Summary

- GREGAL INGENIERIA S.L.'s best-supported source of pricing power is not commodity bandwidth. It is the practical ability to reduce friction in telecom infrastructure work: site acquisition, contract renegotiation, camouflage, execution, maintenance, compliance support and local technical response around Valencia and Spain.

- The same evidence also shows the cap. Spain's fibre market is large, fast and aggressively priced; national operators and low-cost challengers can make legacy wireless access look expensive unless Gregal is serving locations, businesses or infrastructure projects where ordinary procurement cannot solve the whole problem.

The premium begins with deployment friction, not raw bandwidth

The public evidence points to a narrow but economically intelligible form of pricing power at GREGAL INGENIERIA S.L. Customers are unlikely to pay a durable premium because the company can offer more raw internet speed than national operators. On the contrary, the Gregal Telecom tariff page still presents fixed-wireless packages at 4, 6 and 8 Mbps download speeds, with upload rates below 2 Mbps, while large Spanish operators advertise hundreds of megabits or gigabit-class fibre in many places. If the purchase decision is only price per megabit, the company has little room to command a premium.

The more plausible premium is attached to a different customer problem: getting telecom infrastructure deployed, accepted, maintained and kept useful in circumstances where a standard national retail offer does not complete the job. Gregal's own corporate site describes a business founded in Valencia in 2004 to provide independent engineering services for telecom service infrastructure. Its service pages emphasise acquisitions, engineering, execution, maintenance, start-up work and camouflage of telecom infrastructure. That is a different economic surface from a pure retail ISP.

It sits closer to the messy middle of telecom deployment, where property access, structural constraints, municipal concerns, visual impact, construction sequencing, safety and ongoing maintenance can determine whether a site works at all.

This matters for pricing. A commodity broadband customer compares monthly tariffs. A carrier, landlord, enterprise or local project owner compares the cost of a specialist against the value of avoiding failed site negotiations, construction rework, neighbour objections, site downtime, or a delayed coverage plan. In those cases the reference price is not just the cheapest fibre line; it is the expected cost of delay and operational failure.

A local supplier that understands the site, can speak to owners and public bodies, can design a lower-visibility installation, and can maintain the structure may charge more than a generic contractor because the avoided failure is worth more than the service line item.

That is the core economic reading of Gregal: pricing power exists where it sells project certainty and local continuity, not where it sells interchangeable connectivity. The public record gives enough evidence to treat this as a credible thesis, but not enough to treat it as proven margin strength. The difference between the two is important. The company does not publish audited segment revenue, customer concentration, churn, gross margin, service-level results or active subscriber counts. Without those figures, the analysis has to distinguish what is visible from what would still need to be verified privately.

The visible picture is a small Spanish telecom-infrastructure specialist with an access-service brand, a RIPE membership entry, an IPv4 allocation routed through a major upstream network, and public-facing claims about work for major telecom names. The pricing question is therefore not whether Gregal can outscale Movistar, Orange, Vodafone, MASORANGE, DIGI or other fibre challengers. It cannot be assumed to do that. The question is whether its local engineering capability makes it costly enough to replace in the specific situations it serves. On that narrower question, the evidence is more favourable.

The company boundary is an engineering shop with a small access-service surface

The legal and public identity of the business is anchored in Spain under the name GREGAL INGENIERIA S.L. Gregal Telecom's legal notice identifies GREGAL INGENIERIA, S.L. as the responsible company, with Spanish tax number B97514889, a Riba-roja de Turia address in Valencia, telephone contact details and registry information. Commercial registries also point to the same company identity and classify the activity around technical engineering and related advisory work. The public company boundary is therefore not a faceless web brand. It is a Spanish limited company with a long operating history and a stated telecom-engineering purpose.

The company's own history reinforces that boundary. The official site says the firm was founded in Valencia in November 2004 to deliver independent engineering services in telecom service infrastructure. It describes a multidisciplinary company working across phases from concept and design through exploitation and maintenance. The wording is broad, but it is consistent with a supplier that can participate in the life cycle of telecom infrastructure rather than merely resell connectivity.

Gregal Telecom adds a second surface. Its website positions the group as a national telecom operator and advertises wireless internet access, especially through WiMAX-style service, with references to a Valencian network and independence from other operators. The fixed-wireless product pages are commercially important because they show that the company has faced end customers, not only carrier-side project buyers. They also show the limits of that proposition. The tariff structure is clear, but the advertised speeds are modest by current Spanish fibre standards.

That does not make the service irrelevant; it changes the kind of buyer for whom it can be compelling.

The access-service surface is most likely strongest where ordinary fixed broadband options are unavailable, unreliable, delayed, or insufficiently supported. Gregal Telecom's coverage page tells prospective customers to consult availability, which is typical of a local wireless operator whose practical service area depends on radio reach and site conditions. Its business-oriented language about symmetric access for companies and rapid professional response suggests a continuity and support promise rather than a mass-market price war.

For a small business outside reliable fibre coverage, or for a site needing a specific wireless link, the value proposition may be uptime and local responsibility rather than headline speed.

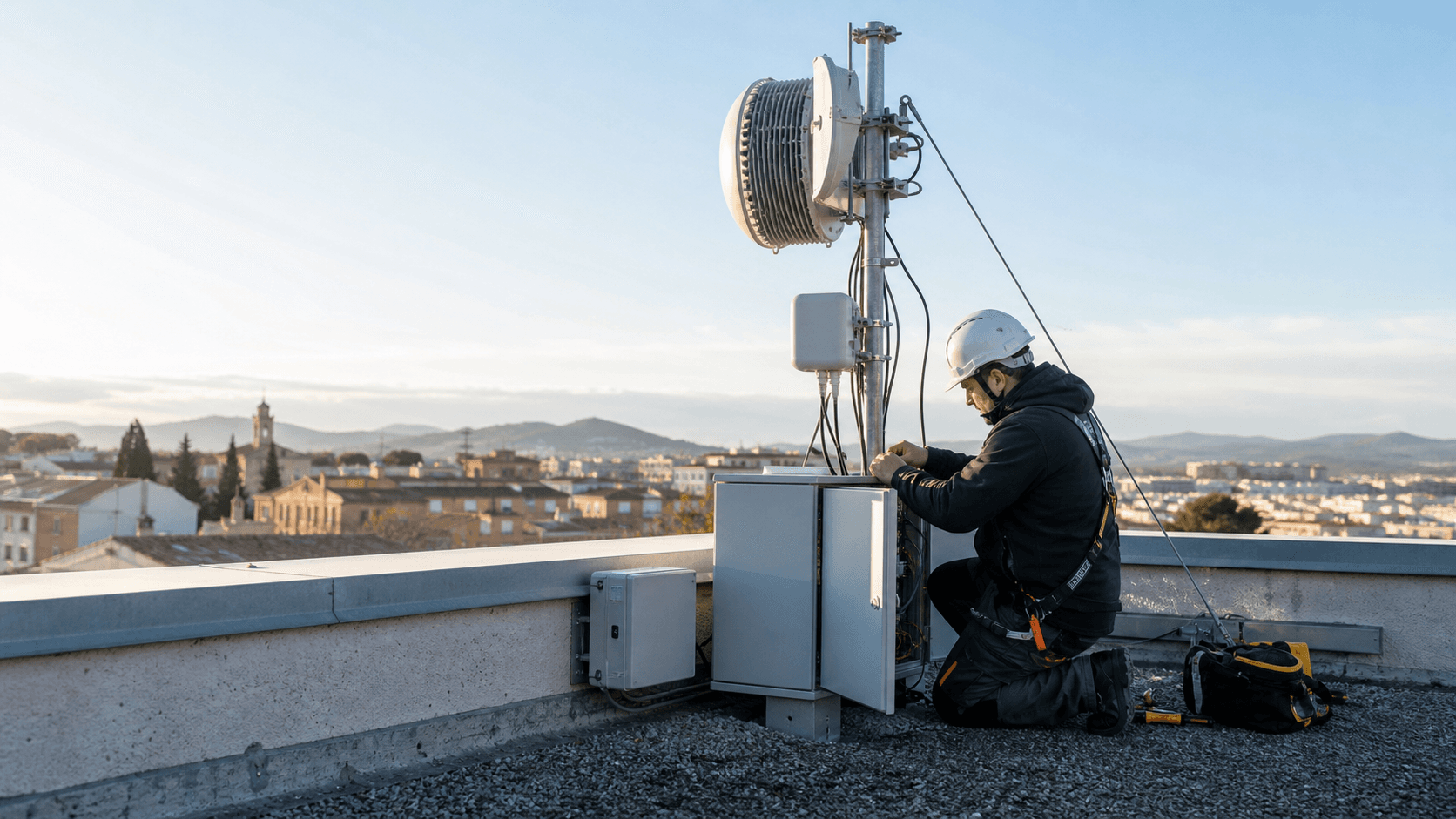

The engineering surface appears more durable than the retail access surface. Gregal's corporate pages cover acquisitions, camouflage, engineering and execution. Its contact-page FAQ describes work on telecom-support structures, including towers and antennas, load and resistance analysis, site evaluation, inspection, maintenance and compliance support. That public description fits the economic profile of a project services company: knowledge-intensive labour, local permitting familiarity, safety responsibilities and site-level execution. Those capabilities can be hard to compare through a simple tariff table.

The company boundary should therefore be read as hybrid, but not evenly weighted. The public evidence favours an engineering and telecom-infrastructure services company with an access service attached to it. That matters because a hybrid company can have more than one margin profile. The broadband offer may be constrained by national retail substitutes, while infrastructure engineering may have better local pricing power if the company is one of a limited number of suppliers trusted to handle complex telecom sites.

The customer pays to keep telecom projects moving

Gregal's strongest customer problem is visible in its acquisitions and camouflage work. The acquisitions page describes prospecting and contracting new infrastructure sites, renegotiating current contracts, modifying existing agreements and representing the client before groups such as neighbours, public bodies, private companies or other required parties. Even without using those words as proof of specific contracts, the service description identifies a real pain point in telecom deployment. Radio and fixed-network infrastructure depend on access to places.

The lease, permit, neighbour acceptance and physical suitability can be as decisive as the radio equipment.

That kind of work creates pricing power differently from a broadband subscription. A carrier or infrastructure owner can buy antennas, routers and civil works from many suppliers, but a failed site negotiation can block a coverage plan. If Gregal can secure a site, renegotiate an agreement, or make a proposed installation acceptable to a building owner or local authority, its value is linked to project completion rather than hours billed. The same logic applies to maintenance or modifications.

A supplier that already knows the site and the stakeholders may be cheaper to retain than to replace, even if another engineering firm offers a lower headline rate.

Camouflage strengthens the same point. Gregal's mimetization page says the company adapts solutions to each project to reduce visual impact, and it presents the GBlock modular camouflage element as a way to form polygonal continuous surfaces, mimic antenna sets without new moulds and simplify transport and rooftop assembly. The economic relevance is not the product description itself; it is the customer problem behind it. Telecom infrastructure often faces visual objections, rooftop access limitations and installation constraints.

A modular system that reduces cranes, adapts to geometry and lowers visual impact can shorten the path from design to acceptance.

The ability to reduce visual conflict can be monetized because visual impact is not a minor aesthetic detail in telecom deployment. Rooftop sites, towers and antennas often face objections from property owners, local communities or municipal processes. If a less visible installation is the difference between consent and rejection, camouflage is not a decorative add-on. It becomes a project-enabling service. That is where pricing power may reach beyond normal contractor margins.

The execution page adds another layer. It indicates that Gregal created an assembly or installations department in 2008 for the execution side of telecom works. A supplier that covers both design and execution can reduce handoff risk. The buyer does not have to coordinate one company for site acquisition, another for engineering, another for installation and another for maintenance. Vertical coordination at small scale can support a premium when the buyer values accountability.

The ceiling is that this power depends on performance and scarcity. If carriers have their own teams, national frame agreements, tower companies or large engineering contractors that can deliver the same acceptance and execution outcomes, Gregal's room narrows. If a project is routine, procurement will compare hourly rates and standard deliverables. The premium is most defensible when the project is local, contested, time-sensitive, visually sensitive, or tied to infrastructure that Gregal already knows.

Network-resource evidence shows presence, not independence

Gregal's public resource evidence supports an operating presence but should not be overstated. RIPE's member listing identifies GREGAL INGENIERIA S.L. in Spain, with a Valencia-area address and contact details. RIPEstat data for 185.247.126.0/24 shows an allocated IPv4 prefix associated with the RIPE organisation record. That is meaningful: it indicates that Gregal is not merely a reseller with no public network-resource footprint.

At the same time, the routing evidence limits the inference. RIPEstat's prefix overview and AS overview show the prefix announced under AS8220, held by COLT Technology Services Group Limited. The routing-status data shows the prefix currently visible through AS8220, while an earlier first-seen route involved AS13287 in 2018. The RPKI validation endpoint reports no validating ROAs for the AS8220 and 185.247.126.0/24 combination at the time checked.

The whois route record also carries a description referring to Pasarela Iluminacion S.L., which should be treated as a caveat rather than folded into the company story as though it were self-explanatory.

In economic terms, the prefix supports "real network entity" but not "independent carrier with deep routing control." If Gregal's traffic is originated through Colt, then Colt is an upstream supplier with bargaining power. Gregal may own or hold address resources and operate customer access, but the public routing record does not show a wide autonomous-system strategy, extensive peering, or multi-homed independence. That matters because pricing power in connectivity is often limited by wholesale inputs.

If the customer premium depends on internet access, and the local operator depends heavily on one upstream path, a share of value can be captured by the upstream provider.

The RIPE resource record also creates a fixed-cost and scarcity context. RIPE's 2026 charging scheme lists an annual contribution per LIR account and fees for independent number resources. RIPE also states that its available IPv4 pool was exhausted in 2019, with only recovered-address waiting-list allocations available under constrained rules. For a small operator, numbering resources are not free administrative trivia. IPv4 scarcity can raise the cost of customer growth, push operators toward carrier-grade NAT, or require purchasing or leasing address space on secondary markets.

It can also make an existing allocation strategically useful.

The lack of a validating ROA is not proof of operational failure, but it is a risk marker. For a company selling connectivity or reliability, routing hygiene matters. Customers rarely ask about RPKI, but resilient routing and clean resource administration are part of the hidden cost of being a provider. If Gregal can show private evidence of updated RPKI, redundant upstreams, monitored route security and service continuity, the network-resource evidence would support a stronger premium.

Without that, the public record supports a more cautious conclusion: Gregal has resource presence, but the customer's premium is more likely tied to local engineering and site continuity than to independent internet backbone economics.

This distinction also protects the analysis from a common error. A RIPE member entry and a /24 allocation should not be converted into a broad claim that the company has carrier-scale bargaining power. The public data says the company has a footprint. It does not say that the footprint gives it the same economics as a national fibre network, a tower company, or a large transit provider.

Pricing power is strongest where delay is more expensive than the quote

The pricing-power question becomes clearer if the buyer is separated into three groups: carriers and infrastructure owners, business customers needing continuity, and residential customers seeking internet access. Gregal's likely pricing power is highest in the first group, situational in the second and weakest in the third.

Carrier and infrastructure buyers can face high delay costs. A site that cannot be contracted, a rooftop that cannot be accepted, a visual-impact objection that stalls a build, or a maintenance issue that leaves equipment unusable can disrupt a larger network plan. In those cases Gregal can sell risk reduction. The buyer is not simply buying a drawing, a bracket, an antenna screen or a technician visit. The buyer is buying a path through a local constraint.

If Gregal has relationships, site knowledge and a history of solving those constraints, procurement may tolerate a higher price because a cheaper supplier can be more expensive in expected outcome terms.

Business customers have a different but related need. Gregal Telecom's advantages page highlights business symmetric access, local response and a Valencian network. A small or medium-sized firm with poor fixed-line alternatives may care more about continuity than about the cheapest advertised bundle. If a local provider can install a wireless link quickly, answer the phone, support a router and keep the connection working, it may retain customers even when nominal bandwidth is lower than a mass-market fibre plan.

That is not universal pricing power; it is conditional pricing power in coverage gaps, temporary sites or business contexts where personal support is valued.

Residential customers face the hardest cap. Gregal's public wireless tariffs give the buyer a price and speed table. National and low-cost operators give the buyer modern fibre and mobile bundles at very aggressive prices. DIGI advertises fibre-plus-mobile combinations with low monthly prices, installation included and short fibre commitment. Movistar advertises symmetric 600 Mbps fibre with installation, a fixed line and no permanence in current promotions. Orange lists 300 Mbps, 600 Mbps and higher packages with mainstream installation and Wi-Fi router propositions.

In that environment, a 4 to 8 Mbps wireless plan cannot claim a general speed or price advantage.

The premium survives only where the substitute fails. That may be a rural or semi-rural property without usable fibre, a business site that needs an interim link before fibre delivery, a location where mobile coverage is limited public evidence, or a customer who values a named local provider over a call-centre relationship. It may also be a customer that needs the same company to understand both infrastructure and access. But if fibre is available and reliable, the customer's next-best price is visible and low. Gregal cannot ignore that anchor.

The official Gregal Telecom tariff page also includes the phrase that any customer need can be negotiated. Economically, negotiation can work both ways. It allows the company to price custom needs where the value is higher than a standard package. It also shows that the standard tariffs are not the whole product. For business access, a negotiated symmetric line may carry a very different margin profile than a residential wireless plan. The missing information is the split between these buyers.

The correct conclusion is therefore narrow. Gregal's pricing power is not a blanket ability to raise broadband prices. It is the ability to charge for solving non-standard telecom problems: acceptance, installation, maintenance, local support and continuity. Where the customer is buying those outcomes, the company may defend price. Where the customer is buying only megabits, the market caps it hard.

Broadband tariffs reveal the cap on consumer-side power

Gregal Telecom's published consumer-style tariffs are valuable because they turn the substitute argument from theory into numbers. The page lists a basic package at 4 Mbps down and 500 Kbps up, a standard package at 6 Mbps down and 1 Mbps up, and a complete package at 8 Mbps down and 1.5 Mbps up. It presents versions with and without fixed telephony, and states that prices are without VAT. A separate contracting page shows a 4 Mbps connection with fixed line priced at EUR 29 before tax and EUR 35.09 with VAT, with installation to be consulted.

Those figures may reflect a legacy or niche access offer, but the competitive implication is still clear. In 2026 Spain, mass-market fibre propositions advertise hundreds of megabits and sometimes gigabit-class speeds at prices that overlap or undercut older wireless products. DIGI promotes fibre-plus-mobile bundles at very low monthly levels, with fibre speeds far above Gregal's public wireless table. Movistar advertises symmetric 600 Mbps fibre in a mainstream package. Orange advertises several fibre tiers and bundled equipment.

Avatel also markets rural connectivity, including fibre and WiMAX-style access, which means even rural fixed-wireless is not a single-provider space.

This does not mean Gregal has no consumer customers. It means the consumer product's economic defence has to be geographic, operational or relational. If the customer has no fibre and weak mobile data, a 4 to 8 Mbps fixed-wireless link can be useful. If the customer needs local installation and support, the provider relationship can matter. If the service is bundled with telephony or a business-specific arrangement, the direct comparison becomes less simple. But the provider cannot rely on the customer being unaware of alternatives. The national price anchor is public and extremely visible.

The no-permanence language on Gregal Telecom's advantages page is also economically double-edged. It lowers customer risk and can help acquisition. It also reduces lock-in. If customers can leave easily, the company has to keep earning the account through service quality, coverage and support. That makes churn, fault response time and complaint handling more important than contract clauses. A no-permanence product can still have practical retention if alternatives are poor, but it does not create contractual pricing power on its own.

The same page claims independence from any operator and a Valencian network. That can support a local identity premium, especially for customers frustrated with national providers. Yet the RIPEstat routing record indicates that at least one public prefix is announced through Colt's AS. That does not invalidate the local-network claim; access networks can be local while upstream internet transit is purchased. It does show that "independence" should be interpreted carefully. The company may control customer access and local operations while still depending on wholesale network inputs.

Consumer-side unit economics are therefore probably sensitive. Installation cost must be recovered across monthly revenue. Wireless equipment, rooftop or mast access, support visits, router costs, backhaul, spectrum-like operational constraints and customer churn all matter. A small plan with no permanence can be profitable only if installation costs are low, support burden is manageable, and churn does not force repeated acquisition spending. Gregal does not publish these figures. The public tariff table tells us the price ceiling; it does not tell us whether the company earns attractive margins under that ceiling.

For valuation of pricing power, this pushes the weight back toward engineering and business continuity. Commodity residential access may keep a local footprint alive and generate recurring revenue, but it is unlikely to be the deepest source of margin unless Gregal serves a set of customers for whom alternatives remain structurally weak.

The cost base is labour, access, sites and resource administration

The public sources suggest a cost base dominated by skilled labour, field execution, administrative compliance, site access and upstream connectivity rather than heavy nationwide fibre capex. Gregal's own descriptions of engineering, acquisitions, installations, maintenance, camouflage and compliance support all require experienced staff. Commercial databases describe the company as small, with employee estimates ranging from around 10 in older local ranking data to 11-25 or 27 in more recent commercial profiles. These figures are not audited by the company, but they are directionally consistent with a small specialist supplier.

Labour is central because the work is judgement-heavy. Site acquisition needs negotiation and local process knowledge. Structural analysis needs engineering competence. Installation and maintenance need trained technicians and safety discipline. Camouflage work requires design adaptation to particular sites. These activities do not scale like software subscriptions. Utilisation matters. If staff are idle between projects, margins suffer. If the company is stretched, service quality and delivery times can suffer. Pricing power therefore depends partly on whether demand for these skills exceeds the company's capacity.

The public financial proxies are mixed and should be treated cautiously. One local ranking source reports around EUR 997,000 of sales and a small profit figure around the 2020 or 2021 period, with 10 employees and minimal share capital. Empresia describes the latest accounts as 2023 and places sales around EUR 0.5 million, while Iberinform presents a broader revenue bracket of EUR 1.5 million to EUR 3 million and 11-25 employees. Empresite cites employee and ranking indicators. These are commercial profiles with different update dates and methods, not a consolidated audited dataset available in the public article.

The safest conclusion is that Gregal is a small company, not that any single revenue number is definitive.

For pricing power, small scale cuts both ways. A small specialist can be valuable where the buyer needs senior attention and local experience. It can move faster than a large bureaucracy, maintain relationships and tailor work. But small scale also limits purchasing power, redundancy, marketing reach and ability to absorb bad projects. If one or two large carrier customers dominate revenue, buyer power can erase the specialist premium. If revenue is spread across many smaller engineering, maintenance and access accounts, the company has more room to defend price.

Network resources and compliance add another cost layer. RIPE membership and number resources involve annual fees. The CNMC operator-register process requires notifications for network or service provision, modifications, cessation and periodic continuation. The CNMC's own administrative page indicates that the operator-register process has no registration cost, but also notes an annual operator tax for operators with gross operating income above EUR 1 million, capped by the regulatory formula. Those obligations are not the largest cost in telecom, but they are part of the fixed burden of being more than an informal installer.

Upstream connectivity is also a cost. If Gregal depends on Colt or other wholesale inputs for internet transit or backhaul, the company's gross margin on access services is partly determined by negotiated wholesale terms. A small operator does not usually get the same unit economics as a national network. That makes local differentiation essential. The company must recover labour, site and upstream costs through service value that customers cannot easily buy from a mass-market substitute.

Capital intensity appears selective rather than nationwide. The company may need vehicles, tools, rooftop equipment, antennas, routers, installation materials and camouflage products, but there is no public evidence of a broad owned fibre network. That can be positive because it lowers balance-sheet risk. It can also limit control over the full service chain. The margin test is whether Gregal can keep the high-value parts of the job - engineering judgement, site access, customer relationship and local support - while buying commodity inputs without losing too much value to suppliers.

Suppliers and upstream networks keep the bargaining range narrow

Gregal's suppliers and counterparties probably include upstream network providers, equipment vendors, landlords, tower or rooftop owners, municipalities, carrier customers, subcontractors, skilled technicians, RIPE and the Spanish telecom regulator. Several of these have bargaining power over the company. That is why the pricing-power analysis must stay bounded.

The most visible upstream network evidence is the announcement of Gregal-associated IPv4 space through AS8220, Colt Technology Services Group Limited. Colt is a large, established provider compared with Gregal. If Gregal depends on Colt for upstream routing, transit or related wholesale services, the small company has limited leverage on those inputs. It may shop among providers, but the public record does not show extensive multihoming or peering that would neutralise supplier power.

The result is a common regional-operator problem: the company can own the customer relationship and local access but still purchase a crucial part of the service from larger networks.

Equipment suppliers create another cap. Gregal Telecom's site includes AVM FritzBox router pages, which show business and office equipment propositions rather than a proprietary customer-premises platform. Using recognised equipment can be sensible; it lowers support complexity and gives customers familiar features such as Wi-Fi, VPN and guest access. It also means the router itself is not a unique source of pricing power. Many providers can supply good customer equipment. The differentiator has to be installation, configuration, support and service continuity.

Site owners and local stakeholders can be even more powerful than upstream networks. Telecom infrastructure needs physical locations. The acquisitions page's emphasis on prospecting, contracting, renegotiation and representation before neighbours, public bodies and private companies implies that access is a continuous commercial problem. A landlord can demand more rent. A community can entity. A municipality can slow the process. A rooftop can have structural or aesthetic limits.

Gregal's role is valuable because these constraints exist, but the same constraints also mean project economics can be squeezed by parties outside Gregal's control.

Carrier customers can also cap margins. Gregal's corporate site displays logos of major telecom names such as Movistar, Orange, Vodafone and Ericsson as client references or associated customers. The article should not convert a logo strip into verified current revenue concentration, but the signal is still relevant. If a material share of revenue comes from work ultimately controlled by large carriers or equipment vendors, procurement discipline will be strong. Large telecom buyers have framework agreements, purchasing departments and alternative suppliers.

A small engineering firm can win work by reliability and local competence, but it will rarely have one-sided pricing power against these buyers.

The labour market is a supplier too. Telecom engineering and safe field execution require skilled people. If Spain's infrastructure market is active, good technicians and engineers have options. Wage pressure can rise, and small companies may need to protect retention. If Gregal is known for specialist site work, its staff knowledge is a key asset. Losing senior staff could reduce pricing power quickly because much of the value is tacit and local.

These supplier dynamics do not erase the premium. They define its range. Gregal can charge more when it is solving a costly local problem, but it must share value with upstream networks, site owners, employees and large buyers. The strongest evidence of durable pricing power would be the ability to renew carrier and business contracts with stable gross margin despite those pressures.

Customer concentration is the unresolved swing factor

The biggest unknown in Gregal's economics is customer concentration. Public sources show the types of customers the company wants to serve, but not the revenue split. The official corporate site is oriented toward telecom infrastructure clients. Gregal Telecom speaks to access customers and businesses. Commercial profiles classify the company in engineering and telecom-related activities. None of these sources discloses how much revenue comes from major carriers, public bodies, local businesses, residential access customers, maintenance agreements, camouflage products, one-off installations or recurring subscriptions.

That missing split changes the pricing-power answer. If one or two national carriers represent most of revenue, Gregal may be operationally useful but commercially exposed. Large buyers can benchmark against other suppliers and pressure rates. They can also change rollout budgets, consolidate procurement or shift work to internal teams. Gregal's local expertise would still matter, but its margin would depend on being indispensable in enough sites to overcome procurement power.

If revenue is more diversified across carrier projects, maintenance contracts, business access customers and local installations, the company is less exposed to any one buyer. A diversified book also allows cross-selling. A business that buys wireless access may later need engineering support, maintenance or site advice. A carrier project may create knowledge useful for future maintenance. A local engineering relationship may lead to recurring support. Public sources do not prove this loop, but the hybrid service mix makes it possible.

Customer concentration also affects working capital. Project engineering can involve timing gaps between labour outlay and payment. Carrier customers can pay slowly. Small local businesses may pay faster but require more support per euro of revenue. Residential accounts provide recurring billing but may be price-sensitive and costly to serve if faults require truck rolls. The ideal mix would combine recurring access or maintenance revenue with higher-margin project services. The public record does not disclose whether Gregal has achieved that mix.

The age of the company is a positive signal but not proof. A firm founded in 2004 and still publicly operating under the same broad identity has survived multiple telecom cycles: 3G and 4G expansion, fibre growth, 5G, copper retirement, WiMAX decline and consolidation among Spanish operators. Survival suggests some practical capability and customer need. It does not automatically imply pricing power. A small company can survive with modest margins if owners accept low returns or if the business is tightly managed.

The older local ranking profit figure, if representative, would point to thin accounting profit rather than obvious surplus economics.

The unofficial market signals are limited. A 2015 forum discussion includes a user in the Valencia area saying they had Gregal Telecom service and that, after adjustments, it worked well. A local business directory page lists the company but has no deep review base. LinkedIn presents a small company profile with a modest follower count. These signals are useful only as colour: they show a visible local presence and some anecdotal customer reference, not broad market validation.

For the pricing-power thesis, customer concentration remains the line between a resilient niche and a constrained contractor. If Gregal can show recurring revenue across many sites and businesses, with renewal rates and margins that survive national fibre competition, the premium is stronger. If revenue depends on a few carrier buyers or legacy wireless customers, the premium is fragile.

Spain's fibre market sets a harsh substitute price

Spain is one of Europe's most fibre-developed markets, and that fact is central to Gregal's pricing power. CNMC reported that fixed broadband lines reached about 19.70 million in March 2026 and that FTTH exceeded 18 million lines. Its Q2 2025 telecom report said FTTH represented more than 90 percent of fixed broadband lines, that xDSL had effectively disappeared because of copper shutdown, and that a large share of fixed broadband lines had speeds above 100 Mbps, with a meaningful portion at 1 Gbps or higher. The same reports show heavy concentration among major operators and the growing importance of DIGI as a low-cost challenger.

This market structure creates both a threat and a niche. The threat is obvious: fibre coverage and low-cost bundles make older wireless access look weak in many locations. If a customer can buy reliable 600 Mbps or 1 Gbps fibre from a national or low-cost operator at a mainstream price, Gregal cannot win by arguing that 4 to 8 Mbps wireless is economically superior. It can only win on availability, service, installation timing, backup, special configuration or local support.

The niche is also real. National coverage statistics do not mean every address has the same options. Rural and peri-urban locations, industrial areas, temporary sites, properties with difficult landlord access, or businesses with specific continuity needs may still face gaps. Dataestur's broadband-coverage resource exists precisely because coverage differs by territory, technology and speed threshold. The European Commission's Spain connectivity policy pages also emphasise rural gap closure, ultrafast coverage and public funding to reach areas outside operators' own deployment incentives.

Those policy priorities imply that even a fibre-rich country has unresolved edge cases.

Gregal's local proposition fits those edge cases better than it fits a city apartment with multiple fibre offers. A local wireless or engineering provider can be useful where the national operator's installation window is too slow, where a site needs an interim link, where a business wants a named support contact, or where a telecom installation requires physical-site work rather than a standard router drop. The substitute price still matters, but it may be the wrong comparison if the buyer is paying to solve a location-specific constraint.

Avatel is a useful comparator because it markets both rural fibre and WiMAX-style access. That shows the competitive field for underserved locations is not empty. A customer without mainstream fibre may still have specialist alternatives. Gregal's price premium therefore depends on micro-local coverage and reputation, not on rural need alone. If Avatel or another local operator reaches the same customer with faster service, the substitute cap moves closer.

Mobile broadband and fixed wireless from national operators add another cap. Movistar's fibre page also references an internet-radio alternative where fibre is not available, with speeds depending on 5G coverage. Mobile networks have improved materially, and CNMC data shows large mobile-line and mobile-broadband bases. For some customers, a 5G router or business mobile backup can replace a local fixed-wireless link. For others, mobile variability, data policy, indoor coverage, latency or support needs may leave room for Gregal.

Cloud platforms change the economics in a different way. They do not replace the access line, but they reduce the need for some local infrastructure and make reliable connectivity more important. A small business that has moved applications to cloud services may care less about a local server and more about internet continuity. That can support backup connectivity or managed router support, but it also lets the customer compare multiple connectivity suppliers more easily. The cloud raises the value of uptime while commoditising some local IT tasks.

The conclusion is that Spain's fibre market makes Gregal's mass-market price ceiling low, but not zero. The company must avoid competing on generic megabits and instead compete on local completion, continuity and hard-to-standardise access problems.

Regulation and operational risk turn reliability into a margin test

Telecom regulation can look like background detail, but for a small operator it becomes part of the reliability promise. Spain's CNMC explains that operators providing electronic communications networks or services must make prior notification for registration and must keep the register updated for modifications, cessation and periodic continuation. The CNMC administrative page also describes certification and cancellation procedures and notes the annual operator tax conditions for operators above the relevant income threshold. These duties are ordinary for the sector, but they impose discipline on small providers.

Regulatory compliance interacts with pricing power because customers buying continuity do not want a provider that is administratively fragile. If Gregal sells business access or infrastructure support, customers need confidence that the company can operate within Spain's telecom rules, maintain resource records and respond to changes. A small local provider with poor administrative discipline can lose trust quickly. A small provider that keeps clean records and communicates clearly can convert compliance into credibility.

Operational risk is more concrete. Wireless access depends on line of sight, interference management, site availability, power, backhaul, weather resilience, equipment maintenance and customer premises setup. Telecom infrastructure work depends on safe rooftop access, structural suitability, permits, landlord cooperation, worker safety and coordination with carrier schedules. Camouflage products reduce one type of risk but introduce execution requirements of their own: fit, durability, load, access and maintenance must be managed.

The public RPKI status for Gregal-associated IPv4 routing is a small but notable example of hidden operational risk. A route can work without a validating ROA, but route-security maturity is increasingly part of responsible network operation. For a customer, the practical question is not the technical acronym; it is whether the provider's connectivity is protected against avoidable routing mistakes and whether the provider can explain its controls. If Gregal has improved this privately, the public record does not show it.

IPv4 scarcity is another risk. RIPE's exhaustion of new IPv4 supply means small operators must manage scarce addresses carefully. Customer growth can be constrained by address availability unless the operator uses CGNAT, IPv6, transfers or leasing. CGNAT can be acceptable for many residential users but problematic for some business applications, remote access and hosting needs. An operator serving SMEs must be clear about address options and costs. This is a place where pricing power can appear: customers needing public addressing or custom network configuration may pay more.

It is also a place where substitutes can bite if larger operators package these features more cheaply.

Operational reliability is finally a margin test because local service can be expensive. If Gregal promises rapid professional response, it needs technicians, vehicles, spare equipment and management capacity. Each truck roll consumes margin. If customers are geographically dispersed or if old wireless equipment generates support calls, the service premium can disappear. The company must either price support properly or keep the network simple enough to support efficiently.

The best evidence that reliability supports pricing power would be service-level data: mean time to repair, first-time fix rates, fault frequency, renewal rates after outages, business customer references and complaint trends. Public sources do not provide those figures. They do, however, show enough operational complexity to make reliability the right lens.

Unofficial signals should be read as smoke, not proof

Public unofficial signals around Gregal are thin. That is not unusual for a small telecom engineering business, but it affects confidence. A large consumer ISP leaves a wide trail of reviews, complaints, forum posts, speed tests and media coverage. A specialist engineering firm may leave very little. The absence of a deep public review base does not mean the company lacks customers. It means the analyst should avoid pretending that sentiment has been proven.

The most useful anecdote found in open web material is an old BandaAncha forum exchange from 2015 in which a Valencia-area user mentioned having Gregal Telecom service and said that, after some adjustments, it worked well. The post is too old and narrow to prove current quality. It is still economically interesting because it matches the expected pattern for local wireless: performance may depend on installation tuning, and the customer experience can improve after technical adjustment. That supports the idea that support and local competence matter.

A Cataloxy listing for Gregal Telecom gives a public directory presence but does not provide a meaningful review base. LinkedIn lists Gregal Ingenieria as a small privately held company in Riba-roja, with a limited follower count and a public description around telecom engineering. The signal is consistent with a small specialist, not a scaled national brand. Commercial registries also support the small-company reading through revenue and employment ranges, though they differ in detail.

For pricing power, weak public buzz can be a risk or simply a feature of the buyer base. If Gregal's most valuable work is carrier-side site engineering, it will not necessarily generate consumer chatter. Carrier procurement and site owners do not review suppliers like restaurant customers. If the access-service business were a large consumer growth story, however, one would expect more public discussion. The limited signal therefore reinforces the view that the strongest economics are probably not in mass consumer broadband.

Unofficial signals also help discipline claims about brand strength. Gregal may have local recognition among certain customers and telecom buyers, but the public record does not support calling it a high-awareness consumer brand. Its advantage is more likely trust within a narrow operating circle. That trust can be valuable but fragile. It is harder to scale and easier to lose if service quality slips.

The correct use of unofficial signals is to identify questions, not to close them. Does Gregal have a loyal base of wireless customers in specific Valencia-area localities? How much of that base remains after fibre expansion? Do business customers buy backup links or primary access? Are carrier-side clients repeat buyers? Does the GBlock camouflage product create repeat orders or one-off project revenue? Public anecdotes cannot answer these questions, but they point to where private diligence should look.

What would prove the premium survives renewal

The most important private metric would be renewal behaviour. Pricing power is not the ability to win a first project through familiarity or a one-time gap. It is the ability to keep customers when they have alternatives. For Gregal, that means tracking carrier project repeat rate, maintenance-contract renewal, business access churn, residential churn after fibre becomes available and the price change customers accept at renewal.

For engineering services, the key evidence would be project-level gross margin and win rate by problem type. A simple revenue total would not be enough. Gregal should know whether site-acquisition work, camouflage, installation, maintenance, compliance support and business access each earn acceptable margins. It should also know whether projects with high visual or stakeholder complexity generate better margins than routine work. If the premium thesis is right, complex sites should show stronger margin and repeat buying.

For access services, the decisive metrics are active customers by technology, ARPU, installation cost, payback period, churn, support cost per customer, fault rate, average response time and the share of customers with fibre or 5G alternatives. A wireless customer who stays because there is no alternative is different from one who stays after fibre arrives because local support is better. The latter is stronger pricing-power evidence. The former may be profitable but is vulnerable to coverage expansion.

For network economics, Gregal would need to show upstream diversity, cost per Mbps, backhaul resilience, address-resource strategy, IPv6 readiness, RPKI status and customer-impact history. The current public route evidence through Colt makes supplier dependence a central question. If the company has multiple upstreams, private peering, backup paths or improved route-security controls, that would materially strengthen the case. If it depends heavily on one upstream and one /24 allocation, pricing power in connectivity remains narrow.

For customer concentration, the private test is blunt: what percentage of revenue comes from the top five customers, and how many of them can rebid the work annually? A business with 40 percent of revenue tied to one large carrier buyer is very different from a business with hundreds of small recurring customers and recurring maintenance contracts. Customer identity need not be public, but the concentration math is essential.

For supplier bargaining power, Gregal should be able to show equipment costs, labour utilisation, subcontractor dependence, site-rent exposure and gross margin after upstream network costs. A local engineering premium can be real and still fail to create attractive economics if too much value leaks to suppliers or if the company underprices support.

For regulatory and reputation risk, useful evidence would include CNMC registration status, periodic continuation records, incident history, complaint logs, safety records, insurance cover, permit success rates and documentation quality. Small telecom suppliers can lose buyer trust through administrative weakness even when technical work is good. Conversely, strong compliance can be a quiet competitive advantage.

For image and public positioning, the most credible editorial visual would be a real telecom-infrastructure scene: a rooftop antenna enclosure, a maintenance technician at a mast, a discreet facade installation, or an exterior office or industrial-estate context tied to Valencia telecom work. It should not be a fake dashboard, invented logo, unreadable network map or abstract technology collage. The company's economic story is physical, local and operational; the image should show that.

The current judgement is therefore conditional but useful. GREGAL INGENIERIA S.L. appears to have defendable pricing power in a narrow band: telecom infrastructure friction, local engineering continuity and connectivity problems where mass-market substitutes do not solve the whole job. It does not appear to have broad consumer-broadband pricing power against Spain's fibre market. Carriers, cloud platforms, national fibre operators, rural challengers, mobile substitutes, site owners, upstream providers and skilled labour all cap the range. The premium reaches as far as the customer believes Gregal can prevent a more expensive failure.

It stops where the purchase becomes a standard connection, a routine installation, or a procurement line that larger providers can fulfil at scale.