Summary

- What it says: A Timor-Leste mobile connection looks simple when a shopkeeper scans a payment, a student sends a message, or a driver waits for work on a handset.

- Main topic: Peering and transit; Telecom spectrum and security

- Context: market / company research report / Timor-Leste

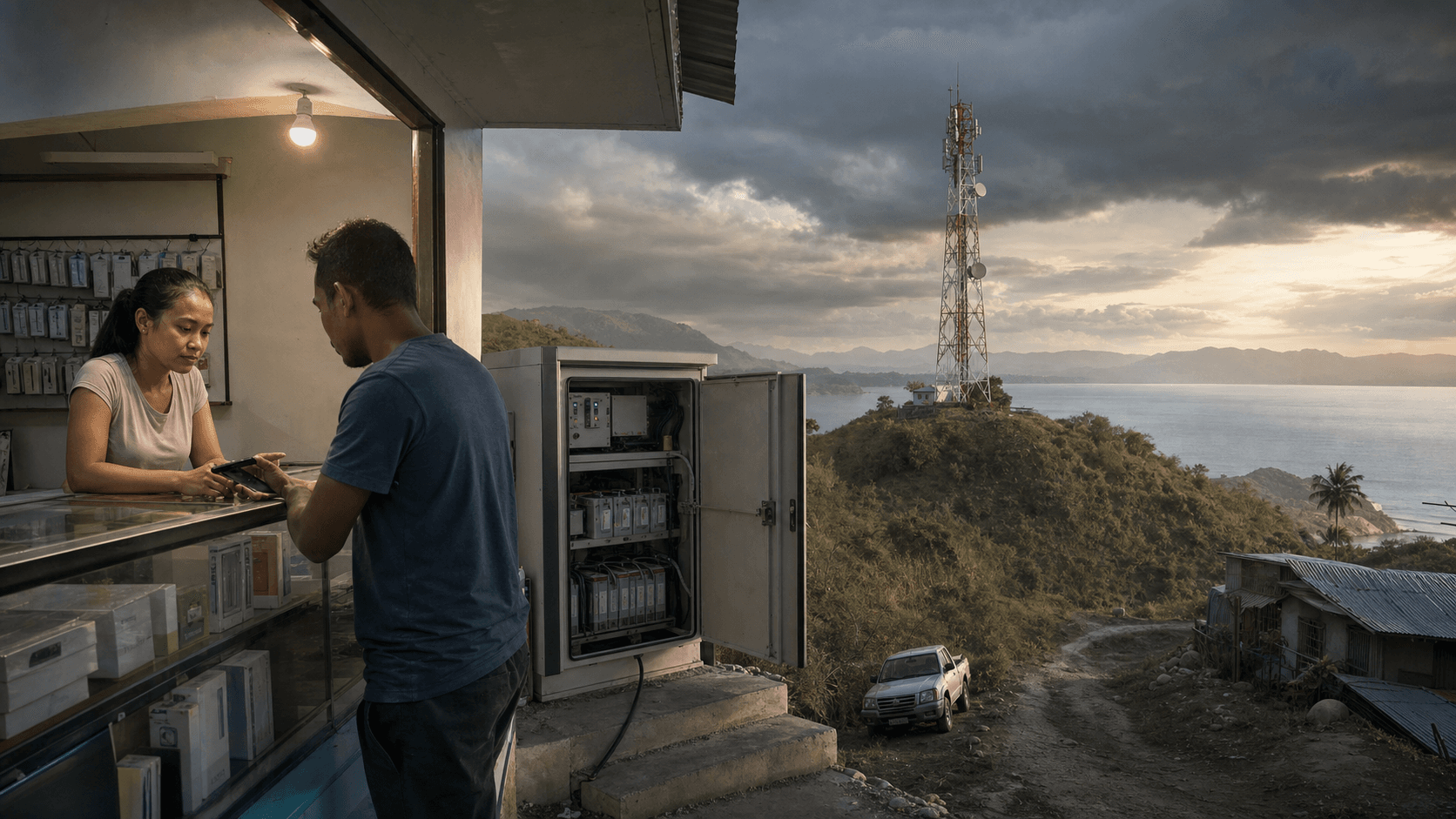

At the counter of a small shop in Dili, the economics of a mobile network can be measured in coins, battery percentage and patience. A customer comes in at lunch with a phone that is almost out of charge. He needs a data package, but the immediate problem is not entertainment. A message from a relative in another municipality is waiting. A payment app may be needed before the afternoon is over. A prospective employer may call from a number he does not know. The shopkeeper's phone is also a terminal: it receives transfer confirmations, checks prepaid balances, and keeps a thin record of the day's trade.

Nobody in that scene thinks about spectrum licences, APNIC records, subsea cables or tower fuel. The service is expected to behave like light from a switch.

That expectation is the business Telkomcel has chosen to sell. In a larger country, a mobile operator can hide many difficult costs behind scale. Dense cities amortise cell sites quickly. A large postpaid base steadies cash flow. Enterprise contracts, towers, fibre and wholesale capacity can be blended across many provinces and tens of millions of customers. Timor-Leste offers the opposite test. The country has roughly 1.4 million people, a scattered geography, a young consumer base, a low-income cash economy and a national habit of relying on mobile networks because fixed broadband has historically been limited.

A network must reach enough places to feel national, but the revenue that pays for it arrives in small increments: a one-dollar top-up, a short call, a data bundle bought before a school assignment, a merchant payment, or a prepaid recharge at a kiosk.

Telkomcel is not just a consumer brand in that story. It is the Timor-Leste operating face of Telekomunikasi Indonesia International (T.L.) S.A., part of Telin and therefore of PT Telkom Indonesia. Telkomcel's own company profile says the brand is owned by Telekomunikasi Indonesia International (T.L.) S.A., that the Timor-Leste company is a subsidiary of PT Telekomunikasi Indonesia International, and that 100% of Telkomcel shares are held by Telin. The same page says Telkomcel was established on September 17, 2012, received a radio-spectrum licence from the Timor-Leste government in October 2012, and provides mobile telecommunications, broadband internet, corporate voice and data services across districts. The primary company page is useful because it ties the public consumer brand to the legal and parent-company identity rather than treating Telkomcel as a loose local label: https://telkomcel.tl/p/company-profile.

The parent-company record matters because Timor-Leste is too small for the usual heroic myth of the stand-alone operator. Telkom Indonesia's 2026 Form 20-F, filed for the 2025 year, describes Telin as an international business operating through formal legal entities in several countries, including Telkomcel in Timor-Leste. It says Telkomcel provides a mix of international data connectivity, cloud and IP transit services, wholesale voice and mobility services, enterprise solutions, mobile services as an MNO and MVNO, and data center operations. That same filing places Timor-Leste inside a wider Telin footprint of international points of presence, data center operations and subsea-cable strategy. The relevant public filing is here: https://www.telkom.co.id/minio/show/data/lampiran/1778861459016_original_PERUSAHAAN-PERSEROAN-PERSERO-PT-TELEKOMUNIKASI-INDONESIA-TBK-20260515-20-F-EDGAR.pdf.

This is the first economic fact about Telkomcel. A Timor-Leste mobile network is local in customer experience but regional in balance-sheet logic. The Dili user sees a SIM card, signal bars and a price. Telkom sees a small foreign operating unit whose strategic value is not only retail minutes but also presence in a neighbouring country, enterprise connectivity, wholesale traffic, a data-center position and an international-service corridor. That parentage does not make local economics easy. It makes them financeable for longer than a purely local entrant might tolerate.

Timor-Leste's mobile-market structure was born from liberalisation. In June 2012, the government said it had received applications from Digicel Pacific, PT Gapura Caraka Kencana, PT Telekomunikasi Indonesia International and Viettel Global Investment for new telecom licences. The government said the process followed a new telecommunications decree-law and a settlement ending Timor Telecom's exclusive rights; it expected new service providers to offer GSM and 3G voice and data services and improve pricing, quality, variety and availability. That official notice is still the cleanest public record of the market opening that made Telkomcel possible: https://timor-leste.gov.tl/?lang=en&p=6974&print=1.

The competition promise was ambitious for a country where telecom infrastructure had to be created almost from scratch. An ITU-hosted presentation by the Timor-Leste regulator said competition was introduced in March 2012, licences were awarded in July 2012 to PT Telekomunikasi Indonesia International and Viettel Global Investment, and the new licensee was expected to cover 94% of the population with GSM mobile telephony and 3G internet access services. It also described the National Communications Authority as replacing ARCOM under the 2012 decree-law. The presentation is not a commercial filing, but it is a useful regulator-side statement of the obligations behind the commercial launch: https://www.itu.int/en/ITU-D/Regional-Presence/AsiaPacific/Documents/Events/2016/Mar-ICTStats/Presentations/ANC%20COUNTRY%20PRESENTATION%20nazario.pdf.

The hard part began after liberalisation. National coverage targets may be politically attractive, but they are economically severe. A mobile site in a dense city has many potential users within a short radius. A site serving a road, a coastal village or a mountainous settlement must be built, powered, protected, visited and connected even when its traffic is modest. Timor-Leste compresses that dilemma into a small national market. A site cannot charge a different price for each slope, weather event, fuel run or microwave hop. The retail plan must look legible to the customer. The capital plan must satisfy engineers.

The parent company must decide that the sum of small transactions, enterprise accounts, wholesale relationships and strategic presence justifies the cost.

Telkomcel's own tariff pages show how unforgiving that arithmetic can be. The prepaid page lists domestic voice at $0.05 per minute on-net and $0.17 per minute to other mobile or fixed operators, with SMS at $0.03 on-net and $0.075 off-net. It also describes the mechanics of registration, recharge and balance checks, including the basic USSD codes that keep a prepaid market alive. The page is not a profit statement, but it is a price book for the everyday transactions out of which the network must recover spectrum fees, site rent, power, staff, interconnection, backhaul, IT systems and depreciation: https://telkomcel.tl/p/simcardprepaid.

The data page is more revealing. Telkomcel says its data network is supported by 3G HSDPA up to 21 Mbps, that its 850 MHz network covers a larger area than 2.1 GHz would, that 4G began in the Dili area in February 2018 and continued expanding to other districts, and that regular non-package data is charged at $0.045 per MB while bundle packages provide cheaper access. The page is somewhat dated in its presentation, but that itself says something about the market: mobile broadband is sold through a set of package and renewal behaviours, not by abstract promises of unlimited abundance. The page is here: https://telkomcel.tl/p/internetrapidodemais.

One can translate those retail facts into a blunt business question. How much national infrastructure can a company sustain when many customers manage spending in small prepaid decisions and when the marginal gigabyte is expected to become cheaper over time? In a low-income market, data growth is not automatically profit growth. More video, messaging, maps, payments and schoolwork increase traffic. They do not necessarily increase revenue per user at the same rate. The network must carry more bits for each dollar, and the bits must cross radio access equipment, backhaul links, international gateways, core systems and support platforms.

A small operator cannot simply wish for the traffic of a modern economy while paying the costs of an old voice network.

The broader market numbers sharpen the point. FRED's World Bank series for Timor-Leste mobile cellular subscriptions reports 116.38 subscriptions per 100 people in 2024, up from 112.65 in 2023 and 108.16 in 2022. That does not mean every person has a phone; prepaid SIM ownership, multiple SIMs and inactive lines complicate the reading. But it does show that mobile connectivity is now structurally embedded in the country. The data series is here: https://fred.stlouisfed.org/series/ITCELSETSP2TLS. World Bank country data put Timor-Leste's 2025 population at about 1.42 million and its 2024 GDP per capita at about $1,332, while internet-use estimates remain far below rich-country levels. Those figures frame Telkomcel's ARPU problem: the addressable market is broad, but the disposable-income pool is shallow. The country page is here: https://data.worldbank.org/country/timor-leste.

For Telkomcel, prepaid revenue per user is not only a finance metric. It is a social contract. If prices rise too quickly, customers ration usage, switch SIMs, delay top-ups or let balances sit. If prices fall too quickly, the network may be unable to fund capacity, maintenance and expansion. If service quality falls, the customer blames the brand, not the geography. A rural teacher does not care whether a weak signal reflects backhaul congestion, power instability, a storm-damaged road, a limited-capacity microwave link or a temporary spectrum constraint.

She experiences one fact: the video will not load, the message is late, or the call drops.

Spectrum is where the contract becomes visible to the state. In 2021, Timor-Leste's Tatoli news agency reported that Telkomcel received a 2300 MHz band allocation of 20 MHz for 15 years, with a spectrum price of $2,637,982.50 paid in one payment, limited to Dili municipality unless further fees supported expansion to other municipalities. The same report said the award was meant to respond to weak connectivity and expensive internet complaints. That public article is here: https://en.tatoli.tl/2021/09/19/telkomcel-telemor-to-improve-network-connections-of-radio-frequency-spectrum/09/.

For a large operator, a $2.64 million spectrum payment might seem minor. In Timor-Leste, it is not trivial. It is a long-dated bet that enough data demand, device adoption and network upgrade activity will convert a spectrum right into operating cash flow. The 2300 MHz band can add capacity, especially in Dili, but capacity spectrum is not the same as coverage spectrum. Lower-frequency holdings help reach wider areas; higher bands help carry more traffic in dense places. A national operator needs both. Telkomcel's old 850 MHz explanation on its data page shows the coverage logic. The 2300 MHz award shows the capacity logic.

The business problem is to earn a return on both in a market where customers are price-sensitive and where Dili's traffic does not automatically pay for every rural coverage obligation.

That is why tower power belongs in the story. A national mobile network is an electricity business in disguise. Every site needs power, backup and maintenance. A grid connection is only the beginning; batteries age, generators need fuel, cooling systems fail, and technicians must reach equipment in rain, heat or poor road conditions. Timor-Leste's public data may show improving electricity access, but telecom reliability is judged by uptime during precisely the moments when normal infrastructure is strained.

When customers rely on a handset for payments, family coordination, transport, news or emergency calls, the tower becomes a piece of public economic infrastructure even though it is owned or operated commercially.

Climate risk makes this more than a theoretical concern. In April 2021, Tropical Cyclone Seroja brought torrential rain, flash floods, landslides and soil liquefaction to Timor-Leste. The World Bank estimated damages to agriculture, roads, bridges and housing at $245 million, with resilient recovery and building-back-better costs potentially exceeding $420 million. The same account described critical infrastructure damage and the way rural communities became further isolated when roads and bridges failed. The article is here: https://blogs.worldbank.org/en/eastasiapacific/recovery-resilience-building-learning-tropical-cyclone-seroja-timor-leste.

For a mobile operator, a cyclone is not just a risk to masts. It is a risk to every assumption in the operating plan. Roads determine field access. Power determines site uptime. Floods determine whether equipment rooms stay dry. Customer income determines top-up behaviour after a shock. Government and humanitarian demand may surge at the same time as normal retail spending weakens. The operator must carry more urgent communications when its own physical system is under stress. Climate resilience is therefore not a corporate-responsibility slogan.

It is a cost centre, an engineering discipline and, in a small market, a test of whether enough redundancy exists to keep national service credible.

The international-capacity story changes the same economics from the other side. For many years Timor-Leste's internet access depended heavily on satellite and microwave routes. A JICA Dili urban master-plan report said that mobile data was provided by Timor Telecom, Telemor and Telkomcel, while international connectivity was then provided only through satellite links, with no submarine fibre connected to Timor-Leste, making internet speed slow and costs higher. It also cited earlier reporting that Telkomcel had spent up to $50 million building infrastructure, from base transceiver stations to customer-service call centres, and expanded to 110 BTS units to cover 95% of Timor-Leste. Those older figures should be read as historical context rather than current site inventory, but they show the magnitude of the first build-out: https://openjicareport.jica.go.jp/pdf/12268603.pdf.

The submarine-cable moment changes what customers will expect. In June 2024 the Timor-Leste government announced the landing of the Timor-Leste South Submarine Cable System, connecting the country to Australia's North West Cable System. The government said the system was designed for 27 Tbps between Timor-Leste and Australia, spanned 607 kilometres, used seven repeaters and included a branch to the Greater Sunrise region. It described the cable as a major step for digital connectivity, lower latency, higher speed and business use. The government announcement is here: https://timor-leste.gov.tl/?lang=en&p=37946&print=1.

The Australian Infrastructure Financing Facility for the Pacific says Timor-Leste was one of the few remaining countries not connected to an international submarine telecommunications cable, that it was supporting the government with AUD7.2 million in advisory support, and that the country's reliance on satellite and microwave made access expensive and slow. Its project page says the cable should enable faster, cheaper and more reliable internet connectivity: https://www.aiffp.gov.au/investments/investment-list/connecting-timor-leste-to-the-internet-via-submarine-cable.

For Telkomcel, a national cable is both relief and pressure. It can lower the structural cost and latency of international capacity. It can make cloud services, enterprise connectivity, content delivery, public administration and digital payments more plausible. It can also reveal domestic bottlenecks that were previously hidden by international scarcity. Once customers believe that the country has a modern external link, they will be less forgiving of congestion, weak indoor coverage, poor device performance or expensive packages.

International capacity is a necessary condition for better mobile internet; it is not the same as a perfect radio access network.

The parent-company angle becomes important again here. Telkom's 2026 filing describes Telin's international cable systems, points of presence, cloud communications platforms, wholesale mobility services and data-center operations. That matters because Telkomcel's Timor-Leste role is not only to sell local SIMs. It can become a local access arm for a wider Telin service set: enterprise connectivity, IP transit, wholesale voice, cloud-adjacent services, roaming, messaging and possibly data-center demand. The company profile already says Telkomcel provides corporate voice and data services.

The parent filing says Telkomcel participates in international data connectivity, cloud and IP transit, wholesale voice and mobility, enterprise solutions and data-center operations. In a small market, the difference between a thin consumer operator and a strategically useful national platform may lie in these non-retail services.

That does not mean enterprise revenue will solve everything. Timor-Leste has a limited corporate base. Government, development agencies, banks, hotels, supermarkets, logistics firms, schools, clinics and NGOs can be valuable customers, but they are not a vast enterprise market by regional standards. The winning operator has to make enterprise and wholesale services deepen the network economics rather than distract from them. A bank branch, a payment agent, an internet cafe, a port user or a government office may buy reliability. The consumer base buys availability. The same towers, backhaul, core and support teams must satisfy both.

Telkomcel's payment surface is therefore more than an app story. T-PAY, branded as Timor Pay, offers QR-code payments, transfers, cash withdrawal and top-up, phone credit and data purchases, and electricity-token functions. Its own site says T-PAY can be registered from any mobile phone number in Timor-Leste, that regular accounts have a daily transaction and balance limit of $100, premium accounts have a $300 limit and KYC, and agents are present in all 13 municipalities. It also says the electronic wallet follows Banco Central de Timor-Leste regulation and identifies Telin Digital Solution, Lda as the service holder under a 2019 permit. The T-PAY page is here: https://t-pay.tl/home-en/.

That gives Telkomcel two linked forms of dependency. First, the network depends on payments and recharges because prepaid cash flow must be made easy. Second, payments depend on the network because a wallet without signal is just a promise. If a small shop uses a phone to sell data, receive QR payments and buy electricity token services, Telkomcel's radio access, USSD, SMS and data functions become part of the local commercial fabric. The more ordinary the payment feels, the more invisible the infrastructure becomes. That invisibility is commercially valuable until it fails.

Then every entity notices that mobile service is not a commodity floating above the economy; it is one of the economy's rails.

Network-resource evidence supports the identity of the operator behind the public brand. APNIC RDAP shows AS58731 as active, named TELINTLSA-AS, in Timor-Leste, with the description Telekomunikasi Indonesia International (T.L.) S.A. and a Timor Plaza address in Dili. The RDAP record is here: https://rdap.apnic.net/autnum/58731. PeeringDB lists Telkomcel under the organisation Telekomunikasi Indonesia International (T.L.) S.A., with ASN 58731, IRR set AS58731:AS-TELKOMCEL, 18 IPv4 prefixes, traffic level of 5-10 Gbps, Asia-Pacific geographic scope and an open peering policy, though it shows no public exchange or facility entries. The PeeringDB record is here: https://www.peeringdb.com/asn/58731.

Those records are not consumer marketing. They are a technical clue about how Telkomcel appears to the internet. The absence of visible public exchange connections in PeeringDB does not prove an absence of private transit or domestic arrangements; PeeringDB is self-reported and incomplete for many smaller markets. But the AS record, traffic range and parent-organisation match help distinguish Telkomcel as a real operating network, not merely a reseller brand. They also show the asymmetry of visibility. Customers see signal bars. Engineers see AS numbers, routes, transit, upstream relationships, abuse contacts and policy choices.

Investors see capital intensity and risk. All are different views of the same company.

Third-party market summaries should be handled with care, but they are still useful signals. A ResearchAndMarkets release distributed by Business Wire in 2024 said Timor-Leste had three telcos - Timor Telecom, Telkomcel and Telemor - jointly providing 98% national coverage with mobile infrastructure; it said all three launched LTE services during 2019 and that mobile broadband penetration had risen with smartphone adoption. It also described the submarine cable as a major pending improvement. Because this is a market-research release rather than an operator or regulator data table, the precise figures should not be treated as Telkomcel's own disclosure. The release is here: https://www.businesswire.com/news/home/20240628295614/en/Timor-Leste-East-Timor-Telecoms-Mobile-and-Broadband-Market-Statistics-and-Analyses-2024---ResearchAndMarkets.com.

The most defensible reading is that Telkomcel is one of three national mobile players in a small, competitive, mobile-first market where coverage expectations are high and fixed broadband has not carried the main household connectivity burden. The market is not greenfield anymore. Customers know what mobile data is. They compare operators. They carry multiple SIMs if that helps them manage coverage and price. They expect 4G in urban life and usable service outside Dili. That maturity is good for demand but hard for margins, because the easy growth from first-time adoption gives way to churn, package competition and capacity spending.

This is where the idea of ARPU must be used carefully. Telkomcel does not publish a clean, current, stand-alone ARPU in the public documents reviewed here. Telkom reports group and segment performance, and market datasets may estimate national indicators, but Telkomcel's own economics are partly hidden inside the parent structure. The better analytical approach is to infer the pressure from observable pieces: a small population, low GDP per capita, prepaid tariff granularity, expensive spectrum, national coverage obligations, international-capacity transition, a three-operator market and climate exposure.

The conclusion is not that Telkomcel is weak. It is that every dollar of recurring revenue must do unusually many jobs.

A Dili-only operator could optimise differently. It could spend on dense capacity, enterprise sales and storefront visibility. A national operator in Timor-Leste must also think about municipalities where traffic is thin, weather is rougher, roads are slower and customer balances are smaller. The country profile on Telkomcel's site says it is committed to mobile telecommunications across all districts. That phrase carries cost. A national footprint means technicians, spares, local relationships, site acquisition, power arrangements, backhaul design and customer support outside the highest-revenue urban zones.

In a politically sensitive sector, being present only where the spreadsheet is attractive is rarely an option.

This creates a subtle parent-company bargain. Telkomcel benefits from Telkom Indonesia's experience, procurement knowledge, technical standards and international relationships. The company profile explicitly invokes support from Telkom Indonesia and Telkomsel. Telkom's own filings present Telin as a global operator with wholesale, international, cloud, platform and data-center capabilities. But local legitimacy cannot simply be imported from Jakarta. A Timor-Leste operator must employ local staff, respond to local complaints, navigate local regulation, support local languages and price for local incomes. Telkom's February 2025 article on Telkomcel said 95% of Telkomcel employees were Timor-Leste citizens and 75% of management positions were held by local talent, with more than half of those by women. Because the article is a company news release, it is an interested source, but it is still relevant evidence of how Telkomcel wants its local role understood: https://www.telkom.co.id/sites/berita/id_ID/news/kiprah-telkomcel-dalam-transformasi-digital-timor-leste-2851.

The ownership question also shapes resilience. A stand-alone small-market operator can be trapped by replacement cycles. Radio equipment ages. Batteries degrade. Core systems need upgrades. Security requirements rise. Software licences and vendor support are priced in global markets, not by a country's income level. Telkom Indonesia's 2025 consolidated financial statements show the parent group dealing with asset modernisation, useful-life changes, depreciation effects, right-of-use assets and frequency licence fees at group scale. These are not Telkomcel-only figures, so they should not be misread as Timor-Leste costs. They do, however, illustrate the accounting reality of telecom: networks are depreciating asset systems that constantly need renewal. The filing is here: https://www.telkom.co.id/minio/show/data/lampiran/1778544447359_original_LK-Konsolidasian-Telkom-Tahun-2025-Audited-Eng.pdf.

Small markets do not escape that cycle; they merely have fewer customers to pay for it. A 4G site in Timor-Leste does not become cheaper because national GDP per capita is lower. Imported equipment, vendor support, fuel, skilled labour, tower steel, batteries, routers and software support are exposed to regional and global cost curves. Currency conditions can matter too, since Timor-Leste uses the US dollar while Telkom reports in rupiah and procures across multiple markets.

Some dollarisation reduces local exchange-rate risk for customers and local operations, but parent-company consolidation and imported inputs still create financial translation and procurement issues.

The competition with Telemor and Timor Telecom makes the price-to-quality trade-off more acute. If one operator has better coverage in a rural area, a customer may keep that SIM for travel. If another offers a cheaper bundle, the customer may shift data spend. If a business needs dependable enterprise service, it may choose redundancy across providers rather than loyalty to one. Multi-SIM behaviour is rational in places where coverage, price and reliability vary by location. It is also difficult for operators because reported SIM counts can overstate unique-user economics while churn erodes the value of acquisition spending.

Non-official market signals fit this pattern. Travel SIM guides, app-store data, social-media complaints and package comparison pages suggest a market where customers are alert to price, registration, coverage and app usability. Those signals are not audited and can be noisy; they should not replace regulator data or company filings. But they help explain why Telkomcel's business is not only a coverage contest. It is a contest over tiny moments of trust. Does the package activate when the customer sends the code? Does the balance show correctly? Does the payment app register? Does a transfer notification arrive? Does customer care answer?

A low-income prepaid user may forgive a premium service failure less than a rich postpaid user, because each failed transaction consumes a larger share of attention and cash.

International roaming is another small but telling surface. Telkomcel's company profile says it brought international roaming services for visitors and Timor-Leste customers travelling abroad, and that customers can make international calls to Indonesia at lower tariff because of its affiliation with Telkomsel. This is where ownership can produce a consumer-facing advantage: regional relationships, interconnection and wholesale traffic can become practical price and service features. But roaming is unlikely to be the core profit engine.

Its importance is strategic and reputational, especially for a country with ties to Indonesia, Australia, Portugal, development organisations and a diaspora of workers and students.

Telkomcel's data-center and enterprise references deserve similar treatment. In a large market, a data center can become a significant stand-alone business. In Timor-Leste, it may be more important as an anchor for public-sector digitisation, enterprise confidence and local hosting than as a massive revenue line. Local hosting can reduce latency, support government and financial applications, and make the country less dependent on every application call leaving the country. But data-center economics require power, cooling, security, connectivity, customer density and operational discipline.

Telkom's parent filing confirms data-center operations in Timor-Leste through Telin/Telkomcel; the commercial upside depends on whether the new international cable, government digitisation and enterprise demand turn local infrastructure into recurring contracts.

The submarine cable could also change bargaining power. Before cable landing, international capacity scarcity gave operators a common constraint. After better capacity arrives, customers and policymakers may ask why prices are not falling faster or quality is not rising faster. Operators can answer, truthfully, that international transit is only one part of cost. Radio access, spectrum, towers, power, distribution, support, local backhaul, taxes, fees and customer acquisition remain. But the political economy of connectivity will shift.

Once the country has a high-capacity external link, mobile operators will be judged on how quickly they convert national infrastructure into ordinary retail experience.

That conversion will not be symmetrical across Timor-Leste. Dili will benefit first because density, enterprise demand and existing network investment concentrate there. Secondary towns and rural areas may see slower changes unless backhaul, power and site economics improve. The spectrum award reported by Tatoli was initially Dili-limited for Telkomcel's 2300 MHz allocation unless additional fees supported municipal expansion. That distinction is important. Capacity investments usually follow traffic. Coverage investments follow obligation, politics and long-run demand development.

A national operator must balance both without creating a two-speed brand: fast urban Telkomcel and merely adequate rural Telkomcel.

The watchpoint for users is service consistency. The watchpoint for the company is unit economics. For policymakers it is whether competition remains healthy enough to discipline prices without making network investment unattractive. Three national mobile operators in a small country can be good for consumers if each has enough scale to invest. It can be destructive if price competition starves maintenance and capacity. The 2012 liberalisation promise was better pricing, quality, variety and availability.

In 2026, the harder question is whether the market structure can keep delivering those outcomes as data demand rises and capital intensity remains high.

Regulation will matter because spectrum, interconnection, numbering, quality of service, consumer protection and competition policy sit at the boundary between private investment and public dependence. The old ITU-hosted regulator presentation described ANC responsibilities after the 2012 decree-law, including overseeing providers, spectrum and sector data. The market has matured since then, but the task is similar: ensure that operators invest, compete and serve without turning every policy complaint into a price cap or every coverage aspiration into an unfunded mandate.

In a small market, regulatory timing can affect real investment decisions. A delayed spectrum process, an unclear fee, or an unrealistic obligation can change where capital goes.

There is also a regional question. Telkomcel sits between Indonesia, Australia and the Pacific connectivity map. Timor-Leste's new cable links south toward Australia. Telkomcel's parentage links it north and west into Indonesia and Telin's international network. The country's political and economic future points in several directions: ASEAN accession ambitions, development ties, labour mobility, oil and gas questions, and digital-government projects. A mobile operator with local retail reach and regional parent infrastructure can be strategically useful if it adapts to those flows.

It can also be exposed if geopolitical or procurement preferences change, or if state-owned and foreign-owned infrastructure becomes a more sensitive public issue.

None of this should obscure the customer at the shop counter. Telecom analysis often moves quickly from a person with a phone to acronyms and assets. In Timor-Leste the link between the two is unusually visible. A $1 or $5 data purchase is not an incidental consumer choice. It is part of the cash stream that pays for a national radio network. A QR payment is not merely a fintech use case. It depends on a signal, a device, a balance, identity registration, a server and a regulated e-money structure.

A tower on a hill is not just steel; it is a promise that the user's ordinary day will not collapse into isolation when a road washes out or an international route congests.

The evidence base for Telkomcel is strong on identity and broad operating role but weaker on granular economics. Public records identify the company, parentage, licence origins, service categories, network AS, some tariff points, broad market structure, spectrum award and international-capacity environment. They do not provide a complete current subscriber count, Telkomcel-only revenue, EBITDA, ARPU, capex, site count, traffic volume, rural coverage map, network-sharing arrangements or detailed wholesale contracts. That gap is not unusual for a private subsidiary inside a large listed parent.

It means the right analysis is not to invent precision but to examine the constraints that are visible.

Those visible constraints point in the same direction. Telkomcel's challenge is to make a national network feel uneventful in a place where uneventfulness is expensive. It must turn a small prepaid market into reliable radio access, buy enough spectrum to keep urban data usable, use parent-company scale without looking foreign or remote, exploit the new cable moment without overpromising, keep payment and recharge surfaces dependable, support enterprise and data-center demand without neglecting consumer coverage, and build resilience against weather that can damage the roads, power and communities the network serves.

The first watchpoint is the post-cable price and quality curve. If the TLSSC materially lowers international capacity constraints, users should eventually feel better latency, better capacity and more credible enterprise services. The change may not be immediate and it may not be uniform, but a lack of visible improvement would raise questions about domestic bottlenecks, backhaul economics or competitive incentives.

The second watchpoint is spectrum and 4G capacity outside Dili. The 2300 MHz award gives Telkomcel urban capacity logic, but Timor-Leste's development story depends on whether municipal and rural users see practical improvements. Capacity concentrated in the capital can make the company look modern while leaving national equity unresolved. A measured expansion plan, tied to real demand and affordable fees, would be more valuable than slogans about national transformation.

The third watchpoint is payment reliability. T-PAY and mobile recharge functions bind Telkomcel to everyday commerce. If wallet, recharge and data activation services become smoother, the company deepens customer dependency. If they are unreliable, the brand loses trust in precisely the use cases that could raise revenue beyond voice and basic data. Payments can lift ARPU indirectly, but only if the network and support experience are disciplined.

The fourth watchpoint is climate resilience. Seroja showed that Timor-Leste's infrastructure risks are not abstract. A mobile operator needs site hardening, spare capacity, field logistics, power backup, route diversity and emergency coordination. These investments may not produce flashy marketing, but they protect the thing customers actually buy: confidence that the phone will work when the easy assumptions fail.

The fifth watchpoint is Telkom's patience. Telkomcel's parentage is a strength because it brings know-how, financing capacity and regional infrastructure. It is also a test because small foreign subsidiaries must continually justify management attention. If Telkom views Timor-Leste as part of a strategic international connectivity map, Telkomcel can keep investing through thin periods. If it sees only a small retail market, capital discipline may become tighter.

The 2026 Telkom filing's description of Telkomcel inside Telin's international services is therefore encouraging: it frames Timor-Leste as more than a tiny mobile sideline.

In the end, Telkomcel is a company built around a modest miracle: making an island network disappear into normal life. The customer at the shop counter should not have to know whether his message crosses 850 MHz coverage, a 2300 MHz capacity layer, a microwave hop, a fibre route, a data center, a submarine cable or an upstream transit arrangement. He should only know that the payment went through, the call connected and the message arrived. The economics of that simplicity are anything but simple. That is why Telkomcel matters.