Summary

- Hrvatski Telekom's strongest public investment case is not simply that it is the incumbent in Croatia. It is that Croatia's network demand is unusually uneven: the Adriatic tourism machine puts huge summer pressure on mobile data, roaming, fibre backhaul, coastal repair crews and island coverage, while the operator must finance spectrum, FTTH, fixed-wireless capacity, regulated access and cybersecurity obligations through the whole year.

- The company entered 2026 with visible operating momentum: 2025 revenue rose 3.6%, adjusted EBITDA after leases rose 3.3%, capex after leases rose 10.5% to EUR 268 million, FTTH coverage reached 1 million households, and Q1 2026 revenue and adjusted EBITDA AL continued to grow. The harder judgement is whether those margins come from durable network advantage or from inflation-linked pricing, tourism-season roaming, handset and accounting mix, and Deutsche Telekom group scale that public reporting does not fully isolate.

- Public evidence supports treating HT as a strategically important national operator, but not as an unambiguous monopoly rent story. HAKOM data show fibre overtaking copper in Q1 2026, heavy migration from copper to fibre wholesale access, large seasonal roaming swings in Q3 2025, and continuing regulation of access, spectrum and security. Independent tests show HT strong on speed and coverage, while Telemach and A1 remain credible rivals in several experience measures and in tourist-data pricing.

The hotel does not buy an average month

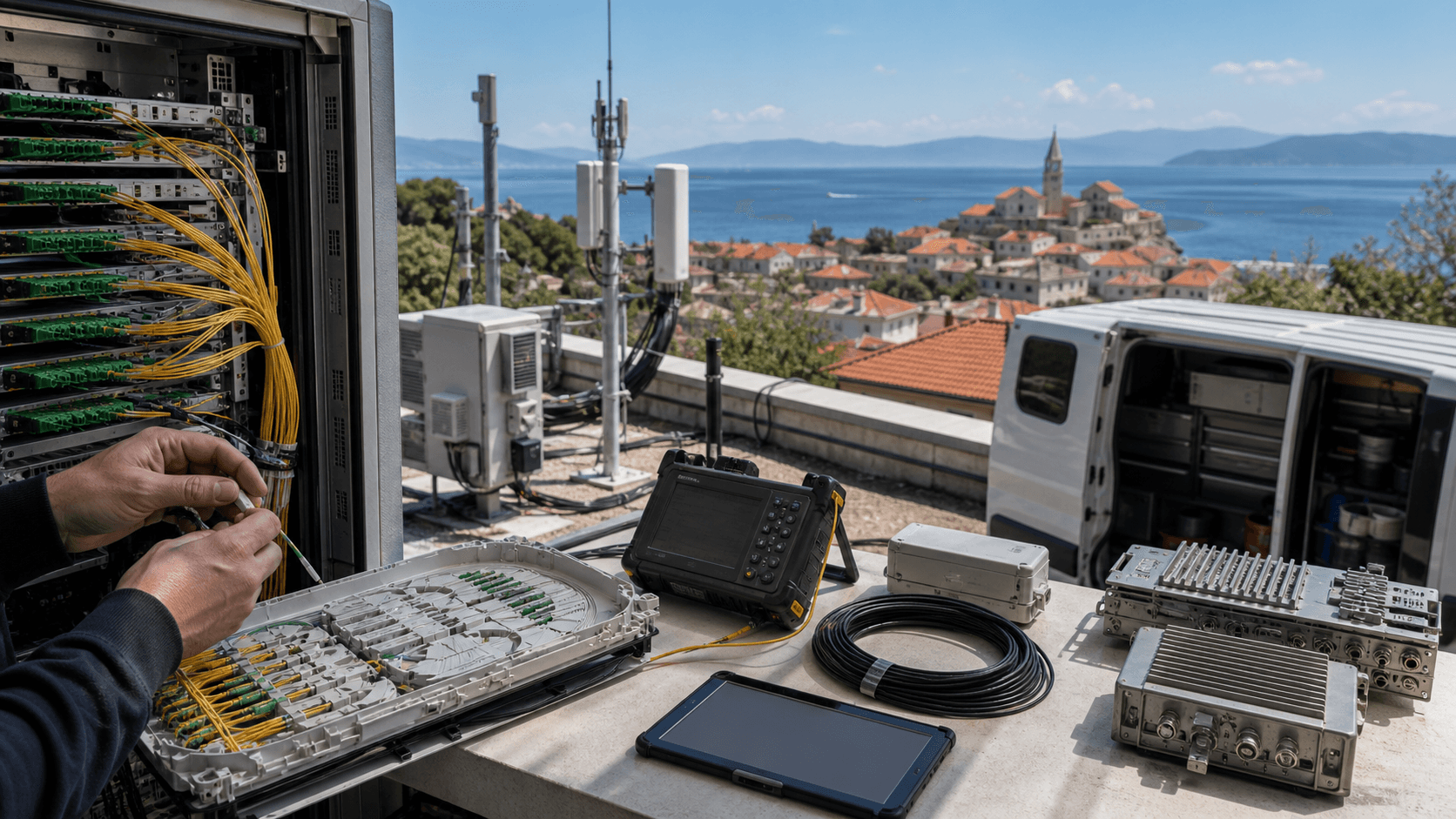

A small hotel group on the Dalmatian coast does not experience broadband as a twelve-month average. It experiences it as a Friday in July when the property-management system, card terminals, guest Wi-Fi, door locks, camera backhaul, staff phones, booking channels and airport-transfer messages all have to work at the same time. The hotel's bill may look like a bundle of fibre, television, mobile subscriptions and backup data. The network cost behind that bill is not a bundle. It is a capacity promise made to a place whose population changes with the season.

That is the right starting unit for Hrvatski Telekom d.d. The company is easy to describe as Croatia's national telecom incumbent and a Deutsche Telekom subsidiary, but the buyer's problem is more concrete than ownership. A coastal buyer wants a connection that will hold up when guests arrive with foreign SIMs, local eSIMs, streaming habits, WhatsApp calls, navigation apps and expectations formed in larger European markets.

A coastal household or holiday-rental owner wants the same thing at a smaller scale: a router that can serve family, guests, cameras, smart meters and remote work without turning August into a troubleshooting season. A small exporter in Split, Rijeka or Zadar wants the booking and logistics stack to behave like a city network even when traffic is peaking at the coast.

Croatia's tourism statistics make the load problem visible. The Croatian Bureau of Statistics reported 20.7 million tourist arrivals and 94.8 million tourist nights in commercial accommodation in 2025, with foreign tourists accounting for 90.3% of nights and the Adriatic Region accounting for 89.4 million nights, or 94.3% of the national total (DZS 2025 tourism release). Istria alone recorded 28.3 million nights, Split-Dalmatia 18.4 million, and Primorje-Gorski Kotar 15.5 million. The buyer's network is therefore not being built only for Croatia's resident population of under four million. It is being built for a resident base plus a foreign visitor layer that is overwhelmingly coastal and concentrated in places where islands, old towns, ferries, hills, marinas and short-stay accommodation change the cost of coverage.

HAKOM's Q3 2025 market data show the same seasonality from the network side. The regulator noted that the quarter covered the peak tourist season, July to September, and reported 438.3 million minutes of international roaming traffic by foreign subscribers in Q3 2025, up 108.1% from Q2, while data roaming revenues reached EUR 33.9 million, up 174.6% from Q2 (HAKOM Q3 2025 quarterly market data). In Q4, foreign-subscriber roaming minutes fell to 84.0 million and data-roaming revenues to EUR 6.1 million (HAKOM Q4 2025 quarterly market data). That gap is not a footnote. It is the rhythm of a tourist network: a coastal capacity surge that produces revenue, congestion risk, customer-service pressure and maintenance urgency in one part of the year, while the towers, fibre routes, core equipment, leases, software licences and security work remain fixed-cost obligations after the season has gone.

The retail market has already converted that load into simple tourist offers. Hrvatski Telekom sells visitors immediate eSIM activation and unlimited gigabytes under its "visiting Croatia" offer (HT tourist connectivity page). A1 markets 10-day, 30-day and 120 GB tourist eSIM/SIM options, including 10 days of unlimited 5G internet at EUR 14.90 and 30 days at EUR 29.00 on the version reviewed for this article (A1 tourist offer). Telemach markets a tourist package around unlimited internet for less than EUR 1.50 per day, with a 10-day unlimited GB package at EUR 14.90 (Telemach tourist package). These pages are not proof of network quality. They are proof that Croatia's operators price visitors as a recognizable demand segment, and that the summer user is not a marginal user. The summer user is a capacity event.

For HT, the economic question is whether that capacity event pays for the network discipline needed in the rest of the year. The hotel pays for continuity, not for an average speed test. It cares whether the fibre installation is actually available at its address, whether mobile backup works when a local cabinet has a fault, whether the support queue can handle changeover day, and whether the operator's regulated access obligations slow or sharpen its investment incentives. Those are not cosmetic details. They are the difference between a retail brand and a national infrastructure business.

The incumbent sells bundles, but the asset is controlled reach

Only after the buyer decision is priced does the corporate history matter. Hrvatski Telekom is the national full-service operator in Croatia, listed on the Zagreb Stock Exchange and integrated into Deutsche Telekom's European footprint. Deutsche Telekom's current Croatia profile describes HT as the leading Croatian telecom company, with the best mobile network and the largest FTTH network, while also pointing to business ICT, cloud, cybersecurity, data centres, IoT and smart-city services (Deutsche Telekom country profile). That profile is promotional, so it should not be treated as independent proof. Its value is in showing how the parent group wants the Croatian company understood: not only as a mobile carrier or fixed-line incumbent, but as a converged network and digital-infrastructure provider.

The public numbers fit that positioning. HT's February 2026 unaudited report for 2025 said revenue rose 3.6%, adjusted EBITDA AL rose 3.3%, net profit after non-controlling interests reached EUR 143 million, market-leading investments rose 10.5% to EUR 268 million, FTTH coverage reached 1 million households, and EUR 160 million was returned to shareholders through dividends and share buybacks (HT FY 2025 investor news). Its Q4 2025 presentation gives more operating texture: revenue was EUR 1.142 billion, adjusted EBITDA AL EUR 430 million, and capex after leases EUR 268 million, with management attributing capex growth to accelerated fibre expansion, mobile investment and data-centre modernization (HT FY 2025 presentation).

The start of 2026 kept the story intact. HT's Q1 2026 release reported revenue up 1.6%, adjusted EBITDA AL up 2.5%, net profit of EUR 29.9 million, capex after leases of EUR 62.6 million and a proposed EUR 1.69 dividend (HT Q1 2026 investor news). The accompanying analyst presentation said HT continued expanding the largest FTTH network in Croatia by 16% year over year, mobile service revenue rose 4.6%, system solutions revenue rose 8.6%, postpaid mobile customers increased 3.9%, and retail fibre customers increased 30% year over year (HT Q1 2026 presentation).

Those figures make HT look like a quality incumbent, but not a costless one. Adjusted EBITDA AL margin in Q1 2026 was 36.2%. That is attractive, but it was earned in a business still spending heavily on capex, still migrating copper users to fibre, still carrying local support work, still maintaining mobile reach and still returning cash to shareholders. The coastal hotel sees one monthly charge. HT sees a portfolio of commitments: spectrum rights, tower leases, passive infrastructure, fibre drops, technicians, service centres, software, cybersecurity, wholesale products and the parent group's operating standards.

The most important phrase in HT's Q1 presentation is not the word "growth." It is "indexation clause implemented from March." Croatia's operators have increasingly used inflation indexation to pass part of the cost shock to subscribers. Industry reports noted that HT and A1 raised monthly tariff prices by 3.7% from March 2026, aligned with Croatia's 2025 average inflation rate, with the change applying to monthly fixed and mobile fees rather than every usage charge (Telecompaper price-indexation report). In 2024, the Economic Institute Zagreb also recorded inflation-linked price increases across the three main operators, including HT's 6.5% increase from July 2024 (EIZ telecommunications sector analysis 2024).

That matters because an incumbent margin can be strong for different reasons. It can be strong because a network is better, because a customer base is sticky, because tourist demand expands the market, because prices have been indexed, because handset activity changes mix, because wholesale regulation shifts, because cost transformation works, or because group reporting smooths the local economics. HT's filings point to service revenue momentum and cost discipline, but they do not cleanly separate genuine network-led pricing power from inflation pass-through and seasonal demand. That is the evidence hinge running through the company.

Fibre migration is a cost before it is a victory lap

The fixed-network story looks simple at headline level: fibre is growing, copper is declining, and HT has the largest FTTH footprint. The HAKOM Q1 2026 market release says total electronic-communications service revenue in Croatia reached EUR 453 million, up 2.76% year over year, and that fibre optic connections reached 497,605, overtaking copper connections, which stood at 466,111, for the first time (HAKOM Q1 2026 market release). For the reader, that can sound like an inevitable technology migration. For an operator, it is a capital-allocation fight.

Fibre creates a better product, but it also moves the operator through awkward overlaps. Copper has to be maintained while fibre is deployed. Customers must be migrated. Installation capacity becomes a limiting factor. Multi-dwelling buildings, rights of way, ducts, poles and street works all create local friction. In coastal towns, old streets and seasonal access constraints make that friction more visible. On islands and in rural areas, the number of premises per kilometre of network is often less forgiving than in dense urban neighbourhoods.

HT's own price-list language makes the migration visible at retail level. Its internet package price document says copper and hybrid internet packages are not available for new and existing residential customers in all areas where HT provides service on its optical access network, and it describes migration of existing copper and hybrid users to fibre under specific conditions (HT internet-package price list). This is not merely a faster-tariff story. It is a customer-base conversion process, with installation charges, address availability, technician work and a possible mismatch between where fibre exists and where customers expect it.

HAKOM's Q4 2025 quarterly data show the migration from the market side. Fixed broadband lines reached 1.184 million. Copper access lines fell 14.8% year over year to 485,882, while fibre optic access lines rose 34.0% to 470,996. Fixed wireless access rose 17.8% and satellite access, from a much smaller base, rose 237.4%. Fixed broadband traffic was 1.220 million TB, up 22.7% year over year (HAKOM Q4 2025 quarterly market data). That is a classic incumbent transition: legacy voice and copper decline, bandwidth demand expands, and the new product requires fresh investment before every old cost disappears.

Wholesale access complicates the story. In Q4 2025, HAKOM reported wholesale broadband access revenues over copper down 11.3% year over year, but wholesale broadband access revenues over fibre up 68.3%. Physical wholesale access via copper and bitstream copper lines fell, while physical wholesale fibre and bitstream fibre lines rose sharply. In Q3 2025, HAKOM reported the same direction: copper wholesale revenues down 10.0%, fibre wholesale revenues up 75.9%, bitstream fibre lines up 114.8%, and data roaming revenues surging in the tourist quarter (HAKOM Q3 2025 quarterly market data).

That is why the wholesale topic should not be reduced to "the incumbent controls the network." The regulator is actively measuring the migration from copper access to fibre access. Alternative operators still matter because they shape retail pricing, wholesale demand and political tolerance for deregulation. HT's 2023 annual report described deregulation of its fibre networks in major Croatian cities as a milestone that allowed it to compete on equal terms in deregulated areas and improve infrastructure use (HT 2023 annual report). But trade press and challenger commentary at the time warned that deregulation could entrench the dominant fixed player in some markets (Mobile Europe on HAKOM deregulation).

Both claims can be true in different localities. Deregulation can help an incumbent monetize fibre in dense, contestable areas where cable, fibre altnets or mobile substitutes exist. It can also create concern where competitors depend on regulated inputs and where building duplicate access infrastructure is uneconomic. The buyer in Dubrovnik, Pula or Split does not care about the legal theory; the buyer cares whether there are credible alternatives, whether installation is timely, whether advertised speeds match address reality, and whether faults can be repaired before a booking period is damaged.

HAKOM's May 2025 Market Day captured the tension around copper retirement. HT's representative said there was not yet a date for copper switch-off, that the market was investing heavily in very high capacity networks, and that the process was complex, resource-intensive and lengthy. Telemach's representative warned that wholesale discontinuation would require competitors to migrate their own users and prepare resources (HAKOM Market Day). The fixed-network economics therefore have two clocks. One is the capex clock for fibre deployment. The other is the regulatory and customer clock for retiring what fibre replaces.

Spectrum turns the coastline into a long contract

Mobile economics are even more visibly tied to fixed commitments. A tourist eSIM may be bought for ten days. Spectrum is bought for years. HT's 2021 investor notice said HAKOM had assigned spectrum in the 700 MHz, 3600 MHz and 26 GHz bands for 5G mobile networks (HT 2021 5G spectrum notice). The 2023 auction then renewed and reassigned key national bands. HAKOM's official 2023 announcement shows HT acquiring 2x10 MHz in 800 MHz for EUR 19.616 million, 2x15 MHz in 900 MHz for EUR 28.840 million, 2x30 MHz in 1800 MHz for EUR 33.020 million, 2x25 MHz in 2100 MHz for EUR 50.240 million and 2x25 MHz in 2600 MHz for EUR 3.598 million. The licences run for 15 years with a possible five-year renewal, and national-band coverage obligations require 99.4% population coverage by 31 December 2029 with outdoor speeds of at least 10/2 Mbit/s in most cases (HAKOM 2023 spectrum award).

That is the hidden lease behind every coastal unlimited-data plan. Low-band spectrum helps reach and indoor coverage; mid-band spectrum helps capacity; mmWave or high-capacity bands matter for dense or specialized deployments. But spectrum alone is not coverage. It needs radio equipment, backhaul, power, site access, optimization, monitoring, service crews and enough margin to justify upgrades before congestion becomes a public complaint. In a country with island settlements, mountainous coastal backdrops and visitor peaks, the spectrum portfolio has to cover both national availability and sudden local density.

Independent network measurements support HT's mobile-quality claim, but also show that competition is not one-dimensional. Opensignal's October 2025 Croatia report named Telemach Croatia's "Best Network" overall, while also saying HT had Croatia's fastest average download speed at 89.0 Mbps, led 5G gaming, shared top honours with Telemach for video experience, and led for overall coverage experience. Telemach led 5G coverage experience, and A1 remained competitive in several categories (Opensignal Croatia mobile experience, October 2025). This is exactly the kind of result one would expect in a three-operator market where an incumbent can be fast and broad, a challenger can win on reliability or coverage measures, and A1 can still discipline pricing and bundles.

The nPerf mobile and fixed reports add another independent view. nPerf's 2025 Croatia mobile award page ranked operators on measured performance, with HT ahead on several mobile indicators in the summary visible to users (nPerf Croatia mobile awards 2025). Its 2025 fixed-broadband report said subscribers of A1, Hrvatski Telekom and Telemach enjoyed the best FTTH internet in Croatia, with different operators leading specific measures such as latency, upload and streaming (nPerf fixed Croatia 2025 report). These sources should not be used as exact financial predictors. They do show that HT's network proposition has third-party support, while the buyer still has alternative operators and substitute technologies to consider.

The summer economics sharpen the mobile question. If peak tourist traffic fills cells in coastal towns, the operator has to decide whether to dimension for peak quality, accept some congestion, price premium plans, offload traffic to Wi-Fi and fibre, or rely on roaming revenue to offset the peak. HT's own mobile tariff page says mobile internet speed depends on signal level, device type and current network load (HT mobile tariffs page). That statement is ordinary, but in Croatia it is analytically important. A device in August is not using the same network conditions as a device in February.

For a hotel, the practical answer is redundancy. Fibre is the main line; 5G fixed wireless or mobile routers can be backup; guest Wi-Fi offloads mobile use indoors; staff phones depend on outdoor mobile coverage; payment terminals may need mobile fallback. HT can benefit from that redundancy because it sells converged accounts, business ICT and mobile services. But the buyer can also split supply: one operator for fibre, another for tourist SIMs, another for backup, Starlink or satellite in hard-to-serve settings.

HAKOM's Q4 2025 data show satellite access still tiny, but growing rapidly from a low base, and fixed wireless access also expanding. That does not threaten HT's whole business. It does set a ceiling on how casually an incumbent can raise prices in areas where alternatives are good enough.

Islands make backhaul an economic variable, not scenery

Croatia's operating geography is not marketing scenery. It changes network cost. Islands and coastal settlements are attractive because they produce tourism revenue, but they also create awkward load shapes: long winter quiet, sudden summer peaks, ferry-dependent repair logistics, exposed sites, visual and permitting constraints, and backhaul paths that cannot always follow the cheapest terrestrial route.

The European Commission's broadband case study on Croatian islands makes the point without needing to involve HT directly. It says high-speed broadband on islands can be challenging and expensive if submarine cables are necessary, and describes a Rab-Cres project that used optical and microwave radio links to create mainland-to-island multi-gigabit connectivity. The islands were mostly rural "white NGA" areas with limited high-speed coverage, and the project used fibre to Krk plus microwave links to Rab and Cres for high-capacity backhaul (European Commission island connectivity case). The operator in that case was A1, not HT, but the lesson applies to the whole Croatian access market: island backhaul is a design decision with cost, resilience and capacity consequences.

The public broadband policy frame points in the same direction. The European Commission's Croatia connectivity page says the national broadband plan aims for at least 100 Mbps to all households, symmetric 1 Gbps connections to public buildings such as schools and health facilities, and 5G in all main cities and towns and along major highways (European Commission digital connectivity in Croatia). That is a national-development objective. For HT, it is a market and regulatory environment in which coverage gaps are not only missed sales; they are political and public-service concerns.

HT's own rural and regional projects show how state support, open access and local development objectives enter the company economics. In April 2025, Split-Dalmatia County and HT started a fibre project for Zmijavci, Lokvicici, Podbablje, Prolozac, Runovici and Imotski, due by 30 June 2026, to bring ultra-fast broadband to nearly 7,500 households. The reported project value was EUR 5.5 million, with HT investing EUR 1.2 million and EUR 4.3 million co-financed through National Recovery and Resilience Plan grants. The network is described as open access, available to other operators on equal terms (SAMENA report on Split-Dalmatia fibre project). The local political quote explicitly links the project to equal living conditions "on the coast, the islands, or in the hinterland."

That is not a pure private-return project. It is infrastructure co-investment in areas where commercial investment alone may be limited public evidence. HT can win work, deepen its footprint and reinforce its national role. It also accepts open-access obligations and execution risk. A hotel in Split-Dalmatia may care only whether the connection is delivered, but the operator's return depends on grant terms, take-up, wholesale use, build cost, maintenance cost and the extent to which high-season tourism users can be converted into year-round revenue.

The coastal geography also changes mobile operations. A mast that serves a sparse island in February may be critical in August. Backhaul that is adequate for residents may be strained by visiting devices, upload-heavy social media, video calls and streaming. Outdoor coverage that looks good on a map may behave differently inside stone buildings, marinas, campsites or crowded old-town streets. When HT markets tourist eSIMs and unlimited gigabytes, it is monetizing this demand. When customers complain about speed, throttling, setup confusion or support response, they are often complaining about the same capacity and labour surface.

This is why the article's opening buyer is a hotel rather than an abstract subscriber. A telecom operator can publish homes-passed, ARPU, capex and margin. The hotel tests whether those numbers have been translated into operational reliability under seasonal stress. A coastal household tests whether fibre migration and mobile backup are real at the address. A small exporter tests whether dedicated capacity, business mobile and cloud/security services are sold as an integrated service or as separate products with separate failure points.

Group scale helps, but it can blur the local margin

HT's Deutsche Telekom connection is economically valuable. It can bring procurement leverage, group technology standards, brand credibility, roaming relationships, product templates, security practices and financing discipline. Deutsche Telekom's 2025 annual report says its Europe segment continued investing in broadband, fibre and 5G, with service revenues from business customers growing 5.5% organically and Croatia contributing across product areas; the Europe segment's adjusted EBITDA AL reached EUR 4.7 billion, up 5.6% year over year, with cash capex before spectrum rising 8.3% because of optical fibre, mobile communications and fixed-network capacity investment (Deutsche Telekom Europe 2025 segment report).

That group context matters for a small national market. A standalone Croatian operator would still need spectrum, software, cybersecurity, procurement, roaming, vendors and IT platforms. HT can draw on a larger parent, while still being measured by local shareholders. Its Q1 2026 presentation shows both the local and group logic: HT Croatia contributes most of the group's Croatian revenue and EBITDA, while Crnogorski Telekom adds a smaller regional component; HT is monitoring M&A opportunities; and it signed an agreement to acquire PRO-PING, a regional broadband provider.

The direction is clear: scale matters in a market where fibre, content, mobile and ICT costs favour integrated operators.

The danger is that group scale can blur the local evidence. If cost transformation is driven by shared technology, vendor terms or parent-group operating practices, the public Croatian accounts may not isolate how much margin comes from local network advantage. If cloud, cybersecurity and system solutions grow, the revenue line becomes less purely telecom access. If capex is partly data-centre modernization and partly fibre/mobile access, the public numbers do not fully show how much investment is going into coastal load, island backhaul, enterprise ICT, radio modernization or legacy replacement.

That distinction matters because investors and policy readers can misread a converged operator. A rising EBITDA margin does not automatically mean the access network is underpriced. It can mean that the operator has raised prices through indexation, shifted customers to higher-value tariffs, benefited from tourism-season roaming, improved cost discipline, grown ICT services, sold more devices, or reduced legacy costs. Conversely, heavy capex does not automatically mean the operator is overinvesting. It can mean that fibre and mobile capacity are prerequisites for maintaining the service quality that makes the margin possible.

The Rijeka Gateway 5G project shows the business-customer side of this shift. In 2024, HT equipped the Rijeka container terminal with a 5G network, with plans to migrate from 5G non-standalone to 5G standalone and enable network slicing for industrial applications, according to Data Center Dynamics reporting (DCD on HT's Rijeka 5G network). That is not a tourist SIM business. It is enterprise-grade communications tied to port automation, latency, availability and industrial processes. If HT can sell more of that work, its economics become less dependent on residential access and more exposed to managed infrastructure and security commitments.

Security is not optional in that model. HAKOM says that under Croatia's Cybersecurity Act, which transposes NIS2, it is the competent authority for cybersecurity requirements for providers of public electronic communications networks and publicly available electronic communications services. Its role includes categorising entities, maintaining lists of key and important entities, supervising implementation of cybersecurity requirements, coordinating on significant incidents and working with the competent CSIRT (HAKOM cybersecurity role). Deutsche Telekom's Croatia transparency report also reminds readers that telecom operators in Croatia have legal obligations around lawful interception and data provisioning, even where the company says it does not have access to certain interception data because direct access is provided to the authority (Deutsche Telekom Croatia transparency report).

For the hotel buyer, none of that appears on the monthly bill. For HT, it is part of the cost of being a national operator. The same network that sells eSIMs to visitors and fibre to households must also satisfy public-network security requirements, incident reporting expectations, lawful-access architecture, data-provisioning processes and enterprise security promises. That adds labour, systems, governance and audit work. It also supports the argument for a premium national operator, especially when buyers include banks, ports, public-sector bodies, utilities, exporters and tourism groups that cannot treat connectivity as a commodity.

Public routing evidence confirms scale but not quality by itself

Network-resource evidence should be used carefully. Autonomous systems, prefixes, route objects and peering records are not companies; they are evidence about network operation. For HT, public routing records do show a significant internet footprint. RIPEstat identifies AS5391 as held by "T-HT Hrvatski Telekom d.d." and active (RIPEstat AS5391 overview). RIPEstat routing-status data on 5 July 2026 showed AS5391 announcing 47 visible IPv4 prefixes and 2 IPv6 prefixes, with 1,126,656 IPv4 addresses in announced space and 60 observed neighbours (RIPEstat AS5391 routing status). PeeringDB lists Croatian Telecom / Hrvatski Telekom as AS5391, a cable/DSL/ISP network with regional scope and heavy inbound traffic, though the PeeringDB record also shows restrictive policy and limited public exchange/facility fields, so it should not be overread (PeeringDB AS5391 API record).

These records do not tell us whether a hotel Wi-Fi network in Hvar will work on a Saturday evening. They do tell us that HT is not merely a reseller of retail service. It operates routed infrastructure with visible announced resources, observed neighbours and a regional internet presence. That matters because national telecom resilience depends on more than radio sites and fibre drops. It also depends on upstream diversity, routing policy, IP address management, DDoS exposure, DNS/service platforms, peering and the operational skill to keep the national traffic layer stable during load changes.

The routing evidence also supports a cautious view of "network-resource evidence" in the broader article. AS5391 should not become a separate subject. Prefixes should not become customers. PeeringDB fields should not be treated as a substitute for financial data. They are a cross-check: HT's public network footprint is consistent with the national-operator role described in filings, regulator data and product pages. The evidence becomes useful when it is combined with HAKOM's market data, independent speed and coverage tests, public product pages, and the buyer-level use case.

The most interesting gap is not whether HT operates a national network. It plainly does. The gap is whether public data tell us enough about where the network earns its margin. HAKOM publishes market-wide traffic, revenues, broadband lines and wholesale trends. HT publishes group and segment numbers. Independent tests publish user-experience rankings. Routing data show network presence. None of these sources cleanly allocate profit between Zagreb fibre, coastal mobile peaks, island backhaul, enterprise ICT, roaming, regulated wholesale access, device sales and parent-group cost sharing.

That limitation should shape the conclusion. HT is strategically important because it sits at the intersection of national coverage, tourist connectivity, fibre migration, mobile spectrum, wholesale access and security obligations. It is not possible, from public evidence alone, to say that every point of margin is caused by superior network economics. Some margin may be explained by inflation-linked pricing and mix. Some may be explained by scale and disciplined costs. Some may be explained by the summer economy. The research case is strongest when it treats those as interacting forces rather than choosing one story too early.

Customer noise is a labour signal, not a verdict

Unofficial market chatter is useful only when it is handled as weak signal. Review sites and forums are biased toward complaints, small samples, unusual cases and people motivated to post. They are not statistically representative of service quality. But they can still reveal what users notice when a national network's promise meets installation queues, router settings, address availability, support scripts and seasonal pressure.

Trustpilot pages for Hrvatski Telekom show a small, overwhelmingly negative sample, with complaints about support, billing, setup and connection quality (Trustpilot HT reviews). The sample is too small and self-selected to prove broad dissatisfaction. Its value is directional: when things go wrong, users often talk less about headline speed and more about resolution time, contract friction and whether the operator's front line can explain the service. A national operator can have strong coverage tests and still lose trust at the support edge.

Croatian forums show a more granular version of the same signal. Bug.hr's Hrvatski Telekom board lists active threads on HT Optika, MAXtv, waiting more than 30 days for a technician, contract renewals and app/service issues (Bug.hr HT forum board). Reddit travel discussions around HT's "visiting Croatia" offer focus on practical eSIM questions, hotspot use, value versus Airalo and whether tourist data offers behave as expected in August (Reddit askcroatia tourist eSIM discussion). These are not facts about the whole customer base. They are evidence that buyer diligence in Croatia often turns on installation, hotspot rules, throttling perceptions, support response and whether a tourist offer works under real load.

Government and regulator guidance reinforces that service quality and complaints are part of the regulated surface. Croatia's public services portal says operators have two-stage complaint and grievance procedures, and that after those stages users can contact HAKOM; complaints can relate to bills, service quality, subscription-contract violations or open-internet rights (gov.hr electronic communications services). That makes support labour part of the infrastructure cost. A field repair in a coastal town, a fibre installation delay, a billing grievance or a tourist eSIM activation issue is not just a retail annoyance. It is the visible edge of a regulated national communications service.

For HT, this cuts both ways. Strong network tests and a large FTTH footprint support premium positioning. Customer noise highlights the cost of delivering that premium through local crews, shops, call centres, apps, contractors and installation processes. The company's 2023 annual report said it brought the technological unit for construction and maintenance of its network back from Ericsson Nikola Tesla to HT from January 2024, after integrating Iskon into HT and accelerating operating-model transformation (HT 2023 annual report). That detail is important: if construction and maintenance capability is more internal, HT may gain control and accountability, but it also carries more direct labour and execution responsibility.

The tourism frame makes labour more valuable. A network issue in a winter suburb is a service problem. A network issue at a coastal hotel in August can affect card payments, bookings, guest reviews and staff coordination. The same technician hours, spare parts and support escalation have a higher economic consequence when visitor density is high. This is why tourist-season economics should not be reduced to roaming revenue. It is also a stress test of local support labour.

The judgement turns on what public data cannot separate

The investment and policy case for HT is strong enough to be taken seriously. The company has national reach, the largest FTTH claim in Croatia, visible mobile-speed and coverage strength, rising fibre take-up, continuing postpaid migration, 5G and enterprise projects, material capex, and a parent group with scale. The Croatian market is not static: HAKOM data show fibre overtaking copper, mobile data and 5G subscriptions growing, fixed voice declining, wholesale fibre replacing wholesale copper, and tourist-season roaming creating dramatic quarterly swings. The buyer-level story is real.

The weakest evidence hinge remains separation. Public reports do not cleanly separate durable network-led margin from tourism-season demand, inflation-linked price increases, handset and device effects, enterprise/system-solution growth, wholesale migration and group-level accounting presentation. HT can say adjusted EBITDA AL rose because of top-line strength, cost discipline and transformation. That is plausible.

But a public reader cannot see how much of the incremental margin came from better mobile network monetization on the coast, how much from March price indexation, how much from postpaid mix, how much from reduced legacy costs, and how much from product mix beyond access.

The same applies to capex. HT's capex increase is real, but public disclosure does not fully allocate it by coastal mobile capacity, island backhaul, FTTH drops, core modernization, data centres, enterprise 5G, security systems or customer-experience platforms. HAKOM's market-wide data show VHCN investment and traffic growth, but not HT-specific local cost by region. Independent tests measure experience, not return on capital. Routing records confirm network operation, not profitability.

What facts would change the judgement? First, region-level data showing coastal and island mobile capacity, utilisation, fault rates and summer congestion before and after investment would clarify whether HT's premium network claims translate into measurable tourist-season resilience. Second, a clearer split of service revenue and EBITDA between access, roaming, ICT/system solutions, device activity and wholesale would show whether the margin is network-led or mix-led. Third, fibre take-up by geography and address type would reveal whether the 1 million homes-passed milestone is turning into profitable adoption or just coverage.

Fourth, wholesale access margins by copper and fibre would show whether regulation is constraining or supporting investment. Fifth, a transparent view of support labour, installation lead times and fault repair by region would show whether customer-service noise is an anecdotal edge case or a hidden capacity limit.

Until those facts are public, the balanced conclusion is this: Hrvatski Telekom is a national infrastructure operator whose value is tied to Croatia's unusually seasonal and coastal demand curve. It is not just a dividend telecom, not just a tourist SIM vendor, not just a fibre incumbent, and not just a Deutsche Telekom outpost.

It is the operator that has to make an August network pay for itself in April, that has to carry island and coastal backhaul where the geography is expensive, that has to sell regulated wholesale access while competing at retail, and that has to meet cybersecurity and public-network obligations while customers judge it through hotel Wi-Fi, mobile speed and technician availability.

That makes HT strategically important. It also makes the margin question more demanding than the headline numbers. The right test is not whether revenue and EBITDA rose. They did. The right test is whether HT can keep converting Croatia's seasonal, coastal and regulated network into durable cash flow without letting inflation pass-through, tourist peaks or parent-group presentation do too much of the explanatory work. For the hotel buyer, the answer will arrive first as an ordinary operational fact: whether the connection holds when the coast fills up.