Summary

- Easy Tech Solution SRL is a Civitavecchia-based Italian company. RIPE NCC records list it as an LIR under registration number 10924661001, with the same Via Annovazzi address and Civitanet contact details that appear on the company website.

- The network evidence is material: AS198257 was created in June 2023, the company holds the IPv4 allocation 185.153.0.0/22 and the IPv6 allocation 2a03:aee0::/29, and public routing views show 5 IPv4 and 9 IPv6 routes visible in July 2026.

- PeeringDB classifies the network as Cable/DSL/ISP, reports 1-5 Gbps of traffic, open peering, IPv6 support, one exchange point and no listed facility footprint. The exchange record places the network on Namex Rome at 10 Gbps, but this is not proof of owned fibre routes or physical diversity.

- Civitanet's public offer is local and bundled: fibre up to 2.5 Gbps, high-density Wi-Fi, flat VoIP, virtual switchboards, video surveillance, support in Civitavecchia and a 25 euros per month promotional residential access price.

- The capital-recovery problem is severe. A public business-data aggregator reports 2023 revenue of EUR 348,562, net profit of EUR 21,105, personnel cost of EUR 53,435 and two employees; another reports EUR 349,000 revenue, EUR 72,000 EBITDA and one employee. Those figures are imperfect, but they describe a small operating base beside national carriers and wholesale fibre networks.

- The judgment is conditional. Easy Tech Solution can justify local control if dense local access, business continuity work, public addresses, voice, Wi-Fi and surveillance support create more gross contribution than the cost of RIPE membership, upstreams, exchange ports, equipment, field labour, compliance and customer support. The current public evidence proves capability; it does not yet prove that the capability earns its cost.

Local control starts with a geographic constraint

The incentive for Easy Tech Solution SRL is not to become a national carrier. It is to make local control in and around Civitavecchia worth more than the capital and operating cost required to keep that control. That is a narrower and more demanding proposition.

Civitavecchia is a port city, not a dense metropolitan market like Milan or Rome. The port creates visible demand for connectivity-adjacent services: logistics, tourism, hospitality, offices, retail points, accommodation, security, payment terminals, guest Wi-Fi and public-sector connectivity all need reliable communications. The Porti di Roma authority reported a 2025 cruise record of 3,556,559 passengers in Civitavecchia, a 2.81% increase on 2024, with 862 cruise calls. That does not mean Easy Tech Solution serves the port or its cruise ecosystem.

It does mean the local economy includes time-sensitive service businesses for which internet access is operational infrastructure rather than a household convenience.

The problem is that local relevance is not the same as local pricing power. A Civitavecchia household can compare a local provider's 25 euros per month offer with national fixed-line packages. A small shop can buy broadband from a national carrier, a wholesale-fibre reseller or a mobile bundle. A professional office may move applications to Microsoft, Google or AWS and then buy managed connectivity through a larger integrator. Local control has to be priced against those alternatives, not against an ideal customer who values local repair time without asking what the larger carrier includes.

That is why the first test is not whether Easy Tech Solution has network resources. It does. The test is whether those resources attach to a dense enough customer base and a broad enough service bundle to recover fixed cost. Network control creates optionality: the company can originate its own routes, use its own address space, peer at Namex Rome, buy from multiple upstreams and present itself as more than a reseller. Optionality becomes value only when customers pay for it directly, when it reduces support and supplier cost, or when it protects customers the larger alternatives handle poorly.

The company is identifiable, but its operating boundary is local

The identity evidence is clear. The RIPE NCC member page for Easy Tech Solution SRL lists Via Annovazzi 15 in Civitavecchia, the phone number +39 0766 580583, the email address [email protected] and Italy as the serviced area. The RIPE Database organisation entity gives the same company name, Italy as country, the registration number 10924661001 and an LIR organisation type. The organisation entity was created in May 2016 and last modified in May 2026.

The company website uses the Civitanet brand. It describes Civitanet as a "Wireless Internet Provider" for home and business, with assistance local to Civitavecchia. Its contact section gives Via Vincenzo Annovazzi 15, the same fixed telephone number, a toll-free sales line and the same [email protected] mailbox. The privacy text names Civitanet at that address as data controller. That alignment between RIPE records and the website reduces the risk that the resource records belong to an unrelated holder.

The commercial boundary is still much narrower than the RIPE page's country field. "Areas serviced: IT" is an RIR member-service label, not evidence of national retail coverage. The website's own positioning is local: it says the company designs and manages networks with local support in Civitavecchia, offers rapid intervention, and sells solutions for homes and businesses. PeeringDB gives the network a European scope, but that describes network reach, not retail presence.

Third-party company-data pages reinforce the small-company frame. FatturatoItalia identifies Easy Tech Solution SRL as active, founded in 2010, registered in Rome's company chamber under REA RM 1264715, with ATECO 62.09.09 for other IT-related services. It reports 2023 revenue of EUR 348,562, net profit of EUR 21,105, personnel cost of EUR 53,435 and two employees. Xray Finance reports the same 2023 revenue rounded to EUR 349,000, EBITDA of EUR 72,000, net profit of EUR 21,000, total assets of EUR 458,000, net equity of EUR 131,000 and one employee.

The employee figures differ, and these are public aggregators rather than direct filings inspected here. The right use is directional: the company appears small, not a scaled fixed-access challenger.

That scale matters. A small operator can be profitable if it controls a compact footprint, avoids heavy civil works and sells support-heavy services that national carriers neglect. It can also be trapped between consumer prices and professional-service cost. The legal company is real and the network identity is real. The question is whether the local footprint is dense and differentiated enough.

Civitanet sells more than a connection

The public Civitanet offer is not just commodity internet access. The homepage advertises fibre, high-density Wi-Fi, flat VoIP, virtual switchboards with interactive voice response and call queues, and video surveillance with cloud or local recording. It presents those services as scalable for private users, businesses and public administration, with performance, security and transparency. The fibre card claims speeds up to 2.5 Gbps with low latency and service-level terms on request.

This matters because the business model for a small local ISP rarely works on access alone. If the customer buys only a residential connection, the operator competes on monthly price, installation fee, modem cost and basic reliability. Civitanet's promotional box sets that battlefield bluntly: 25 euros per month, free activation, free modem and no hidden costs. That is a customer-acquisition offer, not evidence of high margin.

The higher-value revenue pools are elsewhere. High-density Wi-Fi for hotels, retail, events and offices can command project fees and support retainers. VoIP and virtual switchboards can attach monthly seats, numbers, call routing and business support to the access line. Video surveillance creates installation, storage, maintenance and remote-support opportunities. Public-address allocation and routing control can serve professional users who need stable inbound reach. Local field response can matter when a site depends on payment terminals, cameras, remote work or guest access.

The company therefore has two possible economic stories. The weaker story is that it is a small retail ISP offering a cheap residential broadband plan in a market where national carriers and wholesale fibre resellers can match or undercut it. The stronger story is that access is the entry product for a local continuity stack: connectivity, LAN design, Wi-Fi coverage, voice, cameras, address management and on-site support. The public website supports the stronger story as an offer. It does not disclose how much revenue actually comes from those higher-contribution services.

That missing mix is central. A EUR 25 monthly access customer generates EUR 300 per year before VAT effects, payment costs, support calls, upstream transit, address sharing systems, customer equipment, installation labour and bad debt. A business Wi-Fi or surveillance project can produce the same gross revenue in a single visit, but it also consumes skilled labour and equipment. Value creation depends on the mix, not on the menu.

The resource footprint is stronger than a reseller's footprint

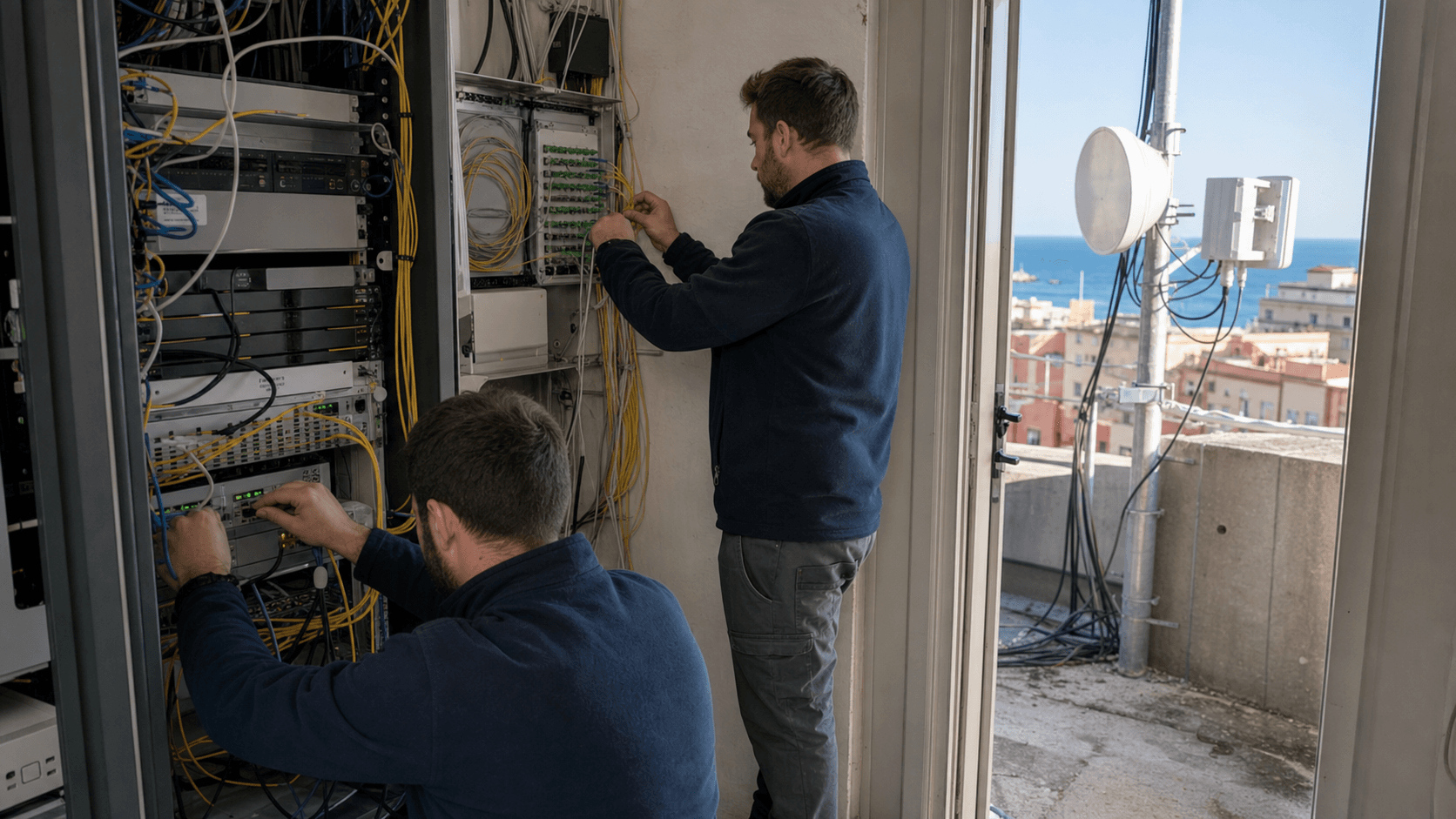

Easy Tech Solution's network-resource evidence is stronger than would be expected from a pure local reseller. The RIPE Database aut-num record for AS198257 was created on 7 June 2023 and names the autonomous system "ASN-EASYTECH". The routing policy lists transit from AS207594 and AS203462, and exports the AS198257:AS-EASYTECH set back to those providers. The same record is maintained by RIPE-NCC-END-MNT and it-easytech-1-mnt.

The IPv4 allocation 185.153.0.0 - 185.153.3.255 carries the netname IT-EASYTECH-20160520, country IT, a Civitavecchia-area geolocation, the organisation ORG-ETSS3-RIPE and ALLOCATED PA status. It was created in May 2016. The IPv6 allocation 2a03:aee0::/29 carries the same netname and organisation, was created in June 2023 and has ALLOCATED-BY-RIR status. These are not marketing claims; they are public registry records.

RIPEstat's AS overview for AS198257 says the holder is "ASN-EASYTECH Easy Tech Solution SRL" and that the AS was announced at the query time on 11 July 2026. Its announced-prefixes data for the preceding two weeks listed 185.153.0.0/22 and the four component /24 routes, plus 2a03:aee0::/29 and eight visible /32 IPv6 routes. RIPEstat's routing-consistency view showed the listed prefixes in both BGP and RIPE whois, and it identified 8 observed neighbours. Its RPKI validation API returned "valid" for both 185.153.0.0/22 originated by AS198257 and 2a03:aee0::/29 originated by AS198257.

PeeringDB adds a commercial interconnection layer. The network profile for Easy Tech Solution lists ASN 198257, the Civitanet website, a Civitanet looking glass, IRR as-set AS198257:AS-EASYTECH, Cable/DSL/ISP as network type, 10 IPv4 prefix-limit information, 2 IPv6 prefix-limit information, traffic of 1-5 Gbps, mostly inbound traffic ratio, Europe scope, IPv6 support, open peering, one exchange point and no listed facilities. The netixlan record places the network at Namex Rome: VLAN Peering with a 10,000 Mbps port, IPv4 address 193.201.28.222, IPv6 address 2001:7f8:10::19:8257 and route-server participation.

That is valuable evidence of control. It means Easy Tech Solution can run BGP, present its own origin, manage route objects and peer in Rome. It also sets a boundary on what is proven. AS ownership does not prove fibre ownership. Prefix origination does not prove customer count. A 10 Gbps exchange port does not prove sustained demand. PeeringDB traffic bands are self-reported and deliberately broad. "No listed facilities" does not mean no physical presence; it means the voluntary PeeringDB record does not disclose one.

The resource footprint gives the company tools to negotiate and differentiate. The business still has to monetize those tools.

IPv4 scarcity makes that monetization more important. RIPE NCC says it exhausted its remaining IPv4 pool in November 2019 and that networks now often mitigate scarcity through transfers or address-sharing technologies such as CGNAT. Easy Tech Solution's /22 contains 1,024 IPv4 addresses before any subdivision, customer assignment, infrastructure use or conservation policy. That is not enough to give every mass-market customer a dedicated public address if the customer base grows materially, but it is enough to create a managed address pool, reserve public addresses for business customers and reduce total dependence on upstream addressing.

The economic value is not the theoretical address count; it is the ability to decide which customers receive scarce public reach and what they pay for it.

Capital recovery begins before customer growth is visible

The cost of local network control arrives before the payback is visible. Easy Tech Solution has to pay for RIR membership, routing administration, upstream capacity, exchange access, routers, switches, customer equipment, fibre drops, wireless gear where applicable, field tools, vehicles, installation labour, support labour, billing, compliance and bad-debt management. Many of those costs are fixed or semi-fixed over the customer base.

RIPE's 2026 charging scheme sets the annual contribution at EUR 1,800 per LIR account, with additional charges for independent resources and ASN assignments as defined in the document. That fee is not the largest cost in an ISP budget, but it is a useful marker: resource independence is not free, and the burden is proportionally heavier for a company with a few hundred thousand euros of revenue than for a national carrier.

Upstream and exchange economics are more important. A local ISP wants enough independent reach to avoid being captive to a single supplier. The RIPE aut-num record lists Connectivia and NovaConn as transit providers. BGP.tools also shows AS203462 NOVACONN SRL and AS207594 Connectivia S.r.l as upstreams, with IPv4 and IPv6 connectivity. PeeringDB shows Namex Rome exchange participation. This is a sensible setup: buy full reach from upstreams, peer locally where it lowers latency or transit cost, and preserve enough routing independence to change suppliers if commercial terms worsen.

But two logical upstreams are not the same as fully independent physical paths. Public routing records do not disclose whether both suppliers enter Civitavecchia through the same duct, site, building, power dependency or regional aggregation route. They do not show committed capacity, burst terms, outage credits or congestion. A small operator can look multihomed in BGP and still depend on shared infrastructure underneath.

The field cost is even harder to infer. Civitanet advertises fibre up to 2.5 Gbps, dense Wi-Fi and video surveillance. Those services require equipment procurement and skilled visits. If most work is customer-funded project labour, the model can be resilient. If the operator gives away installation and customer equipment to win low-priced access accounts, payback stretches. The website's residential promotion includes free activation and a free modem, which is attractive to the buyer but pushes recovery into future monthly margin.

Capital recovery is therefore a cohort question. How much does it cost to connect and support a household, a shop, a hotel, a public office or a business with Wi-Fi and voice? How long does that customer stay? What gross contribution remains after transit, support and equipment? Without those facts, visible growth in routes, website offers or exchange participation cannot be treated as value creation.

A simple illustration shows the constraint. At 25 euros per month, 1,000 fully paying access customers would produce EUR 300,000 of annual gross billings before VAT treatment and before any other services. That would still have to cover upstreams, exchange connectivity, customer equipment, billing, support, field work, site costs, bad debt, marketing and corporate overhead. A local network with fewer customers can work if the average customer buys business services or project work. A local network with many low-price customers can work if support costs and churn are very low.

A local network with both low density and low average revenue struggles, even if its routing setup looks technically respectable.

Pricing power is the weak link

The public price signal is the hardest evidence for Easy Tech Solution. A EUR 25 per month consumer promotion is not unusual in Italy, but it limits the room for network-control cost. If activation and modem are free, the operator needs low churn, low fault rates, dense installation geography and upsell into higher-value services. Otherwise, the first year of a customer relationship can be consumed by acquisition cost.

The broader Italian market confirms the pressure. AGCOM's Communication Markets Monitoring System for n. 1/2026, updated to December 2025, reported 20.53 million fixed-network lines and 19.38 million broadband and ultrabroadband lines. Broadband and ultrabroadband lines increased by 314,000 over the year, or 1.6%, but the mix shifted sharply: DSL was down 22.6%, FTTC was down 8.9%, FWA was up 13.2% and FTTH was up 19.6% to 7.01 million accesses.

That sounds like a growth market, but growth in access count and speed class does not guarantee pricing power. The national operators dominate the base. AGCOM's December 2025 broadband and ultrabroadband share chart gives TIM 32.7%, Fastweb+Vodafone 29.6%, Wind Tre 14.6%, Sky Italia 4.5%, Iliad 3.6%, Tiscali 2.8%, Eolo 2.6% and Others 9.8%. In business broadband and ultrabroadband lines, TIM and Fastweb+Vodafone together held 71.5% of the 3.005 million business lines. "Others" held 8.8%.

For a small local operator, those shares mean three things. First, national carriers have scale advantages in procurement, customer acquisition, brand trust and back-office systems. Second, the consolidation of Fastweb and Vodafone creates a stronger converged fixed-mobile competitor. Third, the "Others" bucket is large enough for regional specialists but fragmented enough that no small provider can assume market-wide pricing discipline.

Rising usage compounds the tension. AGCOM reported fixed-network download traffic of 59.10 exabytes in 2025, up 11.0%, and upload traffic of 8.33 exabytes, up 15.0%. Average daily fixed traffic reached 189.2 petabytes, up 11.8%. Customers expect more capacity each year, while mass-market prices stay visible and comparable. If Easy Tech Solution cannot pass usage growth into price, it needs falling unit transit cost, better peering, denser access utilization or more service revenue per customer.

The positive side is that a small operator does not need to win Italy. It needs enough profitable Civitavecchia accounts and business sites. The negative side is that national pricing sets the reference point before the local operator can explain why its support is worth more.

That reference price also changes the negotiation with business customers. A small business may understand that downtime is costly, but it still begins the conversation with the household broadband price it sees online. To sell a materially higher monthly fee, Easy Tech Solution must define the extra product: static public addressing, monitored router, voice continuity, guest Wi-Fi separation, camera uptime, backup access, priority repair or a measurable service commitment. If the premium is not named, the customer will treat the local provider's extra work as part of the basic line.

That is how local service quality can become a subsidy rather than a margin source.

Supplier dependence turns control into a shared asset

Local control is not absolute. Easy Tech Solution controls an AS, routes and address space, but it still depends on upstream networks, exchange infrastructure, equipment vendors, wholesale fibre availability, power, ducts, landlords and customer-premises equipment. The economic question is where control changes the outcome and where it merely adds cost.

The upstream dependency is explicit in the RIPE aut-num record: AS198257 imports default reach from Connectivia and NovaConn. NovaConn's own RIPE record describes it as an internet service provider and lists AS198257 among customer relationships. Connectivia's public routing record shows a larger interconnection posture, including transit from major carriers and peering at Namex. This can be good for Easy Tech Solution because upstream suppliers bring broader reach and content proximity that a local operator could not build alone.

It also means supplier price and quality feed directly into margin. If upstream transit, exchange port cost, remote peering, equipment replacement or colocation cost rises faster than customer revenue, the local operator bears the squeeze. If an upstream outage affects both logical paths through shared transport, the customer sees the local brand, not the hidden supplier chain.

Wholesale fibre is a second dependency. Open Fiber says it operates Italy's largest pure fibre infrastructure on a wholesale-only model with equal access for operators. Its homepage, updated 30 April 2026, reports 4.28 million customers served, 6.34 thousand FTTH municipalities covered, 17.428 million FTTH connected property units and 168,037 km of network infrastructure. FiberCop's Piano Italia 1 Giga page and the Italian government's Plan Italy 1 Giga materials point to publicly supported gigabit coverage targets of at least 1 Gbit/s download and 200 Mbit/s upload in areas lacking adequate private investment.

For Easy Tech Solution, wholesale fibre can be both threat and tool. It is a threat because a large carrier or reseller can enter a street without replicating every civil asset. It is a tool because a local provider can use wholesale access to expand or avoid uneconomic builds, then differentiate with support, voice, Wi-Fi, surveillance and routing. The value is not in owning every metre of cable. It is in owning the customer relationship and the parts of the local network where control improves restoration, customization or cost.

The most dangerous strategy would be to pay for ownership everywhere while earning reseller economics. The best strategy would identify the local segments where Easy Tech Solution's own infrastructure changes gross margin and customer retention, then buy or rent the rest.

National carriers and wholesale fibre set the ceiling

Competition in Civitavecchia is shaped by Italy's national broadband transition. The Italian and EU policy frame is explicit: Italy's ultra-broadband strategy aims to provide gigabit connectivity to all, and the European Commission's country page says Plan Italy 1 Giga has a planned allocation of EUR 3.8 billion to provide 1 Gbps download and 200 Mbps upload in grey and market-failure areas, covering 8.5 million households by 2026. The Italian government's own page says the plan was designed to connect civic addresses that had no existing or planned network capable of at least 300 Mbps download in peak hour.

This public funding and wholesale-network expansion reduce the scarcity value of a local access footprint. When fibre was rare, a local operator with routes, poles, building access or wireless coverage could price the scarcity. As FTTH and FWA availability expands, the buyer asks a different question: why this provider?

National carriers answer with bundles, mobile convergence, television, brand, call centres, financing and discounts. Open Fiber and FiberCop change the economics by letting multiple service providers sell over a shared physical network in covered areas. Cloud providers and content networks improve local performance through Italian regions, edge locations and private-connectivity ecosystems. Each of these forces makes raw access less differentiated.

The local operator can still win, but it has to win on a different axis. It can answer the phone locally. It can design Wi-Fi for a hotel or retail space. It can combine a fibre line, public address, VoIP numbers, cameras and on-site support in one accountable contract. It can handle a small public office or SME whose work is too small for a national enterprise team and too operationally important for a low-touch consumer plan.

That is a valuable niche if priced correctly. It is not a protected niche. A larger carrier can discount access to win the customer, then attach cloud, mobile and security services. A systems integrator can resell connectivity and own the managed-service relationship. A wholesale network can make physical access less scarce. Easy Tech Solution's defence is service density and trust, not scale.

Cloud substitutes compete for the margin above access

Cloud platforms do not remove the need for a local access line. They do change who captures the higher-margin part of the customer's IT budget. AWS says it plans to invest more than EUR 1.2 billion over five years to expand its Italian cloud infrastructure and services in the AWS Europe (Milan) Region, building on offices in Milan and Rome, two Direct Connect locations and 16 edge locations across Milan, Rome and Palermo. Google Cloud's Milan region launched with three zones and standard services, with data residency controls, encryption, organisational policies and VPC Service Controls.

Microsoft ExpressRoute lets customers extend on-premises networks into Microsoft cloud services over private connections through a connectivity provider, with bandwidth options from 50 Mbps to 10 Gbps and Milan peering locations listed for Italy North.

Those facts matter because Easy Tech Solution's best economic case is not simply "we sell internet." It is "we keep a local organisation connected and operational." Cloud platforms and larger carrier partners are moving into that same budget line. A business can put applications in the cloud, buy Microsoft 365 or Google services, use a national carrier for the line, and treat local hardware as minimal. If that happens, the local ISP may keep only the access margin while the cloud and integrator capture software, security, backup, identity and management spend.

The opportunity is to make cloud adoption increase the need for local continuity. A shop using cloud point-of-sale systems needs a reliable primary line and a tested backup path. A hotel using cloud booking and Wi-Fi authentication needs local wireless design and monitoring. A professional office using cloud voice or collaboration tools needs LAN, voice quality and support. A surveillance customer using cloud recording needs upstream stability and camera maintenance.

In that model, cloud is not an enemy. It is a reason to sell continuity. But continuity has to be specified and priced. A customer paying 25 euros per month for residential internet is not buying dual access, failover testing, backup power, priority restoration and managed Wi-Fi. A business that depends on cloud workflows might pay for those things if the local provider explains the risk and proves the operational difference.

That is where Easy Tech Solution's local-control footprint could earn its cost. Not by trying to out-cloud the cloud platforms, and not by matching a national carrier's marketing budget, but by owning the last-mile accountability that cloud services still require.

The strategic risk is disintermediation of the relationship above the access line. When a cloud vendor, national carrier or managed-service provider owns identity, email, backup, endpoint management and security, the access provider becomes easier to replace. When the local provider owns the access line plus site documentation, Wi-Fi topology, voice numbers, camera placement, failover testing and emergency contact process, it becomes harder to substitute without operational friction. The difference is not branding; it is stored local knowledge.

Easy Tech Solution's website points toward that broader service position, but the public evidence does not show how much of the customer base has bought it.

Local demand is visible, but customer concentration is not

The public evidence gives signs of demand, not a full customer map. Civitanet advertises services for homes, enterprises and public administration. Its service menu fits local SMEs, hospitality, retail, offices and sites that need Wi-Fi, voice and cameras. Civitavecchia's port economy gives the local market more operational texture than a purely residential town. The company's RIPE and PeeringDB records show a real routed network rather than a purely virtual storefront.

What is missing is concentration. The company does not publish subscriber count, active business sites, churn, average revenue per user, top-customer exposure, split between access and project revenue, or the share of revenue coming from port-related, public-sector, hospitality, residential or professional customers. Public company-data aggregators show small revenue and low headcount, but not mix.

A small local provider can be safe with many tiny prepaid customers and several high-margin project accounts. It can be fragile if a few businesses or public institutions carry the margin while residential lines barely cover support. It can also be fragile if most revenue comes from project work and the access network is maintained for strategic reasons rather than cash contribution.

Unofficial market signals are mixed and should be treated carefully. Cylex lists Civitanet as an internet-service provider at Via Vincenzo Annovazzi 15, shows opening hours and contact details, and displays a Yably-derived score of 1.8 out of 5 from 21 reviews. Facebook search results show a Civitanet FIBRA presence and ISP-style promotional language, but access to the page is limited and social metrics are weak evidence. These signals may indicate customer dissatisfaction, small local visibility or normal review-platform bias. They do not prove service quality or financial risk.

The useful conclusion is narrower. Easy Tech Solution has enough public presence to be a real local operator, but not enough disclosed customer evidence to prove a durable moat. The evidence that would matter is not a follower count or a review score. It is retention by cohort, support ticket rate, business-site count, gross margin by product and the number of customers paying for more than commodity access.

Customer concentration would change the risk assessment in both directions. A few hotel, retail, public-office or logistics customers paying for managed Wi-Fi, voice and surveillance could make the company more profitable than its headline access price suggests. The same concentration could also create cliff risk if one buyer changes supplier or if a larger carrier bundles the site into a national contract. Many small residential accounts would reduce single-customer risk but increase support intensity and acquisition payback pressure. The current evidence is not enough to choose between those cases.

Regulation and operational risk raise the fixed burden

Italian telecom is a liberalised market, but not an obligation-free market. The ICLG 2026 Italy telecoms chapter summarizes the framework: public electronic communications networks and services require general authorisation from the Ministry of Enterprises and Made in Italy under the Electronic Communications Code, with AGCOM supervision. It also describes traffic-data retention, lawful-interception obligations for authorised public communications networks and services, open-internet rules, cybersecurity responsibilities and the role of the Italian National Cybersecurity Agency.

For a small ISP, this is another scale problem. Compliance costs do not fall neatly with headcount. A provider needs accurate customer records, privacy handling, security processes, abuse contacts, cooperation procedures, consumer-contract discipline, transparency and resilience planning. None of those tasks is as visible as a fibre speed claim, but failure can create legal, reputational and operational cost.

The routing layer adds its own duties. RIPE membership and address allocations require accurate registry data. RPKI and IRR records reduce route-hijack and filtering risk. Abuse handling matters because IPinfo tags at least one IP in AS198257 with recent BitTorrent and VPN signals; those tags are not accusations against the company, but they illustrate that residential and business access networks attract abuse, copyright and security workload. A small operator with its own resources cannot simply send every issue upstream.

Operational risk is also physical. Civitavecchia is a coastal port city near Rome; field service may involve older buildings, ducts, wireless sites, customer premises, port-adjacent traffic and seasonal demand. Power, equipment availability, civil-work permission and customer-premises faults can all turn a low monthly fee into a support burden. A local operator's advantage is that it can respond locally. Its downside is that the same local field team covers many failure types.

This is why "strategy without resource allocation is marketing." The website's promise of rapid local intervention is valuable only if the company funds enough people, spares, monitoring and supplier escalation. The public financial snapshots suggest a very lean organisation. Lean can mean efficient. It can also mean under-resourced if the network and customer base are broader than the staff can support.

The judgment turns on proof of paid continuity

The base judgment is neither dismissal nor endorsement. Easy Tech Solution SRL has a real local-network footprint, a coherent local brand, a service bundle that could support higher-margin SME work, and public routing evidence that separates it from a simple reseller. It also operates in a market where national carriers, wholesale FTTH, FWA, cloud platforms and managed-service substitutes cap access pricing and compete for the value above the line.

The company can recover the cost of local control if three conditions hold. First, its Civitavecchia footprint must be dense enough that installation, support and upstream costs fall per active account. Second, it must sell enough higher-contribution services - business fibre, public addresses, VoIP, virtual switchboards, high-density Wi-Fi, cameras and support - to keep gross margin above the cost of access operations. Third, it must turn routing and local control into measurable continuity that customers pay for, not just into technical inventory.

The public evidence proves the inventory better than the economics. It shows resources, routes, exchange presence, advertised services, promotional pricing and small-company financial signals. It does not show subscriber cohorts, churn, margin, capex, debt, customer concentration, physical route diversity, service levels sold, or the share of revenue tied to managed local services.

The facts that would change the judgment are specific. A disclosed count of active lines by product and municipality would show density. Gross margin by residential access, business access, voice, Wi-Fi and surveillance would show whether the bundle pays. Capex and depreciation would show whether the network is being renewed or sweated. Upstream contracts and physical path maps would show whether two logical providers create real resilience. Customer-retention data would show whether local support beats national substitutes.

A list of business and public-sector service categories, without exposing private customers, would show whether the company has moved beyond EUR 25 access economics.

Until then, the best reading is cautious. Easy Tech Solution has the tools of local network control and a market where local continuity can matter. The risk is that customers receive the benefit of that control at commodity prices while the company carries the fixed cost. The value creation test is whether local accountability becomes a priced product, not merely a local promise.