Summary

- Intellicom Ireland Ltd can earn a premium where the buyer is not just buying minutes, broadband or software seats, but a low-drama migration from legacy telephony into hosted voice, unified communications, contact-centre and managed connectivity operations.

- The ceiling is set by DigitalWell group integration, supplier dependence, public-tender discipline and substitute platforms such as Microsoft Teams Phone, Zoom Phone, Amazon Connect, Genesys Cloud CX and larger Irish carriers.

The premium starts with service continuity, not bandwidth

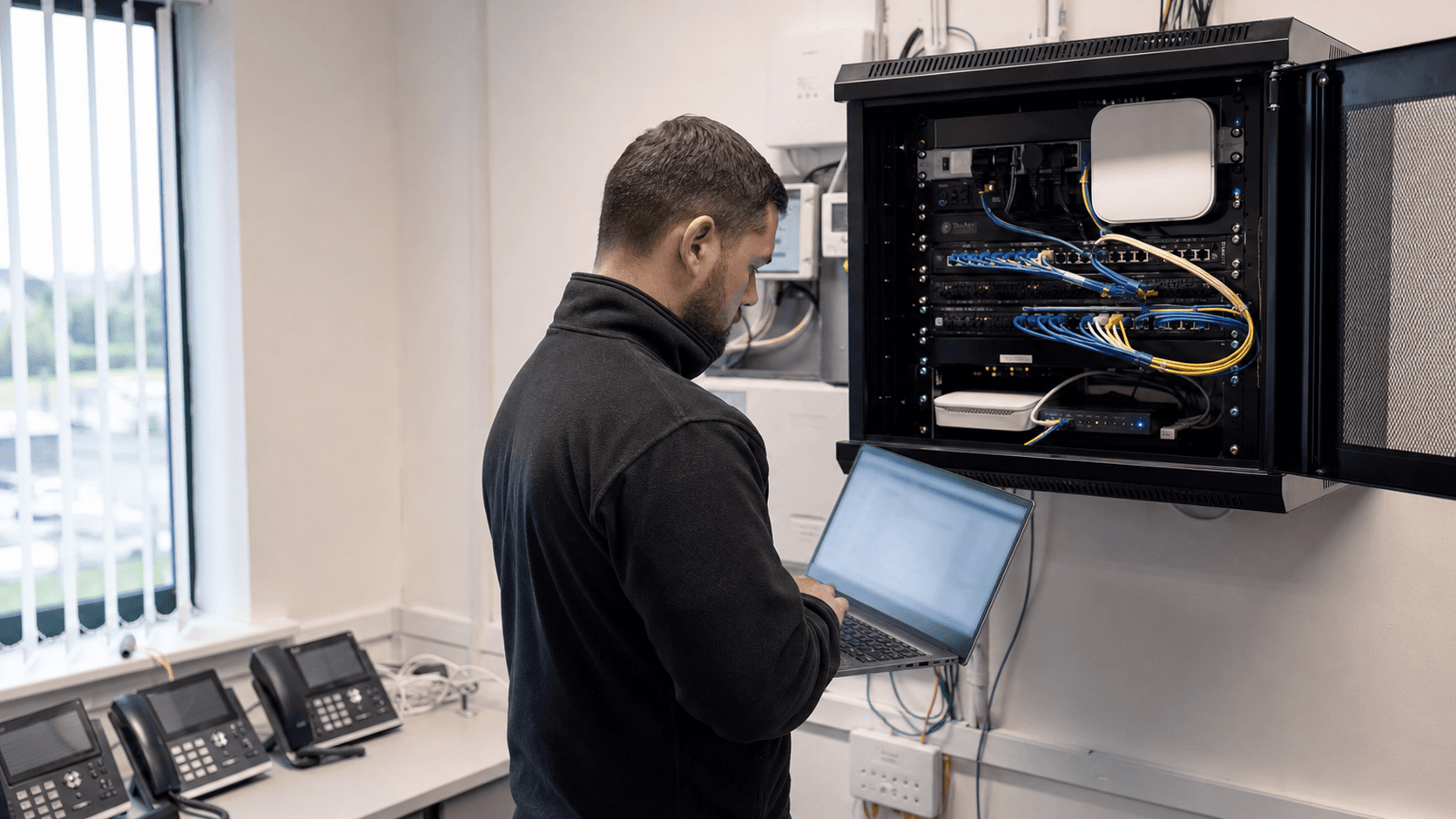

The economic question around Intellicom Ireland Ltd is not whether it owns enough network infrastructure to dictate Irish broadband prices. The public evidence does not support that kind of story. The narrower and more useful question is whether Intellicom can charge more than a commodity reseller for solving a customer problem that is expensive to get wrong: moving business voice, contact-centre and site connectivity from ageing telephone estates into a managed, supportable, cloud-linked operating model.

That problem is valuable because the buyer does not experience it as a neat software purchase. A multi-site council, museum, retailer, healthcare provider or contact-centre operator has telephone numbers that must port correctly, reception desks that must keep answering, call queues that must route to the right teams, supervisors who need reporting, legacy handsets and analogue endpoints that may still matter, security and recording obligations, and users who blame the supplier when a call fails. The substitute price for a basic voice seat may be visible online, but the cost of a failed migration is private, immediate and reputational.

Intellicom's pricing power therefore begins with continuity. If the customer believes the supplier knows how Irish numbering, local access, SIP trunks, contact-centre routing, customer-service workflows and physical site constraints fit together, the cheapest advertised cloud seat is not the whole benchmark. A buyer may pay more for a supplier that can audit the current estate, stage the cutover, provide local support and carry responsibility across carrier, software and site boundaries.

That is a meaningful but bounded premium. It does not protect every euro of revenue. Commodity broadband, mobile, cloud licenses and contact-centre platforms are contestable. A procurement team can compare large carriers, managed service providers and global SaaS vendors. A customer with strong internal communications engineering can buy directly from Microsoft, AWS, Zoom or Genesys and manage local carrier pieces itself. Intellicom's strongest position is where the buyer has enough operational complexity to need help but not enough internal telecom depth to run the migration and support model as a do-it-yourself project.

The evidence also points to a premium that has to be renewed, not merely won. Public-sector and enterprise customers can tolerate high switching cost for a period, but they eventually retender, benchmark or consolidate. Intellicom's value survives renewal only if service records show fewer outages, faster changes, cleaner reporting, better call quality and lower total operating friction than the buyer could get from a larger carrier or a platform-direct route. The economic incentive is not growth for its own sake. It is the conversion of local implementation risk into recurring managed-service margin.

The operating boundary is an acquired voice and communications specialist

Intellicom Ireland Ltd is an Irish company rather than a vague trading label. Public company information identifies Intellicom Ireland Limited with company number 404152, a 2005 formation date, normal status and a telecommunications principal activity. RIPE's database connects the same registration number to Intellicom Ireland Ltd as an Irish Local Internet Registry. The legal identity matters because the article is about the company that holds number-resource records and public procurement traces, not an unrelated American technology business with a similar name.

The commercial boundary is more complicated. Intellicom was acquired by Welltel in 2020, before Welltel later traded as DigitalWell. DigitalWell's acquisition announcement described Intellicom as a provider of cloud and on-premises telephone, contact-centre, unified communications and connectivity solutions, sold both directly and through channel partners. It also said Intellicom had a team of about 20 and worked across customer service, telecommunications, retail, government, finance and health.

Duke Capital's 2021 annual report, discussing financing connected to Welltel's acquisitions, described Intellicom as a supplier, installer and supporter of IP telephony solutions to more than 350 corporate clients across Ireland.

Those details are more economically revealing than the sector label. Intellicom's heritage appears to be in business communications engineering and support, not in mass-market retail broadband. The acquisition logic was to add cloud unified communications and contact-centre capability to a broader managed communications platform. DigitalWell's current public materials emphasise end-to-end ownership across connectivity, voice infrastructure, contact-centre platforms and automation.

That framing suggests Intellicom's assets and skills are now part of a wider stack, where the customer buys accountability across several layers rather than a single product SKU.

For pricing power, group ownership cuts both ways. It can strengthen the offer because Intellicom can sit inside a larger organisation with more support coverage, broader products, more vendor relationships and more balance-sheet credibility. DigitalWell says it serves enterprise clients, SMEs and public-sector organisations, operates across many countries and offers 24/7 support coverage, guaranteed uptime and certification claims. A buyer with mission-critical communications may see that as lower execution risk than dealing with a small standalone installer.

But the same integration blurs Intellicom's standalone economics. The company may retain legal, resource or legacy customer significance while commercial delivery, support and product strategy are increasingly DigitalWell-led. The premium may accrue at group level rather than inside Intellicom as a separate profit centre. When assessing Intellicom, the safer conclusion is that it is a valuable local communications operating surface within DigitalWell, not an independent national carrier whose pricing power can be read from its own brand visibility alone.

Network-resource records show control points, not a standalone national carrier

The strongest hard infrastructure evidence is in RIPE records. RIPE lists Intellicom Ireland Ltd among Local Internet Registries offering services in Ireland. The member detail page gives a Dublin address at Two Haddington Buildings, Haddington Road, D04 HE94, an Irish service area, a phone number and a contact email at DigitalWell's domain. The RIPE database entity for ORG-IIL24-RIPE names Intellicom Ireland Ltd, country IE, registration number 404152, organisation type LIR, and maintainers including an Intellicom maintainer and RIPE NCC.

The resource record then becomes more specific. RIPE's inverse organisation lookup shows a provider-aggregatable IPv4 allocation, 185.144.124.0 to 185.144.127.255, netnamed IE-INTELLICOM-20160323, with allocated PA status. A maintainer lookup also shows a smaller assigned PA record for 185.144.124.0 to 185.144.125.255 with the netname INFRA_CORK, maintained by both WellTel-NOC and Intellicom's maintainer. RIPEstat's prefix overview reports 185.144.124.0/22 as announced, with AS16171 as the origin and STRENCOM Fulnett Limited as the holder.

This is important evidence, but it has to be interpreted correctly. It supports a number-resource and operational network footprint. It does not by itself prove Intellicom is selling broad consumer access, national fibre, cloud hosting or transit at scale. The origin ASN is associated with Strencom/Fulnett, and DigitalWell separately announced the acquisition of Strencom in 2021 to add secure connectivity, cloud infrastructure, managed hosting and a nationwide network. The picture is therefore one of group-level network consolidation: Intellicom-held address space appears to ride on, or be managed alongside, a Strencom/DigitalWell backbone.

AS16171's RIPE aut-num entity reinforces the group-network context. It describes a Strencom backbone in Cork, includes INEX peering references and lists import-export relationships with Irish and international networks such as BT Ireland, Eircom, Microsoft EU, Amazon, Virgin-related routes and transit providers. RIPEstat's AS16171 data shows multiple announced prefixes, including Intellicom's 185.144.124.0/22. PeeringDB and other BGP visibility tools also associate AS16171 with INEX presence. The economic meaning is resilience and optionality, not unlimited market power.

RIPE membership has modest direct cost compared with enterprise communications revenue. RIPE's 2026 charging scheme lists an annual contribution of EUR 1,800 per LIR account, with additional charges for independent resources and ASN assignments. That fee is not the cost base that determines customer pricing. The more relevant cost base is labour, platform licensing, upstream connectivity, support tooling, procurement compliance and the operational overhead of keeping voice services available.

The product is migration accountability for fragmented estates

Intellicom's public history points to a business model built around communications projects that turn into recurring support. The customer's old state is fragmented: fixed lines, primary-rate interfaces, PBX hardware, voicemail, reception desks, hunt groups, contact-centre queues, call recording, remote staff, branch offices and broadband circuits. The promised new state is simpler: hosted voice, unified communications, SIP, cloud contact centre, reporting, managed connectivity and a support desk that can own the problem when something breaks.

That creates several revenue streams. There is project revenue for audit, design, installation, configuration and migration. There is hardware or equipment margin on phones, session border controllers, routers, switches and site equipment where needed. There is recurring service revenue from support, monitoring, managed connectivity, call charges, hosted voice seats, contact-centre seats, call recording, reporting and change requests. There may also be vendor resale margin where DigitalWell or Intellicom delivers Microsoft, Genesys, Amazon, private-cloud or other communications platforms as part of a managed package.

The pricing mechanism is not pure license arbitrage. In a transparent software market, customers can see that Amazon Connect prices voice by usage, Genesys publishes per-user contact-centre tiers, Zoom markets phone plans and Microsoft documents Teams Phone calling options. Those visible alternatives put pressure on any supplier that tries to mark up commodity seats without adding service value. Intellicom's defensible margin has to come from design, implementation, support and accountability around the service, not from pretending customers cannot find cloud price cards.

The best customer problem is a buyer that has to keep service levels while changing the underlying communications estate. A council replacing a phone system and contact centre does not simply ask, "How much is a seat?" It asks whether its public lines, out-of-hours routing, reception teams, dispersed offices and reporting obligations will work on Monday morning after the cutover. A museum or healthcare provider asks whether calls reach the right location, whether resilience exists for public-facing services and whether support is available when the supplier stack spans carrier, cloud, devices and customer premises.

The channel-partner evidence also matters. DigitalWell's Intellicom announcement said Intellicom sold direct and through channel partners. That can extend reach but dilute pricing control. If a partner owns the customer relationship, Intellicom or the group may be providing platform, installation or specialist support rather than commanding the full gross margin. Conversely, a direct customer with multiple sites and local service needs gives more room for premium pricing because the supplier can bundle discovery, migration, support and future change into one accountable service.

Contract durability comes from operational entanglement

The most durable part of this business is not the contract wording. It is the entanglement that develops once communications workflows are embedded. A business phone or contact-centre implementation touches numbers, call flows, voicemail, reporting, compliance records, integrations, business hours, failover paths, user permissions, device inventories and training. When those pieces are working, the customer is cautious about changing supplier just to shave a small amount off a monthly seat price.

That caution is the source of renewal power. A supplier that has mapped the estate, fixed early problems and become the first call for service changes knows the customer's real topology better than a challenger. The customer may not have up-to-date internal documentation. It may have added exceptions over time. It may have emergency lines, lift phones, alarms or reception workflows that were discovered only during implementation. Even where these edge cases are not the largest revenue items, they make the buyer sensitive to transition risk.

There is also a labour-market dimension. Local support labour is scarce because the work is hybrid. A good communications engineer needs enough carrier knowledge to understand numbers and SIP, enough networking to diagnose packet loss and routing, enough vendor knowledge to configure cloud systems, enough customer-service sense to translate queues and call flows, and enough project discipline to stage a migration without disruption. If Intellicom or DigitalWell can keep experienced people close to the customer, it can charge for reduced anxiety as much as for hardware or licenses.

Durability weakens at renewal when the customer's estate becomes standardised. Once numbers are ported, users are trained, call flows are documented and the platform is stable, the buyer can benchmark more aggressively. If the implementation lands on a common SaaS platform, a different managed service provider may be able to take over support. If the buyer consolidates on Microsoft Teams Phone or a global contact-centre platform, the software vendor's ecosystem makes substitution easier. That is why renewal evidence matters more than first-year project wins.

The best proof of surviving pricing power would be private retention data: gross revenue retention by cohort, renewal uplift after the initial term, support tickets per user, mean time to repair, customer churn after public retenders, service-credit history, number of customers buying more than one service line, and margin by direct versus channel-led accounts. Without those metrics, the public evidence supports a qualitative thesis but not a precise margin number.

Pricing power is strongest where downtime is expensive but procurement capacity is thin

The customer problem that gives Intellicom its best pricing position is a middle zone. At one end, a very small company may accept a low-cost cloud phone plan and basic broadband because the operational risk is tolerable. At the other end, a very large enterprise may have its own network team, procurement experts and global platform relationships. Intellicom's strongest opportunity is between those extremes: organisations large enough to suffer from downtime and complex call routing, but not so large that they can internally own every design, migration and support task.

Irish SMEs, mid-market firms, local public bodies and distributed service organisations fit that pattern. They may have sites outside Dublin, legacy systems inherited from previous suppliers, staff who still rely on desk phones, and customer-facing teams that cannot stop answering. The buyer wants a communications outcome, not an engineering research project. That makes a supplier with local installation experience, Irish numbering familiarity, support labour and group-level connectivity more valuable than a bare license provider.

The public-sector examples illustrate demand shape rather than guaranteed profitability. Procurement aggregators show the National Museum of Ireland awarding a dedicated-business telephone network services contract to Intellicom Ireland Ltd in 2021, with a value shown around EUR 200,000. Separate procurement listings describe a National Museum VoIP telephone system across several museum sites, and a Donegal County Council process for an IP telephony, contact-centre and unified communications replacement. These records indicate that the relevant buying problem was multi-site telephony and service migration.

They also show that public customers formalise competition and can reopen the market at renewal.

Pricing power is weaker where the buyer treats the service as a commodity access line. Ireland's fixed broadband market is moving toward higher-speed fibre availability, and ComReg's Q1 2026 sector report said fixed broadband lines reached about 1.77 million while FTTP lines stood at 1,093,776, or 62 percent of fixed broadband lines. When basic connectivity improves and is available from multiple carriers, the margin on access alone falls. The premium has to move up the stack into resilience design, voice quality, security, reporting and support.

The strongest invoice line is likely a bundle that hides the pure commodity comparison: design plus migration plus managed support plus connectivity plus telephony plus contact-centre functionality. Bundling can be legitimate if it lowers total operating risk. It becomes vulnerable if the buyer cannot see performance improvement or if the supplier uses complexity mainly to stop benchmarking. The private metric that would settle the question is not gross revenue growth. It is the margin and retention of customers buying multiple managed communications services after the first renewal.

Unit economics depend on utilisation of scarce support labour

Intellicom's unit economics are likely labour-led. The public evidence points to a team-based communications integrator rather than a capital-intensive access network owner. In 2020 DigitalWell described Intellicom as having about 20 staff. Duke Capital later described the company as supporting IP telephony solutions to more than 350 corporate clients across Ireland. Even if those figures have changed under DigitalWell, they capture the model: a relatively small specialist team can support many accounts if the platform is standardised, documentation is good and support tickets are controlled.

The attractive version of the model has three layers. First, project work funds the initial discovery and migration. Second, recurring support and platform revenue continue after the cutover. Third, the supplier reuses templates, vendor expertise and network infrastructure across customers, so each new customer does not require a completely new technical design. When that flywheel works, gross margin improves because senior engineers are used on high-value design and escalation while routine tasks are handled by process, tooling and first-line support.

The unattractive version is easy to imagine. Every customer is bespoke. Legacy systems are poorly documented. Cutovers overrun. Engineers spend too much time on low-margin site visits. The support desk absorbs recurring problems caused by underpriced contracts. Vendor costs rise faster than customer prices. Public contracts demand fixed pricing while service volumes change. In that case, the company wins revenue but not value creation. Strategy without disciplined resource allocation becomes sales motion rather than economic advantage.

Capital needs appear moderate but not zero. RIPE membership and address-resource administration are small costs. Customer premises equipment and hosted platform infrastructure require working capital. Secure voice, session border control, monitoring, private cloud, connectivity and data-centre arrangements require ongoing investment either directly or through DigitalWell and Strencom assets. The group also has to maintain certifications, security tooling, support systems and vendor skills. The more the offer promises resilience, uptime and security, the less it can be run as a thin reseller operation.

Private metrics would show whether the labour model scales. The relevant ones are tickets per endpoint, gross margin by customer size, implementation hours versus quoted hours, utilisation of senior engineers, remote-resolution rates, vendor pass-through margin, project backlog, customer support satisfaction, renewal uplift and attach rate for connectivity or security services. If these metrics are strong, Intellicom's premium can survive price pressure. If they are weak, the business may be buying revenue with scarce support labour.

Upstream carriers, platforms and cloud vendors cap the premium

Intellicom's customer promise depends on suppliers it does not fully control. The RIPE and BGP records show number-resource control and group-network routing, but the broader communications stack still relies on carriers, exchange points, transit providers, SaaS platforms, device vendors and cloud services. AS16171's RIPE record lists relationships with Irish networks, international networks and transit providers. That gives operational reach, but it also shows that no small Irish communications provider is economically isolated from upstream bargaining power.

Carrier dependence matters most in access and voice quality. If a customer's sites depend on wholesale broadband, leased lines, mobile backup, SIP trunks or number portability processes, Intellicom can coordinate the service but cannot repeal the physics or commercial terms of upstream networks. A major carrier outage, delayed port, degraded circuit or supplier price increase can land on the customer experience even if the root cause is outside Intellicom's direct control. The company can charge for navigating that complexity, but the complexity also caps margin.

Platform dependence is equally important. DigitalWell's current materials describe customer-experience and workplace communications built around modern contact-centre and cloud communications platforms, including public references to Genesys Cloud CX and Amazon Connect in its broader service set. Microsoft Teams Phone, Zoom Phone, Amazon Connect and Genesys all provide visible alternative paths for customers. Their price cards and ecosystems create a reference point for procurement. If a managed provider charges materially more, it has to prove service value in migration, resilience, integration and support.

Supplier bargaining power can also increase as customers standardise. A buyer that wants a particular platform may treat Intellicom as an implementation and support partner rather than a strategic service owner. That lowers switching cost at the supplier layer, because another certified partner can bid for the same platform. Conversely, when Intellicom or DigitalWell provides an integrated private-cloud communications service, managed connectivity and local support bundle, the supplier has more room to differentiate. The risk is that customers may view private-cloud or bundled architectures as lock-in unless the performance case is clear.

This is where the nearest substitute price becomes a practical discipline. A customer can compare a Microsoft Teams Phone calling plan, Zoom Phone plan, Amazon Connect usage model or Genesys seat tier with a managed-service quote. The comparison will not include all migration labour, support, continuity and integration costs, but it gives procurement a ceiling. Intellicom's premium survives only when it can make the total cost of failure, delay and unmanaged complexity more visible than the headline cost of platform seats.

Public procurement shows demand but also exposes retender risk

Public procurement is useful because it reveals the kind of work buyers think they are buying. The National Museum record describes a VoIP-based phone system across museum sites, replacing an end-of-life estate. The listed sites include public-facing and operational locations, making continuity and support more important than a simple desk-phone swap. A third-party tender tracker reports an award to Intellicom Ireland Ltd for dedicated-business telephone network services with a value around EUR 200,000 and an estimated renewal window several years later.

That is exactly the kind of customer problem where migration accountability can earn a premium.

The Donegal County Council listing is also instructive even without treating it as an Intellicom win. It describes a buyer seeking to replace existing telephony infrastructure, contact-centre capability and unified communications. The buyer wanted design, supply, installation and implementation for a diverse and dispersed organisation. That language maps directly onto the economics of the category: the buyer is purchasing reduced execution risk across sites, users and public-service workflows.

But procurement is a double-edged signal. It validates demand and creates referenceability, yet it forces price comparison. Public buyers can specify service requirements, demand support obligations, evaluate multiple suppliers and retender after the contract period. They may also award frameworks where the supplier has to compete for drawdowns or where pricing is capped. For Intellicom, public-sector work is valuable if it creates sticky support relationships and multi-year recurring revenue. It is less attractive if it produces one-off implementation pressure with thin recurring margin.

Unofficial market signals should be handled carefully. Virgin Media Business's number-transfer page lists Intellicom Ireland Ltd among selectable providers for porting, which suggests the name remains visible in Irish business voice operations. Open procurement aggregators and tender trackers show Intellicom in telephony-related public-sector contexts. Peering and BGP tools show Intellicom address space under the Strencom/DigitalWell routing environment. These are useful signals, not audited proof of current revenue, market share or customer satisfaction.

The fact pattern supports a measured conclusion. Intellicom has enough public trace to be more than a shell identity. It has company registration, RIPE LIR status, address space, acquisition history, procurement signals and group-platform context. But public evidence does not show a standalone revenue line, current customer count, market share, churn, gross margin or capital expenditure. The pricing-power thesis must therefore stay grounded in the customer problem and avoid overstating financial certainty.

The Irish market is making connectivity easier to substitute

The wider Irish market is not moving in a way that lets small providers charge freely for basic connectivity. ComReg's most recent sector data before this article shows fixed broadband continuing to grow, with FTTP becoming the majority of fixed broadband lines in Q1 2026. Its Q3 2025 fixed voice report showed about 1.01 million fixed voice subscriber lines, down 9 percent year on year, with Eir still the largest fixed-voice provider and other named operators sharing the market.

The long-run direction is clear: legacy fixed voice is shrinking, high-speed broadband availability is rising and customers have more routes to cloud communications.

That direction creates demand and pressure at the same time. It creates demand because businesses need to leave older voice infrastructure behind. ComReg's legacy migration material records Eircom's intention to move copper-based services toward fibre and ultimately switch off copper access. Businesses that still depend on traditional lines need advice, migration planning and resilience design. Intellicom's category benefits from that transition because buyers want help crossing the old-to-new boundary.

It creates pressure because once the new broadband and cloud layer is in place, the service can become easier to substitute. Fibre availability, National Broadband Ireland's rollout and carrier competition reduce dependence on a single local access provider. Cloud communications platforms reduce dependence on a proprietary PBX. Procurement can compare managed providers against direct SaaS, large carriers and specialist contact-centre implementers. The customer's question shifts from "Who can make this work?" to "Who can keep this working at the best total cost?"

DigitalWell's broader strategy appears designed to respond to that pressure by owning more of the communications outcome. Its public materials speak about end-to-end ownership across connectivity, voice infrastructure, contact-centre platforms and automation. Its Strencom acquisition added secure connectivity, cloud infrastructure and managed hosting. Its ANS acquisition added managed cloud, security and IT services. In that context, Intellicom's voice and contact-centre heritage is one component of a larger attempt to bundle business communications, cloud, security and customer experience.

The bundle is economically sensible if customers value one accountable partner. It is vulnerable if customers unbundle the stack at renewal. A CFO may ask why the organisation needs a managed voice specialist if Microsoft, Zoom, AWS or Genesys can provide the platform and a large carrier can provide access. Intellicom's answer must be empirical: faster cutovers, fewer incidents, better call quality, better reporting, stronger continuity plans, less internal labour and lower total operating risk.

Customer concentration and integration risk are the hidden swing factors

The biggest unknown is customer concentration. Public materials mention more than 350 corporate clients at one historical point, and DigitalWell's acquisition announcement cited Intellicom customers including 11890, Capita, Iconic Offices and Merrion Vaults group. That suggests some breadth, but it does not tell us current revenue concentration, contract sizes or dependency on a handful of public-sector or enterprise accounts. In a support-led business, the difference between many small recurring accounts and a few demanding large customers is decisive.

If Intellicom's customers are diversified and buy recurring support, connectivity and communications services, pricing power improves. The company can spread support labour, standardise implementations and tolerate the occasional lost account. If revenue depends on a few contracts with heavy service obligations, the buyer has more bargaining power at renewal. A large customer can demand price concessions, threaten retendering or force bespoke support that consumes senior engineers. Concentration would also magnify operational incidents.

Integration risk is the second swing factor. Being part of DigitalWell gives Intellicom access to a wider platform and stronger sales proposition, but acquisitions can create operational complexity. Customers inherited from Intellicom, Welltel, Strencom, ANS, Capstone and other acquired businesses may sit on different systems, contracts, vendors and support practices. The economic prize is cross-selling and standardisation. The economic risk is a patchwork that raises support cost and confuses accountability.

DigitalWell's public "about us" materials present growth through acquisitions and international reach as strengths. That can be true, but value creation depends on integration discipline. If the group can migrate customers onto common support processes and communications platforms while preserving local service quality, Intellicom's legacy customer base becomes more profitable. If not, the group may face the classic buy-and-build problem: revenue grows faster than operational coherence.

Operational risk also includes security and resilience. Business voice and contact-centre systems are exposed to toll fraud, account compromise, denial-of-service risk, recording obligations and customer-data sensitivity. DigitalWell's public security-oriented voice materials show the group understands that risk as a product opportunity. The same risk can become a liability if service design fails. Pricing power in critical communications requires trust; trust can evaporate quickly after outages, security incidents or repeated support failures.

Geopolitical risk is limited compared with cross-border backbone or defence infrastructure, but supplier exposure still matters. Cloud and communications vendors can change prices, data-residency terms, product roadmaps and support conditions. International platforms can move faster than local integrators. Regulatory changes around numbering, consumer rights, open internet, cybersecurity and copper migration can alter operating requirements. For Intellicom, the practical risk is less about sanctions or geopolitics and more about being squeezed between powerful global platforms and demanding local customers.

What would change the judgment

The current judgment is that Intellicom Ireland Ltd has focused pricing power in Irish business communications migration and managed continuity, but not broad pricing power over connectivity. The facts support a specialist with local trust, public-sector relevance, RIPE resource control and DigitalWell group infrastructure. They do not support treating the company as a standalone carrier with defensible monopoly economics.

Several facts would make the thesis stronger. First, evidence of high gross revenue retention after the first renewal would show that customers keep paying after the migration risk has passed. Second, net revenue expansion from existing accounts would show that Intellicom or DigitalWell can cross-sell connectivity, security, contact centre and cloud communications rather than merely defend old voice contracts. Third, low support incidents per endpoint and fast repair times would prove that the premium buys reliability. Fourth, strong direct-customer margins would show that channel partners are not capturing most of the economics.

Evidence of independent network advantage would also matter. If Intellicom-held resources were paired with more directly controlled routing, larger address holdings, distinctive SIP infrastructure, private-cloud communications capacity or measurable service-quality advantages, the infrastructure part of the thesis would rise. Today, the public records show useful control points inside a group network, not a proprietary national moat.

Several facts would weaken the thesis. Falling retention after contracts expire would imply that the premium is mostly implementation timing, not durable value. Heavy reliance on a few public-sector or enterprise contracts would increase buyer bargaining power. Rising vendor pass-through costs without matching customer price increases would squeeze margin. A shift by customers toward platform-direct Microsoft, Zoom, AWS or Genesys models would reduce the managed-provider premium unless Intellicom remains the preferred implementation partner. Poor documentation or acquisition integration problems would turn support labour into a cost trap.

The final test is renewal behaviour. If customers renew because Intellicom reduces communications risk, the business has value creation. If they renew only because switching is painful, the premium is weaker and more exposed to a disciplined procurement event. For now, the evidence says the premium reaches as far as local service continuity, migration accountability and managed operational knowledge. It does not reach far enough to escape carrier substitutes, cloud platforms or procurement benchmarking.