Summary

- AVENIR TELEMATIQUE SAS is best read as a French managed cloud and infrastructure operator inside the Eurofiber France perimeter, not as a broad mass-market carrier. Its public value proposition is reliability, sovereign French hosting, managed private cloud, IaaS, object storage, datacenter resilience and security compliance.

- The economic question is whether customers will pay enough for accountable local reliability to fund the real cost stack. Public evidence supports a real network footprint and operational platform, but current pricing, customer concentration and contract-margin evidence remain too sparse for a confident upside case.

Reliability Is The Product, Not A Feature

The economic incentive behind AVENIR TELEMATIQUE SAS is simple: make reliability billable. A customer does not choose a managed cloud or regional infrastructure provider only because storage exists somewhere in France. The customer pays because downtime has a business cost, because health data and public-sector workloads carry compliance exposure, because in-house teams may not want to maintain redundant platforms, and because a named accountable provider can be more useful than a cheaper, more abstract commodity service when something breaks.

That is the commercial opening for Avenir Telematique. The current Eurofiber Cloud Infra site frames the offer around French cloud services for sensitive applications, with HDS and ISO 27001 certification, private cloud, IaaS, Kubernetes, Docker, object storage, firewall, datacenters and connectivity. The old ATE identity has not disappeared from the legal layer: the legal notice identifies Avenir Telematique as the site editor and host, gives the company form as a simplified joint-stock company, and lists the RCS number 347 607 764.

But the market-facing brand now points to Eurofiber Cloud Infra, described on the site as a brand of Avenir Telematique and a subsidiary of Eurofiber France.

That structure matters for the economics. A standalone small hosting company has to sell trust while carrying most of the operational burden itself. A subsidiary inside a larger fibre and digital-infrastructure group can sell the same trust with a broader network story behind it. The question is not whether the parent brand sounds larger.

It is whether group ownership lowers the unit cost of reliability enough to improve margins, or whether the offer remains exposed to the same hard inputs that weigh on every infrastructure provider: electricity, hardware refresh, software licensing, network transit, specialist labour, compliance audits and customer support.

The best reading from the public evidence is that Avenir Telematique competes in the reliability premium rather than in raw capacity. It is not trying to be the cheapest entity store in Europe, the biggest hyperscale region, or the broadest consumer ISP. The pages stress dedicated resources, high availability, multi-site continuity, French hosting, health-data certification, managed security and local expert support. Those features are expensive to deliver. They are also the features that let a provider resist pure price comparison. If the customer only wants cheap compute, commodity public cloud wins.

If the customer wants accountable continuity for a regulated workload, Avenir Telematique has a reason to exist.

The downside is that reliability has to be proven before it is paid for, and paid for before it becomes attractive capital allocation. A public promise of 99.99 percent service availability, multi-site replication or support around the clock is not margin by itself. It is an obligation. The provider has to keep staff, sites, monitoring, backup architecture, network routes and vendor support ahead of the failures customers are paying to avoid. In this model, every promise that raises willingness to pay also raises delivery cost.

That is why the article's core judgement is cautious. Avenir Telematique has credible pieces of a reliability business: legal continuity, a French cloud brand, datacenter claims, HDS and ISO 27001 positioning, a registered autonomous system, visible announced prefixes and a relationship with the wider Eurofiber France network. What public evidence does not show is whether enough customers pay high enough recurring fees, over long enough contracts, to turn that reliability obligation into attractive economics rather than a heavy operating burden.

The Legal Company Now Sits Inside Eurofiber's French Cloud Stack

The legal identity is not hard to locate. Public French enterprise data lists SIREN 347607764 for AVENIR TELEMATIQUE, with the commercial name Eurofiber Cloud Infra and the sigle ATE. It records the principal activity under data processing, hosting and related activities, shows the company as active, and places the current registered office at 15 rue Rouget de Lisle, 92130 Issy-les-Moulineaux. The current company website's legal notice is consistent with that identity: it names Avenir Telematique, gives the SAS legal form, lists capital of 67,500 euros, and gives RCS Nanterre 347 607 764.

The historical signal is also useful, but it should not be overstated. Avenir Telematique's name dates from a French technology lineage in which telematics, hosting and early internet services overlapped. Public secondary summaries describe an origin in the late 1980s around the Lille area and a later transition into hosting, managed services and telecom operations. The more important current fact is that the operating presentation has shifted to Eurofiber Cloud Infra. The footer of the current website states that Eurofiber Cloud Infra is a brand of Avenir Telematique and a subsidiary of Eurofiber France.

The about page places the company inside Eurofiber France's broader infrastructure story and says its expertise covers the data value chain from datacenters to telecoms to cloud services.

This gives Avenir Telematique two boundaries. The first is legal: Avenir Telematique remains the French company named on the legal page and public registry record. The second is commercial: Eurofiber Cloud Infra is the brand under which the market sees the products. The distinction matters because customers buy service continuity, contracts and accountability, not database names. A public-sector buyer, health-sector buyer or mid-market customer wants to know who operates the infrastructure, where the data sits, what certificates apply, who supports incidents and whether the provider is embedded in a credible network group.

The registry data also points to a business that is no longer a tiny local operator in a legal sense. The French official company search identifies the enterprise category as ETI for 2023 and lists six establishments, four of them open. It names Eurofiber Holding B.V. as president of the SAS, SCVE as director general, and KPMG S.A. as statutory auditor. Those are governance indicators of a group-controlled operating company. They do not tell us service margins, but they do reduce the risk that Avenir Telematique is merely a shell around a legacy brand.

There is one confusing financial signal. The official company search includes a 2023 financial line with net result of 1,675,276 euros and a turnover field displayed as zero. That field is not usable as evidence that the operating company had no revenue; it is more likely a limitation of disclosed or normalized data in the public API for this particular company record. The right conclusion is narrower: current revenue is not transparently visible in the public materials used for this article. That absence itself matters, because an economic thesis about reliability pricing needs evidence on contract size, churn, utilisation and gross margin.

Public identity data can confirm the company exists and is active. It cannot confirm that the reliability premium is large enough.

The legal-company view therefore supports a specific thesis. Avenir Telematique is not an anonymous infrastructure record. It is an active French company with a current commercial brand, a parent-group relationship and a registered office. But the public file leaves the economic engine partly opaque. The article must therefore judge operating logic, network evidence and market positioning rather than pretend to know revenue quality that is not disclosed.

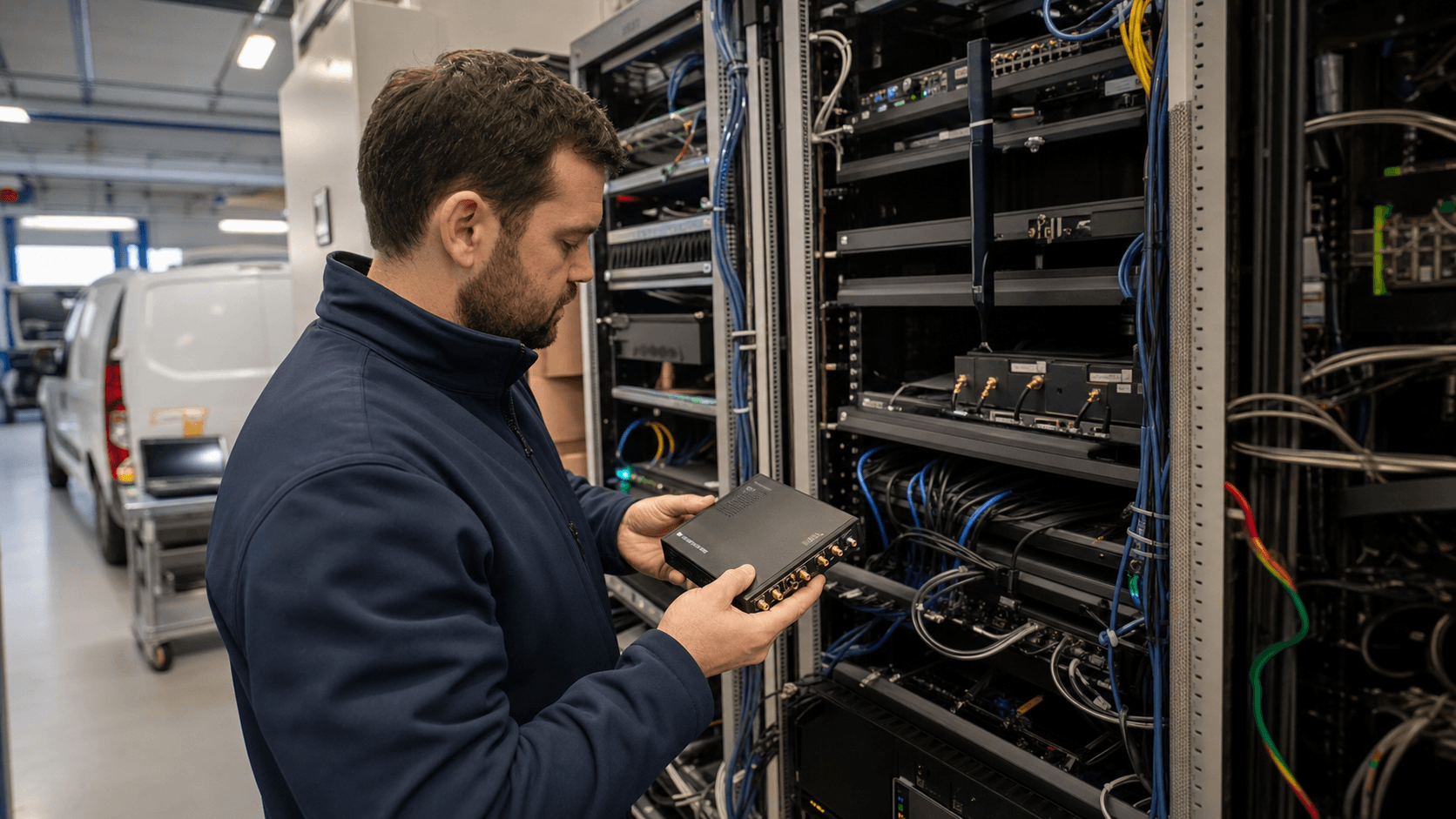

The Boundary Is Managed Cloud, Datacenters And Network Accountability

The current product perimeter is clearer than the revenue perimeter. Eurofiber Cloud Infra presents a French trusted cloud offer with private cloud, IaaS, managed container platforms, S3-compatible object storage, firewalls and datacenters. The homepage and solution pages repeatedly connect those services to sensitive applications, HDS and ISO 27001 compliance, sovereign hosting, local support, and continuity of activity.

Private cloud is the highest-accountability part of that boundary. The private-cloud page describes dedicated, physically isolated resources for critical data and applications. It highlights custom sizing, performance stability, regulatory compliance, predictable cost and high availability. The feature list includes VMware Cloud Foundation or Proxmox VE, storage technologies such as VMware vSAN, Ceph and S3, software-defined networking, integrated firewall and load balancing, multi-availability-zone architecture, disaster recovery and live migration. This is not a cheap shared-hosting claim. It is a managed infrastructure claim.

The provider is asking customers to pay for isolation, design help, support and continuity.

The IaaS page broadens that into self-service consumption. It positions VMware Cloud Director as the management layer, offers compute, storage and backup controls, and describes pay-as-you-go billing. It also says the cloud platform is distributed across several geographic zones, with synchronous replication between Lille, Toulouse and Nimes and automated disaster recovery. That matters because it turns the pricing problem into a utilisation problem. If capacity is reserved, mirrored or distributed across sites, idle resilience can be expensive. The customer values it only during failure or audit, but the provider funds it every day.

Object storage adds another economic layer. The S3 page describes sovereign, secure storage hosted fully in France, with native encryption, access controls, immutable buckets, no egress charges or hidden fees, and replication across Lille, Toulouse and Nimes. That is a commercially important claim because many cloud customers dislike unpredictable egress fees. But "no egress cost" does not make bandwidth free. It moves the recovery of bandwidth cost into the base price, capacity price or margin model. If customers use heavy outbound traffic, the provider still has to pay network and platform costs.

If the offer is priced too cheaply, transparent billing can become a margin risk.

The datacenter boundary is equally important. The datacenter page says Eurofiber Cloud Infra uses French datacenters in Lille, Toulouse and Nimes, claims security, redundancy, availability, HDS compatibility and environmental efficiency, and gives specific site information for Nimes and Toulouse. It describes the Nimes site as Tier 3+ with 24/7 supervised access and PUE of 1.2, and the Toulouse site as Tier 3+ with strong fibre connectivity and PUE of 1.4.

It also says Eurofiber Cloud Infra is present at ETIX Lille #1, ETIX Lille #2 and ETIX Toulouse #1, while proprietary Eurofiber DC sites in southern France support availability and sovereignty.

This boundary is a reasonable market niche. It is neither pure cloud software nor pure fibre. It combines sites, network, managed services and compliance. The economic upside is bundling: a customer that needs private cloud, backup, object storage, firewalling and certified hosting may prefer one accountable provider. The economic downside is that each layer has a different cost rhythm. Hardware refresh can arrive in lumps. Certifications require recurring audit discipline. Support has labour cost. Datacenter power costs fluctuate. Fibre and transit depend on upstream contracts.

Software platforms such as VMware, Veeam, Fortinet or backup and orchestration tools carry licensing and partner economics.

The company can create value only if the bundle lets it charge more than the sum of those input costs. If it merely resells commodity infrastructure with local labels, competition will compress the margin. If it genuinely lowers customer risk through design, proximity, sector knowledge and support, customers with regulated or continuity-sensitive workloads may pay a premium. The boundary is therefore attractive but unforgiving.

Resource Records Show A Real Network Footprint, But Not Carrier Scale

The network evidence should be used carefully. ASNs, prefixes and registry handles are evidence of routing and resource operation. They are not the company itself, and they do not prove the full service catalogue. For Avenir Telematique, the resource evidence supports a real network footprint attached to the Eurofiber France perimeter, while also showing why the company should not be described as a broad carrier on public evidence alone.

RIPE RDAP for AS24935 identifies the active autnum handle AS24935 with the name ATE-AS. Its entity records include Eurofiber France LIR Admin, Eurofiber Cloud Infra maintenance, Eurofiber France SAS as an organization record, and abuse contact data under the Eurofiber domain. RIPE Stat's AS overview lists the holder as "ATE-AS Eurofiber France SAS" and marks the AS as announced. That is meaningful: the legacy ATE network identity remains visible in current routing data, now under Eurofiber France administration.

RIPE Stat's announced-prefix data, queried for the late June to July 11, 2026 window, lists multiple IPv4 and IPv6 prefixes originated by AS24935. The routing-status view shows 19 IPv4 prefixes and four IPv6 prefixes in announced space at the query time, with 4,864 IPv4 addresses and 65,536 IPv6 /48 units reported in the RIPE Stat format. Visibility was strong in that snapshot, with IPv4 seen by 325 of 325 relevant RIS peers and IPv6 by 321 of 322. The first-seen origin in routing-status goes back to 2010 for 109.197.240.0/21, which supports a long-running routing presence rather than a new marketing wrapper.

But the same data argues for restraint. RIPE Stat's neighbour view for AS24935 showed one observed neighbour, AS35625. AS35625 is Eurofiber France's own AS, identified in RIPE Stat as "EUROFIBER-FRANCE Eurofiber France SAS." The AS35625 RDAP remarks describe full transit relationships with Lumen, GTT and Orange and list multiple exchange presences such as FranceIX, Equinix IX Paris, LillIX and several DE-CIX locations. That suggests AS24935 is currently visible as a network behind the wider Eurofiber France network rather than as a separately diversified peering platform in the public snapshot.

PeeringDB reinforces that interpretation. The PeeringDB entry for AS24935 is named "Eurofiber France - ATE," with aka "Cloud Infra," the website at ate.info, a reported traffic band of 5-10 Gbps, a mostly outbound traffic ratio, type "Content," 50 IPv4 and 20 IPv6 prefixes in the informational fields, and zero listed internet-exchange or facility counts. PeeringDB is a self-reported industry database, so it is not a regulatory record. Still, the signal fits the rest of the evidence: AS24935 is operational, but the visible peering profile is modest and not presented as an independent national transit platform.

This distinction is central to the economic judgement. Avenir Telematique can credibly say it has network resources and operational control in the Eurofiber France stack. It should not be valued as if those records alone demonstrate broad wholesale network scale. The resource footprint helps the reliability proposition because the provider can originate and manage address space, integrate cloud and network operations, and draw on Eurofiber France's broader upstream and interconnection fabric. It does not eliminate the need to pay for upstream connectivity, routing operations, DDoS protection, monitoring and support.

Nor does it prove that customers choose Avenir Telematique primarily for network transit rather than managed cloud and continuity.

The resource evidence therefore supports the article's cautious middle view. The company is not just a reseller with a website. It has visible routing history and active address-originating infrastructure. But the public record points to a managed cloud and infrastructure reliability business whose network component is important, not to a carrier-scale network business whose standalone economics are obvious.

Redundancy Has To Pay For Upstream Dependence

Redundancy is the product customers notice only when failure arrives. For the provider, it is a daily expense. Avenir Telematique's public offer leans heavily on multi-site continuity: data hosted in France, datacenters in Lille, Toulouse and Nimes, replication across sites, multi-AZ options, high availability, automated disaster recovery, backup integration and support promises. Those claims have commercial value, but only if they are monetised through customer contracts that cover the idle capacity and engineering discipline behind them.

The first dependency is upstream connectivity. AS24935 is visible through AS35625 in RIPE Stat's neighbour snapshot, and AS35625's RDAP remarks list upstream transit from Lumen, GTT and Orange, plus multiple exchange locations. That is a rational group architecture: let the cloud-infrastructure unit use the larger Eurofiber France network perimeter rather than maintain every external route itself. The customer may benefit from group network scale and route diversity. The economic risk is that group dependence can hide the true cost allocation.

If cloud services are charged internally for network use, margins depend on transfer pricing. If they are not charged fully, the cloud unit may appear stronger than its standalone economics. If customers generate heavy traffic under simple billing, the group still absorbs real capacity cost somewhere.

The second dependency is datacenter resilience. The company describes sites with redundancy, 24/7 supervision, Tier 3+ positioning and strong connectivity. It also describes partnerships with ETIX in Lille and Toulouse, while pointing to Eurofiber DC sites in the south. Multi-site service is harder than single-site hosting. It requires consistent operations, route design, backup validation, recovery runbooks, equipment spares, monitoring across domains, and incident communication. Customers want one accountability chain; the provider has to coordinate several.

The third dependency is vendor technology. The product pages reference VMware, Proxmox, Dell Technologies, Fortinet, Kubernetes, Docker, Cloudflare, Arista, Veeam, HAProxy, Cisco and NixOS through partner or technology logos. Some of those are open platforms, some are commercial dependencies, and some are ecosystem signals rather than contractual proof. The economic point is that managed reliability is not delivered only with owned assets. It is assembled through hardware, orchestration, backup, network, security and support inputs. Margin depends on negotiating those inputs well and avoiding over-customised deployments that cannot be reused.

The fourth dependency is people. The certification page points to ITIL v4 certified teams. The private-cloud and IaaS pages repeatedly describe expert support, accompaniment, implementation help, supervision and dedicated or local technical teams. Around-the-clock supervision is a labour and process cost even when incident volume is low. A provider selling regulated continuity has to keep enough expertise available to respond without turning every incident into a bespoke scramble. That staffing cost is sticky. If revenue stalls, it does not fall cleanly.

This is why the reliability premium must be explicit. Customers cannot expect local accountability, multi-site architecture, certified health-data hosting, security monitoring, support and predictable cost at commodity margins. Avenir Telematique's strategy is viable only if buyers understand the alternative cost of failure.

For a health application, public body, ministry supplier, regional industrial company or mid-market software platform, the alternative may be building a compliant architecture internally, hiring scarce infrastructure staff, spreading workloads across hyperscale regions, and taking direct responsibility for restoration. In those cases, Avenir Telematique can charge for avoided complexity. For a low-criticality workload, that case weakens quickly.

The public evidence shows credible redundancy architecture. It does not show enough customer-level pricing to prove that redundancy is fully paid for. That is the crux.

The Revenue Model Favors Contracted Assurance Over Commodity Capacity

Avenir Telematique's revenue model is likely strongest where the customer pays for assurance rather than for undifferentiated units. The website does not publish a simple tariff grid for most core services. Instead, the private cloud, IaaS, partner and datacenter pages repeatedly direct customers to contact the company, co-design architecture, choose dedicated or managed resources, and build around compliance and continuity requirements. That sales motion points to contracted infrastructure, not anonymous self-service volume.

The private-cloud economics are different from public-cloud spot consumption. Dedicated private cloud lets a provider price around reserved infrastructure, custom architecture and support. If the customer is stable, the provider can plan hardware and capacity more accurately. If the contract includes support and compliance duties, the provider can earn margin on expertise rather than only on CPU, RAM and storage. The downside is sales-cycle friction. Each custom deal can consume engineering time before revenue is won, and bespoke architectures can limit standardisation.

IaaS creates a more elastic model. The IaaS page describes pay-as-you-go billing for VMware Cloud Director environments, with compute, storage and backup resources managed through a portal. Consumption billing can improve customer adoption because it avoids oversized commitments. But it also imports the classic cloud-provider risk: utilisation volatility. The provider has to own or reserve enough platform capacity for peak demand, while revenue follows actual usage. In a small or mid-sized provider, poor utilisation can quickly hurt returns on hardware and datacenter investment.

Object storage adds a third model. The S3 page says the offer has simple and transparent pricing, no egress charges and no hidden fees, and a monthly model based on used gigabytes. That is attractive for customers tired of surprise cloud bills. It also means the provider must be disciplined about customer traffic patterns and replication costs. Storing data across three French datacenters raises resilience and appeal, but it also multiplies write, capacity and operational requirements. A customer that stores cold backups may be profitable.

A customer with frequent heavy restores and outbound transfer may be less profitable if egress is not separately charged.

The partner programme indicates another route to scale. It targets software publishers, SaaS/PaaS companies and managed service providers that want to add sovereign, certified infrastructure to their catalogue. Partners can improve distribution efficiency if they bring repeatable workloads. They can also compress margin if the partner expects discounting or if the provider becomes an invisible backend for someone else's customer relationship. The page's promise of technical and regulatory support, including 24/7 support, is valuable, but it is not costless.

Customer logos and sector references point to public sector, health, ministries, local authorities, distribution and industry. The about and partner pages say more than 500 clients trust the platform. That is a useful market signal, but it does not reveal revenue concentration, average contract value, churn, or how many customers buy only one product versus a full managed stack. A provider with 500 small customers can be more support-intensive than a provider with 50 standardised large contracts. The public evidence does not answer that.

The likely revenue sweet spot is therefore not volume-only cloud. It is regulated or continuity-sensitive mid-market and institutional demand where the buyer values French hosting, named support, compliance, recoverability and architecture assistance. Those customers can make local reliability economical. They can also be slow buyers, demanding buyers and price-sensitive buyers when budgets tighten. Avenir Telematique's commercial success depends on turning trust into multi-year recurring contracts rather than project work or low-margin capacity resale.

Public Pricing Gaps Make Margin Judgment Cautious

The hardest part of judging Avenir Telematique is not identity or product description. It is price evidence. Public pages are rich in service claims and thin in actual tariffs. That is normal for custom private cloud and managed infrastructure, but it limits outside confidence. The article can describe the cost stack and value proposition. It cannot prove whether price exceeds cost by enough to create strong returns.

The pricing clues point in different directions. Private cloud promises predictable, stable and transparent cost by using dedicated infrastructure adapted to customer needs. That can justify premium contracts, because customers buy budget visibility and compliance assurance. IaaS offers pay-as-you-go. That can attract usage but exposes the provider to utilisation and platform-cost management. Object storage says no egress fees, no hidden costs and a per-gigabyte consumption model. That can be compelling against hyperscale billing complexity, but it means heavy network and replication costs must be recovered elsewhere.

The public enterprise registry does not solve the problem. It identifies the company as active, lists open establishments and records a 2023 net result figure, but the turnover field shown in the public search API is zero. That is too ambiguous for revenue analysis. It may reflect missing turnover disclosure, normalization rules or data limitations. It cannot be used as a meaningful revenue denominator. Without revenue, gross margin, EBITDA, capex, utilisation, contract length or churn, public analysis has to stay probabilistic.

The cost side is easier to understand. The provider must fund datacenter capacity in multiple French locations, network engineering, routing operations, hardware refresh, storage replication, backup tooling, security devices, certifications, audits, support, monitoring, incident response and customer onboarding. Some of those costs scale with usage. Others are fixed or step-fixed. A new storage cluster, firewall platform, router refresh or certification renewal may be required before the next euro of revenue arrives. That creates operating leverage when growth is strong, but margin pressure when utilisation is weak.

Commodity alternatives keep pressure on the top line. A customer comparing only compute or storage can choose OVHcloud, Scaleway, AWS, Microsoft Azure, Google Cloud, Orange Business, SFR Business, hosted VMware partners or a local MSP using another backend. Some alternatives have more self-service pricing, larger ecosystems or lower headline unit costs. Avenir Telematique therefore needs the customer to compare total risk, not just unit price. The sellable difference is not "we have servers"; it is "we will help keep your critical services available, compliant, recoverable and locally accountable."

The reliability thesis becomes stronger when pricing is tied to outcomes that customers actually fear: downtime, failed recovery, health-data compliance, audit exposure, uncontrolled egress bills, lack of local support, and weak incident ownership. It becomes weaker when customers treat infrastructure as a generic line item. The public site is correctly aimed at the stronger buyer psychology. It stresses security, continuity, French hosting, expert accompaniment and compliance. But the lack of public price and contract evidence means an outside reader should not infer high margins just because the language is premium.

In short, Avenir Telematique has the shape of a premium reliability provider, but not enough disclosed pricing evidence to prove premium economics. That is not a flaw in the company. It is a limit of the public record.

Capital Needs Sit In Power, Hardware, Licenses And People

Reliability businesses are capital hungry even when they look like service businesses. Avenir Telematique's current offer implies recurring capital and operating needs across physical sites, compute, storage, networking, software and staff. The company can reduce some burden through Eurofiber group infrastructure and datacenter partnerships, but it cannot escape the basic economics of infrastructure renewal.

Datacenter claims are the most visible capital signal. The public site lists French sites in Lille, Toulouse and Nimes, describes redundancy and round-the-clock availability, and gives PUE indicators of 1.2 at Nimes and 1.4 at Toulouse. Efficient power usage is economically important because energy is one of the largest variable or semi-variable costs in datacenter operations. Better PUE lowers the power overhead beyond IT load. But high availability, cooling efficiency, physical security and redundant infrastructure all require investment.

Even if some sites are partner sites, the service provider pays for the reliability it sells through wholesale, colocation, internal transfer or owned-site economics.

Hardware refresh is the second pressure. Private cloud and IaaS need servers, storage, switches, routers, firewall appliances and backup infrastructure. Customers paying for critical applications do not tolerate ageing platforms that increase incident risk or performance inconsistency. The private-cloud page references technologies and partners that imply serious infrastructure: Dell, VMware, Proxmox, Ceph, S3, Fortinet, Arista, Cisco and Veeam among others. Whether owned directly or delivered through vendor relationships, those capabilities require procurement, lifecycle management and support contracts.

Licensing risk deserves attention. VMware-based private cloud and VMware Cloud Director environments have been attractive to enterprises because they match existing skills and migration paths. But VMware ecosystem costs have become a board-level concern for many customers and providers after industry licensing changes. Avenir Telematique's inclusion of Proxmox VE alongside VMware Cloud Foundation is therefore commercially sensible. It gives customers an alternative architecture and gives the provider negotiating flexibility. But supporting multiple stacks also raises operational complexity.

Engineers, runbooks, backup integration, security controls and customer support need to work across more than one platform.

People are the third capital-like commitment. Skilled infrastructure staff are not inventory that can be turned off between deals. HDS, ISO 27001, ITIL process maturity, security monitoring, disaster recovery and customer onboarding require specialists. The certification page's emphasis on standards and ITIL, and the product pages' emphasis on expert support, imply a service model where human capability is part of the product. That can justify higher pricing, but it also raises break-even scale.

Network equipment and upstream capacity form the fourth pressure. The AS24935 routing evidence shows visible announced prefixes; the AS35625 context shows group transit and exchange arrangements. To customers, network availability is bundled into service. To the provider, it is routers, optics, capacity planning, DDoS posture, routing security, monitoring and escalation. A failure in this layer can damage the whole reliability brand even if the compute stack is healthy.

The most attractive version of the business is one where these investments are shared across many similar customers. A standardised private-cloud architecture, repeatable S3 storage platform, repeatable backup model and well-defined support tiers can spread cost. The least attractive version is one where each customer demands unique architecture, exceptions, audits and bespoke support at prices that do not recover engineering time. Public materials lean toward custom design and co-construction, which helps sales but can pressure standardisation.

The capital question is therefore not whether Avenir Telematique has infrastructure. It clearly claims and evidences meaningful infrastructure. The question is whether its commercial model turns that infrastructure into repeatable, high-utilisation, recurring revenue instead of a permanent obligation to overbuild for every customer's worst day.

Health And Public-Sector Compliance Raises Both Price And Cost

Health-data and public-sector positioning are central to Avenir Telematique's premium case. The certifications page says Eurofiber Cloud Infra is ISO/IEC 27001:2022 certified and certified as a health-data host. It describes HDS as relevant to health actors and states that there is no transfer of personal health data to a third country outside the European Economic Area. The datacenter and cloud pages repeat the HDS, ISO 27001 and GDPR themes, making compliance a core selling point rather than a footnote.

The legal backdrop supports why this matters. Article L1111-8 of the French Public Health Code requires a certificate of conformity for hosting personal health data on digital media in the relevant circumstances. It also requires the hosting service to be contractual, limits use of hosted data to the hosting service, and includes obligations around confidentiality, return of data and control. For a customer in health or adjacent social and medico-social activity, this is not optional decoration. It affects vendor selection.

Compliance can raise willingness to pay. A hospital supplier, telemedicine platform, health software provider, local authority, ministry contractor or healthcare-adjacent SaaS company may not want to assemble HDS hosting, ISO 27001 controls, backups, incident process, French residency assurances and network reliability from scratch. A provider that packages these features can reduce procurement friction and operational risk. The customer pays not just for compute but for a defensible control environment.

Compliance also raises cost. Certifications require process discipline, audits, evidence management, access controls, incident handling, supplier oversight, staff training and documentation. The provider has to maintain controls even when customers are not actively testing them. If a customer requires contractual commitments around data location, audit rights, recovery objectives or security incident reporting, those obligations consume legal, technical and operational capacity. The better the compliance promise, the less room there is for informal operations.

Public-sector and regulated customers also shape cash flow. They can be sticky once integrated, but procurement can be slow. They may demand strong service levels, clear liability terms, data-portability commitments and competitive tendering. The Eurofiber Cloud Infra site shows trust markers through references to public sector, health, ministries, local authorities, distribution and industry, and displays many customer logos. Those are useful market signals, but they do not reveal concentration. If a few large public or health contracts carry much of the revenue, renewal risk matters.

If the customer base is broad but small, support intensity matters.

This is where local accountability becomes economically important. Hyperscale cloud providers can offer certifications, regions and large ecosystems. But local providers can compete on proximity, French-language technical engagement, custom architecture, named teams, and direct accountability for continuity plans. Avenir Telematique's strongest pitch is likely not "we are more certified than everyone else." It is "we can combine certification, French sites, managed design and local support in one accountable relationship."

The risk is that compliance becomes table stakes. If enough competitors offer HDS, ISO 27001, sovereign hosting and managed services, the premium falls. The company then needs either superior support, stronger sector expertise, better network integration, more transparent pricing or deeper Eurofiber group leverage. Compliance opens the door. It does not guarantee margin forever.

Customers Buy Local Assurance, But Concentration Is Hard To See

The public site says more than 500 customers trust Eurofiber Cloud Infra and presents a set of logos and sectors including public sector, health, ministries, local authorities, distribution and industry. That supports demand for the general proposition: there is a buyer pool for French managed cloud and infrastructure services tied to compliance and continuity. It does not, by itself, show revenue quality.

Customer concentration is one of the biggest unknowns. A reliability provider can look diversified by logo count while still depending on a small number of large contracts. Conversely, it can have no single dominant customer but still carry high support costs because many customers require small, custom deployments. The public evidence does not provide revenue by customer, sector, product or contract duration. That means any judgement must treat customer quality as unresolved.

The most attractive customer for Avenir Telematique is one with a real cost of failure and limited appetite to self-manage. Examples include a health software vendor needing HDS hosting, a regional public body with continuity obligations, a mid-market industrial firm running critical systems, a software publisher that wants a French certified backend, or a managed service provider that needs a sovereign infrastructure partner. These customers can rationally pay for local assurance because the alternative is not just cheaper cloud.

It is internal headcount, external consultants, audit work, backup design, disaster-recovery drills and incident risk.

The least attractive customer is one that wants all the language of assurance without paying for it. If a buyer demands 24/7 support, high availability, multi-site replication, security monitoring and compliance documentation but negotiates as if buying a commodity virtual machine, the provider carries downside without compensation. Avenir Telematique's pricing discipline is therefore central. The company should be willing to lose customers whose workloads are not valuable enough to fund the reliability promise.

Market dependence also matters. The company is French, the sites are French, and the compliance proposition is heavily tied to French and European data expectations. That is a strength when buyers want sovereignty and local accountability. It is a limit if the customer needs global edge presence, many cloud regions, huge developer ecosystems or aggressive unit pricing. The brand should not try to be every cloud to every buyer. Its economic niche is strongest where French residency, HDS, support and continuity are decision criteria.

There is also a group cross-sell angle. As part of the Eurofiber France perimeter, Avenir Telematique can benefit from customers that need both connectivity and cloud infrastructure. The about page describes Eurofiber as a European digital infrastructure operator with a large fibre footprint and strong business reach. If Eurofiber can bundle fibre, datacenter access, private cloud, storage and managed security into one relationship, Avenir Telematique's customer acquisition cost could fall and account depth could improve.

But group membership can also blur accountability if customers experience multiple brands, contracts or support chains.

The article's judgement is therefore conditional. Avenir Telematique looks best when its customer base values accountable French reliability enough to sign recurring, multi-product contracts. It looks weaker if customer demand is fragmented, price-led or dependent on a few public-sector renewals that periodically reset pricing pressure.

Substitutes Are Plentiful Unless Accountability Is Bundled

The competitive threat is not that Avenir Telematique lacks a proposition. It is that many parts of the proposition can be bought elsewhere. A customer can buy public cloud from hyperscalers, French cloud and hosting from OVHcloud or Scaleway, connectivity and managed services from Orange Business or SFR Business, colocation from large datacenter operators, backup from specialist vendors, and support from local MSPs. The company wins only if the bundle is more valuable than assembling those substitutes.

Hyperscale cloud is the obvious alternative for elastic workloads. AWS, Microsoft Azure and Google Cloud offer deep services, global regions, developer ecosystems and large security programmes. They can be hard to beat on breadth. But their strengths can become weaknesses for some customers: pricing complexity, egress charges, self-service support tiers, non-local accountability, multi-region design complexity and dependence on in-house skills. Avenir Telematique's response is not to out-hyperscale them. It is to offer simpler accountability for critical French workloads.

French cloud competitors are more direct. OVHcloud and Scaleway can offer domestic brand recognition, French datacenters and more visible public pricing. OVHcloud has much larger scale and a broad product portfolio. Scaleway has developer appeal and clear cloud products. These competitors pressure Avenir Telematique on price transparency and self-service. Avenir Telematique's best defence is managed continuity, custom private cloud, HDS-oriented service, multi-site recovery and local support. If a customer wants a credit card cloud account, Avenir Telematique is probably not the natural first choice.

If the customer wants design accountability and regulated hosting, the niche is stronger.

Telecom incumbents and business-service providers are another substitute. Orange Business, SFR Business and other integrated telecom providers can bundle access, security, cloud, voice and managed services. They can offer broad coverage and established procurement relationships. Avenir Telematique's advantage, if any, is likely focus and flexibility: a smaller specialised cloud-infrastructure unit may be more responsive to mid-market or regulated workloads that do not fit standard incumbent bundles. That advantage must be earned operationally, not assumed.

Datacenter and colocation providers offer another path. A customer with internal infrastructure skills can rent colocation, buy network services and operate its own stack. This can be cheaper at scale and more controlled for sophisticated teams. It is less attractive for organisations that lack 24/7 operations, compliance discipline or disaster-recovery expertise. Avenir Telematique therefore competes against internal build as much as against external providers.

The substitute analysis points back to accountability. The company's strongest differentiated product is not a single feature. It is the combination of French sites, managed cloud architecture, resource operation, compliance claims, backup and recovery, security tooling, and local expert support. Any one of those can be copied or bought elsewhere. The bundle is harder to replace if the provider executes well and if contracts make one accountable party responsible for outcomes.

That is also why vague strategy would be dangerous. Avenir Telematique should avoid broad claims that make it sound like a generic cloud. The market already has generic cloud. Its economic claim is narrower and better: for sensitive French and European workloads, the customer can buy reliability, support and compliance from a provider with real infrastructure and a Eurofiber network context. If that claim is priced with discipline, it can create value. If it is discounted into commodity capacity, the substitutes win.

Operational And Regulatory Risk Is The Downside Customers Transfer

The customer pays Avenir Telematique to absorb risk, but the risk does not disappear. It moves to the provider. That is the defining economic trade. A regulated customer transfers part of the burden of infrastructure operations, data hosting, recovery planning, network continuity and security process. Avenir Telematique receives revenue in exchange for carrying that burden. If it prices accurately, the trade creates value for both sides. If it prices poorly, the provider inherits downside without adequate compensation.

Operational risk starts with uptime. The site describes 24/7 availability, redundant datacenters, high-availability cloud, multi-AZ options, synchronous replication and automated disaster recovery. These are credible promises only if recovery is regularly tested and operationally integrated. Backups that exist but cannot be restored quickly do not support a reliability premium. Replication that protects against one failure mode but not operational error can create false comfort. The provider's processes matter as much as the architecture.

Cyber risk is another pressure. The certification and product pages mention security by design, firewalls, anti-DDoS, IDS/IPS, WAF, SOC supervision and incident response. For customers, these are reasons to outsource. For the provider, they are obligations. A breach, prolonged outage or failed response would hurt the very trust premium the company sells. The risk is amplified in health and public-sector contexts because data sensitivity and reporting expectations are higher.

Regulatory risk is not limited to health data. GDPR, data residency, contractual processing roles, third-country transfer risk, audit evidence and supplier control all matter for European infrastructure providers. The HDS legal framework is particularly explicit about certification and contractual obligations for hosting personal health data. Eurofiber Cloud Infra's pages state no transfer of personal health data to a third country outside the EEA. That is a strong assurance, but it requires continuing control over infrastructure, subcontractors, support access and data flows.

Technology-change risk also matters. Infrastructure providers must refresh hardware, adapt to software licensing changes, secure supply chains, maintain backup compatibility and support changing customer workloads. A platform built around yesterday's profitable stack can become less attractive if licensing shifts or if customers move toward containers, managed databases or cloud-native patterns. Eurofiber Cloud Infra's inclusion of Docker and Kubernetes offerings helps address that shift. But managed containers bring their own operational complexity and require strong platform engineering.

Geopolitical risk is less direct than for cross-border operators, but sovereignty is a market theme. Customers worried about extra-European access, foreign cloud legislation or public-sector control may value French and European hosting. That can help Avenir Telematique. But sovereignty claims invite scrutiny. The provider must be clear about where data sits, who can access it, what vendors are involved, and how support is delivered.

Finally, reputation risk is high because reliability providers sell confidence. A commodity provider can sometimes recover from an outage with credits and price. A provider whose pitch is "guarantee your activity" faces a harsher standard. Every incident becomes a test of the premium. The company therefore needs operational humility: avoid promising more than architecture and staffing can support, and avoid contracts that make support obligations unprofitable.

The downside customers transfer is exactly what gives the business value. It is also what makes the business unforgiving.

The Market Signals Are Useful But Not Conclusive

Unofficial and semi-official market signals help fill gaps, but they must be labelled as signals rather than proof. PeeringDB, customer logos, product language and public registry snippets all say something. None of them substitute for audited segment accounts, contract data or customer interviews.

PeeringDB's entry for AS24935 is a useful industry signal. It reports 5-10 Gbps traffic, mostly outbound, content-type classification, zero listed exchange or facility counts, and a website pointing to ATE. That suggests a modest routing profile associated with hosted content or cloud services rather than a large access or transit network. Because PeeringDB is maintained through community and operator-supplied data, it should be treated as indicative. It is not a regulator and not a financial source.

Still, it aligns with RIPE Stat: the company has visible network resources, but the current public footprint is not large enough to drive an aggressive network-scale thesis.

Customer logos are another signal. Eurofiber Cloud Infra shows public sector, health, ministries, local authorities, distribution and industrial logos and says more than 500 clients trust the platform. This supports market relevance. It does not tell us current revenue, whether the logos are active contracts, how large each customer is, or which products they use. Logos are useful for understanding target sectors; they are weak for estimating concentration and margin.

The technology-partner logos also signal capability and cost. Dell, Fortinet, VMware, Arista, Veeam, Cisco and other named ecosystem elements imply that the platform is not a hobbyist stack. They also imply vendor dependencies. The signal is therefore two-sided: credibility and cost.

The French enterprise registry signal is similarly mixed. It confirms legal existence, active status, activity classification, current office, establishments and governance. It includes a financial result figure, but the turnover field is not informative. The right interpretation is that Avenir Telematique is a real and active operating company in a group structure, while current operating revenue remains opaque to an outside reader.

The strongest market signal is the coherence between brand, product, network and regulation. Avenir Telematique is not presenting one story on its website and a totally different one in resource records. The site says French managed cloud and infrastructure; the registry says hosting and related data-processing activity; RIPE shows ATE-AS under Eurofiber France; PeeringDB names Eurofiber France - ATE with Cloud Infra as aka. That coherence raises confidence in the operating boundary.

The weakest signal is economic proof. Public materials do not show enough price points, contract values, renewal rates, utilisation rates, cloud gross margin, capex intensity or customer concentration. For an equity-like judgement, that is a major gap. For an infrastructure-market profile, it is acceptable as long as the conclusion stays bounded.

The bounded conclusion is this: public signals support Avenir Telematique as a credible French managed cloud and reliability provider inside Eurofiber France. They do not prove that it earns high margins, that its redundancy is fully paid for, or that customer demand is deep enough to support aggressive expansion without margin pressure.

The Judgement Turns On Evidence That Is Still Missing

The investment-style judgement is conditional but useful. Avenir Telematique can make customers pay for reliability if it sells to buyers whose cost of failure is higher than the premium it charges. It has the right public ingredients: French legal identity, Eurofiber group context, active routing resources, managed cloud services, multi-site datacenter positioning, HDS and ISO 27001 claims, private cloud, IaaS, object storage, firewall, backup, local support and sector relevance. Those ingredients create a credible product for customers that need accountability.

The company cannot rely on those ingredients alone. Reliability is expensive. Upstream connectivity, equipment refresh, datacenter power, software licensing, security monitoring, audits, staff and support all have to be paid before failure occurs. If customers underpay, reliability turns into a loss-leading promise. If the provider overbuilds for too many custom cases, utilisation suffers. If it prices fairly but cannot explain the value, customers drift to cheaper substitutes.

The facts that would change the judgement are concrete. First, public or sourced evidence of recurring revenue growth by product would show whether demand is broadening. Second, gross margin or EBITDA by cloud-infrastructure line would show whether reliability is profitable after network, hardware, energy and staff costs. Third, customer concentration data would show whether the business depends on a few large public or health contracts. Fourth, contract duration and renewal rates would show whether customers treat the company as embedded infrastructure rather than replaceable hosting.

Fifth, capex and utilisation data by datacenter and platform would show whether multi-site redundancy is efficiently used. Sixth, incident and recovery performance would show whether the reliability promise is operationally proven.

There are also product facts that matter. Evidence that customers adopt multiple services together - for example private cloud plus S3 backup plus firewall plus connectivity - would strengthen the bundling case. Evidence that customers use only low-margin storage or capacity would weaken it. Proof that the Eurofiber France network relationship lowers transit and access costs would strengthen the model. Proof that the cloud unit is dependent on internal subsidies would weaken it.

The present judgement is therefore neither dismissive nor promotional. Avenir Telematique has a real economic role: it can be the accountable French infrastructure layer for customers that cannot afford weak continuity and do not want to self-operate regulated platforms. The market need is real. The public evidence supports the company's ability to serve it. But the economic prize depends on pricing discipline and repeatability. Reliability is valuable only when the customer pays for the boring parts: spare capacity, audits, backup validation, monitoring, router operations, power efficiency, support coverage and recovery planning.

If Avenir Telematique can keep the offer focused on customers who value those parts, the Eurofiber Cloud Infra position is defensible. If it chases generic cloud volume or lets support-heavy custom work dilute margins, the same reliability promise becomes a cost trap. The price of owning network reliability is not a slogan. It is the full cost of being the party customers call when the cheaper alternative fails.