Summary

- The paid unit is a Hong Kong data-centre rack, reserved power, cooling and cross-connect account. For Data Campus Limited, the public case begins with a directory entry and RIPE NCC membership evidence, then moves quickly to the city economics that determine whether a buyer should pay for a local rack before traffic has moved.

- The strongest conclusion is conditional. Hong Kong locality, power reliability, carrier density, HKIX access, cloud on-ramps and facility labour can make a Data Campus account valuable, but public records do not disclose utilisation, booked power, PUE, outage history, cross-connect count, customer concentration, support cost or churn. Those private facts would decide whether the premium is earned.

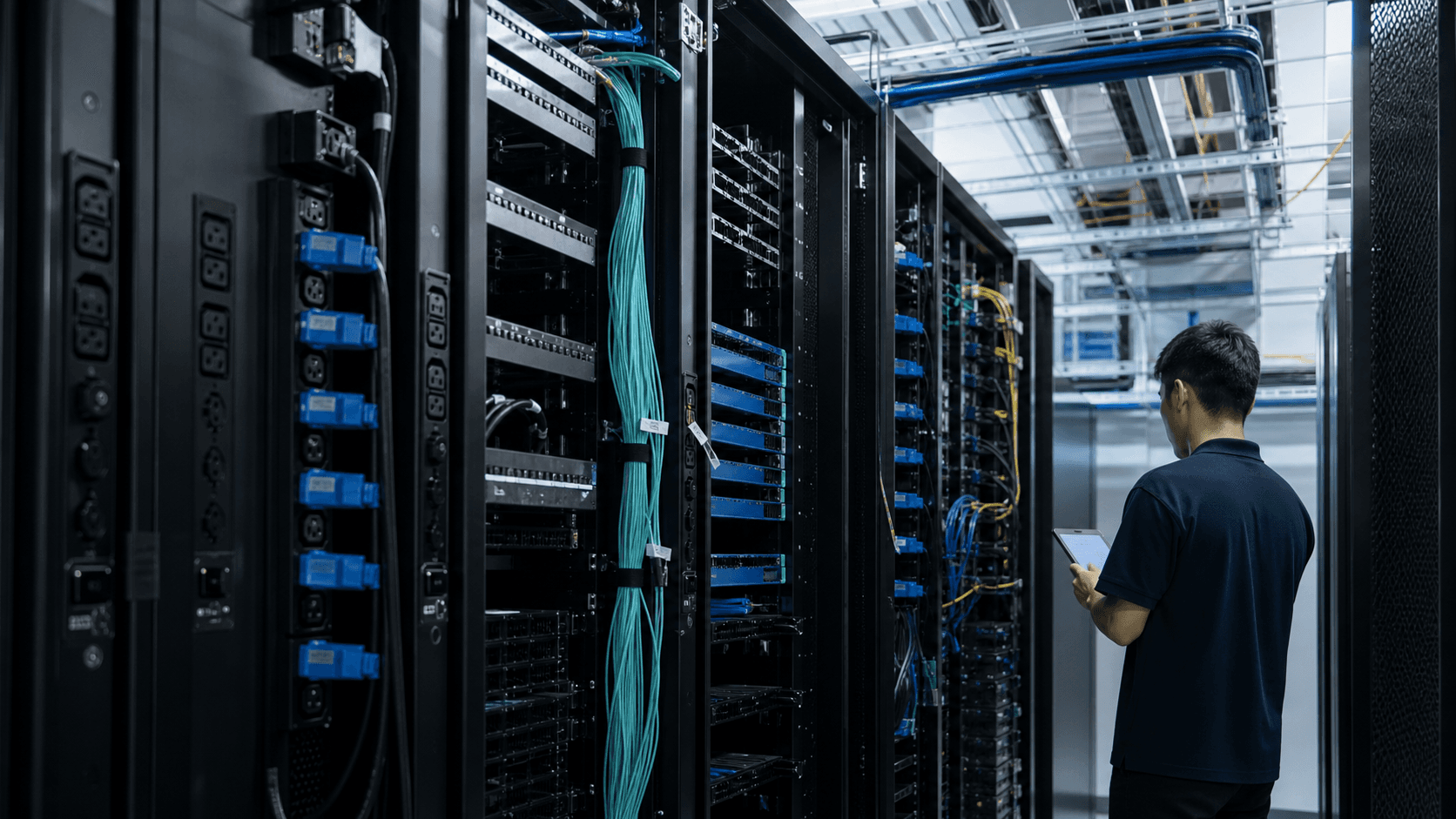

A buyer pays for the rack before it buys the route

A buyer standing in front of a Hong Kong renewal has a deceptively small decision to make: keep a rack account with Data Campus Limited, expand it, or move the workload somewhere else. The first visible entity is a cabinet with power strips, cable trays and a cross-connect order. The paid unit is wider. It is a data-centre rack, power reservation and cross-connect account that bundles the right to consume scarce electrical capacity, remove heat, reach the facility, receive remote-hands support, buy local carrier paths, connect to clouds and keep servers in a Hong Kong operating jurisdiction.

The cross-connect is the moment the account becomes visible to the network team. The rent starts earlier.

That matters because the cheapest substitute is rarely a like-for-like Hong Kong rack. A buyer can place the workload in Singapore, where the regional cloud and colocation ecosystem is deep but power policy has become a major constraint. It can choose Tokyo, where cloud-region density and carrier depth are strong but latency and data-residency trade-offs differ for Hong Kong-facing users. It can move into a hyperscale cloud region and replace cabinets with virtual machines, managed databases and private connectivity. It can keep a smaller on-premise server room if the workload is modest.

It can use a managed hosting provider and avoid direct facility management. It can also delay deployment, accepting slower growth rather than locking in a costly rack. Data Campus has to compete against all of those choices, not only against the operator in the next meet-me room.

The public evidence around the company itself is thin, and that has to be part of the judgement. The linked directory entry for Data Campus Limited identifies the entity in Hong Kong context (https://btw.media/en/directory/data-campus-limited). The RIPE NCC public membership allocation list includes hk.datacampus under Data Campus Limited (https://ftp.ripe.net/ripe/stats/membership/alloclist.txt). That is useful legal and network-resource context. It does not, by itself, show a live colocation hall, an available rack count, uptime, customer names, revenue, power draw or cross-connect volume. A buyer should therefore avoid reading a registry footprint as a facility audit.

The commercial question is still meaningful. If Data Campus is being evaluated as the account counterparty for a Hong Kong data-centre rack, the buyer is pricing seven mechanisms. The first is operating capacity: whether the rack, electrical feed, cooling and building processes can carry the workload. The second is specialist labour: whether remote hands and facility staff reduce the buyer's own support burden. The third is capital intensity: whether the provider has already absorbed building, UPS, generator, cooling, security and network-room costs.

The fourth is locality: whether Hong Kong jurisdiction, privacy rules, telecom density and customer latency matter enough. The fifth is upstream dependence: electricity suppliers, landlords, carriers, IX operators and cloud on-ramp sites shape the service before Data Campus touches the server. The sixth is switching cost: migration risk, downtime windows, equipment moves and readdressing create friction. The seventh is substitution: Singapore, Tokyo, cloud, on-premise rooms, managed hosting and delay keep the price honest.

The first third of the decision can therefore be answered directly. The customer buys a reserved operating position in Hong Kong, not only a cable. It is expensive because the account converts power, cooling, access control, facility labour, local carrier reach and compliance comfort into a monthly service. Public evidence supports the value of Hong Kong as a data-centre and interconnection location, but it does not yet show that Data Campus has high utilisation, superior reliability or unusual customer retention. The article's judgement turns on that gap.

Hong Kong locality is a commercial feature, not scenery

Hong Kong's data-centre appeal is not just that it is geographically close to southern China and Southeast Asia. The government data-centre portal describes Hong Kong as a financial, trading and logistics hub with regional offices and headquarters of global corporations, demand from business growth in Mainland China and the region, robust telecom infrastructure, low risk of natural calamities and data-privacy protection under the Personal Data (Privacy) Ordinance (https://www.datacentre.gov.hk/en/accommodating_data_centres/why_hk.html). Those are general city claims, but they explain why a Hong Kong rack can survive a cost comparison against a cheaper or larger regional deployment.

The practical buyer is often not choosing between perfection and waste. It is choosing where a specific workload should live. A payments system serving Hong Kong merchants, a media platform with Hong Kong users, a trading-support system, an enterprise edge stack, a branch-network aggregation node or a regulated data store may prefer local placement even if a hyperscale platform in another city is cheaper per compute unit. Locality can reduce latency, simplify access for engineers, keep data closer to the business unit, preserve local carrier options and avoid moving every operational dependency into one cloud contract.

It can also satisfy executives who want equipment in a jurisdiction they understand and can physically visit.

Locality has a cost. Hong Kong is dense, land is expensive, industrial-building conversion can be awkward, and power density is not free. The same official site says data centres in Hong Kong tend to cluster around Tsuen Wan, Kwai Chung, Shatin, Kwun Tong, Kowloon Bay, San Po Kong, Chai Wan and Tseung Kwan O (https://www.datacentre.gov.hk/en/accommodating_data_centres/find_a_site.html). It also says industrial buildings may need lease review, waiver applications or lease modification depending on land-use conditions. That means a buyer paying a rack provider is also paying someone to absorb building-market friction that an ordinary office server room never faces.

This is where a Data Campus account should be judged through locality rather than only through price per rack unit. A Hong Kong rack is most valuable when the workload has a Hong Kong operating reason: user proximity, local incident response, local telecom handoff, data-transfer discipline, cross-border architecture or a need to keep one physical anchor outside the public cloud. If the workload has no local reason, the buyer should challenge the rack account hard. Singapore, Tokyo and a hyperscale region can provide more scale, more automation or more procurement simplicity for many use cases.

Data Campus wins only if Hong Kong itself remains part of the operating design.

The locality value also changes the way evidence should be read. Public city-level sources can support the premise that Hong Kong is a serious data-centre market. They cannot show that one Data Campus cabinet has available power, clean cabling, rapid hands-on response or a diverse carrier path. The public company evidence should therefore be treated as a doorway into a procurement process, not as the conclusion.

The buyer should ask for facility address, authorised-use status, utility feed details, rack-density options, cooling design, site-access process, remote-hands service levels, carrier list, cross-connect pricing, cloud-path options and recent incident history. Without those facts, locality is a reason to keep asking, not a reason to sign blindly.

Power reservation is the first scarce input

The rack begins with electricity. Hong Kong's data-centre portal says the territory has a robust electricity supply network, two power suppliers, connected transmission networks for emergency support and reliability levels exceeding or around 99.999 percent depending on utility area (https://www.datacentre.gov.hk/en/accommodating_data_centres/power_supply.html). It also says dual power-feed requirements can be fulfilled by using two inputs from different power companies or different substations of the same power company. Those statements are important because the buyer is not merely renting metal. It is reserving an electrical position in a city where the value of a rack rises with the certainty that power can be delivered, monitored and restored.

Power is the cleanest explanation for why a colocation account can look expensive. The buyer's server may cost a fixed amount, but the facility has to build for continuous load, redundancy, switchgear, UPS systems, backup generation, distribution, monitoring and safety. A single under-provisioned cabinet can create heat and electrical risk for neighbours. A high-density deployment can change airflow, breaker loading and cooling demand. The monthly charge therefore includes a reservation against a finite and actively managed capacity pool. The rack is less like office rent and more like an option on reliable utility-backed load.

The provider's upstream dependence begins here. Data Campus cannot create Hong Kong grid reliability on its own. It depends on the relevant power company, the building's electrical infrastructure, landlord permissions, generator and fuel arrangements, maintenance contractors, UPS design and the facility's own capacity discipline. The buyer should ask not only how much power is included, but whether it is committed or burstable, how overage is handled, whether A and B feeds are truly independent, how cabinets are metered, whether power changes require lead time, and who pays for additional circuits.

A rack that looks cheap can become expensive if the buyer later discovers that expansion power is unavailable.

Public benchmarks from HKIX show why this granular view matters. HKIX's site-access guidelines say its standard input is 220V AC with dual power sources and that an equipment rack is provisioned for 13A power consumption (https://www.hkix.net/hkix/site-access.htm). Its data-centre policy says standard cabinets are provisioned for 13A, that customers are responsible for ensuring power is sufficient, and that HKIX may inspect or require changes if equipment consumes excessive power (https://www.hkix.net/hkix/access-policy.htm). HKIX is not Data Campus, and its rules should not be imported as Data Campus contract terms. But the policies show the operating reality of dense interconnection rooms: power is allocated, policed and priced before network traffic becomes the issue.

Power reservation also explains the difference between a rack account and a cloud instance. A public cloud hides the power problem inside a hyperscale provider. The buyer sees virtual capacity and region pricing, not switchgear, breaker panels, generator tests or cabinet limits. That is useful when the workload can be abstracted. It is less useful when the buyer has physical equipment, legacy appliances, deterministic network hardware, proprietary storage, compliance-driven inspection needs or low-latency paths into local carriers.

Data Campus can charge for the friction the cloud removes only when the buyer needs physical control enough to accept facility economics.

The judgement on power is therefore conditional but firm. Hong Kong's public power-reliability record and policy support make local racks commercially credible. They do not show that Data Campus has spare power, resilient feeds or a competitive power price. The private facts that would change the account are booked power, available expansion power, actual cabinet density, metered consumption, PUE, utility incidents, generator-test discipline and the ratio of sold rack capacity to installed electrical capacity. Without those numbers, the buyer should pay for confirmed power, not for a city reputation.

Cooling converts electricity into usable capacity

A rack with power but poor cooling is not capacity. It is a liability. Hong Kong's official energy-efficiency page states that high-performance and high-availability data-centre demand has been increasing, that high-density servers consume more power and generate more heat, and that cooling, UPS and power distribution drive further electricity demand (https://www.datacentre.gov.hk/en/facilitation_measures/energy_efficiency.html). That language is blunt enough for procurement: the buyer's economic unit is not a cabinet footprint; it is a cooled and supportable load.

Cooling is one reason the rack should be framed before the cross-connect. A cross-connect can be ordered after equipment is installed. Cooling has to be designed before the cabinet is filled. The provider needs airflow management, chilled-water or direct-expansion systems, hot-aisle and cold-aisle discipline, humidity control, leak detection, environmental monitoring, alarm response and enough spare thermal capacity to handle failure modes.

If a buyer asks only how fast a cable can be patched to a carrier, it may miss the more expensive question: whether the server load can run safely through Hong Kong summer heat, partial equipment failure and future density growth.

Hong Kong's cooling policy also shows that facility economics are partly regulatory and partly engineering. The official water-supply page says high-tier data centres may consider water-cooled air-conditioning for energy efficiency and points to the Fresh Water Cooling Towers Scheme (https://www.datacentre.gov.hk/en/accommodating_data_centres/water_supply.html). The scheme page says projects using fresh-water cooling towers need approval paths involving EMSD, the Water Supplies Department and the Buildings Department, and that applicants should allow time for interdependent approvals and engage experienced professionals (https://www.datacentre.gov.hk/en/facilitation_measures/fresh_water_cooling_towers_scheme.html). A buyer does not see this in a cross-connect order, but it sits inside the rack price.

The cooling issue is also where smaller providers face a credibility test. Large operators can point to public certifications, sustainability reporting, LEED language, PUE ranges or named design standards. For Data Campus, the public record available for this article does not disclose PUE, cooling architecture, certification, maintenance regime or thermal incident history. That absence does not make the account weak by itself. Private companies often disclose little. It does mean the buyer should ask for operating evidence before treating the provider like a scaled carrier-neutral campus.

The substitute analysis changes under cooling pressure. A managed hosting provider may offer a cleaner answer if the buyer does not need physical access. A hyperscale cloud region may be more efficient if workloads are elastic and can avoid dedicated cabinet reservations. Tokyo or Singapore colocation may offer different climate, power and campus options, but neither removes cooling cost. An on-premise server room may seem cheaper until the buyer prices air-conditioning, monitoring, fire suppression, after-hours response and the risk that office facilities staff are not data-centre operators.

Delay can also be rational if a buyer needs high-density GPU capacity that a small cabinet cannot support cleanly.

Cooling turns the value proposition into an operating discipline. Data Campus earns a premium if it can show that reserved power is matched by reliable thermal capacity, that expansion requests are realistic, that remote-hands staff understand airflow and equipment placement, and that the account will not become trapped by a cabinet-density ceiling. It loses pricing power if it can only offer rack space without transparent cooling limits. The first cross-connect may carry revenue, but the cooling plant determines whether the equipment should have been installed there at all.

Facility access and remote hands are labour sold as uptime

The most underrated part of a rack account is labour. Buyers often compare cabinet rent and cross-connect charges, then treat site access and remote hands as minor add-ons. That is wrong for Hong Kong deployments where engineers, carriers, couriers and equipment vendors all need controlled access to a dense facility. The account buys someone else's procedures: entry approval, identity checks, escort rules, equipment move-in and move-out, cabling standards, power-change controls, after-hours work and the right to call a human when a server, port or power feed needs attention.

HKIX gives a useful public example of the labour burden. Its site-access guidelines require authorised persons, prior site-access applications, at least one working day's notice in general, staff or identity verification, equipment move-in/out procedures and rejection of unapproved equipment delivery (https://www.hkix.net/hkix/site-access.htm). Its data-centre policy restricts access to licensed areas, limits visitor numbers, assigns responsibility for representatives, requires clean and tidy areas, bans photography and recording devices, and requires equipment and cabling to comply with power and clearance rules (https://www.hkix.net/hkix/access-policy.htm). Again, HKIX is not Data Campus. The value of the example is that serious interconnection facilities operate through rules, not casual keycard convenience.

For a buyer, those rules become money. A local engineer dispatched to Hong Kong after a failed disk, optics replacement or serial-console issue has travel time, security waiting time and after-hours cost. A remote-hands service can reduce that burden if it is responsive and competent. It can also create risk if instructions are misunderstood or if the provider's support desk is thin. Data Campus should therefore be measured not only by rack price, but by the cost of avoiding unnecessary site visits and the cost of delays when on-site work is unavoidable.

This is where scarce specialist labour enters the price. Facility staff must understand power, cable management, access discipline, hardware handling, safety procedures, escalation and customer communication. They do not need to design the buyer's network, but they need enough operational literacy to execute instructions accurately. In a small facility or a provider without public staffing evidence, the buyer should ask who provides remote hands, whether support is in-house or contracted, what hours are covered, how urgent work is priced, whether a named escalation path exists, and what work is excluded.

Remote hands also influence switching cost. Once equipment is installed and local procedures are learned, moving to another facility is not a simple procurement change. The buyer has to plan maintenance windows, re-cable carriers, order new cross-connects, replicate addressing or routing, move or replace hardware, change access lists, test backups and keep services running during the transition. That friction can make an imperfect rack account sticky. It can also let a provider retain customers without demonstrating strong performance if the cost of moving is high.

Data Campus' retention value is therefore impossible to judge publicly without churn, renewal and incident evidence.

The buyer should price facility access as a risk-control product. A Hong Kong rack is more valuable if the provider can absorb mundane work quickly, keep clean records, enforce safety without blocking urgent repairs, and coordinate carriers in a way that reduces the buyer's own labour. It is less valuable if the buyer still has to manage every physical exception directly. In that case the rack account becomes only a room rental with power, and Singapore, Tokyo, cloud or managed hosting will look more attractive.

Carrier proximity is useful only after the rack is credible

Hong Kong's interconnection market is deep enough to make carrier proximity a real asset. The official data-centre portal says Hong Kong's telecom networks connect to external submarine cable systems and that the city has a liberalised market of Internet transit, exchange, hosting and content providers (https://www.datacentre.gov.hk/en/accommodating_data_centres/why_hk.html). HKIX describes itself as a neutral layer-two settlement-free Internet exchange point based in Hong Kong for faster and cheaper interconnections among networks, and says local exchange helps avoid routing local traffic through overseas paths (https://www.hkix.net/hkix/whatishkix.htm). For a rack buyer, those facts explain why a Hong Kong facility can create value beyond server storage.

The cross-connect is still not the starting point. Carrier density pays off only if the rack has credible power, cooling, access and support. A buyer can order several cross-connects and still have a poor account if cabinet density is constrained, hands-on support is slow or facility access complicates maintenance. Conversely, a modest carrier list can be sufficient if the workload needs only one local transit provider, one private cloud path and a backup route.

The economic question is not "How many carriers are nearby?" It is "Which specific carrier or exchange paths does this workload need, and can the facility deliver them without fragile operating dependencies?"

HKIX pricing makes this practical. Its charge table lists port charges for GE, 10GE, 100GE and 400GE interfaces and says the port charges do not cover local circuit or loop charges, cross-connect charges, satellite-site special connection charges or other charges needed to make the connection (https://www.hkix.net/hkix/Charge/ChargeTable.htm). That line is a procurement warning. Interconnection is layered. The buyer may pay the IX, the facility, the local loop provider, the carrier and the account provider. A cheap cabinet can become expensive if every useful path carries additional cross-connect, local-loop or special site charges.

The public entity list also shows why Hong Kong remains a dense market. HKIX lists a large roster of directly connected networks, including cloud, content, carrier and enterprise names such as Amazon, Alibaba, Cloudflare, China Mobile, China Telecom, China Unicom, Equinix, Google, HKBN, HGC and many others (https://www.hkix.net/hkix/participant.htm). That does not show that Data Campus has direct access to each entity. It does show that a Hong Kong rack can be evaluated against a real local ecosystem rather than against a thin transit market.

SUNeVision's public materials illustrate the competitive bar. Its iAdvantage page says SUNeVision's data-centre footprint spans more than 280MW of power capacity across 3 million square feet of gross floor area, lists MEGA-i, MEGA Plus, MEGA Two, MEGA IDC and MEGA Gateway, and says MEGA-i has more than 200 telco carriers and service providers, about 15,000 cross-connects across its data centres, submarine-cable points of presence, cloud-neutral services and AWS Direct Connect access (https://www.sunevision.com/index.php/our-business/iadvantage). Those are operator claims, but they set a high comparison point. If Data Campus offers a smaller or less public facility surface, it has to win on fit, price, support, specific locality or account flexibility.

PeeringDB facility records reinforce the carrier-density map. MEGA-i is listed with 263 networks and four local exchanges, including HKIX, and its facility record shows a Chai Wan location (https://www.peeringdb.com/fac/225). Equinix HK2 is a separate public facility record in Hong Kong (https://www.peeringdb.com/fac/1118). China Mobile International's GNC Hong Kong also appears as a facility record (https://www.peeringdb.com/fac/7911). These records are industry-database evidence, not guarantees of service. They help a buyer identify where cloud and network adjacency is visible, and they sharpen the question Data Campus must answer: which of these ecosystems can the account actually reach, at what cost and with what lead time?

Carrier proximity is therefore a multiplier, not a standalone asset. It multiplies a good rack account by reducing latency, local-loop cost, upstream transit dependence and migration friction. It does not rescue weak power, cooling or support. Data Campus' strongest sales case is not "we can cross-connect." It is "we can reserve and operate a Hong Kong position from which the right cross-connects are practical."

Cloud adjacency changes the substitute, not the need for discipline

Cloud adjacency is the reason many buyers hesitate before abandoning colocation. AWS lists Equinix HK1 in Tsuen Wan as an AWS Direct Connect location associated with Asia Pacific Hong Kong, and it also lists iAdvantage MEGA-i in Hong Kong with an associated Asia Pacific Singapore region path, with AWS advising high-availability designs using more than one Direct Connect location (https://aws.amazon.com/directconnect/locations/). Microsoft lists Hong Kong and Hong Kong2 ExpressRoute locations, including Equinix HK1 and iAdvantage MEGA-i, with providers such as China Telecom Global, China Unicom Global, Console Connect, Equinix, Megaport, NTT DOCOMO BUSINESS, Tata Communications, Verizon, Zayo and Zenlayer (https://learn.microsoft.com/en-us/azure/expressroute/expressroute-locations-providers). Google Cloud's colocation-facility documentation lists Hong Kong facilities tied to asia-east2, including Equinix HK2, MEGA-i and China Mobile International GNC Hong Kong (https://docs.cloud.google.com/network-connectivity/docs/interconnect/concepts/choosing-colocation-facilities).

These lists matter because they make cloud a complement and a substitute at the same time. A buyer can keep physical equipment in Hong Kong and use private connectivity into AWS, Azure or Google Cloud. It can also skip the rack and put more of the stack directly inside a hyperscale region. Data Campus has to price against both behaviours. A rack account is more valuable if it gives the buyer low-friction paths to clouds while preserving physical control. It is less valuable if the buyer can rebuild the workload in cloud services and avoid cabinet-level constraints.

Cloud adjacency also changes failure design. A company with a Hong Kong rack may use it for network appliances, caching, security controls, storage replication, private access to carriers or low-latency systems, while keeping application compute in cloud. The rack then becomes a control point rather than the whole application estate. That control point needs high uptime because failure can affect many dependent services. The cross-connects matter, but the economic risk sits in the whole chain: power, cooling, equipment, facility access, carrier paths, cloud ports, routing policy and incident escalation.

The cloud substitute is not always cheaper after risk is priced. Hyperscale cloud can reduce capital expenditure, remove hardware support, provide automated scaling and make regional replication easier. It can also raise egress cost, increase dependence on one provider, complicate inspection of physical controls, expose the buyer to service-policy changes and require new staff skills. A buyer with stable workloads, owned appliances or local network functions may still prefer colocation. A buyer with elastic compute, cloud-native architecture and little need for physical gear should demand a stronger justification for any rack renewal.

This is also where Singapore and Tokyo become credible alternatives. The AWS Direct Connect page lists Singapore locations such as Equinix SG2 and Global Switch Singapore, and Tokyo-related options appear across AWS, Azure and Google connectivity lists. Microsoft lists Tokyo, Tokyo2 and Tokyo3 ExpressRoute locations, while Google lists Tokyo and Osaka interconnection facilities in the Asia section of its documentation. These sources do not compare prices, but they show that a Hong Kong buyer with regional flexibility can choose other mature cloud-adjacent hubs.

Data Campus must therefore sell Hong Kong-specific reasons, not generic "Asia-Pacific connectivity."

The provider's private evidence would be decisive. A buyer should ask how Data Campus reaches major cloud on-ramps, whether connectivity is direct, reseller-mediated or carrier-dependent, what cross-connect and local-loop fees apply, how long installations take, what redundancy options exist, and whether multiple cloud paths can be built without a single facility or carrier dependency. Cloud adjacency is not a marketing badge. It is a route-design and cost-control question.

Compliance and locality burden create both value and friction

Hong Kong locality has a compliance dimension. The data-centre portal says Hong Kong has free flow of information, data-privacy protection under the Personal Data (Privacy) Ordinance and a business environment supportive of regional data-centre operations (https://www.datacentre.gov.hk/en/accommodating_data_centres/why_hk.html). The Digital Policy Office says data centres support pillar sectors such as financial services, trading and logistics, and that the government supports data-centre development through a facilitation unit, promotion, industrial-building measures and identification of high-tier sites (https://www.digitalpolicy.gov.hk/en/our_work/digital_infrastructure/industry_development/data_centre/). These public statements help explain why Hong Kong remains relevant even when other hubs offer larger campuses.

The compliance value is not a vague comfort word. It decomposes into failure cost, audit cost, data-transfer review, legal familiarity, incident response and executive accountability. A bank, logistics company, platform operator or professional-services firm may value the ability to keep certain systems in Hong Kong, reach local carriers, dispatch local staff and show that physical infrastructure is not hidden in another jurisdiction. That value can justify paying for a local rack even when cloud compute elsewhere is cheaper.

Compliance also creates friction. Hong Kong facilities may need land-use permissions, lease waivers, energy-saving plans, building works, cooling approvals and industry standards. The concessionary-measures page says building owners may apply for nil-waiver-fee changes for eligible industrial-building space, and lease modifications for high-tier data-centre use can be assessed under data-centre-specific arrangements, with conditions on eligible zones, building age, completion time and data-centre use (https://www.datacentre.gov.hk/en/facilitation_measures/concessionary_measures.html). That policy exists because facility conversion is not frictionless. The buyer's monthly account partly pays for someone else navigating that friction.

Data Campus' counterparty evidence is therefore important but limited public evidence. The directory page and RIPE member-list line show a named Hong Kong company in the network-resource ecosystem. They do not show whether a specific facility has the right land-use status, whether any industrial-building conversion was approved, whether a cooling tower scheme applies, whether security controls are audited, or whether the provider has customer-ready compliance documents. The buyer should ask for the contractual entity, facility-use rights, insurance, security policy, data-access rules, subcontractor list and customer-audit process.

The compliance substitute is not simply "move to Singapore" or "move to Tokyo." Both alternatives have strong infrastructure markets, but they change legal context, user latency, operating access and incident accountability. Hyperscale cloud can provide rich compliance documents, but it changes physical-control assumptions and may concentrate dependency. Managed hosting can simplify controls if the provider is mature, but it may obscure facility-level visibility. On-premise rooms can feel controllable, but they often lack professional environmental and access controls.

Delay reduces immediate risk but can defer a necessary resilience upgrade.

The Data Campus account earns a premium if it converts Hong Kong compliance and locality into reduced operating burden. It does not earn a premium merely by being in Hong Kong. The buyer needs evidence that the company can carry facility access, physical security, data-centre operations, cross-connect coordination and support in a way that reduces audit and incident cost. That evidence is private unless the company publishes certifications or customer case studies. Public city policy explains why the category matters; contract diligence decides whether the counterparty fits.

Market signals point to selective demand, not automatic scarcity

The market signal around Data Campus itself is quiet. Public search and industry-database checks do not surface a rich body of buyer reviews, forum discussion, visible PeeringDB network presence or facility marketing under the company name. That silence should not be overread; small or private infrastructure accounts often leave little public trace. But it means the early-warning signal comes more from regional buyer behaviour than from company-specific chatter.

Hong Kong remains visible in official policy, HKIX participation, cloud on-ramp lists and operator marketing, while Singapore and Tokyo remain credible substitutes with their own cloud and colocation ecosystems.

The regional signal is that buyers are shopping for power and locality at the same time. Singapore is still a major hub, but its data-centre policy debate has trained buyers to ask where additional megawatts will come from and under what sustainability conditions. Tokyo offers major cloud and carrier depth, but not Hong Kong locality. Hong Kong official pages emphasise reliable power, low natural-disaster risk, telecom density and data-centre facilitation. SUNeVision emphasises large power capacity, cross-connects and carrier-neutral scale. HKIX publishes port charges and entity lists.

Those public signals show a market where rack buyers compare power reservation, cloud adjacency and interconnection density, not merely rent.

For Data Campus, that signal cuts both ways. It supports demand for Hong Kong rack accounts if the provider can place customers near the right carriers and clouds. It also raises the burden of evidence because buyers can benchmark the account against larger operators with more visible facility claims. A small provider can still be attractive if it offers responsive support, flexible commercial terms, a useful location, available power or a specific customer relationship. It cannot rely on general market scarcity if public alternatives can show clearer capacity, connectivity or operating evidence.

Buyer chatter in this market is best treated as an alert, not as a fact. Complaints about data-centre pricing, long cross-connect lead times, power constraints, cloud egress bills, facility access friction or support responsiveness may help a buyer frame questions. They should not be used as evidence that Data Campus performs well or poorly. The concrete due-diligence list is more useful: ask for live rack availability, power lead time, cross-connect lead time, remote-hands response times, carrier list, cloud path options, historical incidents, maintenance windows, customer references and renewal behaviour.

The market signal also warns against overbuilding. A Hong Kong rack can be valuable, but not every workload deserves one. Some customer-facing systems can run acceptably from cloud regions with content delivery and regional failover. Some appliances can be replaced by virtual network functions. Some legacy workloads should be retired rather than re-homed. Some data should stay closer to a Hong Kong user or audit function. Data Campus' sale is strongest where the buyer can name the workload that needs a local physical anchor and weakest where the rack is an inherited habit.

The best market test is therefore behavioural. If the buyer is prepared to sign only for a small starter cabinet, refuses committed power, avoids diverse paths and keeps a cloud migration project alive, the rack is probably an option rather than a strategic anchor. If the buyer wants reserved expansion power, predictable remote hands, two independent carrier routes, private cloud paths, documented access procedures and renewal rights around adjacent capacity, the rack has become infrastructure.

Data Campus should prefer the second kind of account even if the first is easier to book, because the second account reveals why Hong Kong locality is worth paying for. It also gives the buyer a cleaner way to measure value: the account should reduce migration risk, incident labour and latency uncertainty, not merely hold equipment.

Utilisation is the private fact that would change the price

Public evidence can describe Hong Kong's market and the buyer's options. It cannot show whether Data Campus' racks are full, half empty, oversold, expanding or under strain. Utilisation is the private fact that would most change the commercial judgement. High utilisation can indicate customer demand, scarce power, sticky accounts and pricing power. It can also indicate limited expansion headroom and longer lead times. Low utilisation can indicate available capacity and negotiable pricing. It can also indicate weak demand or facility limitations.

Without the number, the buyer should not infer strength from the existence of a rack account.

Booked power matters more than raw cabinet count. A facility may have many physical racks but limited committed kilowatts. A provider may sell cabinets at low density while reserving power for future upgrades, or it may have stranded space because electrical or cooling capacity is constrained. The buyer should ask for current sold load, committed but unused load, expansion power, density tiers and the process for adding power. If Data Campus cannot answer clearly, the account should be priced conservatively.

Cross-connect count is another decisive private metric. A high cross-connect count can show a useful ecosystem and customer reliance. It can also show operational complexity and cable-management risk. A low count can be fine for a focused facility, but it weakens any claim that the account sells broad interconnection. Public competitors set a benchmark here: SUNeVision states around 15,000 cross-connects across its data centres and more than 200 telco carriers and service providers at MEGA-i (https://www.sunevision.com/index.php/our-business/iadvantage). Data Campus does not need to match that scale to be useful, but it needs to be clear about what it actually offers.

Outage history belongs in the same category. Public sources do not disclose Data Campus facility incidents. That absence should be neither penalised nor ignored. The buyer should ask for planned-maintenance history, unplanned outage minutes, power events, cooling alarms, security incidents, cross-connect faults and post-incident reports. A provider with few incidents and clear reporting earns a different price from one that merely says service has been stable. Reliability is not a mood; it is evidence of how failures were prevented, contained and explained.

Retention and churn complete the picture. A rack account can be sticky because customers are satisfied or because migration is painful. Those are different businesses. Data Campus would look stronger if it could show renewal rates, expansion by existing customers, low churn, customer references and support satisfaction. It would look weaker if customers retain only the minimum footprint, move new workloads elsewhere or use the facility as a temporary bridge. The public record does not answer this, so the buyer has to make renewal evidence part of procurement.

Customer concentration is the companion risk. A small provider can look highly utilised if a few customers hold most cabinets or most committed power. That can be healthy if those customers are stable, expanding and technically mature. It can be dangerous if one customer drives unusual density, custom access needs, unusual carrier dependencies or negotiating leverage that affects other customers. A buyer does not need the provider to disclose every tenant name, but it should ask whether any single account can materially affect capacity planning, support queues, maintenance windows or future pricing.

Concentration can also explain why a facility feels available today but becomes hard to expand tomorrow: the constraint may not be empty space, but the provider's decision to reserve headroom for existing larger customers.

The same logic applies to cross-connect concentration. Ten cross-connects spread across several carriers, cloud paths and customer types may be more resilient than a larger number clustered around one upstream provider. A buyer should ask where the practical diversity sits: different physical meet-me rooms, different carriers, different ducts, different cloud on-ramps, or simply different ports on the same commercial path. If the answer is unclear, the account should be treated as a single-site operating position with useful locality, not as a fully diversified interconnection platform.

The missing private facts fall into three classes. The economics class includes unit margin, booked power, cross-connect revenue, remote-hands cost and expansion capex. The reliability class includes outage history, maintenance quality, power and cooling incidents, access failures and support response. The retention class includes churn, renewal terms, customer concentration and expansion behaviour. A Data Campus rack can be worth paying for if those facts are strong. Without them, the buyer should pay only for the confirmed service and keep migration options open.

Singapore, Tokyo and cloud set the outside price

Every Hong Kong rack is priced in a regional market. Singapore is the clearest outside comparison because it combines financial-sector demand, cloud density, carrier depth and regional headquarters logic. It can be a substitute for workloads serving Southeast Asia or for companies whose operational centre already sits there. But Singapore is not a free escape. Power availability, sustainability conditions, high land cost and capacity allocation can make the market difficult for buyers seeking new large deployments.

A Hong Kong rack can therefore remain attractive where the workload is Hong Kong-facing, the power reservation is available and the buyer does not need Singapore locality.

Tokyo is a different substitute. It offers major cloud and carrier ecosystems, strong enterprise demand and deep technical labour. It can be a good location for North Asia or global-cloud architectures. It is less natural for workloads whose customers, engineers, compliance questions or carrier dependencies are Hong Kong-based. Tokyo also introduces language, procurement, latency and operational-access differences. For Data Campus, Tokyo is a price discipline more than a direct replacement for every workload. It tells the buyer that mature alternatives exist, but it does not erase Hong Kong locality.

Hyperscale cloud is the most aggressive substitute because it changes the unit from rack to service. Instead of buying space, power and cross-connects, the buyer buys compute, storage, managed databases, load balancing, private connectivity and security services. That can be superior for elastic workloads, new applications and teams that do not want hardware operations. It can be inferior for workloads with fixed appliances, deterministic network paths, large data egress, inspection requirements, local handoff needs or sunk equipment value.

The buyer should compare the full cost of ownership, not a single monthly rack line against a single virtual-machine price.

An on-premise server room is still a substitute for smaller companies, but it is often a false economy. Office cooling, power protection, access logging, fire suppression, monitoring, backup connectivity and after-hours response all have costs. If those costs are ignored, the on-premise room looks cheap. If they are counted, colocation may be cheaper and safer even before carrier proximity is priced. Data Campus can win against on-premise rooms by selling professional operations at a scale the buyer cannot efficiently build alone.

Managed hosting sits between cloud and colocation. It can reduce physical-management burden while preserving dedicated or semi-dedicated infrastructure. It may be attractive for buyers that need stable applications but not direct rack control. It may be weaker when the buyer needs its own network appliances, custom hardware, direct carrier choice or strict physical separation. Data Campus should not fight managed hosting by pretending every customer needs a bare rack. It should win where physical control and Hong Kong interconnection are real requirements.

Delayed deployment is the quiet substitute. A buyer facing uncertain demand may reserve less, defer a new cabinet, virtualise more, consolidate workloads or wait for clearer power and cloud pricing. This is a serious threat to a provider because not buying is often easier than moving. The sales case therefore needs urgency rooted in workload risk: expiring leases, capacity exhaustion, resilience gaps, regulatory expectations, latency problems or upcoming product launches. Without a named urgency, the buyer can keep the option alive and avoid committing to a rack that may sit underused.

The outside price disciplines Data Campus. It cannot sell a Hong Kong rack as if the buyer has no alternatives. It can sell a Hong Kong operating position if the buyer needs local power, cooling, access, carrier proximity and cloud adjacency now. The strongest commercial answer is not that Singapore, Tokyo or cloud are inferior. It is that they solve different problems, and this workload still needs a Hong Kong rack.

The final judgement turns on whether the rack reduces operating risk

Data Campus Limited matters if its account reduces operating risk before the first cross-connect is ordered. The public evidence supports a serious Hong Kong market: government policy favours data-centre development, official pages emphasise power reliability and telecom infrastructure, HKIX shows a dense exchange ecosystem, cloud providers list Hong Kong interconnection options, and SUNeVision's public claims demonstrate the scale of local competition.

The company-specific public evidence is much thinner: a directory entry and RIPE membership context identify the counterparty, but do not disclose facility utilisation, service quality or customer outcomes.

That split should shape the buyer's decision. The right question is not whether Hong Kong colocation can be valuable. It can. The right question is whether Data Campus converts Hong Kong locality into a reliable account. The buyer should price confirmed power, cooling capacity, site-access rules, remote-hands capability, carrier reach, cloud path options, cross-connect lead times, support responsiveness and contract remedies. It should avoid paying for assumed density, assumed uptime or assumed customer demand.

The account is worth more when four conditions are met. First, the workload has a Hong Kong reason: latency, local users, local carrier handoff, inspection, legal familiarity or operational access. Second, the provider can show available and expandable power matched by cooling capacity. Third, remote hands and facility access reduce the buyer's own labour rather than creating delays. Fourth, the interconnection path reaches the needed carriers, IXs and clouds at known cost and lead time. If those conditions are absent, Data Campus is competing mainly on generic cabinet rent, a much weaker position.

The seven cost mechanisms line up clearly. Operating capacity is power plus cooling, not empty rack space. Specialist labour is remote hands, access control and facility coordination. Capital intensity is the building, electrical, cooling, UPS, generator, security and meet-me-room stack that the buyer avoids building. Locality burden is Hong Kong land use, utility dependence, privacy context and local access. Upstream dependence is electricity, landlord rights, carriers, IXs and cloud on-ramps. Switching cost is migration downtime, equipment movement, re-cabling and route redesign.

The practical substitute is any combination of Singapore, Tokyo, hyperscale cloud, on-premise rooms, managed hosting or delayed deployment.

The final judgement is therefore neither a dismissal nor a blank cheque. Data Campus can be commercially important as a Hong Kong rack counterparty if it can show that the account reserves a usable position in a constrained, carrier-rich city. The rack earns its rent when it lowers the buyer's total cost of continuity: fewer site visits, fewer facility surprises, clearer power headroom, cleaner cooling limits, faster cross-connects, better cloud paths and less migration risk.

It loses the argument when the buyer can get the same operating result from a larger Hong Kong facility, a Singapore or Tokyo deployment, a hyperscale cloud region, managed hosting or a delayed project with less uncertainty.

The buyer should keep the rack before the cross-connect in its mental model. The cable is only the visible edge of the account. The value is created earlier, when power is reserved, heat is removed, access is controlled, hands are available, carriers are near, clouds are reachable and Hong Kong locality still matters. Data Campus sells that bundle if the private evidence supports it.

Until utilisation, booked power, PUE, outage history, cross-connect count, customer concentration and churn are disclosed in procurement, the fair public conclusion is disciplined: Hong Kong can justify the account, but Data Campus still has to show that its rack is the one worth renewing.