Summary

- AS Telia Finland Oyj should not be priced as if an autonomous-system label were a business by itself. The public record points to AS20569 and to a resource-holder surface; the commercial analysis has to ask whether that surface is tied to Telia Finland's real operating unit: paid continuity for offices, mobile users, sites, secure networks and data-centre-connected workloads.

- The strongest official evidence is not the routing clue. Telia Finland's own business pages describe office internet that combines fixed broadband and mobile backup, DataNet private networks for domestic and international sites, higher-grade business internet, data-centre services, wholesale access, and support paths. Those services show what a customer actually buys.

- The costly part is not only spectrum or number resources. It is installation, routing discipline, customer premises equipment, backup access, monitoring, field repair, security filtering, IPv4 scarcity, fibre or mobile access selection, and escalation when the fault is partly inside Telia's network and partly inside a partner or customer environment.

- Telia Company reporting makes the test sharper. Finland is a mature business with service revenue under pressure in mobile, fixed and business solutions carrying more of the growth burden, and explicit simplification work. Public segment numbers support a real national operator, but they do not reveal the margin or renewal economics of any single AS20569-linked service.

- The evidence limit is central to the judgement. Public routing records can show that a named resource exists and can direct readers to RIPEstat or RDAP accountability, but they cannot prove customer count, service quality, SLA performance, fault history, supplier contracts, utilisation, churn, or whether a buyer renews because Telia creates value rather than because migration is painful.

The Hidden Cost Stack Is The Product

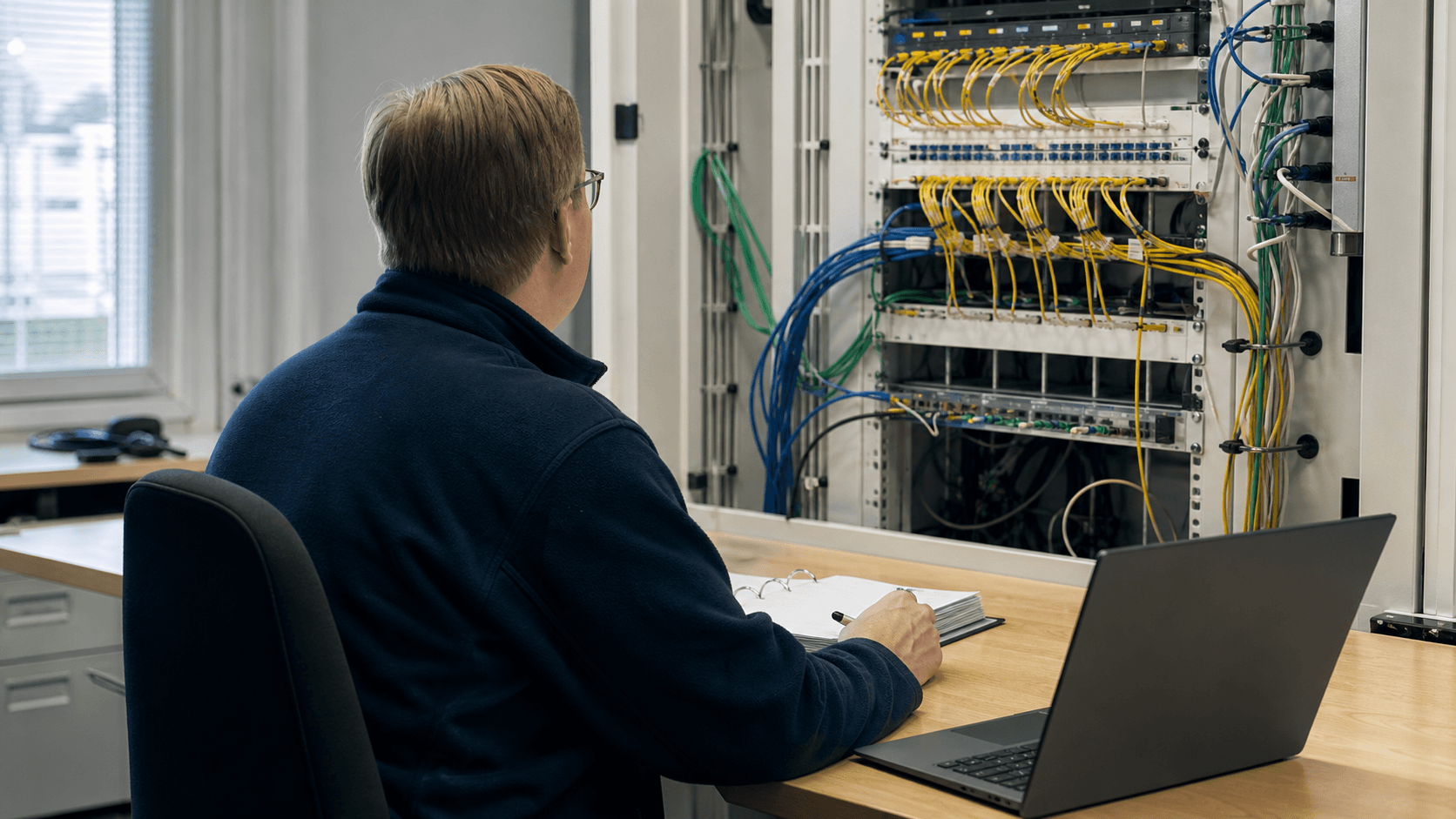

The useful place to start is not an autonomous-system number. It is the cost stack that a customer normally does not see. A Finnish office, municipal site, store, factory floor or regional service depot pays for connectivity because a failed link quickly becomes lost revenue, broken appointments, inaccessible records, stalled card payments, poor customer service, or a security exception. The visible invoice might say business internet, mobile broadband, private network, colocation, router service or mobile subscription.

The economic product is narrower and more demanding: keep the customer's operating environment reachable, document who owns the fault, and make the next failure cheaper to solve than switching providers would be.

That is the right lens for AS Telia Finland Oyj. The public BTW directory page at https://btw.media/en/directory/as-telia-finland-oyj identifies the existing directory company entity and frames it around visible routing resources. The relevant public routing question is AS20569, described in public resource context as AINAIP-AS Telia Finland Oyj. That is a useful clue, but it is not a business model. A resource-holder record is a public accountability surface. It does not say which customer bought a service, whether that service is active, whether the route is central to Telia Finland's wider network, or whether the operator can turn the record into reliable operating value.

The short name, Telia Finland, matters because the customer-facing economics sit in Telia Finland's wider service estate. Telia's business site at https://www.telia.fi/yrityksille presents an enterprise menu that includes phone subscriptions, mobile broadband, M2M subscriptions, network design, LAN, SD-WAN, DataNet, mobile-work networking, private networks, SASE, push-to-talk, office internet, demanding-use internet, international internet, cyber services, cloud, data-centre capacity, customer-service and switchboard services, IoT, design, deployment, management, monitoring and service desk. That menu is not proof of any AS20569 margin, but it is strong evidence of the operating unit a buyer can actually purchase.

The strongest paid unit is therefore an operating-continuity account. A customer buys access, routing, backup, equipment, monitoring, repair, security, address stability, escalation, and an accountable supplier boundary. It buys someone to decide whether the failure is fixed broadband, mobile backup, customer equipment, local power, fibre access, DNS, cloud reachability, DDoS filtering, peering, address allocation, or a partner network. That is why a resource record alone is inadequate. A route object can identify public reachability.

It cannot tell whether Telia can stop a retailer's payment outage, a municipality's remote-service failure, a factory's sensor gap, or a law firm's secure access problem from becoming a customer-retention event.

The cost stack is expensive because it combines capital and labour. Spectrum rights, fibre backbones, colocation rooms, routers, mobile radio sites, monitoring systems and IP address resources are the visible capital. Field visits, design work, security review, customer-premises configuration, change windows, service-desk triage, escalation to other providers, and documentation are the labour. A small customer may perceive the service as a monthly access bill; Telia has to price the hidden work of making that access useful when something breaks. The customer renews if the provider reduces the cost of uncertainty.

The customer shops alternatives if the provider only supplies a public resource label and an opaque support path.

The simplest customer test is a renewal after a bad incident. Suppose a regional professional office has a fixed access path, a mobile backup, a managed router, public addressing for partner systems, a private connection to a hosted application and staff who cannot operate manually for more than a few hours. The first invoice line may be modest. The real account value appears when the fixed link fails during business hours. If the router fails over cleanly, the help desk understands the site, the public address dependency is documented, and the customer can see what degraded and what survived, the renewal conversation changes.

The customer is not comparing raw megabits. It is comparing the avoided cost of a failed workday with the price of a better continuity bundle.

That is also where Telia can lose the account. If support cannot explain whether the problem was local fibre, mobile signal, customer equipment, routing, DNS, DDoS mitigation or a partner service, the same customer learns that the bundle was less accountable than advertised. At that point a national competitor, a local fibre company, a managed-service provider or an in-house IT team can attack the account by offering clarity. The public AS record cannot defend against that. Only service evidence can.

Pricing has to be read through that operational lens. Telia's public business price list at https://www.telia.fi/yrityksille/asiakastuki/laskut-ja-maksaminen/yritysasiakkaiden-palveluhinnasto supports the idea that ordinary business subscriptions, M2M connections, service changes and network add-ons are granular commercial units rather than one monolithic telecom product. Granularity can be attractive because the customer pays only for the pieces it needs. It can also hide the true price of resilience if installation, public-address use, backup, service level and support are treated as add-ons after the buyer has already anchored on a cheap line. The better commercial model is to make the full cost of failure visible before the customer buys.

The resource-holder surface fits into this pricing only when it affects that failure cost. Public addressing, routing control and accountable AS information can matter for firewalls, partner allowlists, traffic engineering, monitoring, customer migrations and abuse handling. They are not automatically valuable to every customer. A coffee shop may not care which AS is behind its connection if card payments and Wi-Fi work. A data-centre customer, industrial site or public-sector buyer may care deeply if addresses, routes, traffic paths and escalation contacts are part of the risk file.

The article therefore treats AS20569 as a diligence pointer and tests whether Telia Finland's official operating model gives it business relevance.

What AS20569 Can Prove

AS20569 should be treated as evidence, not as an entity. The public routing source listed for this directory record is RIPEstat's AS overview endpoint at https://stat.ripe.net/data/as-overview/data.json?resource=AS20569. A careful reader can use that endpoint to test whether the public routing system associates AS20569 with the Telia Finland naming trail. That kind of source supports accountability because autonomous-system records are designed to expose routing identity, holder names, and public operational metadata. It does not support a claim that AS20569 is a separate company, a product line, a customer, a relationship endpoint, or a profit centre.

The distinction matters because Telia Finland already has a much larger and better documented Finnish operating network. Public Telia Finland records identify RIPE organisation ORG-SA28-RIPE at https://rest.db.ripe.net/ripe/organisation/ORG-SA28-RIPE.json and AS1759 at https://rest.db.ripe.net/ripe/aut-num/AS1759.json as part of the national Telia Finland routing surface; PeeringDB's Telia Finland page at https://www.peeringdb.com/net/18481 adds public interconnection context. That broader surface is relevant context, but it is not the same thing as the AS20569 directory clue. In this article, AS20569 is the assigned public-resource evidence. Wider Telia Finland sources are used only to decide whether a plausible operating unit exists behind the resource-holder trail.

The public record can answer a narrow question: is there a routing-resource pointer that makes the directory entry worth investigating? Yes. It can also answer a second narrow question: does Telia Finland have official business services that could give such a pointer operating meaning? Yes. Telia Finland's legal and business presence is visible on its own company page at https://www.telia.fi/telia-yrityksena, which states that Telia Finland Oyj is registered in the Finnish trade register, conducts VAT-liable activity, and lists the communications regulator as Viestintavirasto, now Traficom. The same page gives complaints and reporting routes. That does not validate AS20569 by itself, but it anchors the legal counterparty behind the public brand.

The public record cannot answer the commercial questions that matter most. It cannot say whether AS20569 carries a customer-facing service today, whether it is legacy Aina-related infrastructure, whether it is operationally material or peripheral, whether the address resources attached to it are heavily used, whether any customer contract names it, or whether a fault on that routing surface would affect a revenue-critical service. It cannot show service-level commitments, repair performance, utilisation, route diversity, upstream contracts, customer concentration, or gross margin. Those are private facts.

That is why this article prices against evidence limits. The directory clue is useful only if it leads to operating proof. The proof has to come from official product pages, financial segment reporting, regulator records, public network and spectrum sources, customer-facing service language, and credible market signals. A weak version of the Telia Finland case would stop at "AS20569 exists." A stronger version asks what a customer buys, what Telia must spend to deliver it, what substitutes discipline the price, and what evidence would convert a routing pointer into business confidence.

There is also a naming-risk problem. AINAIP looks like a historical or specialised resource label rather than the current consumer-facing Telia brand. That does not make it wrong or irrelevant. Telecom networks accumulate old labels, acquired assets, private route names and legacy service traces. But it does make the public evidence weaker for commercial purposes. If a buyer sees an AS label that does not map cleanly to a current service page, the right response is not to invent a business around the label.

The right response is to ask Telia for the mapping: which contracts, addresses, prefixes, sites or services depend on this resource, and what happens if it changes?

For public accountability, the label is still useful. It tells the reader where to look and which public resource namespace to test. For business valuation, it is incomplete. A telecommunications company can have many valid resource records that are operationally necessary but financially small. It can also have obscure records that quietly support valuable services. The public record alone does not distinguish those cases. That uncertainty is not a defect in the article; it is the central business risk.

The Official Paid Unit Is Continuity

Telia's office-internet service is the simplest official expression of the continuity product. The Yritysnetti page at https://www.telia.fi/yrityksille/palvelut/tietoverkot-ja-yhteydet/yritysnetti describes a business-premises internet connection using fixed broadband and mobile network connections. It says combining fixed broadband and the mobile network helps continuity in fault situations; it also says the customer gets the necessary package without investing in equipment or technical expertise or worrying about installation and basic maintenance. The page presents 4G pre-delivery for fast start and offers either fixed plus fast 4G or 4G/5G-only setups.

That product answers the first question directly: the customer buys usable site connectivity, not just bits. The invoice may look like a broadband product. The actual value is a managed path into the customer's premises, a backup route, customer equipment, installation, and the promise that the service can be matched to the site. A small company could buy a cheaper SIM or a consumer broadband line. It pays more if the provider absorbs the work of making the site dependable.

The demanding-use internet page at https://www.telia.fi/yrityksille/palvelut/tietoverkot-ja-yhteydet/internetyhteys-yrityksille raises the value proposition. It describes Yritysinternet Plus as a customisable internet connection for companies for which network operation is business-critical. It highlights high capacity, availability, performance planning, backup connections, service levels, firewall and harmful-traffic filtering. That is a different unit from ordinary access. It is a purchased option on uptime, security and future growth.

DataNet, at https://www.telia.fi/yrityksille/palvelut/tietoverkot-ja-yhteydet/datanet-yritysverkko, makes the private-network logic explicit. Telia says DataNet can form a company network between sites in one or several countries; lets selected stakeholders access a secure private network; can carry data, voice, video and real-time applications; can connect to external services including the internet and partner networks; can be delivered by one supplier; and meets PCI DSS requirements linked to card payment. It also describes design, testing, deployment, transfer to maintenance, chosen service levels, central management, monitoring, repair according to service level, 24/7 technical support, traffic prioritisation, multiple VPNs, internet VPN, backup connections, data-centre links, DHCP and protection against common denial-of-service attacks.

DataNet is where the cost stack becomes visible. The customer's problem is not "find me an AS." It is "connect these offices, partners, clouds, applications and payment obligations without exposing the business to unmanaged failure." Telia's cost is not only transport. It is design, segmentation, support, security posture, monitoring, and the credibility to coordinate when traffic crosses boundaries. Public routing data can support that credibility, but it cannot substitute for it.

Data-centre services add another layer. Telia's data-centre page at https://www.telia.fi/yrityksille/palvelut/konesalipalvelut says its data centres provide flexible and secure data-centre and cloud services so customers need not invest in their own servers or maintenance. The Helsinki Data Center page at https://www.telia.fi/yrityksille/palvelut/konesalipalvelut/datakeskukset describes domestic data storage, full maintenance, solutions ranging from a few servers to whole data-centre rooms, expert support for sustainable infrastructure planning, colocation space, and international backbone connections for links to offices and data centres elsewhere. That is operating value that a resource record can only hint at.

The official service evidence therefore points to an account model. Telia can be paid for the bundle around reachability: office internet, private networks, demanding internet, data centres, backup paths, monitoring, support and security. AS20569 is useful if it helps establish accountable public reachability. It is commercially weak if it remains a loose routing clue with no connection to the customer's continuity purchase.

The account model also explains why the buyer's substitute is not only another telecom operator. A customer can split the problem: buy fibre from one provider, a mobile backup from another, security from a specialist, cloud networking from a hyperscaler, equipment support from an integrator and monitoring from its own IT team. That split can be rational if Telia cannot show unified responsibility.

Telia's value improves when the customer would lose something by splitting the account: a known site design, a single repair path, integrated backup, coherent addressing, service-level clarity, or data-centre connectivity that works with private networking.

The official pages are therefore not just marketing evidence. They reveal which parts of the customer's work Telia wants to own. Yritysnetti says Telia can own the office access and backup problem. Yritysinternet Plus says Telia can own higher-performance internet and protection for business-critical use. DataNet says Telia can own site-to-site and stakeholder access. Data-centre pages say Telia can own hosting-adjacent infrastructure. The business judgement asks whether AS20569 is somewhere inside that ownership map or merely next to it.

Why That Unit Is Costly

The unit is costly because Telia has to own the awkward middle between customer premises and the public internet. A business site is not an abstract network node. It has an electrical panel, a landlord boundary, cabling, routers, Wi-Fi, firewalls, mobile signal variation, applications, point-of-sale terminals, VPN users, guest networks, cameras, voice services, cloud dependencies, documentation gaps and staff who call support only after the service is already failing. The supplier earns trust by knowing enough about that boundary to repair it quickly or to prove that the problem lies elsewhere.

Installation labour is the first cost. Yritysnetti's promise that the customer need not invest in technical expertise or worry about installation and basic maintenance sounds convenient, but for Telia it means provisioning, shipping or installing equipment, documenting the site, managing router lifecycle, testing fixed and mobile routes, and responding when the customer changes premises or applications. That work does not scale like a software subscription. It consumes people, scheduling and local knowledge.

Redundancy is the second cost. A fixed-plus-mobile service is valuable because a single failure should not end the workday. But redundancy requires design. The backup path has to be tested. The router has to fail over cleanly. The mobile cell has to have enough capacity. The customer has to understand what still works when the backup path is active and what is degraded. A provider that sells backup without testing it only postpones the outage. A provider that designs backup honestly may have higher labour and equipment costs but can justify a higher retention price.

Monitoring is a related cost. A customer-facing commitment means little if the provider first learns about a fault from an angry caller. Useful monitoring has to distinguish customer-premises power failures, last-mile faults, mobile congestion, routing anomalies, DDoS events, data-centre incidents and application-layer failures. A Telia service desk that can see only part of that chain may still be responsible in the customer's mind. That gap is expensive because it turns every ambiguous incident into investigation labour.

Security is the third cost. DDoS filtering, firewall services, harmful-traffic filtering, private-network segmentation and SASE-style services are not magic wrappers. They require policy, monitoring, updates, incident triage, customer education and integration with the customer's applications. Telia can spread these costs across its network and enterprise customer base, but each business account still has its own risk posture. A retailer, a municipality, a software company and a logistics operator do not need the same controls.

IPv4 and public-address management is a fourth cost. Public network resources are scarce, operationally valuable and often sticky. A customer may need public IPv4 addresses for partner allowlists, VPNs, remote access, industrial devices, payment integrations or monitoring. A route or address allocation can create switching friction, but that friction is not pure value. It raises Telia's responsibility. If address stability keeps a customer, Telia must also explain how those addresses are documented, filtered, secured and migrated when necessary.

Supplier and partner dependence is the fifth cost. Telia's model includes wholesale, fibre partnerships, shared radio assets, cloud connections, equipment vendors and systems integrators. The Finnish Shared Network at https://yhteisverkko.fi/en/suomen-yhteisverkko/ says DNA and Telia Finland founded Suomen Yhteisverkko in 2014 to design, implement and maintain a mobile network in Northern and Eastern Finland, and that its direct customers are Telia and DNA rather than end users. Nokia's supplier release at https://www.nokia.com/intelligence team/nokia-wins-5g-deal-with-finnish-shared-network-syv/ says the SYV 5G modernisation covered more than half of Finland's area and included radio access equipment, IP transport, upgrades to 2G, 3G and 4G, field maintenance, monitoring and implementation. Shared infrastructure can lower cost and improve rural economics, but it also means Telia has to manage a supplier and joint-network layer that customers may not see.

Cost is therefore not a reason to dismiss Telia's value. It is the reason the public record must be connected to a paid unit. If Telia uses its resources to make customer failures easier to absorb, the cost stack supports retention. If the customer experiences only opaque support and commodity access, the same cost stack becomes a burden that substitutes can attack.

The final cost is organisational focus. A national operator can own too many half-adjacent services and let complexity eat the margin. Telia's recent Finnish actions suggest the opposite intention: keep the network, secure connectivity and infrastructure surfaces; partner or transfer some labour-heavy enterprise IT work; use fibre partnerships where direct ownership is not required; and share rural radio infrastructure where duplication would be inefficient. That makes economic sense, but it also raises an evidence question. If a resource record sits outside the focused core, its value may be lower.

If it supports the focused core, it may be more important than its public visibility suggests.

Segment Numbers Show A Real Business But Not The Route Margin

Telia Company reporting confirms that Finland is a real national operating business, not merely a name attached to a routing record. The Q1 2026 report at https://mb.cision.com/Main/40/4339564/4055902.pdf gives Finland revenue of SEK 3.569 billion, service revenue of SEK 3.077 billion, adjusted EBITDA of SEK 1.121 billion and capex excluding spectrum and leases of SEK 284 million for the quarter. It says like-for-like service revenue grew 0.3%, mobile service revenue declined 2.0%, fixed service revenue rose 3.2%, mobile postpaid subscriptions excluding M2M declined by 79,000 year on year to 2.396 million, broadband subscriptions rose by 9,000 to 627,000, and TV subscriptions rose by 8,000 to 659,000.

Those numbers matter because they put the resource-holder question in a mature-market context. Telia Finland is not trying to prove that people in Finland need connectivity. The demand is established. The issue is whether Telia can move enough of that demand into higher-confidence fixed, business, secure and managed services to offset pressure in ordinary mobile. The Q1 2026 report's shape supports the article's thesis: fixed and business solutions are more strategically important when mobile subscriber trends are soft.

The 2025 year-end report at https://mb.cision.com/Main/40/4299511/3904809.pdf gives the longer view. Finland generated SEK 14.956 billion of revenue, SEK 12.844 billion of service revenue, SEK 4.682 billion of adjusted EBITDA and SEK 1.371 billion of capex excluding spectrum and leases in 2025. Those are enough to treat Telia Finland as a substantial operating unit. They are not enough to infer the profitability of AS20569-linked resources, an individual route, a single DataNet customer, a fixed-mobile office account, a Helsinki Data Center account or a public-sector connectivity contract.

The Q1 2025 MFN/Cision release at https://mfn.se/cis/a/telia-company/telia-companys-delarsrapport-januari-mars-2025-1ab066b5 is useful because it describes management's direction in words. It says Finland continued simplifying the business by scaling down non-core activities; a weak macro environment contributed to a service-revenue decline in that quarter; consumer mobile subscription losses continued, though at a lower pace than a year earlier; small and medium-sized enterprise focus produced positive subscription growth in that segment; and cost savings from the change programme produced lower resource costs and 6% EBITDA growth. That management commentary is consistent with a continuity-account strategy: reduce diffuse activities, focus on customers that value accountable business services, and protect margins through cost discipline.

The CGI transaction adds the operating boundary. The June 2026 release at https://www.prnewswire.com/news-releases/cgi-and-telia-announce-agreement-for-business-services-transfer-and-new-strategic-partnership-302785980.html says CGI and Telia agreed on a business-services transfer and partnership in Finland. Telia's cloud and capacity services for enterprise customers and IT end-user services would transfer to CGI, nearly 250 Telia employees would move to CGI, and Telia Helsinki Datacenter was excluded. The same release says Telia Finland has nearly 3,000 employees, around 4.2 million subscriptions across services and invests about EUR 200 million annually in nationwide telecommunications networks and secure ICT services.

That release is commercially revealing. Telia appears to be keeping the infrastructure and connectivity surfaces that fit the continuity thesis while moving some enterprise IT labour to a specialist partner. A customer can still buy Telia network services, secure connectivity and data-centre infrastructure. CGI may carry more of the generic cloud or end-user IT work. That can improve economics if Telia avoids labour-heavy service layers where it lacks scale and concentrates on resources that strengthen customer dependence on its network.

But the public financial record still cannot prove the final question: is a particular resource-holder surface worth paying for? Segment reporting supports the existence and strategic direction of the business. It does not show AS20569 traffic, customer contracts, service-level penalties, support cost, address utilisation, route incidents or renewal uplift. The correct conclusion is conditional: Telia Finland has the operating estate to make resource records meaningful, but the public record alone does not prove how meaningful AS20569 is.

The same caution applies to parent-company scale. Telia Company is large enough to buy equipment, fund spectrum, operate shared functions and support cross-border enterprise customers. Scale can lower procurement and operating costs. It can also make small resource surfaces invisible inside group reporting. A buyer should not assume that group strength automatically makes every Finnish route or service high quality. The better inference is narrower: Telia has the resources and incentives to professionalise continuity services, but the quality of a specific AS20569-linked surface has to be proven by operational records.

Nor should a reader confuse segment EBITDA with customer value. A high margin can come from efficiency, market power, low support cost, deferred investment or customer inertia. A lower margin can come from investment, transition costs or labour-heavy service improvement. The customer cares less about reported margin than about whether Telia can prevent or shorten failures. The investor cares about both. A good Telia Finland account is one where the customer pays for avoided risk and Telia can deliver that risk reduction without uncontrolled support labour.

Fibre, Radio And Public Resources Have To Work Together

Telia's operating value depends on combining multiple access layers. A pure mobile story is too narrow. A pure fibre story is also too narrow. Finland uses mobile networks heavily, but fixed networks carry much of the data. Traficom's mobile statistics page at https://tieto.traficom.fi/en/statistics/development-finnish-mobile-networks says Finland has had just over 9 million mobile subscriptions in use since 2012, that by December 2025 only a small share were voice-only, that most household and business subscriptions included unlimited data, and that mobile data use reached 78 GB per capita per month in the second half of 2025. That supports the mobile load problem: customers treat mobile as an everyday broadband utility.

Traficom's fixed-network statistics at https://tieto.traficom.fi/en/statistics/development-fixed-communications-networks-finland show the other side. Fibre availability reached 80% of Finnish households by September 2025, around 2.3 million homes; 80% of households had access to gigabit download speeds; and fixed networks carried a large share of communications-network data traffic. That supports the fibre option: heavy and predictable traffic often belongs on fixed networks, while mobile works as mobility, backup, rapid deployment or access where fibre is absent.

Telia's Valokuitunen move is a practical answer to this mixed demand. The Cision release at https://news.cision.com/telia-company/r/telia-to-increase-ownership-in-finland-s-leading-fiber-operator-valokuitunen%2Cc4314793 says Telia agreed to increase its ownership in Valokuitunen from 40% to 49%; the company is described as Finland's leading FTTH operator, reaching more than 400,000 homes in over 100 municipalities through an open-access model; Brookfield would hold 51%; and the cash consideration was approximately EUR 30 million. Telia does not need to own every fibre path outright if it can secure service access, influence and customer reach through an open-access fibre platform.

Spectrum remains paid optionality. Traficom's public mobile frequency table at https://traficom.fi/en/radio-licences-and-frequencies/use-radio-frequencies/frequencies-and-license-holders-public-mobile-networks lists Telia Finland across public mobile network bands including low-band, mid-band and millimetre-wave holdings. The Finnish Ministry's 2018 3.5 GHz auction release at https://lvm.fi/en/-/spectrum-auction-concluded-984712 says Telia Finland won the 3410-3540 MHz block with a EUR 30.258 million bid. The 2020 26 GHz release at https://valtioneuvosto.fi/en/-/1410829/5g-spectrum-auction-concluded-1206517 says Telia Finland Plc won 25.9-26.7 GHz for EUR 7 million with licences valid to 31 December 2033. These licences do not prove AS20569 value, but they prove that Telia has paid for national capacity rights that can support business services when paired with fibre, routing and support.

The access mix explains why public network resources matter but cannot carry the conclusion. IP addresses and autonomous-system records are part of the operating control layer. They can support routing, customer addressing, firewall rules, partner allowlists, monitoring and migration continuity. Yet they are valuable only when paired with services that customers need to renew. A dormant or peripheral routing record has little commercial force. A routing record tied to a private network, data-centre link, office backup or public-sector continuity contract can be a retention asset.

Market Dependence Is A Retention Test

Telia Finland's market dependence is not a simple share question. A national operator can have millions of subscriptions and still lose the most valuable accounts if customers re-bundle connectivity around fibre, cloud, security and integrators. The public subscription numbers in Telia's Q1 2026 report show why. Mobile postpaid subscriptions excluding M2M were down year on year, while broadband and TV subscriptions rose. Fixed service revenue grew faster than mobile service revenue. The market signal is that customers still need Telia-like infrastructure, but the paid mix is changing.

In that environment, resource evidence becomes useful only if it improves retention. A static address, stable route or known AS contact can matter for a company with partner allowlists, VPNs, industrial devices, hosted services or public-sector compliance duties. It can be irrelevant to a price-sensitive consumer or small office that can replace the connection with another operator's router. Telia's task is to identify where the resource surface creates real switching cost and then make that switching cost feel like service value, not lock-in.

The fibre market sharpens the test. As fibre availability expands, mobile-only broadband becomes less defensible for heavy fixed use in areas where fibre is affordable and timely. Telia can still win if it controls the customer relationship, offers mobile backup, sells managed CPE, connects to data centres, or participates in open-access fibre through Valokuitunen. It loses if the customer sees Telia as an expensive wrapper around infrastructure someone else can provide more transparently.

The enterprise market adds another layer. A small firm may accept a single supplier if the bundle is simple and reliable. A larger organisation may require multi-carrier diversity, documented failover and separate security controls. Telia can be the prime provider, one of several access legs, a data-centre provider, a mobile backup supplier, a private-network operator or a security partner. The account value depends on which role it earns. Public resource records can support credibility in several of those roles, but they cannot choose the role.

That is why market chatter should be used cautiously. Price-comparison pages, user complaints, social posts and performance reports can reveal how buyers perceive speed, reliability and service friction. They should not be treated as audited proof of network quality. The official and regulator sources establish the operating context. Market signals show where Telia may face pressure: price, mobile subscriber churn, customer-service cost, speed competition, fibre alternatives and the expectation that a telecom provider should be easy to deal with when something breaks.

Substitutes Discipline The Price

The substitute set is broad. A customer can buy from a larger incumbent or near-peer such as Elisa or DNA/Telenor, from a specialist managed-service provider, from a local fibre builder, from an open-access fibre provider, from a systems integrator, from a hyperscale cloud networking service, from an in-house team, from mobile-only broadband, from delayed installation, or from no active dependency if the service is not truly mission-critical. Each substitute attacks a different piece of Telia's continuity account.

The larger-operator substitute attacks scale and price. If a customer can get comparable coverage, faster speeds, better customer service or a cheaper bundle from another national operator, Telia's public resource trail does not matter. The route record will not keep the customer. Telia's defence is to show better continuity at the specific site: fixed-mobile design, backup testing, customer-equipment ownership, support response, data-centre reach, security filtering, or a credible path from business sales to technical repair.

The specialist-provider substitute attacks labour quality. A systems integrator or managed-security provider may not own the underlying network, but it may know the customer's applications better than Telia does. CGI's partnership with Telia shows that this boundary is not theoretical. If the customer's main pain is end-user IT or cloud operations, a specialist may carry the relationship. Telia remains valuable if it supplies the secure data-centre infrastructure, access underlay and network services the specialist depends on.

The in-house substitute attacks control. Larger enterprises can build SD-WAN, multi-carrier access, cloud direct connects, security tooling and operational monitoring with their own teams. They may want Telia as one access supplier rather than the accountable wrapper. Telia's response is to offer enough network, radio, fibre, address, security and service-level insight that outsourcing the underlay still reduces risk.

The delayed-purchase substitute attacks urgency. A customer may know the site is fragile but avoid buying a better service until the next failure. Telia's business challenge is to make risk visible before the outage. Public records do not do that for ordinary buyers. A useful sales and retention process shows the current path, the backup, the address dependencies, the likely failure modes, the cost of downtime and the price of improvement. Without that, the customer treats resilience as optional.

The no-active-dependency substitute is the hardest for a resource-holder article. Some public records create the appearance of importance without an active commercial dependency. A route, address block or historical AS name can remain visible even if it supports little current revenue. The buyer's due-diligence question is whether any customer actually depends on this surface. Public evidence cannot answer that for AS20569. It can only identify the evidence gap and point to the private records that would answer it.

Substitution also disciplines pricing before a failure happens. If Telia sells a site connection as a commodity, the customer will compare monthly fees. If Telia sells documented continuity, the customer will compare downtime risk. The first market is brutal because mobile and fibre offers are visible and often discounted. The second market is harder to enter but easier to defend because the buyer must evaluate installation memory, support quality, backup design, address dependencies and recovery evidence. Telia's public services are strongest when they move the buyer into the second market.

The delayed-purchase substitute is especially important for small and medium-sized enterprises. A business owner may know that the current setup is fragile but keep paying for the old service because improvement requires attention. Telia can either wait for the next outage and hope the customer blames the situation rather than the provider, or it can use renewal moments to surface dependencies: Which applications fail without fixed access? Which users need mobile fallback? Which public IP addresses are hardcoded into partner systems? Which sites need service outside ordinary business hours? Which traffic should be prioritised?

Those questions create consultative value, but they also require trained sales and support labour.

Regulation And Trust Raise The Stakes

Telecom services are regulated infrastructure, and Telia Finland's public trust surface is part of the operating value. The company page at https://www.telia.fi/telia-yrityksena identifies Traficom's predecessor as the communications supervisor and provides complaint and reporting paths. That is basic, but basic matters. A customer deciding whether to depend on a telecom provider wants a legal counterparty, a complaint route and a regulator-backed environment.

Public-sector and defence signals raise the ceiling. Telia Wholesale's page at https://www.telia.fi/operaattoreille includes a 2026 news item saying Telia Finland and Telia Cygate were approved as a NATO framework supplier and that Telia can participate in NATO and member-country procurements. A separate Telia article at https://www.telia.fi/telia-yrityksena/medialle/artikkeli/telia-naton-puitetoimittaja-intelligence team says Telia was selected as the first Finnish operator in that role. Another 2026 release at https://www.sttinfo.fi/tiedote/72123158/telia-toimii-nato-innovation-range-testaustoiminnan-virallisena-yhteyksien-tarjoajana?lang=fi&publisherId=69820923 says Telia was the official connectivity provider for NATO Innovation Range testing in Finland. Airbus's announcement at https://www.criticalcommunications.airbus.com/en/intelligence team/stories/2026-05-airbus-and-telia-form-a-strategic-partnership-for-critical-communications-in-finland says Airbus and Telia formed a strategic partnership for critical communications in Finland.

These signals should be handled carefully. They do not prove that AS20569 drives defence revenue. They do prove that Telia Finland is trying to sit in higher-trust procurement and critical communications contexts where uptime, jurisdiction, security and supplier accountability matter more than ordinary consumer speed claims. The economic value is not the headline; it is the option to sell continuity to customers whose tolerance for unmanaged failure is low.

Regulation can also cut against Telia. The Finnish Competition and Consumer Authority release at https://www.kkv.fi/en/current/press-releases/the-market-court-outlined-calls-to-telias-telephone-based-customer-services-concerning-existing-contracts-are-too-expensive/ says the Market Court outlined that calls to Telia's telephone-based customer service concerning existing contracts were too expensive. That is not a network-quality finding, and it should not be overread. It is still a useful market signal because mature telecom customers evaluate friction as part of trust. A provider cannot sell continuity while making ordinary service resolution feel costly or opaque.

Unofficial performance signals are similarly bounded. Opensignal's Finland page at https://insights.opensignal.com/finland summarised the competitive field in May 2026 as DNA leading overall speeds, Elisa leading coverage, and Telia winning consistency while sharing the reliability lead with Elisa. This is not a regulator ruling, and testing methodologies have limits. It is useful because it aligns with Telia's best commercial angle: not always the fastest headline, but dependable experience and reliability.

The Evidence Gaps Are Not Details

The main gaps are not cosmetic. Public evidence does not show AS20569 customer count, traffic volume, prefix inventory, utilisation, incidents, upstream relationships, route diversity, SLA history, address allocation, or whether the resource still maps to a customer-facing product. It also does not show the economics of a specific office-internet account, DataNet account, data-centre customer, NATO-related opportunity, CGI-partnered enterprise service or Valokuitunen-linked fibre account. Those are the facts that would turn a public routing clue into an underwriting view.

The first private fact that would change the judgement is service mapping. Which customer-facing products, if any, rely on AS20569? Is it tied to legacy Aina infrastructure, a regional customer base, a Telia-controlled route domain, an enterprise service, a wholesale arrangement or a historical record? A route that still supports paying customers is different from a route that exists mostly for continuity or administrative history.

The second private fact is utilisation and dependency. How much traffic crosses the surface? Are there business-critical customers, public-sector users, static-address customers, partner allowlists or VPNs that would make migration expensive? Are customers told which resource surface they depend on? Does Telia maintain current documentation? Public routing data can point to accountability; it cannot show dependency.

The third private fact is fault history. How often do customers experience failures in the relevant services? How many are caused by Telia-controlled infrastructure, shared-network layers, fibre partners, customer equipment, power, software, security events or external internet paths? What are the repair times by service tier? Telia's public pages describe service levels and support; only private operating or customer records show performance.

The fourth private fact is renewal behaviour. Do customers renew because Telia reduces risk, or because switching is painful? Switching friction can protect revenue in the short term, especially when addresses, VPNs, routers, payment systems and partner rules are involved. It can also create future churn if the customer feels trapped. Operating value is strongest when a renewal follows a demonstrated avoided outage, not merely a migration burden.

The fifth private fact is margin by bundle. A site with fixed broadband, mobile backup, managed router, DDoS filtering, public IPv4, service desk and a higher service level can be profitable if priced correctly. It can be unattractive if field support, churn prevention, equipment replacement and outage handling consume too much labour. Segment EBITDA does not reveal this bundle-level economics.

The Proof That Would Change The Judgement

The article's judgement would become stronger with a clean service map for AS20569. That map would show whether the resource supports current Telia products, legacy customer networks, Telia-controlled infrastructure, an acquired regional asset, wholesale traffic, enterprise accounts or a standby surface. It would also show whether any customers are contractually dependent on the resource or whether it is merely visible in public routing systems. Without that map, the safest conclusion is bounded: AS20569 is a legitimate evidence trail, not a standalone business proof.

Traffic and utilisation data would also change the view. If AS20569 carries material customer traffic, supports multiple prefixes, or appears in route-monitoring alerts tied to paying services, it deserves more weight. If it is lightly used, unannounced, or mostly administrative, it deserves less. Public URLs can help readers ask the question; they cannot answer utilisation with enough confidence for a business conclusion.

Customer renewal data would be decisive. A high renewal rate after documented outage recovery would support the continuity thesis. A high renewal rate accompanied by complaints, poor documentation or migration friction would be weaker. Telia needs customers to renew because it lowers risk, not because leaving is confusing. The difference is visible in support records, churn reasons, win-loss analysis and customer interviews, not in a public AS overview.

Service-level performance would matter as much as revenue. A provider can sell backup, monitoring and repair targets, but the proof is repair time, customer communication, root-cause clarity and repeat-incident reduction. If Telia can show that office-internet, DataNet, demanding-use internet and data-centre-connected accounts experience fewer severe failures or recover faster than substitutes, the operating value is real. If not, the services are just more line items.

The final proof would be dependency transparency. A mature continuity provider can tell a customer what depends on Telia, what depends on partners, what depends on customer equipment and what can be moved without disruption. That transparency may sound like it weakens lock-in, but it usually strengthens trust. Customers pay more willingly for a provider that can explain the exit path than for a provider that benefits from hidden complexity.

The Business Judgement

AS Telia Finland Oyj matters because the public record exposes a resource-holder surface that should not be ignored. The directory page, the AS20569 routing pointer, Telia Finland's legal presence and the wider official service evidence together make the entity worth analysing. But the resource record is only a starting point. It is not the commercial conclusion.

The customer actually buys operating continuity: office access, private networking, backup paths, managed equipment, data-centre reach, security controls, public-address stability, support and escalation. That unit is costly because it combines spectrum, fibre, routing resources, hardware, field work, monitoring, security labour, partner coordination and documentation. Public evidence can prove that Telia Finland has an official business service estate and a substantial national operating context. It cannot prove that AS20569 is the source of customer value or that any particular customer is better off paying for it.

The most defensible view is conditional but useful. If AS20569 is tied to an active Telia Finland operating surface that supports customer connectivity, address continuity or private-network reachability, then the record has value as part of a larger continuity account. If it is merely a loose or legacy routing label, it should be treated as a weak public clue and no more. In either case, network and resource records are evidence, not entities. The business judgement has to move from public resource accountability to operating proof.

Telia Finland's advantage is that it has real proof in adjacent layers: business internet that combines fixed and mobile access, DataNet private networks, demanding-use internet, data-centre services, fibre optionality through Valokuitunen, shared rural radio economics through Suomen Yhteisverkko, critical-communications references, and segment-level reporting that shows a mature but substantial Finnish operation. Its risk is that customers increasingly compare providers by price, speed, reliability, customer-service friction and the ability to work with integrators or cloud platforms.

Telia has to make the public footprint mean something a buyer can feel in a fault, a renewal or a migration decision.

The decision rule is practical. Give the resource record weight when Telia can connect it to a service map, a customer dependency, a documented address or route requirement, a tested backup path, a support owner and a repair history. Discount it when the only evidence is a name, an AS number, a stale label or a public endpoint with no connection to paid continuity. That rule protects both sides of the analysis: it respects public resource accountability without pretending that registry visibility is the same as customer value.

That is the final test. A routing record can start diligence. It cannot close it. Telia Finland earns the account only when it connects public resources to operating value: lower failure cost, clearer responsibility, better backup, documented dependencies, credible repair, and a customer who can explain why paying Telia is cheaper than discovering the missing proof during an outage.