Summary

- FRANCE MEDIAS MONDE SA's local network-control case is defensive rather than retail-commercial: RIPE membership, broadcast distribution, ST 2110 migration, external data-center use, cloud migration and multilingual digital distribution support mission reach and resilience, but they do not by themselves prove pricing power or a telecom resale business.

- The capital recovery test turns on whether FMM can convert public funding, limited own resources and supplier-dependent infrastructure into measurable lower distribution risk, better direct audience access, lower unit delivery cost and stronger editorial continuity than a simpler carrier/cloud/platform stack would provide.

The operating boundary is French, but the audience obligation is global

The first economic fact about FRANCE MEDIAS MONDE SA is a constraint, not an opportunity. The company is legally and physically anchored in France, with a registered office in Issy-les-Moulineaux, a French public limited company structure, and a public-service broadcasting mandate. Its brands, however, are built for audiences that sit outside a normal domestic media territory. France 24, RFI and Monte Carlo Doualiya do not exist only to monetize French households. They are meant to reach viewers, listeners and digital users across continents, languages, political systems and connectivity conditions.

That geography matters because it makes the network problem unlike a standard French media distribution problem. A domestic broadcaster can bargain with national telecom operators, connected-TV platforms, advertising agencies and local regulators around a largely national audience base. FMM must reach a listener in a rural African region where internet access may be intermittent, a viewer using a hotel television feed, a young user receiving video through a social platform, a listener in Paris on DAB+, and an audience in a country where French international outlets may face censorship or service disruption.

Its operating headquarters are local; its distribution obligation is not.

The company describes its own reach in explicitly global terms. France 24 is presented as a 24-hour news channel in French, Arabic, English and Spanish, and FMM's key figures describe access to hundreds of millions of households worldwide. RFI broadcasts in French and many other languages through FM, DAB+, shortwave, satellite, internet, apps and partner stations. MCD serves Arabic-speaking audiences from Paris toward the Middle East and nearby regions. The group also runs or participates in digital-first offers such as InfoMigrants, ENTR and ZOA. That portfolio is not the product of a narrow access network; it is a distribution mesh.

The capital recovery question therefore starts with the difference between ownership and control. FMM does not need to own every delivery pipe to control its mission. It needs enough technical and contractual control to keep news available, verifiable and adaptable when audiences move between broadcast, social video, proprietary apps, satellite, radio, connected television and partner outlets.

If that control costs more than it saves, or if it duplicates capabilities that Akamai, Scaleway, Claranet, public broadcasters, telecom carriers or global platforms already provide at scale, the spending becomes a sovereignty premium rather than a value-creating asset.

That is not automatically bad. A public international media group may rationally pay a sovereignty premium where the alternative is dependence on opaque platform ranking, local political shutdowns or fragile third-party distribution. But the premium still needs discipline. It should buy resilience, editorial continuity, audience access and optionality. It should not become a loosely justified technology program whose benefits are described in audience totals while its costs sit in fixed budgets.

The business model funds mission reach, not telecom margin

FMM's business model is mainly public-service funding with small commercial and external project contributions. The company's 2026 financing page says the core budget is financed largely through an allocation of value-added-tax proceeds, with additional official-development-assistance funding for international proximity projects and smaller external resources from bodies such as the Agence Francaise de Developpement and the European Union. Advertising and other own resources are explicitly limited by the nature of multilingual global news and a fragmented advertising market.

That structure changes the interpretation of revenue growth. For a private telecom operator, growth can be tested through subscriber additions, ARPU, churn, gross margin, contribution margin, capex intensity and return on invested capital. For FMM, the buyer is not primarily a broadband household or an enterprise connectivity customer. The payer is largely the French public purse, supplemented by limited commercial resources and project-specific funding. The beneficiary is a global audience and the French public-interest objective of international information reach.

The downside sits with taxpayers, employees and the credibility of a public media institution if the cost base outruns political support.

The group has reported strong audience and digital performance. In 2025, FMM said its channels reached 278 million weekly contacts worldwide, and that digital video views and audio starts approached 5 billion for the year. Its own 2026 budget communication says strategic priorities include verified and balanced information in 21 languages, fighting information manipulation, digital transformation, artificial-intelligence work, proximity projects in Beirut, Dakar and Bucharest, and the renewal of television control rooms. Those are plausible mission priorities. They are not, by themselves, proof of economic value creation.

For Elias Ward's lens, the distinction is important. Visibility can rise while value creation remains uncertain. A record month on Facebook, YouTube or TikTok proves demand for content in a moment of geopolitical tension; it does not prove the group controls distribution economics. A rise in weekly digital contacts proves that audiences found FMM content somewhere; it does not prove that owned environments are becoming more valuable than third-party platforms. A stable public dotation can keep service quality high; it does not show that a technical investment earns its cost.

The recoverable economic value lies in avoided dependence and measurable efficiency. If FMM's network and platform choices reduce outages, keep editorial delivery alive during censorship, lower distribution costs per audience contact, increase direct traffic to owned apps and sites, or improve production flexibility across radio and television, then local control has an economic rationale. If the same outputs can be bought from bigger suppliers with simpler contracts and lower fixed costs, local control is harder to defend.

The resource evidence shows operational seriousness, not an ISP franchise

The RIPE NCC member listing for FRANCE MEDIAS MONDE SA is meaningful, but it must be interpreted carefully. RIPE membership records a number-resource governance footprint and a French service-area context. It is evidence that the organization sits close enough to internet-number-resource administration to manage operational responsibilities. It is not evidence that FMM sells broadband, IP transit, hosting or managed connectivity to third parties.

That distinction is central to the investment case. A media group can need RIPE membership, IP address administration, routing competence, DNS management, data-center arrangements and delivery resilience without becoming a telecom carrier. The evidence supports a local-control thesis, not a retail-ISP thesis. It says FMM has an operational internet layer that matters to its mission. It does not say FMM has a customer-facing network business with recoverable network margin.

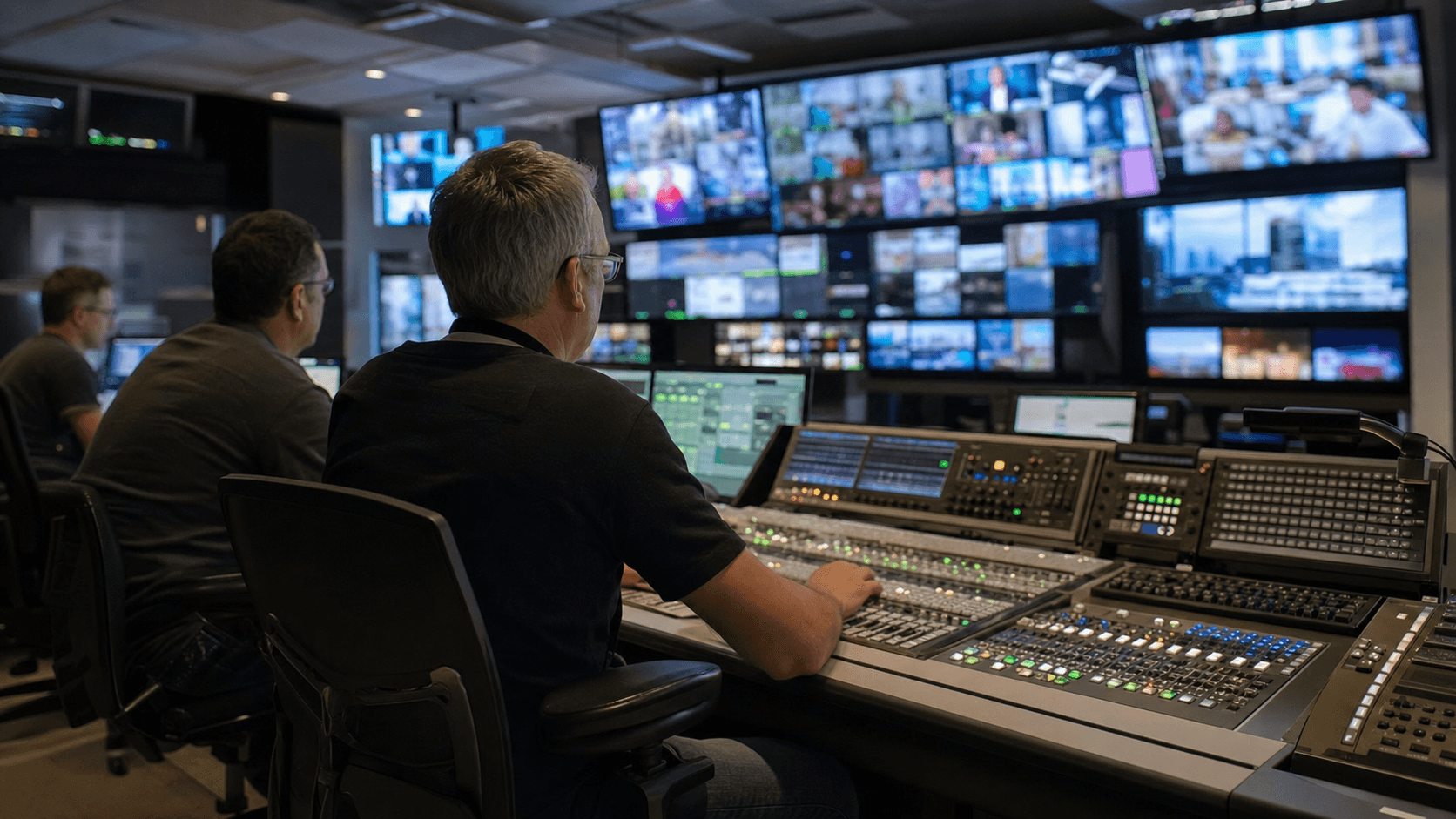

The technical evidence is broader than the RIPE entry. FMM's 2024 activity report describes broadcast infrastructure moving toward SMPTE ST 2110, a standard that transports video over IP networks and allows greater flexibility and shared use of radio and television resources. The same report describes moving part of the group's server rooms to an external data center selected through a joint public-audiovisual tender, with security and energy-efficiency objectives.

It also describes a progressive cloud migration for some software developments and a microservices approach that should help remote editorial teams work on common television, radio and digital tools.

This is the important operational boundary. FMM is not just renting social distribution and uploading clips. It is modernizing the production and distribution stack that sits behind live channels, radio services, foreign-language digital production and global audience access. ST 2110 migration can reduce siloed television and radio infrastructure. External data-center use can improve resilience and energy performance. Cloud and microservices can make remote editorial work easier across Paris, Bucharest, Dakar, Lagos, Nairobi, Phnom Penh, Bogota and Beirut. Those are real operational reasons to invest.

But they also deepen supplier dependence. External data centers, cloud services, content-delivery networks, platform distribution and broadcast partners all shift part of the control plane outside FMM. That does not make the strategy wrong. It means the investment case is hybrid. Local control is not ownership of every asset; it is the ability to decide which parts must be internal, which parts can be outsourced, and how the whole system behaves under stress.

The test is whether FMM can articulate that architecture in economic terms. The company should be able to show which workloads require internal control, which are better on third-party cloud, which delivery channels are mission-critical, which are audience-acquisition tools, and which supplier dependencies carry unacceptable concentration risk. Without that map, RIPE membership and IP transformation risk becoming badges of technical maturity rather than proof of capital recovery.

Broadcast reach still carries value where internet access is uneven

The strongest argument for FMM's local-control footprint is that global news distribution is not yet an all-cloud, all-app market. FMM's own reception pages emphasize that RFI remains available through FM, DAB+, shortwave, satellite, internet, apps and partner radio stations. The company says RFI and MCD have one of the world's large FM and partner-radio footprints, while France 24 is present across cable, DTT, free-to-air, OTT, hotel rooms, airlines, cultural institutions, websites, apps and social platforms.

This matters because the least connected audiences are often the most expensive to reach with pure digital economics. A global cloud platform can deliver video efficiently where connectivity, devices, app stores and payment infrastructure are strong. It does not solve the last-mile problem in regions where electricity, mobile data, censorship, platform blocking or device affordability limit access. For a public international broadcaster, old distribution technologies can remain economically rational because they buy reach and continuity where digital-only delivery would exclude the audience the mission is meant to serve.

FMM's DAB+ activity in France is a small but telling example. In 2025 it signed a partnership around DAB+ promotion, and the announcement framed DAB+ as a way for RFI and MCD to be accessible in selected French cities such as Paris, Marseille, Bordeaux, Lille, Lyon, Strasbourg and Toulouse. The same communication highlighted that DAB+ offers radio without internet access and with ecological and reliability benefits. In pure growth-accounting terms, that may not look like a high-margin platform. In resilience-accounting terms, it keeps an independent radio pathway alive.

France 24's availability on France.tv also shows the mixed strategy. By putting the French-language channel on France Televisions' streaming platform, FMM extends domestic access and catch-up availability through another public-media platform rather than only through its own site or global social networks. The economics are again hybrid: FMM gets distribution leverage from a larger public platform, but it shares the user relationship and analytics environment.

For capital recovery, the question is not whether broadcast is modern or old. It is whether each delivery mode has a defined role. FM, DAB+, shortwave and satellite should protect access where internet dependence is a weakness. Proprietary sites and apps should deepen direct relationships and first-party usage. Social platforms should acquire audience, especially younger and mobile users, without becoming the only route to scale. CDNs and cloud should provide elastic delivery and engineering leverage, while internal network and production control should preserve resilience and editorial continuity.

If FMM can allocate capital by those roles, the distribution footprint can earn its cost even without telecom-style margins. If each layer simply adds cost because no team is willing to retire legacy delivery or negotiate harder with suppliers, the footprint becomes a fixed-cost trap.

The cost base is too fixed for vague transformation spending

The 2024 activity report gives the clearest warning about economics. FMM described 2024 as a constrained budget year, with public funding reductions during the year and the removal of most transformation-program credits initially expected. The report says the company drew on its own funds to offset part of the deleted transformation financing because the digital transformation was considered a priority. It also says the particular budget structure, composed of more than 95% fixed charges and far smaller than those of competitors, could not absorb the cut at constant scope in the short term.

That is a hard capital-recovery backdrop. A business with very high fixed charges has little room for technology programs that do not reduce future cost or protect high-value output. Every new control room, data-center move, ST 2110 upgrade, cloud migration and regional digital hub has to be examined not only as an editorial enabler but as a future operating-cost claim. If it creates another fixed layer, the organization becomes less flexible.

If it replaces older assets, reduces duplicated radio and television workflows, lowers energy consumption, simplifies remote production, or avoids emergency distribution spending, it may improve resilience and unit economics.

The 2024 cost breakdown is instructive. The report identifies program offers as the largest cost block, with distribution and diffusion, digital environments and transformation programs, communication and marketing, externally funded projects, support functions, common means and salary-related charges making up the rest. The full digital cost was described as much larger than the narrow digital-environment line once digital editorial teams, transformation programs, digital offers and reused broadcast content were included. That matters because digital is not a cheap add-on.

It is an operating mode that absorbs intelligence team, production, technology and platform costs.

The 2026 budget communication sharpens the issue. The company planned a stable core public allocation, additional public support through development-aid and information-manipulation programs, and own resources of roughly EUR 14.8 million. It also referred to indispensable investments in technical infrastructure, the renewal of television control rooms and major headquarters works linked to energy-consumption rules. Even when the building works are owner-funded, the management burden and operational disruption are real.

In that setting, "digital transformation" is not a strategy. It is a spending category that needs proof. The proof should be measured in shorter production cycles, fewer duplicated systems, lower outage risk, lower delivery cost per stream or listener, better reuse of content across languages, lower energy intensity, faster correspondent workflows, and a larger share of audience reached through environments where FMM controls presentation and data. A public broadcaster can justify mission spending; it cannot justify permanent fixed-cost growth simply by pointing to audience totals on third-party platforms.

Pricing power is weak because the main payer is the state

FMM has limited conventional pricing power. Its core funding is not set by a market price for users. It depends on public budget choices, parliamentary decisions, ministry support and the wider politics of French public broadcasting. The group can grow advertising, partnerships, training, syndication and project funding at the margin, but its own resources remain small relative to the public grant.

This has a direct implication for local network control. A private carrier can invest in a route, data center or access platform and recover the cost through customer contracts. FMM must recover cost through public value, cost avoidance and mission performance. That means the "price" of its services is political. If the French state and taxpayers believe the international information mission is strategically important, FMM can fund resilience investments even when direct commercial return is low. If the public-media settlement tightens, the same fixed infrastructure becomes vulnerable.

The 2025 financial statement announcement is useful here. FMM said it reached a balanced result in 2025, improving from an initially budgeted deficit, helped by charge control, a parliamentary amendment and an exceptional foreign-ministry subsidy linked to fighting disinformation. That shows management discipline, but it also shows dependence. Break-even was achieved in a budget environment where political and ministry support mattered. The capital recovery of technical infrastructure is therefore not separable from public-policy support.

The commercial side is not irrelevant. FMM's global audience, digital reach and brand trust can support advertising, partnerships and external project finance. France 24's digital audience on YouTube, RFI's language services, MCD's Arabic-language reach, InfoMigrants, ENTR and ZOA can all carry value. But own resources are too small to finance the core network footprint on their own. They can improve the margin of safety; they cannot replace the public funding base.

That makes supplier choice even more important. If FMM has weak pricing power, it must have strong procurement discipline. It should buy scale where global suppliers are structurally cheaper, retain control where mission risk is high, and avoid bespoke platforms that cannot be maintained without permanent incremental funding. The harder the budget environment becomes, the more every internal-control claim needs a costed alternative: what would Akamai, Scaleway, Claranet, a public-broadcast partner, a cloud provider, a satellite distributor or a managed-service vendor charge for the same result, and what risk would that transfer create?

Supplier dependence is not a flaw, but unmanaged concentration would be

FMM's legal notice and public web footprint show a supplier-dependent media stack. The legal notice names web hosts including Claranet, Akamai, Scaleway and DigitalOcean for different sites. A public IP lookup for the corporate francemediasmonde.com address places the address at Scaleway's AS12876. DNS lookups for France 24 and RFI show Akamai delivery paths. None of this is surprising. A global video and audio publisher should use content-delivery, hosting and cloud suppliers. The question is whether supplier dependence is diversified, governed and tested.

For a media group, Akamai-style CDN dependence is often economically rational. Traffic is spiky, global and driven by news events. FMM's April 2026 release about nearly 700 million video views and audio plays in March shows the nature of the load: platform consumption surged around conflict coverage, with large volumes on Facebook, YouTube and TikTok. Owning enough physical distribution to serve that kind of event-driven demand directly would be capital-intensive and probably inefficient. Buying CDN and platform scale is sensible.

But platform scale brings platform risk. FMM's own 2024 activity report used the phrase "reasoned hyperdistribution" to describe being present on major platforms and social networks while also investing in proprietary environments. That is the right direction. If Facebook, YouTube, TikTok, Instagram, WhatsApp, X and platform algorithms become the dominant discovery layer, FMM gains reach but loses control over ranking, monetization, data and policy enforcement. The public purpose may remain intact editorially while the distribution economics are set elsewhere.

Cloud and data-center migration create a similar tradeoff. Moving servers and broadcast infrastructure toward external data centers and cloud software can improve security, energy efficiency and remote collaboration. It can also expose FMM to vendor terms, price escalation, service concentration and cross-border policy questions. The more FMM's foreign-language services rely on a common cloud workflow, the more important exit rights, backup workflows, data portability and incident testing become.

The right benchmark is not full independence. Full independence would be uneconomic. The right benchmark is operational substitutability. Can FMM move a service if a supplier fails? Can it keep a live channel, audio stream, app, intelligence team tool or regional hub functioning during a major outage or political block? Can it shift between CDN, satellite, DAB+, FM, shortwave, partner radio, France.tv, YouTube and owned apps when one path degrades? If yes, supplier dependence is a managed portfolio. If no, local control is narrower than the public story implies.

Audience scale is real, but platform scale can hide weak unit economics

FMM's audience scale is not imaginary. In 2025 it reported 278 million weekly contacts and roughly 5 billion digital video views and audio starts. It also said its social-platform communities exceeded 127 million subscribers, with sharp growth on Instagram and TikTok. France 24's YouTube performance is especially strong, with the company saying it remained the leading French media brand on YouTube and had more than 18 million subscribers across its four language channels by 2025. RFI also reported large video growth, especially in African languages.

The issue is not whether people watch or listen. The issue is who controls the economics of that watch and listen. A YouTube view is not the same as a proprietary-site visit, a live TV household, a DAB+ listener, a podcast subscriber, a WhatsApp follower or a partner-radio broadcast. Each has different data access, monetization, reliability, editorial presentation, platform risk and unit cost. FMM's own digital release wisely separates proprietary visits from platform views, but the public performance story still leans heavily on aggregate digital volume.

A capital recovery test needs unit analysis. FMM should know the cost per weekly contact by channel and region, even if the figure is used internally rather than as public commercial disclosure. It should know whether a French-language France 24 viewer on france.tv is cheaper or more valuable than a YouTube viewer. It should know whether DAB+ city availability is drawing incremental listeners or merely shifting existing audiences. It should know whether RFI's language services on social platforms drive durable direct relationships or remain dependent on platform recommendation.

It should know which partner-radio relationships provide resilience in censorship environments and which are low-impact legacy arrangements.

Without that unit view, audience growth can mislead. A conflict-driven spike can make digital strategy look stronger than it is. A platform's algorithmic preference for live or short video can boost consumption for one quarter and disappear the next. A foreign-language expansion can create political value but add permanent editorial and distribution costs. A new hub can improve proximity but duplicate functions already available through correspondents and partners.

This does not argue against growth. It argues against treating growth as value creation. The article's core question is whether local control earns its cost when bigger carriers, cloud platforms and managed-service substitutes offer simpler alternatives. The answer depends on whether FMM can translate audience scale into controlled, resilient, cost-disciplined reach. If the audience is large but the economics are set by third parties, FMM has mission impact but limited pricing power.

Customer concentration is political rather than commercial

FMM's customer concentration risk is unusual because its dominant customer is effectively the public-funding settlement. The group serves many audiences, but those audiences do not pay for the service at the level required to fund the operation. The French state, through public audiovisual financing and ministry-linked programs, carries the core financial obligation. That concentration is both a strength and a vulnerability.

It is a strength because it permits investment in audiences and languages that a private broadcaster would underserve. RFI can maintain language services and broadcast paths that do not maximize advertising yield. France 24 can cover international crises with a public-service objective. MCD can maintain Arabic-language service from Paris. FMM can participate in efforts such as the cooperation with Deutsche Welle around an Information Shield, regional hubs and disinformation resilience, even where immediate commercial return is limited.

It is a vulnerability because funding is politically contestable. The French public broadcasting sector has faced repeated reform proposals, budget scrutiny and criticism over neutrality, efficiency and governance. Reuters Institute's 2026 France analysis described public-service media scrutiny, polarized debate and low trust in news overall. Guardian reporting on a 2026 parliamentary report described proposals for major cuts and restructuring in French public broadcasting, while noting political controversy around the report. These are market signals, not settled financial statements, but they show the pressure around the payer.

FMM is somewhat different from domestic France Televisions or Radio France because its mission is international and tied to foreign policy, language, public diplomacy and information integrity. That can protect it when geopolitical tensions rise. The 2026 budget communication itself frames FMM's mission in terms of hybrid war, disinformation and competition with actors that have much larger means. But strategic relevance can cut both ways. It can justify funding; it can also invite political demands, governance scrutiny or expectations that the group do more with less.

This creates a tough management problem. The group must speak the language of public value without losing cost discipline. It must defend international information reach without assuming that public funding will automatically rise with audience demand. It must show that network-control spending is not a technical preference but a mission-risk hedge with measurable outputs. In a politically concentrated revenue model, evidence of efficiency is not optional. It is part of the license to keep investing.

Larger carriers and cloud platforms are substitutes, not just suppliers

The realistic alternatives to FMM's local control are not theoretical. Telecom carriers, global cloud providers, CDN networks, public broadcaster partnerships, YouTube, Facebook, TikTok, WhatsApp, satellite distributors, OTT platforms and managed broadcast-service vendors all offer pieces of the distribution stack. In many cases they offer scale FMM cannot match. That makes them substitutes for internal control as well as suppliers to it.

The simplest alternative would be to buy more managed services: outsource more playout, host more workloads in cloud, rely more heavily on CDNs, publish more through major social video networks, use public-broadcast partner platforms domestically, and keep only editorial production and brand governance internal. That would reduce some capex and staffing complexity. It would also reduce direct control over presentation, data, routing resilience and emergency fallback.

The strongest argument for internal or semi-internal control is that FMM's mission is not the same as a private media company's monetization strategy. The group operates in countries where censorship and service disruption are real. Its own 2024 activity report mentions continuing censorship and cutoffs of its media in Russia, Mali, Burkina Faso, Niger, Tripoli and Khartoum. RFI's page notes FM transmitters shut down in Mali, Burkina Faso and Niger. In those environments, dependence on a single platform or local distribution partner is risky. Redundant routes can be worth the cost.

But the redundancy must be selective. A public broadcaster does not need to duplicate every capability a cloud provider can perform better. It should not build expensive internal systems to avoid a dependency that can be managed contractually. The best strategy is a layered one: internal editorial systems where content integrity and continuity matter; external cloud and data centers where scale, energy performance and flexibility matter; CDNs and platforms where burst delivery and youth reach matter; broadcast and radio paths where internet independence matters; and partnerships where local relevance or political resilience require it.

The question is whether FMM is already running that layered strategy or drifting into accumulation. The 2024 activity report and 2026 budget communication point in the right direction: ST 2110, external data center, cloud, microservices, regional hubs, AI roadmap, proprietary environments and platform distribution. The risk is that every layer is justified as strategic and none is forced to show what it replaces. Capital recovery requires substitution discipline: each new network-control layer should retire, reduce or materially improve something else.

Regulation and geopolitics raise the value of resilience

Regulation and geopolitics are not side issues for FMM. They are core operating conditions. Arcom's 2025 audio-video trends work shows a French market where the television set remains heavily used but smartphones, connected devices, paid video offers and platform consumption are structurally important. The Reuters Institute's 2026 global report says social media and video networks have overtaken both television and owned news websites/apps as sources of news across surveyed markets, with online news video now watched weekly by a large majority globally. Those shifts directly affect FMM's distribution economics.

At the same time, the international information environment is becoming more hostile. FMM and Deutsche Welle's Information Shield cooperation is explicitly framed around manipulation and disinformation, especially around Central and Eastern Europe and Russian-origin information operations. FMM's 2026 budget communication references hybrid war, disinformation, proximity hubs and support from the Ministry for Europe and Foreign Affairs. The group is not merely chasing audience. It is being asked to serve as part of a democratic information infrastructure.

That can make local network control more valuable than a spreadsheet of commercial returns would suggest. If an outlet must serve audiences during conflict, censorship, platform manipulation or local service interruptions, redundancy and control have option value. A DAB+ signal that works without internet, a satellite path, a partner-radio network, a direct app, a data-center failover plan or a cloud workflow available to remote editorial teams can all matter when a normal commercial path fails.

But option value is not unlimited. The fact that resilience is important does not mean every resilience spend is efficient. A disciplined public media network should run incident scenarios: what fails if a major CDN goes down, if a social platform reduces news visibility, if a local FM relay is censored, if a regional hub loses connectivity, if a cloud provider raises prices, if a cyber incident affects a production system, if an app store restricts access, or if public funding is frozen midyear. Those scenarios should map to the capital plan.

FMM's compliance and transparency posture also matters. Its JTI renewal and public anti-corruption and whistleblowing materials support institutional credibility. In a public-funding model, governance credibility lowers political risk. If FMM can show that network-control spending is procured, tested, benchmarked and tied to mission outputs, it is easier to defend. If the spending looks like technical opacity, it becomes a target.

Unofficial signals point to pressure on both audience and funding

The unofficial market signals are consistent: the French and global news market is moving toward video, platforms, creators and lower trust, while public broadcasters face sharper political scrutiny. Reuters Institute's France pages show low overall trust in news, growing creator and platform use, and a public-service media debate shaped by politics. Arcom's trends show the persistence of television and radio but also the importance of smartphones, connected TV and paid video environments. Press reporting on French public-broadcasting reform shows that public media budgets and structures are politically contested.

Those signals should not be treated as audited facts about FMM's performance. They are better read as pressure indicators. They imply that FMM needs platform reach because audiences are there. They imply that FMM cannot abandon television and radio because those channels remain material and often resilient. They imply that public trust is fragile, so transparent governance and editorial standards matter. They imply that public funding cannot be assumed to grow simply because the international information environment is tense.

They also make the core strategic tradeoff sharper. If young audiences use YouTube, TikTok, Instagram, WhatsApp and creators for news, then FMM must be there. If public-service media are judged partly on independence and trust, then FMM cannot let platform logic fully shape its journalism. If television remains important, then France 24's linear and connected-TV presence still matters. If radio remains heavily consumed and DAB+ can work without internet, then RFI and MCD's broadcast pathways have value.

If direct websites and apps are the only places where FMM controls presentation and data, then owned environments deserve investment even if platform volumes are larger.

This is why the local-control argument is neither simple ownership nationalism nor simple outsourcing. The market is moving in two directions at once. Scale and discovery are moving to global platforms. Trust, accountability and continuity require direct institutional control. FMM's strategy must therefore optimize between reach and independence, not maximize one at the expense of the other.

The judgment: control earns its cost only if it lowers mission risk per euro

The current evidence supports a cautious positive judgment on FMM's local network-control footprint, but not an unconditional one. The company has a legitimate reason to maintain more distribution control than a normal commercial publisher. It serves multilingual international audiences, operates in high-risk information environments, faces censorship, and must combine broadcast, radio, digital, social, satellite and partner distribution. Its RIPE membership, ST 2110 transition, data-center migration, cloud work, DAB+ presence, France.tv integration, platform scale and regional hubs together show a real operational footprint.

The weakness is not relevance. The weakness is measurable recovery. FMM's own reports show a very fixed cost base, limited own resources, constrained public funding, transformation credits vulnerable to cuts, and reliance on exceptional or project-linked public support. The company can defend technical investment only by showing that the control it buys is cheaper, safer or more strategically effective than the managed-service alternative.

That means the investment case should be expressed as mission risk per euro. Does ST 2110 reduce duplicated radio and television costs, increase flexibility and improve resilience? Does an external data center lower energy cost and improve failover enough to justify migration risk? Does cloud migration reduce development and support cost while keeping exit options? Do proprietary environments increase direct audience relationships enough to balance platform dependence? Do DAB+, FM, shortwave and satellite protect unique audiences or merely maintain legacy cost?

Do regional hubs produce local relevance that a correspondent network could not achieve more cheaply?

If FMM can answer yes with data, local network control earns its cost. If it cannot, the argument weakens. Larger carriers and global platforms will always offer simpler alternatives. They will often be cheaper at the unit-delivery level. FMM should use them aggressively where they are commodities and resist them where they threaten continuity, editorial control or access to audiences under pressure.

The practical conclusion is not to shrink the network footprint blindly. It is to turn the footprint into a portfolio with explicit economic roles: resilience routes, direct-audience assets, elastic delivery suppliers, production-control systems, regional-proximity assets and platform-acquisition channels. Each role should have its own metrics and sunset logic. A public media group can tolerate low commercial margin if the mission return is clear. It cannot tolerate unclear control spending inside a fixed-cost base.

What would change the judgment

Several facts would strengthen the case that FMM's local network-control footprint earns its cost. The first would be a published or internally audited channel-by-channel unit-cost framework showing cost per weekly contact, stream, listener or household by distribution path and region. The second would be evidence that ST 2110 and control-room renewal materially reduce duplicated infrastructure, operating hours, energy consumption or incident recovery time.

The third would be stronger direct-audience evidence: sustained growth in owned-site and app usage relative to platform-only views, higher newsletter or app retention, and more first-party engagement in key languages.

The fourth would be resilience evidence. If FMM can show that its mixed distribution stack kept services available during censorship, platform throttling, CDN incidents, cyber events or local connectivity failures, the control premium becomes easier to defend. The fifth would be procurement benchmarking: clear comparisons showing where managed-service substitutes were cheaper and selected, where internal control was more expensive but justified, and where legacy assets were retired after migration.

Facts that would weaken the judgment are equally concrete. If digital audience growth remains overwhelmingly platform-dependent while proprietary environments stagnate, FMM's direct-control story weakens. If technical infrastructure spending grows while fixed costs remain above 95% and no legacy systems are retired, capital recovery becomes doubtful. If own resources stay near the mid-teens of millions of euros while public funding tightens, the organization becomes more exposed to political budget cycles. If regional hubs add permanent cost without measurable audience, trust or resilience gains, they risk becoming symbolic expansion.

The decisive evidence is not a bigger audience headline. FMM already has scale. The decisive evidence is whether the group can show that each euro spent on local network control buys something a global platform or managed supplier cannot reliably provide: independent reach, continuity under pressure, lower long-run operating cost, or direct trust with audiences that matter to the public mission. Until that proof is visible, FRANCE MEDIAS MONDE SA should be treated as a strategically important public international media operator with real network-control needs, but not as a conventional network business with demonstrated pricing power.