Summary

- Ipcore Datacenters S.L has credible public evidence of a Madrid carrier-neutral colocation business: the company site describes 1,200 square metres of space, private and shared racks, redundant power and cooling, 24x7 staffing, 10-plus carrier points of presence, remote-hands support and links to internet exchanges and third-party data centres.

- The strongest economic case is not hyperscale growth. It is renewal leverage: customers that need local Madrid racks, cross-connects, remote handling and multiple carrier options may value continuity enough to absorb disciplined price increases and supplier pass-throughs.

- The main weakness is undisclosed concentration. Public sources do not reveal customer count, rack occupancy, contract duration, churn, revenue by product, top-customer share, channel mix, power cost recovery, debt, margin or capex commitments, so customer dependence must be treated as bounded uncertainty rather than as an established fact.

The incentive is to stay necessary when customers can bargain

The first question for Ipcore Datacenters S.L is not whether Madrid needs more digital infrastructure. Madrid clearly sits inside one of Europe's expanding data-centre and interconnection markets. SpainDC and market advisers describe a Spanish capacity build-out driven by cloud, artificial intelligence, enterprise outsourcing and the growing importance of Southern Europe as a connectivity corridor.

Ipcore's own site presents a more specific proposition: a carrier-neutral Madrid data centre near Autovia A-2 and Madrid Airport, offering colocation, connectivity, remote support and a meet-me-room environment for customers that want choice among carriers.

The harder question is whether that proposition gives Ipcore enough bargaining power. Colocation is a recurring-revenue business, but it is not automatically a high-margin business. A rack customer can be sticky because migrating servers, IP addressing, cross-connects, DNS, firewall rules, carrier circuits and support routines is inconvenient. That stickiness can support renewal pricing. It can also become fragile if the customer is large enough to bargain, if a reseller or channel controls the end relationship, or if competing Madrid facilities offer a cleaner migration path.

The economic incentive is therefore to be operationally necessary without becoming operationally captured.

That distinction matters for customer dependence. If Ipcore's demand is spread across many small and mid-sized customers, each customer may value responsive support while none can dictate terms. If demand is instead shaped by a handful of anchor accounts, managed-service providers, carriers or resellers, then those accounts may have renewal leverage. They can ask for bespoke support, delayed pass-throughs, custom power terms, extra cross-connect work, preferential access or price protection.

A small facility can look full and still carry weak economics if too much of its utilisation depends on a few buyers whose cost of leaving is lower than the operator's cost of losing them.

The public record does not disclose which version is true. There is no customer list, no top-ten revenue concentration, no churn figure, no occupancy history and no contract-duration schedule. The correct judgment is not to invent concentration, but to test the incentives that concentration would create. Ipcore's operating boundary makes the test concrete. The company sells space, power, connectivity and hands-on support in a single Madrid facility. Those services can become sticky when they are integrated into a customer's operating stack.

They can become low-margin when the customer treats them as a commodity rack purchase and uses Madrid's growing queue of planned capacity as leverage.

The management problem is therefore one of discipline. Ipcore needs to fill space, but not at any price. It needs to offer remote support, but not let bespoke work turn every recurring customer into a labour-intensive exception. It needs to pass through power, carrier and equipment costs where contracts allow, but not overplay pass-throughs in a market where alternative facilities exist. It needs customers and channels, but not so few that one renewal can change the investment plan. That is why customer dependence is the right economic lens.

Identity narrows the case to Madrid colocation and connectivity

Ipcore Datacenters S.L should be analysed as an operating company tied to a Madrid data-centre facility, not as a generic cloud brand. The official legal notice names IPCore Datacenters SL as the website owner, gives tax ID B86088945, lists Calle Marzo 16, 28022 Madrid as the registered address, and states that the website provides information about carrier-neutral data-centre services in Madrid, including colocation, connectivity and related services. The same address appears on the company's homepage contact block and in RIPE organisation data. That alignment supports a real company identity, not just a marketing landing page.

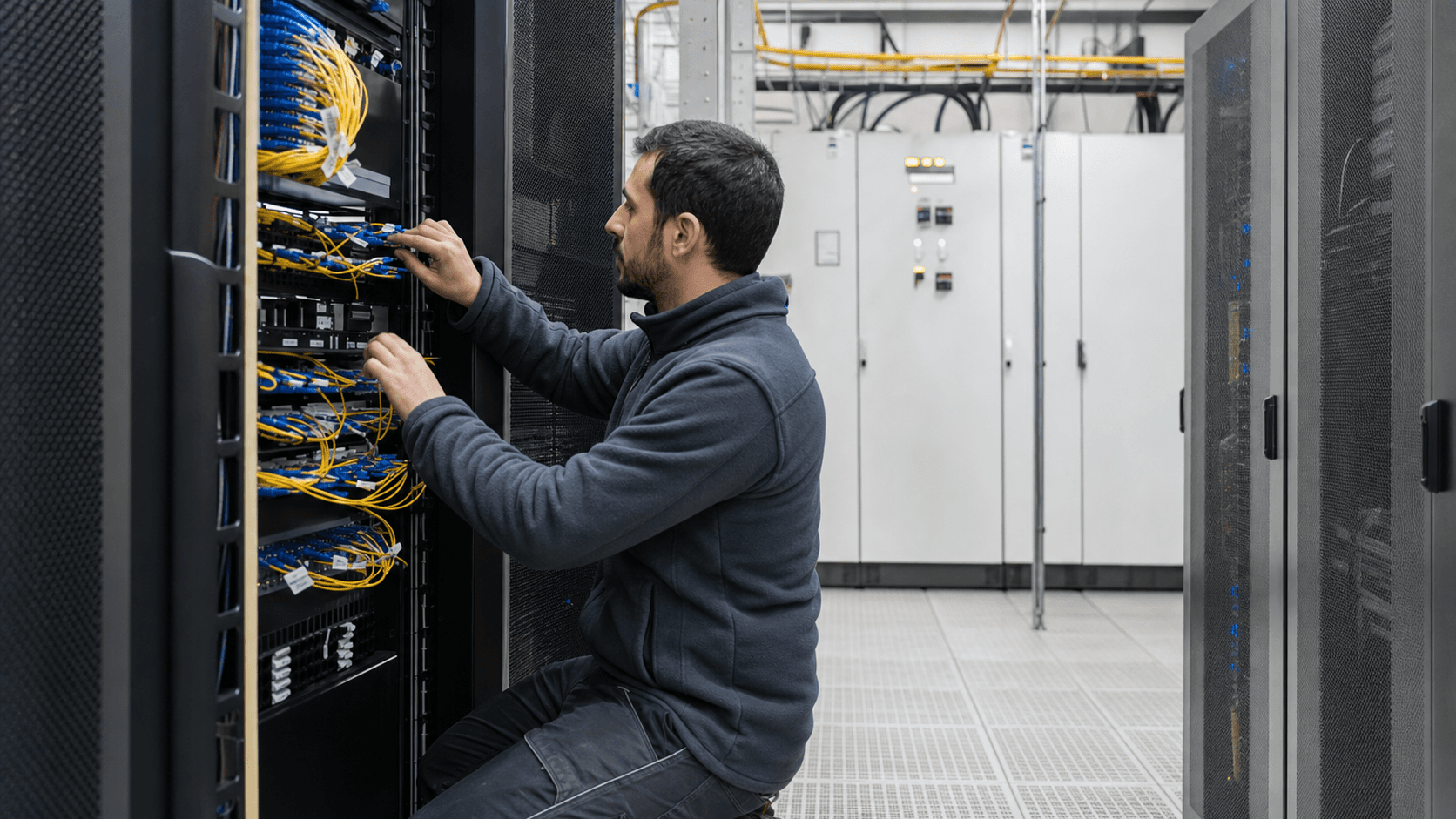

The company site is unusually useful because it defines the commercial boundary. Ipcore introduces itself as a carrier-neutral data-centre provider. Its colocation page describes 42U and 20U private rack enclosures, redundant A+B power feeds, 2N UPS support, metered or unmetered electrical power options from 1 kVA to 5 kVA, custom rack space, fenced spaces, meet-me-room space for carriers and roof space for antenna and satellite-dish colocation.

The networking page describes direct interconnection between carriers and customers, more than ten on-site carrier points of presence, fibre links to internet exchanges and third-party data centres, cross-connects, DCI links, IXP fibre links to Espanix and DE-CIX, fibre and copper client cross-connects, and radio-frequency links.

The support page adds another layer: 24x7x365 remote hands, incoming hardware handling, rack mounting, cabling management, switching of storage devices, network cards and connectors, and RMA or return shipping. That list matters because it is a labour promise, not only a space promise. A customer that cannot send staff to Madrid can still deploy and maintain hardware if Ipcore performs practical tasks on site. The service can be valuable, but it also changes the margin model. A rack sold with occasional cross-connect work is different from a rack sold with frequent manual intervention, emergency handling and device swaps.

Facility claims also frame the asset. Ipcore says its Madrid data centre is a secure, single-tenant, free-standing building near Autovia A-2 and Madrid Airport, staffed 24x7, with CCTV security, fire protection, ISO 9001, ISO 50001 and ISO 14001 certifications, 2N UPS, backup diesel generation, 2N cooling, redundant fibre entrance pathways, hot-aisle/cold-aisle layout, raised floor and locked rack enclosures. The site says the centre has 1,200 square metres of highly connected space for private racks, shared rack space and private cubes.

Third-party data-centre directories repeat similar themes, including one Madrid facility, carrier-neutral positioning and space for private racks and shared racks.

This identity excludes several tempting but unsupported interpretations. Ipcore is not shown publicly as a hyperscale campus developer, a national fibre-access operator, a public cloud platform, a global IP-transit carrier or a software-as-a-service company. It may host customers that do those things, and it may sell connectivity around them, but the public evidence points to a Madrid colocation and interconnection operator. That boundary is economically important.

The value of the company is likely to sit in local facility execution, power reliability, connectivity choice, support responsiveness and renewal retention, not in global network scale.

The operating boundary is racks, power, cross-connects and support

Ipcore's business model looks like a compact version of the classic carrier-neutral colocation model. The customer pays for physical presence in a controlled environment. The operator provides secure space, rack or partial-rack capacity, power, cooling, fire protection, access control, connectivity options, cross-connects, technical support and a stable address for network deployment. The customer benefits from not having to build or maintain a private equipment room. The operator benefits if it can spread fixed infrastructure and staffing costs across a dense base of recurring customers.

The customer proposition has three parts. The first is continuity. Servers, routers, switches and storage need stable power, cooling, access control and predictable maintenance routines. The second is optionality. A carrier-neutral facility is more valuable when customers can choose among multiple network providers, connect to internet exchanges, take cross-connects and avoid dependence on one carrier. The third is operational convenience. Remote-hands support lets customers treat the site as an extension of their own infrastructure even when they do not have staff in Madrid.

Those three features can create renewal leverage. A customer that has spent years wiring cabinets, building cross-connects, negotiating circuits and operationalising support routines may not want to move for a modest saving. If Ipcore's facility is reliable and responsive, renewal discussions may focus less on raw rack price and more on risk avoidance. That is where pricing power can emerge in a small facility. It is not monopoly power. It is the practical friction of moving live infrastructure.

The same features also create support-cost exposure. Every additional service promise has a cost. Cross-connects require record-keeping, physical work, port management and fault isolation. Remote hands require staff availability, training and process control. Incoming hardware handling requires receiving discipline, storage, chain-of-custody and shipping coordination. Roof space for antennas and radio links may require access management, safety procedures and maintenance coordination. When customers are many and work orders are standard, these services can be efficient.

When a few customers require unusual procedures, they can turn into margin leakage.

The power model is another boundary. Ipcore publishes power options from 1 kVA to 5 kVA for racks and describes redundant power feeds and UPS support. The economics of those options depend on how power is contracted, metered, priced and escalated. A facility can recover energy costs through metered billing, fixed allowance, overage charges or contract escalators. Public sources do not reveal which terms Ipcore uses by customer or how exposed it is to electricity-price volatility. That gap matters because data-centre power is not a minor utility line. It is a core input that can decide whether a customer contract is profitable.

The business therefore depends on a careful balance. Too little flexibility and Ipcore becomes one more small rack seller in Madrid. Too much bespoke support and it becomes a custom operations shop with data-centre capex attached. The best version of the model is standardised enough to protect margin, yet responsive enough to make customers reluctant to leave. Customer dependence is dangerous when that balance tilts toward custom work for a small number of accounts.

Network-resource evidence points to a real but compact footprint

The network evidence supports an operating footprint, but it does not support a claim of broad network dominance. RIPE NCC lists Ipcore Datacenters S.L as a member in Spain, and RIPE REST organisation data identifies ORG-IDS10-RIPE with the company name, country ES, registration number B86088945, LIR type and the Madrid address. RIPEstat's AS overview shows AS198432 as announced and held under the name IPCORE-AS Ipcore Datacenters S.L. RIPEstat's announced-prefix data showed, during research, seven IPv4 /24 prefixes and one IPv6 /32 prefix announced by AS198432.

BGP.tools also describes AS198432 as active and allocated under RIPE, with a small originated-prefix footprint. It lists prefixes including 5.2.88.0/24, 5.2.89.0/24, 5.2.90.0/24, 5.2.91.0/24, 5.2.95.0/24, 185.75.179.0/24, 185.164.184.0/24 and 2a00:e9c0::/32. Several descriptions include Ipcore core, customers or data-centre wording, while one prefix is described in third-party BGP tooling as associated with Copysan Comunicaciones S.L. That should be treated as routing evidence, not as proof of Ipcore's full customer base or economic exposure.

There is also an upstream-evidence caution. RIPEstat WHOIS data for AS198432 shows an aut-num entity created in May 2012 with import policy from AS174 and AS1299 and export policy to those ASNs. BGP.tools, as a live observational source, listed AS49600 NEAR IP, S.L. as an upstream and peer. Those two facts are not necessarily contradictory. RIPE database policy entities can lag, be incomplete or describe permitted routing relationships, while live BGP collectors show observed paths at a point in time. The important conclusion is not that one supplier is definitive.

It is that public data is limited public evidence to reconstruct Ipcore's commercial transit contracts.

PeeringDB adds facility evidence rather than AS customer evidence. It lists IPCore Datacenter Madrid as a facility at Calle Marzo 16 in Madrid, with organisation IPCore Datacenter SL, website ipcore.com, country ES, 17 networks and one local exchange. That is a meaningful interconnection signal. It suggests the facility is known inside a user-maintained interconnection database and that networks are associated with the location. It does not prove traffic volume, rack occupancy, customer revenue or contract quality.

Ipcore's own networking language fits this compact network picture. The company sells cross-connects to carrier PoPs, fibre links to internet exchanges, DCI links and third-party data-centre connectivity. That is a facility-enabled connectivity proposition. It can be attractive to customers that need local Madrid connectivity choice without building their own network presence. But it is not the same as being a large transit network. The public AS and prefix footprint is real, yet small enough that analysts should avoid overclaiming control.

IPv4 scarcity makes the resource evidence more valuable but not decisive. RIPE NCC says its remaining IPv4 pool was exhausted in November 2019 and that LIRs now depend on recovered-address waiting-list rules for small /24 allocations if eligible. For a hosting and colocation operator, stable IPv4 resources can help customers and internal services, but they do not replace reliable power, cooling, support, cross-connect density or customer retention. Internet-number resources are part of the evidence base. They are not the business itself.

Revenue quality depends on renewal leverage, not only filling space

The revenue question is whether Ipcore can convert physical capacity into durable contribution. A full facility is not enough if the revenue is underpriced, excessively bespoke or exposed to unrecovered input costs. In colocation, the best revenue has several qualities: recurring monthly billing, clear power recovery, standardised support charges, renewal escalators, cross-connect fees, low churn and customer diversity. Weak revenue can look similar from the outside, especially when public sources disclose services but not financial terms.

Ipcore's offer creates several potential revenue lines. Rack or partial-rack space is the base. Power can be metered or unmetered within published options. Cross-connects can generate installation and recurring charges. Remote-hands work can be billed by hour, by task, by support plan or bundled into a broader service. Roof and radio-link space may add specialised income. Carrier and meet-me-room services can produce value if carriers need presence and customers need choice. Each line can improve economics if priced correctly; each can erode economics if bundled too generously to win or retain a customer.

The company's public scale indicators point to caution. Empresite's INFORMA-derived page describes Ipcore Datacenters S.L as a limited company in communications, with a 2011 constitution date, activity related to data-centre installation and maintenance, server hosting and technical rooms, a 2024 employee count of seven, and a revenue band between 0.6 million and 1.5 million EUR. Axesor describes the company as a microenterprise, gives a 2024 accounts-deposit reference, and places sales in a lower band.

These are secondary commercial-data sources, not audited analysis for this article, but they align with the operational picture of a compact facility rather than a large campus owner.

That scale does not make the company unattractive. Small colocation facilities can have defensible niches if they serve customers whose needs are too operationally specific for generic cloud and too small for hyperscale procurement. The issue is the shape of demand. A diversified base of SMEs, hosting companies, network operators and specialised infrastructure users may produce stable cash flow. A few large customers may produce similar near-term revenue but less pricing power. The difference would only become visible in renewal negotiations, outage behaviour, arrears, custom-work demands and customer exits.

Customer concentration also affects capex discipline. If a customer asks for more power density, dedicated space, custom cabling, additional cooling or unusual access procedures, the operator must decide whether that investment benefits the whole facility or mainly one account. A broad improvement can raise the facility's long-term value. A customer-specific improvement can create stranded cost if the customer leaves. This is where Elias Ward's lens is blunt: revenue growth is not value creation unless it earns a return on the resources it consumes.

The public record does not show occupancy, booked monthly recurring revenue, average rack price, average power draw, support revenue or collection quality. That absence limits the valuation conclusion. Ipcore has credible services and operating evidence, but public sources do not prove that its revenue is diversified, escalated, high-margin or protected by long contract terms. The correct posture is positive on operating reality and cautious on economic power.

Bespoke support can protect retention and consume margin

Remote support is one of Ipcore's clearest differentiators. The company says it can help remote and out-of-country businesses with incoming hardware deliveries, setup and maintenance of server fleets, 24x7 remote hands, rack mounting, cabling, component switching and return shipping. For a customer outside Spain, that can be the difference between using a Madrid facility and avoiding it. A rack without trustworthy hands is just space. A rack with a responsive local team becomes a managed operating point.

This support layer can create customer stickiness. Once a customer trusts a facility team with urgent swaps, cable tracing, shipment handling and after-hours response, the customer may be less likely to move. Institutional memory accumulates: which cabinet holds which devices, how the customer labels equipment, which contact approves emergency access, which courier routines work, which circuits are critical and which devices have fragile power arrangements. That practical knowledge is hard to reproduce quickly in a new site.

But support also creates a labour-capacity problem. A seven-employee signal in secondary company data, if directionally right, suggests limited organisational slack. Even if staffing differs from the public estimate, the facility is still compact. A small team can deliver high-quality support when workloads are predictable and procedures are standard. It can be strained when customers cluster requests around incidents, migrations, audits, hardware refreshes or carrier outages. The risk is not only wage cost. It is management distraction and service inconsistency.

Bespoke support also changes the bargaining relationship. A customer that relies heavily on Ipcore's team may be sticky, but may also demand preferential treatment. It can argue that its custom workflow deserves bundled support, faster response, reduced charges or dedicated coordination. If the customer is large enough, Ipcore may accept terms that weaken support margins because losing the customer would create a larger revenue hole. That is the customer-dependence trap: the feature that makes the customer sticky can also make the operator dependent.

The cleanest model is to price support transparently. Standard remote-hands tasks can be defined, billed and measured. Non-standard work can require quotes, change windows and customer approval. Emergency support can carry a premium. Shipping and storage can be controlled by written process. The company may already do this; the public site does not disclose the commercial terms. What matters for economic judgment is whether support has become a disciplined service line or an implicit concession inside rack pricing.

For Ipcore, the support question is therefore central to renewal leverage. If customers renew because the facility team is reliable and support is properly charged, support protects margin. If customers renew only after receiving unpriced custom labour, support protects revenue at the expense of value creation. Public evidence cannot distinguish those cases. The fact that Ipcore markets remote hands so clearly means the question should be asked, not ignored.

Supplier pass-throughs are the hidden discipline test

The customer-dependence question cannot be separated from supplier dependence. Ipcore's public offer depends on power, cooling systems, UPS equipment, backup generation, fire protection, security systems, carrier access, upstream internet connectivity, internet exchange reach, cabling materials, rack hardware and technical labour. A data-centre operator can control the customer relationship and still be squeezed by supplier costs if contracts do not let it pass those costs through.

Power is the most visible pass-through risk. Ipcore describes redundant UPS, backup diesel generation, 2N cooling and rack power options. Those features support resilience, but they also consume capital and operating expense. Energy prices, grid charges, generator maintenance, fuel testing, battery replacement and cooling efficiency all affect margins. Customers often resist power-price changes because their own budgets are fixed. If contracts include metered power or clear escalation mechanisms, the operator can protect itself.

If contracts bundle power too generously, high-utilisation customers may become less profitable as energy intensity rises.

Cooling is the next risk. Ipcore states that it uses precision cooling systems from manufacturers such as Emerson and Uniflair, combined with hot-aisle and cold-aisle containment to support efficiency and higher densities. That is credible facility language, but it points to a capital cycle. Cooling equipment ages, spare parts matter, density expectations rise and regulatory scrutiny around energy efficiency increases. A small facility can compete by being practical and efficient, yet it must avoid accepting workloads whose heat and power profile exceed the economics of the room.

Connectivity inputs are also exposed. Ipcore markets 10-plus carrier points of presence, fibre links to internet exchanges, DCI links and cross-connect options. The value to customers is optionality. The cost to the operator is maintaining carrier relationships, meet-me-room discipline, fibre pathways, documentation and troubleshooting coordination. If Ipcore buys upstream internet capacity or relies on network partners for certain routes, it must manage those costs against customer pricing.

Public routing data shows Ipcore has an active AS and observed upstream relationships, but it does not show commercial rates, minimum commits, failover design or supplier concentration.

The Spanish and European context raises the stakes. Spain's telecommunications sector remains competitive, with large fixed and mobile operators holding substantial market shares, and CNMC's 2024 report shows heavy investment in fibre and mobile networks. In data centres, SpainDC, Colliers and Cushman & Wakefield describe strong capacity growth, pressure to deliver power on time, and expanding AI and cloud demand. EU rules are also increasing transparency and sustainability expectations for data centres above key thresholds. Those forces make supplier management more important, not less.

The discipline test is straightforward. When power, cooling, network, labour or compliance costs rise, can Ipcore pass them through without losing customers? If the customer base is diversified and values the facility's operating continuity, the answer may be yes. If a few customers determine utilisation or a channel controls demand, pass-throughs become harder. The company may then absorb costs to protect occupancy, weakening the economics that justify future investment.

Customer concentration is the central uncertainty, not a public fact

There is no public evidence that Ipcore is dangerously concentrated. There is also no public evidence that it is safely diversified. That is the analytical centre of the article. Customer dependence must be treated as an uncertainty with clear economic consequences, not as a rumour or an accusation.

Small data-centre facilities can develop concentration in several ways. One managed-service provider can take many racks and resell services to end customers. One enterprise can lease a dedicated cage or room. One carrier can become the preferred route to customers. One channel partner can originate most new demand. One hosting customer can use a large share of remote-hands time. One international customer can need unusual support and shipping procedures. None of these patterns is inherently bad. They become risky when the operator invests around them without contract protection.

The customer-side leverage is easy to understand. A large customer can threaten to move future deployments to a larger Madrid provider. It can ask for price freezes in exchange for renewal. It can demand support credits after incidents. It can insist that power increases be delayed. It can request custom access or security procedures. It can turn a standard service into a bespoke operating arrangement. If that customer represents a large share of revenue, the operator's negotiating position weakens even if the service is technically good.

Channel dependence can be subtler. A reseller or integrator may bring customers to the facility, but it may also own the commercial relationship. The facility then becomes partly dependent on the channel's sales pace, pricing expectations and customer-retention behaviour. If the channel shifts demand to another site, the facility may lose customers it never directly controlled. Ipcore's public materials do not show whether it sells mostly direct, through partners, through carriers or through managed-service intermediaries. That absence should be a standard diligence item.

Contract duration matters as much as customer count. A facility with a few large customers on long contracts with escalators and clear power pass-throughs may be healthier than a facility with many monthly customers that churn or bargain constantly. Conversely, a facility with long contracts at underpriced rates can trap the operator in weak economics. Public pages do not disclose initial terms, renewal rights, service-level credits, support pricing, power escalators or early termination provisions.

The right conclusion is that concentration risk is asymmetric. If Ipcore is diversified, the public evidence of facility, connectivity and support can support a solid local niche thesis. If it is concentrated, the same evidence becomes a warning: the company may be operationally real but economically exposed to a few renewal decisions. Because public sources do not resolve the matter, the investment judgment should stay conditional.

Madrid gives alternative buyers but also stronger substitutes

Madrid is helpful and dangerous for Ipcore. It is helpful because the region has growing demand for colocation, cloud connectivity, enterprise outsourcing and AI-adjacent infrastructure. A customer that wants Madrid presence has reasons to prefer local capacity, carrier choice and access to Iberian traffic flows. Madrid also has a rich interconnection environment. DE-CIX Madrid describes itself as part of the largest neutral interconnection ecosystem in Southern Europe, connecting to more than 200 local networks and to other DE-CIX hubs.

Internet Society Pulse lists 12 active IXPs in Spain as of July 2026 and identifies DE-CIX Madrid and Espanix LANs among the Madrid exchange points.

That ecosystem creates alternative buyers. A facility with carrier-neutral access can appeal to hosting providers, cloud-adjacent service firms, content platforms, network operators, SMEs with latency-sensitive workloads, backup-location customers, equipment vendors, security firms and international companies needing a Madrid node. If one customer leaves, a healthy market should offer replacements. This is the positive side of being in Madrid rather than an isolated market.

The same ecosystem creates substitutes. Baxtel's Madrid facility map places Ipcore among many nearby facilities, including sites associated with Global Switch, Digital Realty, Equinix, OASIX, NxN, Prime, CyrusOne, Cogent, Templus, Nabiax, ADAM, Data4, NTT and others across the broader metro area. Cushman & Wakefield describes Madrid as Spain's main data-centre hub, with substantial capacity in operation, construction and planning, and notes land and energy constraints pushing investors to areas around the city.

In its Iberian snapshot, Colliers reports 175 MW IT operational in Madrid and more than 1,400 MW IT planned or under development.

For Ipcore, substitutes affect pricing. If the customer needs only a commodity rack, the facility competes against larger platforms with scale, brand, certifications, cloud on-ramps, procurement teams and newer high-density designs. If the customer needs responsive remote hands, a specific Madrid location, carrier diversity, existing cross-connects or practical access to the Ipcore ecosystem, the substitute set narrows. The more specific the operating need, the stronger Ipcore's renewal leverage.

The AI data-centre boom complicates the picture. Large developments may focus on hyperscale and high-density AI loads that are not natural substitutes for a 1 kVA to 5 kVA rack customer. In that case, new capacity does not directly destroy Ipcore's niche. But the boom can still change expectations. Customers may ask about liquid cooling, higher densities, sustainability metrics, power availability and cloud connectivity. Even if Ipcore is not chasing AI campuses, it must operate in a market whose benchmark is moving.

The best strategic position is therefore not to imitate hyperscale. It is to own the compact Madrid colocation niche: reliable racks, carrier choice, practical support, disciplined power terms and customers whose switching cost is operationally real. The worst position is to discount against larger facilities while accepting support obligations and power risk that those larger facilities price more rigorously.

Regulation and energy scrutiny move from background cost to board-level constraint

Data-centre regulation is shifting from technical paperwork to economic pressure. The European Commission says the Energy Efficiency Directive introduced monitoring and reporting obligations for the energy performance of data centres and that a European database collects and publishes energy-performance and water-footprint data for facilities with significant consumption.

Commission materials on minimum performance standards state that the recast directive introduced mandatory public reporting for data centres with power demand above 500 kW, followed by Delegated Regulation EU 2024/1364 on harmonised reporting elements and the first phase of a Union rating scheme.

Whether a specific Ipcore facility crosses each regulatory threshold is not established in the public sources reviewed here. The company's site says it offers rack power options from 1 kVA to 5 kVA and says its UPS systems can scale up to 200 kW per frame, but those claims do not disclose installed IT load, contracted load or reporting status. The point is broader: as EU transparency rules and market expectations become stricter, energy performance, PUE, water use, renewable-energy sourcing, heat reuse and reporting discipline become more visible in buyer decisions.

That shift can help disciplined operators. If Ipcore's ISO 50001 energy-management claim is current and operationally meaningful, it can support conversations with customers that care about energy discipline. Efficient hot-aisle and cold-aisle containment can lower operating cost and improve resilience. A small facility that knows its loads well may manage energy more carefully than a speculative project chasing scale.

The shift can also raise cost. Reporting, measurement, documentation, audits, metering, supplier data, energy procurement and compliance work require attention. Larger operators can spread these functions across many facilities. A smaller operator may have to absorb them inside a lean team or buy external help. If customers are price-sensitive and contracts do not allow compliance-cost recovery, regulatory tightening becomes another margin squeeze.

Spain's grid context adds a further constraint. SpainDC and market reports highlight access to power-grid capacity as one of the key challenges for data-centre growth. Colliers says investor attention is shifting toward the ability to execute and deliver power on time, particularly in energy-constrained hubs. This is not only a problem for new hyperscale campuses. Existing smaller facilities also need reliable power contracts, maintenance discipline and a clear answer for customers asking whether the site can support future density.

Operational risk remains basic but unforgiving. A colocation customer judges the facility by outages, response times, power quality, cooling stability, security, access control, cabling discipline and communications during incidents. One bad incident can reshape renewal leverage. A few customers can absorb management attention during a crisis. The economic answer is not only technical redundancy. It is process, transparency and contract design that prevent one incident from turning into a permanent price concession.

Unofficial signals confirm presence but do not prove economic power

Third-party signals are useful here because they triangulate operating reality. Data Center Map describes IPCore Datacenters S.L as a Madrid colocation provider and repeats the 1,200-square-metre and 500-cabinet language. DataCenterPlatform lists IPCore Datacenter SL Spain with one data centre, colocation category, Calle Marzo 16 address and [email protected]. Baxtel lists IPCore Madrid as operational, at Calle Marzo, operated by IPCore Datacenter SL, with one facility in one market. Datacenters.com describes the IPCore Madrid Data Center as a carrier-neutral facility near Autovia A-2 and Madrid Airport, with 1,200 square metres and redundant infrastructure.

These sources should not be overused. They may repeat company-provided content, and their commercial profiles are not audited facility reports. They do not prove occupancy, power availability, revenue, customer quality or profitability. Their value is narrower: they show that Ipcore's facility appears in the market's data-centre reference layer, not only on the company website. That supports the reality of the operating subject.

Business-data pages also need careful handling. Empresite and Axesor provide Spanish commercial registry and company-data extracts that identify Ipcore's tax number, legal form, Madrid address, activity description and small scale. Empresite gives a 2024 employee count of seven and a revenue band between 0.6 million and 1.5 million EUR. Axesor describes the company as a microenterprise and gives a sales band between 250,001 and 750,000 EUR. These two revenue bands do not perfectly match. That discrepancy is a reason to treat them as directional signals, not as final financial statements.

The unofficial market signals point in one direction: Ipcore is visible, real and small. That combination can be attractive if the company has a loyal customer base and disciplined contracts. It can be vulnerable if market growth tempts it to chase larger customers without the balance sheet, staffing or contract protection to absorb custom demands. The public record does not identify major public-sector tenders, large named customers, sanctions issues or clear credit distress in the sources reviewed. It also does not provide enough financial detail to dismiss those questions.

The right use of unofficial signals is therefore to frame diligence. The facility appears to exist and operate. The company appears legally registered and commercially active. The network footprint is visible and compact. The data-centre market around Madrid is expanding. The unanswered question is whether these facts add up to pricing power or merely to participation in a competitive market.

What would change the judgment

The judgment would improve with evidence that customer dependence is low and contract discipline is high. The most important facts would be customer count, top-five and top-ten revenue share, occupancy by cabinet and power, average contract duration, renewal rates, churn, expansion bookings, support revenue, remote-hands utilisation, cross-connect counts, power metering arrangements, pass-through clauses and bad-debt history. A diversified base of customers on contracts with clear escalators would make Ipcore's compact size look like focus rather than fragility.

The judgment would also improve with proof of controlled supplier exposure. Useful evidence would include electricity procurement terms, backup-generator maintenance records, UPS and battery refresh schedules, cooling capacity, PUE history, carrier and upstream diversity, IXP access terms, insurance coverage, incident history, ISO certificate status and compliance reporting. If Ipcore can show that power, cooling and carrier costs are either hedged, passed through or priced into customer contracts, the margin risk falls materially.

The judgment would worsen if a few customers or channels determine most demand without strong contract protection. It would worsen if remote hands are heavily bundled into rack pricing, if power is under-recovered, if a major customer has below-market renewal rights, if staffing is too thin for the support promise, if network diversity is weaker than marketing language suggests, or if facility upgrades are required for customers that have not committed capital or term. It would also worsen if Madrid's larger operators begin competing directly for the same low-density, support-heavy customers at prices Ipcore cannot match.

For now, Ipcore is best understood as a credible Madrid colocation and connectivity specialist with a real facility and a compact network-resource footprint. The company sits in a market with strong demand signals, but demand does not automatically equal value creation. The economic case depends on whether Ipcore can turn facility convenience, carrier neutrality and remote support into renewal leverage while preventing a small number of customers, channels or suppliers from setting the terms of the business.