Summary

- EDF power solutions SA is best understood as an EDF group renewable power developer, owner and operator with a RIPE local internet registry footprint, not as a public ISP proved by registry data alone.

- RIPE records identify EDF power solutions SA as a French LIR with legacy IPv4 space, while RIPEstat shows the visible /24 routes originated by Equinix AS15830; that points to governed resources and outsourced connectivity, not independent carrier economics.

- The company can plausibly charge for reliability through long-term power purchase agreements, asset availability, storage, solar, wind, maintenance and corporate energy services, but public evidence is thin on customer pricing, margins, outage performance and network cost allocation.

- The judgment is conditional: EDF power solutions SA has credible operating reasons to fund reliable connectivity, but the public record does not yet prove that customers pay a distinct premium large enough to cover redundancy, field operations, equipment refresh and compliance overhead.

Paid Reliability Starts With Someone Else's Downside

The economic incentive behind paid reliability is simple: the customer is not buying uptime as an abstract virtue. The customer is buying a smaller probability of a costly interruption. In telecommunications, that may mean a bank branch that cannot process payments, an industrial site that cannot reach cloud systems, or a local service provider that loses customers when a backbone path fails.

In power infrastructure, the same incentive appears through a different surface: a corporate buyer wants predictable renewable output, a grid operator wants controllable injections, a site owner wants monitored equipment, and an industrial customer wants a supplier that remains accountable after construction is finished.

EDF power solutions SA belongs to the second category more than the first. Its public identity is rooted in renewable energy. The official corporate site presents EDF power solutions as an international renewable power company active across development, financing, construction, operation and maintenance of low-carbon energy assets. The French site emphasizes solar, wind, storage and related services for public authorities, landowners, companies and territories. The company therefore earns its strongest claim to reliability not by selling mass-market internet access, but by making infrastructure perform over time.

That distinction matters because this article begins from a network-resource signal. RIPE identifies EDF power solutions SA as a French local internet registry. RIPE records also associate the company with a legacy IPv4 block named Electricite-de-France. Those records are useful evidence of number-resource governance and operational dependence on routed networks. They are not proof that the entity is a consumer ISP, a transit carrier, a hosting business or a cloud provider. Treating the resource record as the identity would inflate the telecom thesis and miss the more interesting economics.

The real question is narrower and harder. Can EDF power solutions SA make customers pay enough for reliability, local accountability and redundancy to cover the hidden costs that reliability imposes? For a renewable power operator, those costs include supervisory control systems, data links, cybersecurity, site monitoring, grid-connection coordination, field maintenance, spare parts, sensors, software, control-room processes, power electronics and the corporate network that links assets, customers and suppliers.

For the RIPE resource footprint, they include membership administration, address management, routing hygiene, upstream connectivity and provider accountability. For customers, the value appears as a cleaner power contract, a functioning asset, a battery that responds when called, or a supplier able to take responsibility across the life of a project.

The answer is not visible in one public price list. EDF group reports the scale of its renewable and storage portfolio and publishes financial results at group level, but the public materials do not break out every contract term, network bill, asset-level availability penalty or customer concentration metric for EDF power solutions SA. The company can probably recover part of the reliability cost through long-term power purchase agreements, energy services and asset availability. The public record does not prove that it recovers all of it at attractive margins. That gap is the center of the judgment.

The Entity Is an Energy Operator, Not a Telecom Carrier

The operating boundary starts with the company's own presentation. EDF power solutions describes itself as a global player in low-carbon energy, with activities across solar power, wind power, storage, hydrogen, hybrid solutions and electricity supply to companies. Its French website frames the business around renewable project development, construction, financing, operation and maintenance. It addresses landowners, local authorities, companies and public partners. That is a power-infrastructure boundary, not a retail connectivity boundary.

The French corporate record and RIPE record align on legal identity. RIPE's organisation entity for ORG-ERS13-RIPE lists the org-name as EDF power solutions SA, the country as France, the registration number as 379 677 636 R.C.S. Nanterre, and the organisation type as LIR. The address shown in RIPE is 43 Boulevard des Bouvets, Nanterre Cedex. French public business-directory data also links the company identity to Nanterre and the same registration number.

The official legal notices for EDF power solutions web properties refer to the corporate group and publication responsibilities, while the company pages reflect the rebranded power-solutions identity.

The energy boundary is also visible through EDF group reporting. EDF's 2025 financial-results materials show the group treating renewables and storage as a major strategic segment, with net installed capacity and the project development portfolio reported in gigawatts, not in broadband subscribers or IP transit ports. EDF power solutions appears in the same strategic orbit as EDF's renewable development, asset management and disposal decisions. The June 2026 agreement to sell EDF power solutions' United States and Canada business to KKR further reinforces that the asset base is renewable generation and storage, not telecom access.

This boundary changes how to read the RIPE membership. A local internet registry can exist inside a non-telecom enterprise because the enterprise has durable needs for address space, routed service, internal segmentation, provider coordination, data centers, remote sites or operational technology. Many large industrial firms need governed IP resources even when they do not sell internet access. EDF power solutions SA therefore should be evaluated as a resource holder and infrastructure operator with network dependence, not as a regional ISP by default.

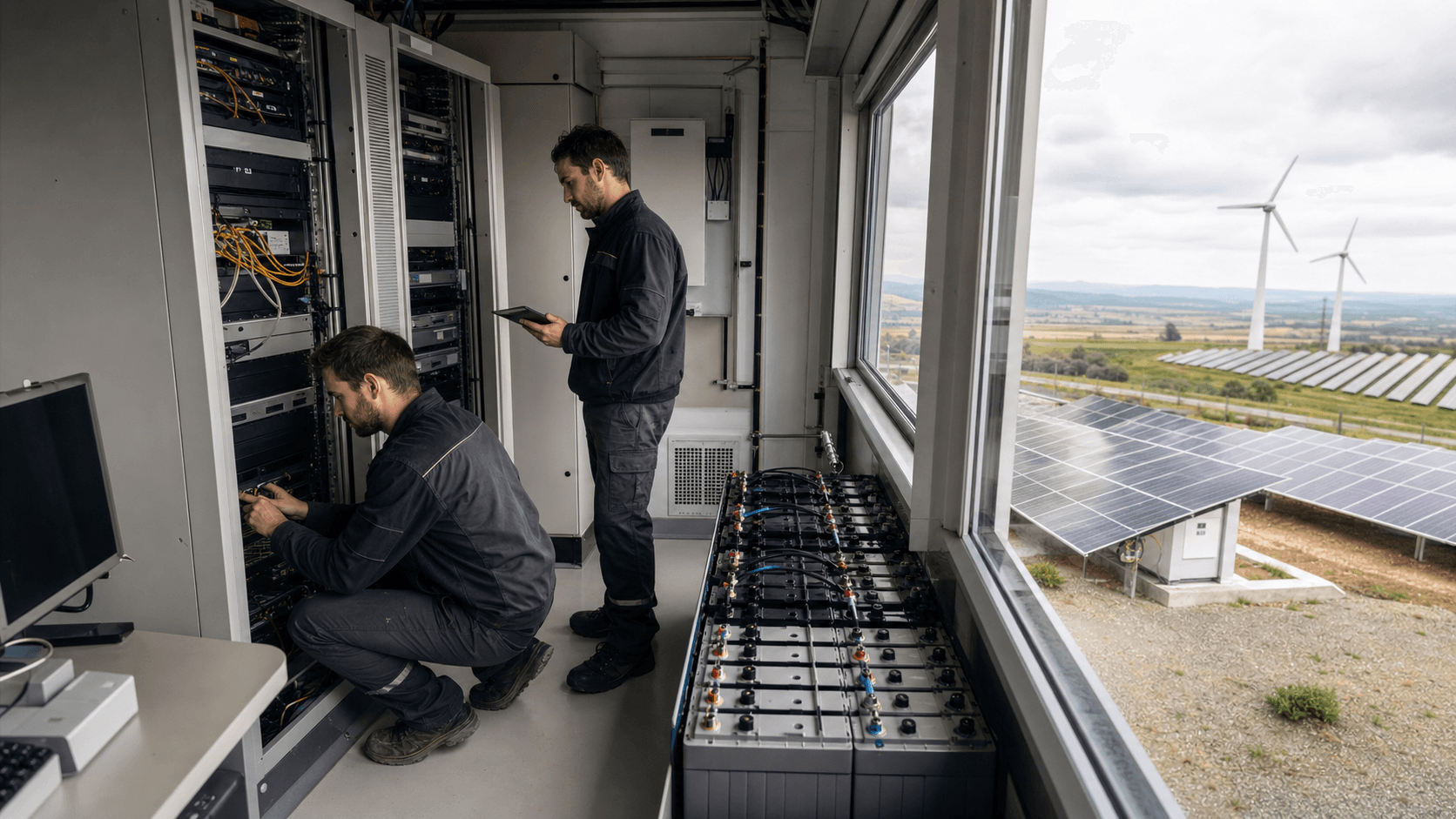

That does not make the telecom evidence irrelevant. The company's assets are geographically distributed and operationally sensitive. Renewable sites, storage units, substations, control systems, corporate offices, maintenance teams and market interfaces all depend on reliable communications. If a solar plant, wind farm, battery, trading interface, monitoring platform or maintenance system loses connectivity at the wrong moment, the cost can show up as lost availability, delayed response, poorer forecasting, grid-operator friction or customer dissatisfaction.

The internet resource evidence is a clue that network governance has become part of the operating stack.

The public article therefore has to keep two truths together. EDF power solutions SA is not publicly evidenced as a telecom carrier selling IP transit or retail broadband. It is, however, a reliability business in an adjacent and increasingly digital sense. Its customers pay for energy assets and services that only work commercially when the physical infrastructure, control layer and communication layer all keep performing.

The Business Model Sells Long-Term Electrical Assurance

The core business model is project-based infrastructure converted into long-term service. EDF power solutions develops renewable power assets, arranges financing, builds or supervises construction, operates and maintains facilities, and sells power or energy services through contracts. On the French site, the company offers solar and wind development, storage, repowering, operation and maintenance, and solutions for companies that want decarbonized electricity. The value proposition is not a one-time equipment sale. It is the promise that a site will be developed, connected, maintained and useful over a long period.

That model is capital intensive but economically coherent. A renewable project absorbs development risk before revenue is visible: site control, permits, grid connection, studies, procurement, financing, construction and commissioning. Once operating, it depends on energy price exposure, contracted offtake, subsidies or tenders where applicable, operations cost, availability and asset life. A company with EDF's brand and balance-sheet context can lower some customer risk because buyers know the supplier is part of a large energy group with technical capacity and institutional access. But brand does not eliminate the cost of delivery.

Reliability is embedded in several product lines. A corporate power purchase agreement gives a buyer confidence about renewable supply and price structure over time. A solar project on or near a customer's site gives the customer a visible decarbonization asset, but the economics still depend on equipment performance, meter data, maintenance and electricity-price assumptions. A battery storage asset creates value only if it can charge, discharge, communicate and respond to market or grid signals when needed.

Operations and maintenance work monetizes reliability more directly: the customer pays for inspection, performance management, fault detection, repair and life extension.

The economic question is who carries the downside when reliability fails. If EDF power solutions sells a simple development service and transfers the asset, the buyer bears more operating risk after completion. If the company owns the asset and sells power under a long-term agreement, EDF power solutions retains more performance risk and must price it into the contract. If the company provides operations and maintenance, the customer expects local accountability and measurable response. If the company offers storage or flexibility, poor communications or delayed dispatch can turn a technical problem into a revenue problem.

The company's own messaging leans toward accountability across the project life cycle. It emphasizes development, construction, operation, maintenance and long-term support rather than only project origination. That makes the reliability premium plausible. Customers do not only buy electrons; they buy a counterparty that can handle permitting complexity, grid interaction, asset monitoring, maintenance and performance.

The missing evidence is price. Public pages describe solutions, sectors and capabilities, but they do not disclose contract spreads, maintenance fees, performance guarantees, capacity-payment terms, storage revenue stacks or penalties. Without those details, it is impossible to prove that the company earns an economic premium for reliability rather than merely absorbing reliability cost as the price of staying competitive. The business model supports paid reliability. The public record does not yet quantify how much customers pay for it.

RIPE Records Show Governance Over Addresses, Not a Retail Network

The most concrete network-resource evidence is the RIPE record. The organisation entity lists EDF power solutions SA as ORG-ERS13-RIPE, a French local internet registry. The same RIPE query shows a legacy IPv4 allocation, 163.114.144.0 to 163.114.145.255, with the netname Electricite-de-France and the organisation set to ORG-ERS13-RIPE. The block is a /23, or 512 IPv4 addresses before any internal subnetting. Route objects for 163.114.144.0/24 and 163.114.145.0/24 list AS15830 as origin and are maintained by the EDF power solutions RIPE maintainer.

Those details tell an analyst several useful things. First, EDF power solutions SA has a formal resource-holder role in RIPE's system. That brings administrative obligations: contact accuracy, abuse handling, maintainer control, database hygiene, membership fees where applicable and a governance relationship with the regional internet registry. Second, the address space is not just a forgotten entry in a static database. RIPEstat's routing-status data for the /23 shows the more-specific /24s visible with AS15830 as origin.

Third, the maintainer and route objects imply deliberate routing arrangement rather than a random third-party listing.

They do not prove that EDF power solutions operates its own autonomous system. The public RIPE evidence reviewed here did not identify an EDF power solutions aut-num as the origin. Instead, the visible origin is AS15830, the Equinix Internet Access and Equinix Connect global IP transit platform. RIPEstat's prefix overview for 163.114.144.0/24 also identifies AS15830 and the Equinix holder. RPKI validation for the sample prefix and AS15830 returns unknown rather than valid.

That is a caution point, not a service-quality verdict: it means the reviewed route-origin authorization evidence did not provide a cryptographic validation signal for that prefix-origin pair at query time.

The economic inference is that EDF power solutions likely relies on a professional upstream or connectivity provider to originate the visible prefixes. That is normal for a non-telecom enterprise. It can be a rational choice: outsourcing origin and transit to Equinix may reduce the need to run a full carrier-grade external routing operation, while still allowing the enterprise to control address resources and maintain continuity across services. The trade-off is dependence. The enterprise pays for provider reliability and support rather than owning every layer directly.

For the article's core question, the RIPE record sets a floor and a limit. The floor is that network reliability is not incidental. A company that holds governed IPv4 space and maintains route objects has enough need for stable addressing to warrant registry administration. The limit is that the resource record does not reveal revenue, customers, redundancy architecture, security posture, traffic volume, service-level agreements or unit economics. It proves resource governance, not telecom profitability.

This is why resource evidence must be used as evidence rather than identity. The company can be tracked in a regional-ISP evidence set because it appears in RIPE membership and routing data. But public judgment should not call it a carrier unless the company sells carrier services or operates carrier infrastructure in public evidence. The better conclusion is more disciplined: EDF power solutions SA has a visible number-resource footprint that supports its broader infrastructure reliability needs.

Equinix Routing Turns Number Resources Into an Outsourced Reliability Choice

AS15830 is important because it changes the cost structure. RIPE's aut-num record describes AS15830 as Equinix Internet Access and Equinix Connect, a global IP transit platform. The same record lists global upstream relationships with major carriers and explains Equinix's routing-policy context. RIPEstat identifies AS15830 as announced and held by Equinix. When EDF power solutions SA's visible more-specific prefixes are originated by AS15830, the likely economic arrangement is not that EDF power solutions is selling transit from its own backbone.

It is that EDF power solutions is using a professional interconnection and internet-access platform to bring its address space onto the public internet.

That arrangement can be economically sensible. Equinix specializes in data centers, interconnection and enterprise connectivity. A renewable power operator does not necessarily gain advantage by staffing a carrier backbone, negotiating broad peering and operating every external routing function itself. If the business need is reliable access for enterprise systems, control platforms, monitoring, partner portals, data exchange or externally reachable services, a provider such as Equinix can supply resilience and operational support at a predictable cost.

But outsourcing reliability does not eliminate the bill. It changes where the bill appears. EDF power solutions still needs to pay for connectivity, cross-connects, service tiers, support, security controls, equipment, internal networking, monitoring, change management and incident response. It also needs internal staff or outsourced specialists who know how to manage provider relationships, addresses, DNS, firewall rules, segmentation and remote-site connectivity.

The financial question becomes whether those costs are recovered through better energy-service contracts, lower outage loss, higher availability, operational efficiency or customer willingness to pay for a credible counterparty.

There is a second implication: the customer may not see the network line item. A corporate offtaker buying renewable power from EDF power solutions is unlikely to pay a separate fee for the public route origin of EDF's address block. The customer pays for the power contract, service reliability, asset performance and accountability. The network cost is buried inside the operating model. That makes pricing discipline harder to observe from outside. A company can be spending materially on reliability without disclosing it as a standalone revenue product.

The route-origin data also forces a sharper view of redundancy. A /23 split into two visible /24 route objects originated by one provider is not the same as a multi-AS public transit fabric. It may be perfectly adequate for enterprise needs, but it is not proof of wide carrier diversity. If EDF power solutions needs higher resilience for critical systems, the important evidence would be multi-site architecture, private circuits, backup providers, segmented operational networks, satellite or mobile fallback at remote assets, tested incident procedures and cyber recovery metrics. Those are not visible in the RIPE record.

Thus Equinix routing is a reliability choice, not a full answer. It suggests EDF power solutions prefers governed resources plus professional connectivity over building a public internet carrier identity. That is likely rational. The unanswered question is whether the company has priced the resulting reliability spend into the services that customers actually buy.

The Operational Network Is Wider Than the Internet Prefix

For EDF power solutions, the operational network is larger than the two visible /24s. A renewable power company runs a distributed physical system. Solar sites, wind farms, battery systems, substations, meters, weather stations, inverters, turbines, SCADA equipment, maintenance teams, corporate applications and market interfaces all exchange data. Some of that communication may use private telecom circuits, mobile service, radio, utility networks, managed service providers, cloud platforms or data-center connectivity rather than the public prefixes visible in RIPE. The public prefix is a window, not a map.

This wider network matters because reliability in renewable energy is increasingly data dependent. Power output needs to be forecast. Asset performance needs to be monitored. Faults need to be detected quickly. Grid-code requirements can involve telemetry, remote control and compliance reporting. Batteries need dispatch instructions and market signals. Operations teams need remote access under strict security rules. Customers may require reporting on generation, certificates, carbon accounting, production history and site performance. The communications layer is therefore part of the product even when it is not sold as connectivity.

The company's official materials support this view. EDF power solutions presents itself as active across the entire life cycle of renewable assets and offers operation and maintenance services. Its French pages discuss services for companies, local authorities and landowners, and its expertise pages include storage and hybrid solutions. A June 2026 EDF power solutions announcement about commissioning its first battery storage facility in mainland France highlights the move into assets whose economics depend on control, dispatch and responsiveness.

Storage makes the data layer more valuable because a battery can earn or protect value only if it is available when the system needs it.

The operational network also has physical consequences. A field technician responding to a wind turbine fault needs accurate diagnostics. A solar operator needs inverter and production data. A battery operator needs software, communication and power electronics to work together. A corporate customer paying for renewable supply wants credible performance reporting. Every additional site increases the number of endpoints, vendors, sensors, access controls and incident paths. Reliability is not just bandwidth; it is repeatable operational coordination.

This is where a power company starts to resemble a telecom economics case without becoming a telecom company. It faces upstream dependencies, local support needs, equipment-refresh cycles, cyber obligations, vendor lock-in, redundancy choices and customer promises. A cheap network architecture can reduce near-term cost and create expensive failures later. A robust architecture can protect the operating model and still destroy margin if customers do not pay enough for the premium.

The public evidence does not show EDF power solutions' internal network blueprint. That is normal; it would be sensitive. But the scale of the renewable portfolio, the presence of storage, the RIPE resource footprint and the life-cycle service model make one conclusion reasonable: network reliability is an enabling cost of the business, not a decorative IT expense.

Pricing Power Comes Through PPAs, Flexibility and Availability

If EDF power solutions SA earns a reliability premium, it most likely earns it through energy contracts rather than telecom tariffs. Corporate power purchase agreements are the cleanest example. A customer commits to buy power or associated attributes over a defined period, usually because it wants price visibility, decarbonization credibility and a financeable supply arrangement. The developer gains bankable revenue that can support investment. The customer pays for a combination of energy, risk transfer and execution capability.

The French EDF power solutions pages aimed at companies emphasize renewable electricity solutions and long-term supply arrangements. That suggests a route to pricing power: customers that need credible decarbonization and reliable delivery may prefer a large integrated counterparty over a smaller developer with less operational depth. The value is not just the megawatt-hour. It is the package of origination, permitting, construction, asset operation, reporting, performance and counterpart risk. Reliability can be monetized if it reduces the customer's procurement uncertainty.

Storage and flexibility add another route. Batteries are not valuable because they exist; they are valuable because they respond. A battery can help manage intermittency, provide system services, shift energy, support grid needs or improve project economics depending on market design. EDF power solutions' June 2026 announcement about a mainland France battery storage facility is therefore more than a technology milestone. It points toward reliability as dispatchable capability. The more the revenue stack depends on being available at the right moment, the more communications, control systems and maintenance matter.

Operations and maintenance may monetize reliability most directly. A customer that owns an asset but lacks EDF's operating platform can pay for monitoring, preventive maintenance, troubleshooting and performance management. The supplier's economic upside depends on efficient field operations and technology that catches problems before they become outages. The customer benefit is lower downtime and better production. Here again, network reliability is a cost embedded inside a service fee.

The public limitation is that tariffs and contract economics are sparse. EDF power solutions does not publish a comprehensive price sheet for corporate PPAs, storage services, maintenance packages or performance guarantees. EDF group reporting gives segment scale and financial context, but it does not reveal the unit economics of a specific EDF power solutions SA customer in France. It does not show how much premium a buyer pays for reliability versus the lowest available renewable supply.

That lack of evidence matters. A market can value reliability and still resist paying for it. Corporate buyers often want green power, low price, flexible terms and high service quality at once. Public authorities may award tenders under strict pricing pressure. Industrial customers may compare a long-term PPA against wholesale-market exposure, certificates, on-site generation, efficiency projects or simply waiting for cheaper technology. EDF power solutions can claim a premium only where its reliability reduces risk enough to overcome those alternatives.

The best judgment is that pricing power exists but is uneven. It is stronger for complex customers needing long-term supply, reporting, project execution and credible maintenance. It is weaker where the customer sees renewable power as a commodity and can substitute another developer, another PPA, wholesale-market purchases or self-financed on-site assets.

Costs Arrive as Capital, Maintenance, Data and Compliance

The reliability bill arrives before the customer can fully judge the service. EDF power solutions must fund development staff, engineering, grid studies, permitting, procurement, construction management, land relationships, community engagement, financing work and project controls before a power asset becomes a revenue-generating site. Once operating, it must fund maintenance, spares, software, cyber controls, monitoring, safety processes, insurance, asset management and customer reporting. If it owns the asset, it also carries capital risk; if it operates for others, it carries service-delivery risk.

Capital needs are visible in EDF group reporting. Renewables and storage are strategic growth areas, and EDF reports installed capacity, its project development portfolio and disposals in that context. The June 2026 sale agreement for the United States and Canada business shows capital allocation discipline at group level: EDF is willing to reshape its renewable footprint when a transaction better serves balance-sheet or strategic priorities. That is a reminder that growth in renewables is not automatically value creation. Assets must earn enough over their lives to justify the capital tied up in them.

Maintenance is less glamorous but often more decisive. Wind turbines, solar modules, inverters, transformers, battery systems and grid-connection equipment degrade, fail, require inspection and need spare parts. A reliability promise means the operator cannot defer maintenance indefinitely. Field teams need vehicles, training, safety procedures, inventory and dispatch systems. A larger fleet can create scale economies, but it also multiplies failure points.

Data and communication costs sit inside that same maintenance system. Remote monitoring reduces unnecessary site visits and shortens diagnosis, but it requires sensors, connectivity, secure access, software platforms and staff who can interpret alarms. Cybersecurity is not optional. Energy assets are part of a critical-infrastructure environment, and the European NIS2 framework expands cyber obligations across essential and important sectors. French ANSSI guidance reinforces that affected entities must prepare governance, risk management and incident-reporting capabilities.

Even if the exact scope for each corporate entity depends on legal classification, the direction is clear: energy infrastructure faces more cyber and operational-resilience overhead, not less.

RIPE membership adds a smaller but concrete administrative cost. RIPE NCC's charging scheme sets membership and resource-related fees for members. For a large energy operator, those charges are not material beside project capital, but they symbolize a broader point. Reliability has many small recurring costs: registry administration, address management, provider contracts, audits, cyber tooling, support retainers, spare equipment and compliance reporting. None is the whole margin story. Together they create a cost base that must be recovered from customers.

The key economic danger is cost invisibility. Customers may value the result of reliability but resist the price of the system that creates it. If EDF power solutions prices too low to win projects, it can grow capacity while under-earning on maintenance, network support and compliance. If it prices too high, customers may choose a cheaper developer or a less integrated service. The company has to make reliability visible enough to charge for it without turning every customer negotiation into a debate over overhead.

Suppliers and Upstream Dependencies Set the Real Redundancy Bill

Reliability is never fully owned. EDF power solutions depends on equipment suppliers, contractors, grid operators, data-center and connectivity providers, software vendors, maintenance partners, financial counterparties and public authorities. The company can coordinate these dependencies, but it cannot abolish them. The cost of redundancy is the cost of making sure one weak supplier does not break the promise made to the customer.

In the network layer, Equinix is the visible upstream routing counterparty for the reviewed public prefixes. That relationship can improve reliability by placing external routing with a specialist provider. It can also create dependence on the provider's service quality, support responsiveness, commercial terms and data-center footprint. If critical public services, remote access or enterprise systems use these resources, EDF power solutions needs provider accountability, backup plans and internal expertise. A resource holder that outsources origin still owns the customer impact of a failure.

In the energy layer, supplier dependence is broader. Solar projects depend on module, inverter, tracker, transformer and construction suppliers. Wind projects depend on turbine manufacturers, blade logistics, grid equipment, operations contractors and specialist maintenance. Batteries depend on cell supply, power conversion systems, energy-management software, fire-safety design and warranty structures. Each supplier choice changes the reliability cost curve. A cheaper component may increase maintenance risk. A premium supplier may lower outage probability but raise capital cost.

A software vendor may create operational efficiency while adding cyber and lock-in exposure.

Grid operators are another dependency. Renewable projects need interconnection, curtailment rules, metering, dispatch coordination and compliance with grid-code requirements. In France, RTE's public electricity reports show the system context in which renewables and flexibility operate. Rising renewable penetration can increase the value of storage, forecasting and flexibility, but it also raises the importance of grid coordination. EDF power solutions can build and operate assets, but grid access and system rules shape their revenue.

The company also depends on EDF group context. Being part of EDF can lower financing friction, improve credibility and support access to expertise. It can also bring capital-allocation pressure from a group balancing nuclear, networks, customers, renewables, debt, disposals and state policy. The June 2026 KKR transaction for North America shows that renewable assets can be bought, sold or restructured when group priorities change. Customers may like the EDF name, but they still need clarity about which entity owns the contract and who remains accountable over time.

The redundancy bill therefore has two parts: direct spending and managerial coordination. Direct spending buys better equipment, extra connectivity, spares and support. Coordination turns suppliers into a reliable system. EDF power solutions' economic challenge is to make customers pay for both, because reliability fails when the second is underfunded.

Customer Concentration Is Hidden Behind Group Scale

The public record gives company scale but not customer concentration. EDF power solutions' own materials describe a global presence and a broad set of markets. EDF group reporting places renewables and storage inside a large energy group. The French site addresses companies, landowners, public authorities and territories. That breadth suggests the company is not dependent on a single small customer class. But breadth of marketing audience is not the same as disclosed revenue diversification.

Customer concentration matters because reliability businesses often look strongest where they are most exposed. A large corporate PPA can support financing and validate the developer, but it can also concentrate revenue and negotiation leverage. A public tender can create long-term income, but public procurement may press prices down and impose strict obligations. A large industrial buyer may value service continuity, but it may also have sophisticated procurement teams that demand penalties, reporting and price concessions. A storage or flexibility contract may offer attractive revenue, but market-rule changes can alter returns.

EDF power solutions likely benefits from EDF's brand and market access. A corporate buyer seeking renewable power may prefer a known energy group to an unknown project developer. A local authority may prefer a supplier with experience in permitting and maintenance. A landowner may value a counterparty that can finish a project and stay solvent through the operating life. These advantages can reduce customer-acquisition risk and support pricing, but they do not prove margins.

The article's core question requires knowing whether customers pay enough for reliability. Public materials do not disclose the share of revenue from long-term contracted PPAs, merchant exposure, operations and maintenance, storage, project disposals, development fees or customer-specific services. Nor do they disclose renewal rates, average contract duration, service-credit exposure or asset availability by customer segment. EDF group reporting is too aggregated to answer those questions at EDF power solutions SA level.

The lack of disclosure does not mean the economics are poor. Privately held project companies and group subsidiaries often do not publish customer-level data. Still, outside judgment must apply a discount. A reliability premium is strongest when customers have high switching costs, long contracts, measurable service needs and limited alternatives. It is weakest when customers can rebid projects, buy certificates, switch developer, use wholesale power or accept lower service quality for a lower price.

The right conclusion is cautious. EDF power solutions has the brand, capabilities and sector position to win customers that value reliability. The public record does not reveal whether those customers are concentrated, how they price risk, or whether their contracts adequately compensate the company for redundancy and accountability.

Competition Includes the Grid, Rival Developers and Self-Insurance

The competitive set is wider than other EDF-branded entities. EDF power solutions competes with renewable developers, utilities, independent power producers, infrastructure funds, energy-service companies, equipment-backed developers, storage specialists, corporate PPA intermediaries and the customer's own decision to delay or self-insure. In some cases it also competes with the wholesale electricity market: a buyer can decide that market exposure plus certificates is cheaper than a bespoke long-term renewable contract.

Rival developers can undercut on price if they accept lower margins, cheaper equipment, less service depth or more merchant risk. Infrastructure funds can bid aggressively for contracted assets if capital costs are favorable. Equipment manufacturers can support developer partners with financing or warranty packages. Utilities can bundle supply, balancing and customer relationships. Storage specialists can focus tightly on flexibility revenue while a broader renewable developer must allocate capital across many technologies.

The regulated grid is not a competitor in the same commercial sense, but it is a substitute for some reliability claims. A customer already receives physical electricity through the grid. If its main need is decarbonization accounting rather than physical on-site resilience, it may compare EDF power solutions against other certificate-backed or grid-connected options. If the customer wants physical resilience at its site, it may compare EDF against on-site solar, batteries, diesel backup, efficiency projects, demand-response contracts or a different energy-services integrator.

Self-insurance is the quiet rival. A customer may decide to split its energy procurement among several suppliers, buy shorter contracts, install a smaller on-site system, keep backup generation, or accept operational risk rather than pay a premium for a more accountable solution. In telecom terms, this is similar to buying two ordinary links instead of a managed resilient service. The customer's internal tolerance for risk caps the supplier's pricing power.

EDF power solutions' advantage is integration. It can combine development, financing, construction, operation and maintenance under a recognized energy name. It can draw on EDF group credibility and technical knowledge. It can offer customers a counterparty that understands both power assets and long-term operation. That integration is valuable when the customer wants less procurement complexity and clearer accountability.

The disadvantage is cost. Integrated reliability is expensive. A specialized competitor can attack one slice of the value chain. A low-cost developer can accept a narrower service promise. A customer can unbundle the package. EDF power solutions must therefore show that its broader accountability prevents enough downside to justify the price. Without public case studies, performance data or customer-level pricing, that claim remains plausible rather than proven.

Regulation and Cyber Risk Raise the Price of Accountability

Energy infrastructure has a regulatory weight that ordinary digital services do not. Renewable projects face permitting, environmental obligations, land rules, grid connection processes, safety requirements, market rules and reporting. In Europe, cyber and operational resilience obligations are also tightening. The NIS2 framework expands attention to risk management, incident handling and governance across essential and important entities, including energy-related sectors. French ANSSI materials make clear that affected organisations need structured preparation rather than ad hoc security.

For EDF power solutions, this regulatory environment raises both value and cost. It raises value because customers may prefer a supplier able to manage compliance and institutional relationships. A corporate buyer does not want its renewable project delayed by weak permitting, grid or cyber processes. A public authority wants a developer that can meet procedural expectations. A storage asset participating in system services needs compliance discipline. Local accountability has commercial worth in that environment.

It raises cost because compliance consumes management attention. Cyber controls, incident reporting, vendor risk management, asset inventories, access control, network segmentation, monitoring and recovery exercises all need funding. Grid requirements and market rules require documentation and operational discipline. Safety and environmental rules impose field processes. Public scrutiny can make mistakes more expensive. The larger and more distributed the portfolio, the more compliance becomes a system rather than a file.

Geopolitical risk also matters through supply chains. Renewable equipment supply has faced policy, trade and concentration concerns in recent years, especially around solar modules, batteries, inverters, raw materials and technology dependence. EDF power solutions can mitigate some of that through procurement strategy and group scale, but it cannot escape global supply-chain economics. If equipment prices fall, project economics can improve. If supply chains tighten, warranties fail, cyber rules restrict vendors or trade measures raise costs, the reliability premium must be renegotiated or absorbed.

The RIPE and network layer adds a smaller but related governance task. Resource holders need accurate contacts, secure maintainer practices and provider coordination. If public prefixes support corporate or operational services, route leaks, misconfiguration, DDoS exposure, poor access control or provider incidents can spill into business continuity. The reviewed RPKI status for a sample EDF-routed prefix was unknown, which does not prove weakness but does point to a visible area where stronger public route-origin assurance would improve the reliability story.

The regulatory lesson is that accountability is not a slogan. It is a cost structure. EDF power solutions can turn that cost into customer value only if buyers believe the company reduces their risk more than a cheaper provider would.

Market Signals Support Demand but Cut Both Ways

Several market signals support demand for EDF power solutions' reliability proposition. Corporate decarbonization remains a durable procurement driver. RTE's public electricity reporting for France continues to put renewable generation, storage, flexibility and system balance at the center of power-market discussion. CRE's work on power purchase agreements shows that long-term renewable contracting is a recognized market issue in France. IEA analysis points to growing electricity demand from digitalization and data centers, which strengthens the long-term need for reliable power and grid flexibility.

The June 2026 EDF agreement to sell EDF power solutions in the United States and Canada to KKR is another signal. KKR framed the transaction around electricity-demand growth and renewable infrastructure opportunities. EDF framed it as a transaction for the North American business. This does not directly price EDF power solutions SA in France, but it confirms investor appetite for renewable platforms that can serve rising demand and provide contracted infrastructure exposure. The market is willing to put capital behind the thesis that power reliability and low-carbon supply have strategic value.

Those signals also cut the other way. Investor appetite can raise asset prices and reduce returns for buyers. Demand for renewable projects can intensify competition among developers. Data-center power demand can make grid access more valuable, but it can also trigger congestion, permitting scrutiny and local political resistance. Storage can create new revenue, but as more batteries enter a market, spreads and ancillary-service prices can compress. Corporate buyers may want green power, but they remain price sensitive.

There is also a technology-deflation problem. Renewable equipment costs can fall over time, which helps new projects but can make older contracts look expensive to buyers. Customers may delay decisions if they expect cheaper solar, batteries or better contract terms later. Developers must recover reliability spending while competing against future lower-cost alternatives.

Unofficial signals are thinner. EDF power solutions has public visibility through its website, corporate announcements, recruitment and transaction coverage, but there is little reliable open-market chatter that reveals customer satisfaction, pricing power or network-service performance. That absence should be treated as a confidence limit. It is not evidence of failure. It is evidence that the outside view cannot yet verify the economic premium.

The market backdrop is therefore supportive but not conclusive. Demand for reliable low-carbon energy, storage and flexibility is real. Capital is interested. Regulators are focused on system reliability and cyber resilience. Yet competition, procurement discipline and undisclosed contract economics can still prevent the company from earning excess returns. The thesis works only if EDF power solutions converts reliability into paid, durable contracts rather than absorbing it as overhead.

Those market signals still leave a conservative margin judgment. The central weakness in the public case is not identity. EDF power solutions SA is identifiable through official company materials, EDF group reporting, French registration data and RIPE records. The weakness is margin evidence. The public record does not provide customer-level pricing, contract terms, asset-level availability, network spend, cyber spend, SLA penalties, return on invested capital by project class or cost allocation between development, operations and digital systems.

That gap is common in private infrastructure businesses, but it matters for a telecom-economics lens. Reliability is valuable only when the customer pays more than the supplier spends to create it. If EDF power solutions uses better monitoring, stronger maintenance, professional connectivity and compliance discipline to reduce outages and win long contracts, the cost can create value. If customers treat these capabilities as minimum requirements and award contracts mostly on price, the same cost becomes margin pressure.

The RIPE evidence reinforces the conservative view. A /23 of legacy IPv4 space, visible more-specific routes and Equinix origin are meaningful for resource governance. They are not evidence of a telecom revenue stream. There is no public indication from the reviewed records that EDF power solutions sells IP transit, broadband access, hosting or managed network services to third parties. The company may need reliable internet resources for its own operations, but customers paying for power projects may not separately compensate the network layer.

The energy evidence also requires caution. EDF group reports strong strategic commitment to renewables and storage, but group-level strategy does not guarantee subsidiary-level returns. The KKR transaction shows that renewable platforms can attract capital, but it also shows that EDF is willing to sell assets where strategic or capital-allocation logic points that way. The French battery announcement shows capability, but not profitability. Corporate PPA pages show a product route, but not pricing power.

The most defensible answer to the core question is therefore conditional. EDF power solutions SA can make some customers pay for reliability where the customer needs long-term renewable supply, credible project execution, asset availability, storage response, reporting and maintenance. It is less clear that the public evidence proves enough aggregate premium to cover the full cost of upstream connectivity, equipment refresh, field support and regulatory overhead. The company has the right reasons to fund reliability. Whether customers fully fund it remains undisclosed.

That is not a weak conclusion. It is the correct boundary for the evidence. A company can be strategically important and still face hard unit economics. Reliability is worth money, but not infinite money. The supplier has to prove that avoided downside is worth the price.

What Would Change the Judgment

Several facts would materially improve confidence. The first would be customer-contract evidence. Multi-year corporate PPAs, storage contracts, operations-and-maintenance agreements or public tenders that disclose price structure, minimum commitments, duration, performance obligations and penalty terms would show whether reliability is monetized or merely promised. Names alone would not be enough. The important evidence would be the economic structure: who owns the asset, who carries availability risk, how inflation and power-price exposure are handled, and whether service quality affects payment.

The second would be operating-performance evidence. Public asset availability, battery response performance, maintenance response times, curtailment exposure, forecast accuracy, incident rates or service-credit history would show whether EDF power solutions' reliability system produces measurable results. For the network layer, stronger public routing hygiene such as visible valid route-origin authorizations for the reviewed prefixes, published resilience architecture or audited cyber controls would improve confidence that resource governance is matched by operational discipline.

The third would be cost evidence. Segment-level operating margin, capital employed, maintenance spending, cyber and digital investment, network-provider costs or return on invested capital for EDF power solutions SA would show whether the company earns more than it spends to be reliable. Without that, outside analysis has to infer from group scale and market signals.

The fourth would be customer concentration and renewal data. A reliability business is more valuable when customers renew, expand and accept premium pricing because switching creates risk. It is less valuable when customers rebid aggressively or treat the supplier as interchangeable. Renewal rates, churn, average contract term and customer concentration would make the pricing-power question much clearer.

The fifth would be regulatory clarity. Public mapping of NIS2 scope, energy-market obligations, grid-service eligibility, storage revenue rules and cyber certification would help estimate compliance cost and competitive advantage. Compliance can be a barrier to entry if larger operators handle it better. It can also be an equal burden that compresses margins across the market.

Until those facts are visible, the judgment stays balanced. EDF power solutions SA is a credible renewable power operator with real reasons to own network reliability, maintain number resources and spend on redundant operations. Its RIPE footprint should be treated as evidence of digital operating infrastructure, not as proof of an ISP business. The company can charge for reliability when customers need an accountable long-term energy counterparty. The unanswered question is whether enough customers pay enough, for long enough, to cover the full cost of making that promise durable.