Summary

- EWK Herzogenbuchsee AG is best understood as a local infrastructure utility with a communications line of business, not as a standalone broadband growth company. Its strategic value is local: preserving relevance in Herzogenbuchsee and nearby municipalities, using utility assets to lower fibre construction friction, and keeping customer relationships close.

- The communications model separates local access economics from product-scale economics. EWK owns and operates local access infrastructure and basic signal distribution, while GA Buchsi AG and Quickline provide much of the consumer-facing internet, television, fixed-line, and mobile product layer.

- The available evidence supports a defensible local network, but not a high-growth telecom story. EWK reports near-complete HFC-to-FTTH conversion, a 52.52 percent holding in GA Buchsi AG, CHF 4.53 million of communications fixed assets in 2025, and modest local customer growth in its own supply area in 2024, while the broader GA Buchsi customer base showed pressure in cable TV and fixed telephony.

- The investment case turns on post-build economics. If fibre conversion reduces maintenance costs, raises penetration, and lets EWK or GA Buchsi retain profitable households and SMEs, communications can support the multi-utility. If retail margins remain with larger partners and local take-up stalls, EWK's network remains useful but financially capped.

Management's Incentive Is To Stay Useful Where Scale Does Not Travel

The management problem for EWK Herzogenbuchsee AG is not whether fibre is important. The market has already answered that. Swiss households expect fixed broadband, reliable television, mobile data, and low-friction service recovery. Companies in smaller towns also expect connectivity to behave like a basic utility, not like a speculative technology product. The harder question is whether a municipal utility below national telecom scale can still earn a useful role when the most powerful economics in communications sit with national brands, mobile spectrum holders, cloud platforms, large peering networks, and software-heavy product bundles.

That is the right starting point because the economic incentive is defensive before it is expansive. EWK does not need to become a national network operator to justify its communications activity. It needs to remain relevant in the part of the value chain where proximity matters: access network construction, customer trust, fast repair, use of existing conduits, local building knowledge, and a visible relationship with municipalities and households. The company says its core mission is secure, sustainable, efficient, and economic supply of energy, water, and communications. That language matters.

It frames broadband as part of a utility compact rather than a venture-backed subscriber land grab.

The trade-off is that local relevance can be confused with pricing power. A household may prefer the local utility because staff know the street, the house connection, and the service history. That preference does not automatically allow a higher broadband margin if national competitors can offer converged mobile, fibre, television, and discount bundles. Nor does it give EWK the economics of a hyperscale platform, where each additional customer can often be served with a much lower marginal cost once software and infrastructure are in place.

EWK's network requires field work, civil infrastructure, maintenance, customer visits, and depreciation.

So the central economic question is who pays, who benefits, and who carries the downside. The household pays for access and product bundles. GA Buchsi AG and Quickline benefit from retail product reach. EWK benefits from owning local access, keeping the customer relationship near the municipality, and sharing in GA Buchsi through its holding. The downside sits with EWK when capital expenditure, asset depreciation, operational failures, or weak penetration reduce the return on a network that cannot easily be moved somewhere else.

That makes EWK a useful case study in regional ISP economics. It is neither a pure infrastructure wholesaler nor a national retail challenger. It is a local utility trying to protect a valuable place in the chain while the market around it scales elsewhere.

Identity And Boundary: A Local Utility With A Telecom Line, Not A Cloud Platform

EWK Herzogenbuchsee AG is anchored in Herzogenbuchsee in the canton of Bern. Its own company materials describe it as the provider of energy, water, and communications services for Herzogenbuchsee and surrounding municipalities. Its headquarters are listed at Eisenbahnstrasse 2 in Herzogenbuchsee, and its public materials emphasize electricity, gas, water, wastewater-related mandates, district heating, and communications rather than one single telecom product.

The company states that it has around 40 employees; its 2025 annual report says that by the start of 2026 it had 44 monthly salary employees and seven hourly employees, while the statutory note reports that average employment did not exceed 50 full-time equivalents.

That size is central to the analysis. EWK is large enough to maintain real assets and specialist staff, but small enough that every capital decision matters. The company's 2025 annual report shows total assets of CHF 29.49 million, equity of CHF 18.91 million, and net revenue of CHF 20.32 million. Those figures are meaningful for a municipal utility, but they are tiny beside national telecom groups or cloud infrastructure companies. EWK cannot win by outspending them. It must win by making local infrastructure ownership and multi-utility customer contact more efficient than an outside provider can make it.

The ownership boundary also matters. The sole shareholder is the municipality of Herzogenbuchsee. That creates a different incentive structure from a private telecom operator seeking maximum subscriber growth or a quick exit. A municipal shareholder can value security of supply, local service quality, dividend continuity, local control, and long-term infrastructure renewal. But municipal ownership can also limit appetite for high-risk growth. The 2025 annual report says EWK wants to preserve independence while using cooperation to gain cost advantages and know-how.

That is a sensible posture for a small multi-utility, but it implies that communications is part of a portfolio strategy, not a standalone attempt to dominate the Swiss broadband market.

The boundary of the communications business is narrower than the brand experience customers may see. EWK is responsible for local communications access and basic distribution in its area, while internet, television replay, fixed telephony, and mobile offers are sold through GA Buchsi AG using Quickline products. EWK is therefore exposed to communications economics, but it does not own the whole stack. Its value is strongest in the local access layer, local service layer, and shareholder link to GA Buchsi. It is weaker in national product development, mobile scale, content packaging, and backbone economics.

This boundary is not a weakness by itself. It may be the only realistic boundary for a local Swiss utility. The risk is misreading the company as a miniature cloud or national telecom platform. It is better read as a local infrastructure allocator that must decide how much capital to put behind communications when other regulated and essential utility networks also demand investment.

The Communications Business Is A Network Access Business With A Partner Product Layer

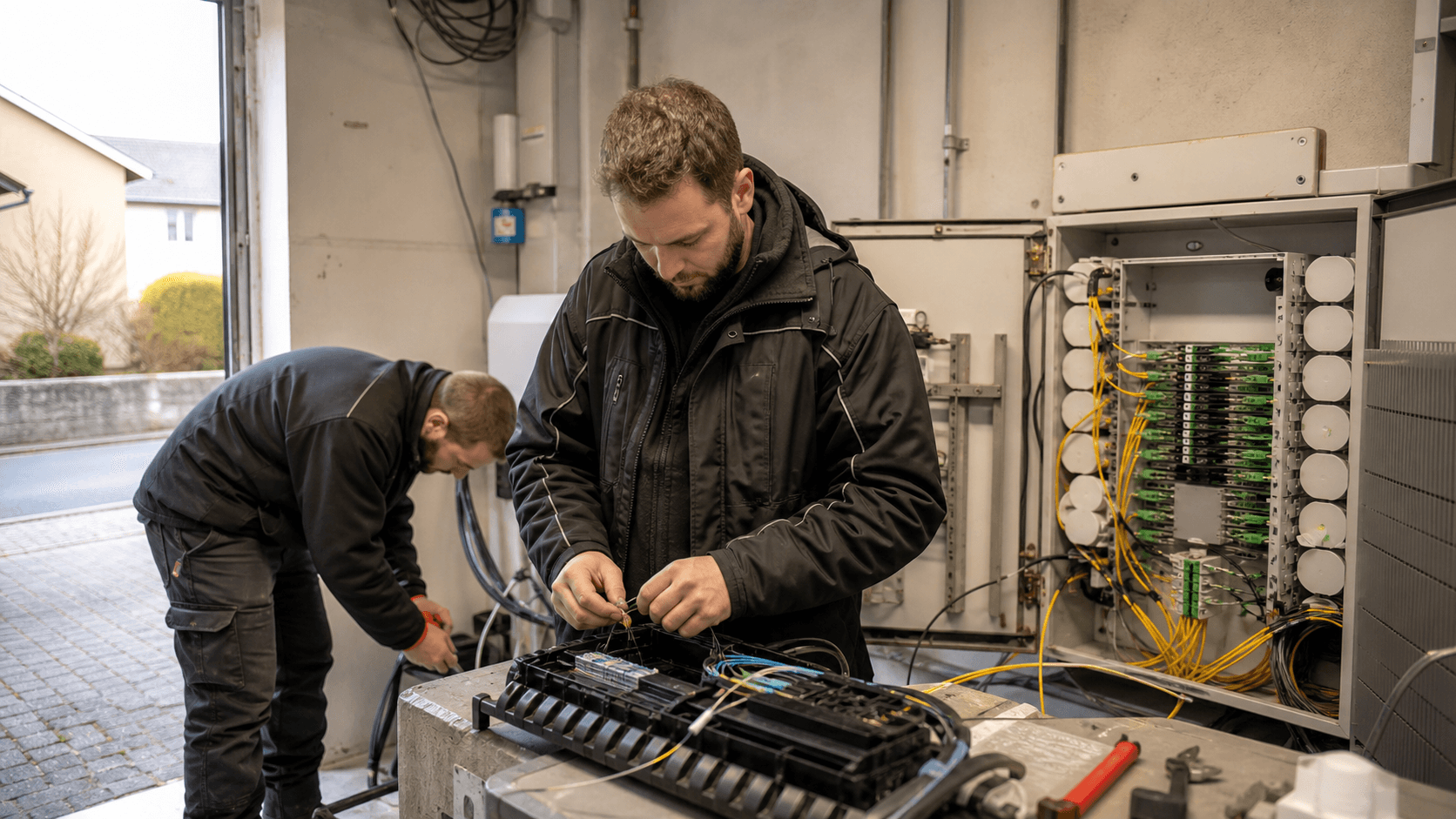

EWK's communications history stretches back to 1974, when its predecessor began distributing radio and television signals through copper cable linked to a community antenna. The original motive was practical and local: reduce rooftop antennas and provide a shared signal service. Over time surrounding municipalities and television cooperatives joined. The company now describes a modern communications network that lets households receive radio and television and access the internet, with fibre-to-the-home construction intended to give all households fast internet and reliable television and radio signals.

The current model has three layers. The first layer is the physical local access network. EWK's materials describe fibre running from a point of presence to fibre distribution, then to the building entry point and optical outlet in the apartment. The company says it uses existing electricity conduits where possible. That is one of the most important economic advantages a multi-utility can have. Civil works are a large part of access network cost.

A utility that already understands ducts, building connections, street works, and local permissions can reduce friction relative to an outsider that must negotiate each step with less local knowledge.

The second layer is basic signal and connection economics. EWK explains that the digital connection gives access to its fibre cable network and includes components such as a transmission fee for construction, maintenance, and operation of the network, plus rights-related fees. It also notes that national radio and television household fees are collected separately by Serafe. The ability to seal a connection if the customer does not want the basic television and radio service is economically relevant because it shows that the network fee is not merely hidden in a broad municipal charge.

It is a service price customers can accept or reject within the rules of the offer.

The third layer is retail telecommunications product packaging. EWK states that additional services such as internet, television with replay, fixed-line telephony, and mobile telephony are not billed by EWK itself but by GA Buchsi AG using Quickline products. EWK co-founded GA Buchsi AG in 2018 after a looser regional association of municipalities, television cooperatives, and EWK decided that a more flexible company was needed. EWK's 2025 annual report records a 52.52 percent holding in GA Buchsi AG with a book value of CHF 525,200.

EWK's anniversary material says GA Buchsi serves around 9,000 customers in surrounding municipalities with a basic radio and television offer and Quickline products.

That structure makes economic sense, but it limits where profit can arise. Local access ownership can support stable network fees, customer retention, and lower field costs. Retail scale, product innovation, mobile integration, and national marketing sit more naturally with Quickline. EWK's management has to defend the local layer while making sure the partner layer remains attractive enough that customers do not defect to national alternatives.

Demand Looks Real Locally, But The Addressable Market Is Narrow

The demand evidence is strongest at the level of necessity. Broadband access has become a household and SME utility. EWK's own communications head, quoted in company anniversary material, describes a stable and fast connection as expected, with outages unacceptable to users. That is a credible description of customer behavior. Work, education, entertainment, administration, security devices, cloud applications, and payment tools have all made connectivity part of everyday service continuity. For a regional utility, that creates a durable reason to stay in communications even if headline growth is limited.

The reported subscriber figures, however, argue for caution. EWK's 2024 annual report gives communication statistics for Herzogenbuchsee, Drei Hoefe, and Seeberg. Cable television connections rose from 3,040 in 2023 to 3,259 in 2024, an increase of 7 percent. Internet subscriptions rose from 2,311 to 2,410, an increase of 4 percent. Internet telephony fell from 1,294 to 1,279, a decline of 1 percent. Those numbers show that local demand can still grow, particularly when the service area changes and fibre conversion continues. They do not show explosive broadband expansion.

The broader GA Buchsi figures are more sobering. In 2024, the annual report shows GA Buchsi cable television customers falling from 6,691 to 6,530, down 2 percent. Internet subscriptions were effectively flat, moving from 5,179 to 5,163. Internet telephony fell from 3,062 to 2,863, down 6 percent. Those movements are consistent with a mature market: fixed internet remains essential, linear television and fixed voice face structural pressure, and customer growth must be won from competitors rather than from first-time broadband adoption.

This matters because local network investment has a fixed-cost character. Fibre conversion, headend cooling, customer portals, operational processes, and maintenance crews are not costless because take-up is modest. A network with 2,410 local internet subscriptions can be strategically important, but it must be judged against the capital tied up in communications assets and the cost of keeping service quality high. EWK's 2025 annual report lists communications assets with a book value of CHF 4.53 million, additions of CHF 671,000, and depreciation of CHF 310,000. In 2024, communications additions were higher, at about CHF 1.15 million.

The addressable market is also geographically constrained. EWK's communications service-area materials refer to Herzogenbuchsee, Drei Hoefe, Seeberg, and related regional networks, while other company material also references Oberonz and Hermiswil in the wider communications context. This is not a market where EWK can simply add the next million customers. Growth likely comes from higher penetration, better product attachment, local municipal or cooperative network absorption, and preventing churn. That is valuable, but it is a different growth curve from cloud infrastructure or national mobile convergence.

Resource-Holder Status Adds Control, Not Standalone Pricing Power

EWK has visible internet-number-resource evidence. RIPE NCC records identify EWK Herzogenbuchsee AG as a local internet registry under the organisation entity ORG-EHA10-RIPE, with the same Herzogenbuchsee address and the Swiss company registration number CHE-105.334.294. RIPE's public member list also shows EWK Herzogenbuchsee AG in Switzerland. In routing database search results, a small IPv4 assignment, 213.221.255.96 to 213.221.255.103, appears with the name GARHNET and a description tied to EWK Herzogenbuchsee.

For investors and operators, that evidence is useful because it confirms that EWK is not only a marketing reseller with no network footprint. It has a recognized resource-holder relationship and historical address space evidence. But the economic interpretation needs discipline. A registry entry does not equal backbone scale, a national peering advantage, or a unique customer moat. The visible assignment is tiny, and RIPEstat routing status for the 213.221.255.96/29 range shows no global visibility for the more-specific block at the query time, with a less-specific 213.221.192.0/18 route originated by AS15600.

AS15600 is registered as QUICKLINE. The aut-num record lists Quickline AG in Nidau and shows major upstream and peering relationships. The record references upstreams including Cogent, Arelion, and Swisscom, and it lists private or public peering relationships with large networks and content platforms such as Google, Amazon, Netflix, Meta, Init7, and others. RIPEstat identifies AS15600 as announced and associated with Quickline, and its announced-prefixes data shows multiple IPv4 and IPv6 prefixes visible globally.

The conclusion is that EWK's resource-holder status supports operational credibility, but the route-scale economics appear to sit primarily with the Quickline environment rather than with EWK as a standalone autonomous network. That is not surprising. Regional cable and fibre operators often benefit from a larger partner's backbone, transit, peering, product development, and network operations capabilities. The partner can spread those functions across many local networks. The local utility supplies the last-mile relationship, access footprint, local maintenance, and municipal legitimacy.

This distinction affects pricing power. If a small business customer in Herzogenbuchsee needs reliable broadband, the visible local access owner matters. If the same customer asks for cloud connectivity, low-latency content delivery, mobile bundles, managed security, or national account pricing, the economics are more likely to depend on Quickline and other larger providers. EWK can still be strategically important without capturing the full margin of the communications value chain.

Revenue Quality Depends On Bundled Utility Trust More Than Subscriber Growth

EWK does not disclose a clean communications segment income statement in the public annual reports reviewed. That limits any attempt to calculate standalone broadband margins. The company reports net revenue of CHF 20.32 million in 2025, down from CHF 23.51 million in 2024, with revenue from networks of CHF 9.22 million, energy trade revenue of CHF 7.78 million, services revenue of CHF 2.77 million, and own work of CHF 533,000. EBITDA was CHF 3.01 million, EBIT was CHF 1.26 million, and annual profit was CHF 897,000. The 2024 figures show EBITDA of CHF 2.67 million, EBIT of CHF 919,000, and annual profit of CHF 798,000.

Those figures show an economically functional utility, not a high-margin software business. The 2025 EBITDA margin was 14.8 percent and the annual result margin was 4.4 percent. That is compatible with asset-heavy local infrastructure, regulated or politically constrained pricing, and a public-service expectation. EWK's own strategic language reinforces that point. It aims for an appropriate profit at regionally competitive prices, uses cooperation for cost advantages and know-how, and wants to preserve independence.

For communications, revenue quality likely depends less on rapid subscriber additions and more on retention, trust, and multi-utility bundling. A household that knows EWK through electricity, water, or local service interactions may be more willing to stay with the local communications network. A small business may value fast repair and a known local contact. Municipal ownership may reassure customers that the network will not disappear after a change in national marketing priorities. Those are real advantages, but they are customer-stickiness advantages, not proof of superior ARPU.

The public pricing description also suggests constrained upside. EWK separates the digital connection and network transmission fee from additional Quickline products billed by GA Buchsi. That makes the local access fee visible, but it also exposes customers to price comparison. If the access fee is too high, customers can ask whether they need the basic connection. If the retail bundle is too expensive, they can compare Quickline and GA Buchsi offers with national alternatives. The local utility relationship reduces friction, but it does not remove competition.

The best interpretation is that communications revenue can improve the quality of EWK's total utility relationship. It gives the company more touchpoints, supports a broader local service promise, and can share civil infrastructure knowledge with electricity and other networks. It may also provide dividend or equity value through GA Buchsi. But absent segment disclosure, it is not possible to claim that communications is the company's highest-return business. The safer claim is that it is a strategic adjunct to the multi-utility model, with financial value depending on post-fibre operating cost, penetration, and partner economics.

Capital Intensity Is The Main Constraint Below Cloud Scale

The strongest economic argument against overvaluing EWK's communications business is capital intensity. Fibre is durable, useful, and preferred for many fixed broadband use cases, but it is not free. EWK's own materials describe a long transition from copper and HFC toward fibre-to-the-home. The 2025 annual report says the HFC-to-FTTH conversion in Herzogenbuchsee and Seeberg was nearly complete and that the fibre conversion across the GA Buchsi supply territory had been successfully completed.

The 2024 annual report said the final HFC connections in Seeberg and Herzogenbuchsee were to be converted by the end of 2025 so that HFC could be decommissioned in the GA Buchsi territory at the start of 2026.

That investment should reduce future complexity if the old network can truly be retired. Running fewer access technologies can lower maintenance burden, simplify customer installations, reduce fault types, and make retail products more consistent. The economic benefit of fibre conversion therefore appears after the capital cycle, not necessarily during it. The question is whether depreciation and financing pressure fall faster than revenue pressure from competition and product substitution.

EWK's balance sheet shows why this matters. In 2025, total fixed assets were CHF 22.99 million, including CHF 20.24 million of immobile and technical fixed assets. Communications assets alone had a book value of CHF 4.53 million. Total additions across fixed assets were about CHF 3.34 million, and total depreciation was about CHF 1.99 million. Operating cash flow was CHF 3.60 million, investment cash flow was negative CHF 2.63 million, and free cash flow was CHF 969,000 before a CHF 675,000 dividend. Liquid funds at year-end were CHF 155,000.

The 2024 cash flow was tighter. Operating cash flow was CHF 2.42 million, investment cash flow was negative CHF 3.03 million, and free cash flow was negative CHF 608,000 before the same CHF 675,000 dividend. Liquid funds fell from CHF 1.34 million to CHF 61,000. The 2025 annual report openly notes that since EWK's founding in 2000, revenue and staff have grown, fixed assets have tripled, mandates have quadrupled, profit has remained almost constant, and liquid funds have been used up.

That is a clear warning against treating communications growth as costless. Every local fibre build competes with electricity, water, wastewater, heat, IT, and building investments. The communications line may be strategically necessary, but it still consumes capital and management attention. Below national scale, the winning case depends on disciplined construction, shared utility infrastructure, high take-up, and lower maintenance after HFC retirement. Without those, fibre can become a balance-sheet burden even while customers enjoy better service.

Supplier And Upstream Dependence Push Strategic Value Toward Quickline

EWK's communications business is interdependent by design. The company can operate local network assets and maintain customer proximity, but it relies on broader partnerships for products, backbone reach, peering, and retail breadth. Quickline is the most visible partner. EWK's anniversary material describes Quickline as a Swiss provider based in Nidau that develops internet, digital television, fixed-line, and mobile products with 24 independent regional utilities and cable companies.

Quickline's own company page presents itself as a Swiss provider of internet, television, fixed-line, and mobile services and emphasizes the strength of a network of regionally rooted partners.

GA Buchsi sits between local network and national product scale. EWK co-founded GA Buchsi in 2018 after the previous regional association wanted more flexibility and faster decision-making. EWK says it continued business management, operational management, and maintenance for GA Buchsi partner communications networks. That gives EWK operational influence, but it also means the end-customer product proposition depends on GA Buchsi and Quickline remaining competitive.

The routing evidence points in the same direction. Quickline's AS15600 carries the globally visible network identity associated with the larger connectivity environment. Its routing records show upstream relationships and extensive peering that a local utility could not economically reproduce on its own. That is a benefit to EWK's customers because it gives the regional product access to national and international connectivity economics. But it also means strategic value and bargaining power are shared. If Quickline product economics improve, EWK can benefit through customer retention and GA Buchsi.

If Quickline loses relevance against Swisscom, Sunrise, Salt, or future fixed-mobile bundles, EWK's local access quality may not be enough by itself.

This dependence is not only technical. It is commercial. The customer's bill and perception are shaped by product features: internet speed tiers, television replay, mobile integration, customer portal, service bundles, installation experience, and support quality. EWK can influence some of those through local service and GA Buchsi, but it does not own all of them. The local network can be excellent while the retail offer still feels ordinary if national rivals discount aggressively or bundle mobile subscriptions more effectively.

The upside is that EWK avoids trying to recreate functions that require scale. It can focus on the part of the chain where it has a plausible advantage. The downside is that communications economics may be capped by partner terms. The most important undisclosed data would be the effective margin split between local access, GA Buchsi retail activity, and Quickline product economics. Without it, the prudent view is that EWK's supplier and upstream dependence is manageable but material.

Customer Concentration Is Municipal And Regional Even Without Named Accounts

EWK does not need a single named customer concentration to have concentration risk. Its communications market is concentrated by geography and by municipal identity. Herzogenbuchsee, Drei Hoefe, Seeberg, and nearby communities define both the opportunity and the ceiling. The same local characteristics that make EWK trusted also limit diversification. A storm, civil-works disruption, reputation problem, political disagreement, or major competitive campaign in this region would affect a meaningful share of the communications base.

Municipal ownership sharpens the point. The sole shareholder is the municipality of Herzogenbuchsee, and EWK has historically paid dividends while also funding infrastructure. That creates an implicit tension. Residents and local businesses want reliable service and fair prices. The shareholder wants a financially sound utility and an adequate dividend. Management must preserve capital for networks that are essential but expensive. In 2025, after investment and dividend payments, year-end liquid funds were still modest.

That does not imply distress, but it does show why concentrated infrastructure businesses cannot be managed only for subscriber additions.

The customer base is also likely concentrated in household and SME service continuity rather than in large enterprise connectivity. EWK's public communications material is built around digital access, radio and television, internet access, telephony, and regional customer closeness. That is a sound local proposition. It is not evidence of a large wholesale carrier business, hyperscale data center connectivity, or complex enterprise network outsourcing. For smaller firms, the value is practical: fast connection, local accountability, and fewer service interruptions. For households, the value is convenience and trust.

The economic risk is that those customers are price-sensitive even when they value reliability. A household may like local service but still switch if a national operator offers a compelling mobile and fixed broadband bundle. An SME may value local repair but still need specialized cloud, security, or multi-site services from a larger provider. If customers view internet access as interchangeable, EWK's local advantage becomes a churn-reduction tool rather than a pricing tool.

The best way for EWK to reduce concentration risk is not to pretend it can become national. It is to increase the economic density of the region it already serves. That means higher fibre penetration, more multi-service adoption through GA Buchsi, useful SME support, local contracts where service continuity matters, and careful expansion through nearby network takeovers or mandates only when the economics are clear. The 2018 Drei Hoefe network takeover and the 2024 Seeberg acquisition show that adjacent growth can happen. The question is whether those additions produce durable margin after conversion costs.

Competition And Substitutes Keep The Ceiling Low

Switzerland is not an underserved broadband market where a local fibre operator can assume customers have no alternatives. ComCom's latest activity reporting describes Switzerland as having very strong broadband infrastructure and competition between infrastructures and services. It reports fixed broadband subscriptions equivalent to 46.4 percent of the population at the end of 2024, one of the stronger positions among OECD countries, and roughly 1.5 million fibre-to-the-home or fibre-to-the-building subscriptions, about 35 percent of broadband subscriptions.

It also describes near-complete modern mobile coverage, with 4G and 5G widely available and advanced 5G reaching a large share of the population.

That market context puts pressure on EWK. Customers are accustomed to strong networks. A local provider does not get credit merely for offering broadband. It has to offer a reason to stay. EWK's reason is local reliability, field knowledge, municipal familiarity, and the Quickline/GA Buchsi product set. Those are credible reasons, but they operate inside a crowded market.

The substitutes are several. Swisscom remains a powerful national fixed and mobile provider, and EWK's own anniversary account says Swisscom rejected EWK's request for a joint fibre build before EWK decided to invest independently. That anecdote is strategically revealing. Swisscom's refusal pushed EWK toward independent investment, giving local control but also placing capex risk on EWK and its partners. Sunrise and Salt add further fixed-mobile pressure, while cable, fibre, and mobile broadband can all compete for household attention depending on address, speed, installation, and promotional pricing.

There is also product substitution within the communications bundle. Fixed voice continues to decline, as EWK's 2024 figures for GA Buchsi and its own local communication area show. Traditional cable television faces streaming and app-based viewing pressure. Internet access remains essential, but if television and voice revenue weaken, the economics of the bundle change. The network must be paid for increasingly by broadband value, not by an older triple-play structure.

This is where cloud competition enters indirectly. EWK is not competing with cloud platforms for local access. But cloud and streaming services change what customers value. They make the broadband pipe more important while taking more of the application-level value away from local operators. Customers pay Netflix, Microsoft, Google, Apple, and many others for experiences that ride over the local network. The local operator must keep investing so those services work well, but it does not automatically participate in the application margin. That is the structural challenge below cloud scale.

Operational And Regulatory Risk Is Shared Across The Multi-Utility Base

EWK's multi-utility model spreads some risk and creates others. Electricity, water, gas, heat, wastewater-related services, and communications can share customer service, civil works knowledge, metering, field logistics, premises access, and management capabilities. That is a real advantage for a small operator. The company itself emphasizes the complementarity of its operating areas and the value of synergies and risk diversification.

At the same time, every utility line brings its own regulatory, technical, and renewal burden. The 2025 annual report says the industry is in transformation, that regulatory requirements are high, and that administrative, technical, and financial effort for utilities is increasing while revenues are strongly regulated and strategic room is constrained. Even when that comment applies broadly to energy and utility operations, it affects communications because management time and capital are shared. A cyber or IT requirement in one area can require investment across the organization.

A building upgrade for the GA Buchsi headend, smart-meter investment, or process documentation work can compete for the same finance and staff capacity.

EWK's 2025 report mentions a review against the federal ICT minimum standard for critical infrastructure and says the technical foundation was basically well built while process documentation still needed work. That is a normal kind of finding for a small infrastructure operator, but it is important. Communications reliability is no longer only about cables and amplifiers. It includes access control, incident response, documentation, vendor management, customer data, portal availability, and network monitoring. A local provider's brand advantage can be damaged quickly if a fault is handled poorly.

There is also public expectation risk. Because EWK is a municipal utility, customers may judge it differently from a remote provider. They may be less tolerant of visible failure because the company is local, familiar, and partly an expression of municipal competence. The same closeness that supports trust raises the reputational cost of outages. The communications head's comment that outages are a "no-go" captures that operating reality.

Regulatory risk is not limited to telecom law. Rights fees, national household media charges, data protection, critical infrastructure expectations, utility accounting, procurement norms, and public-sector oversight can all affect economics. EWK's pricing room is therefore narrower than a simple private-market model would suggest. It must be competitive, politically acceptable, and sufficient to maintain assets. That is a difficult balance, especially when customers benchmark broadband prices against national promotions rather than against the full local cost of resilient infrastructure.

Geopolitical risk is indirect but not absent. EWK is not operating submarine cables or cross-border backbone capacity, but its customers depend on international equipment supply chains, content networks, transit markets, cybersecurity norms, and the resilience of larger Swiss and European connectivity partners. A regional utility cannot control those layers. It can only choose dependable partners, document its own processes, invest in resilient local access, and avoid overpromising independence where the wider internet value chain remains shared.

Unofficial Signals Confirm Familiar Local Advantages, Not Hidden Scale

The informal signals around EWK support the thesis of a serious regional operator with local trust, but they do not reveal hidden national scale. The company's 25-year communications retrospective is unusually useful because it explains why the business exists: community antenna origins, regional cooperation, the shift from copper and HFC to fibre, and the decision to create GA Buchsi for faster and more flexible action. It also describes a Quickline shop in the EWK building and EWK's continuing role in management and maintenance of partner networks.

The local event signal is similar. In the 2025 annual report, EWK describes participation in HAGA 2025, a regional exhibition with more than 100 exhibitors, where it presented smart meters and Quickline products of GA Buchsi AG. That is not a financial metric, but it is a practical demand-generation signal. A regional ISP wins partly by being physically present where customers ask questions. National advertising may build brand awareness, but a local exhibition can reduce hesitation for customers who want to know who will answer the phone or come to the premises.

The customer-closeness claims are credible because they match the business model. EWK says it differentiates through knowing customers by name, reacting quickly, focusing on the region, and valuing loyal customers rather than only chasing new ones. These are not claims that create a valuation by themselves. Many local providers say similar things. But they are consistent with a market where the local access owner cannot outspend national operators and must instead reduce churn through service quality.

Unofficially, the most important signal may be what is absent. There is no public evidence in the reviewed materials of an aggressive expansion plan, a large enterprise connectivity push, a proprietary cloud platform, or independent backbone strategy. That absence supports a conservative economic interpretation. EWK is not trying to become something it is not. It is building and finishing local fibre, using a regional retail vehicle, and leaning on Quickline scale for products and network reach.

Those signals should be handled carefully. Local pride, a shop, an anniversary story, and event presence can explain customer retention. They do not prove segment margin, ARPU, churn, wholesale economics, or return on invested capital. The serious analyst should treat them as qualitative support for the local-service thesis, not as substitute financial evidence. The next stage of diligence would need hard customer and margin data.

What Would Change The Judgment

The current judgment is that EWK's communications business is strategically rational and locally valuable, but financially bounded. It can strengthen the multi-utility, protect local relevance, and support resilient service in Herzogenbuchsee and nearby communities. It should not be valued as a high-growth telecom platform without more evidence.

Several facts could improve that judgment. The first would be segment-level profitability showing that communications earns attractive margins after depreciation, support costs, and partner payments. The second would be post-FTTH evidence that capex and maintenance costs fall meaningfully once HFC is decommissioned. The third would be sustained growth in internet subscriptions and multi-service attachment without heavy discounting. The fourth would be low churn against Swisscom, Sunrise, Salt, and other alternatives.

The fifth would be clear evidence that GA Buchsi's retail economics return enough value to EWK through dividends, service fees, or equity value to justify the capital tied up in local access.

The judgment would also improve if EWK demonstrated repeatable adjacent expansion. Taking over or upgrading nearby networks can make sense if the acquired assets are contiguous, ducts and field operations overlap, customers can be moved to fibre efficiently, and partner products are already ready. The Drei Hoefe and Seeberg examples show a path, but each addition must be evaluated after conversion costs. Regional scale helps only if it improves density rather than adding scattered obligations.

There are also facts that would weaken the view. If internet subscriptions flatten after the fibre build, if GA Buchsi customer numbers continue to decline beyond voice and traditional television, if Quickline product competitiveness weakens, or if maintenance costs remain high despite FTTH conversion, communications would look more like a defensive cost center than an earnings contributor. Liquidity pressure or dividend expectations could also reduce investment flexibility. A major outage, cyber incident, or failed process audit would damage the local-trust premium quickly.

For now, EWK's best strategy is disciplined realism. It should treat communications as a core local infrastructure service that protects customer relevance and supports the regional utility compact. It should avoid pretending that fibre ownership alone creates national pricing power. It should use Quickline for scale where scale matters, GA Buchsi for regional product reach, and its own staff for the local work that outside providers find harder to replicate.

That is not a glamorous conclusion, but it is economically coherent. Below cloud scale, the valuable role is not to own every layer. It is to own the layer where local knowledge lowers cost, improves reliability, and keeps customers from seeing broadband as just another interchangeable offer. EWK Herzogenbuchsee AG appears to understand that role. The remaining question is whether the completed fibre cycle can turn that understanding into durable cash generation rather than simply better service funded by a tight local balance sheet.