also a real denominator. Financial records accumulate. Prior-year returns matter. Payroll history matters. Customer lists matter. Campaign history matters. App integrations matter. The more Intuit turns these records into an AI-personalized platform, the more valuable the integrated context becomes and the harder it may be to leave. That is not automatically bad. Deep systems of record create switching costs because they hold useful state. But buyers should price that state honestly. Export, migration, accountant access, customer-list portability, API terms, data deletion and retention policies are not afterthoughts.

They determine whether the customer controls the record or merely rents the workflow.

The best alternative may sometimes be doing less automation. A tiny business with a simple ledger may not need a complex AI assistant if a monthly accountant review is cheaper and safer. A taxpayer with a simple return may use a free filing route. A business with a regulated marketing audience may prefer human-controlled campaigns until consent and audit state are mature. Intuit's platform is most compelling where the same records support repeated decisions across accounting, tax, payments, payroll, credit, cash flow and customer growth.

It is less compelling when the workflow is rare, high-risk, poorly structured or cheaper to handle manually.

The measurement framework

The right metric is cost per accepted financial step. It is specific enough to be useful and broad enough to compare across QuickBooks, TurboTax, Credit Karma and Mailchimp.

An accepted QuickBooks step might be a categorized transaction, matched receipt, reconciled payment, sent invoice reminder, payroll action or closed monthly report. An accepted TurboTax step might be a completed checklist item, verified document upload, product-eligibility decision, expert-reviewed answer, filed return or amendment. An accepted Credit Karma step might be a credit-improvement action the user understands and chooses, not merely an offer impression. An accepted Mailchimp step might be a campaign or segment that passes consent, content, audience and performance review.

For each step, the buyer should track five gates.

First is source provenance. What records, documents, transactions, forms, accounts, audience fields or reports supported the output? Were they current? Were they complete? Did the user know what was missing?

Second is permission and consent. Who or what had access to the data? Did the user approve the connection? Did the external AI surface see anything it should not? Could the user revoke access? Were accountant, employee, expert, developer and partner roles separated?

Third is rule currency. Which accounting, tax, sales-tax, payroll, credit or marketing rule was applied? Was the rule current for the date, jurisdiction, product tier and customer situation? What happened when the situation moved outside the supported path?

Fourth is review and accountability. Did a human accept the step? Was it a business owner, accountant, tax expert, product specialist, marketer or developer? Was the review optional or required? Was the guarantee, support or liability boundary visible?

Fifth is recovery. Can the step be corrected, reversed, amended, resynced or explained later? Does the correction update downstream reports, filings, invoices, campaigns or recommendations? Does support have the evidence needed to help?

This framework avoids two weak conclusions. The first weak conclusion is that Intuit's AI must be highly valuable because Intuit has scale, data and model partnerships. The second is that AI in finance is unsafe because mistakes are possible. The useful question is narrower: where does Intuit reduce the total work required to produce accepted financial steps, and where does it merely shift review burden to the customer?

What would prove the platform is working

The strongest evidence would not be a benchmark. It would be repeated deployed evidence with a denominator. For QuickBooks, that could be a controlled cohort showing that AI-assisted categorization, reconciliation and invoice collection reduced accountant correction time without increasing stale-entity, duplicate-document, tax or support issues. For TurboTax, it could be evidence that AI checklists and expert handoff reduced abandoned filings, wrong product paths and amendment rates for specific tax situations, while keeping eligibility language clear.

For Mailchimp, it could be evidence that AI campaign generation improved accepted campaign throughput without increasing compliance, audience or attribution exceptions. For Credit Karma, it could be evidence that AI-guided actions improved user financial outcomes without oversteering users toward unsuitable offers.

Public evidence does not yet provide that level of denominator. Intuit reports strong revenue growth and product adoption signals. It reports AI automation launches and partnerships. It provides developer documentation and governance claims. It provides product pages that describe support, expert review, guarantees and limitations. Those sources are enough to define the stakes and the architecture of the problem. They are not enough to say that Intuit has removed the correction burden for a particular customer segment.

That uncertainty is normal for an AI workflow transition. The first wave of evidence is usually capability and distribution. The second wave is customer adoption. The third, harder wave is accepted-output economics after exceptions. Intuit is in the second wave publicly. It is telling investors and customers that AI automation, human experts and domain data can make financial intelligence more useful. The next proof point is whether support, correction and audit costs fall for the people who actually have to close books, file returns and explain actions.

There are watchpoints. The first is tax eligibility clarity. TurboTax's AI and expert workflows should make eligibility and support boundaries clearer, not smoother. The second is accountant control. QuickBooks AI automation should assist accountants and owners without creating hidden actions that professionals must later unwind. The third is external-AI data boundary. OpenAI and Anthropic experiences should make source, consent and action state visible. The fourth is developer reliability. API, webhook, CDC and app-publishing controls should remain robust as more AI-powered apps touch accounting data. The fifth is commercial incentives.

Credit, capital, payments and marketing recommendations should separate user benefit from marketplace economics.

The sixth is organizational capacity. In May 2026, Intuit said it was reducing its full-time workforce by 17% to simplify the organization and move faster, while estimating $300 million to $340 million in restructuring charges. That may fit the company's efficiency strategy, but it also makes support, expert availability, product quality and governance execution worth watching. AI can reduce some human work. It can also increase the importance of the humans who remain in review, support, tax, security, product and compliance roles.

The verdict

Intuit has a stronger AI workflow position than most software vendors because it already owns high-frequency financial surfaces. QuickBooks, TurboTax, Credit Karma and Mailchimp are not generic productivity apps. They are places where users make decisions about money, tax, credit, customers and compliance. That makes the company's AI automation strategy plausible. It also makes it harder.

The platform should not be judged by assistant fluency. It should be judged by accepted financial decisions that stay sourced, permissioned, current and recoverable. QuickBooks must preserve data provenance and accountant control. TurboTax must preserve rule currency, product eligibility and expert escalation. Credit Karma must preserve user understanding and incentive transparency. Mailchimp must preserve audience consent, campaign evidence and data security. OpenAI and Anthropic integrations must preserve Intuit's data boundaries and make the action path clear.

If Intuit succeeds, the reward is not merely faster answers. It is lower financial-operation friction for people who cannot afford a large finance department, tax department, data team or marketing operations group. A small business owner could get cleaner books, earlier cash-flow warnings, fewer invoice delays and better campaign decisions. A taxpayer could gather documents faster and know earlier when expert help is needed. An accountant could spend less time reconstructing messy records and more time advising. Those are real gains.

If Intuit fails, the failure will not always look like a dramatic hallucination. It will look like quiet correction work: a wrong category discovered at month end, an eligibility surprise late in filing, a stale sync that changes a report, a support ticket that cannot reconstruct the AI step, a campaign built from the wrong audience, or a user who accepted a financial recommendation without understanding the caveat. In finance, quiet correction work is the cost that matters.

The practical buying rule is therefore conservative. Count only accepted steps. Price the review. Test the reversal. Keep the source visible. Require the permission story. Ask what happens when the AI is uncertain, when data is stale, when rules change, when a user revokes consent, when a third-party app breaks and when the customer needs a human. Intuit's platform has the ingredients to automate important financial work. Whether that work is truly removed depends on what happens after the answer sounds right.