Summary

- Botik Technologies LTD appears to be a genuine local telecom operator rather than a paper resource holder: its own site describes the Botik telecommunications system, subscriber contracts, pricing, office support, payment routes and a history in the Pereslavl-Zalessky regional network, while RIPE records identify it as a Russian LIR with IPv4, IPv6 and AS5572 routing evidence.

- The base-case economic judgment is cautious. Resource-holder status and local embeddedness give Botik operating relevance, but the public record does not prove differentiated demand, customer lock-in, scale purchasing power or margin resilience. The conclusion would improve only with evidence of durable enterprise or institutional contracts, stable low churn, controlled upstream costs, rising paid use of real-IP/network services and disclosed cash margins after maintenance capex.

The incentive is to stay relevant below cloud scale

The managerial incentive at Botik Technologies LTD is not the same as the incentive at a national carrier, a hyperscale cloud provider or a wholesale fiber platform. Botik's public footprint points to a local and regional connectivity business anchored in Pereslavl-Zalessky, not to a broad software or cloud platform. In that position, relevance is a defensive economic asset.

A small operator has to keep enough customers, enough physical and administrative control, and enough service trust to remain worth paying when larger substitutes can offer mobile data, national broadband bundles, cloud hosting, packaged television and managed corporate connectivity.

That is the starting point for the investment question. Regional telecom companies often look more durable than they are because subscribers renew monthly, network assets are hard to replicate street by street, and public number resources give the operator a place in Internet infrastructure. But recurring billing is not the same as pricing power. A customer can pay a monthly invoice for years while the provider earns weak returns because backhaul, field support, regulatory compliance, network equipment, address administration, billing friction and repairs consume the spread. The question is not whether Botik has a serviceable network.

The question is who captures the economic surplus from that network.

The public evidence supports the existence of a local access and network-services operation. The RIPE NCC member page lists Botik Technologies LTD as a Local Internet Registry with a Russian Federation service area, a Trudovaja 1 address in Pereslavl-Zalessky and a public published contact points. The RIPE database organisation entity identifies ORG-BTL9-RIPE as Botik Technologies LTD, country RU, org-type LIR, with registration number 1057601333316. Botik's own website describes the "Botik" telecommunications system, subscriber documents, customer office processes, service prices and payment methods.

Its about page says the project began in 1994, that authority to provide services to subscribers was transferred to Botik Technologies from 20 May 2006, and that the company is responsible for maintaining and expanding the system.

Those facts matter because they prevent the easy mistake of treating Botik as only a record in a registry. It is not merely a line attached to an address block. It has public-facing service material, a customer office and a network story tied to a regional scientific and educational environment. But they also constrain the upside case. The evidence is local, operational and practical. It is not evidence of broad national demand, a proprietary platform, a premium enterprise product set or a wholesale customer base with visible contract duration. Below cloud scale, the best operators survive by being necessary in a specific place.

The weakest ones survive administratively while the economics drift toward commodity access.

For Botik, the incentive to remain relevant therefore has three parts. First, preserve local customer relationships that a national carrier cannot serve with the same granularity. Second, use number resources, routing knowledge and support tools to solve real customer problems rather than simply hold addresses. Third, keep fixed and semi-fixed costs low enough that a modest regional price book can still earn cash. The public record gives some support to the first two. It is much less informative on the third.

The public record defines a local operator, not a cloud platform

Botik's public materials are unusually explicit about the local operating boundary. The company is linked to the telecommunications system "Botik" for the Pereslavl region, with a central office at Trudovaja 1, customer-facing hours, a subscriber-management system called Nadmin, payment channels and published price pages. The about-project page traces the broader Botik telecommunications project to 1994 and describes a regional network developed around the A.K. Ailamazyan Program Systems Institute of the Russian Academy of Sciences.

It says the project originally served the institute and later became a main means of access to city computer resources and the Internet for many local enterprises, institutions and private users.

The same page should be read carefully. It is not a modern investor presentation, and it is not audited market share data. It states that more than 8,000 computers at more than 5,000 subscribers were connected at the time of the page's last published edit. That is a useful operating signal, but the edit date on the page is old, and the company does not provide a current subscriber table, churn data or revenue split. The number is still relevant because it shows the scale of the service ambition and the kind of customers Botik historically served: organisations and private persons in a defined local geography.

It should not be carried into 2026 as a current subscriber count without fresh confirmation.

The RIPE record reinforces the boundary. Botik is an LIR, which means it participates in number-resource administration within the RIPE NCC system. The organisation record gives a Pereslavl-Zalessky address and a Russian registration number. The member page gives the same public location and contact pattern. The maintainer, administrative and technical contact records show a maintained RIPE presence, including admin and technical roles connected to Botik Technologies. These are infrastructure-governance facts.

They do not prove that every related address is monetised at attractive margin, and they do not prove a cloud or managed-services business.

The company website points instead to access and adjacent local services. Its homepage links to payment for communication services, prices, user manuals, customer account tools, bank requisites, statistics, an office page, webmail and interactive digital television documents. The price page separates offers for physical persons, individual entrepreneurs and budget organisations, and commercial organisations. That segmentation is important. It implies a business built around customer classes and monthly tariff regimes rather than a single wholesale network product.

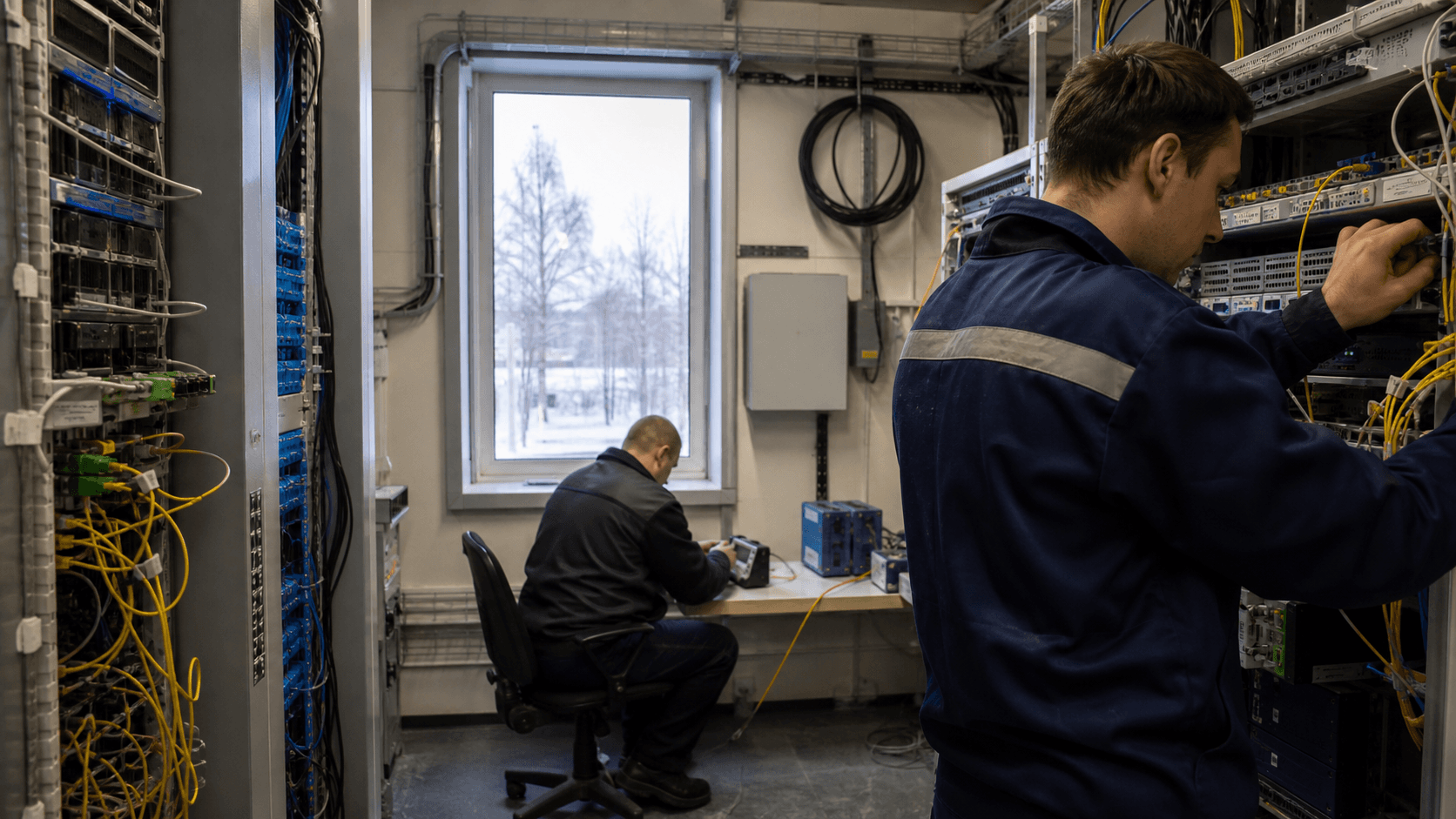

The operating boundary also matters for image and perception. A fair editorial representation of Botik is a local infrastructure scene: cables, office service, access network equipment or regional telecom maintenance. It is not an abstract cloud graphic. The company's economics are likely grounded in local customer acquisition, repair logistics, payment collection, upstream connectivity and address support. None of those is glamorous, but they are the practical points where a small operator can either keep a margin or lose it.

The key identity conclusion is therefore narrow but firm. Botik Technologies LTD is a Russian regional telecom operator with public RIPE LIR status and a customer-facing telecom system in Pereslavl-Zalessky. It should not be valued as a cloud platform merely because it holds resources and operates an autonomous system. It should be evaluated as a local access and network-services company whose differentiated demand must be demonstrated at the subscriber and contract level.

The business model is subscription access plus paid network administration

Botik's own pricing material shows a recognisable small-operator business model: monthly access charges, tariff changes by speed and priority, customer-specific subscriber documents, optional support for real IP addresses or subnets, and different price treatment for residential, budget and commercial customers. The company describes traffic as unlimited in the tariff regimes shown on the price page, with maximum data-transfer speed not dependent on volume or exchange intensity.

That matters because unlimited access shifts the revenue question away from metered traffic and toward the spread between a fixed monthly customer price and variable or step-fixed network costs.

For residential users, the public price page shows high-speed LAN connection organisation being free under typical technical conditions during a promotion, a set of rank-based tariff regimes, a default low-speed "small move" mode, monthly subscription fees for connection states, a rural surcharge and monthly real-IP support fees. The tariff table lists day and night external speeds, external-channel priority and guaranteed minimum speed.

At the top of the residential table, rank 11 shows 100,000 Kbit/s day and night speeds, 18,500 priority units, a 7,900 Kbit/s guaranteed minimum and a monthly price of 1,505 rubles for one plan family or 2,258 rubles for another. Lower ranks fall to cheaper prices with lower priority and guaranteed minimum speed, while the default mode is much slower.

For commercial organisations, the same structure is materially more expensive. The public table shows rank 11 at 100,000 Kbit/s day and night, 18,500 priority units and a 7,900 Kbit/s guaranteed minimum, with a monthly price of 6,022 rubles under one plan family and 9,032 rubles under another. Commercial monthly connection fees are also higher: LAN, LAN radio and NET categories carry larger monthly charges than the residential equivalents. The price page also notes that prices include 20 percent VAT.

This price architecture says a lot about the economic design. Botik is not just selling a binary connection. It is selling a combination of access state, bandwidth regime, priority, minimum speed and administrative services. That creates some opportunity to segment willingness to pay. A household that needs basic connectivity can remain on a lower plan, while a commercial customer can pay for higher priority or a more formal connection type. Paid support for real IP addresses and subnets indicates monetisation of a scarce operational feature, not only raw bandwidth.

The subscriber-document page adds another layer. It says each subscriber receives a personal set of documents governing the relationship with the operator, including the contract, the price list and the service regulations. It also says the current version of the documents is available through Nadmin, and that prices in the price list reflect actual prices for the specific subscriber. This implies that the public price page is not the complete revenue book. It is a window into the model, while individual pricing and service terms may vary by subscriber type, technical condition or special arrangement.

That flexibility can be economically valuable, but it cuts both ways. Personalised terms may let Botik quote for unusual service needs, rural connections or institutional customers. They may also mean the public price sheet cannot be used to infer average revenue per user. A business with many legacy customers, discounts, non-standard arrangements or public-sector constraints can have a more complex revenue mix than its price page suggests. The public record gives no current revenue, no gross margin and no receivables data.

The base-case model is therefore subscription access plus network administration, with optional local services and customer-specific documents. That is a legitimate telecom model. It is also vulnerable to price compression if customers see national mobile broadband, national fixed-line bundles or cloud-hosted tools as adequate substitutes. The value question is whether Botik's local service quality and technical control allow it to charge enough above cost to matter.

Number resources create optionality, but not automatic pricing power

Botik's RIPE and routing records are stronger than its broad commercial visibility. RIPE database records show an IPv4 allocation 95.129.136.0 to 95.129.143.255 linked to ORG-BTL9-RIPE, created in 2009, and another IPv4 allocation 45.81.164.0 to 45.81.167.255 linked to the same organisation, created in 2019. The database also shows IPv6 space 2a01:67e0::/32 linked to Botik, created in 2013.

Route objects connect 45.81.164.0/22 and 2a01:67e0::/32 to origin AS5572 with the description "BOTIK, public network of Pereslavl-Zalessky." The AS5572 aut-num record names the AS as BOTIK and describes it as the public network of Pereslavl-Zalessky.

These are real infrastructure facts. In a small operator, the ability to originate routes, administer address blocks, assign customer addresses, operate reverse DNS and maintain registry data can support differentiated service. Customers who need real IP addresses, stable routing, mail infrastructure, local hosting, institutional connectivity or network troubleshooting may value that capability more than a generic retail broadband bundle. Botik's price page explicitly charges for support of real IP addresses and subnets, which shows that address administration is part of the commercial surface.

But number resources do not automatically equal pricing power. IPv4 scarcity makes addresses useful, but the value belongs to the operator only if customers need the addresses in ways that generate recurring revenue or if the resources can be managed, transferred or deployed in a way that increases cash returns. The RIPE NCC's IPv4 run-out page explains that the RIPE region exhausted its remaining IPv4 pool in November 2019 and that new allocations now come from recovered addresses through a waiting list. That scarcity makes historical allocations more valuable operationally.

It does not prove that Botik can charge a premium if its customers are mostly households using NAT-friendly services.

RIPEstat's AS5572 data confirms that the autonomous system was announced as of 11 July 2026. The announced-prefixes data shows five IPv4 prefixes and one IPv6 prefix visible during the latest two-week window: 95.129.140.0/24, 95.129.136.0/22, 45.81.164.0/22, 95.129.142.0/23, 95.129.141.0/24 and 2a01:67e0::/32. The routing-status data shows visible IPv4 and IPv6 reachability across RIPE RIS peers and announced space of 3,072 IPv4 addresses plus a /32 IPv6 block. That is enough to demonstrate a public network footprint. It is not enough to infer utilisation or profitability.

The best economic reading is optionality with evidence gaps. Botik's resources make it more than a reseller of someone else's retail broadband. They give it control points: origin routing, address assignment, customer-specific network services and technical credibility. Those control points can defend local enterprise and institutional customers that need stable IP addressing and local operator support. They are less valuable if most demand is price-sensitive residential access and if upstream or equipment costs rise faster than tariffs.

The fact pattern that would strengthen the resource-value case is specific. Botik would need to show high utilisation of its address space by paying business or institutional customers, recurring paid real-IP or subnet support, low churn among customers needing static addressing, and evidence that customers choose Botik because of network control rather than because it is simply available. Without those facts, the resources are a necessary input and an option, not proof of value creation.

Routing evidence points to real upstream dependence

AS5572's public routing record also helps identify the downside. The aut-num record lists imports from AS3216, AS13118 and AS31133, with exports announcing AS5572 to each. RIPEstat's neighbour data for AS5572 on 11 July 2026 shows three observed neighbours: AS3216, AS13118 and AS31133. RIPEstat's AS overview identifies AS3216 as PJSC Vimpelcom, AS13118 as PJSC Rostelecom and AS31133 as PJSC MegaFon. In practical terms, Botik's public route visibility depends on relationships with major Russian network operators.

That is normal for a small regional network. It is also a margin fact. A local operator can own customer relationships and still buy reachability from larger networks. If the larger networks have stronger bargaining power, better scale economics, broader mobile offerings and national procurement leverage, the small operator can become a price-taker on the upstream side. Botik may have multiple upstreams, which improves resilience and bargaining compared with a single dependency, but the public record does not disclose contract prices, term length, committed data rates, redundancy costs or minimum volume obligations.

The route objects and RIPEstat neighbour data support a narrow conclusion: Botik operates a visible routed network and is not merely a static member page. They do not prove that it has peering economics comparable to a larger carrier or a metro fiber platform. There is no public evidence in the reviewed material of participation in major Internet exchanges, wholesale transit sales, data-centre interconnection revenue or large enterprise private-network contracts. That absence does not mean such revenue does not exist. It means the public case cannot rely on it.

The economics of upstream dependence are especially important under an unlimited-traffic retail model. Botik's public price page says the relevant tariff regimes are unlimited and traffic is free within the meaning of those plans. Unlimited pricing can be customer-friendly and operationally simple, but it places pressure on capacity planning. If heavy users consume a rising share of bandwidth while prices are sticky, the operator either has to manage priority and guaranteed speeds carefully or invest in more capacity.

The rank-based tariff table is a mechanism for that control: it distinguishes maximum speed, priority and guaranteed minimum speed. It may be the economic governor that lets Botik avoid selling every customer the same undifferentiated unlimited pipe.

This is where the local technical heritage may matter. A network that grew around a research institute and regional computer resources may have more operational knowledge than a simple retail reseller. The Botik about page emphasises economically efficient technical solutions for city-district scale regional networks and the transfer of those "Botik technologies" to other regions. That history suggests a culture of building around constraints. However, the page's historical claims do not substitute for current cost data.

The base case is that routing competence gives Botik credibility and some resilience, while upstream dependence limits margin expansion. Three observed neighbours are better than one, but they are still major suppliers. If those suppliers can also serve the end customer directly, Botik must justify its place with local service, support, customer-specific configuration, payment convenience or institutional trust. Otherwise, the spread between retail tariff and upstream cost can narrow.

The cost base is heavier than the website makes it look

A small access operator's cost base is not just bandwidth. Botik's public materials imply several cost layers: a physical office, customer service staff, payment handling, subscriber-management systems, network maintenance, address administration, local access infrastructure, upstream connectivity, equipment replacement, regulatory compliance and RIPE membership. Each layer is manageable in isolation. Together they define whether the company earns value or simply keeps a regional network alive.

The office page shows a central office, working hours and a customer process for applications and account support. It describes citizens coming to the office to learn connection terms, sign contracts and submit connection requests. It also describes existing subscribers using the office to replenish balances, analyse service state and expenses, and perform account actions. That is valuable local service, but it is not free. Office support is a semi-fixed cost. It can improve retention, especially among households, schools, small businesses or public institutions that prefer in-person support.

It can also weigh on margins if digital self-service does not absorb enough volume.

The subscriber-document workflow has a similar dual effect. Nadmin appears to be a core operational system for subscriber documents, account status, requests and communications. A local system can lower administrative cost if it is mature and tailored to Botik's network. It can raise maintenance risk if it depends on legacy code, local expertise or manual processes. The public site itself still uses older page structures and KOI8-R character encoding on some pages, which is not a direct cost number but is a signal that parts of the web estate are legacy. Legacy systems can be perfectly functional, but they often make change slower.

RIPE membership adds a visible external cost. The RIPE NCC Charging Scheme 2026 states that the annual contribution per LIR account is EUR 1,800, with additional charges of EUR 75 per independent Internet number resource assignment and EUR 50 per ASN assignment for defined categories, plus a EUR 1,000 sign-up fee for new members or additional LIR accounts. Botik's precise bill cannot be calculated from the public article evidence alone, because it depends on the exact chargeable categories and account structure. The point is that resource-holder status carries recurring administrative cost.

For a small operator, EUR-denominated fees also interact with payment friction and currency risk.

Capital needs are the least visible but most important unknown. The price page references LAN, LAN radio and NET connection types, rural surcharges, support for real IP addresses and high-speed connection organisation. Those categories imply access infrastructure and customer-premises or network equipment. The public record does not disclose the age of the network, the share of fiber versus radio or copper, maintenance capex, replacement schedules, power costs, pole/duct arrangements or local repair labour. It also does not disclose whether Botik owns, leases or shares key infrastructure.

That missing capex data prevents a strong margin conclusion. A company can show attractive monthly prices and still have weak free cash flow if it must continually repair access lines, replace equipment, buy capacity or support legacy systems. Conversely, a long-established local network with mostly depreciated infrastructure can generate useful cash if churn is low and support costs are controlled. The same public facts can support either outcome. The deciding evidence is not available in the public record reviewed here.

Therefore the cost-base conclusion is cautious. Botik likely carries enough fixed and semi-fixed cost that scale matters. It does not need hyperscale to survive, but it does need density, low churn and disciplined maintenance. Resource-holder status helps the proposition, but it also adds governance obligations. The margin risk is that the company has to behave like a full operator while competing on prices that customers compare with national bundles.

Customer demand looks local, mixed and insufficiently disclosed

Botik's public demand story is local and mixed across households, organisations and institutions. The about page says the system has served enterprises, institutions and hundreds of residents, and it specifically mentions science and education institutions, medical institutions, commercial enterprises and municipal/government institutions in the city. The price page separates physical persons, individual entrepreneurs and budget organisations, and commercial organisations. The office page is written for both prospective and existing subscribers. These sources together point to a customer base broader than ordinary residential broadband.

That matters because institutional and commercial customers can be more valuable than households if they need static addresses, reliable support, local routing knowledge, mail services, internal resources or bespoke connection terms. A school, medical institution or local company may value a provider that understands the building, the local network history and the administrative workflow. The personal subscriber-document model also suggests Botik can tailor terms, which may help retain customers whose needs do not fit a national carrier's standard package.

However, customer mix is not customer concentration. The public record does not show top customers, contract duration, renewal rates, churn, average revenue per user, bad-debt experience or public-sector exposure. It does not show whether a small number of institutions account for a large share of revenue. It does not show whether households are growing, shrinking or substituting away to mobile and national broadband offers. It does not show whether the "more than 5,000 subscribers" historical figure remains valid in 2026.

This is a critical uncertainty because the local model can be either defensible or fragile depending on density. If Botik has a dense cluster of loyal customers in a geography where it already has infrastructure, incremental revenue can be attractive. If the customer base is dispersed, price-sensitive or aging, support and maintenance can consume the economics. The rural surcharge in the public price page is a reminder that geography matters: serving less dense areas requires extra compensation or a willingness to accept lower margins.

The company also appears to support communication and account-management tools beyond raw access. The homepage links to webmail, subscriber messaging, Nadmin user help, payment pages and video lessons. That ecosystem can reduce churn by embedding Botik in customer routines. It can also be a burden if customers expect extensive support for older tools at low monthly prices. The difference between stickiness and support drag depends on the ratio of service usage to service cost.

Demand differentiation is therefore plausible but unproven. Botik can plausibly claim local embeddedness, subscriber support, network-resource control and a long operating history. It cannot, from the public record alone, claim that these attributes produce premium pricing or durable cash margins. The evidence needed to move the conclusion would include current subscriber counts by segment, churn by segment, renewal rates for institutional customers, average monthly revenue by tariff class, bad-debt trends and the share of customers paying for real-IP or special network services.

Without those disclosures, the correct economic stance is to separate operating relevance from value creation. Botik likely remains relevant to a set of local customers. Whether that relevance is enough to produce attractive returns is still open.

Pricing shows discipline but also the limits of a local tariff book

Botik's price list is one of the best windows into management's commercial logic. It does not read like a generic broadband flyer. It uses ranks, speed ceilings, priority units, guaranteed minimum speed and connection states. It separates plan families. It charges different customer classes differently. It prices real-IP support and subnet support. It treats rural service as a surcharge. That is a disciplined way to ration network capacity and monetise operational features.

The spread between residential and commercial pricing is especially informative. The commercial rank 11 monthly price is roughly four times the residential price for a comparable speed/priority structure under the same plan family. Commercial monthly connection fees are also much higher than residential fees. This suggests that Botik recognises business customers as a different economic pool, not merely as households with a company name. If business customers value uptime, static addressing, support and local accountability, that segmentation can protect margin.

The plan design also tries to avoid the trap of pure headline speed. The table does not only advertise maximum speed. It includes priority and guaranteed minimum speed. In a constrained network, that distinction matters. A provider that sells every plan on peak speed alone may disappoint customers or overbuild capacity. A provider that prices priority and minimum speed can better match cost to revenue. Botik's public tariff architecture therefore looks more thoughtful than a simple commodity access table.

Yet pricing discipline is not the same as pricing power. The prices are denominated in rubles and appear modest in absolute terms for the lower ranks, while RIPE fees, equipment, imported technology exposure, software maintenance and some upstream relationships may have cost components that are less flexible. The public table also notes that connection organisation can be free under typical technical conditions during a promotion. Free installation can reduce acquisition friction, but it moves payback risk onto the operator. If customers churn before the installation and support cost is recovered, economics weaken.

The real-IP pricing is another example. A monthly fee for supporting a single real IP address or subnet can monetise scarcity. But the amounts shown on the public page are small relative to the cost of professional network operations unless there is meaningful volume. A real-IP charge can be a useful add-on; it is unlikely by itself to transform the economics unless attached to higher-value customers who also buy business-grade access, hosting or support.

The price page's statement that all prices include VAT is also relevant. VAT-inclusive pricing constrains the gross-to-net economics from the provider's perspective. Customers see the full price; the operator must manage tax-inclusive revenue against operating costs. That is standard, but it reinforces the need to avoid reading tariff prices as pure net revenue.

The most likely interpretation is that Botik has a locally adapted price book designed to balance fairness, capacity and customer segmentation. That is a positive management signal. The negative signal is that the price book does not prove enough demand to absorb cost inflation or national-carrier price competition. If Botik can regularly sell higher-rank commercial plans, special offers and paid address services, the model can work. If most subscribers sit on low-priced plans and require high support, the margin risk remains.

Substitutes are national, mobile and cloud-shaped

Botik's realistic substitutes are not only other regional fixed-line providers. Customers can substitute in at least four ways. A household can use national mobile broadband or a bundled fixed/mobile provider. A small business can buy connectivity from a national carrier with a wider service desk and bundled voice, mobile and cloud products. An institution can move applications to cloud-hosted platforms and reduce the importance of local mail, local servers or public addressing. A technically capable customer can use address sharing, VPNs and managed services to avoid paying a local operator for some network features.

The RIPEstat neighbour data underlines the competitive context because Botik's observed upstreams are also large operators: Vimpelcom, Rostelecom and MegaFon. Those networks have national scale, procurement leverage and brand reach. They may be suppliers, competitors or both depending on the customer and location. A small operator buying reachability from larger networks has to make itself more valuable to the end customer than the supplier's direct offer.

Cloud competition is subtler. Botik does not appear to be presenting itself as a cloud platform, but cloud defaults still affect local telecom economics. If a local business once needed static addressing, mail infrastructure, local servers and on-premise troubleshooting, cloud migration can reduce some of that demand. At the same time, cloud use increases the need for reliable access. The question is whether Botik captures value as the access provider or loses higher-margin local services as applications move elsewhere.

IPv4 scarcity also creates substitutes. RIPE NCC's run-out explanation notes that networks mitigate scarcity by acquiring addresses through the transfer market or deploying address-sharing technologies such as carrier-grade NAT, while IPv6 remains the long-term solution. For Botik, that means real-IP support has value, but customers may not all need it. Residential users often accept shared addressing if applications work. Business and institutional users may need static/public addressing, but the public record does not show how many Botik customers pay for it.

The company's local history is its strongest defence. A national carrier can compete on scale, but it may not replicate local institutional memory, office support or customer-specific technical arrangements. Botik's about page frames the project as a regional system with scientific and educational roots. If that history translates into trusted relationships with local schools, institutes, municipal entities and businesses, the company may be stickier than its size suggests.

Still, strategy without resource allocation is only language. To defend against substitutes, Botik would need continued investment in service reliability, customer tools, local field support and upstream redundancy. It would also need to know which services customers truly value. The public record does not show a modern product roadmap or investment plan. That is not a defect in the service, but it is an analytical limit. The base case should assume competitive pressure from national networks and cloud substitution unless proven otherwise by customer retention and pricing data.

The substitute analysis points to a mixed conclusion. Botik's local embeddedness is real, and its network-resource control can help with customers who need more than generic access. But the broader market gives customers many ways to reduce dependence on a small operator. That is why the margin case must rest on demonstrated local demand and operating discipline, not on RIPE status alone.

Sanctions and payment friction raise the governance cost of being useful

Botik's Russian location adds a governance and payment layer to the economic model. RIPE NCC's information page for Russian members says Russian members need to choose the right transaction code for payments and discusses Russian VAT legislation in the context of RIPE NCC billing. RIPE NCC's sanctions transparency reporting says the organisation must comply with EU sanctions and may freeze the registration, not the use, of resources in the RIPE Database if sanctions apply to a member or resource holder.

It also notes that OFAC screening can affect banking institutions in the Netherlands and RIPE NCC's ability to invoice and receive payments.

There is no evidence in the reviewed public record that Botik itself is sanctioned or that its resources are frozen. The point is broader. Russian RIPE members operate in an environment where resource administration, billing and compliance checks are more sensitive than they were before 2022. Even when a company is not targeted, payment rails, documentation, screening and banking risk can make administrative continuity more complicated.

For a large carrier, compliance overhead can be absorbed across a big revenue base. For a smaller regional operator, the same overhead can matter more. The RIPE NCC annual LIR fee is modest in absolute terms for a healthy telecom business, but it is EUR-denominated and sits alongside other compliance and administrative tasks. If payments become harder, if documentation requests rise, or if banking routes narrow, management time and financial friction increase. That is not an existential conclusion. It is a cost-of-being-in-the-system conclusion.

Sanctions pressure also affects supplier and equipment choices. The public evidence gathered here does not identify Botik's equipment vendors, financing arrangements or spare-parts supply chain. That means the article cannot claim a specific hardware exposure. But any Russian network operator in 2026 faces a more complex procurement environment than before the war and sanctions escalation. Imported network equipment, software updates, vendor support and payment mechanisms can all become more difficult or more expensive, even if the operator remains locally focused.

The route-dependence evidence compounds the point. Botik's observed network neighbours are major Russian operators. That may provide domestic resilience, but it also means the network is embedded in a market shaped by Russian telecom regulation, national carrier economics and sanctions-related external constraints. If upstream prices, settlement terms or technical interconnection conditions change, Botik's ability to pass costs through to households and local institutions may be limited.

The regulatory conclusion should remain precise. Botik is publicly listed as a RIPE NCC member/LIR and appears to maintain public resource records. The company site shows subscriber contracts and telecom-service payment documentation. The broader compliance environment for Russian RIPE members includes sanctions screening, payment-process details and possible registration freezes for sanctioned resource holders. The public record does not show Botik as a sanctioned entity. It does show that governance status is not costless, and that the administrative side of number resources can become a real operating consideration.

This matters for valuation because resource-holder status is often discussed as an asset. It is an asset only if the company can maintain it, pay for it, document it and use it commercially. In Botik's case, the governance layer strengthens the case that management competence matters. A careless operator could lose optionality through administrative failure even if its local network still works.

The unofficial signals are quiet, which is itself useful

The unofficial signal set around Botik is thin and should be treated with restraint. The useful public signals are not rumours or social-media claims. They are operational traces: the website's current and historical pages, news items, the Nadmin and webmail links, BGP Toolkit's prefix page showing PTR records under botik.ru and pereslavl.ru, and the visible RIPEstat routing data. These signals point to an operating local network with real hostnames, customer-facing tools and a long web history. They do not show a strong independent market narrative.

The quietness cuts both ways. A small regional provider does not need a loud national brand to be economically viable. In fact, the best local infrastructure businesses can be boring: customers pay because the service works, not because the company markets aggressively. A dated website may still serve a loyal local base. A local office may matter more than a polished online funnel. PTR records for mail, DNS, monitoring, wiki or institutional hostnames can indicate practical network use rather than marketing.

But the same quietness limits the upside case. There is no public evidence in the reviewed material of rapid growth, outside investment, major acquisitions, large new enterprise wins, wholesale partnerships or expansion into cloud services. There is no visible customer review corpus strong enough to infer satisfaction. There is no public procurement trail in the reviewed set sufficient to identify durable government or institutional contracts. The unofficial market signal therefore supports existence and continuity, not acceleration.

This is why the article's economic conclusion has to be grounded in what is visible. Botik appears to have a real network, a service model, a resource footprint and a local history. The public record does not show enough demand intensity to prove that the company earns returns above its cost of capital. A local operator can survive for a long time with low margins, especially if the mission includes community service, institutional continuity or technical heritage. Survival and attractive value creation are different.

The quiet signal set also affects risk. If customers value Botik for local trust and reliability, a sudden shift to aggressive national pricing, mobile substitution or cloud-hosted services could take time to show up publicly. A small operator's erosion can be gradual: fewer new connections, lower willingness to pay for special services, more support per customer, delayed equipment refresh, and slow migration of institutional workloads. None of that is visible in RIPE routing data until much later.

Therefore unofficial signals are useful mainly as guardrails. They support the view that Botik is operational, locally embedded and technically present. They do not support a promotional thesis. The correct language is modest: the company has operating relevance, but the public evidence is limited public evidence to prove differentiated demand at a margin-rich level.

The base case is a necessary local operator with price-taker risk

Putting the evidence together, Botik Technologies LTD looks like a necessary local operator with price-taker risk. Necessary, because its public materials, local history, customer tools, tariffs, office support and RIPE routing footprint show that it occupies a real place in Pereslavl-Zalessky connectivity. Price-taker risk, because its upstream neighbours are major operators, its scale is local, its product set appears access-led, and its public disclosures do not demonstrate unique demand, current subscriber growth or margin durability.

The strongest positive evidence is not any single source. It is the alignment of sources. The company site says Botik provides telecom services, subscriber documents and local support. The RIPE member page says Botik Technologies LTD is an LIR in Russia. The RIPE database links the company to AS5572, IPv4 allocations and IPv6 space. RIPEstat confirms that AS5572 is announced and visible. The price page shows practical monetisation of access, priority, guaranteed minimum speed and real IP support. That combination is enough to say Botik is a real operating network business.

The strongest negative evidence is also an alignment: absence of public financials, absence of current customer metrics, absence of disclosed upstream terms, absence of current capex data, absence of visible premium product expansion and reliance on large upstream networks. These gaps do not mean the business is weak. They mean an outside analyst cannot prove the value-creation case from public evidence.

Under the base case, Botik's economic value likely depends on four operating disciplines. First, hold dense local customer relationships where support and history matter. Second, sell business and institutional services that value static addressing, local troubleshooting and reliability. Third, manage upstream capacity and network maintenance so unlimited tariffs do not become a cost trap. Fourth, keep administrative and compliance obligations under control, including RIPE membership, resource records, billing and Russian member payment processes.

If those disciplines are working, Botik can remain valuable below cloud scale. It does not need to become a platform. It needs to be the provider that local customers trust for connectivity and network administration, while charging enough for higher-value users to cover the full cost base. If those disciplines are not working, resource-holder status becomes a fixed obligation attached to a commodity access business.

The conclusion is therefore deliberately conditional. Botik has enough infrastructure evidence to deserve coverage as a regional ISP economics case. It does not have enough public demand or margin evidence to earn a bullish conclusion. The fair base-case thesis is that Botik's resource status and local embeddedness create useful optionality, but the company remains exposed to supplier concentration, national-carrier substitutes, cloud migration and cost inflation unless it can prove durable differentiated demand.

The facts that would change the judgment are concrete

The judgment would change if Botik disclosed or if public records revealed stronger evidence in five areas.

First, current customer and revenue mix. A current subscriber count by household, commercial, budget organisation and institutional segment would be more valuable than historical statements. The most important numbers would be average revenue per user, churn, net additions, bad-debt rate and the share of customers buying higher-rank plans or paid real-IP/subnet support. Evidence that commercial and institutional customers represent a large, stable share of revenue would materially improve the case.

Second, contract durability. Multi-year contracts with schools, research institutions, medical facilities, municipal bodies or local enterprises would show that Botik's local embeddedness has contractual value. A public-sector procurement trail or disclosed framework agreements could support that claim. Without it, the article can only infer possible institutional relevance from the company's history and public text.

Third, cost and capital discipline. The key evidence would be upstream cost per Mbps or committed capacity, network utilisation, equipment age, maintenance capex, field-service cost, office staffing cost and free cash flow after replacement capex. A small operator with depreciated infrastructure and disciplined capacity planning can be much stronger than it looks. A small operator with old infrastructure and rising repairs can be weaker than its recurring revenue suggests.

Fourth, supplier diversification. The public record already shows three observed upstream neighbours. What would improve the conclusion is evidence of favourable long-term terms, real redundancy, settlement flexibility, access to neutral interconnection, or supplier arrangements that prevent larger carriers from squeezing Botik's spread. The existence of three neighbours is positive. The economics of those relationships are undisclosed.

Fifth, product differentiation. Botik would look more attractive if it showed growing demand for services that national carriers and mobile substitutes do not easily replicate: managed local networks, static-address bundles, institutional network support, security services, local hosting, resilient access for critical facilities or specialist support for science and education customers. Resource control then becomes a commercial lever rather than a governance record.

The opposite facts would weaken the judgment. Declining subscriber counts, reliance on low-price residential plans, rising upstream costs, heavy support burden, unpaid invoices, equipment shortages, loss of institutional customers, reduced route visibility or inability to maintain RIPE obligations would all push Botik toward the price-taker side of the question.

For now, the economic answer is balanced but conservative. Botik Technologies LTD appears to have enough operational substance to earn value from being a local resource-holding network operator if its customers value local support and network control. The public record does not yet show enough differentiated demand or disclosed margin structure to prove that it captures that value. Until those facts appear, the margin risk below cloud scale remains the central issue.