Summary

- Horizon Teleports GmbH looks more substantial than a paper resource holder: public company pages, RIPE records, WTA certification references and partner material point to a Moosburg teleport with 16 antennas, C-, Ku- and Ka-band capability, 24/7 monitoring claims, redundant power, dark-fiber connectivity, AS198218 and active IPv4 and IPv6 announcements.

- The margin question is unresolved because the public record proves infrastructure and activity better than it proves pricing power. The company can sell local accountability, German/EU operational presence and bespoke satellite/IP support, but it still depends on satellite operators, upstream carriers, skilled engineers and customer-specific projects that may cap operating leverage.

Local Accountability Is The Product, Not The Slogan

The economic incentive for Horizon Teleports GmbH starts with a buyer who does not want to be reduced to a support ticket inside a distant global platform. A broadcaster with a live channel, a maritime operator with a crew welfare link, a telco serving a remote site, or a government-linked user with a resilient communications need may care less about the abstract language of satellite connectivity and more about a named operations team, a known facility and a reachable escalation path.

That is the local accountability buyers might pay for: somebody in Moosburg, backed by a network operations centre and physical ground infrastructure, is responsible for keeping the link working.

That value proposition is credible only if the buyer's problem is complex enough to need it. The public material around Horizon Teleports describes uplink and downlink services, IP trunking, GSM backhauling, carrier monitoring, broadband, mobility and managed pay-TV functions. Those are not one uniform product. They range from raw transport to managed technical operations. The more the sale resembles a managed outcome, the more room there is for a premium. The more it resembles commodity capacity resale, the less room there is for differentiation.

The company therefore sits in a difficult but potentially useful middle position. It is not merely an address in a RIPE member list. It has public evidence of a teleport site, antenna assets and operational services. Yet it is also not a satellite owner, a hyperscale cloud platform or a global carrier with massive purchasing power. It must persuade customers that the human and physical nearness of a German teleport is worth paying for even when cheaper or simpler routes exist.

For an Elias Ward reading, the question is not whether the service sounds necessary. Many communications services sound necessary when described from the supplier's side. The question is who bears the downside when a link fails, when a satellite beam changes, when a broadcast feed needs urgent troubleshooting, when a compliance team asks where the operational responsibility sits, or when a remote network needs engineering attention outside office hours. If the downside sits with the customer's revenue, reputation, safety or regulatory position, then reachable accountability has value.

If the downside is modest and the workload can be shifted to a platform dashboard, then Horizon's local support becomes a cost centre before it becomes pricing power.

That distinction matters because the cost of providing accountability is real. It requires engineers, tools, spectrum and equipment competence, maintenance, power resilience, upstream diversity, satellite relationships, customer support discipline and enough spare capacity to absorb faults. A small teleport cannot talk its way into margin. It has to convert operating control into customer willingness to pay.

What Horizon Teleports Is Actually Selling

Horizon Teleports presents itself as a teleport facility operated from Moosburg, north of Munich, with services across broadcast, data, broadband, GSM backhaul, carrier monitoring, mobility, maritime, offshore and pay-TV managed services. Its own pages say the facility provides access to satellites from 55 degrees west to 78 degrees east and supports C-, Ku- and Ka-band services. Its service descriptions also place the company in workflows where satellite links meet terrestrial IP and media operations: video contribution, distribution, IP trunking, broadband networks, aviation and offshore connectivity, and managed OTT or pay-TV elements.

That mix is economically important. A pure capacity broker is exposed to buyer comparison and supplier price pressure. A pure managed service provider can earn more if it owns workflow knowledge, customer context and operational credibility. Horizon appears to be trying to sell the latter, but much of its public evidence still needs to be read carefully. The website contains specific infrastructure claims, but it also contains duplicated sections and visible template remnants.

That does not invalidate the operational claims, but it means the strongest public facts are the ones corroborated by other sources: RIPE records, WTA certification references, HorizonSat material, local press, partner announcements and observed routing data.

The company identity is clear enough for a research profile. Horizon Teleports GmbH gives its address as Degernpoint K7, 85368 Moosburg an der Isar. Its imprint names the Munich district court commercial register number HRB 201439, a Munich registered office, German VAT number DE 285 496 150 and Bundesnetzagentur as regulatory authority. RIPE's organisation record separately identifies Horizon Teleports GmbH as a German local Internet registry with the same broad Moosburg location and HRB reference.

Public company directories also classify it within satellite telecommunications and show the company as active, although those private directories are secondary evidence rather than statutory filings.

The operating boundary is also clearer than the financial boundary. Horizon Teleports is described in older public launch material as a division or subsidiary connected to Dubai-based HorizonSat. HorizonSat's own website says it owns a state-of-the-art Tier-3 teleport north of Munich and describes Horizon Teleports as part of its technical support and service delivery architecture. A 2026 ABS announcement calls Horizon Teleports HorizonSat's Germany-based subsidiary and frames it as a ground-services partner for EMEA connectivity.

That supports a group context, but it does not disclose transfer pricing, ownership percentages, customer contracts, revenue, debt, capex, or whether value is captured in the German company or elsewhere in the group.

The clean conclusion is narrower than the marketing language. Horizon Teleports GmbH is best read as a German satellite ground-infrastructure and managed-connectivity operating company within a broader HorizonSat commercial orbit. It sells local execution, antenna access, IP and broadcast integration, monitoring and support. It does not prove, from public sources alone, that it owns the satellite capacity, controls the end-customer relationship in every case, or captures the full economics of the services in which its facility participates.

The Moosburg Boundary Is Physical, Not Just RIPE Paper

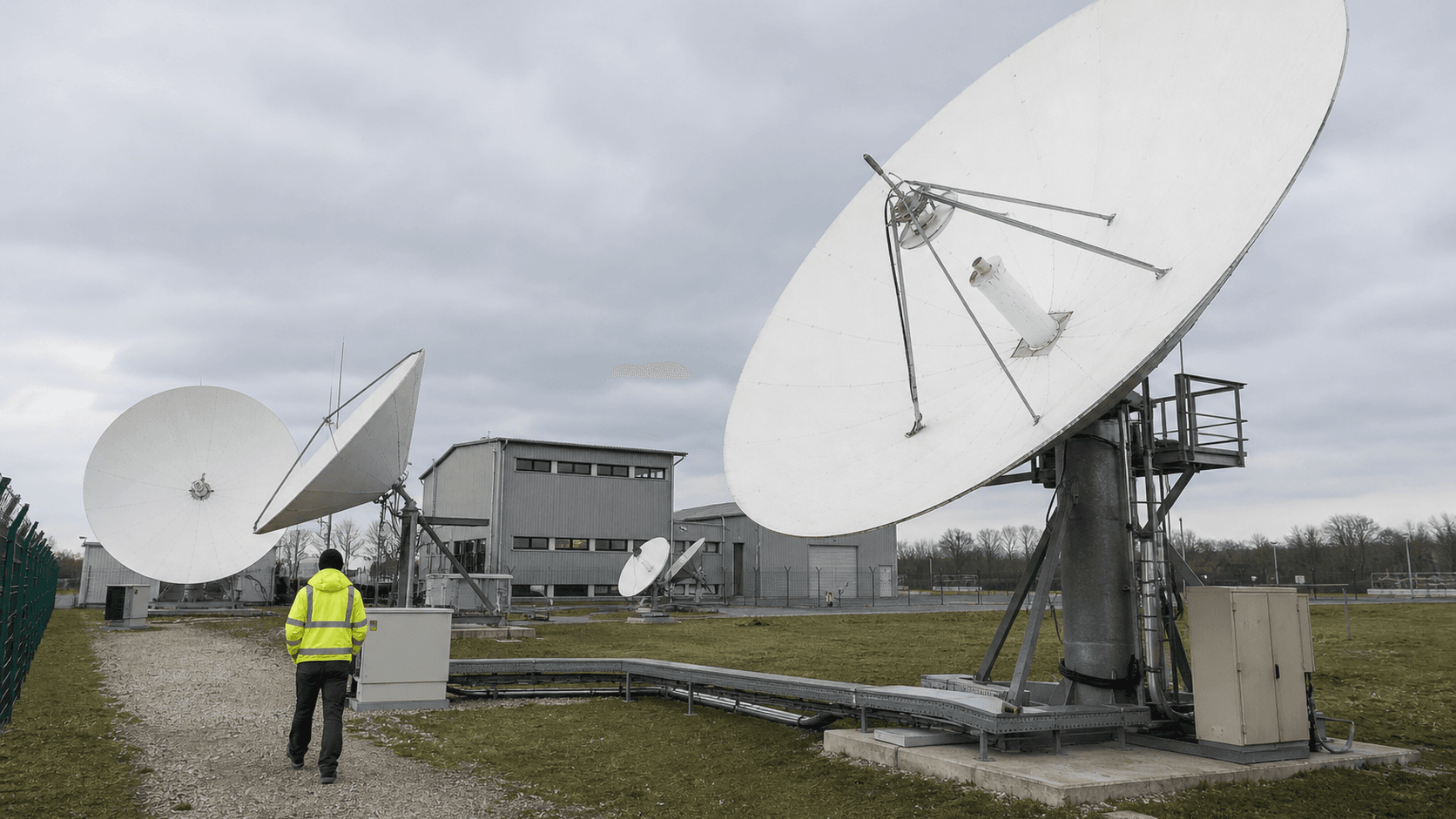

The strongest evidence for Horizon Teleports is physical. Its public facility page describes an outdoor infrastructure base of 16 antennas ranging from 2.4 metres to 9.4 metres, with rain blowers, hot-air de-icing on larger antennas, motorised azimuth and elevation control, full C-, Ku- and Ka-band support, redundant low-noise amplifier systems, redundant high-power amplifiers, fibre links through the transmit and receive chain, antenna controllers and separate shelters for each antenna.

It also describes indoor infrastructure with remotely controllable power distribution units, redundant transformers, UPS backup, diesel generator support, matrix switching and redundant dark-fibre IP connectivity.

Those details matter because teleport economics are equipment economics before they are software economics. Antennas, RF chains, HPAs, LNAs, converters, controllers, shelters, spectrum assignments and power resilience do not scale like a web application. They require procurement, installation, preventive maintenance and specialist troubleshooting. Even if the company can reuse one facility across many customers, each new managed link can add configuration work, monitoring complexity and supplier coordination. The cost base is not infinitely variable.

The original Moosburg launch material adds useful context. It describes the facility as built on a 17,000 square metre site, with a network operations centre, server room and antenna park. It says the first eight 7-metre and 9-metre antennas were installed around the early operating phase and that the plan was to reach 16 antennas by the end of 2014. The later facility page's 16-antenna claim is consistent with that build-out path. Local press coverage of the antenna dispute also supports the reality of a physical antenna project, because the controversy concerned whether the company could build multiple parabolic antennas at the site.

WTA certification references add another layer. Horizon's own page says the Moosburg teleport achieved Tier 3 Full Certification under the World Teleport Association program. Other WTA-related public material explains that full certification involves independent validation after a questionnaire and that tiers run from 1 to 4, with 4 highest. The certification is not a financial audit and should not be treated as proof of profitability, but it is useful evidence that the facility was evaluated against operational standards rather than simply described in marketing copy.

The public facility claims also reveal why margin is demanding. A teleport that promises 99.90 percent uptime or says actual availability has been 100 percent over a prior three-year period is selling reliability. Reliability consumes capital. Backup generators, UPS systems, dark fibre, redundant amplifiers and 24/7 monitoring do not pay for themselves unless customers pay enough for resilience or unless the same infrastructure supports many revenue streams. The site can create operating leverage if it is well utilised. It can become a fixed-cost trap if demand is lumpy, customer-specific, or won mainly on price.

That is why the Moosburg boundary is central to the investment view. The facility gives Horizon a tangible reason to exist. It also creates the cost hurdle the company must clear.

The Network Footprint Gives Buyers A Local Control Point

The network-resource evidence gives Horizon Teleports a second form of operating reality. RIPE NCC lists Horizon Teleports GmbH as a member in Germany, with a Moosburg address and service area in Germany. RIPE's organisation entity identifies ORG-htG4-RIPE as Horizon Teleports GmbH, country DE, organisation type LIR, with a created date in 2011 and a last-modified date in May 2026. Its aut-num entity for AS198218 gives the AS name HTS-MOOSBURG, status assigned, and import and export policy with AS1299 and AS174.

That is useful because it shows the company is not just using someone else's network identity in public marketing. It holds and operates an autonomous system associated with its Moosburg name. RIPEstat's overview on 13 July 2026 showed AS198218 announced. RIPEstat's routing-status data showed 8 IPv4 prefixes representing 14,848 IPv4 addresses and one IPv6 prefix at /32 scale, with full visibility among the checked RIS peers at that query time.

The announced-prefixes feed listed examples including 82.205.160.0/21, 82.205.168.0/21, 82.205.176.0/21, 164.40.160.0/21, 82.205.202.0/23, 82.205.204.0/22, 82.205.208.0/20, 82.205.128.0/22, 82.205.184.0/24 and 2a03:d080::/32.

Routing evidence is not the same as revenue evidence. It does not prove how many customers are live, how much traffic is paid, or whether the IP space is used for Horizon's own customers, HorizonSat group customers, third-party assignments, or legacy arrangements. It does, however, show a public internet control point with upstream dependencies and active resource management. For a buyer that wants satellite capacity tied into IP services, that matters.

The upstream pattern also reveals the independence limit. RIPE and RIPEstat identify AS1299 and AS174 as upstream neighbours or import/export counterparties. AS1299 is Arelion's global backbone. AS174 is Cogent. Both are large carriers. Horizon can control its local teleport and AS policy, but it still depends on upstream IP providers for broader internet reach. If those costs rise, routes degrade, contracts change, or the economics of IP transit shift, Horizon's margin absorbs the effect unless it can pass costs through.

RPKI validation is a positive operational signal. RIPEstat showed valid route-origin authorisation for checked prefixes such as 82.205.168.0/21 and 2a03:d080::/32. In a market where route leaks and mis-originations can hurt service credibility, valid RPKI posture supports the argument that Horizon has at least some disciplined network-resource management. It still does not prove customer concentration, profitability or support quality. It does prove that the company's number-resource footprint is active enough to be part of the business model rather than a dead registry relic.

For margin, the network footprint creates both product value and cost. It lets Horizon offer local control and routing accountability. It also ties the company to upstream carrier bills, resource governance, abuse handling, security practice and operational monitoring.

Revenue Depends On Managed Outcomes, Not Raw Capacity

Horizon's revenue quality depends on whether customers buy managed outcomes or interchangeable inputs. The official service menu is broad: TV distribution, TV contribution, IP trunking, carrier monitoring, broadband, GSM backhauling, aeronautical connectivity, mobility, offshore and maritime connectivity, and pay-TV managed services. HorizonSat's pages add managed broadband, private corporate networks, turnkey deployment and technical support.

ABS's 2026 partnership announcement describes a unified suite combining ABS satellite coverage with Horizon Teleports' ground capabilities for IP trunking, carrier monitoring, broadband connectivity, GSM backhauling and mobility solutions.

These services have different margin profiles. Carrier monitoring can be a specialist service if a satellite operator or broadcaster values trained staff, measurement discipline, alerting and interference detection. Managed pay-TV or OTT support can carry workflow value if Horizon handles encoding, conditional access, monitoring, uplink redundancy, origin packaging and customer-specific operations. GSM backhaul and broadband can be valuable where terrestrial infrastructure is weak or where quick restoration matters. But raw bandwidth, simple uplink capacity and generic IP transit are easier to compare on price.

The company therefore needs the customer to pay for avoided complexity. A broadcaster can buy cloud encoding from AWS, content delivery from Akamai, capacity from satellite operators, connectivity from carriers and remote support from systems integrators. A maritime or remote-site buyer can compare GEO services, LEO services, VSAT integrators, Starlink resellers, Eutelsat OneWeb partners and regional telecom providers. Horizon's route to margin is to make the bundle easier, more accountable and more resilient than a do-it-yourself mix of suppliers.

That route is plausible for complex customers. If a buyer has a live television feed, an offshore platform, a remote network, a government-linked site or a multi-country EMEA requirement, one accountable engineering team may be worth more than a cheaper capacity quote. A one-stop shop can reduce internal coordination cost. Local German infrastructure can also matter to buyers that want an EU operating anchor, a known regulatory environment, or a terrestrial handoff point in Europe.

The risk is that "one-stop shop" becomes a low-margin service wrapper. If Horizon buys satellite capacity, relies on upstream carriers, runs specialist equipment and supplies 24/7 staff, then a managed sale must carry enough gross margin to pay for all of that. Customers may value support but still refuse to pay a durable premium if they can threaten to move the workload to a larger teleport, a satellite operator's managed service, a global network integrator, or a cloud-centric workflow.

The public record does not disclose revenue, average contract length, churn, utilisation, gross margin, or customer mix. That absence matters. The infrastructure can support a serious business, but the economics remain unproven until Horizon shows whether its customers buy accountable operations at premium rates or mostly buy commoditised satellite/IP capacity with support included.

The Cost Base Is Built For Reliability Before Growth

Horizon's cost base is shaped by reliability promises. A teleport that keeps antennas heated, powered, redundant and staffed cannot operate like a light reseller. The public facility page lists redundant transformers, UPS capacity, generator backup, remote-controlled PDUs, matrix switching, dark fibre and redundant RF elements. The services page describes trained staff offering carrier monitoring across a wide look angle. HorizonSat's support page says the Dubai NOC is backed by Horizon Teleports' Munich NOC and that staff include satellite, video and IP expertise.

A job listing for teleport or satellite communication engineers describes experience with dish antennas, LNAs, HPAs, frequency converters, RF over fibre, link budgets, EIRP, beamwidth, spectrum analysers, troubleshooting and customer support.

That tells us where the labour cost sits. Horizon needs people who can understand RF, satellite link budgets, IP circuits, media workflows and customer escalation. This is not a generic call-centre model. It is a specialist operations model. Specialist operations can be defensible if the know-how is scarce and the consequences of failure are high. They can also be expensive, especially in Germany, where technical labour, compliance, insurance, power and facility maintenance are not low-cost inputs.

The company also has supplier costs that grow with service activity. Satellite capacity must be procured, leased, bundled or partnered. Uplink chains require equipment upkeep. Backhaul to international points of presence needs carrier relationships. IP transit uses upstream networks. Broadcast and OTT services involve encoding, conditional access, CDN or cloud pieces. Every additional "managed" promise can add more support load if the company does not standardise the offer.

This is why utilisation is the key unseen variable. If many customers share the same facility, same NOC, same support stack, same antennas and same monitoring tools, fixed costs can be spread across higher revenue. If work arrives as bespoke projects with unique satellite beams, customer equipment, security requirements and troubleshooting expectations, labour can rise almost one-for-one with revenue. Revenue growth would then look healthy while value creation remains thin.

Power and resilience are another margin swing factor. The public site refers to heavy electrical backup and generator capacity. Those assets are useful in a buyer conversation because they show service continuity planning. But power equipment must be tested, maintained and replaced. Diesel storage, UPS batteries, transformers, cooling, de-icing and antenna motors all carry lifecycle cost. A customer paying for occasional service may not fully compensate the facility for that standby expense.

The company therefore needs pricing discipline. It should not sell German reliability at commodity transport prices. The more it promises immediate support, custom design, multi-supplier coordination and high availability, the more it needs minimum contract values, pass-through clauses, engineering charges, set-up fees or longer commitments. Without those, local accountability becomes something customers appreciate but do not fund.

Suppliers Set The Ceiling On Independence

Horizon can own local execution without owning the whole stack. That is both the business opportunity and the ceiling. The official and partner sources point to dependence on satellite operators including Eutelsat, Intelsat, APT, RSCC, Yahsat, Africasat, ABS, Apstar and Azercosmos across different contexts. Horizon's own satellite page lists multiple orbital positions and antenna specifications. ABS's 2026 announcement describes enhanced Ku-band capacity and integrated ground services through Horizon Teleports. HorizonSat says it operates on Eutelsat, RSCC, ABS, Apstar and Azercosmos satellites.

That supplier pattern is normal for a teleport and service integrator. It also means Horizon's offer is partly derivative. If a satellite operator changes pricing, coverage, wholesale terms or strategic channel policy, Horizon must adapt. If a large satellite operator sells directly to the same customer segment, Horizon's role could be reduced to local operations or last-mile integration. If a LEO provider offers a simpler direct terminal plus service plan, parts of Horizon's value proposition may be bypassed.

The upstream IP side has the same structure. AS198218 imports from and exports to AS1299 and AS174. Arelion and Cogent are not small suppliers. They are global internet backbones with their own pricing, capacity and routing policies. Horizon benefits from that reach. It cannot claim full independence from it. It can add local routing control, redundancy and monitoring, but the end-to-end service still relies on third-party networks.

Data-centre and point-of-presence references create another dependency layer. Horizon's facility page mentions international points of presence including Equinix Munich, Munich carrier infrastructure, Amsterdam, Telehouse London, Cogent Toronto, Telex Chicago, Telex Atlanta and Singapore. Some of the names appear dated or imprecise, so they should be treated as indicative rather than a current verified interconnection map. The strategic point is still clear: the teleport's value grows when it is stitched into major carrier-neutral locations, but those locations come with colocation, cross-connect and transport costs.

For customers, this supplier web can be a benefit. They may prefer Horizon to manage the complexity of satellite capacity, RF chains, IP transit, monitoring and escalation. For Horizon, it is margin dilution unless the company can charge for that orchestration. The danger is being squeezed between powerful upstream suppliers and demanding end customers.

The facts that would improve the view are simple: documented multi-year capacity agreements with favourable terms, evidence that Horizon controls a differentiated beam or ground-station capability, customer contracts that pay for engineering support separately from bandwidth, and proof that partner announcements such as the ABS agreement are generating recurring revenue rather than only strategic positioning.

Customers May Value Reachable Support More Than Scale

The customer question is who needs a Moosburg-based teleport enough to pay for it. Horizon's materials repeatedly mention telcos, governments, large institutions, corporate users, public protection and disaster recovery, TV broadcasters, ISPs, maritime and offshore customers, aviation users and pay-TV operators. HorizonSat's home page says its customers include large corporations, government sector, telecom operators, TV broadcasters and ISPs. The 2026 ABS announcement refers to EMEA connectivity and industries including offshore and maritime.

That customer list is plausible, but it is not a customer disclosure. No public source found for this assignment gives Horizon's revenue by customer, top-customer concentration, backlog, renewal rate, churn, average contract value or case studies with named end users. This is a material gap. A teleport can look diversified because its service menu is broad while actual revenue depends on a few contracts. It can also look small because public customer references are thin while the real customer base is private, government-linked, or wholesale.

The margin risk is concentration. If one satellite operator, one broadcasting customer, one government-related project or one group affiliate supplies a large share of traffic, Horizon's negotiating position may be weaker than the facility suggests. Customer concentration also changes how to read local accountability. A few demanding customers may value named support, but they may also extract bespoke service at negotiated prices. Broad customer diversity would make local support more scalable.

Horizon's local accountability may be especially valuable where buyers need human escalation. Live broadcast contribution, interference monitoring, emergency backhaul, maritime operations and private networks create operational anxiety. A buyer can justify paying more if downtime creates revenue loss, safety risk or reputational damage. A buyer with a non-critical, best-effort service will compare price and convenience.

The company also has a data-sovereignty and locality angle, but it should not be overstated. A German facility and German regulatory environment can comfort certain EU customers. It does not automatically mean all customer data, content, routing, satellite hops or support processes remain in Germany. HorizonSat material points to Dubai and Munich NOCs working together, and satellite coverage naturally crosses borders. The value is better framed as accountable local infrastructure within a cross-border network, not as absolute locality.

The strongest customer thesis is therefore narrower than the marketing breadth. Horizon is most likely to earn margin from customers that need a technical operator rather than a bandwidth shop: broadcasters with live operations, regional satellite operators needing ground support, telcos serving remote markets, maritime/offshore users with high downtime costs, and institutions that want a known EU teleport with group reach into EMEA. The weaker thesis is that every connectivity buyer will pay extra for local support. They will not.

The Competitive Set Is Wider Than Other Teleports

Horizon's competition is not limited to other German antenna parks. It competes with large teleport operators, satellite operators, global systems integrators, carrier-managed services, LEO constellations, cloud media platforms and CDNs. That breadth is the main strategic pressure on margin.

Traditional teleport competitors can match the operational language. WTA certification lists include operators such as Eutelsat, Telespazio, Speedcast, STN, Globecast, Santander Teleport, Arqiva, Intelsat, Orange and others. Some have greater scale, broader geography, deeper procurement power or stronger enterprise sales channels. A Tier 3 certification helps Horizon show seriousness, but it does not make it the default vendor when a global buyer wants multi-region coverage or a satellite operator wants a strategic ground partner.

Carrier substitutes pressure the IP and private-network side. Large carriers can offer terrestrial access, managed IP, MPLS, cloud on-ramps and global operations with one contract. A customer that mainly needs secure connectivity may prefer that simplicity if satellite is only a backup component. Horizon has to win where the satellite and RF expertise are central, not incidental.

LEO satellite services pressure parts of the broadband and mobility story. Starlink positions business connectivity around high-speed, low-latency broadband in remote places. Eutelsat describes OneWeb as a global low Earth orbit network for high-speed, low-latency connectivity on land, at sea and in the air. These services do not eliminate the need for teleports, gateways, enterprise integration or managed service partners, but they change buyer expectations. If a buyer can install a terminal and buy service directly or through a large reseller, the bespoke teleport margin pool shrinks.

Cloud and CDN substitutes pressure broadcast and OTT workflows. AWS Elemental MediaLive lets customers encode live video for broadcast and streaming, including cloud-controlled on-premises processing through MediaLive Anywhere. Akamai sells adaptive media delivery at global scale. For many media customers, the centre of gravity has moved from satellite distribution alone to hybrid cloud, IP contribution, OTT packaging, security and audience delivery.

Horizon can participate in that workflow through managed pay-TV, uplink, monitoring and CDN-adjacent functions, but it must show why its operations are cheaper or safer than assembling the workflow through cloud-native vendors.

The competitive implication is uncomfortable. Horizon's facility is an advantage only when the buyer's problem needs local satellite ground control, specialist RF/IP support, accountable escalation and cross-border integration. When the buyer mainly needs capacity, generic IP, simple remote broadband, or OTT distribution at scale, larger platforms can look cleaner. Horizon's margin depends on selecting the first kind of customer and avoiding the second kind unless the price reflects the work.

Regulation And Local Permission Are Part Of The Operating Model

Satellite ground infrastructure is regulated infrastructure. Horizon's imprint names Bundesnetzagentur as regulatory authority. Bundesnetzagentur's satellite communications pages describe national and international spectrum planning, coordination, harmonisation, standardisation and national spectrum assignments for satellite networks and earth stations. Its earth-station guidance says a frequency assignment allowing the use of frequencies is required before transmitting, and that assignments depend on factors such as designated frequencies, compatibility with other use and efficient spectrum use.

That regulatory layer matters economically because it adds process and accountability. A teleport cannot simply point a dish and transmit. It needs appropriate assignments, coordination and electromagnetic compliance. Local press coverage from 2015 around Moosburg's antenna dispute illustrates how local permission, antenna construction and Bundesnetzagentur processes can become part of the business risk. The press accounts should not be overread as a current dispute; they are historical signals that the physical facility faced local scrutiny around parabolic antennas and site certificates.

Security obligations are also part of the operating environment. Bundesnetzagentur's security catalogue page describes requirements for telecommunications and data processing systems and the processing of personal data as the basis for a security concept, prepared with BSI and data-protection authorities. EU NIS2 creates a wider cybersecurity framework across critical sectors, including digital infrastructure.

Whether and how every Horizon service falls within a given category depends on service details and German implementation, but the direction is clear: network and digital infrastructure providers face rising expectations around security, incident handling and operational resilience.

Regulation can help Horizon's differentiation. A buyer may prefer a German operating company with visible regulatory accountability over a loosely defined foreign reseller. It can also raise costs. Security documentation, frequency assignments, incident procedures, compliance management, audits and local permitting consume management attention. If the company serves government-linked, telecom or media customers, evidence demands can increase.

Geopolitical risk also sits in the supplier set. Horizon's public satellite pages and group pages include satellite names and operator references that span multiple jurisdictions. Older material mentions RSCC and Yamal alongside Eutelsat, Intelsat, APT, Yahsat, Africasat, ABS and others. Because sanctions, export controls, customer policies and satellite availability can change, current traffic and supplier exposure would need confirmation before drawing a hard conclusion.

The safe economic point is that cross-border satellite service providers carry geopolitical and procurement complexity that a buyer may want Horizon to manage but may not always pay for explicitly.

The regulatory view is therefore balanced. German locality may support trust and enterprise acceptance. It also makes the cost of being a credible operator higher than the cost of being a simple reseller.

Unofficial Signals Support Activity But Not Margin

The public soft signals are consistent with an active business, but none should be treated as proof of margin. Horizon's LinkedIn page lists the company in telecommunications, describes a 2014 founding year, gives a size band of 11-50 employees and repeats claims about antennas, satellite look angle, redundant infrastructure, 24/7 NOC support, managed services and proactive monitoring. Recent public LinkedIn updates promote OTT, carrier monitoring, aviation connectivity, security, NOC support and the ability to transmit programs using satellites and fibre networks.

Those posts are useful because they show what Horizon wants the market to associate with the brand in 2025 and 2026: monitoring, support, satellite connectivity, broadcast, OTT, aviation and secure infrastructure. They are not proof that customers bought those services at attractive prices. Social posts measure sales emphasis, not sales conversion.

Job-market signals tell a similar story. A public job listing for a teleport or satellite communication engineer describes RF subsystem operation, installation and troubleshooting, dish antennas, LNAs, HPAs, frequency converters, RF over fibre, link budgets, EIRP, beamwidth, spectrum analysers, ticket portals, email, phone and Microsoft Teams support. That is a useful labour signal because it matches the technical complexity described on Horizon's site. It also reinforces the margin issue: the company needs trained people, and trained people cost money.

The ABS partnership announcement is a stronger activity signal because it comes from a satellite operator and is recent. It says ABS renewed and expanded a long-standing partnership with HorizonSat and would use Horizon Teleports' Germany-based ground services to extend EMEA coverage, combining ABS satellite coverage with Horizon Teleports infrastructure and technical expertise. This is closer to commercial validation than a self-description. Even here, it does not disclose contract value, term, exclusivity, volume or economics.

Local historical press around the Moosburg antenna dispute is useful in a different way. It confirms public attention to the antenna build-out and the interaction between local construction concerns and telecommunications regulation. It does not prove current operating success. It shows that physical infrastructure creates public and administrative surface area.

The correct use of unofficial signals is disciplined. They support activity, positioning, labour demand and market intent. They should not be converted into claims that Horizon is growing, profitable, winning major customers, or enjoying pricing power. For this article's economic question, they make the local-accountability thesis more credible but do not answer the margin question.

The Facts That Would Change The Investment View

The current public evidence supports a cautious thesis: Horizon Teleports has a tangible German teleport and network-resource footprint that can justify local accountability as a product, but the public record does not prove that accountability converts into durable pricing power. The facility, AS, announced prefixes, WTA certification references, NOC claims and ABS partnership all support operational substance. The missing pieces are financial and contractual.

The first fact that would change the judgment is utilisation. A high-utilisation antenna park with recurring managed contracts is a very different business from a lumpy project shop. Public evidence of average antenna utilisation, active carriers monitored, live managed channels, recurring IP trunking circuits, or sustained traffic sold to third parties would clarify whether fixed costs are being absorbed efficiently.

The second fact is contract quality. Multi-year contracts with broadcasters, satellite operators, maritime integrators, telcos or government-linked customers would support pricing power, especially if they include engineering fees, support tiers, inflation protection, minimum commitments and pass-through treatment for satellite capacity and IP transit. Short, customer-specific, low-margin projects would weaken the view.

The third fact is customer concentration. If one group affiliate, one satellite operator, or one anchor customer drives most revenue, Horizon's local accountability may be less valuable than it appears because the buyer can negotiate aggressively. A diversified base across media, telecom, mobility, government and enterprise would make the business more resilient.

The fourth fact is supplier economics. Better disclosure on satellite capacity agreements, upstream carrier costs, data-centre interconnect costs and cloud/CDN integration would show whether Horizon has procurement leverage. The company does not need to own every layer, but it must avoid being a thin margin layer between powerful suppliers and price-sensitive buyers.

The fifth fact is service differentiation. Evidence that customers choose Horizon because its Moosburg facility solves hard RF, monitoring, compliance or support problems would strengthen the thesis. Evidence that customers choose mainly for price or temporary capacity would weaken it. WTA certification helps, but customer proof would matter more.

The final fact is growth without operational dilution. If Horizon can add ABS-type partnerships, media workflows or managed connectivity contracts without adding proportionate headcount and bespoke support cost, local accountability can become margin. If every new service requires another specialist, another supplier exception and another custom runbook, growth may only enlarge the workload.

The answer to the title question is therefore conditional. Horizon Teleports can turn local accountability into margin if it charges for reliability, engineering and German operational control rather than giving them away as sales comfort. The public record proves enough infrastructure to take the company seriously. It does not yet prove enough pricing power to call the margin durable.