Summary

- The paid unit for Internet Systems Group ISG is a local access and field-support account: installation, last-mile coordination, outage recovery, technical continuity and upstream discipline around a connection, not merely the retail price of a megabit.

- Official STPI material gives the strongest evidence for the service shape. It describes SoftNET, SoftLINK internet leased-line connectivity, Category-A ISP licensing, last-mile options, NOC support, redundancy, service statistics and all-India delivery claims; those facts are stronger than route-table inference.

- Public routing and registry records confirm resource stewardship and visible network presence around Software Technology Parks of India and AS7633, but they do not prove customer profitability, support speed, churn, contract price, utilisation, service credits or the quality of a particular field visit.

- The commercial risk is substitution. If a customer can tolerate cheaper mobile broadband, another local ISP, a national carrier link, satellite, an internal private link or a delayed installation, ISG's price is capped; if downtime and service uncertainty are expensive, local response can remain worth paying for.

The Renewal Moment

A useful way to value Internet Systems Group ISG is to start at the moment when a customer decides whether to renew a link after an outage, a slow installation, a building move or a price increase. The buyer is not only asking whether bandwidth is available somewhere else. In most Indian business districts, there is almost always another form of access: a national carrier, a neighbourhood ISP, mobile broadband, fixed wireless, a leased line from a large operator, a managed link through a building provider, or a plan to wait until fibre construction reaches the site.

The renewal question is narrower and more practical: when the circuit fails, who answers, who can reach the premises, who can coordinate the last mile, who has enough upstream leverage to keep the connection usable, and who carries the relationship when the cheap alternative becomes operationally expensive?

That is the setting in which ISG should be priced. The public directory page identifies Internet Systems Group ISG as an India-based regional internet service provider linked to a public directory entry at https://btw.media/en/directory/internet-systems-group-isg. The richer external evidence points to Software Technology Parks of India, its SoftNET internet services, and number-resource records using the Internet Systems Group ISG contact handle. STPI's own data-communication page describes High Speed Data Communication services, SoftNET, SoftLINK, point-to-point connectivity, microwave and fibre last-mile choices, a Category-A ISP unified licence, 61 independent gateways through NOCs at STPI centres, support practices and claimed uptime features at https://stpi.in/en/internet-services-data-communications. Those claims do not settle the economics, but they show the service being sold as managed access with support obligations rather than anonymous best-effort broadband.

The paid unit is therefore the local access and field-support account. The cheaper substitute is any access path that gives enough throughput without the same service wrapper: a large national operator, another local ISP, mobile broadband, 5G fixed wireless, satellite, an in-house private link, or a delayed installation. The costly driver is not simply wholesale capacity; it is the labour, coordination and redundancy needed to install, maintain and recover a customer connection. The strongest public evidence class is official STPI service and annual-report material, supported by TRAI market data and bounded APNIC/BGP records.

The three missing proof categories that would change the judgement are economics, reliability and retention: account-level margin and price, measured outage response and utilisation, and renewal or churn behaviour by customer type.

This makes the thesis modest but testable. ISG matters if the customer purchase unit is a staffed access relationship under local constraints. It matters less if the customer is buying only commodity bandwidth and can switch without meaningful operational loss. Public records can show that a network exists, that an organisation describes services, that a regulator counts subscribers, and that routes are visible.

They cannot show whether the technician arrived fast enough, whether the customer paid a premium, whether a competitor could have delivered the same service for less, or whether the account stayed because the service actually reduced downtime.

Identity And Operating Surface

The public identity trail around ISG is unusual because the most concrete records are not a glossy retail page under a standalone brand. They are institutional and technical records tied to Software Technology Parks of India. APNIC's public query for Internet Systems Group ISG returns a person/contact record with the handle II4-AP, Software Technology Parks of India address details in Bengaluru, and maintenance references connected to SoftNET at https://wq.apnic.net/apnic-bin/whois.pl?searchtext=Internet%20Systems%20Group. A handle is not a company balance sheet and not a customer list. It is a contact and resource-administration clue. Still, it matters because it places ISG in the operating surface where IP-number resources, network contacts and STPI infrastructure meet.

The institutional context is important. STPI describes itself as an organisation under the Ministry of Electronics and Information Technology, with a mandate that includes IT/ITES promotion, innovation support and data-communication services at https://stpi.in/en/about-stpi. Its citizens' charter also lists data-communication services among its public-facing functions and speaks in terms of quality services and negligible downtime at https://stpi.in/en/citizens-charter. The business inference should be bounded: STPI's broader public mandate does not mean every access account is profitable, nor does it mean every local service visit is better than a private competitor's. It does mean that the network service sits inside an institution that has reasons to value reliability, compliance, technology-park customers and support continuity.

The 2024-25 annual report gives the clearest scale markers. The report says STPI holds a Category-A ISP unified licence, provides SoftLINK internet leased-line connectivity through SoftNET, carried about 43 Gbps of internet bandwidth across the country to around 665 customers in 2024-25, used microwave and fibre for last-mile delivery, and reported nearly 99.9% uptime for the network service in that year. It also puts the organisation in a wider footprint of STPI centres and IT infrastructure. The report is available through STPI's annual-report page at https://stpi.in/en/stpi-annual-reports and the 2024-25 English report at https://stpi.in/sites/default/files/annual-reports-documents/stpi_annual_report_2024_2025_eng.pdf.

Those numbers help define the operating surface without completing the investment case. Roughly 665 customers against 43 Gbps implies a service book that is not mass consumer broadband. It is compatible with leased-line, institutional and business-service economics, where the paid unit can include account management, last-mile design, maintenance windows, escalation and local recovery. But the report does not disclose revenue per SoftNET customer, margin by service line, per-city utilisation, churn, service credits or customer concentration. It is group context and service description, not account economics.

The TRAI market record adds another bounded view. TRAI's Yearly Performance Indicators report for 2024-25 records India's huge broadband and internet market, with total internet subscribers near 969.10 million and broadband subscribers near 944.12 million as of 31 March 2025. It also lists Software Technology Parks of India with a small ISP subscriber base in the annexures, including a total of 672 internet subscribers at that date. The report is published from TRAI's performance-indicator page at https://www.trai.gov.in/release-publication/reports/performance-indicators-reports, and the 2024-25 PDF is at https://www.trai.gov.in/sites/default/files/2025-07/YIR_08072025_0.pdf. Again, the evidence is useful because it confirms small-scale ISP presence in a vast market; it does not tell us which subscriber is profitable or which link was renewed after a repair.

What The Customer Actually Buys

The customer does not buy a metaphysical thing called "internet" from a regional provider. The purchase is a bundle of usable access, local installation, responsibility for the last mile, escalation when the service degrades, and the expectation that someone familiar with the circuit can respond before the customer's own operations absorb too much loss. In a leased-line or business-connectivity setting, the invoice can look like bandwidth, but the decision often prices labour and continuity.

A buyer may compare two quotes on Mbps, then renew the more expensive one because the cheaper line does not solve the building entry, the RF path, the fibre handoff, the NOC escalation or the after-hours fault process.

STPI's own service language supports this interpretation. Its data-communication page does not describe only capacity. It describes point-to-point and point-to-multipoint access, SoftPOINT and SoftLINK services, telecom-network delivery, microwave and fibre last-mile options, multi-homed gateways, redundancy at last mile and network levels, 24x7x365 support by a qualified technical team, online bandwidth statistics and single-point contact for support. Those are operating promises around a connection. They are exactly the pieces that turn bandwidth into a field-support account.

The purchase unit also includes buyer anxiety. A software exporter, an IT park tenant, a data-processing office, a local service firm or a government-linked unit does not always have the internal staff to negotiate with every access-layer owner, test every last-mile path or argue with multiple providers during a fault. A regional provider with local history can sell simplification: one contact, one service history, one set of escalation habits, one support memory of the premises.

That support memory can be commercially valuable if it prevents repeated truck rolls, avoids fresh surveys, or gives the buyer confidence that a link change will not create a new operational problem.

The evidence does not let us claim that every ISG or SoftNET customer buys this exact bundle. It lets us say the public service description points in that direction. STPI's SoftNET material names the ingredients of managed business connectivity, and the annual report's customer count and bandwidth scale are consistent with a business-access model rather than a mass retail broadband business. The economics therefore depend on the willingness of customers to pay for support, not only on market price per Mbps.

This matters in the "cheaper access" comparison. If the buyer needs only a backup connection for email and basic browsing, a low-cost mobile plan or an inexpensive local broadband line can be sufficient. If the buyer's downtime cost is high, the cheaper substitute may be a false saving. The gap between those two cases is the space where ISG can earn a premium or lose the renewal. The price ceiling comes from substitutes; the price floor comes from the actual cost of field labour, upstream capacity, maintenance and support.

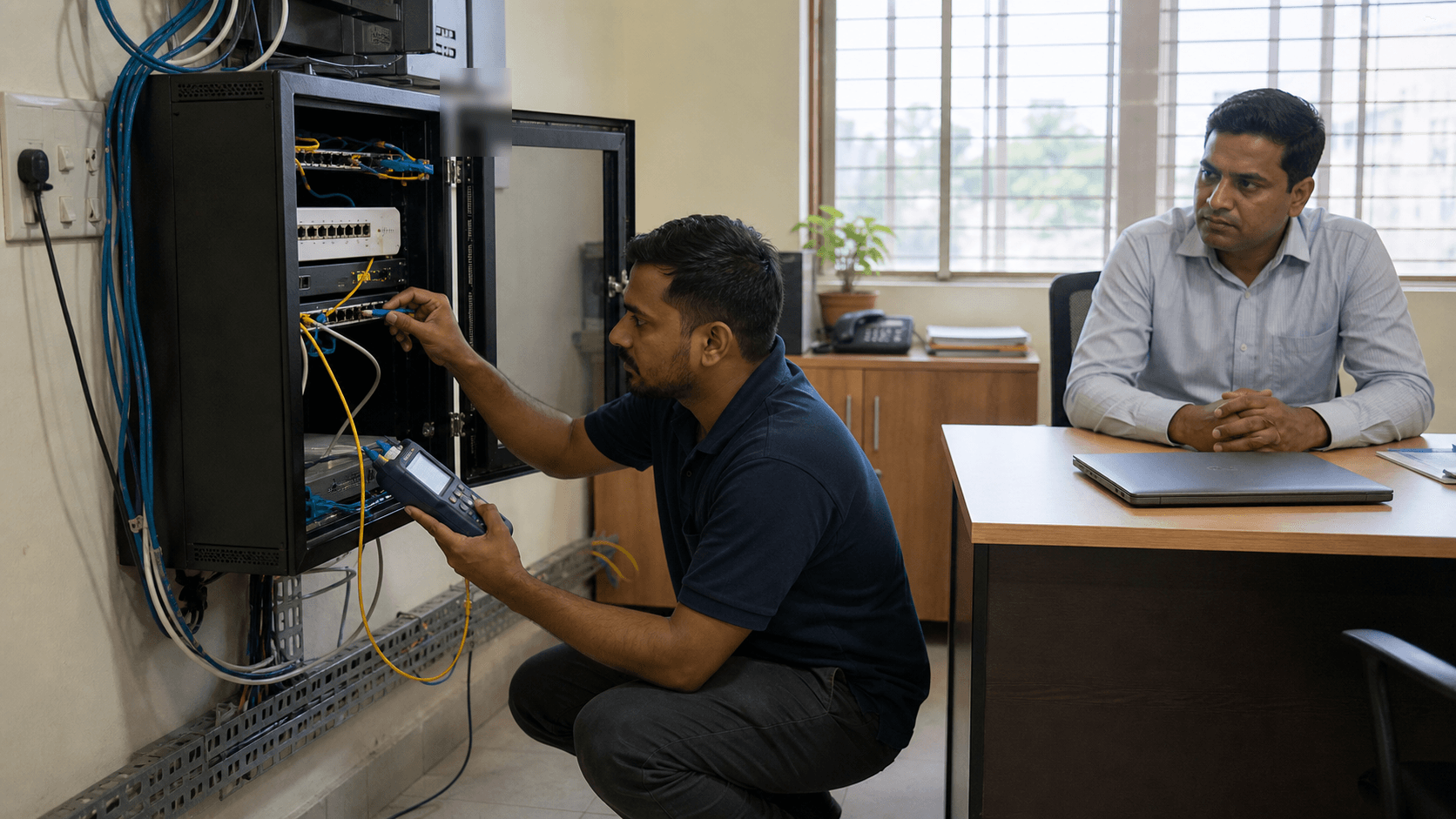

Why The Unit Is Costly

The cost structure begins with last-mile reality. A provider can buy upstream capacity and still fail commercially if it cannot deliver the final connection reliably into a customer's premises. STPI's public page describes multiple last-mile modes: RF and microwave, point-to-point radio, copper or fibre through major service providers, and fibre switches at NOCs meant to reduce provisioning time and improve troubleshooting. Each method carries different costs. Microwave needs line-of-sight, rooftop access, survey work, spectrum or equipment discipline, maintenance and weather resilience.

Fibre needs route availability, civil coordination, building entry, fault isolation and dependency on the party controlling the strand. Copper can be cheaper but may not support the same performance or recovery expectation.

Local support labour is the second cost. A help desk can close tickets cheaply when the fault is a remote configuration issue. It is expensive when someone must visit a roof, inspect a fibre handoff, coordinate with a building manager, replace equipment, re-terminate a cable, test signal levels or argue with a wholesale access owner. A field technician's time is not only wage cost; it is scheduling, vehicle time, spares, safety, coordination, supervision, repeat visits and the cost of keeping enough skilled staff available for failures that arrive unevenly.

This is why a regional provider can look costly next to mobile broadband while still being rational for a customer whose outage loss is larger than the monthly discount.

Redundancy is the third cost. The official service page emphasizes redundancy at the last mile, router, switch and gateway levels, along with multi-homed gateway design. Redundancy consumes capital and operating expense before it produces visible revenue. Spare paths, spare equipment, upstream diversity and monitoring tools are valuable only when a fault happens. In quiet months, the buyer can mistake resilience for overpricing. In a bad month, the same buyer may treat resilience as the product.

Upstream capacity and interconnection are the fourth cost. A provider that originates or manages routes still depends on upstream and peer relationships for reachability beyond its own network. Public BGP views show that AS7633 has observed connectivity involving major Indian networks such as Tata Communications, Bharti Airtel, Reliance Jio, Bharti Telesonic, Powergrid Teleservices and BSNL at https://bgp.he.net/AS7633. The observed route table is not a contract file. It does not show price, committed information rate, settlement terms, capacity headroom or outage history. But it does show that the network is not isolated, and that upstream bargaining and interconnection discipline are part of the business.

The fifth cost is administration. IP-number resources, reverse DNS, abuse contacts, routing entities, registry updates, licence obligations, reporting and internal controls take staff time. APNIC explains that Whois stores address usage, routing policies, reverse DNS delegations and network contact information for operational purposes at https://www.apnic.net/manage-ip/using-whois/. IRINN, the Indian registry for internet number resources, frames its role around IPv4, IPv6, autonomous-system numbers and resource management at https://www.irinn.in/. These records are not revenue evidence, but they remind us that a business-access provider must maintain more than cables.

Upstream Bargaining And Peering

The upstream question is where a regional or institutional ISP can be either disciplined or squeezed. If it has credible alternatives for transit, peering and exchange access, it can control quality and cost. If it depends too heavily on one upstream path, it may have less leverage during price increases, faults or congestion. Public records show pieces of this story but not the full commercial picture.

APNIC's aut-num record for AS7633 identifies Software Technology Parks of India - Bangalore and SoftNET-AS-AP at https://wq.apnic.net/apnic-bin/whois.pl?searchtext=AS7633. The same record includes legacy policy information naming imports and exports with AS701 and AS97. That is useful history, not a current purchase contract. The stronger contemporary public clue is a route-collector view such as Hurricane Electric's AS7633 page, which lists observed prefixes, peers, RPKI status and exchange presence at https://bgp.he.net/AS7633. HE's page showed a meaningful number of originated prefixes, observed peers and RPKI-valid routes when reviewed. This supports the claim that AS7633 has public routing presence and multiple visible counterparties.

Multiple visible peers are not the same as bargaining power. A peer relationship may carry little traffic, may be mediated through an exchange, may be mostly backup, may have low capacity, or may not represent a commercial agreement at all. A transit path may be contracted by another part of the organisation. Route visibility can persist after commercial importance changes.

The right conclusion is narrower: the public network record is consistent with a network that participates in the broader internet routing system and has observable reachability; it does not prove that ISG has cheap upstream terms or enough spare capacity to protect margins.

The bargaining issue also works at the access layer. A provider may own some last-mile assets and still rely on fibre or copper from large service providers for particular buildings. STPI's service page explicitly describes last-mile options that can use major service providers alongside its own microwave or radio networks. That means the provider's unit economics can vary account by account. A building served by existing fibre and known equipment can be profitable. A difficult rooftop, a weak line-of-sight path or a recurring third-party fibre fault can turn a contract into a low-margin support burden.

This is where upstream bargaining and local labour meet. A provider with several upstream and last-mile options can protect the customer better, but only if the commercial contract allows it to spend on redundancy and recovery. A customer that buys the cheapest possible plan may not have funded the resilience it expects. A provider that oversells support may face the opposite problem: it promises field response that its staff, spares or third-party access owners cannot deliver consistently.

The key private facts would be port utilisation, committed bandwidth by customer, upstream rate cards, peering and transit contract terms, fault-ticket resolution times, last-mile ownership by account and the share of customers with funded redundancy. None of those appear in public routing records. Without them, the best analysis treats upstream discipline as a plausible economic differentiator, not a proven margin engine.

Competition: The Cheap Substitute Is Real

The competitive pressure is not theoretical. India is one of the world's largest internet markets, and TRAI's 2024-25 report shows a market dominated in subscriber volume by wireless and broadband scale. Wireless ARPU, data usage and data revenue per GB in the report illustrate the pressure that cheap mobile data can put on any access provider whose customer need is not genuinely specialised. A business buyer can look at low-cost mobile broadband, a second SIM router or fixed wireless and ask why a managed connection costs more. The answer must be operational, not rhetorical.

National operators create a different pressure. Large carriers can price aggressively, bundle connectivity with voice, cloud, security or managed services, and use national fibre reach to win business accounts. They may not always be faster on a particular field visit, but they can often present a lower headline price or a broader procurement relationship. If a customer already buys services from Bharti Airtel, Reliance Jio, Tata Communications, BSNL or another large operator, the incremental cost of adding one more link can look attractive.

Public AS7633 peer observations that include some of those names show ecosystem proximity, not immunity from their competition.

Local ISPs pressure the other side of the account. A neighbourhood provider may know a building better, have faster informal access to a rooftop or riser, or quote a lower installation fee because it already serves nearby customers. This can be especially powerful for small offices where uptime loss is annoying but not catastrophic. The regional provider's advantage must then come from credibility, compliance comfort, service history or better escalation, not just local presence.

Satellite and fixed wireless add future optionality. In 2025, reporting on Starlink's India licence progress highlighted the direction of satellite competition and the continuing role of regulatory approvals, security review and spectrum arrangements in making that access commercially available; one public report is at https://apnews.com/article/6d6c924fa5ca1c1dd9e97dfedcf6420d. Satellite does not automatically replace a managed terrestrial link. Latency, indoor installation, weather resilience, pricing, policy terms and business support all matter. But it increases the menu of substitutes for some customers, especially where terrestrial construction is slow or expensive.

Delayed installation is also a competitor. A customer may decide that it can wait, use temporary wireless access, split workloads or keep an existing imperfect line rather than pay a premium for a new managed service. This is important because it reframes churn. Churn is not only a switch to another named provider. It can be a decision not to buy now, to reduce bandwidth, to postpone redundancy or to accept lower service quality.

Therefore, ISG's defensible position is not "access exists." Access is abundant in some areas and improving in others. The defensible position is "this access can be installed, maintained and recovered with lower operational uncertainty for a customer whose downtime cost justifies the premium." That position can be strong for some business and institutional accounts and weak for price-sensitive customers that treat connectivity as interchangeable.

Revenue Logic And Customer Dependence

The revenue logic of the local access and field-support account is a mix of recurring service fees, bandwidth tiers, installation or provisioning charges, possible value-added services, and the implicit renewal value of trust. STPI's public material describes internet leased-line connectivity, point-to-point services and bandwidth-on-demand features. It does not publish the contract book.

The annual report's service statistics allow only a cautious inference: with about 43 Gbps carried to around 665 customers, the operation appears to be focused on fewer, more service-intensive accounts rather than millions of small retail subscribers.

TRAI's annexure number, listing STPI at 672 internet subscribers as of 31 March 2025, is broadly consistent with that scale. But it should not be forced into a revenue model. A subscriber in a regulator table may not equal a commercial customer in an annual report; a customer may have multiple links; a subscriber may have different speed, service class or geography; and the count says nothing about price. The value of the TRAI number is comparative. In a national market with hundreds of millions of broadband users, STPI's ISP count is small. Smallness can be a weakness if it means limited scale.

It can be a feature if the service is deliberately focused on institutional or business connectivity that needs higher support attention.

Customer dependence is the central uncertainty. If revenue is concentrated in a few large accounts, retention and support quality become more important because one lost renewal can matter. If accounts are diverse but small, field labour can become expensive relative to monthly fee. If customers are tied to STPI infrastructure, technology parks or public-sector affiliations, the churn profile may differ from that of normal retail broadband. The public record does not disclose the mix.

The customer purchase unit helps discipline the inference. A buyer that values field response can renew even when a cheaper link is available. A buyer that values only throughput will compare prices and churn. The article's judgement therefore turns on what the customer is actually solving. An export-oriented software office with service commitments to overseas clients may value predictable repair and managed escalation. A small office using cloud applications with flexible hours may not. A public-sector or incubator-linked user may value institutional compatibility. A price-sensitive private user may choose another provider.

The market signal to watch is not only advertised price. It is whether customers complain about or praise installation speed, fault handling, after-hours response and billing clarity. Public reviews, forums and informal comments can colour that risk, but they cannot establish account economics by themselves. A few loud complaints may reflect normal service noise; a few positive references may reflect isolated success. The better evidence would be repeat-renewal rates, fault-ticket ageing, service-credit frequency, customer cohort retention and support staffing by region. Those facts are private.

Pricing The Account Against Cheaper Access

The cleanest pricing test is to ask what problem disappears when the customer pays more. If the problem is simply "the office needs internet," the cheaper substitute has a strong case. If the problem is "the office needs a connection that someone can install, monitor, explain and recover when the local handoff fails," the managed account has a better case. This difference is not semantic. It determines which cost line the buyer is comparing. A commodity access comparison looks at monthly tariff and headline speed.

A field-response comparison looks at installation risk, downtime cost, staff distraction, customer commitments, security comfort and the cost of coordinating multiple suppliers during a fault.

For ISG, the customer purchase unit should be priced as a bundle of four commitments. The first is access: the physical or wireless path, the port, the bandwidth tier and the route to the wider internet. The second is installation: survey, building access, line-of-sight assessment where relevant, fibre or copper handoff, equipment setup and acceptance testing. The third is continuity: monitoring, escalation, upstream or last-mile coordination and restoration. The fourth is memory: knowledge of the customer's site, past faults, equipment, contacts and tolerance for downtime.

The fourth item is often the least visible in a quote and the most visible during a renewal dispute.

The cheap substitute can attack each commitment differently. Mobile broadband attacks access price. A national carrier attacks scale and bundled procurement. A local ISP attacks proximity and installation speed. Satellite attacks locations where terrestrial delivery is slow or unreliable. An in-house private link attacks control. Delaying installation attacks urgency. ISG's response cannot be that those substitutes do not exist. It has to be that the full expected cost of those substitutes is higher once field response, support continuity and operating risk are included.

That expected-cost argument is strongest when the customer has measurable outage loss. A software export unit with deadlines, a service desk handling external clients, a small data-processing office, a regulated service provider or a technology-park tenant may treat internet failure as more than inconvenience. Every hour of uncertainty can mean staff idle time, missed delivery commitments, additional mobile workarounds, reputational cost and managerial distraction. In that case, paying for a provider that knows the site and has escalation routines can be rational even if the monthly price is higher.

The argument is weaker for customers with low switching friction. If cloud applications can tolerate mobile backup, if staff can work from home, if a national operator already serves the building, or if downtime has low revenue impact, cheaper access becomes harder to beat. The buyer may still value support, but not enough to fund redundant paths or rapid dispatch. That creates a margin trap for the provider: it may carry support expectations while customers pay commodity prices. In such accounts, the right commercial answer may be a lower service tier, clearer limits or a refusal to promise recovery that the price cannot fund.

Public documents rarely show this trade. Annual reports can say customers and bandwidth; regulator tables can count subscribers; service pages can describe redundancy. None of that reveals the price conversation at renewal. The decisive evidence would be a side-by-side comparison of quoted service levels, actual repair history and customer loss from downtime. Because that evidence is private, the article's judgement stays conditional: ISG's business case improves as the customer's outage cost and support complexity rise, and weakens as access becomes interchangeable.

Supplier Dependence By Account

Supplier dependence is not a single corporate ratio. It changes from one customer site to another. A link served over a known STPI microwave path has a different dependency map from a link delivered through third-party fibre. A circuit in a well-served technology park has different economics from a circuit requiring fresh rooftop access, civil coordination or a difficult building handoff. The official service page is useful because it names multiple last-mile modes, but the same variety means margins can diverge widely across accounts.

The access supplier can own the bottleneck even when ISG owns the customer relationship. If a fibre strand is controlled by a major service provider, ISG may have to coordinate repair without controlling the field crew that fixes the cut. If a building manager limits access to a riser or rooftop, the provider may carry customer anger without controlling the door. If a radio path depends on line-of-sight and local equipment conditions, the provider may need skilled labour even when upstream capacity is adequate. These are practical constraints that do not appear in subscriber counts.

Upstream dependence has the same account-level character. A provider may have multiple observed peers or upstream paths but still face congestion, pricing pressure or operational concentration on a route that matters to a specific customer workload. A customer using foreign SaaS platforms may care about international reachability; a customer exchanging traffic with domestic networks may care about Indian interconnection; a customer with backup workloads may care about burst capacity. Public BGP tables can suggest reachability but not the quality of a path for a customer's application mix.

The field-support account therefore requires commercial discipline. A provider should avoid selling a premium recovery promise where it has weak supplier control and no funded redundancy. It should charge properly when the account needs spare equipment, alternative last-mile paths or frequent site work. It should separate access price from support expectation so the buyer understands why a cheaper quote may deliver less recovery. If the provider fails at that separation, it can be squeezed from both directions: suppliers raise cost or slow repair, while customers benchmark against cheap access.

This supplier-dependence lens also keeps the public evidence in proportion. A Category-A ISP licence and AS7633 route visibility show operating capacity and legal scope. They do not say that a particular building's handoff is under ISG's direct control. A national centre footprint shows reach. It does not say that every local support team has equal skill or spare inventory. The account is where the economics land.

Group Context And Its Limits

STPI's broader public role can make the service more credible to some buyers. A technology-park customer or public-sector-linked user may value institutional continuity, documented processes, established centres and a provider that understands compliance-sensitive environments. The annual report's centre footprint, infrastructure discussion and data-communication service narrative all help explain why the service can exist at national scale. They also explain why a buyer might trust the provider more than a lightly capitalised local access reseller.

But group context has a hard limit. STPI's total revenue, expenditure and surplus do not tell us whether the ISG-relevant access account is profitable. A surplus in the organisation can coexist with a low-margin connectivity service. A public-service objective can justify a service that is strategically important even if it is not the highest-return activity. Conversely, a small subscriber base can produce strong economics if customers buy high-support leased connectivity. The annual report does not settle which case applies.

This matters because parent or institution evidence can easily become a false comfort. If an analyst says "STPI is established, therefore this access service is economically strong," the key step is missing. Establishment can reduce counterparty risk and support trust, but it does not pay for a difficult truck roll. It does not prove that customers accept price increases. It does not prove that upstream suppliers offer favourable terms. It does not prove that an outage is restored inside a customer's tolerance window.

The better use of group evidence is to define capability boundaries. The public material supports a view that the provider has an institutional service platform, NOC language, declared redundancy, national service intent and a named network-resource footprint. It supports the idea that ISG should be considered in the category of managed business access rather than informal neighbourhood broadband. It does not support a claim that the service has pricing power everywhere.

This distinction protects the article from two opposite mistakes. The first mistake is dismissing ISG because the public directory entry is short and the consumer market is dominated by large names. The second is overstating ISG because official pages and route records look substantial. The right middle position is that ISG appears commercially relevant where support-weighted access is valuable, and commercially exposed where customers can buy the same practical result more cheaply.

Regulation And Operating Risk

Regulation matters because connectivity is not an unregulated local trade. STPI's page says it holds a Category-A ISP unified licence with all-India service area. That licence context matters for eligibility, lawful operation, reporting and compliance. It also introduces risk. Telecom policy, licence terms, security requirements, lawful interception obligations, spectrum and satellite policy, right-of-way rules, and number-resource administration can alter both cost and competitive position.

TRAI's performance-indicator reports provide the market frame, but the larger regulatory environment is broader than any one table. A provider serving business or institutional accounts must keep records, handle abuse and operational contacts, manage resource information and comply with network rules that can change. APNIC and IRINN records show the public-facing administration layer for number resources. Licence and regulator filings show only part of the operating load. The rest appears in staff time, compliance systems, vendor management and the ability to respond when regulators or upstream networks require changes.

Operational risk is more immediate. Microwave and RF links can face line-of-sight issues, rooftop access disputes, weather effects, equipment failures and interference. Fibre can be cut, delayed by civil work, constrained by building access, or dependent on another carrier's repair schedule. Power, cooling and equipment spares can decide whether a theoretical redundant path works during an actual fault. A NOC can detect a problem quickly and still be limited by field access. That is why the paid unit includes field response: the network is not only a map of links but a practice of keeping them usable.

There is also institutional risk in reading STPI evidence. STPI's public mandate and annual report are credible starting points, but they are not a standalone proof of commercial excellence. A public or quasi-public institutional setting can bring trust, reach and stability. It can also bring slower procurement, uneven local execution, legacy systems or pricing that does not match private-market expectations. The article should not assume either virtue or weakness. It should ask whether the customer receives enough practical service benefit to justify any premium over cheaper access.

Geopolitical and national-policy risk is indirect but real. Internet infrastructure in India sits in a policy environment where security review, data governance, telecom competition, satellite entry and public digital infrastructure all affect business access. A provider with government-linked institutional history may be better placed for some compliance-heavy customers and less flexible for others. The evidence available here does not show whether that helps or hurts ISG's renewal economics. It only shows that the service is embedded in a regulated and policy-sensitive environment.

What Public Network Records Prove

Public network records are useful because they reduce ambiguity about existence, contact, resources and route visibility. APNIC's II4-AP record connects Internet Systems Group ISG to Software Technology Parks of India contact details. APNIC records for SoftNET and STPI address blocks, such as https://wq.apnic.net/apnic-bin/whois.pl?searchtext=SOFTNET-IN and https://wq.apnic.net/apnic-bin/whois.pl?searchtext=164.164.0.0, show resource assignments and related administration. The AS7633 record identifies a SoftNET autonomous system. HE's BGP view shows public routing observations for that autonomous system. Together, these facts support a conclusion that the relevant network has public-number-resource presence and route visibility.

They also help separate real operating evidence from marketing language. A service page can claim reach; number-resource and route records can show that routes and contacts exist in public infrastructure systems. A regulator table can show that a provider is counted in official ISP subscriber data. An annual report can disclose service scale, bandwidth and uptime claims. The strongest reading combines all of these: official service description, annual-report scale, regulator listing and public routing presence.

But the records do not prove the commercial outcome. A route object is not a customer. An ASN is not a profit centre. An IP block is not a service-level agreement. A visible peer is not necessarily a paid contract or a resilient capacity path. A contact handle is not a field team. A route table cannot tell whether a customer's application was reachable during a fibre cut, whether a technician had the right spare part, or whether a customer renewed because the provider solved the problem quickly.

They also do not prove modernity by themselves. Some registry records can carry legacy descriptions or policy statements that remain visible after network design changes. APNIC explains that Whois is an operational database for address usage, routing policy, reverse DNS and contacts, not a commercial disclosure system. HE's BGP page is an observed routing view, not an audited service report.

The right method is to treat these records as bounded evidence: they can support existence, administration, address space, route origin and visible counterparties; they cannot support claims about current contract terms, customer experience or profitability.

For ISG, this limitation is not a footnote. It is part of the commercial mechanism. The public record leaves open the very facts a customer would care about most: how often links fail, how fast support responds, what redundancy is funded, what the customer pays, what competitors quote, how congested upstream paths become, and whether renewal is driven by satisfaction or lock-in. A serious assessment must keep those facts open instead of filling them with route-table confidence.

Field Response As The Premium

If ISG earns a premium, it is likely earned in the difference between a link and a solved fault. Field response has economic value because outages are local before they are abstract. The customer experiences a broken video call, a failed build upload, a missed client deadline, a dead payment terminal, an unreachable office VPN, a support queue that cannot work, or a data-transfer delay. The provider experiences a ticket, a circuit ID, a suspected last-mile issue, a vendor call, a technician dispatch, an equipment question and a recovery target. The business value lies in collapsing the distance between those two views.

Local support labour is not glamorous, but it is a defensible product when the customer cannot self-serve. A national operator may have a stronger backbone but a slower building-level response in a particular locality. A cheap ISP may be fast in one building and unreliable in another. Mobile broadband may be good enough until indoor signal, contention, device management or monthly data patterns become a constraint. Satellite may be useful where terrestrial access is weak, but it has its own installation, policy and service variables.

The provider that can diagnose and recover the actual customer site may win even when its Mbps price is not the lowest.

The official STPI material repeatedly points to support structure: NOCs, single-point support, fault logs, technical support, redundancy and network management tools. Those terms are not enough to prove performance, but they tell us what the provider wants customers to value. The commercial test is whether customers experience those features as lower downtime. If they do, the premium is rational. If they do not, the same features become marketing overhead.

Field response also affects upstream bargaining indirectly. A provider with disciplined support can identify whether a fault is upstream congestion, last-mile failure, customer-equipment error or local power trouble. That diagnostic ability reduces wasted work and strengthens escalation with suppliers. A provider without that discipline can spend more on repeated visits while customers still see poor service. In other words, support labour can protect both revenue and cost, but only when it is organised well.

This is why the customer purchase unit cannot be reduced to bandwidth. The buyer is purchasing response capacity under uncertainty. The seller is carrying standby labour and operational know-how that may be invisible during normal service. Cheaper access wins when the buyer does not value that standby capacity. ISG wins when the buyer's expected outage cost exceeds the price gap.

Unofficial Signals And Their Proper Weight

Unofficial market signals can be useful, but only when kept in their place. Search snippets, informal complaints, social comments, job postings, procurement notices, peer references and local trade talk may reveal whether a provider is known for slow installations, trusted field staff, public-sector reliability, billing friction, old equipment or niche strength. They can also mislead. Connectivity markets create strong feelings because customers usually speak publicly when something breaks, not when a circuit runs quietly for months.

For ISG, the public evidence base available here is strong enough that informal signals should not carry the main conclusion. Official STPI pages, the annual report, TRAI reports, APNIC records and BGP views already establish the service shape, institutional setting and network presence. Informal signals would be most useful for the unresolved parts: whether local support is actually responsive, whether customers perceive value against cheaper access, whether renewal friction is high, whether installation lead times vary by city, and whether competitor quotes are forcing discounting.

The absence of rich public chatter is itself only a weak signal. A small business-access provider or institutional service can have limited consumer-facing review volume because its customers buy through procurement, local account relationships or technology-park channels. Low visibility does not mean low quality; it may mean the service is narrow. Conversely, quiet public channels do not prove satisfaction. The best use of unofficial signals is to identify questions for field research, not to settle them.

The relevant market question is therefore not "what do public comments say?" but "what would a buyer hear from comparable customers?" A strong buyer reference would say that installation was predictable, support understood the site, outages were resolved quickly, and the provider was worth the price gap. A weak reference would say that the same support features were promised but the customer still had to chase multiple parties while cheaper alternatives improved. Those are retention facts, not route facts.

Private Facts That Would Change The Assessment

The first changing fact is account-level gross margin. If ISG or the relevant SoftNET service earns healthy margin after upstream, last-mile, field-labour and support costs, then the premium story is financially stronger. If the service is thinly priced or cross-subsidised, the strategic value may be institutional rather than commercial. STPI's annual report gives total revenue, expenditure and surplus for the organisation, but it does not isolate SoftNET account margin. Group surplus cannot be treated as proof of line-level profitability.

The second changing fact is outage and response performance. Claimed uptime is useful, especially when the annual report cites nearly 99.9% for the network service, but customers buy experienced reliability. Mean time to repair, repeated-fault rates, service-credit incidence, customer-impact minutes, after-hours dispatch success and last-mile vendor performance would determine whether field response is real. Public material does not disclose those metrics by region or customer type.

The third changing fact is churn and renewal. If customers renew at high rates after comparing cheaper access, ISG's support premium is validated. If customers renew mainly because switching is inconvenient or because alternatives are not yet installed, the premium is more fragile. If customers churn when national operators or local fibre providers enter a building, then the local support value is weaker than the service language implies. Public records do not disclose cohort retention, win-back data or reasons for cancellation.

The fourth changing fact is utilisation. A provider carrying 43 Gbps to hundreds of customers can be either comfortably provisioned or capacity-constrained depending on committed information rates, peak usage, oversubscription, contention and upstream headroom. Route tables cannot answer this. A visible peer list does not show whether peak traffic is smooth or congested. Utilisation would affect both quality and cost, and therefore the ability to defend price.

The fifth changing fact is competitive quote behaviour. If national operators and local ISPs quote far below ISG for similar service levels, ISG must justify the gap through response, compliance or reliability. If competitors are cheaper only for best-effort access and become expensive once business support and redundancy are included, ISG's positioning improves. Public price pages rarely capture negotiated business-service reality.

The sixth changing fact is local staff coverage. Field response is only valuable if the staff can reach sites quickly and solve problems. A national service claim can hide uneven city-level execution. The annual report and service pages describe national reach, centres and NOC infrastructure, but they do not show technician density, spare inventory or dispatch times by market. For a customer, those local facts are the product.

Bottom Line

Internet Systems Group ISG should be assessed as a support-weighted access business. The public record is sufficient to show an institutional internet-service surface tied to STPI, SoftNET, business connectivity, public number-resource administration, regulator recognition and visible routing. It is not sufficient to show that every account is profitable, that field response meets customer expectations, or that upstream terms are favourable.

That distinction is the investment and operating judgement. ISG's value is strongest where a customer buys continuity: a connection that can be installed, watched, repaired and escalated by a provider with local knowledge and institutional infrastructure. Its value is weakest where the customer buys only cheap throughput. In a market with national operators, mobile broadband, fixed wireless, satellite options and local ISPs, the customer can always price the alternative. The provider has to prove that the alternative is cheaper only before the fault.

The evidence supports a cautious positive view of service relevance, not an unqualified claim of economic power. STPI's official material and annual report make a credible case that SoftNET-style connectivity is built around managed support, redundancy and business access. TRAI data places the service in a vast and competitive national market with a small ISP footprint. APNIC and BGP records confirm resource and routing presence while sharply limiting what can be inferred. The missing facts are exactly the facts that decide the renewal: price, margin, utilisation, outage response, customer satisfaction and churn.

For a customer deciding whether to renew, the question is practical. If a cheaper substitute can meet the same operational need, ISG loses pricing room. If local support labour, upstream discipline and service memory prevent expensive downtime, the premium can be rational. Public network records can point to the network. They cannot tell us whether the technician got there in time.