The payment that notices the sea

A bank in Athens does not buy a Mediterranean backbone because a marketing page says it is strategic. It buys continuity because a card authorisation cannot be allowed to become a geography lesson. A content platform does not wake up thinking about Koropi, Metamorfosis or Chania. It notices those places when a live stream buffers in the eastern Mediterranean, when a cloud region is close enough but not quite close enough, when a submarine fault sends packets on a longer path, or when a procurement team asks why the second route is really independent from the first. In those moments, TI Sparkle Greece becomes visible. Its product is not simply a rack, a port or a circuit. Its product is the reduced chance that a customer must explain to its own users why the sea has just entered the service experience.

That is the right way to approach the company. TI Sparkle Greece is not a mass-market consumer telecom brand trying to win households with a cheaper mobile bundle. It is a wholesale and enterprise infrastructure business inside the Sparkle group, selling connectivity, colocation, backbone reach and digital services to customers whose own products depend on quiet availability. Sparkle's Greece page says TI Sparkle Greece S.A. is part of Sparkle Group and works through a global backbone of more than 600,000 kilometres; it also says Sparkle's Mediterranean submarine network runs roughly 11,000 kilometres linking Italy, Greece, Cyprus, Turkey and Israel, with privately owned data centres in Catania, Athens, Chania and Istanbul (https://www.tisparkle.com/greece). That is not a decorative claim. It describes a company whose economics sit between local real estate, power, exchange presence, submarine routes and contracts with buyers large enough to know exactly what an avoidable millisecond is worth.

The company is also a useful test of a larger Mediterranean thesis. Cloud computing, AI workloads, streaming, financial software and government digitisation all create more demand for data to sit near users while remaining connected to larger European, Middle Eastern and Asian systems. Greece benefits from that geography, but geography is not a business model by itself. The money is earned by turning geography into dependable optionality: landing points that are physically diverse, data centres that can hold customers' equipment, interconnection points that reduce domestic detours, and parent-company balance sheets that can keep funding equipment before demand is fully proved. TI Sparkle Greece is interesting because it has a real version of those pieces, while still facing the harder wholesale problem that the biggest buyers are both customers and price-setters.

The starting scene, then, is not a corporate lobby. It is an outage bridge. A bank's technology team sees transaction latency rise. A streaming operator sees regional delivery quality deteriorate. A cloud integrator sees an enterprise customer ask whether data can stay in Greece without losing access to global services. Nobody in that meeting cares whether the route is elegant. They care whether there is another route, whether the second route shares the same vulnerable landing, whether the carrier can prove what happened, and whether the price of that proof is less than the business cost of failure. TI Sparkle Greece's commercial job is to be paid for this invisible assurance before the bad day arrives.

A Greek company inside an Italian global carrier

The identity evidence is unusually clear. Sparkle's own Greece page names TI Sparkle Greece S.A., gives an Athens office at Ermou 39 in Metamorfosis, and says the local company manages and operates the whole infrastructure within Greece: the backbone and four data centres at Metamorfosis, Metamorfosis II, Koropi and Chania (https://www.tisparkle.com/greece). TIM's 2025 annual report lists TI Sparkle Greece S.A. in Athens, Greece, as a telecommunications company with share capital of EUR 368,760 and 100 percent participation by Telecom Italia Sparkle S.p.A. (https://www.gruppotim.it/content/dam/gt/investitori/doc---report-finanziari/2025/Annual%20report%202025.pdf). A Legal Entity Identifier record for 213800GZ2W1ZI8VNEO07 names TI Sparkle Greece MAE, marks the entity active, records validation against the Greek General Commercial Registry, and gives creation on 29 March 2001 (https://www.lei-lookup.com/record/213800GZ2W1ZI8VNEO07/).

Those facts matter because wholesale telecom is full of brand layers. A customer may buy a circuit from one sales office, peer with another autonomous system, place equipment in a data centre operated by a local subsidiary, and rely on a submarine cable marketed under a project name. The legal and operating chain has to be intelligible. Here the chain is not perfect in every public detail, but it is good enough to anchor the research judgement: TI Sparkle Greece is the Greek subsidiary of Sparkle, itself the international wholesale infrastructure arm that TIM has been trying to sell, and the Greek company has been present long enough to be more than a temporary sales branch.

Sparkle itself presents a larger wholesale platform. Its April 2025 corporate presentation says the company had more than 1,600 customers, 136 Tbps of data traffic and EUR 1 billion of revenues as of December 2024; it also describes more than 600,000 kilometres of fibre, 181 proprietary points of presence, more than 1,000 partner points of presence, two global network operations centres and one security operations centre (https://www.tisparkle.com/sites/en/files/2025-04/Sparkle%20Corporate%20Presentation%20April%202025_0.pdf). Those are group figures, not Greek subsidiary revenue. They should not be read as TI Sparkle Greece's standalone scale. They do show the parent's economic universe: carriers, ISPs, content providers, media platforms, multinational enterprises and mobile operators buying reach, capacity, IP transit, cloud connectivity and operational response.

The Greek unit's advantage is that it sits where the group narrative meets concrete geography. Sparkle says the Aegean network has three landing points, Aghia Marina, Vravrona and Chania, and two landing stations at Koropi and Chania, with a ring configuration and guaranteed availability of 99.99 percent; it also says the Koropi landing station is connected with the Metamorfosis data centre through a double-routing fibre connection (https://www.tisparkle.com/greece). The language is technical, but the economic meaning is simple. If a carrier wants to sell Greece as a resilient Mediterranean access point, it must make the landing station, metro fibre, data centre and international backbone behave like one service.

That is expensive. It is also why the business is defensible when executed well. A reseller can buy capacity and sell a port. A local facility operator can lease rack space. A large cloud platform can bring immense demand and bargaining power. TI Sparkle Greece's position is strongest where those roles overlap: a buyer wants local Greek infrastructure, international routes, cloud access, interconnection and operational responsibility from one group that can speak both the local and global language of backbone reliability.

The Aegean network as an insurance policy

The Aegean network is the heart of the company's wholesale story. Sparkle says it is part of the wider Mediterranean submarine network and that it links landing points and data centres in a protected ring (https://www.tisparkle.com/greece). A ring is not magic. It is a design choice that gives operators another direction to send traffic when a link, landing segment, equipment path or metro route fails. The customer does not pay for geometry; the customer pays for the possibility that a single incident does not become a public apology.

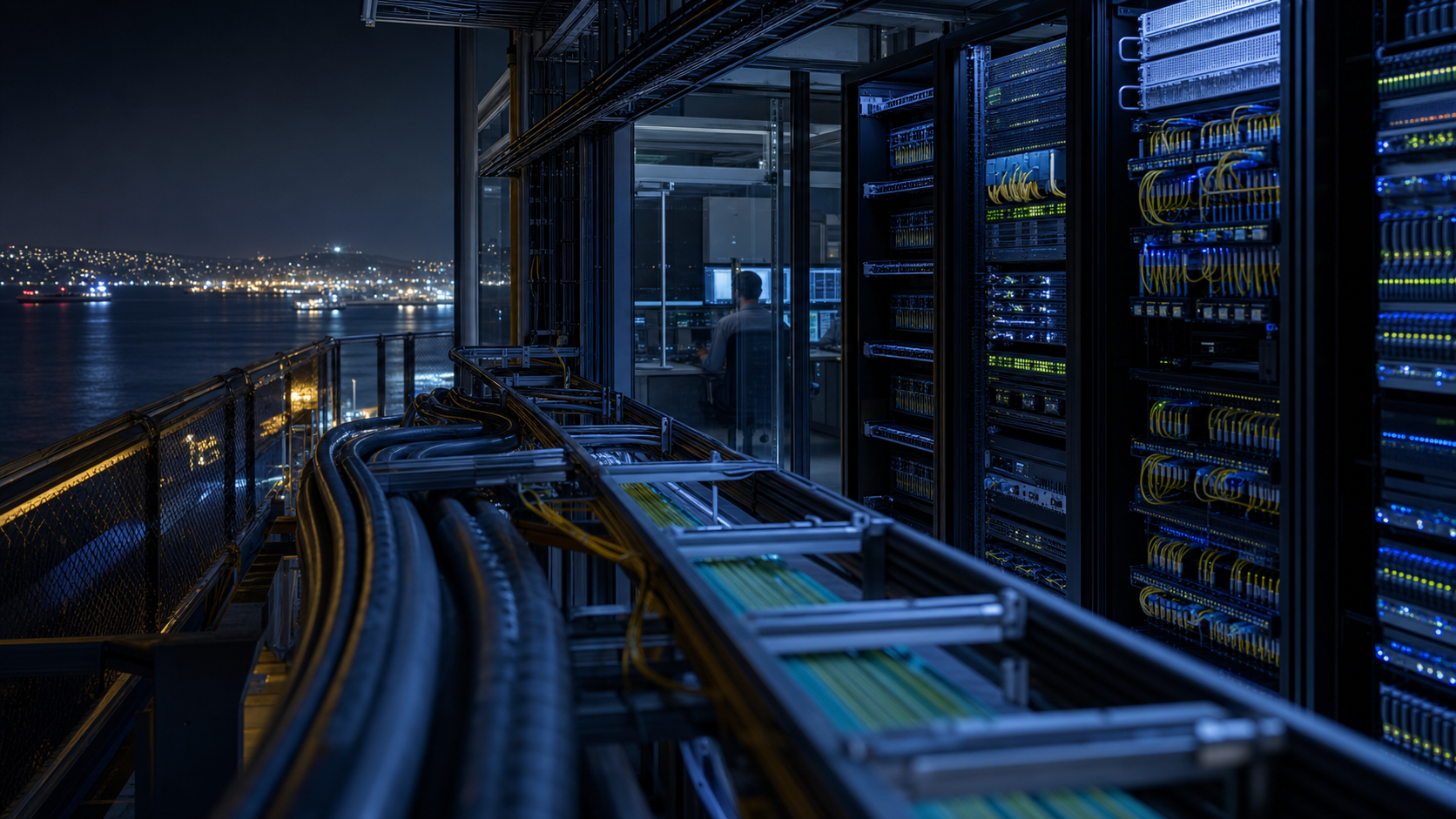

Sparkle's 2021 Metamorfosis II announcement makes the Greek asset base more concrete. It says Sparkle then operated four open data centres in Greece, three in Athens and one in Chania, for a total area of 14,000 square metres and 13.7 MW of power; it also says those facilities were integrated with Nibble, Sparkle's pan-Mediterranean optical network, and Seabone, Sparkle's Tier-1 global backbone (https://www.tisparkle.com/sparkle-launches-data-center-metamorfosis-II). Metamorfosis II itself was described as about 6,000 square metres, with up to 700 racks and 7.7 MW of power, built to anti-seismic criteria and designed for high reliability and security. The facility was also presented as energy efficient, with Tier III, LEED Gold and ISO 14001 certification.

Sparkle's current Greece data-centre page adds a service list: colocation, connectivity, networking, cloud solutions, disaster recovery, capacity, PCI-DSS, ISO 9001, ISO/IEC 27001, ISO 14001 and ISO 20000. It also says the sites provide 1 Mbps to 100 Gbps connectivity in a carrier-neutral environment, 24/7 support in Greek and English, 2N back-up throughout each building, direct access to major cloud providers, and internet service by Sparkle Greece's own local internet registry AS number directly connected to GR-IX (https://www.tisparkle.com/our-platform/backbone-infrastructure-platform/data-center-solutions/sparkle-greece-data-center). That page is marketing, but it is marketing with operational content. It tells us what Sparkle believes customers buy in Greece: not merely a building, but power, managed support, routing, exchange reach and access to cloud platforms.

The facility footprint changes the nature of the revenue. Wholesale capacity can be volatile; prices fall over time as equipment improves and alternative routes appear. Colocation and data-centre services have different stickiness. Once a bank, carrier, media platform or enterprise places equipment in a facility, the cost of moving includes procurement, migration risk, cabling, audits, security review, remote-hands habit and the risk of disturbing a service that already works. That does not make the customer captive. Sophisticated buyers deliberately avoid captivity. But it does mean a well-connected data centre can become an operating base around which customers buy additional ports, cross-connects, dark fibre, cloud connectivity and disaster-recovery capacity.

This is why the word "invisible" matters. A large buyer may not care about the brand as a public symbol. It cares that the Athens facility has power, the Chania site has landing relevance, the Koropi connection adds route diversity, and the carrier can prove that the service is not two labels on the same physical risk. A finance customer may ask for evidence that a disaster-recovery design does not fail when Attica has a power or fibre incident. A content platform may ask for enough peering and transit diversity to avoid hauling Greek traffic too far before it reaches users. An international carrier may need an Aegean handoff that does not depend on a single congested path north or west.

The price of that assurance is not only capex. It is spare capacity that may sit idle until a failure, maintenance shift or traffic surge makes it valuable. The economic temptation in telecom is to sweat assets to maximise utilisation. The resilience product requires the opposite in selected places. It requires margin to carry underused ports, protected fibre paths, monitoring staff, maintenance windows, emergency spares, audited procedures and contracts with enough clarity that a customer knows who answers at three in the morning. TI Sparkle Greece's opportunity is to make buyers pay for that spare readiness. Its risk is that the biggest buyers demand the readiness while forcing the price toward commodity bandwidth.

Chania and the new routes around old bottlenecks

The most important recent strategic evidence is BlueMed. In May 2024 Sparkle announced the landing of the BlueMed submarine cable in Chania, Crete, saying it strengthened Greece's position as a digital hub for traffic between Europe, Africa, the Middle East and Asia (https://www.tisparkle.com/media/press-release/sparkle-brings-bluemed-cable-crete-and-opens-new-digital-route). The same announcement says BlueMed connects Italy with France, Greece and other Mediterranean countries, is part of the wider Blue and Raman systems built with Google and other operators, and has four fibre pairs with initial design capacity of more than 25 Tbps per pair. From Palermo, the cable crossed the Strait of Messina to Crete, with onward Mediterranean branches planned toward Aqaba in Jordan; in Crete it reaches Sparkle's Chania data centre, a landing station connected to island terrestrial networks and Sparkle's MedNautilus network.

That single announcement ties the company's Greek economics to the modern politics of routes. For years, the basic problem of Europe-Asia internet connectivity has been that the shortest route is not necessarily the least risky route. Cable systems, landing permits, terrestrial crossings, conflict risk, repair delays and concentration around chokepoints all influence a packet's path. A buyer with enough traffic does not want a beautiful route; it wants a route portfolio. BlueMed's commercial promise is not just more capacity. It is another way to enter and leave the Mediterranean, another way to connect Greece into a wider Europe-Middle East-Asia design, and another bargaining chip for buyers that ask carriers to prove diversity.

The fact that Google is named as part of the wider Blue and Raman project changes the economics. Hyperscalers and large content platforms do not merely consume wholesale telecom products. They reshape them. They bring enormous volume, sophisticated engineering teams and the ability to finance or co-finance new capacity. They also pressure carriers by comparing every route against self-build, consortium participation, cloud on-ramps, private network arrangements and rival wholesale providers. A carrier such as Sparkle needs hyperscaler demand because it fills large systems and justifies investment. But that demand is not passive. It arrives with procurement leverage.

This is why Chania matters more than its size alone. A Chania landing point that links BlueMed, MedNautilus and terrestrial Greek networks gives Sparkle Greece a story that a pure Athens data-centre operator cannot easily copy. It also gives customers a way to think about Greece as more than an end market. Greece becomes a switching surface: a place to land, host, cross-connect, route west, route east, serve the domestic market and support regional recovery. The value is highest where customers believe the route is operationally real rather than a line on a map.

The watchpoint is timing and utilisation. A cable can be landed before it is fully commercial across every intended segment. Capacity can exist before customers commit. An announced route can improve a seller's strategic position without immediately improving reported revenue. Sparkle's 2024 release said further Mediterranean landings and full operation from Genoa to Aqaba were expected by that year; the public evidence reviewed here is enough to establish the Chania landing and the route ambition, but not enough to price the actual sold capacity by segment. That distinction matters. Telecom infrastructure often looks most valuable in presentations just before utilisation, pricing and maintenance reality arrive.

What public routing records add

The routing records add a harder edge to the company picture. PeeringDB's public record for AS198477 names "TI Sparkle Greece", gives the organisation as TI Sparkle Greece S.A., website https://www.tisparkle.com/greece, network type Cable/DSL/ISP, regional scope, open peering policy, traffic level of 1-5 Gbps and a mostly outbound traffic ratio (https://www.peeringdb.com/net/8240). It also lists an operational 10G presence at GR-IX Athens with IPv4 176.126.38.14 and IPv6 2001:7f8:6e::14. PeeringDB's facility record for TI Sparkle Greece (IDC) in Metamorfosi lists 36 networks and five local exchanges, including GR-IX Athens, Free-IX Greece, NetIX, NetIX Greece and NVL-IX, plus carriers such as EXA Infrastructure, Grid Telecom and NetIX (https://www.peeringdb.com/fac/2951).

RIPEstat's overview for AS198477 reports the holder as TISGR-NET TI SPARKLE GREECE SA and marks the AS as announced; its announced-prefixes view showed 16 prefixes in the 19 June to 3 July 2026 observation window (https://stat.ripe.net/data/as-overview/data.json?resource=AS198477 and https://stat.ripe.net/data/announced-prefixes/data.json?resource=AS198477). The RIPE whois record identifies AS198477 as TISGR-NET, includes import and export routing policy entries, refers to Seabone AS6762 as an upstream and lists GR-IX peerings and customer announcements (https://stat.ripe.net/data/whois/data.json?resource=AS198477). These are not sales contracts. They are public signals that the Greek unit has a visible routing surface, peers at a domestic exchange and is linked into the Sparkle global network.

That evidence should lower one risk and raise another. It lowers the risk that TI Sparkle Greece is merely a name attached to a building with no visible network role. It raises the question of scale. A PeeringDB traffic range of 1-5 Gbps for AS198477 is modest compared with the group claims around Seabone and global data traffic. The right interpretation is not that the Greek business is small or unimportant. The right interpretation is that the local AS record captures only part of the Greek operating surface. Sparkle Greece's value likely lies in a combination of local internet service, data-centre interconnection, group backbone access, submarine infrastructure and private customer arrangements that are not fully visible in public BGP data.

That combination is typical of wholesale telecom economics. The public internet sees enough to confirm that a route exists. It does not see the whole commercial stack. A bank's private connectivity, a carrier's wavelength, a cloud direct connection, a disaster-recovery link or a dark-fibre arrangement may matter more financially than visible public peering traffic. The visible records still matter because they show whether a company can participate in the interconnection commons. TI Sparkle Greece can. It is at GR-IX, its Metamorfosi site is an exchange and network aggregation point, and its routing policy connects it back to Seabone.

The route evidence also shapes the customer-dependency surface. A domestic Greek ISP may use TI Sparkle Greece for upstream or co-location. A foreign carrier may use it for access to Greece and the eastern Mediterranean. A cloud customer may use Sparkle's data centre for proximity, redundancy or a cross-connect to a public cloud service. A content platform may value the ability to hand off traffic closer to Greek users or to buy a Mediterranean path with operational support in the same commercial family. Each customer type has different price elasticity. The largest content and cloud buyers can demand lower unit costs. Smaller enterprises may pay for service, support and trust. The carrier's margin depends on mixing those customers without allowing the most powerful buyers to set the price for everyone.

Data-centre economics beneath the backbone story

The backbone story can make the company sound weightless, as if traffic simply moves across maps. The economics are physical. Data centres require land, power, cooling, security, diesel or other back-up arrangements, environmental control, network rooms, cabling discipline, certification work, fire suppression, guards and technicians. Sparkle's Greece data-centre page lists 99.999 percent power availability, 99.99 percent cooling availability, 24/7 on-site security, camera monitoring, automatic fire detection and gas-based extinguishing, 2N back-up throughout each building and 24/7 support (https://www.tisparkle.com/our-platform/backbone-infrastructure-platform/data-center-solutions/sparkle-greece-data-center). Those features are not free. They are the cost base that makes a carrier's resilience claims credible.

Metamorfosis II is a useful example. The 2021 launch figure of 7.7 MW of total power and 700 racks is large enough to matter in the Greek market, but not large enough to play the same game as the biggest global hyperscale campuses (https://www.tisparkle.com/sparkle-launches-data-center-metamorfosis-II). That middle scale can be attractive. It is big enough to host serious enterprise, carrier and cloud-adjacent workloads; it is small enough that the site has to win by connectivity, certification, support and location rather than brute force power scale. In a market where AWS, Microsoft and Google all influence buyer expectations, a carrier-owned data centre cannot assume that all cloud demand becomes local colocation demand. It must position itself where cloud and network needs meet.

AWS's June 2026 announcement of an Athens Local Zone illustrates the demand trend without proving any Sparkle relationship. AWS said the Athens Local Zone would be generally available in July 2026, would place compute, storage, networking, analytics, AI, machine learning and databases in or near Athens, and would deliver single-digit millisecond latency for Greek end users through a high-bandwidth connection to nearby AWS regions (https://press.aboutamazon.com/aws-international/2026/6/aws-brings-compute-storage-and-ai-services-to-athens-with-new-local-zone-available-july-2026). It also named financial institutions, healthcare providers and government agencies as examples of customers with local speed, data-residency and regulatory needs. The announcement is not about TI Sparkle Greece. It is about the kind of demand environment in which TI Sparkle Greece must compete and sell.

For Sparkle Greece, local cloud infrastructure is both friend and threat. It is a friend because every cloud node, local zone, direct-connect site and content cache increases the need for local routes, back-up paths, cross-connects and enterprise migration advice. It is a threat because hyperscalers can internalise more of the network and force partners to accept sharper pricing. The biggest cloud platforms buy telecom inputs the way airlines buy fuel: constantly, professionally and with little sentiment. They need carriers, but they do not want to be dependent on any single carrier's story. TI Sparkle Greece's defensible position therefore depends on specific assets that a cloud platform cannot instantly replicate: Aegean landing geography, existing data-centre relationships, Greek operational staff, cable-system participation and the broader Seabone/Sparkle contract surface.

The bank or content-platform scene returns here. A Greek bank deciding where to host disaster recovery will not buy a service merely because a carrier is old. It will ask whether the site is certified, whether the connectivity options are diverse, whether remote hands are competent, whether auditors understand the facility, whether the price is explainable and whether there is a path to cloud services. A streaming platform will ask where caches sit, how traffic leaves Greece, whether peak events can be absorbed, and whether a reroute turns a football match into a complaint storm. A carrier will ask about cross-connect fees, port options, optical handoffs, repair terms and route separation. Each question converts infrastructure into contract language. That conversion is where margin is won or lost.

The parent-company balance-sheet question

No account of TI Sparkle Greece is complete without the parent. TIM has been reshaping its balance sheet and corporate perimeter, and Sparkle is a major part of that story. In April 2025 TIM said it had signed an agreement with Boost BidCo, a vehicle controlled by Italy's Ministry of Economy and Finance and participated in by Retelit, for the disposal of Sparkle; the agreement set Sparkle's enterprise value at EUR 700 million, with the disposal price adjusted for net debt and working capital at closing and a possible adjustment if certain 2025 EBITDA targets were not met (https://www.gruppotim.it/en/press-archive/corporate/2025/PR-TIM-Sale-of-Sparkle.html). On 14 April 2026 TIM announced that the parties had extended the long-stop date for closing to 15 October 2026, while still saying the transaction was expected to be finalised in the second quarter of 2026 (https://www.gruppotim.it/en/press-archive/sparkle/2026/PR-TIM-Waiver-Sparkle.html).

The financial disclosures show why this matters. TIM's March 2026 financial statement release says Telecom Italia Sparkle was classified under IFRS 5 as an asset held for sale and that Sparkle is active in developing fibre-optic networks for international wholesale customers (https://www.gruppotim.it/en/press-archive/corporate/2026/PR-BoD-11-March-2026.html). The same release reports TIM Group revenues of EUR 13.734 billion for 2025 under the Sparkle-discontinued-operations perimeter, net profit of EUR 519 million, and a negative EUR 76 million result related to discontinued operations/non-current assets held for sale, mainly from the Telecom Italia Sparkle group. It also says a later adjustment of the Sparkle stake to presumed realisation price contributed EUR -115 million within the result related to held-for-sale assets.

For TI Sparkle Greece, this is not accounting trivia. A wholesale infrastructure company sells long-term confidence. Customers buying route diversity, colocation or disaster recovery care about ownership stability, investment capacity, maintenance discipline and management continuity. A sale to a state-backed and infrastructure-backed buyer could strengthen Sparkle's strategic position if it brings patient capital and political support for critical routes. It could also create temporary uncertainty if customers wait to see how governance, service agreements, capital allocation and integration with Retelit evolve.

The April 2025 TIM agreement also said that, at closing, TIM and Sparkle would sign a contract regulating reciprocal services after the transaction (https://www.gruppotim.it/en/press-archive/corporate/2025/PR-TIM-Sale-of-Sparkle.html). That detail is important. Sparkle's value has partly come from being embedded in a larger Italian telecom group. If ownership changes, customers will want to know whether operational dependencies remain smooth. Does Sparkle keep the same backbone priorities? Does procurement speed improve or slow? Does the new owner invest more aggressively in Mediterranean route diversity? Does TIM remain a major customer or partner under clear service terms? These questions are not visible in TI Sparkle Greece's local pages, but they influence the credibility of any long-term Greek infrastructure sale.

The financial discipline can cut both ways. A parent under pressure may require higher returns from assets, limiting speculative builds. That can protect margin. It can also cause underinvestment in a market where routes and data-centre capacity need to be ready before customer demand fully arrives. A new owner may have a stronger strategic mandate to treat Sparkle as sovereign infrastructure. That can support cable and landing investments whose private payback is long. It can also expose the company to political priorities that are not always the same as customer priorities. For Greek buyers, the best outcome is boring: enough capital, enough operational continuity and no disruption to service accountability.

Wholesale contracts and the bargaining power of giants

The article's central economic question is whether TI Sparkle Greece can earn a premium for resilience when the largest buyers are trained to erode premiums. Sparkle's customer categories include carriers, ISPs, OTTs, media and content players, application service providers and corporate customers (https://www.tisparkle.com/greece). Its corporate presentation says Sparkle sells infrastructure and global connectivity to international and national carriers, OTTs, ISPs, media and content providers and multinational enterprises (https://www.tisparkle.com/sites/en/files/2025-04/Sparkle%20Corporate%20Presentation%20April%202025_0.pdf). Those customer types do not behave alike.

Large carriers may buy capacity as one input in a global route book. Their loyalty is limited by performance, price and available alternatives. Content platforms and CDNs bring volume but expect interconnection efficiency. Hyperscalers and cloud buyers can demand direct access, low latency, compliance language and price transparency while also building their own networks. Enterprises and banks may pay more for assurance, but they often buy through integrators and procurement departments that compare services line by line. Government and institutional buyers may prize local resilience, yet tenders can compress margins unless the technical requirements are well specified.

This is why wholesale telecom companies like layered products. A raw wavelength or IP transit commit is vulnerable to price decline. A bundled offer that includes colocation, protected fibre, managed connectivity, security features, cloud access, disaster recovery, service reporting and trusted local support is harder to compare. Sparkle's Greece data-centre page makes this layering explicit: colocation; IP transit from Tier 1 and Tier 2 providers; MPLS, SD-WAN and Ethernet up to 100 Gbps; dark fibre; GR-IX access; direct access to Sparkle cloud solutions and major cloud providers including AWS, Microsoft Azure and Google (https://www.tisparkle.com/our-platform/backbone-infrastructure-platform/data-center-solutions/sparkle-greece-data-center). The buyer may think it is buying latency. Sparkle wants it to buy an operating environment.

But buyers are not naïve. A platform with a content-delivery footprint will ask whether paying Sparkle for premium routing materially improves user experience compared with buying from another carrier, caching locally, or shifting more traffic through its own backbone. A bank will ask whether a disaster-recovery contract is worth the premium compared with using a hyperscaler local zone, a rival data centre, or a dual-provider architecture. A carrier will ask whether the route through Chania is truly independent from other Mediterranean risks and whether volume discounts justify concentrating spend. If the answer is only "we are strategic", the price will fall. If the answer is demonstrated performance, physically diverse paths and audited operational response, the premium has a chance.

Grid Telecom's 2021 collaboration announcement provides a partner-side market signal. It described TI Sparkle Greece as operating in Greece since 2001, then serving through three proprietary data centres with 8,000 square metres and 6 MW, and as a leader in the cloud and data-centre market with 40 percent market share and more than 100 clients, including telecom providers, organisations and domestic and multinational companies (https://www.grid-telecom.com/nea/anakoinoseis/grid-telecom-ti-sparkle-greece-collaboration). The figures are older and come from a partner announcement, not audited standalone accounts, so they should be treated as directional. Still, the claim supports a consistent picture: Sparkle Greece is not only a route name; it has a customer base and a data-centre role in the local market.

The more difficult question is whether that role will grow or be squeezed. Greece's digital-infrastructure market is becoming more crowded. Hyperscaler announcements raise customer expectations. Neutral data-centre operators and energy-linked fibre owners can compete on facilities and domestic routes. Global carriers can sell international capacity. Sparkle Greece's best response is not to be the cheapest in any single layer. It is to make the layers work together: Aegean landing points, Chania, Metamorfosis, Koropi, Seabone, BlueMed, GR-IX, cloud access and operational support. The risk is that customers unbundle the layers and buy each from the lowest bidder.

Cable risk has become a budget line

Submarine cable risk used to be a specialist topic. It is now a board-level theme for infrastructure buyers. The European Commission's 2025 EU Action Plan on Cable Security says submarine cables in EU seas, including the Mediterranean, Atlantic, North Sea, Black Sea and Baltic Sea, require stronger resilience and security, and frames the issue around prevention, detection, response, repair and deterrence (https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX%3A52025JC0009). The International Cable Protection Committee says submarine telecommunications cables carry the vast majority of international data traffic, that the global network comprises around 500 cable systems and 1.8 million kilometres of cable infrastructure, and that 150-200 submarine telecom cable faults occur globally each year, with about 70-80 percent caused by accidental human activity such as fishing and anchors rather than sabotage (https://www.iscpc.org/).

Those numbers change how a customer should read TI Sparkle Greece. A cable operator is not selling a world without faults. It is selling a world in which faults are anticipated, rerouted, repaired and explained. In that world, diversity is a product, but only if it is real. Two circuits that leave a building in different ducts but land on the same constrained international path are not true insurance. Two submarine routes that share a congested or politically sensitive terrestrial crossing may be less diverse than the sales slide suggests. A carrier's job is to make the difference visible to customers without exposing sensitive operating detail.

Greece is well placed for this conversation. It sits near the point where European, Middle Eastern, North African and Asian connectivity strategies intersect. Chania, Athens, Koropi and Aghia Marina are not just Greek place names in this context; they are possible answers to the question of how traffic should move when another path becomes less attractive. Sparkle's BlueMed announcement explicitly ties Chania to traffic between Europe, Africa, the Middle East and Asia and says GreenMed is being developed to create a diversified low-latency route between Central Europe, the Balkans and the central and eastern Mediterranean (https://www.tisparkle.com/media/press-release/sparkle-brings-bluemed-cable-crete-and-opens-new-digital-route). The commercial claim is resilience through route optionality.

Yet cable risk is also a cost burden. Repair arrangements, marine maintenance, permits, landing-station hardening, route surveys, monitoring, spare equipment and coordination with governments all have costs. The EU's attention can help by making resilience more fundable and politically recognised. It can also increase compliance and reporting expectations. For a company such as TI Sparkle Greece, the best world is one in which public policy rewards operators that have already built diverse landing and data-centre infrastructure. The harder world is one in which policy creates more obligations while hyperscalers and carriers still resist paying higher route premiums.

The economic issue is therefore not whether submarine cables are risky. They are. The issue is who pays for the reduction of that risk. End users expect their banking app, video call or cloud software to work. Banks, platforms and enterprises push carriers for service levels. Carriers push vendors, cable consortia and governments for repair speed and permits. Investors push operators for returns. Somewhere in that chain, idle capacity and route diversity must be funded. TI Sparkle Greece's value is highest if it can persuade customers that the Greek route, the Chania landing and the Metamorfosis data-centre layer reduce a risk that customers can no longer ignore.

How the evidence should be read

The public evidence for TI Sparkle Greece is strong on identity, assets and strategic role, but weaker on standalone economics. The strongest first-party evidence is Sparkle's own Greece page, Greece data-centre page, Metamorfosis II launch and BlueMed Chania announcement. Together they support the identity of the Greek subsidiary, the four-data-centre footprint, the Aegean network, landing points, Koropi and Chania landing stations, protected ring language, Metamorfosis II capacity, certifications, cloud access, GR-IX connection and BlueMed's Chania role (https://www.tisparkle.com/greece, https://www.tisparkle.com/our-platform/backbone-infrastructure-platform/data-center-solutions/sparkle-greece-data-center, https://www.tisparkle.com/sparkle-launches-data-center-metamorfosis-II and https://www.tisparkle.com/media/press-release/sparkle-brings-bluemed-cable-crete-and-opens-new-digital-route).

The best public network evidence is PeeringDB and RIPEstat. PeeringDB confirms AS198477's public identity and GR-IX Athens presence; PeeringDB's facility page confirms the Metamorfosi site as a visible interconnection location with networks, exchanges and carriers; RIPEstat confirms AS198477's announced state and observed prefixes (https://www.peeringdb.com/net/8240, https://www.peeringdb.com/fac/2951 and https://stat.ripe.net/data/announced-prefixes/data.json?resource=AS198477). This evidence does not reveal utilisation, paid customer mix or contract terms. It supports the claim that TI Sparkle Greece has a real public routing and interconnection surface.

The ownership and balance-sheet evidence comes from TIM. The 2025 annual report confirms TI Sparkle Greece S.A. as a Greek subsidiary held through Telecom Italia Sparkle S.p.A.; TIM's 2025 financial release classifies Sparkle as held for sale and describes the group as developing fibre-optic networks for international wholesale customers; TIM's sale announcement and 2026 long-stop extension show the EUR 700 million sale process and its timing uncertainty (https://www.gruppotim.it/content/dam/gt/investitori/doc---report-finanziari/2025/Annual%20report%202025.pdf, https://www.gruppotim.it/en/press-archive/corporate/2026/PR-BoD-11-March-2026.html, https://www.gruppotim.it/en/press-archive/corporate/2025/PR-TIM-Sale-of-Sparkle.html and https://www.gruppotim.it/en/press-archive/sparkle/2026/PR-TIM-Waiver-Sparkle.html). This evidence supports parent context, not Greek subsidiary revenue.

The demand and risk evidence comes from adjacent sources. AWS's Athens Local Zone announcement shows that regulated, low-latency and local-data workloads are becoming a formal Greek cloud-infrastructure category (https://press.aboutamazon.com/aws-international/2026/6/aws-brings-compute-storage-and-ai-services-to-athens-with-new-local-zone-available-july-2026). The EU cable-security action plan and ICPC statements show that subsea resilience has become a recognised operational and policy concern (https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX%3A52025JC0009 and https://www.iscpc.org/). These sources do not say those customers use Sparkle Greece. They define the market conditions in which Sparkle Greece's assets have value.

The gaps are important. Public sources do not disclose TI Sparkle Greece revenue, EBITDA, ARPU, rack occupancy, power utilisation, sold wavelength capacity, cable-system utilisation, cross-connect revenue, churn, renewal rates, outage history, route-level service credits, hyperscaler contract terms, enterprise concentration or capex commitments by Greek site. They also do not disclose how the pending Sparkle sale will affect Greek investment. Those missing facts do not weaken the asset evidence. They limit valuation precision. The company can be described as strategically well placed; it cannot be priced from the public record with confidence.

The watchpoints

The first watchpoint is sale execution. If the Sparkle sale closes cleanly, with stable service agreements and clearer investment backing, TI Sparkle Greece may gain from being part of a more focused infrastructure owner. If closing drifts, or if post-sale arrangements distract management, wholesale customers may hesitate to make long-term commitments. The Greek unit sells confidence, and confidence dislikes unresolved ownership questions.

The second watchpoint is BlueMed commercialisation. The Chania landing is strategically important, but value will depend on sold capacity, route diversity that customers accept as real, integration with data-centre and terrestrial routes, and the degree to which BlueMed and related systems become preferred paths for Europe-Middle East-Asia traffic. A cable landing can be a trophy, a spare path or a revenue engine. The difference lies in contracts, not announcements.

The third watchpoint is hyperscaler behaviour. AWS's Athens Local Zone, Microsoft's Greek cloud-region plans and Google-linked submarine investment all point in the same direction: global platforms see Greece as a more serious digital-infrastructure market. That helps Sparkle Greece by growing demand. It also gives large buyers more ways to bypass, bargain with or selectively use carriers. Sparkle's strongest defence is to own route-specific value that hyperscalers cannot cheaply replace at every layer.

The fourth watchpoint is domestic interconnection depth. PeeringDB's record for AS198477 is credible but modest in traffic range. The more important question is whether Sparkle's Greek facilities remain attractive meeting points for domestic networks, international carriers, cloud access and enterprise disaster recovery. Facility-level network and exchange counts at Metamorfosi are encouraging. The next test is whether those ecosystems deepen as Greek cloud and data-centre competition grows.

The fifth watchpoint is power and facility economics. Data-centre demand can rise while margins fall if power costs, cooling constraints, certification requirements, construction inflation or customer concentration move against operators. Metamorfosis II's 7.7 MW and the Greek portfolio's 13.7 MW total power figure give Sparkle meaningful scale, but they also mean exposure to energy procurement, utilisation risk and capital upkeep. A high-availability site that is under-filled is an expensive promise waiting for revenue.

The sixth watchpoint is repair and incident credibility. The market is learning that cable faults are normal operating events. Customers will increasingly ask for real incident reporting, route mapping at an appropriate level, service-credit clarity and evidence that diversity claims survive a correlated failure. TI Sparkle Greece's protected ring, Chania landing and data-centre network give it a strong story. The story must be backed by operational evidence when serious buyers ask.

A company paid for what does not happen

The final judgement is positive but not simple. TI Sparkle Greece has a clear identity, a long Greek operating history, four Greek data centres, a visible Aegean network, landing infrastructure, GR-IX presence, public routing records, a parent global backbone, BlueMed's Chania landing and an asset mix that fits the region's digital-infrastructure moment. It is not just a logo on a wholesale price sheet. It is one of the companies through which Greece can sell itself as a Mediterranean connectivity hub rather than merely a national end market.

The economics, however, are harder than the strategic map suggests. Wholesale telecom rewards scale but punishes undifferentiated capacity. Data centres create stickier customer relationships but require constant capital, power discipline and utilisation. Submarine routes create scarcity value but also expose operators to repair risk, geopolitics and long payback periods. Hyperscalers increase demand but press down on unit prices. Parent-company restructuring may bring focus, or it may leave customers waiting for clarity. In that mix, TI Sparkle Greece's real product is not bandwidth. It is trusted optionality.

That trusted optionality is valuable because most customers only notice backbone resilience when it fails. The best carrier contracts are often the ones that produce no story: the payment clears, the content streams, the cloud workload stays close enough, the reroute works, the maintenance window passes, the second path is there when the first one is not. TI Sparkle Greece is paid, at its best, for events that customers never have to explain. The harder it becomes to guarantee that calm in the Mediterranean, the more valuable the company should be. The harder large buyers press the price of calm toward commodity capacity, the more disciplined Sparkle Greece will have to be in proving exactly why its Greek routes, sites and people are worth the premium.