Summary

- Dai Nippon Printing Co., Ltd. is a listed Japanese parent company whose secure-card economics sit inside a much broader printing, information, materials and electronics group. Its most relevant public evidence is not a price list, but DNP Integrated Report 2025, which names Information Security as a focus business, says DNP has Japan's top market share in smart cards, and describes a card-to-biometric identity expansion through Rubicon SEZC.

- The secure-card and identity-production order is valuable when the buyer needs a credential that survives inspection, personalization, fraud pressure, logistics and long service life. Public evidence supports that DNP has the capabilities and market position to sell that bundle, but it does not prove per-order margin, defect rates, issuer retention, government acceptance cycles or the exact premium over a commodity card.

- The strongest pressure on the thesis is substitution. Smartphone identity credentials, low-cost QR labels, outsourced card printers, and rival security printers all reduce the price of a plain credential. DNP's defensible unit is therefore not "a card"; it is an issuer-grade production order in which physical media, chip support, anti-counterfeiting, data handling and continuity matter together.

The hard document that frames the order

The best public starting point for Dai Nippon Printing's secure-card business is DNP Integrated Report 2025. It is a named company report, published by DNP for investors, and it is hard enough to anchor the first judgment because it connects strategy, segment results, technology claims and business targets in one official document. The report proves that DNP treats Information Security as a focus business, not as a small accessory line. It gives FY2024 Information Security sales as 177 billion yen, places the business in Smart Communication, says the information security market is expected to grow at about 7 percent CAGR from 2024 to 2029, and states that DNP has the top market share in Japan for smart cards. It also says DNP acquired a 75 percent stake in Rubicon SEZC in July 2025 to add government ID authentication services across Africa, Asia and South America.

That public document also proves something narrower and more useful for this article: DNP itself defines the value of the card order as a mix of manufacturing and information handling. The report describes strengths in authentication and security technologies, including manufacture and issuance of smart cards, card printers, anti-counterfeiting holograms, biometric devices and software. It points to cryptographic key technologies, factory security, authentication and ID management, cybersecurity, monitoring, cryptographic key management, devices, security consulting and education as parts of the service universe around the card. A buyer is not simply paying for plastic. The buyer is paying for a controlled credential system in which the physical surface, chip, personalization data, keys, anti-tamper features and delivery process have to match.

The same report cannot prove the whole thesis. It does not disclose the selling price of a credit-card run, a national-ID run, a driver's-license run or a corporate-ID run. It does not separate margin by a secure-card order from the rest of DNP's Information Security activity. It does not show rejection rates, personalization error rates, lost-card recovery cost, customer renewal terms, chip sourcing contracts, audit findings or the contractual penalties that decide how much trust is worth in money. It is therefore strong evidence of strategic commitment and capability, but not direct evidence that every secure-card order earns a premium over a commodity print job.

That distinction matters because the economic unit here is the secure-card and identity-production order. A bank, public body, transport operator, employer or credential issuer pays for a batch or continuing program that turns identity data into a durable credential and supporting issuance process. The value only exists if the card is accurate, resistant to tampering, accepted by readers, delivered to the right person, supported over its life, and trusted by the institution that must absorb the cost of fraud, service failure or public embarrassment. The report supports the view that DNP has built a business around that unit. It does not remove the need to test the premium against substitutes.

Company identity and ownership context

Dai Nippon Printing Co., Ltd. is the trade name DNP uses in English. The company is headquartered at 1-1-1 Ichigaya-Kagacho, Shinjuku-ku, Tokyo, and its official corporate page names Yoshinari Kitajima as CEO. DNP traces its founding to October 9, 1876, when its predecessor Shueisha was founded, and the company says it became Dai Nippon Printing in 1935 through the merger of Shueisha and Nisshin Printing. In market terms, it is not a single-product security printer. It is a public, diversified Japanese parent company with a consolidated group around Smart Communication, Life and Healthcare, and Electronics.

That ownership context changes the secure-card question. A stand-alone card shop has to earn its keep mainly from card printers, blanks and service fees. DNP has a wider base: publishing innovation, information innovation, imaging communication, life design, mobility and living, high-performance materials, fine device, optoelectronics, medical healthcare and other group areas. Its company profile for the year ended March 31, 2026 gives consolidated sales of about 1.5126 trillion yen and consolidated employees of 36,360. Its stock information page shows 524,480,692 shares issued and outstanding as of March 31, 2025, including treasury shares, and a shareholder base led by large Japanese trust banks. This makes DNP a listed parent with public-market scrutiny, not a private identity start-up.

The secure-card order benefits from that scale in several ways. First, DNP can carry manufacturing assets, materials knowledge, information systems and compliance staff across multiple businesses. The same group history that produced high-precision printing, photomasks, coating, laminating and imaging can also support hard-to-copy credential surfaces. Second, a large public issuer may prefer a supplier that can show long continuity, large balance-sheet capacity and public reporting discipline. A national-ID program, a bank migration to dual-interface cards or a transport-card refresh is not a casual print purchase. The buyer needs to believe the vendor can remain available, maintain controlled sites, absorb shocks and handle confidential data without becoming the weak point.

Scale can also hide weakness. DNP's public reporting aggregates businesses that have different economics. Smart Communication includes imaging communication, information security, marketing, publishing, and content and XR communication. An investor can see the segment, but not the exact profit of secure cards. A buyer can see the brand, but not the private service levels unless it is in the contract room. The company's breadth therefore supports institutional legitimacy, while also making the individual order harder to value from outside.

For this reason, the article treats DNP's identity as a condition, not a conclusion. The public company is credible enough to be considered a serious credential supplier. The harder question is whether the paid unit, the secure-card and identity-production order, has a durable premium after smartphone identity, low-cost labels, rival printers and in-house issuance options are counted.

What the buyer actually buys

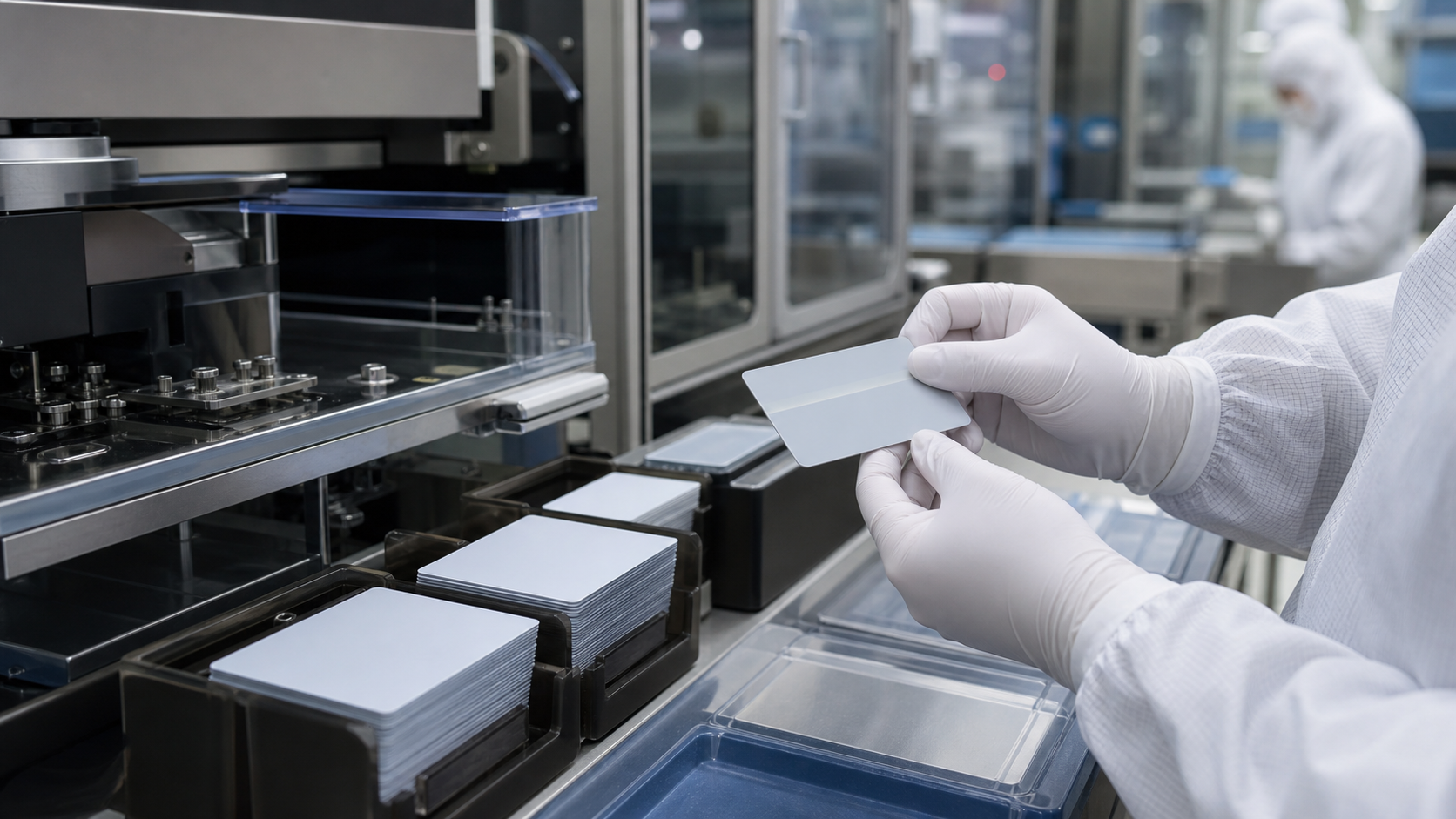

A secure-card order is easiest to misunderstand when it is viewed as a piece of plastic with ink on it. In a bank or government setting, the buyer is purchasing a sequence of commitments. The first is materials selection: card body, chip compatibility, overlay, laminate, hologram, inks and security features. The second is secure design: guilloche patterns, microtext, color-shift inks, UV features, laser engraving, embedded volume holograms and other defenses that make casual copying expensive. The third is personalization: the correct name, photo, account profile, certificate, chip data, magnetic stripe data if used, and any cryptographic or application elements that must be loaded without leakage.

DNP's ID Document Security page is explicit about government ID use cases such as national ID, driver's license and passport. It says DNP provides security components for that market and offers services from design to manufacturing. The same page lists security features for a polycarbonate ID card: OVI and color-matching ink, guilloche patterns, laser engraving, embedded volume hologram, micro-icons, UV fluorescent ink, multiple laser image features, rainbow printing, microtext, surface relief and iridescent ink. Those words are not pricing, but they define the technical reason a buyer may pay more. A plain print vendor can reproduce a layout. A secure-credential supplier must make a document that works under human inspection, machine reading and fraud pressure.

The card printer page adds another layer. DNP's CX-D90HS and CX-D80 series are positioned for gift cards, on-demand ID cards, and corporate and government ID cards. The printer details are industrially mundane, but the details matter. The CX-D90HS lists 600 dpi output, double-side capability, single-side full-color print speed of 25 seconds, a 120-card input and output capacity, compatibility with contact and contactless cards, electronic locks, a status monitor, optional lamination and encoding options. The CX-D80 series lists similar retransfer printing features, a 30-second single-side speed, contact chip and contactless IC encoding options, and optional laminating modules. Consumables are counted in image yields: YMCK ribbon at 1,000 images, other ribbons at 750 images, retransfer film at 1,000 images, and laminate rolls at 600 or 1,000 images depending on the media.

Those figures show why a secure-card order is not a commodity poster run. The unit has bottlenecks. Each card consumes ribbon, film or laminate capacity. A laminator can add 16 to 36 seconds per card, according to DNP's laminator specification. The line must handle card bodies without damaging chips or surfaces. Encoding options add another control point. A card jam, bad image, wrong chip load or wrong recipient is not only spoilage. It can create a privacy incident, failed identity proofing, customer-service cost or fraud opportunity.

The customer therefore buys reliability under constraint. In a financial card, the issuer needs the card to authenticate correctly at terminals and survive daily use. In a public credential, the issuing authority needs citizens or residents to pass identity checks without rework. In a corporate ID, the employer needs a physical token that connects doors, internal systems and visitor rules. In each case, the physical credential is cheap relative to the failure cost. The value of DNP's order is the reduction of that failure cost, not the base material.

Why the order is expensive

The secure-card order is expensive because it combines capital equipment, controlled labor, inspection, materials, information security and logistics in a way that cannot be separated cleanly. A commodity print job can often be checked visually and reprinted if it fails. A secure card that carries personal data, chip functions or government trust has to be correct before it leaves the controlled environment. It may need to pass issuer audits, payment-network rules, local privacy law, customer data restrictions and internal segregation requirements. That means the cost base contains more than printers and plastic.

The fixed-cost side starts with the secure site. DNP's integrated report presents a security-zone model, from outdoor zones through guest, common employee and work zones to a Level 5 high-security zone. The report does not publish the full operating cost of those zones, but the implication is clear. Secure-card orders require buildings, access control, camera coverage, separated work areas, procedures, training, systems, audit logs, and business continuity planning. A supplier that claims to handle millions of credentials must be able to show not just capacity, but controlled capacity.

The equipment side is also broader than the visible card. The card printer page mentions retransfer printing, chip encoding, magnetic stripe encoding, contactless IC encoding and lamination. The ID Document Security page adds hologram application, overlay film, lamination patch and card-body embedding. The Lippmann Hologram page explains that the hologram records interference patterns inside a special photopolymer layer and that only a limited number of manufacturers can mass produce that type. DNP's brand-protection page says holograms can be supplied in label or roll format, with die-cut or adhesive features that make removal difficult. These features require materials chemistry, precision handling and security design, not only layout work.

The variable-cost side includes blanks, chips, inks, films, holograms, carriers, envelopes, delivery, returns, spoilage and support. A secure card also carries the cost of delay. If a bank card refresh is late, cardholders complain and transactions may move to rivals. If a public-credential program misses deadlines, political pressure rises. If a replacement credential is misdelivered, the issuer pays through call-center load and risk investigation. The order price has to compensate the supplier for meeting those time and accuracy constraints.

Compliance makes the unit still more expensive. Payment credentials involve payment-network specifications, issuer requirements and sensitive account data. Government credentials involve identity proofing, personal information, local legal requirements and often a public expectation that the credential will remain valid for years. Even when the end user sees a free card, someone pays for manufacture, personalization, delivery, certificates and support. Public-sector continuity can be more important than per-card price because a failed issuer has to keep serving residents.

The economic burden therefore sits in the hidden middle: the card cannot be so cheap that security controls collapse, but it cannot be so expensive that issuers move to digital-only credentials or rival suppliers. DNP's thesis works if its integrated manufacturing and information-security capability lets it price the order above commodity print while keeping the customer's total failure cost below the cost of switching.

Pricing proxies and substitutes

DNP does not publish a tariff for secure-card orders, so the public record has to be read through proxies. The first proxy is segment scale and margin. For the year ended March 31, 2025, DNP reported Smart Communication net sales of 715,575 million yen and operating income of 34,668 million yen, a 4.8 percent operating income margin. That segment includes more than secure cards, but the margin is useful because it shows the broader business is not a pure software-margin business. It carries physical production, BPO, publishing, marketing and imaging costs. Secure cards must compete for capital inside that mixed segment.

The second proxy is the Information Security focus-business number. DNP Integrated Report 2025 lists FY2024 Information Security sales of 177 billion yen. It also shows DNP planning Information Security sales growth at about 7 percent CAGR and points to growth in online payments, digital transformation, cyberattack response and labor shortages. This does not reveal per-card price, but it places secure cards inside a sizable revenue pool, not a niche craft line. A secure-card order that combines cards, issuance, authentication and support can be meaningful because it belongs to a business measured in hundreds of billions of yen.

The third proxy is equipment throughput and consumable yield. A DNP retransfer printer that prints full-color single-side output in 25 to 30 seconds and consumes ribbon, retransfer film and laminate in finite image rolls creates a visible cost floor for decentralized issuance. If a customer tries to replace a centralized supplier with on-site printers, it must buy machines, consumables, spare parts, secure storage, staff time, waste control and local audit practice. On-site issuance may be attractive for small batches or emergency replacements, but a national, bank or transport issuer still needs a way to manage volume, consistency and sensitive data.

The fourth proxy is a low-cost substitute. TOPPAN, DNP's major Japanese printing peer, describes QR codes and RFID as large markets for assigning unique IDs, and in one public story it says attaching a QR code can cost as little as one cent. That is not a secure-card price, and it comes from a competitor's marketing story, but it is a useful boundary. If a buyer merely needs a cheap identifier on a product, DNP's secure-card order is too expensive. The premium only makes sense when a copied identifier, altered face, broken chip, misissued card or weak proofing process has real cost.

The fifth proxy is digital identity at a zero consumer price. Japan's digital government pages describe My Number Card functions on smartphones and say anyone with a My Number Card and compatible device can use the smartphone service free of charge. The same public material says the physical My Number Card is used for reliable identity verification in person or online and can be added to smartphones. This does not remove the need for physical credentials, because the smartphone service begins from a real card and compatible device. It does show that the end user's willingness to pay for a physical card may be low. The issuer or government must see the value at the system level.

These proxies make the price logic sharper. DNP's secure-card order is not protected by scarcity alone. It is protected only where the customer values audited handling, anti-counterfeiting, long-term durability, physical inspection and continuity more than cheaper labels, app-based credentials or local issuance machines.

Revenue logic and operating leverage

The revenue logic of a secure-card supplier has three layers. The first is the initial production order: design, materials, personalization and delivery. The second is repeat issuance: renewals, replacements, new cardholders, card upgrades, chip migrations and rebranding. The third is adjacent services: authentication, digital keys, identity verification, BPO, customer support, fraud controls, data handling and, increasingly, digital credentials. DNP's public reporting suggests that it is trying to keep all three layers connected.

The DNP Integrated Report 2025 says smart cards are part of a broader Information Security business that includes digital keys, factory security, authentication, cybersecurity, monitoring and consulting. It also names Intelligent Wave, part of the DNP Group, in the context of FEP systems that connect card companies and payment networks and authenticate card usage during card payments. The value is therefore not limited to physical issuance. If a buyer already trusts DNP for card manufacture, it may be easier for DNP to sell adjacent identity and payment infrastructure. If the buyer starts with a software identity project, DNP can argue that it understands the physical credential as well.

Operating leverage comes from reuse. A security design team, materials laboratory, personalization system, audit practice and controlled logistics network can serve multiple customers, as long as each customer's data and features remain separated. A hologram or laminate technology can be sold into ID documents, brand protection and card overlays. A printer platform can support corporate cards, government cards and gift cards. The same information-security organization can support BPO or digital identity services. This reuse is the reason a diversified printer can treat secure cards as more than a mature declining physical product.

The risk is that operating leverage can move in reverse. If card volumes fall faster than expected, fixed sites and specialized staff become harder to absorb. If a large issuer delays a refresh, margin can swing. If a new regulation or chip shortage raises costs, DNP may not be able to pass them through immediately. The integrated report's broader cost discussion says DNP faced high raw-material and fuel prices, yen depreciation, wage increases and inflation, and that it sought to pass cost increases into sales prices while streamlining procurement. Secure-card orders are not immune to that pressure. Card bodies, chips, films, inks, adhesives, power and labor all sit inside the cost base.

The revenue logic therefore depends on order quality. A one-off low-price card run is less attractive than a multi-year issuer program with renewals, support and adjacent identity services. A public-sector credential can be attractive if it produces long continuity, but it can also be slow, politically exposed and procurement-driven. A bank card portfolio can deliver repeat demand, but it is sensitive to card-network rules, chip availability, payment shifts and issuer bargaining power. DNP's public strategy appears to favor the richer version of the order: physical card plus identity infrastructure plus international government authentication. That is the right logic, but the exact private economics remain unproven from public evidence.

Customer dependence and switching costs

The secure-card customer buys trust because switching is costly. A bank cannot replace a card supplier by asking a generic print vendor to copy the front design. It must qualify the new vendor, test card bodies, chips, personalization files, mailers, activation procedures, customer-service flows, fraud controls and disaster recovery. It must also protect sensitive cardholder data during migration. A government credential is even more difficult. The supplier may have to align with laws, citizen-facing service counters, enrollment partners, certificate systems, local offices, reader infrastructure and public communications.

DNP's public claim to Japan's leading smart-card position matters because installed trust creates switching friction. The integrated report says DNP developed rewritable smart cards in 1983 and became Japan's leading smart-card vendor. A buyer with years of prior issuance experience may prefer the known defect profile and audit history over a cheaper new bidder. That preference is not irrational. The visible card is only the end of a controlled chain. The buyer needs to know how exceptions are handled: bad photos, name changes, misprints, lost cards, damaged chips, expired certificates, cardholder complaints, unusual characters, regional delivery problems and emergency reissuance.

At the same time, switching costs can make the buyer more aggressive on price once the supplier is embedded. Large issuers know the supplier wants continuity. Banks, telecom firms, transport systems and public bodies can run competitive tenders, divide lots, bring some issuance in house or benchmark against rivals. A buyer may accept DNP's premium for the first high-risk migration, then negotiate harder on renewals. The supplier's defense is to keep adding value that is hard to compare on a per-card basis: lower error rates, better personalization, faster replacement, stronger audit evidence, more flexible card features, integration with digital identity and reliable support during incidents.

The customer base also differs by card type. Corporate and campus ID orders can be more local and printer-led. A company may use on-site card printers and accept simpler security features. Gift cards can be cost-sensitive and tied to retail campaigns. Payment cards require stronger issuer and network alignment. Government ID orders are slower, larger and more politically sensitive. DNP's product pages cover all of these, but the thesis is strongest at the high-trust end: government ID, driver's licenses, passports, banking and other credentials where a failed card can create fraud, service denial or reputational damage.

The Rubicon acquisition points to DNP's desire to enter that high-trust end more deeply outside Japan. Rubicon is described by DNP as providing services from consulting and biometric data enrollment to development and maintenance of authentication devices and software, with implementation in more than 50 countries and regions. That is not merely a card supply story. It is a bet that governments will pay for identity-production systems that combine secure physical credentials, biometrics and service continuity. The public evidence supports the direction. It does not disclose whether DNP can win those orders profitably against entrenched identity vendors in each country.

Supplier and upstream dependence

The secure-card order looks vertically integrated when it leaves DNP's site, but it depends on upstream materials and technologies. Card bodies need plastics such as PVC, composite PVC, PET-G, ABS or polycarbonate depending on the application. Laminates need patch film or overlay foil. Holograms need special films and controlled production. Chip cards need embedded IC modules and, for payment or government programs, compatibility with reader and certificate environments. Printers need ribbons, retransfer film, laminators, encoders and maintenance.

DNP has internal strengths in several of these areas. Its integrated report emphasizes printing-derived technologies such as microfabrication, precision coating, materials development, post-processing, laminating, holograms, photolithography, information processing, image processing and information security. Its card-printer page shows it supplies ribbons, retransfer films, laminators and laminate media. Its ID Document Security and hologram pages show security components that can be layered into the credential. These public materials support the idea that DNP is not merely buying blanks and printing them. It has internal technology around surfaces, security features and issuance.

The public record still leaves important upstream questions open. It does not disclose chip sourcing by customer program. It does not disclose whether a given payment-card order relies on one or several semiconductor suppliers. It does not show inventory buffers for blank cards, films or inks. It does not show exposure to export controls, regional procurement rules or local-content requirements. It does not show how DNP allocates scarce capacity between high-margin electronics products and secure-card needs if both require precision manufacturing resources.

The cost pressure is also visible at group level. DNP's 2025 report says raw materials and energy prices rose because of imported raw-material costs, yen depreciation, wage increases and broader inflation. The group worked to pass cost increases into sales prices and streamline procurement. A secure-card buyer may resist price increases, especially in public procurement or multi-year bank contracts. That creates margin risk when materials and labor move faster than contract pricing.

Upstream dependence is one reason DNP's secure-card premium must be judged through service continuity, not only feature count. A supplier with better purchasing, site redundancy, quality control and materials know-how can be worth more during shortages. Conversely, if a chip shortage, material disruption or cybersecurity incident hits the supplier, the buyer's dependence becomes a vulnerability. DNP's scale and diversified technology base reduce some supplier risk, but the public record cannot prove resilience for a specific credential program without contract-level service metrics.

Competitors and substitutes

DNP's obvious peer pressure comes from TOPPAN, another Japanese printing group with security, information-management and ID-management capabilities. TOPPAN's public materials describe information management, security DX, securities and business printing, IoT solutions and product authentication. Its story about NFC and RFID tags places government ID and secure payments among its security-solution businesses. This does not prove that TOPPAN wins the same orders as DNP in each market, but it proves the strategic category is not DNP's alone. Japanese printing groups with long histories have moved from print into trust-bearing information media.

Global competitors and substitutes widen the field. Secure identity can be supplied by specialized government-ID vendors, payment-card manufacturers, biometrics firms, mobile-wallet providers, cloud identity companies, local state printers, in-house bureau operations and card-printer distributors. Some buyers may prefer a global identity specialist over a Japanese diversified printer. Others may insist on domestic production for sovereignty reasons. Still others may divide the work: a security printer supplies the card, a technology provider supplies digital certificates, and a local integrator handles enrollment.

The lower-cost substitute is not a rival secure card; it is the claim that the buyer does not need a secure card at all. A QR code label can identify a product at extremely low cost. A smartphone credential can present identity without a new physical card in many settings. A corporate office can print badges locally. A retailer can issue a simple gift card. A government can extend the life of existing credentials. A bank can encourage tokenized payments and mobile wallets. These options do not eliminate secure cards, but they define the price ceiling.

The secure-card order survives when the substitute fails one of four tests. The first is inspection: the credential must be accepted by people and machines in varied locations. The second is durability: the credential must last through years of handling. The third is fraud resistance: copying, alteration or misuse must be costly. The fourth is inclusion: the credential must work for people who cannot, will not or should not rely only on smartphones. Public identity systems often need the physical credential because it remains portable, inspectable and independent of a charged device.

DNP's own product mix acknowledges the hybrid future. It sells card printers and ID document security, but also decentralized identity management and digital keys. The company's best strategic position is therefore not physical against digital. It is physical plus digital. If a buyer needs both a card and a wallet, or both a card and biometric verification, DNP can try to sell continuity across media. If the market moves to digital-only identity faster than expected, DNP's physical-card advantage weakens unless the digital identity platform gains independent traction.

Regulation, geopolitics and operational risk

Secure credentials sit close to public trust, so regulation and geopolitics matter. A government identity credential may involve personal data, residency rights, health insurance, tax access, driver's licensing, border procedures or public benefits. A payment card may involve payment-network rules, sensitive authentication data, anti-fraud expectations and breach liability. A corporate or campus credential may involve building access and employee privacy. In all cases, the supplier has to act as if an error will be examined after the fact.

Japan's My Number Card illustrates the public-sector continuity problem. Japan's digital government page says the My Number system identifies individuals in administrative procedures and allows information coordination among administrative bodies so attached documents can be omitted. It also says the card can be used for identity verification in private services. The same public site describes smartphone My Number Card functions and health-insurance use. This creates long-term demand for reliable identity media and authentication services. It also creates political sensitivity when identity linking or service operation goes wrong. Public trust is part of the product.

Geopolitics becomes more important as DNP moves into overseas government ID authentication. The Rubicon acquisition places DNP in markets across Africa, Asia and South America, according to the integrated report. Government ID projects in emerging markets can be large and durable, but they can also bring election timing, sovereignty concerns, procurement disputes, data-localization rules, currency risk, anti-corruption scrutiny and public suspicion of foreign vendors. The public record supports the growth ambition, not the risk management outcome.

Operational risk is more prosaic but just as important. A secure-card supplier must prevent data leakage, insider abuse, defective personalization, card substitution, missing shipments, file mismatch, poor key handling and disaster interruption. DNP's report says the group implements business continuity management measures to keep business activities from interruption. It also presents a robust security framework for Information Security. Those claims are useful, but buyers would need audit evidence, incident history, recovery time, defect metrics and contractual remedies before treating the risk as solved.

Regulation can also create opportunity. If payment networks push dual-interface cards, if governments require stronger ID, if healthcare or transport systems require physical backup credentials, DNP can sell more advanced cards and services. If regulators accept smartphone credentials broadly and reduce physical renewal needs, card volumes may soften. The article's thesis therefore depends on the direction of regulation: DNP benefits when regulators require strong identity assurance and continuity across physical and digital channels; it loses pricing power when rules allow cheaper bearer proofs for the same use cases.

Network-resource evidence and data locality

Public DNS and hosting records provide a bounded view of DNP's digital surface and a weak clue about public-service locality. They prove only how public-facing domains resolve at the time checked; they do not prove internal architecture, data residency, service uptime, security posture, customer systems or contract performance. The current public checks for dnp.co.jp show mail exchange records pointing to mx1.dnp.co.jp through mx4.dnp.co.jp. TXT records include an SPF policy that authorizes securemx.jp, several DNP IP addresses and Microsoft 365 protection. The global.dnp web domain resolves through Fastly IP addresses, and www.global.dnp points through cdn.adobeaemcloud.com and adobe-aem.map.fastly.net before reaching Fastly addresses. Name servers for dnp.co.jp use the d-53 family.

This matters for the secure-card thesis because identity production is no longer only a factory question. A public company selling authentication, digital keys, decentralized identity and customer contact has to explain which functions are local, which are outsourced, which carry identity data and which are only public communication channels. Adobe Experience Manager Cloud and Fastly records for the public global site are not a weakness by themselves. They are normal public-web dependencies. Microsoft 365 in SPF is also a common enterprise mail dependency. These records show that DNP's public communications layer uses major third-party cloud and network services.

The boundary is important. A public marketing site using Adobe and Fastly does not mean DNP's card-personalization systems, government-ID systems or payment systems use the same public architecture or store data in the same places. It does not prove that sensitive cardholder data touches those services. It does not prove that a cloud outage would stop a secure-card production run. It only shows that part of DNP's public-facing presence depends on third-party digital infrastructure. In an identity business, such dependencies still deserve attention because customer trust is affected by website availability, mail authentication, public notices, support forms and incident communication.

The cloud-service dependency also frames a strategic tension. DNP sells trust that bridges physical and digital identity. To do that, it must integrate with public web services, issuer systems, mobile wallets, certificate services and security tools. The more the value shifts toward digital identity, the more DNP has to prove it can operate as a digital-service company, not only as a secure manufacturer. The public DNS evidence is modest, but it is consistent with a company that uses external web and mail providers for public surfaces while selling higher-assurance systems in its core business.

The evidence does not justify treating a DNS record, IP address, mail host or content provider as the company itself. These are only public-surface clues. The investment question remains whether DNP can convert its manufacturing trust into digital and hybrid identity trust without becoming merely an integrator of other companies' cloud services.

Unofficial and market signals

Unofficial signals in this case are useful mainly as pressure tests. The most relevant is not a social-media rumor; it is market behavior visible in public product and competitor pages. TOPPAN's one-cent QR-code comment is a strong reminder that many identity-like needs are cheap when the required assurance is low. A brand, retailer or logistics customer can often start with a printed code, RFID label or cloud record rather than a secure card. That signal does not refute DNP's high-security card business. It identifies the bottom of the market that DNP should avoid if it wants premium returns.

A second signal is the proliferation of desktop and retransfer card printers for local issuance. DNP sells such printers itself, and the product page is candid about corporate and government ID applications. This creates a dual role. Printer sales help DNP participate in decentralized issuance. They also create a substitute for centralized production in smaller programs. If a university, office, event operator or small municipality can issue acceptable cards locally, it may not need a large production order. The large DNP premium is more defensible when card issuance requires controlled data, scale, cryptographic or chip handling, anti-counterfeiting and consistent nationwide quality.

A third signal is the rise of smartphone identity. Japan's smartphone My Number Card page says the service lets users add My Number Card functions to compatible iPhones and Android devices, with biometric identity verification instead of entering a PIN in some cases, and describes use at Mynaportal, convenience-store certificates, medical institutions and e-Tax. This is official, not rumor, but the market signal is behavioral: users and service providers are being trained to expect credentials in phones. DNP's physical-card order must either remain essential as root credential, backup and inspection medium, or be bundled with digital identity services.

A fourth signal is the global government-ID opportunity that DNP is pursuing through Rubicon. Government ID authentication projects can be attractive because they carry large populations and long service life. They can also be hard to price from outside because revenue recognition, local partners, device sales, software maintenance and enrollment services may be mixed. DNP's target of 140 billion yen cumulative sales in overseas government ID authentication services by fiscal 2030 is ambitious enough to validate the strategic interest, but it remains a target, not proof of realized economics.

These signals suggest a market split. Low-assurance identity becomes cheap and digital. High-assurance identity becomes more complex, mixing physical cards, biometrics, digital wallets, secure enrollment and continuous authentication. DNP's opportunity is in the second market. Its risk is being pulled into the first on price or failing to prove digital-service strength in the second.

What would change the judgment

Several private metrics would strengthen or overturn the current judgment. The first is per-order gross margin for secure-card and identity-production work. If DNP's highest-security orders earn only commodity margins after materials, controlled-site costs, rework, audits and support, then the thesis fails. If they earn a durable premium and renew on multi-year terms, the thesis is stronger than public reporting can show.

The second metric is defect and incident performance. A low reissue rate, low personalization error rate, low card failure rate and clean audit history would prove that DNP's premium is buying lower failure cost. A history of misissued cards, chip failures, mail errors, data incidents or missed deadlines would do the opposite. Public product pages describe capability; only operational history proves reliability.

The third metric is customer retention by issuer type. A bank or public-body credential program that renews after competitive review is stronger evidence than a one-time order. Retention would show that switching costs and service quality work in DNP's favor. Lost flagship accounts would suggest price or performance pressure. Public statements about top share in Japan are helpful, but account-level retention would be more decisive.

The fourth metric is the mix of physical card revenue and digital identity revenue. DNP's strategy appears to combine smart cards, card printers, digital keys, biometric authentication and decentralized identity. If the digital side is growing because DNP is trusted beyond the card, the physical credential can become part of a broader identity platform. If digital identity revenue remains small and card volumes decline, the secure-card order may become a slower-growth manufacturing line.

The fifth metric is overseas government-ID execution. Rubicon's footprint and DNP's target are meaningful, but the key questions are project profitability, country concentration, payment risk, data-localization compliance and post-implementation support. A few large wins could lift the business. A troubled rollout could damage the trust thesis quickly.

The sixth metric is procurement price pressure. Secure-card orders are vulnerable to tenders that specify features tightly enough for multiple vendors to bid. If governments and banks can standardize requirements and shift volume between suppliers, DNP's premium narrows. If DNP's proprietary combination of holograms, personalization, secure process, printers, authentication software and service continuity is hard to replicate, the premium survives.

The available public evidence is therefore supportive but incomplete. It supports DNP as a credible institutional supplier and a serious player in secure-card and identity production. It does not prove that the secure-card order is always high-return. The judgment would change if private metrics showed weak margins, weak retention, high rework, poor digital adoption or government-ID execution problems.

Public evidence and what it supports

DNP Integrated Report 2025 is the central evidence. The investor report page at https://www.global.dnp/en/ir/library/ points to the current report set. The Information Security section at https://www.global.dnp/content/dam/dnp-global/pdf/en/ir/library/annual/DNP_integrated2025e_P38-55.pdf.coredownload.pdf supports DNP's focus on Information Security, the FY2024 Information Security sales figure of 177 billion yen, Japan top market share in smart cards, Rubicon acquisition details and the overseas government-ID sales target. The business-results section at https://www.global.dnp/content/dam/dnp-global/pdf/en/ir/library/annual/DNP_integrated2025e_P98-115.pdf.coredownload.pdf supports Smart Communication segment performance and the broader cost and business-continuity context. These sources are strong for strategy and segment framing, moderate for the secure-card order, and weak for per-order margin.

DNP's company profile at https://www.global.dnp/en/corporate/overview/ supports identity facts: trade name, CEO, headquarters, founding date, capital, sales, employee count and business segments. It is strong for company identity and parent context. It does not price the secure-card order.

DNP's ID Document Security product page at https://www.global.dnp/en/biz/solution/security_solutions/1193101/ supports the claim that DNP sells government-ID security components and services from design to manufacturing. It is strong for feature scope, including polycarbonate-card security features and hologram application types. It does not prove adoption volume or price.

DNP's Card Printer page at https://www.global.dnp/en/biz/solution/security_solutions/1193109/ supports the practical cost stack of on-demand issuance: retransfer printing, 600 dpi output, full-color print speeds, input capacity, encoding options, locks, laminators, ribbon yields and laminate yields. It is strong for production constraints and substitute analysis. It does not show transaction prices.

DNP's Lippmann Hologram page at https://www.global.dnp/en/biz/solution/security_solutions/1193100/ and Brand Protection page at https://www.global.dnp/en/biz/solution/security_solutions/1193099/ support the anti-counterfeiting argument. They show that DNP markets advanced hologram features, mass-production difficulty and brand-protection use cases. They are strong for capability description. They do not prove a secure-card customer's willingness to pay.

DNP's decentralized identity page at https://www.global.dnp/en/biz/solution/security_solutions/20175557/ supports the physical-plus-digital direction. It shows that DNP sells a platform for issuing and verifying verifiable credentials and wallet applications. The broader identity theme page at https://www.global.dnp/en/biz/theme/catrina/ supports DNP's references to international standards and Japan-Australia collaboration. They are strong for strategic adjacency. They do not prove scale.

Japan's digital government My Number page at https://www.digital.go.jp/en/policies/mynumber and smartphone My Number page at https://www.digital.go.jp/en/policies/mynumber/smartphone-certification support public-sector demand and substitution pressure. They show that My Number Card is used for administrative identity verification and private services, and that smartphone My Number Card functions are being expanded. They are strong for the public identity environment in Japan. They do not show DNP's role in any particular government program.

TOPPAN's public solutions page at https://www.holdings.toppan.com/en/solution/ and security-solutions story at https://www.holdings.toppan.com/en/story/story2.html support competitor and substitute pressure. They show that another Japanese printing group also positions printing-derived trust services as a growth field, and the QR-code cost comment gives a useful low-assurance price boundary. They are strong for market context, not proof of DNP pricing.

Public DNS checks support only a narrow network-surface observation. DNP's public web presence resolves through Fastly and Adobe AEM Cloud for www.global.dnp, while dnp.co.jp mail records and SPF show enterprise mail dependencies including Microsoft 365 protection. This is useful for cloud dependency and public communications context. It is not evidence of internal credential-production architecture.

Conclusion

The evidence supports a qualified version of the thesis. Dai Nippon Printing's secure-card and identity-production order is valuable when the buyer is not buying a card at all, but a controlled credential event: security design, material performance, chip or certificate handling, personalization, inspection resistance, delivery, continuity and institutional trust. DNP's official documents show that the company has the scale, history, technology claims and strategic commitment to sell that bundle. Its Information Security business is large enough to matter, its smart-card position in Japan is publicly asserted, and its Rubicon acquisition shows an ambition to move deeper into government identity authentication outside Japan.

The public record also suggests that DNP has to earn the premium continuously. Secure cards face low-cost QR identifiers at the bottom, local card printers in smaller programs, smartphone credentials in consumer identity, and rival security printers in high-assurance markets. A physical card remains valuable when it must be inspected, durable, inclusive and hard to tamper with. It becomes vulnerable when the buyer only needs a cheap identifier or a mobile credential.

The available evidence is consistent with DNP being a serious institutional supplier rather than a commodity printer. The thesis remains unproven without private metrics: secure-card gross margin, defect rates, audit results, renewal rates, issuer concentration, chip-supply resilience, overseas government-ID profitability and digital identity revenue. Until those metrics are visible, the best judgment is disciplined rather than absolute: DNP appears well placed to sell invisible trust in a secure card, but the financial value of each order depends on whether customers keep paying for the hidden controls after cheaper substitutes are available.