Summary

- The relevant unit for Waycom is not an abstract telecom registration or a route table alone. It is a Mendoza access account: Micom advertises high-speed internet across Mendoza, a fibre plan up to 300 Mb, a wireless plan up to 10 Mb, Wi-Fi router inclusion, technical support, a customer portal, separate administration and sales WhatsApp channels, and service cards for fibre, structured cabling, wireless internet, dedicated service, IP telephony and video security (https://micom.com.ar/).

- The network evidence is strong enough for a regional ISP thesis. LACNIC RDAP identifies AS267830 as an active direct allocation to Waycom S.A. and identifies the 45.172.224.0/22 IPv4 block as allocated to Waycom with origin AS267830; bgp.tools shows AS267830 originating visible IPv4 prefixes, using Silica Networks Argentina as upstream, and participating at AR-IX Cabase; PeeringDB lists Waycom with regional scope, 5-10Gbps traffic, four IPv4 prefixes and a 10G operational port at AR-IX Cabase plus an interconnection facility in Mendoza (https://rdap.lacnic.net/rdap/autnum/267830, https://rdap.lacnic.net/rdap/ip/45.172.224.0, https://bgp.tools/as/267830 and https://www.peeringdb.com/asn/267830).

- The evidence does not prove subscriber count, financial margin, fault rate, installation speed, service quality, churn, or wholesale access revenue. It does prove a live retail access surface and a public internet footprint, which is enough to analyse Waycom as a Mendoza regional ISP whose defensibility depends on support economics and interconnection discipline.

- The strongest classification remains regional ISP. The topic set is narrowed to peering and transit rather than wholesale access because public sources show upstream and exchange dependence, not a public wholesale broadband or access-platform offer.

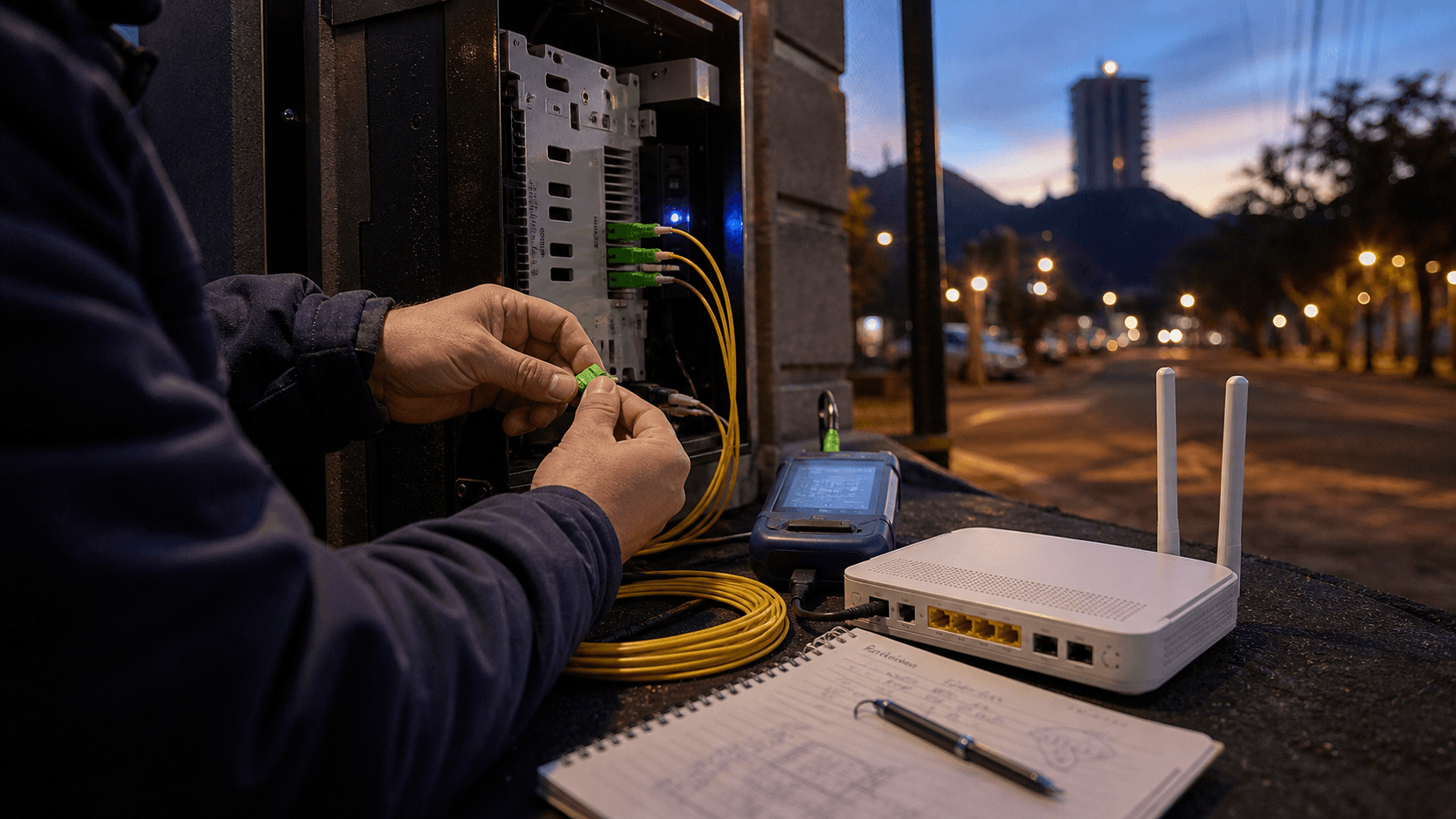

The customer judges the network after the installer leaves

A Mendoza household or small firm does not experience Waycom as an autonomous system. It experiences the company as the line that either works after the installer leaves or becomes the next local problem to solve. The public Micom site opens with a broad promise: "Conectividad sin limites" and "Internet de alta velocidad en toda Mendoza." Beneath that promise sits a small access menu. Fibre is advertised at up to 300 Mb, wireless at up to 10 Mb, both with a Wi-Fi router and technical support. The same page gives separate WhatsApp contact routes for administration, payments and billing, and for sales, coverage and plans.

It also points users to a customer portal at clientes.micom.com.ar.

That customer surface is enough to define the economic unit. The product is not just a megabit figure. It is a monthly relationship that joins installation, router, access path, support desk, billing conversation and renewal decision. A family may care about streaming and online classes. A corner shop may care about card payments, messaging, delivery apps and supplier portals. A small professional office may care about remote meetings, cloud files, voice calls and invoicing.

All of them discover the real price of the service when the connection slows, the Wi-Fi fails, a payment dispute appears, or the account has to be cancelled, moved or upgraded.

For a local ISP, the first sale can be easier than the second month. A 300 Mb fibre plan is an attractive headline, especially in a province where official ENACOM data put Mendoza's average fixed download speed at 212.27 Mbps in the first quarter of 2026. But an advertised speed does not decide the relationship. The company has to decide whether the fault is in the customer's Wi-Fi, the indoor router, an optical drop, a wireless access path, a backhaul handoff, an upstream route, a payment suspension or a capacity problem. The customer usually sees only one brand. The operator sees a chain of dependencies.

This is why Waycom's public service mix is more revealing than a corporate description. Micom's service cards include fibre, structured cabling, wireless internet, dedicated service, IP telephony and video security. The cards are brief, but they show the shape of a local infrastructure business rather than a web-only reseller. The "dedicated service" wording is aimed at business customers with symmetric upload and download needs. IP telephony points to voice as an add-on around the broadband line. Structured cabling and video security point to visits, wiring, premises work and support labour.

Those services turn the company into a local technician and account manager, not only a bandwidth vendor.

The opening case, then, is a household or small firm after installation. The cable is in, the router is powered, the WhatsApp number has been saved, and the first bill has either been paid or is coming due. The customer now compares Micom with larger Argentine fixed providers, mobile broadband, a wireless neighbour provider, satellite backup and perhaps a direct business fibre offer. That comparison is not only about price. It is about who answers, who can come to the premises, who knows whether the building is in coverage, who can explain a fault, and whether the account still feels local enough to be worth keeping.

The access mix makes the fault call the priced unit

The public plan menu contains an important asymmetry. Micom advertises fibre up to 300 Mb and wireless up to 10 Mb. Fibre and wireless are not just two speed tiers. They are two different operating designs. Fibre promises higher capacity and lower latency. Wireless can reach places where fibre is not present, not economical, or slow to install. Both require customer premises equipment and both create support tickets, but the causes of failure are different.

With fibre, the local economics are tied to physical access. A fibre drop may be robust once installed, but the expensive part is planning, install labour, customer education, optical equipment, splicing or connector quality, power continuity and keeping a clean record of where the line runs. In a dense part of Mendoza, the operator can build density and amortise support trips. In a scattered coverage pattern, each installation and fault visit becomes more expensive. The customer does not care whether the problem is a dirty connector, an underpowered router, a neighbour's cable cut or an upstream issue. The customer pays Micom.

With wireless, the economics are even more visibly local. Wireless access can be valuable where geography, building access, street works or fixed-line availability make wired access awkward. But it also introduces line-of-sight, antenna placement, weather, interference, power and rooftop-access questions. A 10 Mb wireless plan can be economically rational if it reaches a customer who has no better option and if it can be supported without repeated visits. It becomes fragile if every weather event, router issue or signal complaint requires field labour that the monthly fee cannot cover.

The difference matters because the public site does not show prices, installation fees, repair-time commitments or minimum terms. Without those figures, the best way to read the business is through cost drivers. Support is listed as part of the plan promise. Administration and sales have public WhatsApp routes. A customer portal exists. Business-facing services are advertised. The cost base therefore includes not only upstream capacity and equipment, but also the time spent answering questions, checking coverage, taking payments, visiting premises, replacing routers, explaining outages and keeping customers from switching.

In this business, the fault call is the priced unit. A support interaction that diagnoses a Wi-Fi password problem in three minutes is cheap. A support interaction that becomes two WhatsApp threads, an unpaid bill dispute, a field visit, a replacement router and an upstream escalation can consume several months of margin. The smaller the operator, the more this matters. Large national providers can dilute call-centre friction across millions of accounts. A Mendoza operator has less room: every avoidable repeat visit and every unresolved local complaint is both cost and reputation risk.

The same logic applies to bundles. IP telephony can deepen the account because the customer uses the line for voice, not only data. Video security and structured cabling can make the relationship stickier because the provider knows the premises. Dedicated service can raise average revenue if business customers pay for more reliable or symmetric connectivity. But every extra product also creates another fault boundary. If voice fails but data works, if a camera does not reach the recorder, if a business link is slow in the evening, the customer expects one local provider to coordinate the answer. Stickiness and support burden move together.

That is why the article's title uses "fault economics." The point is not that Waycom's service is faulty. The point is that local ISP economics are revealed by faults. The sale advertises speed. The renewal prices response. A provider that can close faults cheaply and credibly can defend a local premium. A provider that sells access without matching field and support capacity ends up paying for the gap after the first invoice.

Public network records support a real operator, not a brochure

The routing record is unusually helpful because it connects the public brand to a verifiable internet footprint. LACNIC RDAP identifies AS267830 as an active direct allocation tied to Waycom S.A., with registration dated April 10, 2019, and with Ramiro Anchelerguez listed as the legal representative and administrative, technical and abuse contact. The RDAP entity record gives Waycom S.A. as the registrant. The 45.172.224.0/22 IPv4 block is also active, allocated to Waycom S.A., and lists AS267830 as the origin autonomous system. Its technical contact uses a Micom domain address, which helps bridge the legal and brand evidence.

That is not proof of service quality, but it is important. Many weak telecom profiles rest on a stale registry handle, an old phone number or an unannounced address block. Waycom's public evidence is stronger. bgp.tools shows AS267830 as active under LACNIC, identifies the website as micom.com.ar, labels the network type as Eyeball, and shows visible IPv4 origination including 45.172.224.0/22 and more specific /24 announcements. It also shows Silica Networks Argentina as an upstream and lists AR-IX Cabase participation.

PeeringDB adds a second, operator-maintained view. It lists Waycom under Waycom S.A., associates the network with AS267830, gives the Micom website, lists the IRR as-set AS267830:AS-WAYCOM, shows four IPv4 prefixes and no IPv6 prefixes, reports regional scope and 5-10Gbps traffic, marks the RIR status as ok, and shows a 10G operational public peering connection at AR-IX Cabase. It also places an interconnection facility entry at Cabase MZA in Mendoza. The PeeringDB record was last updated in March 2023, with RIR status updated in June 2024.

The combined evidence supports a clear but bounded claim. Waycom is not only a brand landing page. It has an autonomous-system identity, a routed IPv4 block, a visible upstream, an exchange presence and a Mendoza interconnection footprint. That is sufficient to classify the company as a regional ISP. It is not sufficient to claim high service quality, uptime, subscriber scale or financial performance. Route visibility tells the reader that the operator exists in the public internet. It does not tell the reader whether a technician arrives on time.

The absence of IPv6 in the public records is also a useful caution. PeeringDB lists zero IPv6 prefixes, and bgp.tools shows no IPv6 origination in the observed profile. For many residential customers in Argentina, IPv6 absence may not be noticed day to day. For a network operator, it still says something about modernisation and future support load. IPv4-only access can work, but it may require more NAT, more address management, more abuse handling and more operational work as applications and devices continue to evolve. That is not a fatal weakness for a local ISP, but it is one of the watchpoints a business customer should ask about.

The upstream picture is similarly useful. A single named upstream in bgp.tools is not a scandal; small regional networks often begin with a simple upstream structure and supplement it through a domestic exchange. But the public record means upstream dependence must be part of the analysis. If Silica Networks or a shared regional transport path has a problem, the end customer still calls Micom. If AR-IX paths help keep domestic traffic local, performance may improve for popular content and Argentine networks. If exchange or upstream capacity is underbuilt, evening usage can expose the weakness. The user does not buy an AS path.

The user buys a working access month.

AR-IX and Mendoza interconnection change the cost of being local

PeeringDB's AR-IX Cabase entry is not decorative. A 10G operational connection at an Argentine exchange gives a regional ISP a way to control part of the traffic path instead of buying everything as generic transit. For customers, the value may show up as better routes to domestic networks, better caching economics, lower dependence on a single upstream for some traffic, and lower cost per bit where peering is effective. For the operator, it can mean better bargaining power and a more credible network story.

The facility detail is particularly relevant because it places the interconnection at Cabase MZA in Mendoza. Locality matters in a province where the network is sold as Mendoza access. A regional operator that can interconnect near its operating territory has a different cost and latency profile from one that hauls every packet through Buenos Aires before deciding where it should go. The public record does not let us quantify how much of Micom's traffic stays local or domestic. It does show that Waycom has a route to participate in Argentina's exchange fabric.

This is why "Peering and transit" is the more accurate topic than "Wholesale access economics" for this report. Public evidence shows upstream dependence, exchange participation and traffic-control economics. It does not show Waycom selling wholesale broadband access, wholesale fibre access, voice platforms to retail resellers, or a regulated access platform to local competitors. The company may have private commercial arrangements not visible in public. The published evidence, however, supports interconnection economics rather than a wholesale product thesis.

For a small ISP, peering is not an automatic advantage. It has to be operated. Route filters, capacity planning, RPKI practices, abuse handling, traffic monitoring, router maintenance and escalation routines determine whether an exchange port helps customers or becomes one more failure domain. The public records show RPKI validity on visible prefixes in bgp.tools. That is a positive sign of route-origin hygiene. But RPKI validity does not prove customer performance. It proves that the visible origin authorisation picture is orderly enough to matter in a trust assessment.

Transit dependence is also not a defect. All retail ISPs depend on other networks. The commercial question is whether the dependence is understood, diversified where necessary and priced into the service. A household with a single home link may tolerate occasional slowdowns if the price and support feel fair. A small firm using cloud accounting, remote meetings and card payments will be less tolerant. A business buying dedicated service will ask harder questions about contention, failover, fixed addressing, support hours and repair expectations.

Waycom's public service menu opens that business conversation; the route record shows the network basis on which it would have to answer.

In Mendoza, the local nature of the interconnection can also be a retention tool. A national provider may have larger backbone scale. A local provider can argue that it knows the access neighbourhood, the customer site, the support history and the regional exchange path. That argument is credible only if customers feel the difference during faults. Peering lowers some network costs and improves some paths, but it does not replace answering the phone.

The Mendoza market has moved from scarcity to higher expectations

ENACOM's current fixed-internet data put Mendoza at 397,268 fixed internet accesses in the first quarter of 2026. The technology split is telling: 283,319 were fibre, 62,753 cable modem, 26,928 wireless, 24,069 other and only 199 ADSL. The average fixed download speed in Mendoza was 212.27 Mbps in the same quarter. Compared with earlier years, the province's fixed market has plainly moved away from old copper and toward fibre and other higher-speed access.

That context cuts both ways for Waycom. On the positive side, a Mendoza operator advertising a 300 Mb fibre plan is speaking the market's current language. A customer in a province with a 212 Mbps average fixed download speed will not treat broadband as a novelty. A local ISP that can deliver 300 Mb with good support has a legitimate place in a fibre-heavy market. On the negative side, the same data raise expectations. Customers compare with other fibre options, cable modem offers, mobile data fallback and satellite service. The market is no longer one in which any fixed line is enough.

The wireless figure is also important. ENACOM counted 26,928 wireless fixed accesses in Mendoza in the first quarter of 2026. That is a minority of the province's fixed access base, but not a trivial one. It shows that fixed wireless still has a role where fibre and cable are unavailable, expensive, slow to install or poorly matched to certain locations. Micom's 10 Mb wireless plan therefore should not be dismissed as obsolete. It is better understood as a coverage and continuity product for customers whose practical alternative may be weaker than the fibre average suggests.

At the same time, a 10 Mb wireless plan has to be framed honestly. It is not a substitute for a 300 Mb fibre connection in a household with multiple video streams, cloud backups, online games, home workers and smart devices. It is a local access option where availability, installation, support and price may matter more than speed. If a customer buys it as a stopgap or for a low-demand location, it can be useful. If the provider oversells it against fibre-like expectations, support costs will rise quickly.

The market data also sharpen the small-business case. A shop or office may not need gigabit access. It may need predictable access, stable payment collection, voice continuity, a support number and a provider that can deal with indoor cabling or security cameras. In that case, Waycom's service mix can be more relevant than raw speed. Structured cabling, dedicated service, IP telephony and video security are all ways to become the local communications maintainer for a premises. But once again, the margin sits in execution. A small-business bundle is sticky when one provider solves problems.

It is brittle when every extra product creates another unresolved support path.

This is the central strategic tension. Mendoza's fixed market is modern enough that customers have higher speed expectations. It is still local enough that support and coverage can matter. Waycom can defend itself if it sells the right product to the right premise and closes faults efficiently. It becomes exposed if it competes with larger providers only on headline speed while carrying a local field-service cost base.

Local support is an asset only if it is disciplined

Micom's public contact split is straightforward: administration handles general queries, payments and billing; sales handles contracting, coverage and plans. Both are WhatsApp-facing. That is a normal Latin American local-service pattern and a useful one. WhatsApp lowers friction for a customer who wants to ask whether a street is in coverage, send a payment note, report a fault or ask about a router. It also creates a support queue that can become chaotic if the company does not manage it carefully.

Local support has a different economics from national call-centre support. A national operator may route a customer through layers of automation and remote scripts. A local ISP can win by knowing the customer, the neighbourhood and the installation history. But the same closeness can overload staff. Customers may message at all hours, mix payment and fault questions, ask for sales promises to be honoured by support, or demand a visit before remote diagnosis is complete. The more personal the channel, the more disciplined the back office has to be.

The public site's customer portal matters because it can reduce that burden. A functioning portal can move payments, account status and routine queries away from human chat. The portal page itself is a JavaScript application and does not reveal the customer operations behind it. But its existence supports the view that Micom runs a recurring account business rather than only one-off installations. A portal also changes expectations. Once customers can log in, they expect status, payment confirmation and account history to be reliable.

Billing is not separate from fault economics. A customer whose service is slow may delay payment. A customer whose payment is not recorded may experience suspension as a service fault. A customer who is switching providers may use an unresolved bill as a reason to leave. Administration and support therefore have to communicate. If the payment desk cannot see the service history, disputes become more expensive. If support cannot see billing state, troubleshooting can waste time on an account that is suspended or overdue.

For small businesses, the support asset is even more important. A cafe, clinic, office, warehouse or shop is not evaluating the provider only by a speed test. It is asking whether the provider can keep the point-of-sale terminal online, keep voice reachable, install cabling cleanly, help with cameras, answer about fixed addressing or dedicated service, and explain whether the fault is local, regional or upstream. A local provider can be valuable precisely because it can combine these conversations. It can also be stretched precisely because each conversation requires human context.

The best evidence that would strengthen Waycom's case would be public repair-time targets, business service-level terms, status pages, installation windows, support hours or customer satisfaction data. The public site does not provide those. That absence does not make the business weak, but it limits the conclusion. We can say the support surface exists. We cannot say how well it performs. Readers should treat support quality as the main unresolved variable.

The bundle is defensible because it is physical

One reason local ISPs survive around the world is that broadband is not fully digital. It is physical. Cables must enter buildings. Routers must be placed where Wi-Fi works. Fibre drops need protection. Wireless antennas need signal. Business premises need structured cabling. Cameras need mounts, power and network paths. Voice devices need configuration. These are not jobs that a distant software platform can solve alone.

Waycom's Micom service menu leans into that physicality. Fibre and wireless are access products. Structured cabling is an in-premises product. Dedicated service is a business-connectivity product. IP telephony ties voice to the data path. Video security turns connectivity into a physical-site service. A provider that can install and maintain several of those layers becomes harder to displace than a provider that only sells a cheap data plan.

The economics are attractive when the services reinforce each other. A business customer that uses the same provider for access, cabling and cameras may be less likely to switch after a small price increase. A household that trusts the technician may be less likely to churn after a national provider advertises a promotion. A wireless customer who cannot get fibre immediately may stay if support is responsive. A dedicated-service customer may pay for accountability rather than the lowest consumer price.

The economics are dangerous when the services do not reinforce each other. A camera issue can become an internet complaint. A router issue can become a cabling visit. A voice issue can become a data fault. A wireless alignment issue can become a billing dispute. Every physical product creates inventory, scheduling, warranty and training needs. If the operator is too small to support the bundle, the bundle becomes a catalogue of support liabilities.

This is where local density matters. If Waycom has enough customers in tight Mendoza coverage areas, the field team can amortise visits, learn neighbourhood fault patterns and keep equipment stocked for common problems. If the customer base is scattered or if coverage claims pull the company into awkward locations, each visit costs more. Public sources do not show the coverage map, customer count or field-team size, so the article cannot judge density. It can say density is one of the decisive facts.

The physical bundle also affects substitution. A larger Argentine ISP can offer fibre and perhaps television or mobile discounts. Mobile broadband can work during a fixed outage. Satellite can be a backup for remote premises. A direct business fibre provider can serve higher-value accounts. But none of these automatically replaces a local technician who has already wired the premises and knows the account. The local advantage exists only if the technician and support experience are good enough that the customer remembers them when a cheaper offer appears.

Currency and equipment risk sit behind every local visit

Argentina's access market is exposed to imported equipment and currency-linked inputs. Routers, optical network terminals, switches, wireless radios, antennas, fibre tools, spares, security cameras and power equipment often have prices influenced by dollar-denominated supply chains even when sold locally. A small ISP bills customers in pesos but must maintain equipment whose replacement cost can move faster than retail tolerance.

That matters for Waycom because its public offer includes equipment-heavy services. The fibre plan includes a Wi-Fi router. Wireless access usually needs customer-premises and network-side radio equipment. Structured cabling requires materials and labour. Video security needs cameras and networking gear. IP telephony needs configured devices or adapters. Dedicated service often implies higher-grade equipment and better monitoring.

Equipment risk becomes visible during faults. If a customer router fails, the provider has to decide whether to replace it free, charge for it, refurbish it, or troubleshoot longer before sending a device. If a wireless radio is misaligned or damaged, the visit may consume labour plus hardware. If a business customer needs a camera replaced, the provider has to carry inventory or lose time sourcing parts. If prices rise between installation and replacement, the old monthly fee may no longer cover the new cost.

This is not unique to Waycom. It is part of the economics of every small access operator in a currency-volatile market. But it is more important for a local provider than for a giant carrier because procurement scale is smaller and price adjustments are more sensitive. A large operator can pool equipment orders and average failure rates. A local ISP has to manage spares more carefully. Too little inventory makes repairs slow. Too much inventory ties up cash and risks obsolescence.

The customer rarely sees this. The customer sees a router, an antenna, a cable and a monthly bill. The company sees depreciation, warranty, theft, power damage, configuration time, firmware, replacement policy and recovery when service ends. The more Micom sells as a local service bundle, the more it needs disciplined equipment economics. Good installation reduces future replacement. Clear customer education reduces unnecessary visits. Accurate fault diagnosis prevents swapping a router when the real issue is upstream congestion or indoor interference.

This is another reason the 300 Mb fibre headline should not dominate analysis. The business is less about whether the site can advertise 300 Mb and more about whether the support and equipment cost of delivering a reliable access account can fit inside recurring revenue. A provider can survive with modest speeds if field costs are low and customers trust support. A provider can struggle with high speeds if faults, equipment and churn outrun the monthly account.

Larger providers and substitutes keep the renewal price honest

Waycom's local advantage has to be measured against substitute choices. Mendoza customers can compare local fibre with larger national offers, cable modem, mobile broadband, other wireless providers, satellite and direct business services. The substitution set is not identical for every address. One street may have fibre competition; another may depend on wireless; a rural or semi-rural premise may treat satellite as a backup rather than a primary service. But the customer psychology is the same: a local provider has to be good enough that switching feels risky or unnecessary.

ENACOM's Mendoza technology data show why this pressure is real. Fibre is now the dominant fixed technology in the province by access count. Cable modem remains substantial. Wireless remains material. ADSL is almost gone. That mix means many customers are not choosing between "internet" and "no internet." They are choosing among technologies with different price, installation and support promises. Waycom's fibre product sits in a competitive high-speed market. Its wireless product sits in a coverage and resilience niche. Its dedicated and cabling services sit in a small-business support market.

Mobile broadband is a partial substitute. It can keep a household messaging or a card terminal online during a fixed outage. It may be enough for a low-usage customer who does not want installation. But mobile is usually not a clean substitute for a stable home or business fixed line with router, Wi-Fi, voice and cameras. The danger for a fixed ISP is not that mobile replaces every account. It is that mobile reduces the customer's tolerance for silence. If a phone hotspot works while the fixed provider does not answer, the customer has time to shop.

Satellite is similar. It can be powerful in remote or underserved areas and as a backup path, but it does not automatically beat local fibre on indoor Wi-Fi management, business cabling, voice integration or local service. Starlink's Argentina residential page shows the satellite option exists as part of the consumer imagination, even where exact local availability and price vary by address. For Waycom, satellite is less a direct urban fibre rival than a reminder that weak coverage pockets are no longer captive forever.

Larger fixed providers exert a different pressure. They can bundle mobile, television, fixed internet and promotions. They can market nationally. They may have more backbone capacity and purchasing power. But they can also feel distant when a local fault needs a human answer. Waycom's defensible space is the gap between scale and accountability: customers who want high enough capacity, local support, physical premises services and a provider that can be reached without entering a national queue. The gap is valuable only if service actually feels accountable.

For business customers, the substitute set includes direct fibre and managed connectivity providers. A company buying dedicated service will ask whether Micom can provide symmetric bandwidth, fixed addressing, repair priority, route visibility, phone support and escalation. The public site advertises "servicio dedicado" as exclusive internet for companies with equal upload and download speeds. That is a meaningful claim, but public pages do not disclose service-level terms. A serious buyer should ask for them.

Regulation and public data set the floor, not the advantage

Argentina's ENACOM data are useful because they put Waycom inside a measurable fixed-internet market. They show access counts by technology, average speeds by province and the direction of the market. They do not tell us whether Waycom's service is good or bad. Regulation and reporting set the floor for a telecom market. Local execution creates the advantage.

The same distinction applies to LACNIC and PeeringDB. LACNIC proves number-resource allocation and responsible contacts. bgp.tools and PeeringDB show observed routing and interconnection. These are credibility inputs. They are not a customer guarantee. A clean AS record does not answer a WhatsApp message. A 10G exchange port does not schedule a technician. A valid prefix does not explain a billing dispute. The best operators connect these layers: accurate registry records, sensible routing, enough upstream capacity, clear support and disciplined field operations.

The public record suggests Waycom has several of the inputs. It has an official consumer-facing site. It has a recurring portal. It has service categories that match a local access operator. It has an active LACNIC AS and IPv4 block. It has AR-IX and Mendoza facility visibility in PeeringDB. It has a named upstream and routed prefixes in bgp.tools. It has public WhatsApp channels. Those are stronger signals than a bare company registry row.

The missing facts are just as important. Public sources do not reveal revenue, customer count, churn, installation backlog, repair time, complaint ratio, business-customer share, average revenue per account, support staffing, upstream contract terms, redundancy design, peering utilisation or network-status history. The article's judgement must stay within that boundary. The positive case is that Waycom is a real Mendoza ISP with enough public network evidence to merit regional-operator analysis. The caution is that the public evidence stops before service outcomes.

That boundary should not be treated as a weakness in itself. Private companies often do not publish operating metrics. The analytical point is to identify which facts would change the conclusion. If Waycom showed dense fibre coverage, short repair intervals, strong business retention and diversified upstream paths, the local-account thesis would strengthen. If public complaints rose around unanswered support, if network records went stale, if the AR-IX presence disappeared, or if the company overextended wireless coverage without field capacity, the thesis would weaken.

What would make Waycom more defensible

The first fact is coverage density. A map showing where Micom fibre and wireless are actually available would clarify whether the operator has a compact, efficient footprint or a scattered one. Dense coverage lowers installation and repair cost. It also improves word-of-mouth because customers in the same area can validate each other's experience.

The second is repair transparency. Public support hours, fault categories, response targets and maintenance notices would make the local-support promise more credible. Customers understand that networks fail. They are less forgiving when they cannot tell whether anyone is working on the fault. A small ISP can build trust by making the repair process legible.

The third is business service clarity. The public "servicio dedicado" card is promising, but a business buyer needs more: symmetry, contention, fixed IP options, support hours, escalation, outage credits, router ownership and backup options. Dedicated access is where a regional ISP can raise revenue and reduce churn, but only if the offer is specific enough to be trusted.

The fourth is IPv6 and route-security maturity. Public records show a useful IPv4 footprint and RPKI-valid visible routes, but no visible IPv6 origination. A public statement on IPv6 availability, routing policy and redundancy would strengthen the network story. Many customers will not ask today. Future business and institutional customers will ask more often.

The fifth is equipment policy. Because Micom's offer includes routers, wireless access and physical services, clear rules on equipment ownership, replacement, warranty and cancellation would reduce disputes. Equipment ambiguity turns support calls into billing calls. Billing calls are expensive when they happen over WhatsApp.

The sixth is customer proof. Public case studies, business references or anonymised service metrics would help distinguish Micom from a generic local provider. The strongest evidence for a local ISP is not a slogan. It is a customer who stayed because the provider solved a messy premises problem better than a national operator would have done.

These facts would not change the classification as a regional ISP. They would change confidence in the durability of the economics. The current evidence supports the existence and shape of the operator. It does not yet show the quality of execution.

The investment reading is measured, not promotional

The bull case for Waycom starts with fit. Mendoza has a large and fibre-heavy fixed-internet market, but not every customer wants or can get the same access product. A local operator with fibre, wireless, dedicated service, IP telephony, cabling and video security can occupy useful niches: premises that need installation help, businesses that want one accountable provider, customers who value WhatsApp support, and areas where wireless remains practical. The public network footprint gives that commercial surface technical credibility.

The bear case starts with scale. A small ISP has to pay for local support, customer acquisition, equipment, transit, peering, billing, field visits and premises work without the purchasing power or subscriber base of national carriers. It has to manage customer expectations in a province where average fixed speeds are now above 200 Mbps. It has to support a bundle whose physical components can create costly faults. It has visible upstream and exchange dependence, and the public record does not show redundancy in depth.

Both cases can be true at the same time. Waycom can be a real and useful Mendoza access operator while still facing hard unit economics. Locality is neither a guarantee nor a liability by itself. It is a cost structure. A provider close to the customer can answer faster, install better and build trust. It also carries the cost of being close: field labour, repeated conversations, small disputes, spare parts and reputation that moves through neighbourhoods quickly.

The most accurate conclusion is therefore practical. Waycom's public evidence supports the regional ISP classification and a strong network-resource topic. The company should be judged by the economics of the access account after installation: how often faults occur, how quickly they are closed, how many visits are avoided by good setup, how upstream and exchange paths perform at peak, how equipment is recovered or replaced, and how many customers renew because local support feels valuable. The public record gets us to that question. It does not let us answer it completely.

For a Mendoza household or small firm, the decision is similarly grounded. Choose a local provider if the coverage, support route, installation quality and account relationship are worth more than the cheapest substitute. Press for clarity if the use case is business-critical. Treat the AS, prefix and exchange evidence as proof that there is a real network behind the brand, not as proof that every service month will be good. In local access, the network record earns attention. The fault call earns renewal.

Public evidence reviewed

The official Micom site at https://micom.com.ar/ supports the brand, Mendoza positioning, fibre and wireless plans, Wi-Fi router and support claims, services menu, administration and sales contact routes, and customer portal link. The customer portal shell at https://clientes.micom.com.ar/ supports the existence of a recurring account surface, though its content requires JavaScript and does not reveal operational data.

LACNIC RDAP supports the legal and number-resource evidence: https://rdap.lacnic.net/rdap/autnum/267830 identifies AS267830 as active and allocated to Waycom S.A., while https://rdap.lacnic.net/rdap/ip/45.172.224.0 identifies 45.172.224.0/22 as allocated to Waycom S.A. and linked to origin AS267830. bgp.tools at https://bgp.tools/as/267830 supports current observed routing, upstream, prefix and AR-IX evidence. PeeringDB at https://www.peeringdb.com/asn/267830 supports the operator-maintained network profile, regional scope, traffic band, AR-IX Cabase 10G port and Cabase MZA Mendoza facility entry.

ENACOM's public data package at https://datos.gob.ar/dataset/enacom-internet-fija supports the fixed-internet market context. The technology-by-province CSV at https://indicadores.enacom.gob.ar/Files/DatosAbiertos/internet_accesos_tecnologias_provincias.csv supports Mendoza's first-quarter 2026 access mix. The average-download-speed CSV at https://indicadores.enacom.gob.ar/Files/DatosAbiertos/internet_velocidad_media_descarga_provincias.csv supports Mendoza's 212.27 Mbps first-quarter 2026 average fixed download speed. Starlink's Argentina residential page at https://starlink.com/ar/residential supports the existence of a satellite substitute surface, with the caveat that the page requires JavaScript for full detail.