Summary

- Equinix (Germany) GmbH should be read as a local German operating and resource-control footprint inside Equinix's wider digital-infrastructure platform, not as evidence by itself that the company is a retail ISP or a full managed-network provider. The hard asset is local presence in Germany's interconnection economy, especially Frankfurt, where data center space, power, cloud access, carrier density and DE-CIX proximity create value only if enough customers pay a premium for direct control rather than simpler bundled alternatives.

- The investment case turns on capital recovery. Equinix can justify local German control if cabinets, cross-connects, private cloud links, peering access, smart hands, resilient power and high-density cooling compound into durable customer switching costs. It fails the test if buyers increasingly shift workloads to hyperscale cloud regions, carrier-managed connectivity or lower-cost colocation rivals while Equinix carries the power, cooling, lease, compliance and expansion burden.

The German Footprint Is The Constraint, Not The Brand

The starting incentive is geographic. A company can buy global cloud from a procurement portal, global IP transit from a carrier and managed network operations from a systems integrator, but it cannot avoid geography when latency, data-location policy, power availability and physical interconnection are part of the workload. Germany is a large enough economy to support domestic cloud regions, dense enterprise networking and local recovery infrastructure. It is also a difficult enough market that the company providing the physical layer must win more than marketing visibility.

It must win the right to allocate scarce space, electricity, cooling capacity and operational attention.

Equinix's public German material frames the country as a European interconnection hub and says the company operates data centers in Frankfurt, Dusseldorf, Hamburg and Munich. Its Germany page describes 15 data centers across the country and about 103,000 square meters of colocation capacity. The exact economic boundary of Equinix (Germany) GmbH is not the same as a public segment report: the named German company is visible through RIPE NCC membership evidence, while Equinix's commercial pages speak for the wider Equinix platform. That distinction matters.

The public evidence supports a German resource-holder and local operating footprint. It does not give investors or customers a standalone profit-and-loss account for the German entity.

That makes the capital recovery question sharper. If Germany were a light-touch sales territory, the strategic answer would be simple: sell global platform services into local accounts and book margin centrally. Germany is not that. Equinix's own facility pages describe physical locations, redundancy, power systems, cooling, certifications, security, service options and cloud connectivity. These are fixed commitments. They precede revenue. Once built, the facilities need utilization, density and recurring add-on services to earn their cost.

The constraint is also local in another way. Frankfurt is not merely a German city on a global map. It is one of Europe's core interconnection markets, tied to finance, cloud, carriers and internet exchange traffic. Dusseldorf gives access to the Rhine-Ruhr industrial corridor. Hamburg matters for northern logistics and subsea-route positioning. Munich adds Bavaria's automotive, engineering, finance, media and technology base. The economic purpose of the footprint is therefore not national coverage in the consumer-telecom sense.

It is selective control of places where enterprise networks, carriers, cloud on-ramps and compliance-sensitive workloads need proximity.

That footprint is defensible only if the local bottleneck remains valuable. If customers decide that a hyperscale cloud region, a carrier-provided SD-WAN bundle or a managed hosting partner is enough, the expensive neutral facility becomes less central to the decision. If customers need to compose multiple networks, clouds and enterprise systems under their own operational control, the footprint earns a premium. The local-control test begins there: who pays for optionality, and who carries the downside when the optionality is underused?

Local Control Starts With A Neutral Campus Model

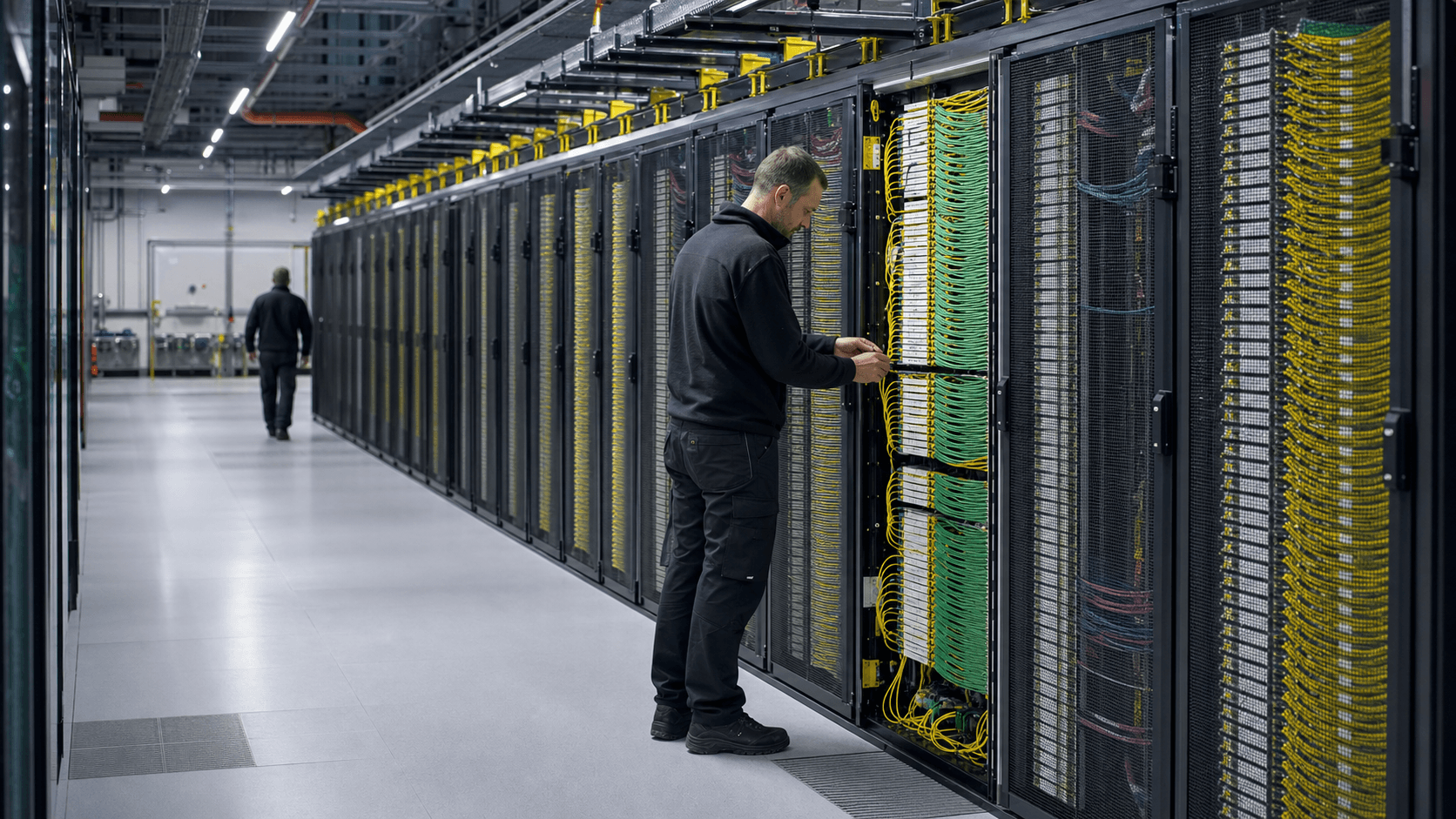

Equinix's German model is best understood as a neutral-campus model. The company does not need to own every network or every cloud service in the stack. It needs enough trusted space, power, cooling, operational processes and interconnection density that customers choose to place their equipment and private links inside its facilities. The value comes from being the meeting point. In that model, the neutral operator earns rent-like recurring revenue from colocation and service revenue from connectivity, cross-connects, remote hands and digital interconnection products.

Frankfurt is the clearest example. Equinix's Frankfurt data-center page describes the metro as a leading financial center and a hub for telecoms, commerce and manufacturing. It also presents the carrier-dense ecosystem as anchored in partnership with DE-CIX Frankfurt and says customers can use Equinix Internet Exchange and other exchange providers. That is a high-value claim because it ties the asset to a network effect: each additional carrier, cloud, enterprise, content provider or financial workload increases the usefulness of being in the same metro, and sometimes the same campus.

The FR2 facility page shows how physical and network control meet. It identifies a Frankfurt address, lists 29,386 square meters of colocation space, N+1 UPS redundancy, N+1 generator redundancy, cooling redundancy, 30 hours or more of generator autonomy at full load, ISO and other certifications, high-density cooling, business continuity options, cross-connects, metro connect, Equinix Internet Access, Equinix Internet Exchange, Equinix Fabric and Network Edge. Those are not abstract platform slogans. They are the cost centers and revenue levers of local control.

The same pattern appears in newer or more specialized facilities. FR13 is described as part of the Frankfurt North-East campus serving local and global businesses in banking, commerce and telecommunications, with advanced cooling language and a minimum cabinet density of 5kVA. Munich is positioned around banking, insurance, automotive, digital media and electronics, with direct on-ramps to AWS and Google mentioned on the Munich page. Dusseldorf is framed around competitive pricing, peering and transit choice, cloud-provider access, recovery and continuity.

Hamburg is framed as a northern gateway with peering, transit and cloud-provider access.

This is not a simple regional ISP story. The evidence is stronger for a colocation and interconnection operator than for a retail access network. RIPE NCC membership and number-resource context matter because they show participation in the internet-resource governance layer, but a resource-holder footprint is not proof that the entity sells broadband, consumer access, wholesale transit or managed cloud. The right reading is narrower and more economically useful: Equinix (Germany) GmbH is attached to the infrastructure layer where network resources, private interconnection and local facilities make customer switching harder.

The campus model creates a good business only when density compounds. A half-used neutral facility is a high fixed-cost property with power exposure. A full, carrier-rich, cloud-rich facility can charge for scarce cabinet positions, private links and operational services because the customer's next-best alternative requires moving equipment, renegotiating connectivity and accepting operational risk. The difference between those two states is the whole investment case.

The Business Model Sells Optionality Before It Sells Bandwidth

Equinix's commercial advantage is not that it can be the cheapest provider of bandwidth. Large carriers can bundle access, transport, security and management. Public clouds can bundle compute, storage, networking and service-level abstractions. Managed-service providers can reduce the number of vendors a buyer must coordinate. Equinix has to sell something less convenient but more valuable for certain customers: optionality under local control.

That optionality takes several forms. First, the customer can colocate equipment in a carrier-neutral facility rather than inside one carrier's network estate. Second, it can buy private interconnection to multiple clouds and networks rather than backhaul every workload through the public internet or a single MPLS provider. Third, it can place latency-sensitive systems close to financial markets, German industrial customers, content distribution nodes or cloud on-ramps. Fourth, it can preserve bargaining power by avoiding lock-in to a single carrier or cloud architecture.

The customer pays for that optionality through recurring colocation fees, power charges, cross-connects, remote support, private connectivity products and the management burden of owning a more modular architecture. The benefit is flexibility. The downside is complexity. A chief information officer who wants one accountable provider may prefer Deutsche Telekom, Vodafone, Telefonica, a global systems integrator or a hyperscale cloud platform. A network architect who needs direct control over latency, routing, counterparty choice and data location may pay Equinix for the neutral layer.

That is why pricing power is conditional. Equinix can command premium economics where the customer's architecture makes the facility a control point. A bank using low-latency connectivity, a cloud architect joining several clouds privately, a content provider near exchange traffic, an enterprise with a German data-location requirement or a network operator needing carrier-dense space may have strong reasons to stay. A small business that only needs resilient hosting, backup and internet access may not.

The Germany footprint also has a two-sided value proposition. Carriers, clouds and service providers want to be where enterprise demand is. Enterprises want to be where carriers, clouds and service providers are. The neutral operator monetizes the meeting place. That is powerful, but it is not automatic. If demand shifts to cloud-native services where the customer never touches physical infrastructure, Equinix must still persuade customers to use private on-ramps, distributed hybrid architecture and colocation for control-sensitive systems.

If demand shifts to AI infrastructure, Equinix must provide enough power density, cooling and deployment speed to keep the workload on its platform rather than losing it to hyperscale campuses.

The model therefore sells optionality before it sells bandwidth. That is a better business than commodity transit when density and switching costs are high. It is a weaker business if optionality becomes a nice-to-have feature that buyers rationalize away during budget pressure.

Network-Resource Evidence Points To Control, Not A Standalone Carrier Story

The RIPE NCC member evidence is important because it places Equinix (Germany) GmbH inside the regional internet-resource system. RIPE NCC membership is consistent with a company that needs to administer internet number resources or participate in the governance and operational framework around them. But the assignment's primary evidence is careful: it records a RIR member and resource-holder footprint and official directory service-area context, not proof that the entity sells ISP, IP transit, cloud, registry or managed-network services.

That caution should remain in the article's economics. Number resources are evidence of control surface. They are not revenue by themselves. An autonomous system number, IP prefix, route object or member directory row is not the company and should not be treated as the business model. The business model depends on how those resources support customer-visible services: internet exchange access, direct interconnection, private cloud connectivity, internet access products, cross-connects, metro links and network-edge services.

Equinix's facility pages provide stronger operating evidence than the membership page alone. FR2 lists Equinix Internet Exchange, Equinix Internet Access, Metro Connect and Cross Connects under interconnection products, alongside Equinix Fabric, Fabric Cloud Router, Equinix Precision Time and Network Edge under digital services. The Germany and metro pages repeatedly emphasize carrier-neutral colocation, cloud on-ramps, major networks and peering or transit choice. Those claims show a local network-control function even when they do not prove a standalone carrier revenue line for the German entity.

Frankfurt's broader exchange environment reinforces the point. DE-CIX Frankfurt is one of the world's largest internet exchanges, and Equinix's own Frankfurt page ties its local ecosystem to DE-CIX. DE-CIX's public materials describe a distributed exchange accessible from many data centers and used by networks, internet service providers, content providers and enterprise networks. For Equinix, that environment raises the value of proximity. The closer a customer's systems are to dense exchange and cloud options, the more credible the case for neutral colocation over a single-carrier or single-cloud answer.

The evidence also defines the boundary. Equinix is not the only route into DE-CIX, cloud regions or German enterprise customers. Digital Realty, NTT, Vantage, CyrusOne, maincubes and other data-center operators all compete for pieces of the same demand. Carriers can sell integrated WAN and security services without asking customers to manage facility choices. Public-cloud providers can abstract away physical networking for many workloads. The resource evidence therefore proves relevance, not inevitability.

The strongest inference is this: Equinix (Germany) GmbH matters where the customer wants local physical and network control in a country with dense interconnection demand. The weakest inference would be to call it a broad German ISP without service evidence. The economic test sits between those poles. Local resources matter if they become embedded in customer architecture. They do not matter enough if they remain merely entries in public registries and facility brochures.

Pricing Power Depends On Switching Costs Inside The Campus

The simplest price test is whether a customer can walk away cheaply. In ordinary telecom procurement, a buyer can often rebid circuits, change managed-service providers or move a workload to a cloud-native architecture over time. In a dense colocation and interconnection environment, the switching cost can be much higher. Equipment has to be moved or duplicated. Cross-connects must be rebuilt. Carrier and cloud links must be reordered. Security, compliance, remote operations, latency and change windows all have to be managed. If the customer is using the facility as a strategic control point, those switching costs support pricing power.

Equinix's German footprint is designed to create that condition. Cross-connects, private cloud access, internet exchange participation, smart hands, high-density cooling and certified facility operations are not independent features. They work together to make the facility operationally sticky. A customer that only rents space and power may be price-sensitive. A customer that uses the facility to connect multiple carriers, clouds and business partners has more reasons to stay even when renewal prices rise.

Pricing power also depends on scarcity. Frankfurt's value comes from being a core interconnection market, but that status brings power, land, planning and competition pressure. Scarcity helps incumbent facilities if customers need immediate, proven capacity. It hurts if expansion requires expensive grid work, new cooling investment or delayed development. In a constrained market, the best existing campuses can earn premiums, but the operator must avoid spending so heavily on growth that incremental returns fall.

The customer-visible product mix is therefore critical. If revenue growth comes from more cabinets, more power draw, more cross-connects and more private cloud links within existing facilities, value creation is plausible. If growth requires new shell capacity, higher power commitments and more cooling investment just to maintain market share, revenue can rise while returns decline. This is the difference between visible growth and economic value.

Equinix's global market signal points to the same tension. Public market coverage of its 2025 analyst day reported plans for higher annual capital expenditures through 2029 and targets for revenue growth, margin and adjusted funds-from-operations growth. Investors reacted negatively because the growth path implied heavier spending before the per-share benefit was visible. That is a global Equinix signal, not a German entity disclosure, but it is highly relevant to Germany. A capital-intensive data center platform earns its valuation only if new power and capacity are sold into durable, premium demand.

In Germany, that means local pricing power has to come from more than "we are in Frankfurt." It must come from being hard to replace. The evidence that would prove it would include high renewal rates, low churn, rising interconnection revenue per cabinet, strong utilization in Frankfurt and Munich, power-density premiums that customers accept, and customer willingness to pay for private multicloud links rather than relying on public cloud networking or bundled carrier services.

Growth Only Creates Value If Power And Space Are Sold Twice

A colocation operator creates value when the same scarce physical base supports multiple revenue streams. The first sale is space and power. The second sale is interconnection, cloud access, operational services and ecosystem participation. If the operator sells only the first, it is closer to a real estate and utility pass-through business. If it sells both, it becomes a network-effect platform with better margins and stronger retention.

Equinix's German materials lean heavily into the second sale. The Germany overview stresses direct connections to major clouds and networks. Frankfurt emphasizes DE-CIX, Equinix Internet Exchange and other IX providers. Dusseldorf and Hamburg mention peering, transit and cloud-provider access. Munich refers to direct on-ramps to AWS and Google. Facility pages list cross-connects, Metro Connect, Equinix Internet Access, Equinix Fabric and Network Edge. The strategic message is consistent: the customer is not just renting a cabinet; it is buying a local control position inside a dense digital supply chain.

This matters because power is becoming the scarce input. Data centers consume electricity before they produce customer value. AI and high-density compute make the problem harder because they can require more power and more advanced cooling per cabinet. Equinix's FR2 page explicitly mentions high-density cooling and liquid cooling, while FR13 uses advanced-cooling language. Those features create the ability to serve higher-value workloads, but they also raise the investment bar.

Selling power and space twice means the operator must extract enough additional revenue from the network layer to justify that investment. A high-density AI deployment that pays for power but brings little interconnection value may be less attractive than a smaller enterprise deployment that buys multiple private links, cross-connects and support services. A hyperscale customer may bring scale and credit quality, but it may also negotiate aggressively and use the facility as one node in a wider procurement strategy. An enterprise customer may pay more per unit but require more sales effort and service support.

Germany's local-control case is strongest where customers need hybrid architecture. A bank may not want all systems in public cloud. A manufacturer may need resilient local connectivity for plants, suppliers and analytics platforms. A content or network provider may need proximity to exchange traffic. A cloud architect may need private links to multiple cloud regions. These workloads justify a premium if the cost of downtime, latency or loss of control is higher than the cost of Equinix.

The weak case is generic capacity. If growth is mostly more megawatts, more square meters and more AI-driven demand without evidence of higher platform revenue per unit, the result may look impressive while returns compress. The article's core judgment is therefore deliberately conditional: Equinix's German footprint is valuable only if local interconnection density turns power and space into recurring platform economics.

The Cost Base Is A Grid, Cooling And Capex Problem

The cost side begins with power. Data centers require reliable electricity, uninterruptible power systems, backup generation, cooling, physical security and continuous operations. Equinix's own facility pages list redundant UPS, generator redundancy, cooling redundancy, certifications, security and amenities. These are not incidental. They are the operating promise customers pay for, and they are also the reason the business is capital-heavy.

Germany adds its own cost pressures. Electricity availability and price matter. Grid connection timing matters. Energy-efficiency regulation matters. Local planning and community acceptance matter. The German Energy Efficiency Act has put data centers under a clearer efficiency and reporting framework, including attention to energy management, power usage effectiveness, renewable electricity and waste-heat utilization. Even when these obligations support the sector's legitimacy, they increase the discipline required to operate profitably.

Equinix's Germany page says all of its German sites are covered by 100 percent renewable energy. That is commercially useful because enterprise and cloud customers often need sustainability evidence. It does not remove the physical constraint. Renewable coverage can be achieved through procurement instruments and contracts, while the local grid still has to deliver dependable power at the right location and time. A customer buying high-density capacity cares about the operational availability of power, not only the annual accounting of renewable coverage.

Cooling is the next constraint. Higher cabinet density and AI workloads increase heat loads. FR2 mentions direct-to-chip liquid cooling in its liquid-cooling section; FR13 and metro pages discuss advanced or AI-ready cooling. These capabilities can support premium workloads, but they also require design, capital, operational expertise and maintenance. The operator benefits if customers pay for density and resilience. The operator suffers if the market expects AI-ready language but does not sign enough high-return contracts to amortize the equipment.

Capital expenditure is the third constraint. Public market coverage of Equinix's 2025 investor day described a plan to raise annual capital expenditures to the $4 billion to $5 billion range from $3.3 billion in 2025, while also reporting targets for 7 percent to 10 percent annual revenue growth through 2029 and adjusted funds-from-operations growth that investors considered less compelling in the near term. Again, those are global signals. But Germany is exactly the kind of market where the global tension becomes local: scarce, strategic, power-intensive and competitive.

The capital recovery test is therefore not "can Equinix build?" It is "can Equinix build or operate locally at returns that beat the alternatives?" Existing facilities with dense interconnection may have strong economics. New capacity added into a higher-cost power and cooling environment must prove itself contract by contract.

Suppliers And Upstream Dependencies Set The Margin Ceiling

Equinix's German customers buy control, but Equinix itself depends on upstream systems it does not fully control. The most important supplier is the power system. Without grid capacity, backup systems, fuel logistics, cooling equipment and maintenance capacity, the facility cannot deliver its promise. Even when Equinix procures renewable energy coverage, it remains dependent on local deliverability, utility planning and the physical resilience of the power chain.

The second dependency is the cloud and carrier ecosystem. Equinix's value proposition improves when AWS, Microsoft Azure, Google Cloud, Oracle, IBM, Alibaba, carriers, content networks and exchange fabrics are reachable in or near its metros. It weakens if customers increasingly choose native cloud networking, direct carrier bundles or hyperscale campuses that bypass the neutral colocation decision. Equinix is powerful because it hosts choice. It is vulnerable because the most valuable counterparties also have their own platforms and bargaining power.

The third dependency is equipment and engineering. High-density cooling, UPS systems, generators, electrical distribution, security systems and monitoring platforms are not optional. Supply-chain delays, cost inflation or equipment shortages can slow deployment and raise capex. A data center operator can hedge with planning and scale, but it cannot escape the physics of infrastructure procurement.

The fourth dependency is labor and operational expertise. Customers paying for mission-critical colocation expect 24x7 security, technical support, remote hands and change discipline. Germany's facility pages highlight support, security and operational amenities because reliability is part of the product. Skilled operations teams, compliance staff and vendor management therefore become margin determinants. A facility with strong utilization but weak operations can destroy trust quickly.

The fifth dependency is regulatory legitimacy. Data centers are increasingly judged not only by uptime but by power use, waste heat, security, resilience and community impact. Germany's efficiency law, EU cybersecurity rules and critical-infrastructure expectations all raise the level of proof required. Compliance can become a barrier to entry for weaker rivals, but it also sets a cost floor for serious operators.

These dependencies define the margin ceiling. Equinix can charge for neutral control, but it cannot keep all of the value if power costs rise, grid upgrades are delayed, suppliers extract premiums, hyperscalers demand concessions or regulation forces new investment. The best version of the business uses scale to secure inputs better than smaller rivals and then monetizes them through interconnection density. The weaker version absorbs the same input inflation as everyone else while customers treat colocation as a commodity.

The local German case should therefore be judged by evidence of procurement advantage, utilization and service mix. A list of facilities is only the supply side. The margin answer requires proof that the German footprint turns upstream dependencies into customer value faster than those dependencies turn into cost.

Customers Benefit From Choice, But Their Concentration Is Invisible

Equinix's public metro pages repeatedly state platform-scale customer and partner numbers, including thousands of enterprises, more than 2,000 network service providers and more than 10,500 customers. Those figures support the density story at the Equinix platform level. They do not reveal customer concentration, revenue by German metro, churn, renewal pricing or how much of the German footprint is sold to a few large buyers.

That absence matters. A dense ecosystem can still have concentrated economics. A hyperscale customer can occupy large amounts of power and space. A financial-services cluster can support premium connectivity but be exposed to sector-specific spending cycles. A carrier ecosystem can be broad in name but concentrated in the networks that matter to enterprise buyers. Without local revenue disclosure, the safest conclusion is that Equinix benefits from a large global ecosystem but has not shown public German unit economics.

The customer benefit is clear. A buyer can place infrastructure near multiple networks and cloud providers, preserve optionality, support continuity plans and avoid dependence on one carrier. For SMEs or mid-market firms with limited network staff, the benefit is more complicated. They may need service continuity but may not want to manage colocation, cross-connects and private cloud links themselves. For them, a managed-service provider or carrier bundle may be simpler even if less flexible.

This is where the article's title question becomes practical. Local network control creates value for the customer who understands and uses it. It may create friction for the customer who simply wants an accountable service outcome. Equinix can address that through partners, marketplaces and digital services, but the buyer's decision still compares control against simplicity. The more complex the customer's architecture, the more Equinix can win. The simpler the requirement, the more substitute providers can compress pricing.

Customer concentration risk also intersects with market dependence. Germany is strong because it combines industrial demand, financial services, cloud regions, carriers and data-location sensitivity. But that does not mean every German metro has the same economics. Frankfurt is a core interconnection hub. Munich has industrial and technology demand. Dusseldorf and Hamburg add regional resilience and access. If demand concentrates even more heavily in Frankfurt, smaller German locations may need a sharper continuity or regional-latency use case to earn their cost.

The proof would be granular: utilization by metro, average recurring revenue per cabinet or per kilowatt, renewal spreads, interconnection attach rates, churn by customer segment and the share of revenue tied to high-density or cloud-adjacent services. Without that, the customer story is strategically credible but financially incomplete.

The Substitutes Are Bigger, Simpler And Sometimes Good Enough

Equinix's competitors are not only other data-center landlords. The real substitutes are larger carriers, hyperscale cloud platforms and managed-service providers that reduce customer complexity. A buyer can use AWS, Azure or Google Cloud in Germany and avoid owning equipment. It can buy managed WAN, SD-WAN, security and cloud connectivity from Deutsche Telekom, Vodafone, Telefonica, Colt, Orange Business or another carrier. It can outsource hosting, recovery and security operations to a systems integrator. It can choose another colocation provider in Frankfurt or nearby markets.

The hyperscale substitute is strongest for new workloads that are cloud-native from the start. If a company can deploy in a German cloud region, use native private networking and accept the cloud provider's operational model, it may not need a neutral colocation footprint. Cloud providers have the advantage of simplicity, pace and bundled services. They also have deep capital budgets and can absorb infrastructure complexity on behalf of customers.

The carrier substitute is strongest where the customer values one contract and one operational throat to choke. A carrier can combine access circuits, managed routers, firewall services, mobile connectivity, cloud connectivity and support. That may be less neutral than Equinix's model, but it is easier to buy. For many enterprises, especially those without a large network engineering team, simpler procurement beats perfect optionality.

The colocation rival substitute is strongest where the customer needs space and power in the same metro but not Equinix's specific ecosystem. Digital Realty has a major Frankfurt presence. NTT Global Data Centers, Vantage, CyrusOne, maincubes and others compete for German or Frankfurt-area demand. Some rivals may offer lower price, newer power capacity, larger wholesale deployments or more attractive terms for hyperscale customers. Equinix's answer must be density, reliability, neutrality and ecosystem value, not merely square meters.

The internet exchange substitute is also relevant. DE-CIX is accessible through many data centers. A customer that needs DE-CIX connectivity does not automatically need Equinix. Equinix's advantage is strongest when its specific campus combines exchange access with cloud on-ramps, carriers, existing customer deployments and operational trust. If the customer can access the same network outcomes elsewhere at lower total cost, Equinix's price premium narrows.

This competition does not make the German footprint unattractive. It makes the required proof more specific. Equinix must show that the control layer solves a problem that bigger, simpler substitutes cannot solve as well. The clearest problems are multi-cloud neutrality, low-latency interconnection, carrier diversity, regulated data location, private exchange access and migration paths for hybrid infrastructure. The weaker problems are generic hosting, generic backup, generic internet access and undifferentiated AI capacity.

Regulation Turns Efficiency From Messaging Into Cost Allocation

Regulation affects Equinix in two ways: it creates demand for local trusted infrastructure, and it raises the cost of operating that infrastructure. Germany and the EU have strong data-protection, cybersecurity, resilience and energy-efficiency expectations. For customers in finance, manufacturing, public-sector-adjacent services or critical supply chains, domestic facilities with documented controls can be attractive. For the operator, the same expectations require investment, reporting, audits and operational discipline.

The German Energy Efficiency Act is central to the cost allocation question. Data centers are no longer judged only by uptime and security. They are expected to manage energy efficiency, renewable electricity and waste heat more explicitly. These requirements may benefit a scaled operator that can invest in efficient systems and documentation. They also make weak utilization more expensive. A partially used facility still has to meet standards, manage reporting and maintain systems.

EU cybersecurity policy adds another layer. NIS2 expands cybersecurity and resilience expectations across essential and important entities, including digital infrastructure categories. Germany's critical-infrastructure rules and BSI oversight can also affect data-center, exchange and network-adjacent operations depending on thresholds and service classification. For customers, this regulatory environment increases the value of credible infrastructure partners. For Equinix, it raises the cost of being credible.

Geopolitical risk is less about sanctions exposure in the narrow sense and more about supply-chain, cloud sovereignty, data transfer and resilience. Enterprises want to know where data and systems sit, who can access them, what happens during outages and how dependent they are on non-European platforms. Equinix's neutral model can help because it lets customers combine local infrastructure with global cloud access. But neutrality does not eliminate geopolitical exposure. It simply gives customers more architecture choices.

Operational risk is more immediate. A major outage, security incident, power event or failed cooling system would damage the trust that supports premium pricing. The facility pages emphasize redundancy and certifications because customers know this. The pricing premium exists only while the operator's reliability record remains credible. Once a customer believes another provider can deliver the same uptime and connectivity with lower cost or simpler management, the premium becomes vulnerable.

Regulation therefore converts efficiency from brand language into economic allocation. Who pays for compliance, energy management, waste-heat readiness, cybersecurity and resilience? If customers recognize those costs as part of a valuable local-control service, Equinix can recover them. If customers treat them as baseline expectations while demanding lower prices, the operator absorbs the burden.

Unofficial Signals Support Demand But Not Unit Economics

Unofficial and market signals are useful here only if they are kept in their place. Investor reaction to Equinix's 2025 growth targets suggests the market believes demand is real but worries about the timing and return of the capital cycle. A separate short-seller episode in 2024 raised allegations around accounting metrics and AI readiness; public coverage recorded Equinix's response that it was reviewing the claims. Those signals are not proof that the allegations are true, and they are not German operating data.

They do show that sophisticated market entities are focused on the same question this article asks: does visible demand translate into durable per-share value after capex?

There are also industry signals. Cloud and AI demand are pushing data-center operators toward higher power density and faster development. At the same time, European hub markets such as Frankfurt, London, Amsterdam and Paris face constraints around land, power, planning and sustainability. These signals support demand for scarce capacity, but they do not prove that every operator or every facility earns attractive returns. Scarcity can raise prices, but it can also raise input costs and lengthen development timelines.

Search, forum and market chatter around data-center capacity, power constraints and cloud demand should therefore be treated as directionally useful but financially incomplete. Buyers may say they need more AI-ready infrastructure. That does not reveal what they will pay, how long they will commit, whether they need Equinix specifically or whether they will move the workload to a hyperscale region.

The strongest unofficial signal for Equinix Germany is not hype. It is the persistence of Frankfurt as a dense interconnection market. Cloud regions, DE-CIX traffic, carrier density and enterprise demand all reinforce the strategic relevance of local control. The weakest signal is generic AI enthusiasm. AI can increase power demand faster than it increases interconnection value, especially if large deployments are negotiated by hyperscalers with strong purchasing power.

The article's handling of unofficial signals is deliberately conservative. They help frame demand, competition and investor concern. They do not settle the economic question. The local footprint earns its cost only if hard operating evidence shows utilization, pricing, interconnection attach, customer retention and returns on incremental capacity.

The Evidence That Would Change The Judgment

The current judgment is conditional positive on strategic relevance and cautious on economic proof. Equinix (Germany) GmbH is relevant because the public evidence connects it to RIPE NCC membership and to a German footprint within one of the world's most important interconnection platforms. Equinix's German pages show multi-metro colocation, cloud on-ramp and peering/transit positioning. Frankfurt's role, DE-CIX proximity, facility certifications, power redundancy, cooling capabilities and product mix all support the local-control thesis.

The caution is that none of the public evidence discloses standalone German unit economics. There is no public article-ready proof of German revenue, German EBITDA, utilization by metro, power-cost recovery, churn, renewal pricing, customer concentration or return on invested capital for the German footprint. Without those facts, the correct answer to the core question is not a simple yes.

It is: yes, if the local-control layer is dense enough to create switching costs and sell interconnection services on top of space and power; no, if customers can obtain enough functionality from larger carriers, hyperscale clouds or rival data centers at lower complexity and lower effective cost.

Several facts would move the judgment upward. First, Equinix could disclose or credibly demonstrate high utilization across Frankfurt, Munich, Dusseldorf and Hamburg, especially in facilities with dense interconnection demand. Second, it could show rising interconnection revenue per cabinet or per kilowatt, proving that the platform sells more than power and space. Third, it could show strong renewal spreads with low churn, proving that customers accept premium pricing because moving is costly. Fourth, it could show that AI-ready and high-density deployments carry attractive returns rather than merely large power commitments.

Fifth, it could show that German renewable-energy, cooling and waste-heat investments reduce operating risk or support pricing rather than functioning only as compliance cost.

Several facts would move the judgment downward. A shift of enterprise workloads into native cloud regions without private interconnection would weaken the neutral-campus model. Large customer concentration at low margins would reduce pricing power. Rising grid or cooling costs that cannot be passed through would compress returns. Delays in power delivery or regulatory approvals would make growth more expensive. Aggressive pricing by Digital Realty, NTT, Vantage, maincubes, CyrusOne or carrier-integrated alternatives would reduce the value of Equinix's footprint unless its ecosystem remains clearly superior.

The final economic answer is therefore practical. Equinix (Germany) GmbH does not win because it is local. It wins if local control is scarce, connected and hard to replace. It loses if local control becomes an expensive way to provide services that buyers can obtain more simply elsewhere. The evidence available today supports the strategic need for the footprint. The evidence still needed is proof that the footprint earns more than its capital and operating cost after power, cooling, supplier dependence and customer alternatives are fully priced.