Summary

- Inpecuarias Fibra S.L. is not just a name in a number-resource register. Its Infibra website markets fibre broadband in Pozoblanco, Añora, Dos Torres, El Viso, Villaralto and Torrecampo, with 300 Mbps, 600 Mbps and 1 Gbps symmetric fibre tiers, fixed voice, television and mobile offers using Movistar or Orange coverage.

- The resource evidence is narrower than full network autonomy. RIPE records identify Inpecuarias Fibra S.L. as a Spanish LIR with IPv4 block 185.248.20.0/22 and IPv6 allocation 2a09:f4c0::/29, but the visible route objects and RIPEstat routing data point to origin AS205718, whose holder is Alcort Ingenieria y Asesoria S.L.

- That means the key economic asset is local access and customer control, not independent global routing. Inpecuarias can benefit from address control and local fibre operation, but the public evidence reviewed does not show that it owns the autonomous-system layer carrying its prefixes.

- Retail pricing leaves little room for waste. Infibra advertises 300 Mbps fibre from 19.90 euros a month, 600 Mbps from 24.90 euros and 1 Gbps from 29.90 euros, all with installation included and permanence conditions. At those prices, utilisation, churn and installation payback matter more than headline speed.

- Group context helps explain the operating boundary. Grupo IPP presents a long-running Los Pedroches energy group, electricity distribution assets, and Infibra as a telecom service built around installation, certification, laying, connectorisation and fusion of fibre, but electricity-group proximity does not by itself prove that every telecom asset is owned, fully utilised or economically separated from regulated infrastructure.

- The judgment is conditional and watchful. Inpecuarias Fibra appears to have a credible local retail footprint and useful resource-holder status, yet its value creation depends on customer density, contract duration, renewal capex, upstream terms, supplier costs, and evidence that local service quality commands retention or premium demand rather than simply matching national fibre prices.

Capital Has To Beat Resale Economics

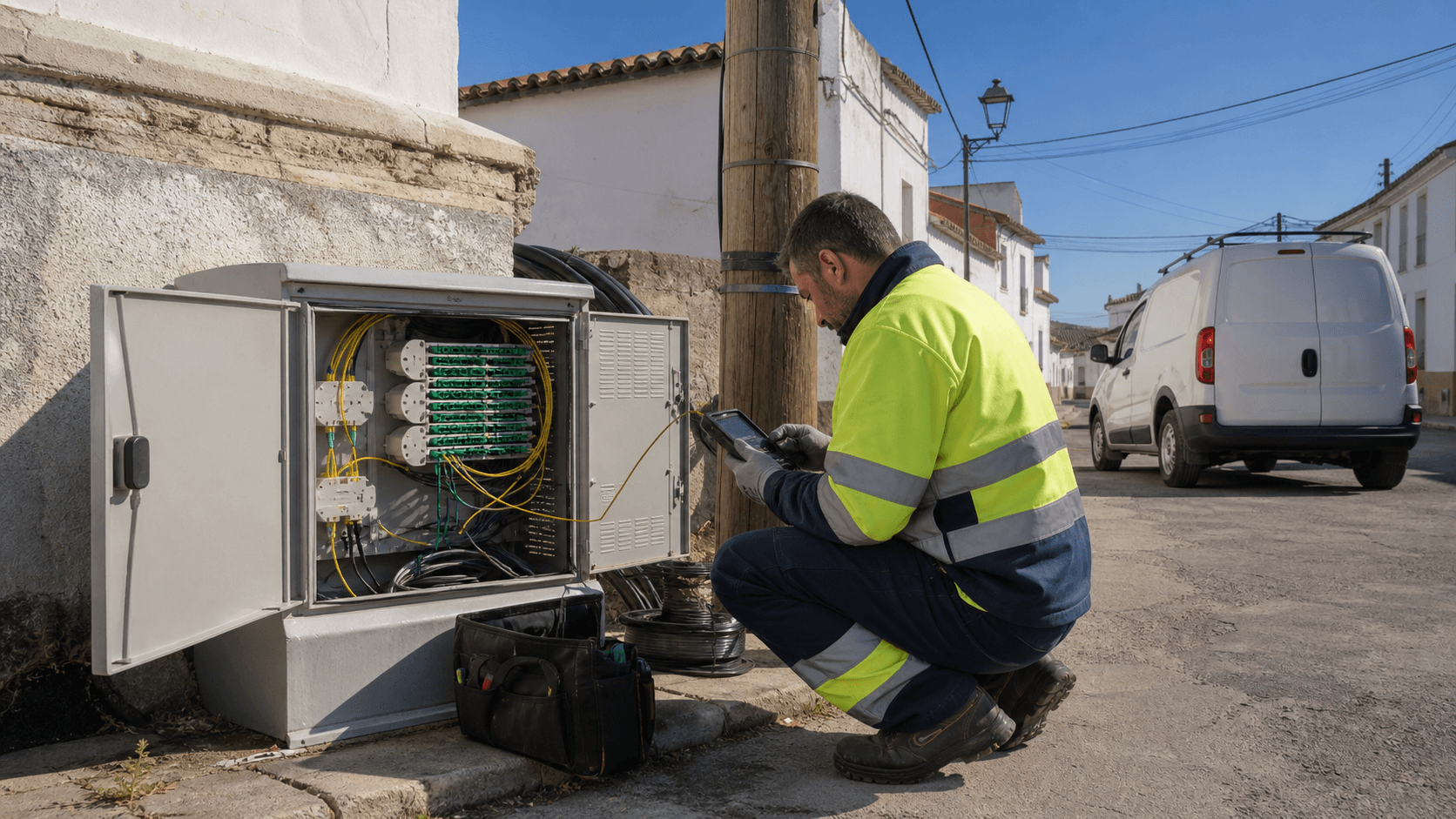

The first economic fact is capital timing. A local fibre operator spends before it knows whether the customer will stay long enough to repay the work. Fibre drops, splitters, cabinets, optical terminals, splicing labour, service vehicles, support systems, billing tools, routers, replacement optics and backup spares all arrive before the subscription stream is secure. Address resources and routing administration add their own costs. They may not dominate the budget, but they make the operator responsible for security, abuse handling, route records and technical contacts.

The reason to accept that burden is control. A pure reseller can acquire a customer quickly, but it usually depends on another operator's physical route, provisioning cycle, repair priority and wholesale price. It controls the brand at the bill, not necessarily the service experience underneath. A local operator that controls the drop, cabinet, access electronics and customer visit can decide where to repair first, which buildings to target, which business sites deserve custom work and which upstream supplier should carry traffic. It can also keep more of the monthly bill if the network is already dense.

Inpecuarias Fibra sits in that trade. The retail offer is local and practical: fibre, mobile, fixed voice and television under the Infibra banner. The public evidence does not support treating it as a national backbone, a cloud platform, a registry operator or a generic technology label. The company is a Spanish local telecom provider with a visible Los Pedroches access footprint and RIPE number resources. That is enough to create economic substance, but it is not enough to guarantee an attractive return.

The return test is severe because Spain has normalized fibre. The CNMC's 2025 sector report says more than 90% of active fixed-broadband lines were already fibre, with almost 20 million fixed broadband lines and 97.1% of those lines above 100 Mbps. In such a market, customers do not pay simply because fibre exists. Fibre is the baseline. The value has to come from local availability, installation speed, support, bundle convenience, business-specific work, a better route, or a price-quality mix that the national operators cannot match in the same streets.

That makes the core question sharper. Inpecuarias Fibra must recover the cost of local control from a small geography, while the customer's visible comparison is a monthly retail tariff. If a household sees 300 Mbps, 600 Mbps and 1 Gbps as commodity speed tiers, the operator must earn its return through density and low service cost. If a business values local response, public addressing or a custom access path, the operator can charge more. The economic issue is not whether network control has theoretical value. It is whether enough local customers pay for the specific control Inpecuarias actually has.

The Company Boundary Is Narrow And Local

The legal and commercial identity is reasonably clear. The Infibra legal notice identifies the social denomination as Inpecuarias Fibra S.L., the commercial name as Infibra, CIF B56030919, and the social address at Cronista Sepulveda in Pozoblanco, Cordoba. RIPE database records use the same company name, Spanish country code and registration number, and identify the organisation as an LIR. Business-directory records also place the company in Pozoblanco and classify it under wired, wireless and satellite telecommunications activities.

The public operating boundary is more useful than the formal service area in the resource registry. Infibra's own fibre page lists Pozoblanco, Añora, Dos Torres, El Viso, Villaralto and Torrecampo as the local footprint for its fibre tariffs. The homepage repeats the same Los Pedroches framing. Its contact page lists customer service in Pozoblanco, a local technical-service telephone number, and office hours. This is the profile of a local access operator, not a company whose value should be judged by national address space alone.

The region matters. Los Pedroches is not Madrid or Barcelona. Customer density, installation routes, field availability and local trust are different in smaller towns. A local operator can have an advantage because technicians know the streets, building access is relationship-driven, and service calls may be handled with less bureaucracy. But the same geography limits scale. A small local footprint cannot absorb capex mistakes the way a national fibre owner can. It must pick buildings, routes and customer segments carefully.

The corporate context also points toward infrastructure familiarity. Grupo IPP says Industrias Pecuarias de Los Pedroches has operated since 1924, presents a regional energy-distribution history, and describes Infibra as a telecom service that installs, certifies, lays, connectorises and fuses multimode and monomode fibre. It also presents a network of electricity-distribution subsidiaries, supplies, medium-voltage lines, transformation centres and low-voltage lines. The useful inference is cultural and operational: the group is not new to field infrastructure.

The unsafe inference would be to assume that every telecom route is group-owned, fully documented or freely usable without cost allocation.

Spanish regulation reinforces that separation. A 2024 BOE publication of a CNMC resolution on electricity distributors' use of fibre in activities other than electricity distribution lists Inpecuarias Pozoblanco, S.L. separately from Inpecuarias Fibra S.L. and sets a 2024 adjustment for that electricity distributor. The company in this article is the telecom operator, not the electricity distributor. The relevant point is that Spain treats utility-associated fibre as an economic and regulatory allocation problem.

If an energy group uses or shares fibre assets for telecom activity, the return calculation has to account for the real cost of those assets, not merely their availability inside the group.

The business directories add scale signals but not full proof. Empresite reports Inpecuarias Fibra as a single-member limited company, active, with a 2024 revenue band of 0.6 million to 1.5 million euros and two employees in 2024. DatosCif reports capital social of 1.6 million euros and shows Industrias Pecuarias de Los Pedroches S.A. as sole shareholder. These are useful signals of small-company economics and parentage, but they are not audited operating disclosures for fibre utilisation, capex, churn or wholesale margin.

Retail Prices Reveal A Volume Business

Infibra's retail menu is the clearest sign of the value challenge. The fibre page advertises 300 Mbps symmetric service at 19.90 euros a month, 600 Mbps at 24.90 euros, and 1 Gbps at 29.90 euros. The same page says VAT is included, installation is included, signup is free, and the plans are subject to permanence. The low step from 300 Mbps to 1 Gbps leaves little price room for treating gigabit as a luxury product. It is a retention and competitive-positioning tool.

Permanence is therefore important. If installation is included and the monthly price starts below 20 euros, the operator needs the customer to stay through the payback period. The public page does not disclose the exact permanence duration in the visible tariff extract, but its repeated presence is economically logical. Without minimum contract duration, a household could consume the free installation, churn quickly, and leave the operator with stranded labour and equipment cost. The hidden unit economic question is installation cost divided by monthly gross contribution, adjusted for churn and support demand.

The fixed-voice offer is also modestly priced. Infibra lists a fixed-only plan at 14.90 euros a month, with installation included, a permanence condition, and compatibility with teleassistance. Fixed voice can matter in a local Spanish market with older households, small businesses and public-service needs. Yet the margin is unlikely to come from voice alone. Voice is a bundle anchor, a retention feature and a way to broaden the relationship, not a standalone growth engine.

Television is priced as an add-on rather than as a high-margin strategic product. Infibra advertises a TV and radio package for 3 euros a month, compatible with any fibre plan and without a permanence commitment for that TV component. The channel list is long, but the price signals that TV is used to complete a household bundle and prevent churn, not to transform the economics. Content licensing, platform support and customer support can absorb much of the apparent price.

Mobile reinforces the reseller layer. Infibra offers mobile tariffs using Movistar coverage and Orange coverage. The Movistar-coverage page includes 4G plans, while the Orange-coverage page includes 5G wording and a range of data allowances. This lets Infibra sell a household bundle without building a radio network. It also means mobile economics depend on wholesale or partner terms. The customer may see one local brand, but a meaningful share of service delivery and cost sits with national mobile networks.

The structure is rational. Fibre creates the home relationship. Fixed voice, mobile and TV fill the bill. Local support reduces churn. But the evidence points to a volume business with some add-on contribution, not a premium network-control business by default. At a 19.90 euro entry price, the company must keep truck rolls low, installation efficient and utilisation high. A local operator can win here, but only if the access network is dense enough and the service process is disciplined.

Resource Holder Status Gives Control But Not Autonomy

The RIPE records matter because they show more than a white-label retail brand. Inpecuarias Fibra is listed by RIPE NCC as a member under the es.infibra handle. The RIPE database organisation record identifies ORG-IFS9-RIPE as Inpecuarias Fibra S.L., country ES, registration number B56030919, and organisation type LIR. That establishes a resource-governance footprint.

The IPv4 allocation is specific: 185.248.20.0 to 185.248.23.255, netname ES-INFIBRA-20180306, status ALLOCATED PA, country ES, created in March 2018. That is a /22, or 1,024 IPv4 addresses. In a market where IPv4 remains scarce, even a small block has operational value. It can support public addressing, avoid full dependence on carrier-grade address sharing, simplify certain business services and make customer moves less dependent on a wholesale carrier's numbering plan.

The IPv6 allocation is larger in address terms: 2a09:f4c0::/29, netname ES-INFIBRA-20190326, status ALLOCATED-BY-RIR. Within that allocation, the reviewed RIPE records also show a more specific 2a09:f4c0::/32 assignment labelled INFIBRA6-1. IPv6 does not carry the same scarcity premium as IPv4, but it carries strategic value. It can support cleaner customer numbering, reduce translation complexity and make the operator less dependent on legacy IPv4 economics over time.

However, resource holding is not the same as full routing autonomy. The RIPE route object for 185.248.20.0/22 lists origin AS205718. The RIPE route6 object for 2a09:f4c0::/32 also lists origin AS205718. RIPEstat's routing-status view for the IPv4 /22 showed origin 205718 visible to 325 of 326 IPv4 RIS peers at the query time. The IPv6 /29 itself had no direct visible origin in that view, while a more-specific 2a09:f4c0::/32 was visible through origin 205718.

RIPEstat's AS overview identifies AS205718 as held by Alcort Ingenieria y Asesoria S.L., not Inpecuarias Fibra S.L. PeeringDB similarly lists AS205718 as Alcort, a regional cable/DSL/ISP network, with an open general peering policy and a 10G operational presence at ESpanix Madrid. This is not a defect. Many small operators rely on a specialist upstream or regional aggregator. But it changes the value claim. Inpecuarias appears to control address resources and a local retail/access footprint; the public routing layer reviewed is carried by Alcort.

That distinction should discipline valuation. A company that holds prefixes can switch routing arrangements more easily than a pure reseller whose customers sit entirely inside another operator's address plan. But if the current origin AS is external, Inpecuarias does not fully control policy, peering, route propagation or upstream resilience by itself. The resource-holder status improves bargaining power and technical options; it does not eliminate dependence.

Routing Through Alcort Makes Dependency The Central Fact

AS205718 is not an empty number. RIPEstat's announced-prefix data showed AS205718 originating a set of IPv4 and IPv6 prefixes associated with multiple Spanish resource holders, including Inpecuarias Fibra's 185.248.20.0/22 and 2a09:f4c0::/32. RIPEstat's routing-consistency view showed these prefixes in BGP and in whois, while also showing import and export relationships with a mix of networks, some present in BGP and some only in whois policy.

PeeringDB gives the commercial shape of that upstream layer. Alcort is listed as regional, supporting IPv4 and IPv6, with not-disclosed traffic levels and ratios, an open policy, and no requirement for multiple locations or ratios. It has an ESpanix Madrid entry with 10G capacity in the PeeringDB extract. For a local operator in Cordoba province, a Madrid exchange or upstream relationship can be perfectly sensible. It provides reach without requiring the local operator to build a national interconnection function.

The economic risk is common-path dependence. Public route-origin data cannot show whether Inpecuarias has physically diverse paths, independent transport to Alcort, backup transit, protected metro backhaul, or redundant power at handoff points. It shows that global visibility exists. It does not show what happens when a local fibre route is cut, a powered site fails, an upstream contract changes, or a peak-hour link becomes congested.

This matters because Infibra sells consumer-facing maximum speeds up to 1 Gbps. A gigabit access link is only valuable if the access network, aggregation, upstream capacity and content paths can handle real demand. The published tariff does not disclose contention ratio, busy-hour throughput, international transit capacity or service-level credits. Most consumer broadband tariffs do not. But for investors, counterparties or business buyers, these are the facts that distinguish valuable local control from commodity access.

There is also a pricing issue. If Alcort or another upstream supplier controls the route to the wider internet, Inpecuarias's gross margin can be squeezed by transit, handoff, backhaul and support terms. Address resources reduce one dependence, but they do not remove the need to buy connectivity and maintain service quality. The value of local ownership depends on how much of the cost stack Inpecuarias can control directly.

The route evidence is still positive. It shows that the Inpecuarias resources are live and globally visible, not merely dormant entries. The IPv4 block has been visible since 2018 in RIPEstat's routing-status data and was visible on the review date. The IPv6 more-specific was also in the AS205718 announced-prefix set. A dormant resource holder would have a weaker economic case. Inpecuarias has live network-resource evidence; the issue is whether the visible routing arrangement leaves it with enough autonomy to earn a return.

The Electricity Group Context Helps Explain The Footprint

Infibra's local-market advantage is more credible when seen inside the Grupo IPP context. Grupo IPP presents a century-long regional energy history, current electricity-distribution assets and a telecom service under the same broad business ecosystem. It says Infibra provides high-speed internet and other telecom services to residential and business customers, and highlights fibre installation and fusion capabilities. That is a plausible origin for a local operator: a group with routes, field crews, civil-work familiarity and community relationships extends into fibre service.

This does not mean telecom is costless. A pole line, duct, building route or utility corridor has an economic owner and a regulatory context. If telecom activity uses assets developed for electricity distribution, Spain's energy regulator cares about cost allocation. The BOE-published CNMC resolution on fibre use by electricity distributors is a reminder that regulated infrastructure cannot simply subsidise unrelated telecom activity without adjustment. The 2024 adjustment listed for Inpecuarias Pozoblanco is small in absolute terms, but the principle is larger: shared infrastructure has to be paid for somewhere.

Local infrastructure groups can still be strong competitors. They may know where demand is, where the difficult routes are, and which customers need fast field response. They may also have a trusted brand in towns where national operators are remote. Infibra's contact page, office address, technical-service number and local office hours support the idea of a service model built on proximity.

The risk is that proximity disguises under-recovery. A group may be willing to keep prices low because telecom supports the broader brand or because fibre was built as part of another infrastructure programme. That can work while assets are new or underused. It becomes dangerous when equipment ages, customers expect gigabit service, national operators discount bundles, and replacement capex arrives. The real test is not whether a regional group can build fibre. It is whether the telecom subsidiary can pay for renewal from telecom cash flows.

The history also raises governance questions. DatosCif's indication that Industrias Pecuarias de Los Pedroches S.A. is sole shareholder and Grupo IPP's presentation of Infibra within the group give a coherent ownership narrative. But group support can cut two ways. It can provide patient capital, local credibility and infrastructure know-how. It can also obscure segment profitability if costs, assets or staff are shared. A lender or buyer would need segment-level accounts, asset schedules and service-level data before assigning a premium to the fibre business.

For the article's economic lens, the group is best treated as an enabler rather than the answer. It helps explain why a small-town operator exists and why it might have field competence. It does not prove that differentiated demand is sufficient. Demand has to appear in take-up, churn, business contracts, premium services or lower unit cost. Otherwise, the group has simply moved capital from one local infrastructure pocket to another.

Unit Economics Depend On Utilisation, Not Just Speed

The most useful way to read Infibra's tariff book is as a utilisation problem. A fibre route with many paying customers can support low retail prices because the fixed cost is shared. The same route with low take-up can destroy value even at gigabit speed. Speed is visible to the customer, but utilisation is what repays the build.

Take the entry fibre plan. At 19.90 euros a month including VAT, annual gross billed revenue is 238.80 euros before considering tax treatment, payment failure, support cost, upstream cost, router or optical terminal cost, field labour and customer acquisition. If installation is included, the payback period depends heavily on how cheaply the company can connect a home and how long the customer remains. A few unnecessary truck rolls can consume months of margin.

The 600 Mbps and 1 Gbps plans add only 5 euros and 10 euros per month above the entry plan. That suggests the capacity upgrade is used to defend the customer relationship and segment heavier users modestly, not to extract a large premium. If network capacity is already available, that can be efficient. If the operator must upgrade aggregation or upstream links to support growing gigabit usage, the small price increments may not be enough.

The fixed-voice and television components improve retention but do not obviously transform the economics. A fixed phone line can help retain households that need teleassistance or traditional calling. A 3 euro TV package can make the bundle feel complete. Mobile offers create a converged household relationship. Yet each add-on brings supplier, support or platform dependencies. Bundling can reduce churn; it can also increase complexity faster than margin.

Business demand is the more promising route to value, but it is less visible. Grupo IPP says Infibra serves residential and business customers, and the fixed-voice page includes an "Empresas" voice plan. Business customers can pay for static addressing, priority repair, custom installation, second paths or internal site links. Publicly visible consumer pages do not show a detailed business-fibre service-level portfolio. That absence does not mean such contracts do not exist. It means the investment case cannot rely on them without separate evidence.

The third-party business directories offer some scale clues. Empresite's 2024 revenue band of 0.6 million to 1.5 million euros and two employees would be consistent with a small, lean operator rather than a large network owner. If accurate, that scale can be attractive if the network is dense and mature, because overhead is low. It can be fragile if the company needs frequent field work, new electronics, outside contractors and upstream upgrades. A two-person reported headcount does not by itself explain who installs, repairs, supports and administers a live fibre footprint.

Unit economics therefore turn on missing facts: homes passed, active subscribers, average revenue per user, churn, installation cost, contract length, customer-acquisition cost, monthly gross margin, business share, backhaul cost and repair volume. Without those, resource-holder status and tariff pages show capability, not return. The company has a plausible economic model; the public evidence does not yet prove that the model earns more than the cost of control.

The Cost Base Is A Field-Service Commitment

Local telecom cost is not only routers and fibre. It is a standing promise to answer phones, visit homes, splice cables, replace customer equipment, troubleshoot Wi-Fi, manage appointments, update billing, handle faults, and keep the network documented. Infibra's contact page gives a customer-service telephone number, technical service marked 24/7, and office hours. That is a useful local differentiator, but it is also a labour commitment.

The field-service burden is especially important in a small geography. A national operator can centralise call centres and use large contractor frameworks. A local operator competes on being reachable and practical. That improves trust, but it means each customer problem can become a direct labour cost. When prices are low, the operator needs fewer avoidable visits. Clean installation, good optical signal, robust customer equipment and clear support boundaries are not technical niceties; they are margin protection.

Equipment renewal is the next burden. Fibre itself has a long life, but active electronics, customer routers, optical network terminals, power systems and test equipment do not. A company can look efficient while old equipment is fully depreciated. The value test arrives when renewal is needed. Does the existing monthly price fund replacement, or does the company need new debt, parent support or a price increase?

The Infibra site's mention of Huawei ONT material in search-visible content is an example of customer-premises equipment reality, not a brand conclusion. Every connected home needs a device, installation and support. If the operator supplies equipment, capital and inventory sit with the provider. If the customer buys or rents equipment, adoption friction rises. Either way, device management is part of the cost base.

Power and physical protection are also relevant. A local fibre provider depends on cabinets, central equipment, backhaul handoffs and customer premises having power. Passive optical distribution reduces active field points compared with some older architectures, but it does not remove the need for powered headend and customer equipment. If the company promises reliability, it needs backup power policies and spare parts, not just a fibre label.

The public record does not show capex schedules, depreciation, asset ages, supplier contracts or service tickets. That should not be treated as suspicious; private companies rarely publish those details. But the absence matters for judgment. The question is whether Inpecuarias Fibra has enough differentiated demand to earn value from network control. That cannot be answered by address resources alone. It requires evidence that the field-service machine earns more than it consumes.

Upstream, Mobile And Content Suppliers Keep Leverage

Inpecuarias Fibra's operating model contains several supplier layers. The most important is upstream connectivity through the AS205718/Alcort routing arrangement. The second is mobile service through Movistar or Orange coverage. The third is television/content delivery. The fourth is equipment, installation and support inputs. Each supplier layer can shift margin away from the local operator if terms worsen.

The Alcort layer is the most strategic because it touches the company's number resources. If Inpecuarias holds the IPv4 and IPv6 allocations but Alcort originates them, the operator has more control than a pure reseller but less control than a self-originating autonomous system with its own peering and transit. It can potentially change arrangements, but doing so requires technical planning, route policy, customer impact management and possibly new transport. The option has value, but it is not frictionless.

Mobile offers are commercially useful but structurally dependent. Advertising Movistar coverage and Orange coverage lets Infibra meet household demand for converged service without spectrum, radio planning or national mobile operations. The downside is that customer experience partly follows the host network and wholesale agreement. If mobile prices move, promotions change or coverage complaints arise, Infibra owns the customer relationship but not the whole production chain.

Television has similar logic. A cheap TV and radio package can help retain households. But TV is not a free byproduct of fibre. It needs content rights, platform reliability, customer support and device compatibility. If content costs rise or platform quality disappoints, the operator may have to choose between passing through cost and protecting bundle price.

Equipment suppliers and installers can also hold leverage. A small operator buying optical terminals, routers, splitters, cabinets and optics has less purchasing power than national carriers. It may rely on contractors for peaks in installation and repair. Inflation in electronics, fuel, vehicles and labour can pressure margins even when customer prices stay fixed. The public tariff pages do not show automatic indexation.

The strategic answer is selective control. Inpecuarias does not need to own every layer. It needs to own the layers where local control changes cost or demand: last-mile access, customer relationship, local repair and address administration. It can buy mobile and wider internet reach. But it must avoid pretending that bought layers are fully controlled layers. A premium for reliability is earned only when the company can define what it controls and what it can guarantee.

Competition Makes Price Premium Hard

Local fibre economics are shaped by competition from both national and local substitutes. The CNMC's 2025 market context shows Spain as a fibre-saturated market, not an early build market. More than 90% of fixed broadband lines were fibre, high-speed tiers were common, and the main national groups still concentrated a large share of retail revenue. That makes the customer's outside option stronger.

In Pozoblanco, directory listings show a cluster of telecom and mobile alternatives, including national-brand shops and local services. Páginas Amarillas lists multiple telecom businesses in the town. This is not a monopoly demand picture. Infibra may have coverage advantages in specific streets or villages, and local support may matter, but customers can compare price and bundle offers against other providers.

The company differentiates with local availability in smaller towns and villages. Its fibre page names Pozoblanco, Añora, Dos Torres, El Viso, Villaralto and Torrecampo. National operators may have brand scale, but local operators can win where they deploy earlier, support faster, or connect routes that national sales channels underserve. That advantage is real in regional ISP economics.

The problem is monetising the advantage. If customers see broadband as a commodity, the local operator's reward is lower churn rather than higher price. A household may stay because the technician responds quickly, not because it accepts a large premium. That means value creation has to come from lower retention cost, fewer faults, denser utilisation and carefully priced business work. Local goodwill helps, but goodwill must convert into lifetime value.

The Cylex profile and other local listings give unofficial market signals. Cylex displayed a 4.55 out of 5 aggregate score from 20 opinions from two sources, while search-visible Facebook and Instagram material shows recent promotions, local contact details and community marketing. These signals suggest active local presence and some customer satisfaction, but they are self-selected and not a service-quality audit. They should influence questions, not close the case.

One useful competitive signal is the type of promotion Infibra uses. Low-price fibre, included installation, permanence, mobile bundles and a very cheap TV add-on are standard tools in a competitive retail market. They protect share. They also cap upside. The more the company has to match national pricing, the more important it becomes to have a local cost advantage. Without that cost advantage, network control becomes a burden rather than a moat.

Regulatory And Public-Record Signals Narrow The Upside

Telecom regulation creates a floor of legitimacy and a cost of compliance. The CNMC explains that operators interested in exploiting public networks or providing electronic communications services to the public in Spain must notify the regulator for registration. Infibra's legal notice says it is registered with the CMT, the predecessor regulator. The Ministry's broadband coverage methodology materials also include Inpecuarias Fibra S.L.U. among operators in the fixed-broadband reporting context. These are positive legitimacy signals.

They are not economic proof. Registration means the company is known to the regulatory system; it does not say the network is profitable. Coverage reporting means the operator participates in a sector map; it does not say utilisation is high. RIPE membership means the company holds number resources; it does not say customers pay a premium. Public records reduce identity risk but do not settle return on capital.

The 2017 BOE notice for the creation of the O-RED business association includes Inpecuarias Fibra among a group of promoters with other local telecom and energy-linked operators. That is useful context because it places Inpecuarias inside a community of small operators facing similar wholesale, infrastructure and regulatory issues. It also suggests that cooperation and shared advocacy may be part of the local-operator model.

The financial directories narrow the upside story. Empresite reports a small employee count and a revenue band well below national-operator scale; DatosCif reports substantial capital social relative to that revenue band. If those signals are accurate, the company has meaningful committed capital but a modest operating base. That can be acceptable for a dense local network with stable customers. It is less attractive if capital must keep rising to defend the same retail price.

The ranking signals in Empresite are also cautionary. The listing says the company slipped in sector, national and provincial rankings and reports no foreign-market activity. Ranking moves in a third-party directory should not be overread, but they do fit the broader thesis: this is a local Spanish telecom company in a mature fibre market, not a high-growth platform with expanding geographic reach.

Regulation also changes wholesale economics. CNMC's 2025 report describes Spain's completed copper switch-off, broad FTTH deployment and the definitive deregulation of residential fixed-broadband wholesale access markets in July 2025, while access to Telefónica physical infrastructure through MARCo remains relevant. For local operators, a market with less regulated wholesale fibre access can reward owned local deployment but also increase exposure to commercial terms. If duct, pole, backhaul or wholesale access costs rise, small operators have less room to absorb it.

The Facts That Would Change The Judgment

The current judgment is neither bullish nor dismissive. Inpecuarias Fibra has real local operating evidence, a visible retail offer, resource-holder status and group infrastructure context. It also has low retail prices, dependence on an external origin AS, supplier exposure and limited public financial detail. That combination supports a conditional view: credible operator, uncertain return on network control.

The first fact that would change the judgment is utilisation. Homes passed, serviceable premises, active fibre customers, village-by-village penetration and peak utilisation would show whether the network has density. A 1 Gbps offer in a dense town route is a different asset from the same offer spread across lightly subscribed streets. Utilisation is the difference between capital productivity and stranded build.

The second fact is contract duration and churn. If included installation is protected by long average tenure and low churn, low monthly prices can still work. If customers churn soon after installation or switch between promotions, the operator carries acquisition cost without lifetime value. The permanence condition helps, but the actual retention data would matter more.

The third fact is gross margin by product. Fibre-only, fibre-plus-mobile, fibre-plus-TV, fixed voice, business voice, static addressing, custom business access and installation work probably have different economics. A blended revenue number would hide whether the company earns attractive margin from business customers or simply adds complexity to keep households.

The fourth fact is capex and asset control. A route inventory separating owned fibre, leased fibre, shared electricity infrastructure, third-party ducts, customer-funded drops, active electronics and backhaul handoffs would clarify the control surface. Replacement cost and remaining useful life would show whether the network is self-funding or awaiting a renewal cliff.

The fifth fact is upstream resilience. Inpecuarias would look stronger if it showed physically diverse paths, independent upstream options, tested failover, current route-authorisation coverage, clear IPv6 deployment and enough capacity to support advertised gigabit usage at busy hour. The RIPE and RIPEstat evidence proves visibility; it does not prove diversity.

The sixth fact is willingness to pay for local control. Business contracts with service-level terms, premium installation charges, public-address revenue, custom route revenue, low support churn or documented customer retention would show that local control earns value. Without that, resource-holder status may simply be a cost of staying credible.

The final fact is cash conversion. Revenue bands, rankings and capital social are useful but incomplete. Operating cash flow, annual network capex, supplier payments, repair cost, receivables and debt would tell whether the company is creating value after maintenance. A local fibre business can look strong while it is sweating old assets. It becomes valuable when it funds renewal and still earns a return.

For now, the capital burden sits with Inpecuarias Fibra. Customers receive low-priced fibre and local support; national suppliers provide mobile coverage and wider network layers; Alcort appears to carry the visible route origin; the group provides regional infrastructure context. The return case will improve when the company can prove that local control either lowers unit cost enough to beat national substitutes or creates enough differentiated demand that customers pay for more than speed.