Summary

- Stripe's production value is not just fast integration. It is the ability to move a commercial event into accepted payment state, invoice state, tax state, fraud state, balance state and payout state that different teams can trust.

- The strongest evidence for Stripe is the breadth of its operating surface: payments, Billing, Tax, Radar, Connect, Treasury, Issuing, Financial Connections, reporting and support tooling are designed to reduce the number of separate systems a business must stitch together.

- The main risks are equally practical: webhook duplication or loss, misunderstood idempotency, tax registration gaps, false fraud decisions, dispute evidence weakness, payout timing, regional payment method failures, support dependence, pricing surprises and migration lock-in.

- Public documentation supports a cautious positive view of Stripe as a production automation platform, but it does not independently prove a merchant's latency, authorization lift, fraud rate, support quality, tax accuracy or reconciliation cost. Those results must be measured inside each business.

The accepted platform state is the product

Stripe's reputation was built on the idea that payments should be programmable. That reputation still matters, but it can distract from the harder question. A developer does not really buy a beautiful API. A merchant does not really buy a checkout form. A finance team does not really buy a dashboard.

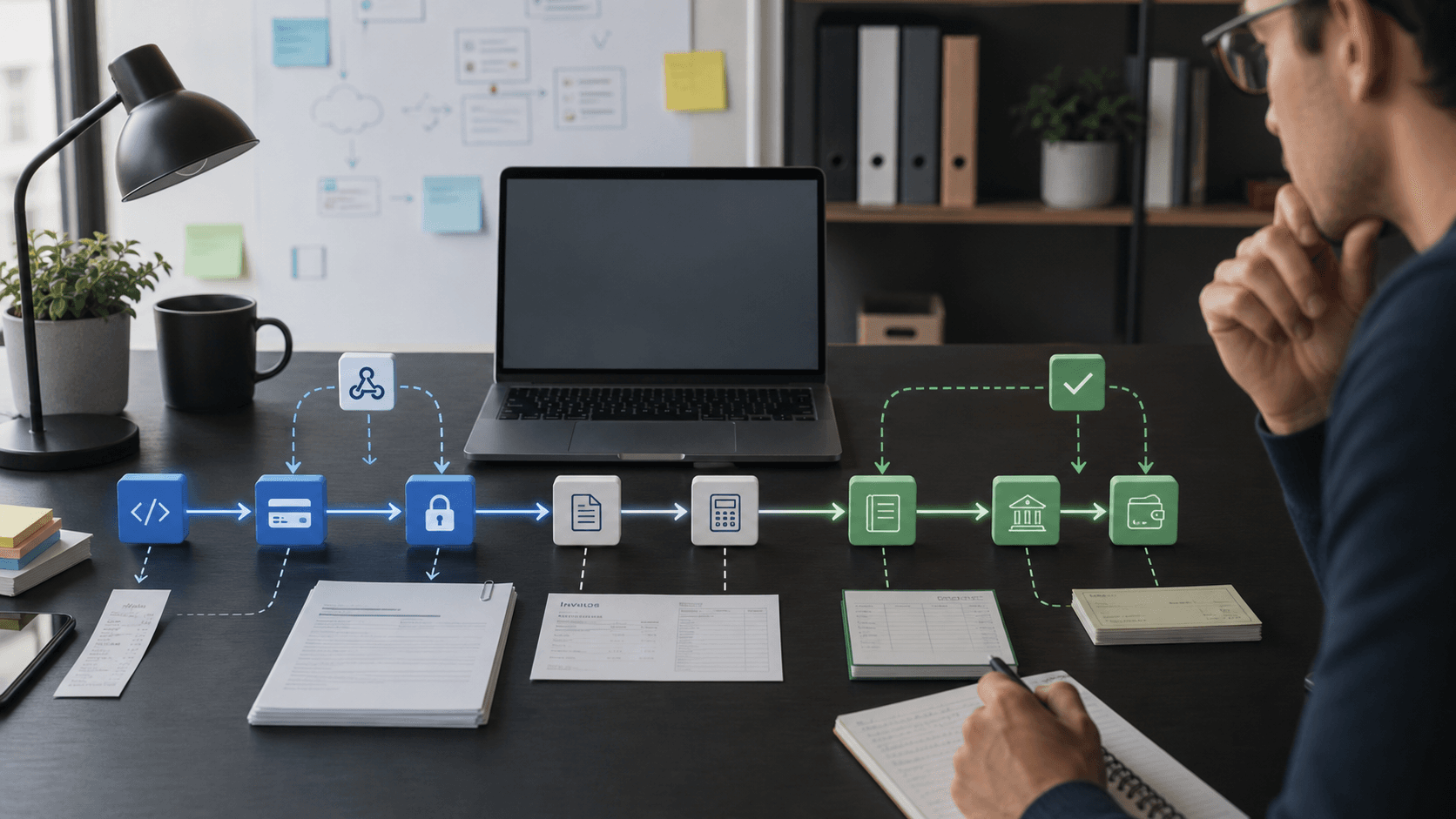

What a business needs is an accepted state that everyone can act on: the customer has paid, the order can be fulfilled, the invoice can be recognized, the tax record can be defended, the fraud decision is understandable, the payout can be reconciled, and the business can explain what happened if a bank, auditor, regulator or angry customer asks.

That is the center of Stripe's value. The company sits between a business and a crowded set of external systems: card networks, issuing banks, acquiring partners, local payment methods, bank accounts, identity checks, fraud signals, tax rules, accounting processes, marketplaces, subscription states and platform payouts. Stripe does not remove all of that complexity. It packages a large part of it behind entities, events, dashboards, reports and support paths. The question is whether that packaging removes enough operational work to justify the fees and dependency.

The public case for Stripe is no longer a small-startup case. Stripe says businesses running on its platform generated $1.9 trillion in total volume in 2025, up 34% from 2024, and that its programmable financial services power more than 5 million businesses directly or through platforms. It also says Link is used by more than 200 million people. Its homepage presents the company as financial infrastructure for revenue, not merely as a card processor, and lists global support for many currencies and payment methods, a large subscription base on Billing, and high historical uptime.

Those claims show the intended frame: Stripe wants to be the financial operating layer for internet businesses.

The danger in that frame is that it can make integration breadth look like proof of operational success. Breadth is not enough. A company can accept a payment and still fail to reconcile it. It can automate subscription invoices and still provision access on the wrong event. It can enable tax calculation and still misunderstand where registration and remittance obligations sit. It can use fraud scoring and still lose good customers or accept bad transactions. It can place payouts in a dashboard and still leave the finance team with a gap between cash received, revenue recognized and fees deducted.

That is why Stripe should be evaluated by repeated production tasks rather than by demonstrations. The first transaction matters less than the thousandth retry. The checkout path matters less than the delayed webhook, the duplicate event, the partially paid invoice, the asynchronous bank debit, the failed payout, the contested chargeback, the month-end balance report and the tax export that appears after the transaction is complete. The system is valuable when those ordinary failures are observable, recoverable and explainable.

A payment is a state machine, not a button

The simplest story about Stripe is that a developer can collect money online. The production story is more complicated because payment is not a single action. A customer may provide a card, a bank account, a wallet or a local payment method. The payment may require authentication. The issuer may decline it. The method may be asynchronous. The same order may be retried. A customer may abandon the flow. A later event may change whether the business should fulfill goods, grant software access or attempt collection again.

Stripe's PaymentIntent model exists because modern payment acceptance is stateful. Public documentation describes PaymentIntents as tracking a checkout flow through a lifecycle and triggering additional authentication steps when required by regulation, custom risk rules or payment method behavior. Stripe also warns that the Dashboard's payment status is a summary and that the PaymentIntent status is the authoritative entity for business logic. That distinction is not academic. A finance or operations team may look at a dashboard status, but the application must decide whether to ship, revoke, retry or wait based on precise state.

The architectural implication is clear: Stripe can reduce payments complexity only when the merchant treats Stripe entities as state that must be mapped carefully into its own system. A successful integration has to store Stripe IDs, handle status transitions, verify whether an event belongs to the right customer and order, and make fulfillment conditional on states that actually mean the money movement is safe enough. The mistake is to treat a callback as a simple success notification.

Stripe's own documentation now recommends higher-level Checkout Sessions with the Payment Element for many integrations rather than direct PaymentIntents, because direct PaymentIntents require more code and some newer features are available through Checkout. That recommendation is commercially important. Stripe is not only selling API primitives; it is steadily pulling customers toward hosted and prebuilt surfaces that absorb more payment-method complexity. For many businesses, that is rational. It can reduce engineering effort, increase access to local methods and simplify authentication handling.

But it also means that the merchant's control moves up a level. The business gets less custom payment plumbing to maintain, but more dependence on Stripe's product choices, checkout behavior and release cadence.

The best way to think about the tradeoff is to separate technical capability from accepted state. Stripe can provide a strong state machine, a tested checkout interface and documented authentication handling. It cannot decide every business rule. A merchant still has to choose when a cart becomes an order, when an invoice becomes revenue, when a subscription becomes access, when a payout becomes cash, and when a delayed payment method is acceptable for fulfillment. Stripe gives the merchant entities and signals. It does not remove responsibility for the mapping.

Idempotency is where reliability becomes a merchant discipline

Idempotency is one of Stripe's most important production concepts because money movement is exactly the kind of operation that cannot tolerate casual retries. If a network request fails after a merchant asks Stripe to create or mutate an entity, the merchant may not know whether Stripe received the request. Retrying with no discipline risks duplicate entities or duplicate operations. Not retrying risks losing a legitimate transaction.

Stripe's API supports idempotency keys for safely retrying requests. Its low-level error handling guidance explains why this matters most during network errors, when the client cannot know whether the server received the request. It also explains that an idempotency key must be reused with the same parameters and that keys expire after 24 hours. The same guidance adds important caveats: rate limiters run before the idempotency layer, some invalid requests are not cached as idempotent results, and a server error can leave the original request in an indeterminate state.

Those details are a good example of the broader Stripe evaluation. The feature is strong, but it is not magic. Idempotency protects a carefully designed integration; it does not rescue one that changes parameters between retries, reuses keys incorrectly, treats all errors the same or fails to store enough local state to reconcile later. A developer can still misuse the primitive. A finance team can still discover duplicate internal orders if the application performs fulfillment before it has safe payment state.

In production, idempotency should be treated as a business control, not a convenience header. The merchant should know which operations must be idempotent, how keys are generated, where they are stored, when retries stop, and how to reconcile an uncertain result. The application should not rely on memory-only state for operations that can move money. It should preserve the Stripe entity ID, the local order ID, the request key, the event ID and the resulting balance or invoice reference in a way that can be investigated.

Stripe's value is that it exposes the reliability primitive and documents how it behaves. The merchant's burden is that the primitive must be installed into local process. The cost of failing to do that is not a vague engineering defect. It is customer double-charging, unpaid orders, manual refund work, support tickets and reconciliation noise.

Webhooks are the handoff between Stripe's state and the merchant's state

If PaymentIntents describe state inside Stripe, webhooks describe the handoff into the merchant's system. This is the most important seam in most Stripe deployments. Subscriptions renew without a customer actively clicking a button. Bank debits can settle later. Disputes arrive after the sale. Fraud decisions can require action. Payouts and balance changes need finance treatment. The merchant must hear about those changes and update local state in the right order.

Stripe's webhook documentation is explicit about the operational pattern. A webhook endpoint should accept an event entities, verify the request, return a successful status quickly before complex logic causes a timeout, and process the business work separately. It also explains signature verification using an HMAC scheme and emphasizes that raw request bodies must not be modified before verification. Those are the basics, but the more important production facts are about delivery behavior.

Stripe documents that undelivered webhook events are resent automatically for up to three days, and that merchants can list events created in the last 30 days to process missed deliveries. It also advises processing only unsuccessfully handled events to avoid duplicates. Public developer discussions and Stripe's own guidance reinforce the same point: webhook delivery is not a single guaranteed exactly-once message. The merchant must design for retries, duplicates and recovery.

That design requirement decides whether Stripe reduces work or moves it somewhere else. A robust merchant integration stores event IDs, maps events to business entities, ignores events that have already been handled, fetches the latest Stripe entity when necessary, and has a manual recovery procedure for periods when its endpoint was down. It can replay missed events without granting access twice or issuing duplicate shipments. It can tolerate a delayed event without assuming that local state is final.

For subscriptions, the issue becomes sharper. Stripe Billing can generate invoices, attempt collection and manage subscription status through a lifecycle. But the merchant still controls the product's access model. Stripe's subscription guidance says integrations should monitor status transitions and use events such as invoice payment and subscription changes to update access. It also notes that an active subscription does not necessarily mean every outstanding invoice has been paid. That kind of nuance is where production systems fail.

If a SaaS product equates one friendly status with full account health, it can provision service incorrectly.

The commercial implication is that Stripe's automation has a hidden integration cost. A simple launch may be fast, but a production-grade launch needs event storage, replay tooling, status mapping, internal dashboards, alerting and operations training. Those are not reasons to avoid Stripe. They are the real price of using it well.

Reconciliation is the finance team's test of developer automation

Developer experience can make payments feel solved before finance agrees. Finance teams live in a different world. They need to know why the bank deposit is smaller than the day's gross sales, which fees were deducted, which refunds or disputes changed the balance, whether a payout batch matches transactions, whether revenue recognition agrees with cash movement, and which currency conversion or settlement rule applied.

Stripe's reporting documentation is useful because it reveals how Stripe expects the reconciliation problem to be divided. The Balance summary report is described as similar to a bank statement and is most useful when a business treats Stripe like a bank account for accounting purposes. It includes activity such as charges, refunds, disputes, adjustments and fees, and provides CSV downloads. The Payout reconciliation report is designed for businesses that want to reconcile each automatic payout with the batch of transactions it settles.

Stripe also notes that instant payouts are controlled by the user and that Stripe cannot identify which transactions are included in each instant payout, leaving responsibility for reconciliation with the merchant.

That last point is important. Stripe can produce reports, but not every payout behavior is equally easy to reconcile. Automation that accelerates cash movement can increase finance work if the settlement trail is not clear. A business choosing instant payouts, manual payouts or complex platform flows needs to price the finance impact, not just the cash-speed benefit.

Stripe also supports programmatic access to balance transactions, which means a business can build its own reconciliation layer. That is attractive for companies with finance engineering capacity. It also raises the bar: the merchant must decide whether Stripe reports are sufficient, whether to sync data into a warehouse, whether to use Stripe Sigma or Data Pipeline, and how to reconcile Stripe state with an ERP, general ledger or internal billing system.

The strongest case for Stripe is that many of these pieces are in one ecosystem. Payments, Billing, Revenue Recognition, Tax, Sigma, balance reports and payout reconciliation can share identifiers and source data. That should reduce the number of brittle handoffs between vendors. The weak point is that "one ecosystem" can become a dependency if the company later wants to change processors, negotiate acquirer economics, route transactions across multiple providers or split finance operations by region.

The right test is practical: how many journal entries, manual exports, support tickets and custom SQL jobs remain after the Stripe integration is live? If Stripe removes custom collection code but leaves finance with a daily spreadsheet fight, the automation is incomplete. If it gives finance a defensible chain from customer event to payment entity to invoice to balance transaction to payout, its value is much greater than a lower-level payment gateway comparison would show.

Billing and tax turn a payment processor into a policy system

Stripe Billing expands the problem from payment acceptance to revenue operations. Subscriptions are not simply recurring charges. They involve trials, plan changes, proration, retries, dunning, invoices, usage, entitlements, failed payments, cancellations and revenue treatment. Stripe's Billing documentation says it can generate invoices, attempt payment collection and manage subscription state throughout the lifecycle. That can remove a large amount of custom code for SaaS companies and marketplaces.

The risk is that Billing also becomes a policy system. Pricing changes, usage metering, discounts, invoice timing and access rules are business decisions encoded into a vendor's entities. That can be excellent if the business wants standard behavior and fast iteration. It can be awkward if pricing becomes highly specialized, if finance wants unusual revenue rules, if the product has complex entitlements, or if legacy contracts do not match Stripe's clean entities. Acquisitions such as Metronome, which Stripe said powers complex usage-based billing models, show that Stripe is investing in the harder end of that market.

But the production question remains: does the merchant's actual monetization model fit the platform without expensive exception handling?

Tax raises the stakes further. Stripe Tax can help calculate and report taxes, but Stripe's own documentation frames tax compliance as a cycle: understand where collection is required, register, calculate and collect, then file and remit. Stripe Tax uses business address, tax registrations, product tax codes, customer location and customer status to determine rates in supported locations. That is a serious automation surface. It is not a guarantee that the merchant has chosen the right registrations, classified products correctly or met filing obligations.

For global digital businesses, that distinction is crucial. A checkout can sell worldwide in minutes, but tax exposure accumulates over time and across jurisdictions. The product tax code that works for one digital service may not work for another. A business-to-business exemption may require customer evidence. A marketplace may need to distinguish platform obligations from seller obligations. A region may change rules or labels. Stripe Tax reports can help, but public documentation notes that report transactions appear with a delay and that jurisdiction naming changes can affect consistency across reports over time.

The commercial case for Stripe Tax is therefore strongest when the alternative is a fragmented stack with manual rate lookup, spreadsheet reporting and weak auditability. Its value is lower if a company already has a mature tax engine, custom nexus analysis and integrated compliance processes. The risk is not that Stripe lacks a tax product. The risk is that teams confuse tax calculation with tax governance.

Fraud automation is an economic tradeoff, not a moral verdict

Fraud prevention is often marketed as protection, but in production it is a tradeoff among fraud loss, authorization rate, customer friction, manual review cost and dispute liability. Stripe Radar and related payment optimization tools sit directly in that tradeoff. A risk model can block bad payments, but it can also block good ones. Authentication can shift liability, but it can also reduce conversion. A rule that feels conservative during a fraud spike can become expensive if it rejects legitimate customers.

Stripe's Radar documentation around 3D Secure shows the nuance. Stripe says it automatically handles soft decline codes indicating that an issuer requires 3D Secure and triggers 3D Secure where regulation requires it. It also warns that indiscriminate 3D Secure use might lower conversion rates. That sentence is the right production frame. Fraud controls are not just technical switches; they are commercial settings.

The public annual letter gives Stripe's side of the value story. It says payment optimization, Radar, checkout and authorization tools use long-running investment in AI and network data to optimize large volumes of transaction flow. It gives examples of customer authorization improvements and dispute reductions. Those examples are useful, but they should not be treated as universal results. Authorization rate depends on merchant category, geography, payment mix, issuer behavior, customer base, transaction size, fraud pressure, refund policy and historical reputation.

The practical question for a merchant is whether Stripe's fraud system improves net revenue after all effects. That means measuring accepted good transactions, blocked fraud, manual review time, chargebacks, dispute win rate, customer complaints, authentication abandonment and support cost. A fraud tool that reduces chargebacks but blocks high-value customers may not be a success. A tool that improves authorization rate but increases later disputes may not be a success either.

Stripe's advantage is that fraud decisions can be connected to payment entities, disputes, authentication flows and reporting. A separate fraud vendor may require more data plumbing and more reconciliation. Stripe's weakness is the same as its strength: placing fraud, payment acceptance and dispute management in one provider can make the merchant more dependent on Stripe's view of risk. Businesses with unusual risk profiles should treat Radar as a system to tune and audit, not a black box to accept.

Disputes are where automation meets the cardholder's bank

Disputes expose the limits of any payment platform. Stripe can notify the merchant, collect evidence, submit responses and automate parts of the process. It cannot make an issuer accept weak evidence. It cannot make a merchant's refund policy clearer after the fact. It cannot recover funds if the merchant misses a deadline or lacks records.

Stripe's dispute documentation says merchants usually have a limited window, often 7 to 21 days depending on the card network, to respond. If they do not respond before the deadline, they automatically lose and cannot retrieve the disputed funds. Stripe also lists email, Dashboard, event and push notifications as channels, and supports programmatic dispute management.

Smart Disputes goes further by automatically assembling and submitting evidence for eligible card disputes, using internal data, merchant transaction data and cardholder data, and determining eligibility based on factors such as reason code, payment method, evidence availability, evidence relevance and cost.

That is an attractive automation story, especially for platforms and high-volume merchants. Manual dispute work is slow, repetitive and easy to mishandle. A system that compiles evidence and prevents missed deadlines can save time and preserve recoverable revenue. But the eligibility language matters. Not every dispute is eligible, not all evidence is equally persuasive, and the underlying merchant process still decides whether strong evidence exists.

For example, a digital goods merchant needs logs that show access, account identity, customer communication and refund policy acceptance. A marketplace needs seller fulfillment evidence and customer messaging. A SaaS company needs records that connect the disputed charge to subscription terms, usage and cancellation history. Stripe can help route and format that evidence, but it cannot invent operational truth.

The dispute surface also changes the economics of Stripe. Card fees are only one part of the cost. Dispute fees, countered dispute fees, operational time, lost goods, customer support and reserve risk can matter more for certain businesses. A company that sells low-risk software subscriptions may find Stripe's dispute workflow manageable. A company with high-ticket goods, complex fulfillment or ambiguous service delivery may need a more active dispute operation.

Connect makes Stripe more strategic and more operationally demanding

Stripe Connect is where Stripe's role expands from merchant processor to platform infrastructure. A platform or marketplace uses Connect to onboard sellers or service providers, accept payments, split money, manage balances, pay out funds, and handle risk across many connected accounts. Stripe's public Connect page says more than 16,000 platforms and marketplaces actively use Connect and that more than 11 million active onboarded accounts get paid through it. The scale matters because Connect is not a feature for a single checkout. It is a system for embedding payments and financial services into other businesses.

The value proposition is strong. A software platform that serves gyms, salons, repair shops, creators, contractors or small retailers can add payments without becoming a full payment institution from scratch. It can monetize transactions, offer faster onboarding, surface dashboards, handle seller payouts and expand into financial services. That can turn vertical software from a workflow tool into a financial operating system.

But Connect also multiplies failure modes. The platform must know which account is responsible for a charge, which balance is available, which party owns a dispute, which seller needs verification, which payout failed, which tax behavior applies and which support path the end user sees. It must decide whether to use Stripe-hosted onboarding, embedded components or custom flows. It must communicate payment risk to users who may not know they are inside a Stripe-powered system.

For platforms, the accepted state is no longer just "customer paid merchant." It may be "customer paid platform, platform retained application fee, seller balance increased, seller verification is sufficient, payout schedule is correct, dispute liability is assigned, tax reporting is not broken, and the end user's dashboard shows the same truth as the platform's internal system." That is a much bigger state machine.

Stripe's recent Sessions 2026 announcements point in the same direction. Stripe highlighted platform pricing tools, embedded components for connected accounts, managed risk options, Smart Disputes for connected accounts, Radar for platform risk, one-click onboarding and cross-border payout capabilities. These are all attempts to reduce platform operating overhead. They also indicate where the hard work is: risk, onboarding, disputes, reporting and payouts.

The commercial question for a platform is not whether Connect makes launch faster. It usually does. The question is whether the platform can run payments as a durable business line. That requires support processes, compliance understanding, seller education, monitoring, escalation paths, finance reconciliation and migration planning. Stripe can carry much of the infrastructure burden, but the platform still owns the customer relationship and much of the operating expectation.

Treasury, Issuing and Financial Connections broaden the state problem

Stripe's newer financial products extend the same theme. Treasury, Issuing and Financial Connections move Stripe beyond accepting money into storing, sending, verifying and spending it. The opportunity is clear: a business that already processes payments through Stripe may want account balances, card programs, bank-account verification, underwriting data, local account details, global payouts and embedded money movement in one environment.

The scope also increases the cost of mistakes. Treasury documentation describes financial accounts that can store funds, send money, support local account details and connect with payments balances, but it also notes availability limits and preview status for certain uses. Issuing documentation describes creating and managing commercial card programs, approving transactions in real time and setting spending controls. Financial Connections allows users to permission financial account data so a business can verify bank accounts, reduce underwriting risk, confirm ownership or build data-powered products.

Each product adds another accepted state. Is the bank account verified? Is the connected account eligible? Are the card controls correct? Did a real-time authorization webhook arrive quickly enough? Is the financial account balance available or pending? Are funds eligible to move from the payments balance to the financial account? Is customer consent sufficient for account data? If the business uses these products casually, the operational blast radius grows.

The benefit is consolidation. A company building embedded finance can avoid stitching together a bank-account verification vendor, card issuing processor, ledger provider, payout system and payment gateway from unrelated pieces. The risk is concentration. If Stripe becomes the merchant's payment processor, billing system, tax helper, fraud layer, payout rail, account data connector and card issuing platform, migration becomes a strategic problem rather than a simple vendor switch.

That does not make the consolidation irrational. For many companies, the opportunity cost of building and maintaining a custom financial infrastructure stack is higher than Stripe's fees. The key is to make the dependency visible. A serious buyer should know which parts of the business would stop, degrade or require manual fallback if Stripe were unavailable, if Stripe changed pricing, if a product stayed in preview, if support response was limited public evidence, or if a regulated feature did not cover a target region.

Reliability claims need operational interpretation

Stripe publishes high historical uptime and operates a public status page. Its documentation also includes health alerts for payment flows and integrations, including basic alerts for certain decline and failed request conditions and advanced alerts for higher support tiers. Support-plan pages describe 24x7 phone, email and chat help for all customers, with paid plans offering priority support, technical account management and escalation features.

Those signals matter, but reliability must be interpreted at the merchant's level. A global status page can say core services are operational while a specific payment method, region, acquiring path, bank, webhook endpoint, merchant configuration or risk rule creates trouble for one business. A 99.999% historical uptime claim does not mean every checkout path has negligible operational risk. It does not eliminate issuer declines, customer authentication friction, local payment method outages, merchant-side bugs, rate limits or support queues.

Stripe's rate-limit documentation is a reminder that stability is a shared responsibility. It says rate limits exist to maximize API stability and prevent abuse, and that clients should treat limits as maximums and avoid unnecessary load. That affects production architecture. A merchant that polls too aggressively, fetches full entities when cached state would do, or performs large backfills through live code can create its own reliability problems.

API versioning is another reliability layer. Stripe's versioning documentation says major releases can contain changes that are not backward-compatible, while monthly releases under the current major line are backward-compatible. It identifies the current version as 2026-06-24.dahlia. The practical point is that Stripe gives businesses a controlled upgrade model, but upgrades still require review. Webhook event versions, SDK versions and account default versions can become hidden dependencies if a company does not manage them deliberately.

Reliability should therefore be measured in workflows, not slogans. How often does checkout fail for reasons under the merchant's control? How fast can the team see and recover from failed webhooks? How many payment states are stuck in manual review? How many payout mismatches appear at month end? How long does support take on account-specific risk holds, tax questions or dispute escalations? How many code changes are required for an API upgrade? Those metrics decide production value.

Pricing is transparent at the entry point and more complex at scale

Stripe's standard pricing message is simple: pay as you go, with no setup fees, monthly fees or hidden fees for standard pricing. That is powerful for startups and new product teams because it removes procurement friction. A business can begin collecting payments before it has the volume, expertise or negotiating leverage to build a custom acquiring setup.

But the commercial question changes as volume and complexity increase. Stripe's pricing pages vary by country and payment method, and the platform includes separate fees or pricing structures for payments, Billing, Tax, Radar, Connect, disputes, instant payouts, currency conversion, support plans and other products. Large businesses may use custom pricing, volume discounts, IC+ pricing or multi-product discounts. Platforms may face different economics again because they monetize payments while carrying connected-account support and risk.

This is not unique to Stripe. Payment economics are inherently layered. The problem is that Stripe's ease of launch can hide cost structure until the business is already dependent. A small team may enable Billing, Tax, Radar, Link, local payment methods, instant payouts and Connect because each product solves a real problem. Later, finance discovers that the combined take rate, dispute cost, currency conversion, failed-payment recovery tools, support plan and migration effort need a full commercial review.

The right comparison is not simply "Stripe fee versus cheaper processor fee." It is "Stripe fee plus residual operating cost versus alternative fee plus integration, compliance, reporting, fraud, support and maintenance cost." Stripe can be expensive as a pure processor and economical as an integrated financial operations platform. It can also be cheap to start and costly to leave.

Migration lock-in is not just contractual. It is data model lock-in. Customer IDs, payment method tokens, subscription entities, invoice history, tax reports, dispute workflows, connected accounts, balances, payout schedules, risk rules and internal dashboards can all become coupled to Stripe's entity model. A business that may later need multi-processor routing, regional acquiring diversity or a different billing architecture should design the abstraction early. Otherwise the future migration project will be paid for with engineering time, finance cleanup and customer friction.

The strongest buyer is the team that prices its own operating work

Stripe is best understood as an exchange: it trades payment and financial infrastructure fees for reduced engineering, compliance, finance and operations work. That exchange is attractive when the buyer can price its own labor honestly. Many businesses underestimate the cost of building payment state machines, subscription billing, dunning, tax exports, fraud tooling, dispute workflows, payout reconciliation and global payment methods. Stripe's appeal is that it makes those costs visible as vendor fees instead of hiding them in years of internal maintenance.

The exchange is weaker when the buyer wants Stripe to remove decisions rather than automate them. Stripe will not decide the merchant's tax nexus. It will not prove every dispute. It will not guarantee that fraud settings maximize net revenue. It will not map every subscription state to product access correctly. It will not reconcile instant payouts that the merchant chooses outside an automatic batch model. It will not make a complex platform's support model simple.

The most mature Stripe customers therefore treat the platform as part of their control system. They design local state around Stripe events. They use idempotency keys deliberately. They define fulfillment rules by authoritative payment state. They test webhook recovery. They monitor rate limits and errors. They reconcile balance and payout reports. They assign ownership for tax registrations, product tax codes and filing. They measure fraud decisions by net revenue, not by blocks alone. They document support escalation paths. They know which Stripe products are core and which are optional.

The least mature customers stop at the happy path. They launch quickly, celebrate the first payment, and then discover the harder work in production: duplicated webhooks, abandoned authentication, subscriptions stuck in incomplete state, tax reports that do not answer the registration question, disputes with weak evidence, payouts that do not match internal orders, support tickets about risk reviews, and a data model that assumes Stripe is permanent.

That contrast explains why Stripe remains strategically important. The company has built a broad, coherent surface for internet commerce at a scale few private technology companies can claim. It can accelerate launch, reduce undifferentiated financial plumbing, and give businesses a path from checkout to financial operations. But its real production value is earned only when the business integrates it as a system of accepted states.

The judgment: strong platform value, conditional certainty

Stripe is a strong choice for developers, SaaS companies, marketplaces, platforms, fintech builders, subscription businesses, finance teams and internet merchants that want to automate money movement without assembling every payment, billing, tax, fraud and reporting component themselves. Its public documentation is unusually detailed about the exact places where production systems fail: idempotency, retries, webhooks, status transitions, reconciliation reports, tax reporting, disputes, rate limits and API versioning. That transparency is a point in its favor because it tells serious buyers where to invest.

The platform is less compelling if a business evaluates it only as an API wrapper around card acceptance. At that level, the fees may look high and the dependency may look unnecessary. Stripe's case improves when the buyer counts the full cost of global checkout, authentication, fraud tuning, subscription state, tax calculation, dispute work, platform payouts, reporting, support and future product expansion. It weakens again if the business has unusual risk, complex tax obligations, strict multi-processor requirements, highly customized billing or a need to own every financial primitive directly.

The central answer is therefore cautious. Stripe can keep payment, billing and financial-state transitions reliable enough for many businesses to automate money movement, but only if those businesses build around Stripe's state model rather than treating it as a fire-and-forget checkout. Its commercial value can exceed fees and lock-in when it replaces real engineering, finance and operations work. It can disappoint when teams count only launch speed and ignore supervision, integration, maintenance, review, exception handling, rollback and unit economics.

Stripe's real test is not whether the first payment succeeds. It is whether the business can explain, weeks later, exactly what happened to the money.