Summary

- The economic unit is a data-centre power and colocation reservation. Cluster Power's strongest public claim is not a single rack, cloud instance or GPU node; it is the promise that a customer can reserve high-density infrastructure backed by power generation, a high-voltage grid connection, cooling, security and a Romanian site inside the European Union.

- Public project claims and proven live capacity need to stay separate. ClusterPower has described a southern Romania campus that can scale to 4,500 racks and 200 MW, and older project material described five planned data centres. The live public evidence is narrower: a first data centre launched in 2022 after about EUR 40 million of investment, a service catalog describing more than 400 racks, Tier III Design Accredited status, NVIDIA DGX-ready colocation partner status, an active AI microsite, and public partner/customer-market signals.

- The power story is the spine. ClusterPower says the campus uses on-site natural-gas-based electricity and cooling, a 110 kV Transelectrica connection, diesel backup, high-density colocation and a claimed PUE of 1.1. Those claims make power availability the product, but the unit-level thesis remains unproven because public evidence does not disclose economics, reliability outcomes or retention behavior.

- The strategic question is whether a Romanian campus can turn power, land, locality and sovereign-cloud demand into a durable alternative to larger Western European data-centre markets. The public record supports a serious first-phase infrastructure story and suggests AI/sovereign-cloud demand, while still leaving the reserved megawatt short of the disclosures a buyer or lender would want.

The reserved megawatt comes first

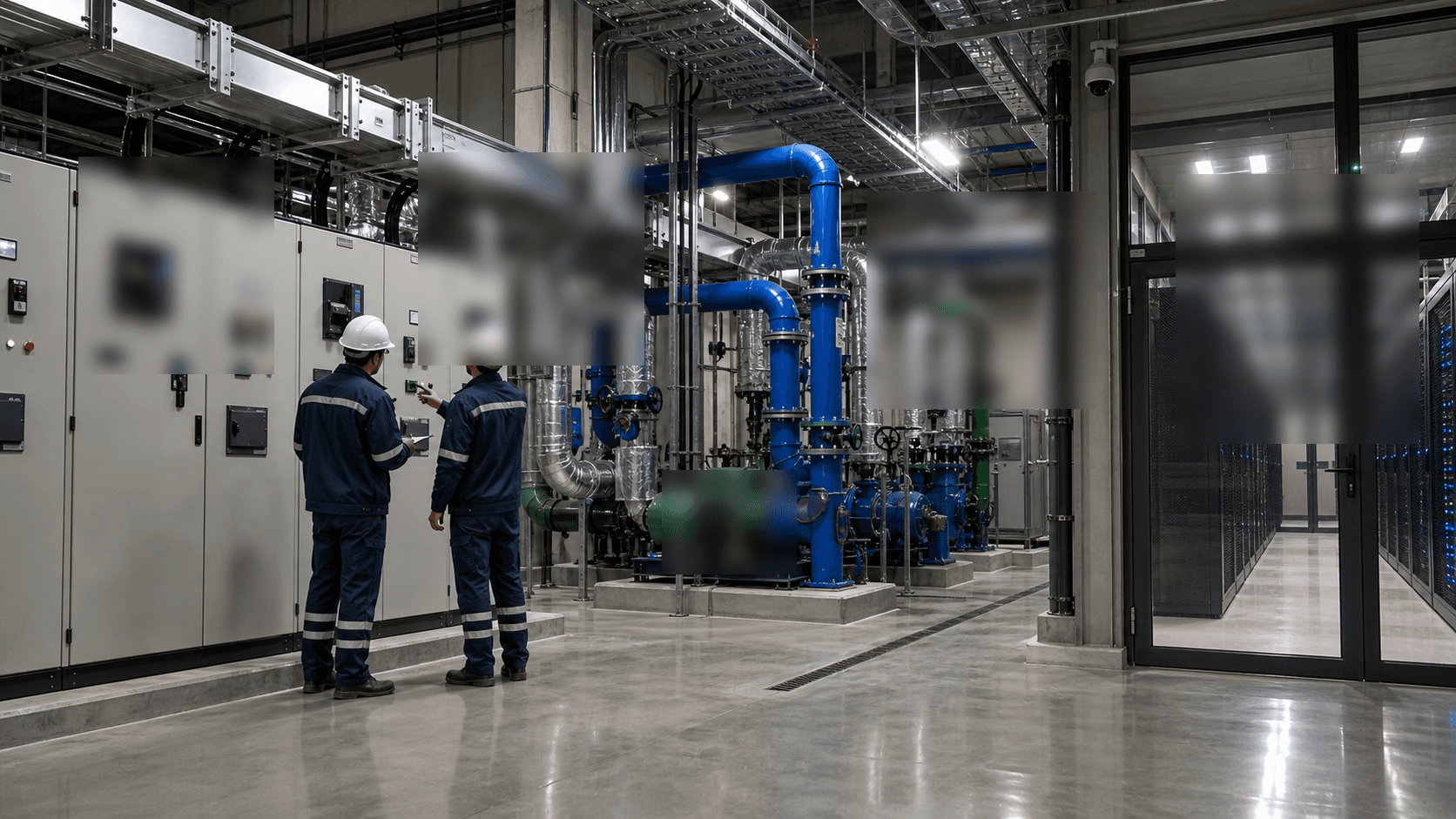

Start with the customer who asks for one megawatt.

That customer may eventually buy racks, cross-connects, remote hands, GPU nodes, storage, private cloud capacity or a managed security service. But the first commercial question is not how many rack units are available. It is whether Cluster Power SRL can make a block of power real, cool it, protect it, connect it, contract it and keep it available over time.

This is the correct lens for ClusterPower because its public material leads with power and infrastructure scale. The company's service catalog and project disclosures present a technology campus in southern Romania, near Craiova, with an ultimate project claim of up to 4,500 racks and 200 MW. The catalog describes a campus with a 110 kV Transelectrica source, self-generation, diesel backup, combined cooling-heating-power equipment, more than 400 racks in the service offer, high-density rack capacity and security controls. The current AI microsite at https://ai.clusterpower.com/ sells dedicated and reserved AI infrastructure rather than casual cloud credit. Its language is built around blocks of GPU capacity, custom architecture, prepayment options, build-and-transfer models and European operation.

The rack is therefore the visible endpoint of a deeper reservation. A buyer can put servers in any number of colocation halls across Europe. A buyer of high-density AI or cloud infrastructure is really reserving a chain of scarce inputs: electrical import capacity, on-site generation, cooling design, switchgear, gas supply, land, permitting, connectivity, security, engineering talent and confidence that the operator will not run out of capital or customers before the load is fully ramped.

The expensive part is not the metal cabinet. It is the unused capacity that has to be carried before the cabinet fills. A reserved megawatt requires power gear to be specified before all customers are known, cooling plant to be sized before the full thermal profile is visible, fuel and electricity exposure to be managed before utilization stabilizes, security and network operations to run continuously, and sales commitments to be long enough to pay back the fixed asset.

If the buyer later cancels, delays hardware delivery or moves workloads to another provider, the operator still owns the substation work, generator maintenance, cooling plant, staff, insurance, land and financing burden. That is why the unit is expensive even when the customer's invoice is described as colocation, GPU service, cloud computing or managed infrastructure.

ClusterPower's promise is that Romania can host that chain. It tells customers that the campus gives access to high-density colocation, HPC and AI infrastructure, scalable cloud computing, storage, backup, cybersecurity and managed services. It also says its data centres are built and operated in the European Union, an explicit nod to GDPR, Schrems II and data-locality concerns. The company is not selling a neutral warehouse. It is selling a sovereign-location infrastructure story for customers that want compute in Central and Southeastern Europe without defaulting to the traditional Frankfurt-London-Amsterdam-Paris-Dublin orbit.

That story has enough evidence to be taken seriously. It also has enough gaps to require restraint. ClusterPower has public proof of a launched first data centre, Tier III design accreditation, DGX-ready partner status, an AI and colocation service catalogue, public partner and customer-market signals, and detailed claims about its power and cooling architecture. It does not publish enough unit evidence on economics, reliability or retention, with contracted MW, measured PUE and churn as the clearest examples. Those gaps are the difference between an impressive project and a proven campus business.

The buyer's substitute is also concrete. It can take a smaller cage in an established European colocation hub, rent public-cloud GPU instances, split workloads across several neocloud providers, buy hardware and place it in another carrier-neutral site, or delay the AI project until a larger platform offers better terms. ClusterPower's edge has to be the combination of available power, local control, high-density readiness, European jurisdiction and a cost story that offsets the operational comfort of larger markets. The evidence supports the existence of the first-phase offer.

It does not yet show whether enough buyers have reserved megawatts for long enough to make the campus economics self-reinforcing.

The entity and the paid unit

Cluster Power SRL is the existing BTW directory entity for this article. The company's current public surface is split between the active AI microsite at https://ai.clusterpower.com/ and the older ClusterPower .ro WordPress material that still hosts the service catalog and project posts. Those public materials describe a Romanian provider of data-centre, cloud, colocation and AI infrastructure services in Central and Southeastern Europe. Older company-posted project material describes the business as founded and owned by Romanian entrepreneurs, while the current analysis keeps the entity name aligned with the directory record rather than trying to create a new legal or operating record from article evidence.

The paid unit for this research is a data-centre power and colocation reservation. That unit can be sold as wholesale colocation, a built-to-suit hall, a private cage, DGX-ready hosting, a GPU cloud block, an IaaS subscription, managed security, storage or backup. The common denominator is not the label on the invoice. It is the reservation of power-backed capacity in a facility that claims to be high-density, redundant, EU-based and engineered around energy production and cooling.

This makes ClusterPower different from a conventional enterprise cloud reseller. A reseller's margin comes from packaging software, support and billing around someone else's infrastructure. ClusterPower's public business case depends on controlling the physical layer: land, power, cooling, racks, security and network access. Its catalog still includes service abstractions such as cloud computing and platform services, but those services are credible only if the campus works as promised.

For a customer, the reservation is a hedge against three problems. The first is Western European scarcity. In established hubs, power queues, land constraints, planning battles and grid limits have become a central part of data-centre procurement. The second is GPU scarcity. AI workloads require dense power, high-speed networking and cooling designs that ordinary enterprise racks were not built to handle. The third is locality. Some enterprises, public-sector buyers and regulated businesses want EU hosting, lower regional latency or a clearer jurisdictional story than a default public-cloud region can provide.

ClusterPower's public materials address all three. The company says it can host high-density colocation and AI infrastructure. It says it offers dedicated and reserved units based on NVIDIA H100 infrastructure on its AI marketing site, while its older catalog and AI service pages describe NVIDIA DGX A100 and NetApp ONTAP AI infrastructure. It says the data centre is Tier III certified or Tier III Design Accredited depending on the page, and its own news states that the 2022 accreditation was Tier III Design Accredited from Uptime Institute.

It says the campus has a 110 kV Transelectrica source, on-site energy generation, redundant cooling and diesel backup.

The commercial value is clear. The proof that customers have filled the campus is not. That distinction should guide every reading of the company.

The project ceiling is not the live floor

ClusterPower's public project ceiling is large. The company's project disclosures have described a first regional hyperscale data-centre campus with up to 4,500 racks and 200 MW. A 2021 company-posted project item, reposting or summarizing external coverage, said a 273,000 square foot campus would scale to a 200 MW power output when five planned data centres came on stream. The same disclosure placed the facility at Mischii in Dolj County and said about half of the initial budget came from Romanian state funding.

Another 2021 company-posted item said the initial investment was RON 172 million, or about EUR 36 million, of which RON 82 million came through state aid granted by the Ministry of Finance. A 2022 company event page said the first data centre was launched at Craiova and the Mischii technology campus after about EUR 40 million of investment, built in roughly six months.

Those are public project claims. They support a narrative of staged expansion, not proof that 200 MW is live and contracted. The difference matters. A 200 MW campus can mean a connection envelope, a master-planned buildout, a long-term power target or a marketing ceiling. It is not the same thing as 200 MW of installed critical IT load, 200 MW of committed customer reservations or 200 MW of utilized capacity.

The proven live floor is smaller but still material. ClusterPower's 2022 event page says the first data centre was launched. Its service catalog describes a technology campus with capacity of more than 400 racks and offices for 200 people. The company says the site has Tier III Design Accredited status, DGX-ready colocation partner status, colocation services, cloud computing services, AI as a service, managed security and storage products.

Its public website is active, its AI microsite advertises reserved H100 infrastructure, and Together AI publicly listed ClusterPower in 2024 as one of the GPU cloud platforms in its multi-cloud network.

That live floor is enough to show that ClusterPower is not merely an unrealized slide deck. It has a real commercial surface and a first data-centre milestone. But the gap between more than 400 racks and up to 4,500 racks is the article's central business question. Customers buying the first megawatts are also buying confidence that the later phases will arrive when needed, that the power chain will remain economic and that the operator can compete for demand before larger European campuses absorb it.

The public record does not yet close that gap. It does not provide a phase-by-phase operating table that links live load, customer reservations, efficiency and commercial performance. In a market where developers often announce enormous power reservations long before load materializes, that absence is not unusual. It does mean that any fair analysis has to treat the 200 MW as a ceiling and the launched first data centre plus service catalog as the current evidence floor.

Power availability is the product

ClusterPower's differentiation begins with power. Company project material and the service catalog say the site uses natural gas to produce its own electrical power and cooling at the same time. They describe a self-engineered energy and cooling production system with a claimed PUE ratio of 1.1. They also describe direct connection to high-voltage infrastructure and to the high-pressure gas transport system.

The service catalog goes further, describing a green self-energy generator, high-density power supply, Rolls-Royce MTU hydrogen-ready equipment used for cooling with estimated PUE below 1.1, a second energy source from Transelectrica through the campus's own 110 kV substation, and diesel generators as a third energy source.

This is not decorative marketing. For high-density AI and cloud workloads, power is the inventory. A data-centre operator can have land, buildings and rack shells, but it cannot sell the next hall if it cannot energize and cool it. A megawatt of reserved capacity is valuable because a customer can map it to GPU clusters, storage arrays, networking equipment, redundancy margins and contract commitments.

The power architecture also shapes the risk. On-site gas-fired generation can reduce dependence on external grid queues and can integrate with combined cooling, heating and power design. It can also expose the operator to gas supply economics, fuel price volatility, emissions rules, maintenance complexity and customer scrutiny over carbon accounting. A 110 kV grid connection can provide credibility and redundancy, but it does not mean that every future megawatt can be drawn without system-level constraints. Diesel generators provide backup, not a cheap primary energy source.

Transelectrica's public network-access page is a useful check on the seriousness of the grid topic. It explains that any applicant complying with legal provisions may be granted access to the transmission grid while observing applicable technical norms, and it lists stages including location approval, technical connection approval, connection contract, grid works, commissioning and energizing the user's installation. For a data-centre campus, those stages are not paperwork trivia. They are part of the real delivery chain. A reservation sold before connection certainty is speculative.

A reservation sold after credible connection work has much more value.

ClusterPower's own claims indicate that it has cleared some of this hurdle for the first phase. The campus is described as directly connected to high-voltage infrastructure, the service catalog names a 110 kV Transelectrica source, and the first data centre has been launched. What the public evidence does not show is how much of the power envelope is firm, how energy pricing is allocated to customers, or whether later phases require additional grid reinforcement.

Those details would determine the economics of the reserved megawatt. If power is firm, redundant, efficiently cooled and contracted at a predictable cost, ClusterPower has a real wedge against constrained European markets. If future power depends on fuel economics, grid upgrades or thin customer commitments, the 200 MW headline is less valuable than it appears.

Cooling is the hidden capacity constraint

Power only becomes sellable data-centre capacity if heat can be removed. ClusterPower's public materials make cooling part of the brand. The company says it produces electrical power and cooling together, uses an innovative combined cooling-heating-power solution, and achieves a claimed PUE of 1.1 or below 1.1 depending on the page. It also markets high-density colocation and DGX-ready hosting, which implies an ability to handle heavier rack loads than ordinary enterprise colocation.

The PUE claim is strategically important. A lower PUE means less total facility energy is needed per unit of IT load. In a market where power is scarce and energy cost can dominate operating economics, that can translate directly into lower customer cost or higher operator margin. For AI infrastructure, cooling has become even more important because GPU racks can run far above traditional 5 kW to 10 kW enterprise-density assumptions. The useful question is not whether a brochure says "high density." It is whether the cooling plant can sustain dense loads across seasons, maintenance windows and partial occupancy conditions.

ClusterPower has some evidence on its side. The company's service catalog says the data centre has rack capacity up to 30 kW for NVIDIA-ready high-performance workloads. The NVIDIA DGX-ready announcement says ClusterPower passed a technical review related to power availability, security and design required to host DGX systems. The service catalog, AI microsite and partner material all emphasize high-density, PUE and energy/cooling integration.

The missing evidence is the operating series. PUE is not a static design label; it is a measured ratio that changes with climate, load factor, redundancy posture, equipment health, part-load efficiency and customer utilization. A lightly loaded facility can have a worse realized PUE than a design figure suggests. A gas-driven cooling system can be efficient in one operating profile and less compelling in another. A high-density rack capability can exist for selected rows without proving that the whole campus is ready for all future phases.

For customers reserving a megawatt, this matters because cooling capacity is part of the reservation. A contract may say one megawatt, but the usable value depends on whether the operator can deliver the density, airflow or liquid-cooling support, maintenance availability and redundancy required by the customer's hardware. ClusterPower's public materials justify a positive hypothesis. They do not yet provide enough measured evidence to prove the realized thermal economics of the campus.

Land, location and permitting

ClusterPower's site near Craiova gives the company a different land and planning profile from the crowded Western European hubs. The company's project material places the campus in southern Romania, in a low seismic activity region, and positions it between the Black Sea, Adriatic Sea and Aegean. The company presents the location as a regional platform for Central and Southeastern Europe rather than a local Romanian facility only.

Land matters because data centres are no longer just boxes with fibre. They need substation space, generator yards, fuel systems, cooling plant, security perimeters, road access, possible expansion phases and increasingly a social licence to consume large blocks of power. A rural or industrial site can be easier to expand than a constrained urban site, but only if permits, grid studies, environmental approvals, gas access and local politics cooperate.

The public evidence proves that at least a first phase reached launch. The 2022 event page says the first data centre was launched at the Craiova event and at the Mischii campus. The Uptime Design Accredited announcement also points to a data centre built near Craiova. That makes the site more concrete than a planned greenfield announcement.

The public evidence does not provide the full permit stack. It does not show building permits for all phases, environmental approvals for the full 200 MW ceiling, gas-connection details, noise conditions, emissions conditions, diesel runtime restrictions, water use permits or local grid-reinforcement approvals. Those are exactly the kinds of records that would matter if the campus tries to move from a first data centre and more than 400 racks toward 4,500 racks and 200 MW.

The location also cuts both ways commercially. Romania can offer power-and-land differentiation, EU jurisdiction and regional proximity. It is not yet one of the default procurement centres for every hyperscale buyer. Large cloud and AI buyers often value ecosystem depth: multiple carriers, repair logistics, hardware vendors, skilled labour, known contractors, financial counterparties, redundancy across nearby campuses and proximity to existing cloud regions. ClusterPower has to persuade customers that its Romanian power and locality benefits outweigh the comfort of established hubs.

Financing and the staged-campus problem

ClusterPower's public financing evidence points to a staged project. The 2021 company post says the initial investment was RON 172 million, or EUR 36 million, with RON 82 million of state aid from the Ministry of Finance and the remainder from company funds and other financing. The 2022 launch event says about EUR 40 million was invested in the first data centre. These figures are credible for an initial phase. They are not enough to finance a fully built 200 MW hyperscale campus by themselves.

This is normal in data-centre development. Campuses are often financed in phases: secure land and permits, build the first powered shell, contract anchor customers, raise debt or equity for the next hall, repeat. The danger is that public attention sticks to the ultimate campus number while capital is tied to actual leasing velocity. A site can be technically promising and still slow to expand if customers do not sign, if debt markets tighten, if hardware availability changes, if utility work is delayed or if energy economics deteriorate.

ClusterPower's model has a potential advantage because it combines colocation, cloud, AI infrastructure and managed services. A pure wholesale colocation developer may need large anchor tenants before a phase becomes financeable. A vertically integrated operator can, in theory, fill part of the site with its own cloud or AI infrastructure and sell higher-value services to enterprises. The AI microsite shows this direction clearly: it advertises H100-based reserved infrastructure, 31-node H100 units, scalable units up to 127 HGX nodes and 1,016 NVIDIA Hopper GPUs, plus flexible prepayments and no transfer or egress costs.

That move can improve margin, but it also increases capital risk. Owning or reserving GPUs, storage, networking and platform operations ties the operator to hardware cycles. H100 infrastructure that looks scarce in one year can face price pressure when newer GPU generations, public-cloud discounts or specialized neocloud competitors enter the market. Colocation can be a real-estate-and-power business; AI cloud becomes a hardware-utilization business. ClusterPower is publicly trying to sit across both.

The missing commercial data becomes more important in that model. The unit-level thesis remains unproven at the economics, reliability and retention levels because public evidence does not disclose examples such as contracted MW, realized PUE or churn. None of those are minor footnotes when the product is a reserved megawatt rather than a small cloud account.

Initial financing is not full-campus economics

The project finance story also has to be read by phase. The public investment figures support a real first build. They do not value the full campus. A roughly EUR 36 million to EUR 40 million first phase can fund land work, initial buildings, electrical and mechanical systems, racks, controls, launch activity and the beginning of a service platform. It does not by itself explain how a 200 MW ceiling would be financed, leased, energized and operated over many years.

This distinction matters because the reservation unit has a time lag. A data-centre developer spends before a customer can use the capacity. It orders equipment, prepares the site, completes grid and gas work, hires operations staff, arranges maintenance, buys insurance, installs security, procures network access and holds enough empty or partly empty capacity to make the sales promise credible. A customer reserving a megawatt may not install all hardware at once. AI customers can ramp in waves as GPUs are delivered. Enterprise customers can delay migrations while application owners, auditors and procurement teams approve the move.

The operator carries that gap.

State-aid language in the company-posted project material is therefore relevant but bounded. Public support can lower the first-phase capital burden and signal that local authorities see strategic value in the project. It does not answer whether later halls are financeable on commercial terms. A lender still wants customer commitments, engineering milestones, grid certainty, insurance coverage, predictable energy treatment and evidence that the site can run without persistent cash leakage.

An equity investor still wants to know whether ClusterPower is selling a high-margin infrastructure service or an expensive buildout whose demand arrives too slowly.

The AI microsite intensifies that question. A pure colocation hall can lease space and power while customers provide their own hardware. A GPU-as-a-service offer can capture more revenue per energized rack, but it adds hardware-cycle risk, inventory risk and platform-support cost. H100-based infrastructure can be scarce in one procurement cycle and less scarce when newer chips ship, public-cloud promotions change, or competitors with larger balance sheets add supply.

A build-and-transfer option can reduce ClusterPower's own hardware exposure if customers ultimately own the system, but it still depends on the campus being a credible long-term home for dense equipment.

This is where the public evidence is strongest and weakest at the same time. It is strongest because ClusterPower can point to a physical campus, an official catalog, first-launch material, vendor and partner positioning, and an AI site that makes the reservation logic explicit. It is weakest because none of those sources shows the current revenue bridge from a first phase to a larger campus. The public record can support a serious capacity option. It cannot yet price the cash yield of that option.

Customer evidence and its limits

ClusterPower has better customer-market evidence than many small infrastructure providers. Its own site says it became an NVIDIA DGX-ready colocation partner in February 2023 after a technical review. It says it is a regional cloud service provider in the NVIDIA Partner Network. A ClusterPower page about NVIDIA-accelerated infrastructure says the company can host large-scale deployments in a customized fit-out model for customers expanding in Central and Eastern Europe.

The Palo Alto Networks case material on ClusterPower's site describes two predominant lines of business: wholesale colocation capacity for large enterprises or third-party data-centre providers, and scalable cloud infrastructure for organisational cloud needs.

The external customer signal from Together AI is especially useful. In March 2024, Together AI said it worked with more than 10 GPU cloud platforms and listed Crusoe Cloud, Applied Digital, Lambda Labs, Vultr, Oracle Cloud and ClusterPower in its cloud network. That does not prove revenue size for ClusterPower. It does show that a visible AI platform viewed ClusterPower as part of a multi-cloud GPU substrate at a time when GPU capacity was a strategic constraint.

This is the right kind of evidence, but it remains bounded. Partner status is not the same as load. A customer mention is not the same as contracted megawatts. A vendor case study is not an occupancy report. NVIDIA and Palo Alto Networks evidence supports technical suitability and go-to-market positioning. Together AI evidence supports market relevance. None of it reveals utilization, unit economics or top-customer concentration.

Customer concentration is a particular risk for a power-led campus. A single large AI platform, cloud provider or wholesale tenant can fill capacity quickly and make a phase bankable. The same customer can also create renewal and bargaining risk. If a tenant accounts for most live load, the operator's headline occupancy can look strong while the revenue base is fragile. If an AI customer moves workloads to another GPU cloud, pushes price concessions or outgrows the site, the operator can be left with specialized capacity and high fixed costs.

ClusterPower does not publish enough to resolve that risk. It sells to large enterprises, third-party data-centre providers, AI users and cloud customers, but the public evidence does not show how balanced those groups are. A better evidence set would group the answer into economics, reliability and retention rather than only naming customers. Until then, the fair conclusion is that ClusterPower has credible market signals but unproven customer depth.

The reservation behaves like a capacity option

A reserved megawatt is closer to an option on future capacity than to an ordinary rack rental. The customer is buying time, certainty and location. It wants to know that a block of electrical and cooling capacity will still be there when GPUs arrive, when a public-sector procurement clears, when a private-cloud migration is ready, or when an AI product moves from trial workload to production workload. The operator, in exchange, wants commitments long enough to justify reserving capacity that another buyer could have used.

That option-like structure changes the risk allocation. If the customer pays only when hardware is live, ClusterPower carries more demand timing risk. If the customer prepays or signs a firm reservation, the customer carries more delay and switching risk. If energy is passed through, the customer carries fuel and grid-price volatility. If energy is bundled, ClusterPower carries more commodity exposure and has to hedge through procurement, self-generation or pricing discipline. Public marketing language about flexible monthly, quarterly, annual or multi-year prepayments is useful because it shows the commercial menu.

It does not show which option is actually used by the largest customers.

The option logic also explains why customer concentration can be helpful and dangerous. One anchor customer can make a phase bankable. It can give lenders comfort, absorb early fixed cost and create a proof point for the next buyer. But an anchor customer can also dominate renegotiation. If one AI platform or wholesale tenant controls a large share of live load, renewal risk becomes a central economic variable. The facility can look occupied while the operator's bargaining position is thin.

If the tenant has portable workloads and alternatives in other European markets, ClusterPower's power advantage has to translate into a renewal price that the tenant still accepts.

Switching cost is not abstract here. Moving high-density infrastructure means scheduling hardware, cabling, networking, cross-connects, storage replication, security review, application downtime planning, data transfer, contract termination and possibly new compliance review. That friction can help a provider retain customers once they are installed. It can also slow the first sale because the buyer knows migration is painful. A cautious buyer will ask for evidence about uptime, maintenance windows, incident response, security attestations, remote-hands quality and energy terms before making the first reservation.

The available evidence suggests that ClusterPower understands the option it is selling. The AI microsite emphasizes custom-built infrastructure, no egress or transfer costs, prepayment flexibility and build-and-transfer choices. The service catalog emphasizes colocation, compute, storage, backup and security around the same campus. Together AI's public mention of ClusterPower in a cloud network suggests that at least one visible AI infrastructure buyer or partner saw the site as relevant to distributed GPU supply. Those signals are meaningful, but they stop short of proving capacity conversion.

The decisive evidence would show how many megawatts have moved from available option to contracted, paid and retained capacity.

Sovereign cloud demand is real, but not automatic

ClusterPower's EU-location argument is straightforward. Its AI microsite says its data centres are built and operated in the European Union, and it explicitly references GDPR and Schrems II. Its service catalog says data is safely stored in the EU in a Tier III data centre, supporting compliance with EU regulations. For Romanian and regional customers, that matters. Public institutions, financial institutions, healthcare providers, manufacturers and regulated businesses often want clearer jurisdictional control, lower regional latency and a procurement story that does not depend entirely on non-European hyperscalers.

That is the demand side of the sovereignty story. The supply side is harder. Sovereign-cloud demand does not automatically flow to a local campus. Buyers still ask about price, certifications, service catalogue depth, security, support, ecosystem compatibility, managed-service maturity, audit rights, disaster recovery and the ability to interoperate with major clouds. Hyperscalers have large compliance teams and mature service portfolios. European colocation providers have broad footprints and network ecosystems. Specialized GPU clouds have aggressive hardware roadmaps.

ClusterPower's advantage is that it can combine location, power and AI/colocation in one Romanian platform. Its disadvantage is that large buyers often prefer multi-region resilience and mature cloud primitives. A single campus can satisfy locality, but it may not satisfy resilience if the buyer needs geographic separation. ClusterPower can be part of a hybrid strategy, but it has to show that its platform can operate as more than a local exception.

The "reserved megawatt" framing helps here. A customer may not migrate every workload to ClusterPower. It may reserve a specific block of AI training, inference, private cloud, backup, disaster recovery or regulated data processing capacity in Romania. That block can be valuable even if the buyer keeps other workloads in AWS, Azure, Google Cloud, Oracle, Equinix, Digital Realty or other European facilities. The commercial opportunity is not to replace the entire cloud market.

It is to sell power-backed, jurisdictionally clear, high-density capacity where the local and regional advantages outweigh the platform breadth of larger rivals.

European campus competition

ClusterPower's project sits inside a European market where the scarce commodity is increasingly power rather than floor space. The International Energy Agency's 2025 Energy and AI report says data centres used about 415 TWh of electricity globally in 2024 and could reach about 945 TWh by 2030, with Europe accounting for 15 percent of 2024 consumption. The report also warns that about 20 percent of planned data-centre projects could face delay unless grid risks are addressed, and that transmission lines and critical components such as transformers and cables have long lead times.

Those facts support ClusterPower's thesis. If established hubs are power-constrained, a Romanian campus with a 110 kV connection, gas-backed on-site generation and expansion land can become more attractive. Customers that previously defaulted to Frankfurt, London, Amsterdam, Paris or Dublin may consider secondary markets if they can get power sooner, at better density, with lower latency to targeted users or stronger locality claims.

But the same facts also increase competition. Every operator now knows that power is the gate. Large European and global data-centre developers are hunting for grid access, on-site generation, renewable procurement, gas turbines, nuclear options, heat reuse and land in secondary markets. ClusterPower is not competing only against facilities already built in Western Europe. It is competing against a wave of developers trying to turn any credible power site into AI capacity.

Scale can also be a disadvantage for a regional entrant. Global operators bring procurement leverage, customer relationships, debt access, construction playbooks, multi-country redundancy and proven operations. They can sign hyperscale customers before construction and use those contracts to finance projects. ClusterPower brings local integration and early Romanian positioning, but it must keep proving that the campus is not just one more ambitious plan in a market full of power-led announcements.

The European competition also changes pricing. If power is scarce, providers with firm capacity can command a premium. If speculative projects overbuild or if AI demand slows, customers will renegotiate and choose the deepest balance sheets. ClusterPower's ability to win depends on whether its reserved megawatts are both real and economically attractive over multi-year terms.

Network and security are supporting evidence, not the core thesis

ClusterPower describes carrier-neutral facilities, dedicated secured circuits to more than 750 data centres, a high-speed backbone, DDoS protection, firewall services, managed security and a large scrubbing centre. Its public service catalog details web application firewall, DDoS, storage, backup and next-generation firewall services. The Palo Alto Networks case material supports a security partnership narrative and quotes the company's CTO on visibility and data-centre security.

These services matter, but they should be treated as support to the power thesis, not as a substitute for it. Security and network services help a customer use the reserved megawatt safely. They do not prove that the megawatt exists, is contracted, is profitable or is efficiently cooled. A carrier-neutral claim is useful, but the article does not have public cross-connect counts, carrier list depth, latency measurements, IP transit volumes or peering statistics. A DDoS service is useful, but the article does not have attack volume, mitigation history or customer retention data.

Bounded public DNS evidence also stays limited. Public DNS checks on the corporate domain showed Cloudflare nameservers, Microsoft mail protection, SPF through Microsoft with one IPv4 address, Microsoft and Google verification strings, and an A record. That is evidence of the public web and corporate-services surface. It is not evidence of data-centre customer architecture, production network resilience, authoritative customer hosting or security outcomes.

This distinction matters because ClusterPower appears in BTW's directory context through number-resource and infrastructure evidence. Network-resource records can support that the entity has an internet infrastructure footprint. They should not be inflated into proof of cloud scale, customer count, live capacity or transit reach. The economic case still rests on physical power-backed capacity.

The conclusion starts at the evidence floor

ClusterPower has a plausible wedge. It is early in Romania's high-density data-centre market, it has public evidence of a first data centre, it has vendor and customer-market signals, and its power-and-cooling story is differentiated. It is operating in a market where AI demand has made electricity access, not merely server availability, a central bottleneck.

The evidence supports a real first-phase infrastructure story. The service catalog, launch material, Tier III Design Accredited announcement, AI microsite, partner pages and Together AI reference are enough to treat ClusterPower as more than a paper project. They suggest that the company has moved beyond an ambition for a Romanian data-centre campus and into a commercial offer that sells colocation, cloud, AI infrastructure and security services around power-backed capacity.

The evidence does not support reading the 200 MW number as live capacity. It remains a project ceiling unless a current public document shows commissioned critical load, customer-occupied load and later-phase energization. The more defensible floor is the first launched data centre, the catalog's more-than-400-rack language, the public AI offer and the partner/customer-market signals around that first phase.

The unit-level thesis remains unproven because the public record does not disclose economics, reliability outcomes or retention behavior. Economics means whether reserved capacity has become contracted and utilized revenue; a contracted-MW figure would be the cleanest example. Reliability means whether claimed design efficiency and power redundancy show up in operation; a measured PUE series would be the cleanest example. Retention means whether customers stay and expand after initial deployments; churn would be the cleanest example.

That grouped gap is the right ending, not a reason to dismiss the company. ClusterPower's public record is consistent with a serious Romanian data-centre operator trying to convert power, cooling, land and EU locality into a valuable capacity option. It is also consistent with a business still between first-phase proof and full-campus economics. A buyer reserving the megawatt before the rack is buying access to scarce infrastructure; the public record still leaves the economics, reliability and retention of that reservation partly private.

What would change the judgement

Several disclosures would materially sharpen the view without requiring private customer contracts to be published.

The first would be a commissioned-capacity statement by phase: powered shell, critical IT load, live racks, reserved capacity and expansion timing. That would turn the 200 MW narrative from a project claim into a measurable buildout story.

The second would be a power and cooling evidence pack: firm grid import terms, on-site generation capacity, energy pricing structure, measured efficiency and operational incidents. That would show whether ClusterPower's power promise is economic and resilient under real load.

The third would be commercial retention evidence: customer-segment mix, renewal behavior, expansion bookings and concentration boundaries. That would reveal whether the reserved megawatt has become a durable recurring unit or remains a credible first-phase offer still waiting for broader demand.

Until those disclosures appear, ClusterPower should be read neither as a 200 MW fully proven hyperscale campus nor as an empty ambition. It is a power-led Romanian data-centre business with a first phase, ambitious expansion claims, visible AI and colocation positioning, and a decisive evidence gap between the reserved megawatt promised to customers and the megawatt publicly shown as live, utilized, contracted capacity.

Public evidence reviewed

- ClusterPower services catalog PDF: https://clusterpower.ro/wp-content/uploads/2022/10/cluster-power-cataloge-oct.pdf

- ClusterPower AI microsite and current sitemap target: https://ai.clusterpower.com/

- ClusterPower project page paths used for historical project claims, with

.roWordPress equivalents prioritized where available and several.compaths observed as moved or returning 404 during this pass: https://clusterpower.ro/clusterpower-builds-200mw-data-centre-in-romania/ and https://clusterpower.com/clusterpower-builds-200mw-data-centre-in-romania/ - ClusterPower state-aid and entrepreneur project disclosure path: https://clusterpower.ro/romanian-entrepreneurs-to-develop-first-hyperscale-data-center-in-the-region/

- ClusterPower launch-event path: https://clusterpower.ro/event/526/

- ClusterPower Tier III Design Accredited announcement path and Uptime link referenced from the AI site: https://clusterpower.ro/clusterpower-received-tier-iii-certification/ and https://uptimeinstitute.com/uptime-institute-awards/list/datacenter/cp1-data-center-1/1625

- ClusterPower NVIDIA DGX-ready colocation partner path: https://clusterpower.ro/clusterpower-becomes-nvidia-dgx-ready-colocation-partner/

- ClusterPower NVIDIA-accelerated infrastructure path: https://clusterpower.ro/clusterpower-offers-customers-in-romania-and-central-europe-nvidia-accelerated-infrastructure-to-speed-ai-workflows/

- Together AI Series B announcement listing ClusterPower in its cloud network: https://www.together.ai/blog/series-a2

- IEA Energy and AI executive summary: https://www.iea.org/reports/energy-and-ai/executive-summary

- Transelectrica network access mode page: https://www.transelectrica.ro/en/web/tel/modalitate-acces

- Transelectrica RET development plan 2024-2033: https://www.transelectrica.ro/en/web/tel/planul-de-dezvoltare-ret-2024-2033

- Public DNS lookups run on 2026-07-06 for

clusterpower.com: Cloudflare nameservers, Microsoft mail protection, SPF and verification TXT records, and an A record at198.202.211.1; used only as bounded public-surface evidence.