Summary

- What it says: Tandaa Networks and the price of being known on the Kenyan coast

- Main topic: Network-resource evidence

- Context: market / company research report / Africa

Tandaa Networks sits in the part of the internet economy where small companies either become trusted local utilities or disappear into the noise of reseller offers, mobile bundles and half-remembered outage stories. Its public identity is simple enough at first glance: a Kenyan coast internet provider, based around Kilifi, selling fibre and fixed-wireless service to homes and businesses, offering wholesale capacity to resellers, and using Mombasa’s growing interconnection ecosystem to reach the wider internet. Its economic identity is more complicated and more useful.

The company is not trying to be Safaricom. It is not built around a national mobile customer base, a dominant mobile-money platform, or a nationwide consumer brand. It is also not just a Facebook page offering Wi-Fi. Tandaa has public routing evidence, an autonomous system, visible Mombasa peering, a current retail ordering site, a billing portal, public support channels, and network presence at serious coastal interconnection sites. The tension is between those two facts.

Tandaa is real infrastructure, but it must sell that infrastructure in a market where most Kenyans already carry the internet in their pocket and where the largest fixed players can bundle brand recognition, retail finance, fibre roll-out, mobile data and service shops at a scale a coastal operator cannot match.

That makes Tandaa a useful test of Kenyan middle-mile and trust economics. A smaller ISP on the coast has to buy or build capacity, reach neighbourhoods, keep links alive through power and weather interruptions, manage field crews, collect payment, work with resellers without losing control of the customer experience, and persuade households that a local fixed connection is worth paying for even when mobile data is good enough for many daily tasks. It has to do this in a country where mobile subscriptions reached 84.1 million by March 2026, mobile data subscriptions reached 62.6 million, and mobile money subscriptions reached 53.4 million.

The mass-market habit is mobile-first. Tandaa’s commercial job is to make fixed access feel local, dependable and worth the monthly commitment.

The core judgement is therefore not whether Tandaa can point to a speed plan or an ASN. It can. The harder question is whether the company can turn coastal proximity into durable economics. If Tandaa is simply one more small ISP selling capacity through loosely controlled last-mile resellers, it is exposed to churn, regulator scrutiny, local reputation shocks and price compression. If it can use Mombasa peering, Kilifi support, a recognizable local brand, and disciplined reseller/account management to deliver a better experience in specific communities, it can own a defensible niche even without national scale.

Identity first: Tandaa, Blue Streak and the licence record

The public record around Tandaa has to be reconciled before any commercial analysis makes sense. The consumer-facing brand is Tandaa Networks. Its official site uses the domain tandaa.africa, identifies Tandaa as a Kilifi-based fibre and wireless connectivity provider for the Kenyan coast, and presents the brand as "Tandaa Networks Ltd" in its footer. LinkedIn describes Tandaa Networks as an ISP providing fibre and wireless connections in Kilifi, Mikindani and selected environs, with wholesale internet for resellers and related services such as CCTV and IoT. PeeringDB’s network profile identifies AS328734 as Tandaa Networks, with the long name Tandaa Networks Limited and the same tandaa.africa website.

The routing record adds a second name. Public ASN directories and AFRINIC-derived whois text identify AS328734, Tandaa-Networks, as registered to Blue Streak Horizons Net Limited, country Kenya. PeeringDB’s organization page for Tandaa Networks Ltd also lists the long name as Bluestreak Horizon Net Ltd and notes that Tandaa is an ISP based in Kilifi on the Kenyan coast. That looks less like a contradiction than a normal operating-brand and legal-resource-holder split, but it is still a diligence point. The brand, the website, the ASN and the network resources need to be read together, not as four separate companies.

Kenya’s current communications licence record complicates the picture further. The Communications Authority of Kenya’s May 2026 register of Unified Licensing Framework licensees lists Tandaa Group Ltd under Network Facilities Provider Tier 3 with a Kilifi postal code, and lists both Tandaa Communications Limited and Tandaa Group Ltd under Application Service Provider. In the same regulator universe, a revoked ASP list shows Blue Streak Horizons Net Limited and licence number TL/ASP/00084 on an ASP revocation list, with a 2016 licence date and 2024 revocation timeline. A CA compliance report also refers to "Bluestreak Horizon (Tandaa)" in a discussion of licensed upstream providers whose capacity was being used by illegal entities, and says the Authority should engage such entities to ensure they work only with licensed resellers and account for their last-mile networks.

The responsible reading is cautious. The current consumer brand and network evidence are active. The current CA register contains Tandaa-named licensees. Older or parallel Blue Streak evidence remains tied to the ASN and to regulator documents. Public evidence does not fully explain whether there was a corporate reorganization, licence replacement, group structure, reseller structure or naming update.

That identity seam matters commercially because fixed-access customers, resellers, landlords, regulators and upstream providers all need to know who is responsible when service fails, invoices are disputed, or last-mile installations fall outside approved practice. For readers evaluating Tandaa, the point is not to assume a legal defect. It is to recognize that the public identity map is part of the risk profile.

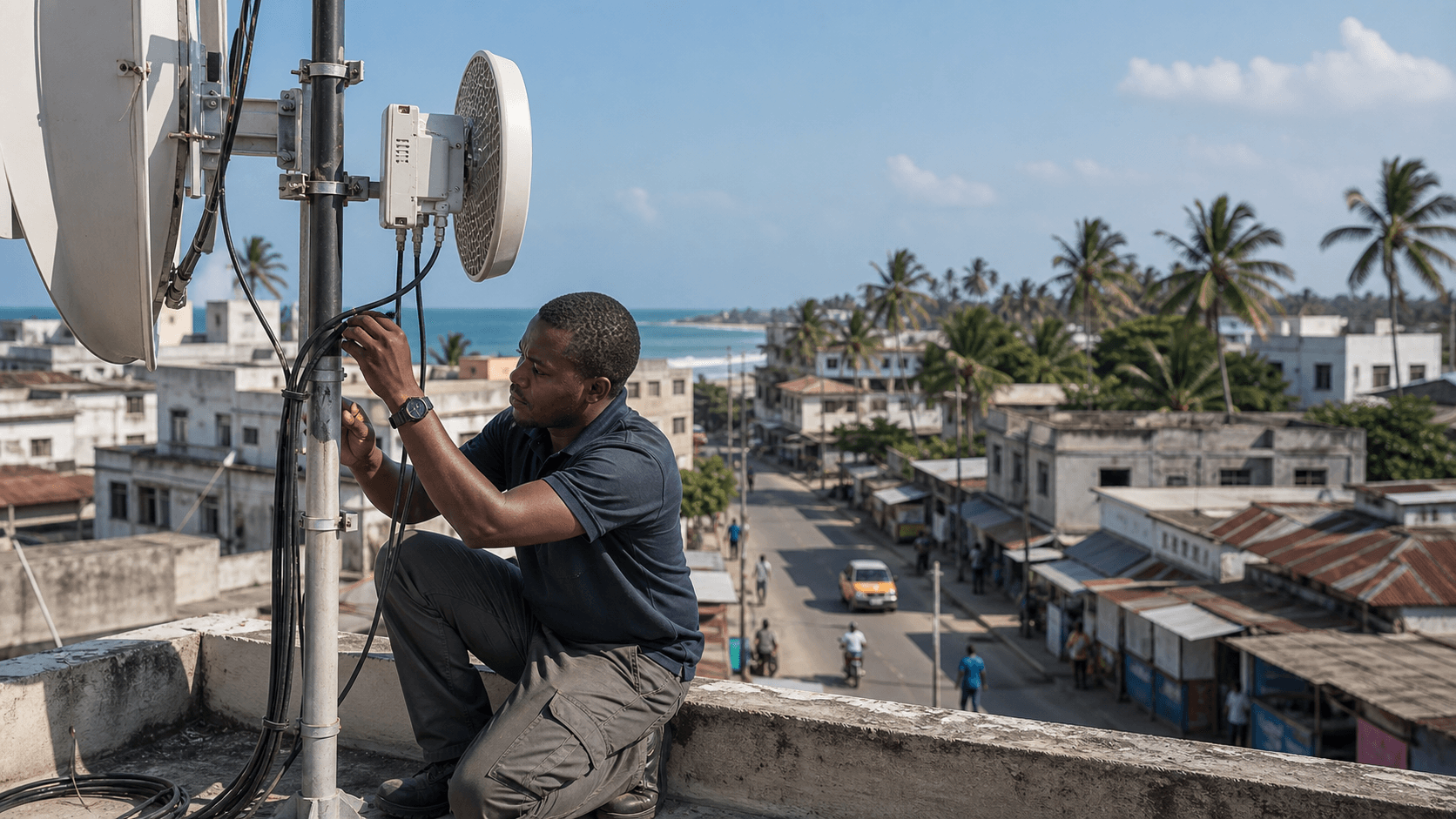

What Tandaa sells

Tandaa’s current public offer is deliberately plain. The official site presents three residential packages: Bronze at 25 Mbps for KES 2,399 per month, Silver at 50 Mbps for KES 3,599 per month, and Gold at 100 Mbps for KES 6,999 per month. It advertises free installation and requires two months of prepayment for activation. The ordering path is built around coverage checking, GPS location, plan selection and WhatsApp dispatch. The site lists [email protected], a direct WhatsApp/phone channel, a Kilifi headquarters, and a backbone label from Mambrui to Vanga. It also carries a customer billing portal under the Tandaa domain.

That product surface tells a lot about the business. The company is selling household and small-business connectivity, not a premium corporate-only service. The plans sit in the part of the Kenyan fixed-broadband market where a customer is not buying gigabit vanity; the customer is deciding whether to pay a monthly amount that competes with mobile data, shared Wi-Fi, a neighbour’s hotspot, office connectivity, or a better-known national fibre brand. The 25 Mbps entry point is not accidental.

In the CA’s March 2026 statistics, the largest fixed subscription speed band in Kenya was 10-30 Mbps, which the regulator attributed mainly to affordability and reliability for most subscribers. Tandaa’s Bronze plan sits squarely inside that mass threshold.

The two-month prepayment is equally revealing. For a small ISP, installation is not free just because the marketing page says it is free. A technician must visit the premises, a drop must be run, a router or customer device must be configured, back-office staff must record the account, and support must be ready for the first complaint. The customer’s first months have to cover part of that acquisition cost and filter out casual leads. A two-month activation payment also tests household cash flow. In a mobile-money country, the customer can top up mobile data in small increments. A fixed connection asks for commitment.

Tandaa’s economics improve when the customer stays, pays reliably and calls support only when something material has happened. They deteriorate when installation labour is spent on low-retention accounts.

The company also presents itself as a wholesale provider. LinkedIn says Tandaa offers wholesale internet to resellers. PeeringDB and route descriptions include language consistent with wholesale pools, network management, source NAT pools and a Nairobi point of presence for wholesale clients. The wholesale layer is important because it allows a small coastal operator to monetize capacity beyond direct retail households. It can sell to smaller neighbourhood Wi-Fi operators, estates, offices, cyber cafes, apartment blocks or local entrepreneurs that already have customer relationships.

Wholesale can improve utilization and extend reach without Tandaa hiring every last field worker itself. But it also creates a control problem. If the reseller sells badly, installs badly, over-contends capacity, ignores customer complaints or operates without the right authorization, the end user may still blame the upstream brand whose capacity makes the service possible.

Geography as a cost structure

Tandaa’s geography is not just a map. It is the cost structure. The official site’s coverage engine labels six coastal counties: Mombasa, Kwale, Kilifi, Tana River, Lamu and Taita-Taveta. It pins places along and near the coast including Kiunga, Lamu, Mambrui, Malindi, Watamu, Kilifi, Mtwapa, Kaloleni, Mazeras, Mombasa, Mariakani, Samburu, Mackinnon Road, Taru, Diani and Vanga. The site’s summary line says fibre and fixed-wireless are built for the coast, with a backbone labelled Mambrui to Vanga. LinkedIn’s public profile narrows the proven commercial base to Kilifi, Mikindani and selected environs.

That footprint is commercially coherent. Mombasa is Kenya’s coastal gateway for submarine cables, data centres and interconnection. Kilifi, Malindi, Watamu, Mtwapa, Diani and the other coastal towns are not one continuous dense Nairobi-style market. They are a chain of towns, tourist corridors, settlements, estates, businesses, schools, hospitality sites, government offices and households with different willingness to pay.

Fixed access economics depend on where Tandaa has a route, where a radio link or fibre drop is practical, where customer density is enough, and where a support crew can respond without turning every repair into a day-long dispatch.

In a dense urban block, a fixed ISP can spread installation and backhaul costs across many customers. Along a coastal corridor, the arithmetic is patchier. There may be excellent demand around a town centre, hotel cluster, apartment block, school, clinic, business park or estate, followed by stretches where customer density thins out. Wireless links can extend reach faster than fibre, but they introduce line-of-sight, spectrum congestion, tower, power and weather considerations. Fibre can deliver better capacity and latency, but it is capital-hungry and vulnerable to cuts, wayleave delays, roadworks and pole access costs.

Tandaa’s use of both fibre and fixed-wireless makes sense because the coast is not a single access topology.

Geography also creates a trust advantage. A local operator can be known by name. Customers can know the office, the technicians, the person on WhatsApp, the reseller in their estate, or the business owner who got connected last month. That familiarity matters in places where national operators may be slower to install, slower to repair or less interested in a small pocket of demand. But familiarity cuts both ways. A local operator has fewer places to hide. When a link is down in Kilifi, the story moves quickly through customers, resellers and local posts. In a known community, service quality becomes reputation, not only a metric.

The Mombasa interconnection advantage

The strongest infrastructure evidence for Tandaa is not on the home-pricing page. It is in Mombasa. PeeringDB lists Tandaa Networks/AS328734 at LINX Mombasa with a 10G open peering entry, IPv4 and IPv6 addresses, and a network profile showing mostly inbound traffic. It also lists Tandaa at iColo Mombasa One in Miritini, iColo Mombasa Two in Nyali, and SEACOM Mombasa CLS. iColo’s own MBA2 page lists Tandaa Networks among the networks present at the facility.

LINX describes Mombasa as a neutral internet exchange at iColo’s MBA1 and MBA2 facilities, built to keep coastal and regional traffic local rather than hairpinning everything through Nairobi, London or other distant hubs.

This is not cosmetic. For a coastal ISP, Mombasa interconnection can be a real edge. The more traffic that can be exchanged locally or through efficient peers, the less Tandaa depends on expensive, congested or indirect transit. Local peering can improve latency to content caches, cloud services, other Kenyan networks and regional routes. It can also make the operator more attractive to business customers and resellers who care about route stability.

Mombasa’s position as a subsea landing and interconnection point means a coastal operator does not have to be a peripheral buyer of backhaul from Nairobi; it can sit closer to the international and regional edge.

PeeringDB’s traffic ratio for Tandaa is mostly inbound, which fits a retail and small-business access provider. Households and offices download video, social media, operating-system updates, cloud documents and messaging content far more than they upload. That traffic shape is commercially important. The margin on a KES 2,399 or KES 3,599 plan depends on how cheaply Tandaa can deliver inbound content during evening peaks. A network with efficient content access, sensible caching, good peering and disciplined contention can sell modest plans profitably.

A network that pays too much for upstream capacity or lets evening congestion rise will convert every new customer into a future support ticket.

The route record also shows a network that is not tiny by local standards. Public directories show IPv4 blocks including 102.204.84.0/22 and 102.222.144.0/22, an IPv6 block, route descriptions for core network management, wholesale pools, source NAT pools, peering and a Nairobi point of presence, and valid RPKI observations in secondary tools. The article should not inflate route counts into subscriber counts. Addresses are not customers. Peering is not profit. But the routing evidence supports the view that Tandaa is an operating network with technical assets, not only a retail brochure.

Kenya is mobile-first, but fixed access is growing

Tandaa’s opportunity exists because Kenya’s fixed broadband market is growing. Its problem exists because the country is still overwhelmingly mobile-first. The CA’s third-quarter FY2025/26 report, covering January to March 2026, recorded 84.1 million active mobile subscriptions and a mobile penetration rate of 157.7 per cent. Mobile data subscriptions reached 62.6 million, with 84.4 per cent on mobile broadband. Mobile money subscriptions reached 53.4 million, a penetration rate above 100 per cent. Smartphones connected to mobile networks rose to 50.2 million.

Against that, fixed data and internet subscriptions reached 2.66 million. That is a serious market and it is growing quickly, up 7.9 per cent in the quarter. Fibre optic subscriptions reached 1.47 million, terrestrial wireless reached 950,317, and satellite reached 25,088 after strong growth attributed to low-earth-orbit services. But fixed access is still a smaller behavioural habit than mobile. A household that has phones, mobile money, WhatsApp, mobile bundles and possibly a mobile router does not automatically need a fixed line. Tandaa has to create a reason.

The fixed market is also not fragmented in a way that gives every small operator easy room. The CA’s top-ten table for March 2026 showed Safaricom leading fixed data subscriptions with 941,501 and a 35.4 per cent share, followed by Jamii Telecommunications at 517,270 and 19.5 per cent, Wananchi Group at 276,607 and 10.4 per cent, Poa Internet at 256,517 and 9.7 per cent, Ahadi Wireless at 245,423 and 9.2 per cent, Vilcom at 159,885 and 6.0 per cent, and Mawingu at 98,078 and 3.7 per cent. Starlink, Dimension Data and Liquid also appeared in the top ten. All other operators combined had 93,677 subscriptions and 3.5 per cent.

That table is sobering for Tandaa. The market is growing, but scale is already concentrated. Safaricom can cross-sell through mobile, M-Pesa, shops, brand trust and enterprise relationships. Jamii and Wananchi have established fixed broadband brands. Poa and Ahadi demonstrate that non-incumbent access models can become meaningful, but they also show how much execution is required to build a subscriber base. Starlink changes the fallback option in places where terrestrial networks are weak, though hardware and monthly pricing keep it from being a universal substitute.

Tandaa’s viable answer is local specificity. It does not need to win all of Kenya. It needs to be better in its coastal pockets than the customer’s available alternatives. That means faster installation where the big brand is absent, better local support where a call centre is slow, more relevant knowledge of a neighbourhood, and enough network quality that a household stops treating mobile data as the dependable fallback.

Unit economics: the KES 2,399 question

The explicit unit-economic problem starts with Tandaa’s Bronze plan: 25 Mbps for KES 2,399 per month, with free installation and two months prepaid. If a customer stays for only a few weeks, the company loses field time, device handling, account setup and support attention. If the customer stays for a year, the same installation becomes a recoverable acquisition cost.

The gross margin depends on take-up density along a route or around a wireless hub, the cost of backhaul into Mombasa or another point of presence, the cost of upstream transit and peering, router or customer-premises equipment recovery, power at relay sites, support labour, payment collection friction, and contention discipline at peak hours. Mobile substitution is the churn floor: if a household can fall back to Safaricom, Airtel, Telkom, Starlink, a neighbour’s connection or a cheaper reseller, Tandaa cannot rely on lock-in alone.

Its plans must deliver enough perceived reliability that KES 2,399 to KES 6,999 feels like a household utility rather than a speculative monthly spend.

That paragraph sounds mechanical, but it is the business. A small ISP’s economics are not won in a national market-share chart. They are won route by route. A 50-metre coverage buffer, a hub circle, a GPS pin, and a WhatsApp order flow are not just user-interface choices. They reveal the operator’s need to know exactly whether the premise is close enough to serve without turning a "free install" into an unpriced construction job. They also reveal why support labour matters. If a technician can do several installations or fixes in one area, the economics improve.

If every complaint requires a long trip, the monthly plan price cannot carry the cost.

Payment collection is part of the same equation. Kenya’s mobile-money infrastructure makes digital payment normal, but it also makes customers used to immediacy and flexibility. Tandaa’s two-month activation requirement gives the company cash up front. After that, retention depends on whether billing is clear, reminders are timely, and service interruptions do not coincide with payment disputes. A household that has prepaid and then experiences outages will feel the problem sharply. A business that pays for a fixed connection but keeps buying mobile bundles as backup will start questioning the fixed line’s purpose.

Wholesale and reseller discipline

Wholesale can be Tandaa’s accelerator and its risk. A reseller relationship can turn Tandaa’s Mombasa and coastal capacity into many neighbourhood retail points without Tandaa directly owning every customer relationship. It can help the company reach apartment clusters, cyber cafes, small offices and local entrepreneurs that already understand their streets. It can also create a useful hierarchy: Tandaa manages middle-mile, peering and capacity; the reseller handles close customer knowledge, installation, payment and support.

But the regulator’s compliance report shows why this model cannot be loose. CA observed that illegal internet entities were buying capacity from licensed players, including "Bluestreak Horizon (Tandaa)", and recommended that licensed upstream providers engage only licensed resellers and account for their last-mile networks. That is a direct warning about the economics of outsourced reach. A licensed operator cannot treat reseller revenue as clean if the downstream installation, customer handling or authorization is weak.

The upstream provider may not be responsible for every reseller decision in the customer’s mind, but the regulator and the market will still ask who supplied the capacity.

For Tandaa, the answer is governance as margin protection. Reseller screening, written terms, service standards, coverage accounting, last-mile records, escalation paths and clear customer ownership all look like overhead. In practice they protect the brand and reduce future losses. The cheapest reseller in a new estate can become the most expensive relationship if it triggers complaints, unpaid invoices, unauthorized installations or regulator attention. The best reseller can be a local distribution arm that gives Tandaa density it could not build alone.

That is why the identity question matters again. If Tandaa, Tandaa Group, Tandaa Communications and Blue Streak/Blue Streak Horizons sit in the same operating story, customers and resellers need clear lines of responsibility. The public evidence does not give enough detail to map the corporate structure. The commercial best case is that the company has rationalized licensing and branding while preserving the network assets. The weaker case is that customers see the brand, regulators see several legal names, and accountability becomes hard to understand when something goes wrong.

Support labour is not a side function

Small ISP support is often discussed as a cost after the network is built. For Tandaa, it is closer to the product itself. A 25 Mbps or 50 Mbps customer may not be able to distinguish between upstream congestion, Wi-Fi interference, a bad router, an overloaded reseller link, a fibre cut, a power problem at a relay site, packet loss at a peering point or an unpaid invoice. The customer experiences all of them as "the internet is down." If the company answers quickly, explains honestly and fixes the problem, the brand earns local trust. If the customer is ignored, the next sale in the neighbourhood becomes harder.

The official site leans into directness: no call-centre posture, WhatsApp order flow, support email, GPS pinning, free installation and a technician running the drop cable. That gives Tandaa a human edge. It also sets expectations. A customer who orders through WhatsApp expects WhatsApp-speed acknowledgement. A customer who gives GPS coordinates expects someone to know whether service is practical. A customer who prepays two months expects activation without a week of ambiguity.

The support burden rises with every product variation. Homes, businesses, CCTV, IoT and wholesale/reseller customers do not call about the same problems. A retail household may need Wi-Fi advice. A reseller may need capacity planning. A business may need restoration priority and predictable routing. CCTV and IoT services introduce power, device, camera, local network and storage issues that can be blamed on the ISP even when they are not pure connectivity faults. The more Tandaa sells beyond internet access, the more it needs disciplined support triage.

This is where smallness can be an asset. A national operator may have better systems, but a local operator can know the actual road, pole, building, estate, technician and reseller. That knowledge can reduce resolution time. The risk is that smallness becomes fragility. If the same few people hold too much operational knowledge, service quality becomes dependent on individual availability. The best local ISPs turn familiarity into documented practice. The worst ones rely on heroic technicians until the customer base outgrows them.

Unofficial market signals

The informal signals around Tandaa are mixed but useful. A local Kilifi ISP listing updated in January 2026 places Tandaa first in its Kilifi provider discussion, says it offers fibre and wireless connections in Kilifi, Mikindani and environs, and repeats a plan range from 10 Mbps to 100 Mbps starting around KES 2,399. Tandaa’s Facebook presence is small, with public positioning around affordable broadband for wholesale and retail users. iColo’s social post welcoming Tandaa to MBA2 reinforces the market signal that Tandaa is visible in Mombasa’s interconnection community.

TestMy.net’s host page, by contrast, showed modest public speed-test averages at research time, around 6.5 Mbps down, 2.8 Mbps up and 175 ms latency. That is not a controlled performance audit, and it may reflect a small or skewed sample, distant test paths, user Wi-Fi issues or old tests. It does suggest that Tandaa’s public speed reputation will depend on actual customer experience, not just the 25/50/100 Mbps plan labels. The absence of a large public complaint trail is also not proof of high satisfaction.

For a small coastal ISP, many complaints and compliments may live in WhatsApp groups, estate conversations, reseller relationships and local posts that do not become indexed review pages.

Those signals point to the same conclusion as the formal evidence. Tandaa has recognition in its local market and in the network community, but not enough public data to claim superior service quality. The company’s trust premium is still something to be earned in repeated interactions. A household will forgive a modest speed if support is honest and the service is stable for school, video, work and payments. It will not forgive repeated unexplained outages merely because the ISP is local.

Competitors and substitutes

Tandaa competes with several different products at once. The first group is national or large fixed operators: Safaricom, Jamii/Faiba, Wananchi/Zuku, Poa, Ahadi, Vilcom, Mawingu and others where they have coverage. These operators bring brand visibility, capital, existing subscribers and, in some cases, stronger retail systems. Safaricom’s fixed lead matters not only because of fibre share but because its mobile and M-Pesa base create trust and payment convenience. Jamii and Wananchi have long fixed-broadband recognition. Poa and Ahadi show that access providers outside the largest incumbents can scale when their distribution model works.

The second competitor is mobile broadband. CA data shows how powerful this substitute is. Mobile data subscriptions reached 62.6 million in March 2026, and mobile broadband consumption continued to rise. For a customer who streams moderately, uses WhatsApp, pays bills, does online classes and works occasionally from home, mobile data may be enough, especially if a fixed line is unreliable. Tandaa has to win on consistency, monthly value, local support or household multi-device use. If it does not, customers will treat mobile as the real internet and fixed access as optional.

The third substitute is satellite. Starlink’s Kenya base remains small compared with Safaricom or Jamii, but CA data places it in the fixed top ten, and satellite subscriptions grew in the quarter. On the coast, satellite is not the cheapest mainstream option for every household, but it changes the psychology in places where terrestrial service is weak or slow to install. A business, lodge, farm, school or remote household may consider satellite if local fixed options are unreliable.

The fourth competitor is the informal access layer: local Wi-Fi providers, resellers, apartment-network operators and small shops that aggregate demand. Tandaa may supply some of this layer through wholesale. It may also compete with it. Informal providers can be close to customers and cheap. They can also damage trust if performance is poor. The commercial challenge is to capture the benefits of local distribution without letting undisciplined resale erode the value of the Tandaa brand.

What the positive case requires

The positive case for Tandaa is credible but narrow. It requires the company to use Mombasa and Kilifi proximity as an operating advantage. The network should buy or exchange traffic efficiently at the coast, keep content paths short, avoid avoidable congestion, and use its local field knowledge to serve communities where national operators are slower or less responsive. It should treat wholesale as a managed channel, not just a bandwidth sale. It should make the identity record legible enough that customers, regulators and partners know who is accountable. It should keep pricing simple and support fast.

If Tandaa can do that, it does not need national dominance. A small ISP can be profitable in a chain of well-chosen coastal pockets if customer density is high enough, support travel is manageable, reseller partners are disciplined, and backhaul costs are controlled. The coast also has demand pockets that care about reliability: tourism, hospitality, remote workers, schools, clinics, county offices, traders, small enterprises, and households that need more stable connectivity than mobile bundles provide. Tandaa’s 25 Mbps and 50 Mbps plans may be exactly right for many such users if delivered honestly.

The positive case also benefits from Mombasa’s infrastructure growth. LINX Mombasa, iColo MBA1/MBA2, SEACOM and coastal subsea proximity improve the economics of being a coast-based network. Tandaa can participate in an internet ecosystem that did not exist at the same maturity a decade ago. The more content, cloud, cache and regional peering moves closer to the coast, the more a coastal ISP can reduce its dependence on distant handoff points.

What could go wrong

The negative case is also straightforward. First, the company could remain too small to absorb support shocks. A few major outages, poor reseller behaviour or delayed installations can damage a local ISP more than they would damage a national brand because the reputation pool is small. Second, pricing pressure could rise if larger operators expand deeper into Tandaa’s strongest areas. If Safaricom, Jamii, Wananchi or Poa can install quickly at comparable prices, Tandaa must compete on support and local trust, not merely availability.

Third, upstream and interconnection advantages do not automatically solve last-mile quality. A 10G peering port at LINX Mombasa is valuable, but the customer’s experience still depends on the access link, Wi-Fi, power, contention, field repair and payment status. Fourth, reseller compliance could become a direct risk. The CA’s enforcement language about illegal entities using licensed upstream capacity is a warning to any operator that sells wholesale without strong controls.

Fifth, the identity record could become a trust problem if not explained commercially. The public can see Tandaa Networks, Tandaa Group, Tandaa Communications, Blue Streak Horizons and Bluestreak Horizon in different places. There may be a perfectly ordinary group structure behind those names. But unless customers and partners can understand responsibility, the ambiguity creates avoidable friction. A telecom service is an accountability product. When it fails, the customer wants to know who owns the fix.

The judgement

Tandaa Networks is best understood as a real Kenyan coastal ISP whose value lies in local density, Mombasa interconnection and community trust rather than national scale. Its strongest assets are visible: a current consumer site, clear retail plans, direct order and support channels, public network resources, PeeringDB presence, LINX Mombasa peering, iColo and SEACOM facility evidence, and a market story around Kilifi and the coast. Its biggest risks are equally visible: mobile-heavy substitution, large fixed competitors, reseller discipline, modest public performance signals, and corporate/licence-name ambiguity in public records.

The company’s economic problem is not finding people who want internet. Kenya has more than enough demand. The problem is turning demand into profitable, retained fixed subscriptions in specific coastal communities. That requires a tight match between coverage and installation cost, enough backhaul and peering efficiency to keep evening performance acceptable, enough support labour to protect trust, and enough payment discipline to keep cash moving without alienating customers.

The decisive facts to watch are practical rather than rhetorical. Does Tandaa improve public performance signals as it grows? Does it publish clearer coverage and business-service evidence? Do reseller relationships become more formal and compliant? Does the current CA register continue to show Tandaa-named licence holders in the relevant categories? Does the company win visible businesses, estates or institutions outside its earliest Kilifi base? Does its Mombasa interconnection translate into lower-latency experience for ordinary users?

If the answers are positive, Tandaa can remain small and still matter. If the answers are weak, it will look like many local ISPs in fast-growing markets: technically real, locally visible, but commercially squeezed between mobile convenience, national fixed brands, informal resellers and the unforgiving economics of support.

Evidence register

https://www.tandaa.africa/ - Tandaa’s official site. It supports the current public identity, Kilifi/coastal positioning, support contact surface, retail ordering posture and the tagline used by the company.

https://www.tandaa.africa/static/js/main.5037c01b.js - Public site resource used to verify visible site content where the React app does not expose all text in the initial HTML. It supports the Bronze/Silver/Gold plan ladder, KES prices, free installation, two-month prepayment, WhatsApp order flow, support email, Kilifi headquarters label, coastal coverage counties and Mambrui-to-Vanga backbone label.

https://clients.tandaa.africa/login - Tandaa customer billing portal. It supports the existence of an account and billing surface under the Tandaa domain.

https://ke.linkedin.com/company/tandaa - LinkedIn company profile. It supports the description of Tandaa Networks as a privately held ISP founded in 2019, based in Kilifi, providing fibre and wireless connections in Kilifi, Mikindani and selected environs, wholesale internet for resellers, CCTV and IoT services.

https://www.peeringdb.com/net/24594 - PeeringDB network profile for AS328734. It supports Tandaa Networks Limited identity, ASN, website, open peering policy, Africa scope, mostly inbound traffic ratio, prefix counts, 20-50 Gbps traffic level, LINX Mombasa peering and Mombasa facility presence.

https://www.peeringdb.com/org/27318 - PeeringDB organization profile. It supports the Tandaa Networks Ltd/Bluestreak Horizon Net Ltd identity reconciliation, Kilifi/Mnarani address context and the description of Tandaa as a coastal ISP deploying carrier-grade IP transport and connectivity.

https://whois.ipip.net/AS328734 and https://bgp.tools/as/328734 - Public ASN/routing directories. They support AS328734 as

Tandaa-Networks, the Blue Streak Horizons Net Limited resource-holder name, Kenya/AFRINIC registration context, address in Kilifi, public route descriptions, RPKI observations and visible exchange participation.https://www.peeringdb.com/ix/4653 - PeeringDB LINX Mombasa profile. It supports the specific 10G Tandaa Networks peering entry at LINX Mombasa and the wider exchange context of 50 peers, 52 connections and significant total capacity.

https://www.linx.net/network/linx-mombasa/ - LINX official Mombasa page. It supports the analysis of Mombasa as a neutral coastal exchange at iColo MBA1/MBA2, designed to keep local and regional traffic local and reduce latency through direct interconnection.

https://www.icolo.io/location/mba2/ - iColo MBA2 official page. It supports Tandaa’s presence at a Mombasa/Nyali data-centre facility near subsea landing points, with Tandaa Networks/AS328734 listed among networks.

https://www.peeringdb.com/fac/1648 - PeeringDB SEACOM Mombasa CLS facility profile. It supports Tandaa Networks/AS328734 as a listed network at the SEACOM Mombasa cable landing station facility.

https://www.ca.go.ke/licensing-procedures - Communications Authority of Kenya licensing procedures. It supports the Unified Licensing Framework discussion, including NFP, ASP and CSP categories, general requirements and the possibility of holding multiple commercial licences with separate accounts.

https://www.ca.go.ke/sites/default/files/2026-05/REGISTER%20OF%20UNIFIED%20LICENSING%20FRAMEWORK%20LICENSEES.pdf - CA May 2026 register. It supports current regulator-list evidence for Tandaa Group Ltd under Network Facilities Provider Tier 3 and for Tandaa Communications Limited/Tandaa Group Ltd under Application Service Provider.

https://www.ca.go.ke/sites/default/files/CA/License%20Register/Revoked%20Licences/List%20of%20Revoked%20of%20Application%20Service%20Providers%20Licences.pdf - CA revoked ASP list. It supports the caution that Blue Streak Horizons Net Limited appears on an ASP revocation list, which is relevant to identity and licensing diligence.

https://www.ca.go.ke/sites/default/files/2025-04/COMPLIANCE%20AND%20ENFORCEMENT%20REPORT%20FOR%20Q2%20FY%202024-2025%20Revised%202.pdf - CA compliance and enforcement report. It supports the analysis of reseller and last-mile accountability risk where illegal entities buy capacity from licensed upstream providers.

https://ca.go.ke/sites/default/files/2026-06/Sector%20Statistics%20Report%20Quarter%203%20%20FY%202025-2026.pdf - CA third-quarter FY2025/26 sector report. It supports the Kenya market context: mobile and mobile-money scale, fixed broadband growth, fixed technology mix, speed-band distribution, top fixed operators and international bandwidth growth.

https://rejnac.com/internet-providers-in-kilifi - Local Kilifi ISP listing. It supports market-context claims about Tandaa’s local visibility, Kilifi/Mikindani footprint, competing local providers, and public price/speed perception.

https://testmy.net/hoststats/tandaa_networks - TestMy.net host statistics. It supports a cautious public performance-signal discussion, not a definitive network-quality conclusion.