Summary

- FIBRA A LA PORTA, S.L. is publicly tied to the Biartel telecom brand in Biar, Alicante, with a legal notice, retail service pages, contact address and RIPE NCC member listing that all support a real local access-provider identity rather than a paper-only name.

- The economic case is strongest where Biartel can turn local presence, fast support and bundled household or SME services into retention; it is weaker where customers compare only headline fiber and mobile prices against national operators and low-cost brands.

- The largest unknowns are margin and control: public sources do not disclose customer count, churn, gross margin, debt, owned fiber depth, wholesale mobile terms, TV-content terms, upstream transit costs, ASN/prefix details, enterprise contract length or capex commitments.

The incentive is to stay necessary before scale arrives

The management problem for a small Spanish access provider is not whether households and businesses need connectivity. They do. The harder question is whether a local operator can remain necessary after fiber access becomes ordinary, mobile data becomes cheap, national bundles compress the visible price of service, and wholesale suppliers sit between the retail customer and many of the inputs that determine margin. FIBRA A LA PORTA, S.L.

matters as a company-research subject because it sits exactly at that point in the market: it appears to serve a local community through the Biartel brand, publishes practical consumer and business tariffs, and holds RIPE NCC member status, yet it does not publicly disclose enough financial or network detail to prove that its local demand is also a defensible economic position.

The public face of the company is local, not abstract. Biartel describes internet, mobile, television and fixed-line service in Biar. Its address appears as Calle Jesus Juan Bernabeu, 9, 03410 Biar, Alicante, and its contact details are presented for customers who want service, support or business advice. The legal notice identifies FIBRA A LA PORTA S.L. as the social denomination behind the Biartel commercial name and gives the CIF B42565333.

A secondary company-data page for FIBRA A LA PORTA places the company in Biar, assigns it fixed-telecommunications activity, records a 2018 founding date, lists a small employee count for 2024 and gives a revenue band between 0.6 million and 1.5 million EUR. That secondary data is not audited financial analysis, but it frames the subject as a small operating company rather than a scaled national carrier.

The investment and strategy question therefore starts with incentives. A small town operator has an incentive to sell reliability, proximity and problem resolution, not only bandwidth. If a household can walk into a local office, ask for help in Spanish, get the same company to handle fiber, mobile, television and fixed voice, and receive faster field support than a remote call center can provide, the service can have value beyond the technical commodity. That value may support retention even when a national operator advertises a cheaper introductory price.

For a small business, the value can be stronger: point-to-point links, fixed voice, mobile lines, VPN or backup services can become part of operating continuity. The customer is no longer buying only internet access; the customer is buying a responsible local party that knows the site and can respond when connectivity breaks.

That is the positive case. The negative case is equally important. Local trust does not automatically become margin. If the operator must pay wholesale mobile input costs, television-content costs, upstream connectivity costs, equipment costs, field labor, shop costs, support costs and maintenance capex, then a low advertised consumer price can leave little room for error. The public record for Biartel shows service breadth, but not unit economics.

Without disclosed ARPU, churn, customer count, installation cost, gross margin, debt, capex or supplier terms, the right conclusion is cautious: the company shows evidence of demand and operating relevance, but not yet evidence of durable pricing power.

Identity points to Biartel, not a cloud-scale network

The entity should be read through its public Biartel identity. The legal notice on the Biartel site names FIBRA A LA PORTA S.L. as the company behind the brand, lists B42565333 as the tax identifier, and places the business at the Biar address also seen in the RIPE NCC member listing and secondary company-data records. The public Biartel pages are written as a local telecom offer: internet in Biar, mobile in Biar, cable television, fixed telephony, bundled packages and services for companies. The contact page repeats the Biar address and phone number and includes customer-consent language that again ties Biartel to Fibra a la Porta, S.L.

That identity matters because it narrows the economic thesis. This is not a public cloud operator with visible global routing depth, a major data-center footprint, disclosed autonomous-system strategy or a large enterprise sales machine. It is a local telecom brand that sells connectivity and adjacent services in a defined Spanish locality. Biartel's own company page says it offers internet, television, telephony and mobile services, emphasizes direct and personalized customer treatment, and describes public offices in the principal areas where it operates.

It also describes technology refresh, social commitment and services such as FTTH, coaxial internet, cable television, IP telephony, virtual switchboards, mobile service over Orange coverage, video-surveillance services, point-to-point links and Wi-Fi hotspot services.

There is a time-line caveat. Biartel's company page states that the operator has a trajectory since 2005. Empresite's company-data page for FIBRA A LA PORTA, S.L. records a founding date in May 2018. Those two statements are not necessarily contradictory, because a commercial activity, related local network operation or brand heritage can predate the present legal vehicle. But the distinction matters. An analyst should not treat the 2005 statement as proof that the current company has been operating under the same legal, capital and customer structure since that year.

The safer reading is that the public brand claims a longer local telecom history, while secondary corporate data identifies the present legal company as younger.

The RIPE NCC member page adds a different layer of identity. It lists FIBRA A LA PORTA, S.L. as a RIPE NCC Local Internet Registry, with the same Biar street address and Spain as the serviced area. That is a meaningful operational signal. RIPE membership can support IP-resource administration and gives the operator a formal relationship with the regional internet registry. In a sector where IPv4 scarcity, address stewardship and network administration matter, this is more than marketing decoration. It shows that the company has taken at least one formal step associated with operating an internet service provider.

But the RIPE listing should not be overread. It does not disclose the company's revenue, margin, customer count, prefixes, traffic volume, upstream providers, routing resilience or peering arrangements. It proves a registry relationship and public member identity, not scale. The distinction is central to the economic judgment: FIBRA A LA PORTA looks real and locally anchored, but its public evidence supports a small access-provider case rather than a cloud-scale network-control case.

The business model is local bundling around a small access footprint

Biartel's published offer is built around the bundle logic common to local telecom operators. The internet page presents fiber service in Biar, with a stated top service of up to 1000 megas and a claim of full fiber coverage in the urban center. The site lists a 500-mega internet tariff at 23.99 EUR per month including VAT and an internet-plus-TV 1000-mega tariff at 39.82 EUR per month including VAT. The commercial page emphasizes no commitment period, router and Wi-Fi equipment, technical support and installation. For a household, that is a straightforward alternative to a national bundle.

For Biartel, it is a way to attach recurring revenue to a local access network and customer-support relationship.

The mobile page extends the bundle. Biartel offers mobile tariffs using Orange coverage and publishes an example of 150 minutes plus 3 GB at 6.90 EUR per month including VAT, with additional data options and customized tariffs. The same page promotes CONECT@Free, described as free mobile internet in Biar for Biartel mobile customers after activation at the office. This is a local-retention device more than a generic national mobile proposition. If a customer's mobile plan carries extra value inside the town, the operator has a small but visible way to connect mobile resale to local loyalty.

The television page adds another anchor. It describes more than 100 channels and a standalone TV tariff of 22.61 EUR per month including VAT, plus the internet-plus-TV bundle. Television can be hard for small operators because content packaging and channel distribution add complexity, but it also provides a reason for older households or multi-room homes to keep the operator. Biartel's page says its TV service can be watched on all televisions in a home without a monthly extra cost. That kind of practical feature can matter in a town market where the operator's sales pitch is convenience and familiarity rather than novelty.

Fixed voice and business services round out the model. The fixed-telephony page lists line and flat-rate options, including national fixed and mobile minute allowances, international fixed-line calling options, call forwarding and virtual-switchboard support. The business page is broader: high-speed fiber, SHDSL, VPN, dedicated lines, traditional and IP telephony, numbering, cloud-labeled services, dedicated servers, hosted machines, backup, IP cameras and multiple mobile lines.

The published copy is marketing material, not a contract schedule, but it shows how the operator wants to move beyond consumer broadband into SME continuity and managed services.

The economic logic is clear. A single-product local ISP can be exposed to price comparison. A bundled local operator can try to increase revenue per customer, reduce churn and spread support costs across more services. If Biartel can sell the household internet line, the TV package, the fixed line and the mobile line, a competitor has to displace a relationship rather than one tariff. If Biartel can also serve local businesses with backup, voice and tailored connectivity, it gains a higher-value layer that may be less sensitive to consumer-advertising discounts.

The weakness is that the same breadth can mask dependency. Mobile service over Orange coverage means Biartel is not the radio-access network owner. Television may involve content and platform inputs. Business services may require equipment, hosting, upstream connectivity, third-party software and technical staff. Bundling improves the customer relationship, but it can also stack wholesale and operational obligations. Without gross-margin disclosure by product line, the public cannot know which services are profitable, which are retention tools and which are mainly defensive.

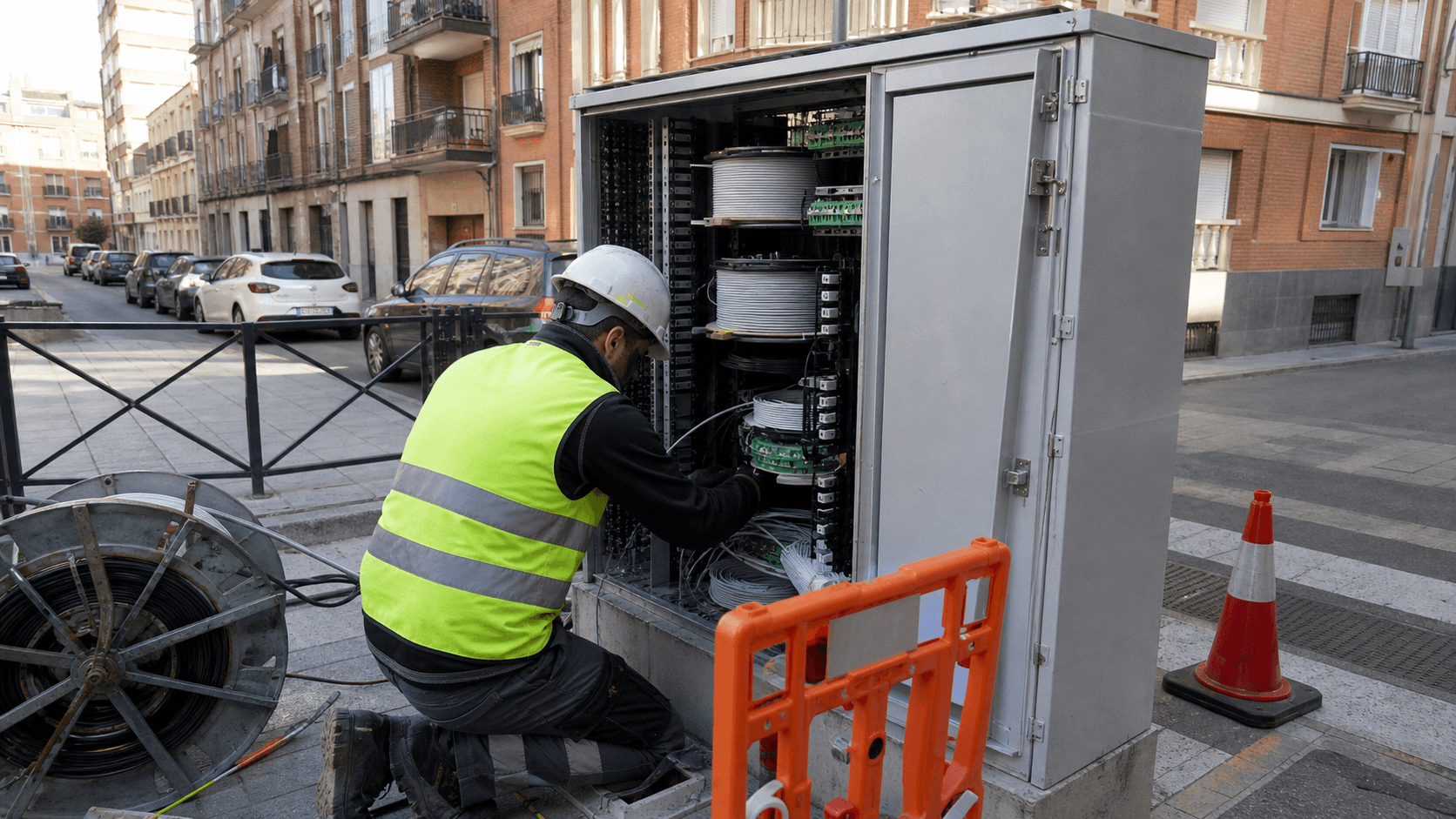

Network evidence supports an access operator, not a public peering platform

The public network evidence is supportive but modest. The strongest direct network signal is the RIPE NCC member listing identifying FIBRA A LA PORTA, S.L. as a Local Internet Registry serving Spain. In practical terms, LIR status can support IP-address administration and a more formal relationship with internet-number resources than a pure reseller would have. It indicates that the company has taken steps associated with managing a network or at least managing registry resources for network operations.

However, public signs of broader internet-network presence are limited. Exact PeeringDB searches for FIBRA A LA PORTA and for Conecta-3 did not return a matching public network profile. That does not prove the company lacks transit, private interconnection or route control; many small operators buy upstream connectivity without maintaining a visible PeeringDB presence. It does mean the public record does not support a claim that FIBRA A LA PORTA is a known public peering entity with a disclosed exchange-point footprint, traffic policy or settlement-free peering strategy.

The company's own web presence also should not be confused with its access network. Public DNS and hosting signals show the Biartel website resolving through an external hosting environment associated with IONOS, and the domain's mail exchange records point to IONOS mail servers. That is normal for a small business and says almost nothing about the company's customer network. It does, however, reinforce the need for discipline: the public-facing website infrastructure is not evidence of proprietary backbone scale.

The relevant network evidence for the company would be customer access plant, upstream connectivity, routing assets, assigned resources, resilience design and enterprise service performance, none of which are fully disclosed publicly.

The Spanish market makes this distinction important. Fiber access is now widely deployed, and national operators have strong fixed and mobile footprints. When fiber coverage becomes ordinary, the value of a local operator depends less on saying "we have fiber" and more on whether it controls enough of the customer experience to create reliability, speed of repair and retention. A local provider can still matter if it owns or controls local plant, has efficient field operations, resolves faults quickly and carries enough upstream resilience to avoid becoming fragile.

But if it is mainly retailing commodity inputs, its differentiation narrows.

The RIPE context adds another layer. RIPE NCC has documented IPv4 exhaustion and the transition to waiting-list allocation for small address blocks. For a small ISP, address administration is operationally valuable because IPv4 is scarce and customer demand has not disappeared. But scarcity cuts both ways. Existing resources can be useful; acquiring or expanding resources can be expensive or slow. If Biartel has enough address capacity for its growth, that helps. If it must rely heavily on carrier-grade NAT, transfers or additional upstream arrangements, customer experience and cost can be affected.

The public record does not tell us where FIBRA A LA PORTA sits on that spectrum.

Network-resource evidence therefore supports a cautious middle position. The company is not merely a marketing website; RIPE membership and the service pages point to a real ISP-like operating role. But there is not enough public evidence to classify it as a network platform with visible routing advantage. The likely thesis is local access economics, not internet-core economics.

Pricing shows useful demand but little room for error

Biartel's consumer pricing is credible for a local market, but it does not obviously reveal excess margin. A 500-mega internet service at 23.99 EUR per month including VAT and a 1000-mega internet-plus-TV bundle at 39.82 EUR per month including VAT are understandable offers for households comparing connectivity options. They are not premium prices in a national European context. A customer can look at those numbers and see affordability; an analyst should look at them and ask how much contribution remains after VAT, installation, router cost, local maintenance, upstream connectivity, support, billing, churn, bad debt and overhead.

The no-commitment language is commercially attractive. It lowers the customer's psychological barrier to signing up and can help a local operator compete against larger brands. But it also weakens one form of contract durability. If customers are not locked into a long commitment period, retention must come from service quality, local support, habit, bundled convenience or switching friction. That can be a healthy model if the operator truly delivers better service. It can be risky if price-led competitors periodically target the town with aggressive offers.

The mobile price points create a similar tension. Biartel's mobile offer starts at low monthly levels and uses Orange coverage, which gives customers access to a national radio network without Biartel owning one. The economic upside is obvious: a small fixed operator can participate in mobile bundles and defend household share. The downside is that mobile margin depends on wholesale terms and usage economics that are not publicly disclosed. If customers use little data and value local billing, the product can be profitable or at least retention-positive.

If wholesale terms are tight and customers demand more data for the same price, mobile can become a thin-margin necessity.

Television adds another margin question. A standalone TV tariff at 22.61 EUR per month including VAT and the inclusion of more than 100 channels give the operator a way to anchor households. But television can bring content costs, platform support, set-up work and customer-service burden. The public site does not disclose channel-cost structure, licensing terms, subscriber counts or churn. It is therefore impossible to know whether TV is a profit center, a retention tool, or a bundle component that protects broadband revenue.

The business-services page points to potentially better economics. SMEs may be willing to pay for uptime, backup, VPN, dedicated connectivity, voice continuity, security cameras or tailored support. A local provider that knows business premises and can respond quickly may command more trust than a national call center. The issue is proof. The public page lists capabilities, but not signed contract lengths, SLAs, reference customers, enterprise ARPU, service-level penalties, gross margin or concentration.

A few larger local business customers could be very valuable, but they could also create concentration risk if one customer represents a large share of revenue.

The published tariffs therefore support demand, not profitability. They show that Biartel has a coherent retail offer and a plausible way to serve Biar households and businesses. They do not show whether the company earns enough on those services to fund network upkeep, staff, customer acquisition and future upgrades without relying on favorable supplier terms or owner support.

Costs sit in field operations, wholesale inputs and customer support

Small telecom operators carry costs that are easy to understate from outside. The visible product is a monthly service fee, but the operating burden includes installation visits, routers, optical-network terminals, drop-cable issues, in-home Wi-Fi problems, billing systems, customer care, outage response, van time, pole or building access, network electronics, upstream connectivity, replacement equipment, regulatory administration and periodic technology refresh. A local operator's strength is its proximity; the cost of that strength is labor intensity.

Biartel's own public pages make support a core part of the offer. The company highlights personalized treatment, local offices, tight response times and technical-support channels. This is economically meaningful. Support quality can be a genuine differentiator against remote national operators, especially for older customers, SMEs and households that value continuity over the absolute lowest price. It can also be expensive. If the company has only a small staff, each support spike matters. A storm, cable cut, equipment failure or regional outage can consume management and technician time quickly.

The public record does not disclose staffing mix, outsourced field arrangements or fault rates.

Capital needs are another key issue. A local fiber network requires electronics, passive infrastructure access, maintenance and upgrade cycles. Even where the civil works are already done, capacity planning does not stop. Customers expect higher speeds over time, Wi-Fi expectations rise, business customers need more resilience, and security standards improve. If Biartel owns meaningful local plant, it has an asset but also a maintenance and reinvestment burden. If it relies more heavily on third-party infrastructure, its capex burden may be lower but its control and margin may also be weaker.

Wholesale inputs sit behind several products. Mobile service uses Orange coverage, so Biartel depends on mobile wholesale arrangements or an intermediary. TV may depend on content and delivery arrangements. Business cloud, server or backup offerings may rely on upstream hosting, colocation, software or connectivity suppliers even if Biartel manages the customer relationship. Fixed internet depends on upstream capacity and, depending on the local access structure, potentially on rights, ducts, poles, electronics suppliers and backhaul. None of these dependencies is unusual.

The economic question is whether the operator has enough scale and contract quality to buy well.

Public policy can help with capital in some contexts, but it does not remove commercial risk. Nearby local operators in Spain have publicly reported public-support projects for broadband extension, and the Spanish and European policy environment has favored rural and small-town connectivity upgrades. Such programs can improve network reach and reduce some deployment burdens. But subsidies or grants usually address specific projects, not the full operating economics of a company. They can also create future obligations, reporting duties and competitive expectations.

There is no public evidence in the reviewed materials that FIBRA A LA PORTA's current margin profile is subsidy-backed or independently strong.

The cost conclusion is simple: the company may have a useful local niche, but the niche is not costless. The most attractive version of the business is one where local customer density, disciplined support, owned or well-controlled access infrastructure and business-service revenue produce stable contribution. The weaker version is one where low retail tariffs, wholesale input costs and support intensity leave little retained cash for upgrades.

Supplier dependence is the central margin variable

For FIBRA A LA PORTA, supplier concentration is likely more important than headline customer demand. Public demand evidence is visible: service pages, tariffs, contact details and a local brand. Supplier economics are mostly hidden. The company uses Orange coverage for mobile, appears to offer a television product, sells business services that may depend on upstream hosting or network partners, and must connect its local customers to the wider internet. If any of those input costs rise faster than retail ARPU, the margin story weakens.

Mobile is the clearest example. A local operator can defend fixed broadband by selling mobile under its own brand, but it rarely controls the mobile network. That makes wholesale price, usage limits, data growth, handset support and customer expectations central. Spanish consumers have become accustomed to large data allowances and aggressive bundle pricing from national and low-cost operators. If Biartel's mobile offer is used mainly by loyal local customers with modest usage, it may support retention. If customers demand national-market data allowances at national-market prices, the product becomes more exposed to wholesale terms.

Television has a similar structure. The public offer of more than 100 channels can be valuable for household stickiness, but channel packaging, rights and platform support can reduce margin. A national operator can spread content and platform costs across a large subscriber base. A small operator must either buy through a platform, negotiate at smaller scale or keep the product simple enough to avoid support overload. The public pages do not disclose enough to assess whether TV is a high-margin service, a break-even loyalty product or a necessary defensive feature.

Upstream connectivity and infrastructure access are also live issues in Spain. Sector reporting has recently focused on the cost and regulatory treatment of access to incumbent infrastructure, including ducts and related passive assets. Even where a local operator has its own last-mile plant in a town, it may still depend on backhaul, upstream transit, equipment vendors and interconnection arrangements. A small company with limited purchasing power can be squeezed if supplier costs rise or if expansion requires access to assets controlled by larger operators.

The RIPE membership may reduce some dependency by giving FIBRA A LA PORTA its own registry relationship, but it is not a full answer. Resource administration helps; traffic still has to move, customers still need installation and support, and retail services still depend on suppliers. In modern fixed-mobile bundles, the retail brand often captures the customer while the economics are divided among several upstream providers. The strength of the retail relationship matters only if the operator keeps enough gross margin after those suppliers are paid.

This is why the most important undisclosed documents would be commercial, not promotional: mobile wholesale agreements, TV platform terms, backhaul and transit contracts, fiber-access rights, equipment leases, debt schedules and business-customer service agreements. The public case cannot prove resilience without them. A small operator can be valuable precisely because it is local, but locality does not protect it from supplier economics.

Customer concentration is hidden, so contract durability is unproven

The published Biartel material suggests two customer groups: households in Biar and local businesses needing connectivity and communications support. Both groups can be attractive. Households provide recurring revenue and word-of-mouth density. SMEs can provide higher ARPU and a greater willingness to pay for rapid support, voice continuity, VPN, backup, security cameras or tailored services. The risk is that the public record does not disclose the mix.

Customer count is the first missing fact. The site states service coverage and tariffs, but not the number of active fiber customers, TV subscribers, mobile lines or business accounts. A local access provider can look stable from outside while having very different economics depending on penetration. If the addressable town is small and customer penetration is high, maintenance costs can be spread efficiently across a dense base. If penetration is modest, the same local fixed costs can consume a larger share of revenue. Without subscriber numbers, neither case can be proven.

Churn is the second missing fact. No-commitment offers are appealing, but they shift the burden of durability onto satisfaction. A low churn rate would show that local support, bundled convenience and the town relationship are working. A high churn rate would show that the operator is exposed to price promotions or service-quality comparisons. Public tariffs cannot answer this. Even customer reviews would have to be treated carefully because they can be selective and unrepresentative; the stronger evidence would be cohort retention, disconnect reasons and win-back rates.

Contract length matters more for business customers. If Biartel has multi-year agreements with municipal, industrial, hospitality, retail or professional-service customers, the economic profile improves. Business customers can make the operator part of their operating base. But if business revenue is project-based, one-off installation work or small monthly lines with easy switching, the durability is weaker. The public business page lists many possible services, but does not name customers or disclose service-level commitments. That is normal for a small provider, yet it limits outside confidence.

Customer concentration can cut both ways. A few important SME customers can lift revenue, improve reputation and justify technical capability. They can also create risk if one contract accounts for too much profit. Conversely, a broad base of small households can be stable but low-margin. The best public evidence would be a balanced mix: dense household penetration, low churn, growing mobile and TV attachment, and a set of business contracts large enough to add margin but diversified enough not to threaten the company if one customer leaves.

Until those facts are known, contract durability remains an assumption. The Biartel brand and local-service promise may well produce loyalty. The public record does not yet prove how much loyalty exists, how it is monetized, or whether it survives aggressive national pricing.

Competition comes from national bundles and realistic substitutes

The competitive threat is not theoretical. Spanish telecom is a mature, fiber-heavy market with large national operators, low-cost challengers and wholesale-backed brands. Recent sector reporting attributed to CNMC data shows high fixed-broadband fiber penetration, heavy concentration among major operators and continued pressure around mobile and fixed bundles. In that setting, a small local operator cannot rely on fiber availability alone as a differentiator. Many customers can obtain fiber, mobile and television bundles from larger brands with extensive advertising budgets and national support structures.

Movistar, MasOrange, Vodafone, Digi and other national or low-cost brands create price and bundle pressure. They can advertise convergent packages, use national mobile networks, spread platform costs across millions of users and absorb short-term promotional discounts. They also have weaknesses: call-center friction, slower local fault resolution, less personalized treatment and sometimes complicated contract terms. A local operator like Biartel can compete where customers value immediacy and trust more than a headline discount. It is vulnerable where customers value only price, speed and brand familiarity.

Fixed wireless and wholesale access are additional substitutes. In areas where fiber is incomplete, fixed wireless can serve as a practical alternative. Where national fiber is present, wholesale-backed providers can enter without building every asset from scratch. Mobile broadband can also substitute for some low-usage households, especially when 5G coverage improves. For businesses, cloud-managed services, national connectivity providers and IT integrators can replace local managed-service offers if the local provider does not maintain quality and credibility.

Biartel's best defense is local integration. A customer who uses Biartel for internet, TV, fixed voice, mobile and business support has more friction than a customer who only buys broadband. A small business that depends on Biartel for voice numbering, backup connectivity and site-specific troubleshooting is less likely to switch for a small monthly saving. The company's public pages clearly point toward this defense: bundles, business services, local support and multiple service categories.

The problem is that larger competitors can copy the visible parts of the offer. They can sell bundles, include mobile, add TV, advertise business support and offer temporary discounts. They may not replicate local office trust, but they can reduce the customer's willingness to pay for it. If a household believes all fiber is the same, Biartel becomes a price-taker. If the household believes Biartel solves local problems faster, the company has a moat of service rather than infrastructure scale.

That distinction also affects acquisition value. A larger regional operator might value Biartel if it brings dense local customers, controlled infrastructure, low churn and a respected brand. It would value the company less if customers are low-margin, supplier-dependent and easily moved by national promotions. The public materials are consistent with a potentially useful local franchise, but they do not prove the franchise's depth.

Regulation and public policy cut both ways

Spain's policy environment has supported broadband extension, rural connectivity and competition, which can help small operators in underserved towns. Public programs and European funding have played a role in extending broadband in many municipalities, and sector data continues to distinguish between urban and rural coverage quality. This background matters for FIBRA A LA PORTA because small-town operators often emerge where national operators historically under-served local demand or where local execution can be faster and more attentive.

Public policy can create opportunity. If rural or smaller-town households need better service and local providers can deploy or maintain access networks efficiently, a small operator can win customers before national competitors focus on the area. Policy support can reduce some deployment costs or make local projects viable. Regulatory pressure can also keep wholesale markets open enough for smaller retail brands to offer mobile or fixed services.

But policy also creates exposure. Telecom is regulated, documented and technically demanding. Operators must manage consumer rights, privacy, emergency and numbering issues where relevant, lawful-interception and data obligations where applicable, network security expectations, billing transparency and registry administration. A small staff must carry a compliance burden that does not scale down perfectly with revenue. RIPE membership itself brings fees, policies and operational responsibilities. These are manageable costs for a capable operator, but they are still costs.

Infrastructure regulation is another swing factor. If access to incumbent ducts, poles or related passive infrastructure becomes more expensive, expansion economics can worsen. If wholesale access remains available and fairly priced, small operators can extend or maintain networks more efficiently. If public funding favors large-scale national projects, local operators may face stronger competition in their own towns. If funding supports local execution, they may benefit. The public record does not show which of these scenarios dominates for Biartel's specific network.

The regulatory point is therefore balanced. FIBRA A LA PORTA operates in a market where public policy recognizes the need for connectivity, but connectivity policy does not guarantee company-level profitability. The operator still has to buy well, maintain service, fund upgrades and retain customers in a competitive market.

Unofficial signals help frame demand, not prove economics

There are useful public signals around Biartel, but they should not be upgraded into hard evidence. A local telecom website with active service pages, retail tariffs, a legal notice, a contact office and a RIPE NCC member listing is stronger than a dormant or vague company profile. It shows a customer-facing operation that has enough public presence to sell, support and be contacted. The same is true of the business-services pages: even if every listed service is not equally important, they show the commercial direction the company wants customers to understand.

The Conecta-3 connection should be handled carefully. The RIPE member listing for FIBRA A LA PORTA uses a contact email at conecta-3.es. Conecta-3's own public pages describe a separate telecom brand operating from Pinoso and nearby areas under CONECTA-3 TELECOM, S.L. with a similar portfolio of internet, mobile, television and business services. That is relevant as an administrative and market-context signal, and it may point to shared know-how, relationships or operating style. It should not be treated as proof that Conecta-3's customers, revenues, grants or infrastructure belong to FIBRA A LA PORTA.

Secondary company-data sources are also useful but limited. Empresite identifies FIBRA A LA PORTA, S.L., its CIF, address, activity, employee count and revenue band. Such sources are helpful for triangulation, especially when they align with the company's own legal notice. They are not a substitute for audited accounts, management interviews or official filings that disclose margins and balance-sheet strength. A revenue band between 0.6 million and 1.5 million EUR, if current and accurate, would imply a small business that must manage overhead carefully. It does not reveal profitability.

Searchable peering and DNS signals must be kept in their lane. The absence of an exact PeeringDB profile is not evidence of no network. External hosting of the website is not evidence of no ISP operations. RIPE membership is not proof of strong peering. Each signal answers only a narrow question. Together, they support a sober view: Biartel appears to be a real local provider with registry status and service breadth, but not a publicly visible scaled network platform.

What would change the judgment

The current judgment is cautiously positive on operating reality and cautious on economic defensibility. FIBRA A LA PORTA, S.L. appears to have a real local telecom brand, a legal identity tied to Biartel, published services, local contact points and RIPE NCC member status. That is enough to treat the company as more than a listing. It is not enough to conclude that it has durable margins, pricing power or strategic scarcity.

Several facts would change the judgment materially. The first would be audited or management-disclosed financials showing stable revenue growth, gross margin, EBITDA, operating cash flow and manageable debt. A small local operator can be attractive if it consistently turns local recurring revenue into cash. It is far less attractive if low tariffs and supplier costs absorb the economics. Even a simple split between consumer broadband, mobile, TV, fixed voice, business connectivity and managed services would improve confidence.

The second would be subscriber and churn data. Household fiber penetration in the served area, TV attach rate, mobile-line attach rate, business-account count, churn by cohort and average revenue per account would show whether Biartel's local promise actually changes customer behavior. The best evidence would be low churn without long commitment periods, because that would mean customers stay voluntarily. The weakest evidence would be high churn hidden by constant promotions.

The third would be infrastructure-control evidence. Details on owned fiber, leased fiber, duct or pole rights, backhaul arrangements, network electronics, resilience design, upstream transit, ASN use, prefix holdings, IPv4 position and any internet-exchange or private-interconnection relationships would separate a controlled local network from a thin retail layer. RIPE membership is a useful starting point, but infrastructure control is where economic power is tested.

The fourth would be supplier diversification. If Biartel has favorable mobile wholesale terms, resilient upstream connectivity, manageable TV-content costs and multiple vendor options, the business is better protected. If it relies heavily on one wholesale mobile path, one upstream network, one content platform or one equipment vendor, the company is more exposed. Supplier concentration can quietly decide margin even when customers are satisfied.

The fifth would be enterprise-contract evidence. Multi-year SME contracts, municipal or institutional customers, managed service agreements and documented service-level performance would strengthen the case that Biartel is not only a household fiber seller. Enterprise continuity services can justify local support and technical capability. But they only matter economically if they are recurring, profitable and diversified.

The sixth would be capex visibility. A plan for network upgrades, equipment replacement, customer-premises equipment, security hardening and capacity expansion would show whether the company can fund the service quality it advertises. Small operators can be resilient when they reinvest steadily. They become fragile when they postpone upgrades to preserve short-term cash.

Until those facts are available, the cleanest conclusion is that FIBRA A LA PORTA, S.L. has a plausible local-service advantage but unproven economics. The Biartel offer is coherent: fiber, mobile, TV, fixed voice, packs and business services in a defined town market. The company has legal and registry signals that support real operations. The public evidence does not show a differentiated peering position, disclosed network scale or audited profitability.

For a reader tracking regional ISP economics, the subject is worth watching because the upside and the risk are the same: a local operator can become indispensable to its community, but only if local trust creates enough retained margin to pay for suppliers, support and the next network upgrade.