Summary

- What it says: Trans World Associates is where Pakistan's cheap data promise meets the hard economics of submarine cables, licensed international gateways, dollar-priced capacity and route diversity.

- Main topic: Regional ISP economics; Currency mismatch in infrastructure; Network-resource evidence; Wholesale access economics

- Context: market / company research report / Pakistan; Karachi; Islamabad; UAE; Oman; Asia-Europe submarine routes

Waiting for the sea, not another router

The revealing scene is not a household in Lahore waiting for a new Wi-Fi router. It is a Pakistani video platform watching stream quality degrade on a match night, a bank wondering whether payment traffic will stay usable, or a smaller ISP deciding whether to buy more international capacity before the evening peak. In those moments the retail brand on the customer bill matters less than the path out of Pakistan, the cable system carrying the traffic, the licensed gateway that can sell capacity, and the operator that can reroute enough load before users turn technical latency into commercial anger.

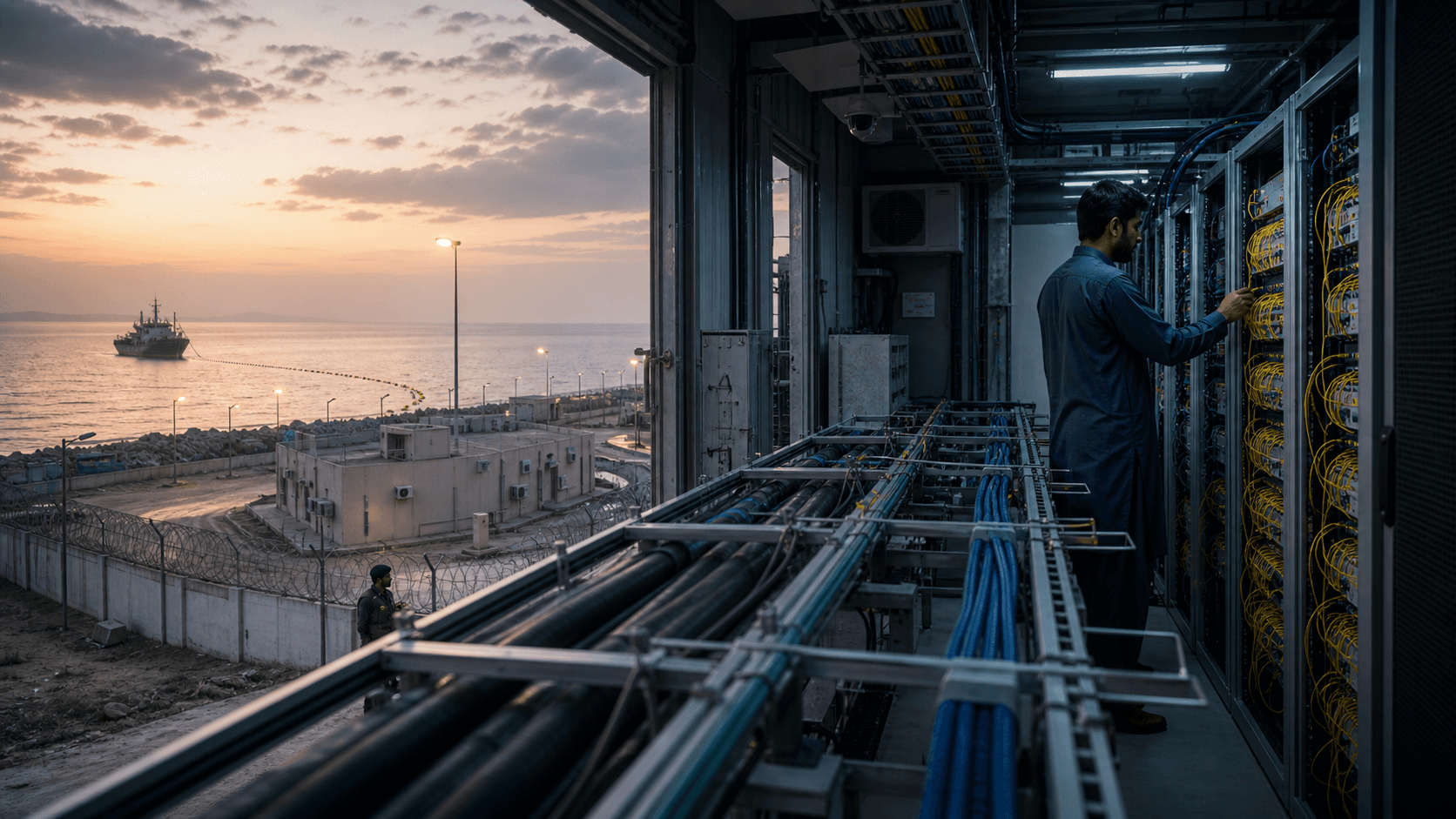

The bottleneck is under the sea and at the landing station, not in the living room.

That is where Trans World Associates (Pvt.) Limited, commonly marketed as Transworld or TWA, becomes economically interesting. The company describes itself as Pakistan's private-sector submarine fibre optic cable network provider, serving mobile operators, ISPs, enterprises and SMEs with high-speed international bandwidth (https://www.tw1.com/). PACRA's August 2025 credit report is more specific: it says TWA is incorporated in Pakistan, owns and operates a private submarine fibre optic cable system, owns and manages landing stations in Pakistan, and delivers bandwidth to telecom operators, ISPs and enterprises nationwide (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). The public identity is therefore not just "internet provider." It is a wholesale international-capacity business sitting between national demand and foreign routes.

The first hard number is the demand base that turns this into a toll-booth business. PTA's 2024-25 annual-report release says Pakistan surpassed 150 million broadband connections, telecom coverage exceeded 92%, data usage reached 27,727 petabytes in 2025, and the country had 17.21 Tbps of international bandwidth while adding four high-capacity submarine cables (https://www.pta.gov.pk/category/pta-releases-annual-report-2024%E2%80%9325-1374704410-2026-01-01). Those figures describe national broadband growth, but they also describe a cost problem. The data is consumed in Pakistani rupees by subscribers who are trained to expect cheap mobile and fixed internet. The cables, optical systems, peering ports, foreign points of presence, maintenance obligations and vendor equipment that make that data usable are priced through a more dollar-linked infrastructure economy.

This is the core mechanism. When mobile operators, ISPs, banks, content platforms and corporate networks sell more service, they create more international-capacity demand. A company with landing rights, cable capacity, LDI authority, global interconnection and domestic backhaul options can sell into that demand before it reaches the retail customer. It is not guaranteed monopoly profit, because PTCL, Cybernet, SCO, terrestrial routes and new cables all matter. But it is bargaining power.

Pakistan's retail broadband market can grow only if enough international capacity is activated, protected and bought at terms local service providers can pass through without breaking their own margins.

The July 2026 SEA-ME-WE 5 fault made the mechanism visible. Dawn reported that PTA was monitoring disruption on the SMW5 cable, that TWA was coordinating with the consortium, and that traffic was being rerouted through alternate international links to minimize service degradation (https://www.dawn.com/news/2012491/pta-says-submarine-cable-fault-may-cause-intermittent-internet-disruption). Business Recorder later reported PTA's statement that the fault had been rectified, internet services had returned to normal operating capacity, and PTA had coordinated with TWA during restoration and rerouting (https://www.brecorder.com/news/amp/40428352). An outage does not prove a company's long-run economics by itself. It does show the practical dependency: capacity is not an abstraction when a cable fault forces the country to lean on alternate routes.

For TWA, the opportunity is to monetize that dependency without becoming the weak point that everyone blames. The company's value rises when Pakistan needs more routes, more activated capacity, more secure enterprise circuits and more direct international interconnection. Its risk rises when a cable fault, dollar cost, regulatory intervention, supplier delay or customer concentration turns the same position into a national-service obligation. TWA is most profitably read as a capacity gatekeeper, not a consumer-ISP story.

Identity, ownership and the operating surface

The formal identity is unusually well supported for a private infrastructure company. PACRA says TWA was incorporated in Pakistan as a private limited company on October 1, 1980, and that its registered and head office is at 24, Retalia Building, G-6 Markaz, Islamabad (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). The same report identifies Junaid Iqbal as CEO and Saad Muzaffar Waraich as President, and describes a seven-member board with telecom, finance, banking and industrial-management experience. This matters because submarine capacity is not a thin software resale business. It requires governance, financing, regulatory management and counterparties who trust the operator to perform over long asset lives.

Ownership also matters. PACRA reports that Orastar Limited holds 90% of TWA and that the remaining 10% is held by the heirs of Dr. Omar Bin Abdul Muniem Al Zawawi, with Orastar described as a B.V.I. company managed by directors based out of Jersey (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). That offshore and Omani-linked ownership history should not be treated as negative by default. It is common for submarine-cable capital to involve cross-border sponsors. But it does mean that TWA's strategic identity is not purely domestic in the way a small local ISP's identity is domestic. It is a Pakistani operating company with international capital, international partners and international route obligations.

The company began operating in 2006, according to PACRA, and its principal activity is to establish and operate a telecommunication system and provide Long Distance and International services under a PTA licence (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). PTA's LDI licensee list shows Transworld Associates (Pvt.) Ltd. with LDI licence LDI-20-2023, issued on December 1, 2023, with date of operation April 3, 2024, and operational status marked operational (https://www.pta.gov.pk/assets/Licensing/6.pdf). This regulatory line is not decorative. It is the permission structure behind international voice and data gateway services, and it is part of why a downstream operator can buy from TWA rather than trying to assemble cross-border connectivity directly.

TWA's own product menu confirms the breadth of the operating surface. The homepage groups the business into carrier and wholesale services, enterprise and ICT solutions, and retail business (https://www.tw1.com/). The I-Connect page sells domestic MPLS connectivity across more than 72 cities, with layer 2 and layer 3 options and enterprise SLAs for activation, availability, latency, packet loss, jitter and restoration (https://www.tw1.com/service/i-connect/). The IPLC page sells clear-channel point-to-point international bandwidth for voice, data, internet or video traffic, with partnerships with Tier-1 global carriers and optional restoration through backup cable systems (https://www.tw1.com/service/iplc/). The LDI voice page says TWA is PTA-licensed, has direct interconnects to major Pakistani mobile networks and PTCL, operates points of presence in Islamabad, Lahore, Karachi, Marseille and Oman, and runs a 24/7 NOC (https://www.tw1.com/service/ldi-voice-services/).

This menu should be read as one economic system. The submarine cable gives route control. The LDI licence gives a regulated gateway position. Domestic MPLS and long-haul transport turn the foreign route into a sellable Pakistan service. Data centre and managed-service products deepen the customer relationship. Retail broadband through the wider Transworld group adds brand visibility, but the strategic profit pool is the wholesale and enterprise layer where capacity, resilience and service guarantees can be priced.

There is a risk of overclaiming. The company calls itself a Tier-1 provider in marketing language, and the phrase can mean different things in different markets. Public records do not prove that TWA has the same global status as the largest worldwide transit networks. They do support a more precise claim: TWA is a nationally important international-capacity operator in Pakistan with its own submarine system, LDI authority, visible interconnection, enterprise services and a financial profile large enough to be rated by PACRA.

The cable is the asset, but the landing is the leverage

TW1 is the foundation asset. Submarine Networks describes the TW1 system as a 1,300 km cable connecting Pakistan, the UAE and Oman, privately owned and operated by Transworld Associates, with landing points in Karachi, Al Seeb and Fujairah, two fibre pairs, initial design capacity of 1.28 Tbps, fourteen repeaters on the Fujairah-Karachi trunk, and operations beginning in 2006 (https://www.submarinenetworks.com/en/systems/intra-asia/tw1). TWA's own article describes TW1 as Pakistan's privately owned submarine fibre optic cable connecting Karachi to the UAE and Oman, with redundancy linked to SEA-ME-WE 5 and regional systems (https://www.tw1.com/submarine-cable-superpower-how-transworld-associates-drives-pakistans-connectivity/).

The economic point is not only ownership of wet plant. It is the ability to turn a landing position into capacity customers can buy. A cable owner must maintain terminal equipment, upgrade optical layers, manage foreign landing partners, coordinate marine repair, keep route records clean, negotiate interconnection, handle customer SLAs and finance expansion before all demand is contracted. The physical route from Karachi to the Gulf becomes commercially valuable only when it is tied to activated wavelengths, upstream and peering choices, domestic backhaul, billing and support.

SEA-ME-WE 5 added a second layer. The SEA-ME-WE 5 consortium's 2016 announcement said the cable landed at Transworld's landing station in Karachi, and described Transworld as already operating TW1, the only private operator in Pakistan, with capacities on regional cables on eastern and western sides for route diversity and resilience (https://seamewe5.com/2016/09/state-of-the-art-high-speed-submarine-cable-sea-me-we-5-lands-at-transworld-landing-station-karachi/). That language matters because a single cable can be a strength and a vulnerability at the same time. The more TWA can sell diversity across multiple systems, the less it is just a TW1 story.

The next systems change the scale again. Pakistan's Press Information Department said in November 2025 that SEA-ME-WE 6 allocated 13.2 Tbps to Pakistan, with 4 Tbps activated immediately, supporting cloud services, data centres, fintech, e-commerce, streaming and the broader digital economy (https://pid.gov.pk/site/press_detail/31076). Dawn reported the same allocation and said the cable links Pakistan to countries between Singapore and France, with more than 100 Tbps of total system capacity (https://www.dawn.com/news/1956718). TWA's press page and industry reports also identify the company as tied to 2Africa's Karachi landing; TWA said 2Africa spans more than 45,000 km, connects 46 landing points across 33 countries and has capacity up to 180 Tbps on 16 fibre pairs (https://www.tw1.com/press-release/a-historic-moment-for-pakistan/), while the 2Africa project site gives the same 180 Tbps trunk-capacity figure (https://www.2africacable.net/about).

The landing-party role is strategically different from simply buying transit. If Pakistan gets more cable systems, the country gains route diversity and potential price competition. But a landing partner that can connect those systems to local customers, local data centres and domestic long-haul routes still controls a valuable interface. The toll booth metaphor is not a claim that TWA can charge anything it wants.

It means TWA sits at a point where many actors have to negotiate: global content networks seeking reach into Pakistan, Pakistani operators seeking foreign capacity, enterprises seeking private circuits, and regulators seeking resilience and security.

The bargaining power is strongest when customers need both capacity and assurance. A low-end reseller can buy ordinary internet access. A bank, exchange, mobile network, cloud customer or video platform needs latency, restoration, route diversity, security documentation and a reachable operations team. That is where landing station, cable route, global PoP and NOC become one bundle.

The revenue logic is wholesale first

PACRA gives unusually useful financial detail. TWA's topline reached about PKR 13,311 million in CY24, up 25.4% from about PKR 10,618 million in CY23 and PKR 8,744 million in CY22 (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). The report says carrier, international and wholesale segments were the main revenue drivers, while the corporate and enterprise segment also grew with managed-service offerings. In 6MCY25, PACRA says carrier contributed 41.9% of revenue, international business 17.4%, wholesale 29.7%, LDI voice 3.2%, and corporate and other sources 7.8%.

That revenue mix is the thesis in numbers. TWA's public story may include retail broadband and enterprise services, but the rated economics are overwhelmingly wholesale and international. Carrier, international and wholesale together accounted for nearly nine-tenths of 6MCY25 revenue in PACRA's segmentation. The business is therefore driven by other networks' need for capacity and route quality, not by a direct consumer relationship alone.

The margin logic follows. PACRA's financial summary shows CY24 sales of PKR 13,311 million, cost of goods sold of PKR 7,076 million, gross profit of PKR 6,235 million, operating profit of PKR 4,825 million and net income of PKR 2,241 million (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). The reported gross profit margin was 46.8%, down from 52.2% in CY23 and 52.4% in CY22, while net profit margin was 16.8%, slightly below 17.9% in CY23 and materially below 25.6% in CY22. A high gross margin confirms that capacity and managed infrastructure can be profitable. The margin compression warns that growth is not free: expansion, finance cost, tax, operations and competitive pricing absorb part of the benefit.

The same report says Pakistan's installed international bandwidth capacity, across operators including PTCL, TWA, SCO and Cybernet, stood at 16.4 Tbps, with activated capacity of 10.26 Tbps, and that PTCL and TWA remained dominant providers supplying the bulk of domestic demand (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). Even allowing for the fact that PTA's 2024-25 public release later cites 17.21 Tbps at sector level, the important distinction is installed versus activated. Installed capacity is an option. Activated capacity is the sellable resource. The economic question is not only how much fibre lands, but how quickly capacity is lit, contracted, routed and paid for.

This is why a cable boom can pressure margins even while it expands the market. New systems increase Pakistan's capacity and resilience. They also increase the amount of capacity that must find customers. If supply arrives faster than retail and enterprise demand can absorb it at good prices, wholesale rates can fall. If demand from streaming, cloud, AI workloads, fintech and mobile broadband rises faster than activated supply, TWA can defend price. The company's public investment case rests on the second outcome, but the first is always possible.

The downstream market is price-sensitive. Dawn's summary of PTA's 2023 report said Pakistan had some of the world's lowest telecom prices, a cost of 1 GB mobile broadband around 12 US cents, low ARPU, and operator pressure from fuel costs and high capital investment (https://www.dawn.com/news/1809693). PTA's 2024-25 release says the sector crossed PKR 1 trillion in revenue and US$ 838 million in investment, but that does not mean every end user can absorb higher tariffs (https://www.pta.gov.pk/category/pta-releases-annual-report-2024%E2%80%9325-1374704410-2026-01-01). The wholesale provider's challenge is to sell more capacity into a market where retail affordability is politically and commercially central.

Capacity is inventory before it is revenue

The most important commercial distinction is between capacity as an engineering possibility and capacity as monetized inventory. A cable may have large design capacity, an operator may have rights on a consortium system, and a national regulator may report aggregate international bandwidth. None of that automatically means the capacity is lit, sold, protected by restoration contracts and paid for by customers whose own revenue can carry the cost. TWA's business sits in that conversion process.

Installed capacity is like shelf space in a market where demand arrives unevenly. A mobile operator may need a large increase before a sports tournament, a streaming platform may need better quality during an entertainment season, a bank may need a private circuit for a new disaster-recovery site, and a cloud customer may need a low-latency path for a narrow application rather than a broad internet-transit uplift. TWA has to decide how much capacity to activate ahead of firm demand, how much to reserve for resilience, and how aggressively to price unused headroom. The wrong answer can be costly in either direction.

Too little activated capacity creates congestion and lost customer trust. Too much early activation can depress returns if downstream buyers wait for lower prices.

This is why the SEA-ME-WE 6 and 2Africa additions should not be read as a simple windfall. Pakistan's 13.2 Tbps SEA-ME-WE 6 allocation and immediate 4 Tbps activation expand the national opportunity (https://pid.gov.pk/site/press_detail/31076). The 2Africa system's 180 Tbps trunk-capacity story strengthens the sense that the regional supply ceiling is moving upward (https://www.2africacable.net/about). But new supply can produce two opposite outcomes. It can make TWA more valuable by giving the company more paths, more services and more negotiating room. It can also make wholesale capacity less scarce if several operators can offer acceptable alternatives.

The difference is productization. A raw terabit is not the same as a route-diverse enterprise service, a restored private circuit, a low-latency content path, a data-centre cross-connect or a managed WAN bundle. TWA's public product pages are important because they show an attempt to move capacity up the value chain. I-Connect turns domestic transport into managed MPLS with service classes and SLAs (https://www.tw1.com/service/i-connect/). IPLC turns global reach into dedicated point-to-point circuits with optional restoration (https://www.tw1.com/service/iplc/). KR-1 turns the landing-station advantage into a hosting and interconnection proposition (https://www.tw1.com/service/data-centre/). Managed Services turns the network into recurring operational support (https://www.tw1.com/service/managed-services/).

That bundling creates a different negotiation with customers. A small ISP buying bulk transit may push mainly on price per Mbps. A bank may push on restoration time, diversity and documentation. A content platform may push on latency to foreign caches, peering quality and evening congestion. A multinational may push on one-window contracting and clear escalation across countries. The same physical cable can support all of those sales, but each sale has a different margin, support burden and failure consequence.

The activated-capacity spread also gives TWA an option value. If Pakistan's traffic grows steadily, unused but reachable capacity can be turned into revenue without a full new cable build. If a rival cable fails, spare capacity can become temporarily more valuable. If a new cable floods the market, the option loses value unless attached to differentiated service. This is why the article's central question is not whether Pakistan needs more bandwidth. It does. The question is who controls high-quality, sellable, restorable bandwidth at the moment buyers need it.

The answer will vary by customer. For commodity internet access, TWA's bargaining power is limited by alternative suppliers and regulatory attention. For route-sensitive, security-sensitive, time-sensitive or reputation-sensitive buyers, the company has a stronger argument. It can sell not only capacity but reduced operational uncertainty: fewer foreign-vendor conversations, fewer route mysteries, fewer outage escalations and fewer internal procurement arguments about who owns the fault. In infrastructure markets, that reduction of uncertainty is often where the durable margin lives.

The cost base is a balance-sheet problem, not just an engineering problem

Submarine-capacity economics look clean from the outside: build or join a cable, light capacity, sell to operators. The balance sheet is less clean. PACRA says TWA's capital structure is leveraged, with borrowings primarily consisting of short- and long-term loans for working capital, network and capacity expansion (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). Its financial summary shows total assets of PKR 35,023 million at December 2024, non-current assets of PKR 26,677 million, borrowings of PKR 11,998 million, shareholders' equity of PKR 13,136 million, and total borrowings to total borrowings plus equity of 47.7%.

Those numbers are consistent with an infrastructure company in expansion mode. TWA needs capital before the customer fully pays. It also needs working capital after service is sold. PACRA reports CY24 trade receivables of PKR 5,106 million and a gross working capital cycle of 145 average days (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). A customer may think it is buying a monthly capacity service, but the operator is financing cable assets, optical equipment, landing-station facilities, domestic links, receivables and maintenance readiness.

The dollar-cost issue sits underneath those balance-sheet lines. Optical systems, submarine upgrades, foreign PoPs, international ports, vendor support, marine maintenance and many equipment inputs are exposed to foreign-currency economics even when Pakistani customers pay in rupees. That does not mean every cost is directly denominated in dollars. It means the replacement and expansion cost of the network is tied to an international technology supply chain. State Bank reporting showed how sharp the macro environment could be: the PKR depreciated 28.5% against the US dollar during FY23 (https://www.sbp.org.pk/reports/annual/aarFY23/Chapter-06.pdf). Even if the rupee later stabilizes, a provider that must keep buying and upgrading international infrastructure cannot ignore currency risk.

The company's 2025 announcements show why capex keeps returning. TWA said it signed an agreement with Huawei to upgrade its long-haul transport network using ROADM-based CDF technology supporting 400G and beyond per wavelength, with bandwidth capability exceeding 25.6 Tb/s and future L-band expansion (https://www.tw1.com/press-release/to-enhance-the-quality-and-capacity-of-internet-services-in-pakistan/). It also announced a partnership with Wateen under which Wateen would provide more than 6,000 km of long-haul fibre network, fibre operation and maintenance services, and co-location facilities to enable TWA's DWDM deployment across Pakistan (https://www.tw1.com/press-release/transworld-and-wateen-sign-strategic-partnership-agreement-to-expand-pakistans-digital/).

These are growth moves, but they are also cost commitments. More long-haul reach improves the ability to sell capacity outside Karachi and Islamabad. More optical capability increases the ceiling on traffic. More co-location and O&M arrangements reduce some build burden while adding supplier dependency. The operator's economics improve if that domestic reach converts submarine capacity into high-value customer contracts. They weaken if the network is upgraded faster than demand, or if aggressive wholesale competition forces TWA to use new capacity mainly to defend share.

The data-centre strategy adds another layer. TWA's KR-1 Data Centre page describes a Tier III Uptime Institute-certified facility with 99.982% availability, located at Pakistan's submarine cable landing station, with direct access to multiple submarine cables and 24/7 smart-hands support (https://www.tw1.com/service/data-centre/). Its January 2025 press note says its Karachi and Islamabad data centres achieved ISO 27001 certification (https://www.tw1.com/press-release/exciting-news-from-transworld-associates/). This turns the landing site into more than a cable hut. It becomes a place where customers may host, interconnect and buy lower-latency access to foreign networks. But data centres also require power, cooling, security, compliance, uptime discipline and capital.

TWA's best economics therefore come from bundling. A standalone megabit of wholesale bandwidth can be competed down. A package combining submarine routes, domestic backhaul, data centre interconnection, managed service, DDoS protection, private circuits and operational support is harder to compare. The question is whether enough customers value the bundle to offset the cost of building it.

Route diversity is the product when things fail

Pakistan's international connectivity problem is not only capacity volume. It is path concentration, repair uncertainty and geopolitics. Dawn's January 2024 report on PTA's annual report said Pakistan then had seven submarine cable connections, the Pak-China optical fibre cable, and 19 cross-border terrestrial links, with key international bandwidth players including PTCL, TWA, Cyber Internet Service Providers and SCO (https://www.dawn.com/news/1809693). PTA's 2024-25 release later says Pakistan is adding four high-capacity submarine cables while supported by 17.21 Tbps of international bandwidth (https://www.pta.gov.pk/category/pta-releases-annual-report-2024%E2%80%9325-1374704410-2026-01-01). More routes reduce fragility, but only if they are genuinely diverse in geography, landing, ownership, power, operations and upstream routing.

TWA's public interconnection evidence is strong. PeeringDB lists AS38193, Trans World Associates, as an NSP with 15,000 IPv4 prefixes, 3,000 IPv6 prefixes, selective peering policy, Asia Pacific scope, and public exchange presence including DE-CIX Frankfurt at 100G, Equinix Muscat at 10G, Equinix Singapore entries at 100G and 500G, HKIX at 10G, NL-ix at 100G, Oman-IX at 10G and SH-IX at 100G (https://www.peeringdb.com/net/3320). BGP.tools identifies AS38193 as a long-running Pakistan network with large peer and upstream visibility, though the exact counts change over time as routing observers update (https://bgp.tools/as/38193). APNIC whois identifies AS38193 as TWA-AS-AP, Transworld Associates (Pvt.) Ltd., country PK, with route export references to major networks including AS174, AS6762 and AS8529 (https://wq.apnic.net/apnic-bin/whois.pl?object_type=aut-num&searchtext=AS38193).

These records do not guarantee customer service quality. PeeringDB is self-maintained, BGP observers see the internet from their own vantage points, and whois records can lag operational reality. They still prove that TWA is not a purely local access provider. It runs a visible autonomous system with foreign interconnection and a peering posture that can matter for content delivery, latency and route control.

The operational test is what happens when a route fails. The July 2026 SMW5 incident is useful because it shows both dependency and mitigation. PTA's public statements, as reported by Dawn and Business Recorder, said users could see intermittent degradation, TWA was coordinating with the SMW5 consortium, traffic was rerouted through alternate international links, and normal operating capacity was restored after the fault was rectified (https://www.dawn.com/news/2012491/pta-says-submarine-cable-fault-may-cause-intermittent-internet-disruption; https://www.brecorder.com/news/amp/40428352). That is exactly what buyers of international capacity should care about: not whether faults never occur, but whether the provider has enough alternative paths, commercial rights and operational control to contain the damage.

The market chatter around such events should be handled carefully. A Tapmad social post captured by search said some users could experience degraded streaming because of an international connectivity issue affecting Pakistan (https://x.com/tapmadtv/status/2072743985161138212). Reddit threads around Pakistan cable faults mix useful user observation, speculation and frustration, including claims about which systems were down and how much capacity remained (https://www.reddit.com/r/PakistaniTech/comments/1oc4bpy/cable_fault_in_peace_submarine_cable_rip/). Those posts are not proof of route status, capacity shares or fault cause. They are market signals. They show how quickly wholesale cable events become retail experience, brand anger and content-quality risk.

For TWA, this is both marketing and liability. If it can demonstrate superior diversity, it can win customers who fear route shocks. If a fault touches a TWA-linked system, the same customers will expect fast reroute, transparent communication and credible restoration estimates. The bigger the company becomes in national capacity, the more every incident becomes reputational.

Regulation turns market share into responsibility

The international gateway is a regulated market because it touches national communications, foreign exchange, lawful intercept, competition, security and consumer welfare. PTA's documents show the authorities watching the wholesale layer closely. A 2024 PTA consultation paper on IP bandwidth reselling says Pakistan's wholesale IP bandwidth market had four major overseas cable operators - PTCL, Transworld Associates, Cybernet and SCO - providing services to downstream fixed-line and cellular operators (https://www.pta.gov.pk/assets/media/2024-09-03-Consultation-Paper-on-IP-Bandwidth-Reselling.pdf). PTA's 2021 significant-market-power determination in wholesale IP bandwidth says PTCL and TWA were providing IP bandwidth services to local loop, LDI and CVAS licensees, and that the authority considered competitive conditions in a market where only a few players served downstream demand (https://www.pta.gov.pk/assets/media/2021-07-23%20Determination%20on%20SMP%20Operators%20in%20Wholesale%20IP%20Bandwidth%20Market%20in%20Pakistan.pdf).

This is the part of the toll booth that is easiest to misunderstand. A narrow wholesale bottleneck can create pricing power. It can also invite regulation. If downstream ISPs or mobile operators believe international bandwidth prices are too high, or if the state believes resilience is inadequate, TWA's position becomes a matter of public policy rather than only private contract. The provider can earn from scarcity, but it cannot behave as if scarcity is politically invisible.

The LDI licence adds another layer of accountability. TWA's own LDI voice page says it operates under PTA licensing, offers direct connectivity to global internet backbones and voice networks, has direct interconnects to all major Pakistani operators, and uses route monitoring and fraud protection (https://www.tw1.com/service/ldi-voice-services/). That is valuable for international carriers and enterprise customers, but it also places TWA inside compliance-sensitive traffic flows. Voice termination, fraud controls, interconnection and international routing are not just technical products; they are regulated obligations.

Security risk is no longer theoretical. PTA's 2024-25 release highlights cybersecurity and national telecom security operations alongside broadband growth (https://www.pta.gov.pk/category/pta-releases-annual-report-2024%E2%80%9325-1374704410-2026-01-01). TWA's data-centre ISO 27001 announcement and managed-service pages show the company selling security, compliance and proactive monitoring into that environment (https://www.tw1.com/press-release/exciting-news-from-transworld-associates/; https://www.tw1.com/service/managed-services/). The commercial opportunity is clear: customers want secure, monitored, compliant connectivity. The operating burden is also clear: a company that hosts, routes and protects traffic must maintain controls that survive audit, incident response and reputational stress.

Geopolitics matters through route choice. Pakistan's submarine paths pass through regions where cable repair, landing permissions, vendor politics and regional conflict can affect timing and trust. The SEA-ME-WE 6 project itself became part of broader global cable-security debate, and industry coverage has noted its high capacity, multiple landing points and route across Southeast Asia, the Middle East and Western Europe (https://www.submarinenetworks.com/en/systems/asia-europe-africa/smw6). TWA does not control the whole geopolitics of a consortium cable. But as a landing and customer-facing operator, it absorbs part of the commercial question: which route is acceptable, how diverse is it, what happens when a segment is impaired, and who gets priority when capacity is scarce?

The best regulatory posture for TWA is therefore not maximal extraction. It is credible leadership: invest ahead of demand, publish enough operational assurance to build trust, price capacity so downstream operators can grow, and cooperate visibly during faults. A private cable owner in a strategic sector needs profit, but it also needs legitimacy.

Customers, competition and the wholesale bargain

TWA's customer set is best inferred from the services it sells and the revenue segments PACRA reports. The homepage says it serves major mobile operators, ISPs, enterprises and SMEs (https://www.tw1.com/). PACRA says cellular mobile operators, ISPs, corporate organizations and SMEs buy bandwidth from submarine operators, and that carrier, international and wholesale segments are TWA's main revenue drivers (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). The IPLC page targets LDIs, ISPs, multinational corporations and international agencies needing point-to-point global circuits (https://www.tw1.com/service/iplc/). The data-centre page targets enterprises, ISPs, telecom operators, cloud providers and AI-driven workloads (https://www.tw1.com/service/data-centre/).

That customer mix creates a useful hedge. Mobile and ISP demand supplies volume. Enterprises and multinationals supply higher-service requirements. Data-centre and managed-service customers may supply stickier contracts. International carriers and content networks supply foreign-route relevance. But the mix also creates conflicting expectations. A mobile operator wants cheap bulk capacity. A bank wants private, secure and restorable circuits. A video platform wants streaming performance during peaks. A global carrier wants stable bilateral terms. A regulator wants resilience and competition.

TWA has to price and operate across all of those needs without letting one customer class subsidize another too visibly.

Competition comes from at least five directions. PTCL remains the incumbent-scale international player, with cable systems and national reach. Cybernet's PEACE role, plus other cable arrivals, adds another private-sector reference point. SCO matters for specific geography and state-linked connectivity. LDI licensees and bandwidth resellers can put pressure on distribution even if they lack full cable ownership. Large global content and cloud networks can also change the market by pushing direct peering, caching, private network extension and edge infrastructure closer to Pakistani users.

This is why TWA's domestic long-haul and data-centre strategy is important. If the company merely sells upstream bits, it is exposed to falling wholesale unit prices. If it can connect submarine landing, data centre, domestic MPLS, managed WAN, DDoS protection and private circuits, it competes on route assurance and operating convenience. The Wateen agreement, with more than 6,000 km of long-haul fibre support, is significant because it helps TWA push its international-capacity position deeper into domestic enterprise and operator markets (https://www.tw1.com/press-release/transworld-and-wateen-sign-strategic-partnership-agreement-to-expand-pakistans-digital/). The Huawei upgrade is significant because higher-capacity wavelengths make it easier to scale the transport layer as demand grows (https://www.tw1.com/press-release/to-enhance-the-quality-and-capacity-of-internet-services-in-pakistan/).

There is a subtle risk in the company's own success. If Pakistan's international-capacity market becomes more diverse and better supplied, TWA's national importance rises but unit scarcity can decline. New cables improve resilience and digital growth, yet they may also reduce the premium attached to any one route. TWA's answer has to be quality, not just capacity: lower latency, stronger restoration, better peering, better NOC response, better enterprise packaging, better security and better domestic delivery.

The Google Verified Peering Provider signal fits this move up the quality ladder. TWA's press page says it became one of Pakistan's first Google Gold-tier verified peering providers in December 2025, with the announcement carried through Business Recorder and Profit coverage referenced by TWA (https://www.tw1.com/press-release/). The claim should be treated as a company-announced status rather than independent financial proof. Still, it points in the right commercial direction: not merely more bandwidth, but better content-network relationships and routing quality.

The question for a buyer is whether TWA can keep that quality while scaling. A company can win wholesale customers through relationships and scarcity. It retains them through predictable performance, documentation, incident response and price discipline. The more Pakistan's demand base grows, the less forgiving customers become.

What would change the judgement

The current judgement is positive but conditional. TWA has a real operating position, visible national relevance, audited-like financial disclosure through PACRA, regulatory standing, cable assets, foreign peering and a service portfolio aligned with Pakistan's digital-growth needs. It should be read as one of the companies underneath Pakistan's broadband expansion, not as a marginal directory listing.

The first fact that would change the view is pricing. Public sources show revenue and growth, but they do not disclose wholesale price trends by route, customer class or contract tenor. If TWA is growing mainly because it is selling more capacity at stable or only gently declining unit prices, the business quality is strong. If growth requires heavy price cuts, longer receivable cycles and higher capex just to defend share, the apparent capacity boom is less attractive.

The second fact is contract concentration. A small number of mobile operators, large ISPs, content networks or government-linked buyers could make the company look stronger than its renewal risk allows. PACRA gives segment shares, not the top ten customer book (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). A lender or acquirer would want customer-level renewal history, minimum commitments, service credits, currency pass-through terms and route-specific margins.

The third fact is true route diversity. Public sources list TW1, SMW5, SMW6, 2Africa and various peering points, but customer contracts differ. Does a specific bank or ISP get automatic restoration? Across which cable systems? At what committed capacity? With what latency and packet-loss assumptions? The IPLC page advertises optional restoration with automatic bandwidth switchover to backup cable systems (https://www.tw1.com/service/iplc/). The difference between optional and standard restoration is economically important.

The fourth fact is financing discipline. PACRA's A+ long-term rating and stable outlook are meaningful, but the report also describes leverage, long-term borrowings and capex commitments (https://www.pacra.com/api/rating-report/MTQ4NjU%3D). A company can be strategically important and still overbuild or misprice risk. The correct diligence question is not whether Pakistan needs capacity. It clearly does. The question is whether TWA earns an adequate return on each new layer of capacity and domestic reach.

The fifth fact is security and outage performance. The market will forgive occasional submarine faults if communication, reroute and restoration are strong. It will not forgive repeated opaque degradation, weak incident updates or uncertainty about which services are protected. The July 2026 SMW5 episode is not a condemnation; it is a live demonstration of the product. Buyers should ask for post-incident reports, reroute timelines, impacted-service classes and lessons learned.

The judgement

Trans World Associates is a strategic wholesale infrastructure company in a country where broadband demand is growing faster than the public usually sees the underlying costs. Pakistan's consumers experience cheap data, streaming, gaming, cloud apps and mobile banking as retail services. Underneath those services sit submarine landing stations, international capacity commitments, dollar-linked equipment, PTA-regulated gateways, global peering, domestic transport, security controls and repair politics. TWA's economic role is to convert that hidden layer into sellable capacity.

The public evidence supports a strong but not risk-free reading. TWA owns and operates TW1, participates in or lands major cable systems, holds operational LDI status, runs AS38193 with visible international peering, generates substantial revenue from carrier, international and wholesale segments, and is investing in long-haul transport, data centres and managed services. It has grown revenue quickly and carries a stable PACRA rating. It also carries leverage, capex burden, receivable risk, supplier dependence and exposure to price-sensitive downstream markets.

The toll booth beneath national broadband growth is valuable only while it remains trusted. If TWA helps Pakistan add capacity, reduce route fragility, improve cloud and content access, and keep wholesale economics workable for downstream operators, its position should strengthen. If new cables create excess capacity, if faults expose weak restoration, if regulation presses prices lower, or if dollar costs outrun rupee revenue, the same position becomes more difficult.

The best single-sentence judgement is this: Trans World Associates is one of Pakistan's most important private capacity intermediaries, and its future depends on turning cable-landing leverage into resilient, competitively priced, security-aware wholesale and enterprise services rather than relying on scarcity alone.