Summary

- What it says: Tejays Dynamic and the Price of Reliability Between India's Mobile Bargain and Enterprise Internet

- Main topic: Telecom spectrum and security

- Context: Asia-Pacific regional ISP

The question starts with Rs.196, not with fibre

An Indian regional customer looking at Tejays Dynamic can ask a blunt question before any network diagram appears: if the national wireless market is carrying a user for Rs.196.04 a month, with average wireless data use at 26.70 GB and average data revenue realization of only Rs.7.51 per GB in the January-March 2026 quarter, why should a leased circuit, corporate broadband line, or point-to-point connection cost anything like enterprise money? TRAI's latest performance release gives the cheap-data side of the comparison (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2276780&lang=1®=3). Tata Tele Business, looking from the enterprise side, says a 100 Mbps smart leased line in India starts at Rs.40,000 a month, depending on fibre availability and SLA (https://www.tatatelebusiness.com/data-services/smart-internet/). Between those two numbers sits the commercial problem Tejays has to solve.

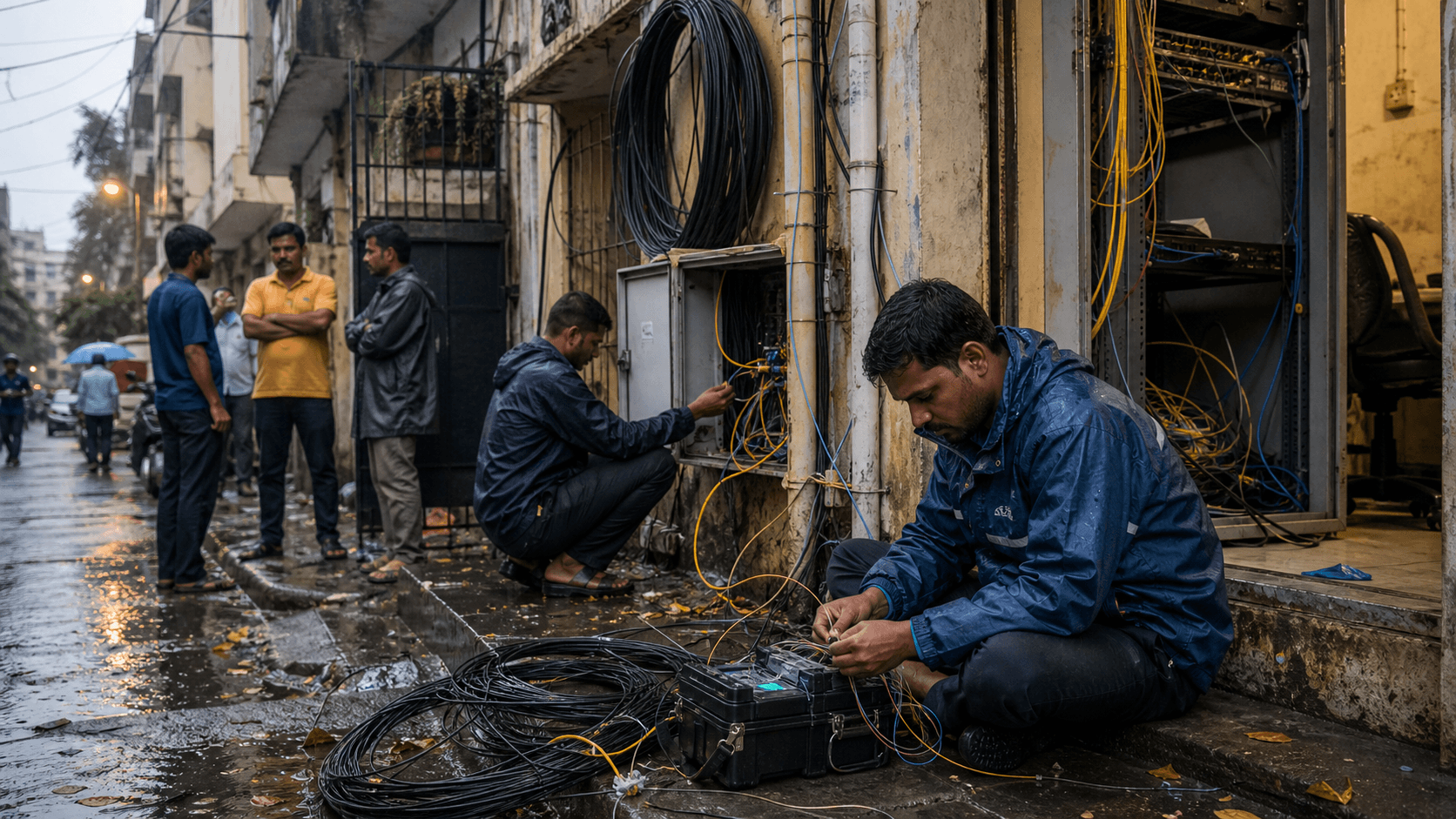

That gap is not a rhetorical flourish. The consumer can hold a mobile plan in one hand and a dedicated access quote in the other, then conclude that the operator is charging for mystery. The operator's answer has to be more concrete: a 1:1 line ties up access engineering, customer-premises equipment, monitoring, repair response, backhaul, power resilience, support labour, payment discipline, and often a route that is uneconomic if only one account sits at the end. Tejays' own site does not publish a tariff card in the open pages reviewed for this article, but it advertises a 99.5 percent uptime SLA, 24/7 proactive support, RF and fibre access options, and business services that include Internet Leased Line, corporate broadband, MPLS-VPN, point-to-point leased line, fibre on lease, and managed services (https://tejays.in/ and https://tejays.in/internet-lease-line/).

So the first judgement on Tejays is not whether it is a national challenger to Reliance Jio or Bharti Airtel. It is whether a Jaipur-headquartered regional network can make enough customers pay for reliability, fixed routing, and local operational accountability while the public memory of Indian internet pricing is shaped by mobile abundance. The market has 1.06588 billion broadband internet subscribers as of March 2026, according to the TRAI release, and wireless scale still dominates the national story (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2276780&lang=1®=3). A regional ISP has to sell into the minority of use cases where cheap shared data is visibly limited public evidence.

That is why Tejays is interesting. Its public footprint is too real to dismiss as a reseller brochure, but too thin to treat as a fully transparent infrastructure company. Its homepage claims more than 10,000 own subscribers, 18 PoPs across India, a Class-A service-provider posture, and a government-and-corporate presence (https://tejays.in/). Its about page raises the PoP claim to 40 OFC PoPs, says the company is headquartered in Jaipur with a corporate office in Gurugram, and describes tie-ups with system integrators, service providers, and regional business partners (https://tejays.in/about-us/). Those claims are not audited operational metrics, but they align with a business that is trying to occupy the difficult middle ground between household broadband and national carrier services.

The economics of that middle ground are unforgiving. A mobile network monetizes enormous pooled demand; a business-access operator often monetizes a specific building, campus, society, rural institution, branch office, or data centre need. A mobile plan can tolerate contention because the product promise is probabilistic. A leased line customer expects symmetric bandwidth, repair ownership, and a named escalation path. Tejays' public language repeatedly points to that distinction: dedicated bandwidth, ring topology, low latency, 24/7 support, proactive monitoring, and handling installation and ongoing management for enterprise links (https://tejays.in/point-to-point-lease-line/ and https://tejays.in/managed-services/).

A Jaipur network with a business-facing vocabulary

Tejays Dynamic Limited presents itself as a networking company rather than a pure retail broadband brand. The official site says the company was started by professionals from information technology and telecommunications, and it describes the business as a provider of wireless and wireline networking infrastructure, solutions, and services in India (https://tejays.in/about-us/). Its menu is revealing: under ISP services it lists broadband, bulk bandwidth, point-to-point leased line, managed services, peering, DoT compliance and licensing, IPTV, and OTT; under corporate services it lists Internet Leased Line, corporate broadband, MPLS-VPN, point-to-point leased line, managed services, fibre on lease, security and surveillance, WiFi, and networking solutions (https://tejays.in/quick-pay/).

The corporate identity is supported by public company-data pages, though those pages do not agree on every detail. Tracxn identifies Tejays Dynamic Limited with CIN U74900RJ2013PLC043940, incorporation in September 2013, ROC Jaipur registration, active status, website tejays.in, and FY2024 revenue of Rs.18.5 crore (https://tracxn.com/d/legal-entities/india/tejays-dynamic-limited/__ZGrTcIUtSLTCEbLAHTXqb-uOs_1PZJg_AKRTWIqlpf8). The Company Check describes it as an active public limited company in Jaipur, with the same CIN, a registered address at C-84, Janpath, Lal Kothi Tonk Road, and 2024 filings, while presenting different capital figures from Tracxn (https://www.thecompanycheck.com/company/tejays-dynamic-limited/U74900RJ2013PLC043940). The discrepancy matters because it warns against pretending that third-party profiles settle ownership, capital, or director history.

The company-facing pages are more useful for the operating model than for legal precision. Tejays says it serves educational institutes, large enterprises, SMEs, rural development initiatives, ISPs, telecom majors, and broadband service providers (https://tejays.in/about-us/). That customer list is broad, but it is coherent for a regional network that sells last-mile access, managed services, and wholesale or partner connectivity. A school, bank branch, rural programme office, logistics depot, small enterprise, and local cable operator all have different buying processes, but they share one requirement: someone must stand behind a local link when the cloud application, payment terminal, online class, CCTV feed, or branch VPN stops working.

The homepage client strip also gives a clue, not a proof. It displays logos or names associated with ACC, Bank of India, Domino's, Flipkart, NIMS, Punjab National Bank, SBI, Suzlon, and Amazon (https://tejays.in/). Without contract details, those logos cannot be converted into revenue, tenure, or direct customer relationships. They do, however, show the audience Tejays wants prospective buyers to imagine: institutions and distributed businesses, not only households comparing monthly broadband bundles. That positioning matters because the customer most likely to accept a higher monthly bill is the one that values operational loss avoidance more than raw gigabytes.

LinkedIn repeats a similar service description, listing ILL, FTTH, IPTV, SD-WAN, WiFi, indoor LAN and outdoor WAN integration, tower installation, P2P/P2M installation and maintenance, rural or VPN connectivity, network integration, and advanced IP routing (https://in.linkedin.com/company/tejays-dynamic-limited). A public LinkedIn page is not a technical inventory, but its emphasis is consistent with the official site and with Tejays' registry footprint. This is a company selling connectivity as a managed local outcome: get the site lit, keep the link watched, provide enough routing competence, and use partners where the company does not own every asset.

The public network record is larger than the brochure

The strongest evidence that Tejays is more than a local broadband wrapper is AS55507. APNIC's public WHOIS record identifies AS55507 as TEJAYS-AS, described as Tejays Dynamic Limited, country IN, with maintainer MAINT-IN-TEJAYS and IRT-TEJAYS-IN (https://wq.apnic.net/apnic-bin/whois.pl?object_type=aut-num&searchtext=AS55507). APNIC RDAP gives the same autonomous-system number, records registration on 5 May 2010, and lists Tejays contact data tied to the C-84 Janpath, Lalkothi Scheme, Tonk Road address (https://rdap.apnic.net/autnum/55507). That network registration predates the 2013 company incorporation date reported by public company-data aggregators, which suggests either a predecessor operating context, a legacy resource path, or a corporate-history detail not fully visible in the open records.

The IP-space evidence adds weight. APNIC RDAP for 45.114.144.0/22 names TEJAYS, describes the resource as allocated portable, and places it in India with Tejays contact information (https://rdap.apnic.net/ip/45.114.144.0/22). BGP tools show AS55507 originating multiple Indian IPv4 prefixes, including 45.114.144.0/22, 45.119.88.0/22, 103.23.118.0/23, 103.229.78.0/23, 103.243.88.0/23, 180.200.240.0/23, 182.237.16.0/23, and 182.237.18.0/23, with RPKI-valid indicators on several ranges (https://bgp.tools/as/55507). Hurricane Electric's BGP page reports 17 IPv4 prefixes originated, 7,168 IPv4 addresses originated, six observed IPv4 peers, and five internet exchange entries for AS55507 at the time viewed (https://bgp.he.net/AS55507).

There is also a related AS135694 record under the Tejays umbrella. PeeringDB lists "Tejays Industries" as AS135694, associated with Tejays Dynamic Ltd. and the older tejays.co.in website, though it shows no current prefixes or exchange points in that profile (https://www.peeringdb.com/net/12619). APNIC RDAP identifies AS135694 as TEJAYS-AS, country IN, registered in September 2016, again using Tejays-related contact structures (https://rdap.apnic.net/autnum/135694). A separate APNIC RDAP record for 103.87.168.0/22 names TIPL and uses a tejays.co.in contact at a Jaipur address (https://rdap.apnic.net/ip/103.87.168.0/22). The public record therefore points to a Tejays family of resources, not just one isolated ASN.

PeeringDB turns that registry evidence into an operating map. Its AS55507 page identifies Tejays Dynamic, also known as TejaysOnline, with website tejays.in, network type Cable/DSL/ISP, traffic level 10-20 Gbps, an open peering policy, and an AS-set listed as AS135694:AS-SET-TEJAYS (https://www.peeringdb.com/net/11676). The PeeringDB API repeats those fields and timestamps the network profile as created in 2016 and updated in February 2025 (https://www.peeringdb.com/api/net/11676). This is not a hyperscale profile; it is a mid-sized eyeball and access network showing enough public routing hygiene to matter.

The exchange-port evidence is specific. PeeringDB's IX LAN API lists Tejays connections at DE-CIX Mumbai with a 3 Gbps speed entry, Extreme IX Delhi at 1 Gbps, NIXI Delhi at two 1 Gbps IPv4 entries, NIXI Mumbai at 1 Gbps, and NIXI Kolkata at 1 Gbps (https://www.peeringdb.com/api/netixlan?net_id=11676). The Hurricane Electric page lists the same exchange geography: DE-CIX Mumbai, Extreme IX Delhi, NIXI Delhi, NIXI Kolkata, and NIXI Mumbai (https://bgp.he.net/AS55507). The IXP Manager export for The IXP shows Tejays Dynamic Ltd as AS55507, member since 12 October 2018, peering policy open, active connection, and a route-server-enabled VLAN using 103.27.170.29 and 2401:7500:fff6::29 (https://ixpmanager.theixp.net/api/v4/member-export/ixf/0.6).

That matters commercially. A small ISP that participates at exchanges can reduce transit load, improve latency to content and networks present at those IXPs, and make its own network more attractive to wholesale or enterprise customers who care about path stability. Peering is not free; it involves port fees, cross-connects, router capacity, engineering time, and monitoring. But it is one of the few tools a regional operator has to change its cost curve. Tejays' public peering record suggests that it is trying to buy and engineer around transit dependency rather than simply resell upstream bandwidth.

The Ciena announcement says the ambition is wholesale-grade

The most explicit technology signal came in February 2025, when Ciena announced that Tejays was working with it to build an adaptive IP network for enterprise and campus customers (https://www.ciena.com/about/intelligence team/press-releases/tejays-picks-ciena-to-modernize-and-automate-ip-network). The announcement said Tejays would converge 4G/5G fronthaul, mid-haul, and backhaul networks onto a common multipurpose infrastructure while enabling wholesale connectivity. It also named Ciena coherent routing, XGS-PON and 25GS-PON, 3926, 3948, 5130, 5164, 5186, and 8114 routers, WaveLogic 5 Nano coherent pluggables, and Navigator Network Control Suite for monitoring, automation, analytics, and multi-layer performance optimization.

Vendor announcements have a promotional purpose, but they also reveal the type of problem a company thinks is worth solving. Tejays did not announce a consumer-plan refresh. It announced routing, access, and monitoring tools for enterprise, campus, mobile transport, edge bandwidth, and wholesale connectivity. The product list reads like an attempt to make a regional network denser and easier to operate, not merely faster in headline terms.

It also points to a capital and skills requirement: coherent routing, PON evolution, router deployment, and a control suite require trained staff, spares discipline, configuration control, and a support model that can survive Indian last-mile realities.

The Ciena deal also helps explain why Tejays would care about both enterprise customers and ISP partners. If the network can aggregate campuses, broadband customers, local access partners, and perhaps small wholesale flows over a more modern IP layer, the incremental cost of another customer improves only if the company has enough demand near its PoPs. That is the core arithmetic of regional networks: fibre and routers are lumpy, but revenue arrives in small contracts.

A 40-PoP claim may sound large on a website; financially, it becomes useful only when each PoP can attract enough paying links to cover space, power, backhaul, support, and capital recovery.

The public facilities list supports the idea that Tejays uses third-party data-centre and carrier facilities rather than owning every heavy asset. PeeringDB's facilities API lists Tejays at Sify Greenfort Noida, Sify Rabale Mumbai, Sify Vashi Mumbai, Sify ITPL Bangalore, Sify Tidel DC Chennai, Sify Banjara Hills Hyderabad, and Sify-DLF Kolkata (https://www.peeringdb.com/api/netfac?net_id=11676). That is a rational pattern for a regional operator seeking national reach: buy colocation and interconnection where scale demands it, use regional access and partner relationships where proximity matters, and avoid building a full national facilities estate.

The risk is that this model can get squeezed from both sides. The regional ISP pays for upstreams, exchange ports, colocation, backhaul, last-mile work, and support, while the customer compares the invoice with a mobile plan or a mass-market fibre bundle. A national operator can cross-subsidize local offers, bundle mobile and fixed access, and absorb churn. A hyperlocal provider can undercut on price with lower overhead and a narrower footprint.

Tejays' strongest defence is not being the cheapest; it is being credible enough on support, routing, local installation, and enterprise handling that customers who cannot afford downtime do not treat the link as a commodity.

Why cheap data does not erase local ISP economics

TRAI's 2026 data sharpen the contrast. India had 1.06588 billion broadband internet subscribers at the end of March 2026, and total wireless mobile plus fixed-wireless-access subscriptions increased from 1.25877 billion to 1.28233 billion during the quarter (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2276780&lang=1®=3). That scale keeps unit data prices low and conditions customers to expect more bandwidth for less money each year. It also makes the visible consumer internet market look almost fully served by national platforms.

But a broadband subscriber count is not the same as a business-grade access estate. Wireline subscribers increased to 48.25 million at the end of March 2026, according to the same PIB release, far smaller than the wireless base (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2276780&lang=1®=3). That difference is where regional fixed operators live. They are not selling a better version of mobile data; they are selling physical access, symmetric throughput, contention control, static addressing or routing options, and accountability. Jio's business leased-line page states the distinction plainly: a leased line is dedicated, un-contended, symmetric, and different from shared broadband (https://www.jio.com/business/services/connectivity/internet-leased-line/). Airtel's business page similarly segments 10 Mbps, 50 Mbps, 100 Mbps, 150 Mbps, 200 Mbps, and 1 Gbps leased-line options by office size and use case (https://www.airtel.in/b2b/internet-leased-line).

For Tejays, the pricing logic is therefore less about selling megabits than selling non-shared responsibility. Its ILL page says the service is dedicated and symmetric, enters customer premises through ring topology for better uptime and redundancy, and uses tie-ups with major telecom partners for competitive pricing and quicker delivery (https://tejays.in/internet-lease-line/). Its corporate broadband page speaks of dedicated internet lines, performance for cloud, video conferencing, point-of-sale transactions, and continuous monitoring (https://tejays.in/corporate-broadband/). Its P2P leased-line page promises dedicated bandwidth, security, reliability, low latency, clear channel, and 24/7 support (https://tejays.in/point-to-point-lease-line/).

The common word is "dedicated." That word has a cost base. If a customer wants 50 Mbps or 100 Mbps available at a branch every business hour, Tejays must reserve capacity through the access network, provision equipment, watch alarms, respond to faults, and manage contention elsewhere. If a circuit runs over RF, weather, line-of-sight, spectrum environment, power, and tower access enter the economics. If it runs over fibre, duct access, splice quality, building permissions, pole or trench permissions, and restoration risk matter.

If Tejays uses a partner last mile, it inherits the partner's delivery discipline and must still face the customer.

The company's refund and cancellation policy makes some of those cost categories visible. It says installation charges, activation fees, one-time wiring, devices, and visiting charges are non-refundable, and that refunds are not provided for temporary downtime from maintenance activity, fibre cuts, power outages, natural calamities, and reasons beyond company control (https://tejays.in/refund-return-cancellation-policy/). The terms page says services depend on network infrastructure and technical feasibility, activation may require equipment at the subscriber premises, speed can vary due to network conditions or external factors, payments must be made before due date to avoid interruption, and routers, ONU/ONT, or CPE may be company-owned or rented (https://tejays.in/terms-conditions-tc/). Those are ordinary ISP clauses, but they describe the business: local physical work, recurring collection, equipment risk, and exceptions to perfect service.

The last mile is where national policy meets wet pavement

India has tried to make telecom infrastructure deployment easier, but the very existence of those reforms shows why a regional ISP's cost base is not trivial. In August 2022, the Ministry of Communications said right-of-way approval time had fallen from 435 days in 2019 to 16 days in July 2022 after reforms and the Gati Shakti Sanchar Portal (https://www.pib.gov.in/PressReleasePage.aspx?PRID=1854472). The same release capped state and union-territory administrative fees for poles at Rs.1,000 per pole and overground optical fibre at Rs.1,000 per kilometre, while reducing the bank guarantee for self-restoration from 100 percent to 20 percent of restoration cost. Those reforms lower friction, but they do not make civil work, building access, or restoration free.

The 2025 National Broadband Mission 2.0 announcement reinforces the point. It says the Gati Shakti Sanchar Portal was launched to streamline right-of-way permissions for optical fibre and tower setup, that the Telecommunications Right of Way Rules 2024 introduced uniform charges from 1 January 2025, and that BharatNet had 214,323 gram panchayats service-ready as of 13 January 2025 (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2102796&lang=1®=3). It also mentions telecom assets mapped on PM Gati Shakti's National Master Plan along with more than 1,600 layers from ministries and departments. A regional operator benefits from this environment, but it still has to execute street-level work.

Tejays' own image brief for itself, if one were to infer it from the website, would not be a clean map of India. It would be a splice tray, a rooftop RF unit, a small rack, a field team waiting for building access, and a NOC phone that rings when a branch VPN drops. The company says it offers RF and fibre options, contrasts them with copper, LAN, or coaxial approaches, and emphasizes upload and download reliability (https://tejays.in/). It says broadband can be provided by RF or fibre across India, depending on customer requirements and local availability (https://tejays.in/broadband/). That flexibility is useful, but it also means Tejays is managing a heterogeneous access plant.

Power and weather are part of the calculation even when they are not named in a tariff. Rajasthan heat, monsoon disruptions, local digging, accidental fibre cuts, and backup-power discipline all convert into truck rolls, overtime, spares, and customer credits or disputes. The company can write exclusions for natural calamities and power outages, but a business customer will still judge the provider by restoration behaviour. That is why the support claims on Tejays' site are not decorative. In a regional ISP, support is both product and cost centre.

The DoT's Unified License agreement also keeps compliance in the cost stack. It requires tariffs to follow TRAI orders and publication or information directions, sets a one-time non-refundable entry-fee structure, and states that annual license fee is 8 percent of adjusted gross revenue, inclusive of a 5 percent Universal Service Obligation levy (https://www.saras.gov.in/main/License%20Agreement/Unified%20Licence.pdf). The DGT page explains that Internet Service authorisation under the Unified License can be Category-A with all-India jurisdiction, Category-B within a service area, or Category-C within a secondary switching area (https://dgtelecom.gov.in/type-of-licenses/). Tejays' public claim to Class-A status should be read against that licensing framework, even though the reviewed open pages do not provide a downloadable licence certificate.

Upstream dependency is visible, and so is the attempt to reduce it

The most obvious dependency in the public routing record is Tata Communications. BGP.tools lists AS4755, Tata Communications, as the single upstream for AS55507 at the time viewed, while also showing peers that include Sify, Bharat Datacenter, Telstra International, Google, Reliance Jio Infocomm, and others (https://bgp.tools/as/55507). IPinfo similarly reports one upstream, Tata Communications, and peers including Tata, Sify, and Reliance Jio (https://ipinfo.io/AS55507). Hurricane Electric's view shows Tata Communications as the top IPv4 peer and lists Reliance Jio, Sify, Telstra Global, Instalinks, and Bharat Datacenter among observed peers (https://bgp.he.net/AS55507).

A single-upstream reading should not be over-interpreted. BGP visibility varies by collector, route policy, and moment. Tejays' own ILL page says it has tie-ups with major telecom partners, not only one carrier (https://tejays.in/internet-lease-line/). Still, the public data suggest that transit concentration is a real watchpoint. If a regional ISP depends heavily on one upstream for global reach, its enterprise reliability story rests partly on that supplier's pricing, outage behaviour, and commercial terms. Peering helps with traffic that can be exchanged locally; it does not replace all upstream transit.

The exchange footprint is the counterweight. DE-CIX Mumbai, Extreme IX Delhi, NIXI Delhi, NIXI Mumbai, and NIXI Kolkata give Tejays a way to localize traffic flows and reduce the burden on paid transit for reachable networks (https://www.peeringdb.com/api/netixlan?net_id=11676). Its open peering policy helps if content networks, cloud edges, regional ISPs, or partner networks are willing to exchange traffic. The peering page on Tejays' own site describes the benefits in business terms: fewer hops, reduced latency, bypassing congested paths, lower reliance on third-party transit providers, and multiple peering points to reduce single points of failure (https://tejays.in/peering/). That is exactly the right economic argument for a regional network.

The harder question is whether Tejays has enough traffic volume to make those ports efficient. PeeringDB lists traffic at 10-20 Gbps (https://www.peeringdb.com/net/11676). In Indian terms, that is a real network but not a giant one. A 3 Gbps DE-CIX Mumbai port and several 1 Gbps NIXI or Extreme IX ports can help performance and cost, but they also need utilization to justify engineering attention. Too much underused interconnection becomes fixed cost; too little interconnection leaves the network exposed to transit price and path quality.

Supplier dependency also appears in the modernization path. Ciena may improve Tejays' network capability, but introducing named vendor platforms can create training, spares, upgrade, and support dependencies (https://www.ciena.com/about/intelligence team/press-releases/tejays-picks-ciena-to-modernize-and-automate-ip-network). That is not a criticism; all operators have vendor dependencies. The point is that a regional ISP attempting enterprise-grade reliability must behave like an infrastructure operator. Cheap routers, ad hoc monitoring, and informal field practices do not scale into campus, wholesale, and backhaul use cases.

Customer dependency is the other side of the same ledger

Tejays' customer set appears fragmented across consumer, SME, enterprise, institutional, wholesale, and partner channels. That fragmentation can reduce dependence on one buyer, but it can also make collections and service management harder. The terms page says charges may be billed monthly, quarterly, or annually and that payments must be made before due date to avoid service interruption (https://tejays.in/terms-conditions-tc/). The refund policy says all dues must be cleared before disconnection and that security deposits may be returned after company-owned equipment is returned in good condition (https://tejays.in/refund-return-cancellation-policy/). Those clauses matter in a market where small business cash flow and local billing discipline can decide whether a technically sound link is commercially sound.

The Tejays homepage's claim of more than 10,000 own subscribers is therefore less important as a trophy than as a density indicator (https://tejays.in/). If the subscribers are concentrated around profitable PoPs and can be served with efficient access loops, they improve operating leverage. If they are scattered, low-ARPU, support-heavy, or dependent on partner networks, they can consume attention without generating enough margin. The public record does not disclose subscriber ARPU, churn, enterprise mix, or wholesale revenue, so the subscriber number is a starting clue rather than a valuation metric.

The company's service pages point to a strategy of moving up the value ladder. Bulk bandwidth is positioned for businesses, data centres, educational institutions, and entities that demand scalable connectivity (https://tejays.in/bulk-bandwidth/). Managed services cover monitoring, maintenance, troubleshooting, security, backup, disaster recovery, vendor management, and capacity planning (https://tejays.in/managed-services/). Fibre on lease is aimed at businesses and service providers that want dedicated fibre without bearing upfront installation and maintenance responsibilities (https://tejays.in/fiber-on-lease/). These are higher-touch products. They can improve margin if delivered well, but they also expose the operator to support quality and project execution risk.

The public customer testimonials on the homepage are modest but thematically useful. They mention supportive staff, constant speed, complaint resolution within a few hours, and 24/7 customer service (https://tejays.in/). Because they are company-selected testimonials, they do not establish average customer experience. They do show what Tejays believes sells: not the most spectacular headline speed, but responsiveness and service continuity. In regional broadband and enterprise access, that is usually the real battleground.

Unofficial market chatter points in the same direction from outside the company. A Reddit networking thread about Indian leased-line pricing captures buyer confusion over why 100-200 Mbps, 1 Gbps, and 10 Gbps dedicated links can differ so sharply from consumer broadband and from each other; one response reduces the issue to two different products and markets, while the original poster argues that the real cost lies in switching gear and SLA (https://www.reddit.com/r/networking/comments/1dfaolo/leased_line_prices_makes_no_sense_to_me/). A Jaipur broadband thread is not about Tejays, but users comparing ACT, Jio, Airtel, and Tata Sky focus on downtime, support, real speeds, ping, and installation promises, not only plan price (https://www.reddit.com/r/jaipur/comments/i2shm2/act_fibernet_reviews_in_jaipur/). That is the market psychology Tejays has to monetize.

Competition comes from carriers, cable operators, and the customer's fallback plan

Tejays competes upward against national operators that can sell mobile, FTTH, enterprise leased line, MPLS, SD-WAN, cloud, security, and IoT under one account structure. Jio's business ILL page emphasizes dedicated bandwidth, enterprise SLA, dual-stack IP, up to 100 Gbps bandwidth, digital self-care, multiple last-mile options, BGP support, and over 1,000 Jio Centers (https://www.jio.com/business/services/connectivity/internet-leased-line/). Airtel says its leased-line connectivity is trusted by more than 35,000 customers and segments speeds from 10 Mbps to 1 Gbps for different office sizes (https://www.airtel.in/b2b/internet-leased-line). Those claims are designed to make a regional provider look small.

It also competes downward against local broadband and cable networks that may have lower prices, looser service terms, and neighbourhood relationships. In some buildings, the incumbent cable or fibre operator controls access. In some industrial clusters, a local provider may respond faster than a national account desk. In some rural or semi-urban settings, wireless local loops or partner arrangements may be the only practical route. Tejays' answer is to be local enough to execute and technical enough to handle enterprise or wholesale requirements.

Competition also comes from customer substitution. A small office can use two mobile 5G routers, a consumer FTTH line, and a backup SIM rather than buying a dedicated circuit. That arrangement may be good enough for email, light SaaS, and WhatsApp-heavy operations. It fails when the business needs stable upload, static addressing, low jitter, monitored uptime, CCTV backhaul, payment uptime, or branch-to-branch control. Tejays has to find customers for whom failure is expensive enough that the price of assurance is rational.

The Ciena announcement suggests Tejays wants to serve exactly those customers: enterprise, campus, mobile transport, wholesale, 5G, broadband, and cloud applications at the edge (https://www.ciena.com/about/intelligence team/press-releases/tejays-picks-ciena-to-modernize-and-automate-ip-network). If Tejays can win institutions, campuses, regional ISPs, and distributed enterprises that value local delivery, the company's scale can be enough. If it drifts toward price-led residential broadband, it faces the worst version of the market: high support expectations, low willingness to pay, and national brands that can price aggressively.

The strongest competitive defence in the public record is the combination of registry independence and local service packaging. Owning and originating IP resources under AS55507 gives Tejays more control than a pure reseller (https://rdap.apnic.net/autnum/55507). Participating in multiple exchanges improves the performance story (https://www.peeringdb.com/net/11676). Offering managed services, peering, bulk bandwidth, fibre lease, and corporate connectivity gives it more than one revenue line (https://tejays.in/managed-services/ and https://tejays.in/fiber-on-lease/). None of these guarantees margin, but together they describe a company with an operating thesis.

Regulation rewards discipline but punishes weak operations

Indian telecom regulation is not just a licence hanging on the wall. For an ISP, it shapes tariff publication, lawful operations, security conditions, revenue reporting, and quality expectations. The Unified License agreement requires compliance with TRAI tariff orders and information publication directions, and it imposes the 8 percent AGR-based licence fee inclusive of the USO levy (https://www.saras.gov.in/main/License%20Agreement/Unified%20Licence.pdf). The DGT license page's Category-A, B, and C structure also matters because jurisdiction determines how widely an ISP can operate under its authorisation (https://dgtelecom.gov.in/type-of-licenses/).

Tejays advertises DoT compliance and licensing as a service category (https://tejays.in/). That is notable. A company that helps others with compliance may have a useful internal capability, or at least a sales story aimed at smaller operators and service providers. But it also means public trust depends on clarity. Tejays' own terms say all tariff plans are published on the company website as per TRAI regulations (https://tejays.in/terms-conditions-tc/). In the public pages reviewed for this article, product descriptions were visible but a simple current tariff table was not easily found. For a company seeking enterprise credibility, clearer public tariff and SLA documents would reduce uncertainty even if final leased-line pricing remains site-specific.

TRAI's quality-of-service framing adds another pressure. The January-March 2026 performance release lists wireline, wireless, and broadband wireline QoS benchmarks, including latency, packet drop, bandwidth utilization to ISP gateway or internet exchange links, jitter, billing-complaint resolution, and call-centre accessibility (https://www.pib.gov.in/PressReleasePage.aspx?PRID=2276780&lang=1®=3). Tejays' 99.5 percent uptime claim is a commercial promise, but the broader regulatory environment increasingly expects measurable service behaviour. If the company wants to sell enterprise reliability, it benefits from publishing more of its own measurable operating record.

Geopolitical risk is quieter but present. Telecom networks in India sit under security, lawful interception, equipment, routing, and data-handling expectations. The Ciena relationship is with a US-headquartered network vendor; the national regulatory environment is concerned with trusted infrastructure, domestic resilience, and critical connectivity (https://www.ciena.com/about/intelligence team/press-releases/tejays-picks-ciena-to-modernize-and-automate-ip-network). That does not create a visible Tejays-specific problem. It does mean that a regional ISP moving into enterprise, campus, wholesale, and possibly mobile-transport roles must maintain stronger governance than a neighbourhood broadband provider.

There is also public-record risk from inconsistent open data. Tracxn reports FY2024 revenue of Rs.18.5 crore and paid-up capital of Rs.2.5 crore (https://tracxn.com/d/legal-entities/india/tejays-dynamic-limited/__ZGrTcIUtSLTCEbLAHTXqb-uOs_1PZJg_AKRTWIqlpf8). The Company Check reports paid-up capital of Rs.6 crore, authorised capital of Rs.15 crore, open charges, director names, and FY2024 filing details (https://www.thecompanycheck.com/company/tejays-dynamic-limited/U74900RJ2013PLC043940). Because these are secondary aggregators and not the full MCA filings themselves, the prudent reading is directional: Tejays appears active, financed, and operational, but the public financial picture is not clean enough to support precise margin claims.

The judgement turns on operating density

The case for Tejays is that it has the ingredients of a defensible regional connectivity company. It has public ASN and address resources, visible peering, claimed PoPs, a service menu that extends beyond household broadband, institutional and enterprise positioning, a national facilities footprint through Sify locations, and a modernization announcement with Ciena. It operates in a country where fixed business connectivity remains a small and valuable layer above mass wireless data, and where every cloud migration, campus digitization, payment terminal, surveillance deployment, and branch network increases dependence on reliable access.

The case against Tejays is that these ingredients do not automatically create profitability. Rs.18.5 crore of reported FY2024 revenue, if accurate, is not large relative to the ambition implied by 40 OFC PoPs, national facilities, Ciena routing, enterprise support, wholesale connectivity, and multi-city peering (https://tracxn.com/d/legal-entities/india/tejays-dynamic-limited/__ZGrTcIUtSLTCEbLAHTXqb-uOs_1PZJg_AKRTWIqlpf8). Even if revenue has grown, the model must cover field teams, colocation, upstream transit, exchange participation, support, capital equipment, licences, local permissions, billing operations, and bad debt. A regional operator can look technically credible and still struggle if customer density is too thin.

The most important public fact that would change this judgement is a current audited revenue split by line of business: retail broadband, Internet Leased Line, point-to-point circuits, bulk bandwidth, fibre lease, managed services, government projects, ISP wholesale, and any telecom-major transport work. If that split showed that most gross margin comes from contracted enterprise, wholesale, and managed connectivity near existing PoPs, Tejays would look like a maturing regional infrastructure operator.

If it showed a heavy dependence on low-ARPU residential broadband scattered across weak-density areas, the same network evidence would look much less attractive.

A second useful fact would be churn and trouble-ticket performance by product. The homepage testimonials emphasize fast complaint resolution (https://tejays.in/). The Ciena announcement emphasizes monitoring and automation (https://www.ciena.com/about/intelligence team/press-releases/tejays-picks-ciena-to-modernize-and-automate-ip-network). But public materials do not show mean time to repair, repeat-fault rates, SLA-credit history, uptime by product, or enterprise renewal rates. In this market, those figures are more valuable than another map. They show whether the service promise is being delivered at a cost the company can bear.

The third watchpoint is transit and peering evolution. If future public views show Tejays adding resilient upstreams, increasing exchange capacity where traffic justifies it, maintaining RPKI-valid resources, and using the Ciena upgrade to improve monitoring, then the company strengthens its reliability narrative. If public routing collapses toward a thin single-upstream pattern, or if peering entries grow stale, the enterprise story weakens. For now, the visible network record is better than the public financial record.

The final read is therefore cautiously positive but highly conditional. Tejays Dynamic is not just a name in a directory; it is an Indian regional network with AS55507, public peering, address resources, service pages, customer-facing support claims, company records, and a recent modernization story. Its commercial challenge is the hardest one in Indian fixed connectivity: convince customers trained by Rs.196 mobile ARPU and Rs.7.51-per-GB data economics that a reliable fixed circuit is a different product.

The company can win that argument only where downtime has a price, density is sufficient, and local execution is visibly better than the alternatives.

That is also why Tejays should be read as a middle-market infrastructure bet rather than a consumer internet story. The public facts support a company trying to stitch Jaipur-origin regional access, national interconnection, enterprise services, and partner-led coverage into a coherent operating model. The uncertainty is whether that stitching produces enough high-quality recurring revenue.

In a country where the cheap-data headline is true but incomplete, Tejays' opportunity is to sell the missing piece: accountable connectivity for customers who discover, usually during an outage, that cheap gigabytes are not the same as dependable service.