Summary

- E.N.A.I. Systems B.V. is best evidenced as a Dutch security-automation and service-centre technology company, not as a conventional mass-market access provider. It develops alarm-centre, care, comfort, digital-safety and control products, supplies applications linked to professional service centres, and maintains a Capelle aan den IJssel operating base with a long corporate history.

- The network-resource evidence is real but bounded. RIPE records identify the company as a Dutch LIR with AS204456, IPv4 space in the 185.222.232.0/22 range and IPv6 space in 2a0d:800::/29, while public routing views point to Eurofiber and Odido as important external network counterparties. That is resource-holder context and potential operating control, not proof of a large retail ISP revenue base.

- The investable question is pricing discipline. ENAI can create value if customers pay recurring fees for monitored systems, secure signalling, reachable engineers and continuity that larger carriers or generic cloud tools cannot tailor as well. It destroys value if it carries telecom obligations, supplier dependence and support labour while competing mainly on cheap connectivity or generic hosting.

The cash-flow test starts with one protected account

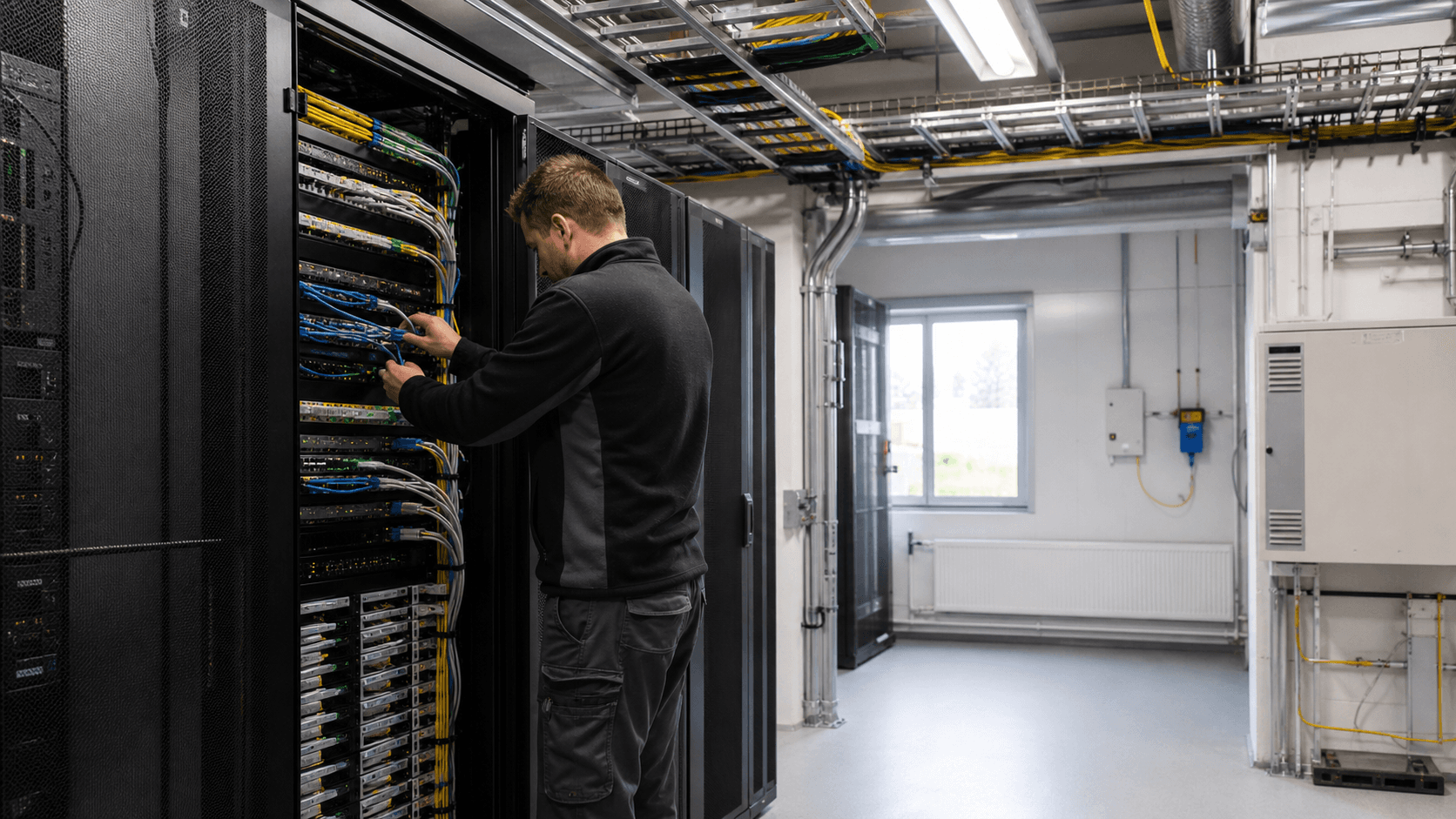

The useful way to look at ENAI is not to begin with an autonomous system number or a product list. Begin with one paying account that needs alarms to be received, processed and acted on when something has gone wrong. The customer may be a professional service provider, a security organisation, a care operator, a building-services integrator or an institution that cannot treat availability as a convenience. That account pays because a signal, an application session, a mobile instruction or an alarm event must move from the field to the right operator and back into an action.

That fee has to carry more than software. It has to pay for network connectivity, upstream carrier relationships, resilient hosting, vendor hardware, mobile-app maintenance, technical support, implementation work, security monitoring, incident handling, spares, documentation, office overhead and the staff who answer when the customer is not interested in hearing that a third-party supplier is responsible. If ENAI sells reliability, it owns the coordination burden even when it does not own every physical cable.

The company's public language supports this reading. ENAI describes itself around safety and comfort, professional service providers, alarm-centre solutions, care, smart environments, digital safety, consultancy, knowledge transfer, 24-hour continuity and control. Those are not the words of a household broadband challenger. They are the words of an operator that tries to make complex safety and communications technology usable for service organisations that have their own customers and reputational risk.

The economic strength is that the buyer is not paying merely for bandwidth. A signal-handling centre, a secure app connection or a managed alarm receiver can justify a higher fee than a commodity internet line if the customer believes ENAI reduces downtime, false alarms, coordination cost and compliance risk. That is value creation: the customer's avoided failure is worth more than ENAI's cost of providing the service.

The weakness is that reliability businesses accumulate fixed costs quickly. The first customer needs enough engineering, routing, software and support to be credible. The tenth customer can share that platform. The hundredth customer can make it attractive. But if account volumes are small, every support promise is expensive. A local team and a resource footprint can look strategically attractive while still producing weak cash return if too much of the cost is held for too few paying events.

That is why the article's central question is about price, not technology. Can ENAI charge enough for local repair, reachable support and accountable continuity to cover transit, backhaul, field work, abuse response and churn? If the answer is yes, the network resources are useful because they support a defensible service layer. If the answer is no, the resources risk becoming a credential around a business whose margins are set by larger carriers, device vendors and application substitutes.

Company identity and operating boundary

The legal and operating identity is relatively clear. Public Dutch company-profile sources identify E.N.A.I. Systems B.V. with KVK number 24070561, a Capelle aan den IJssel address at Rhijnspoor 247 and a corporate history dating back to 1946. The same public records present the business as active and small by headcount, with roughly two dozen full-time employees in recent filings. The figures visible through third-party company profiles also show positive equity in recent years, but do not disclose revenue, gross margin, operating cash flow or product-level economics.

That small-company boundary matters. ENAI's public site speaks in broad terms: alarm centres, apps, live contact, image, access control, GPS tracking, availability services, reporting, invoicing, telephone integration, information security, care support and digital monitoring. A broad portfolio can be commercially powerful if the same customers buy several modules. It can also dilute scarce engineering capacity if each product requires unique maintenance and support.

Company.info's profile gives a more precise description of the operating core. It says ENAI develops complete security solutions for medium-sized and large enterprises, with emphasis on receiving, registering and processing alarm reports. It describes a combination of security automation, telecommunications techniques, turnkey project execution and maintenance, and notes OEM supply for manufacturers of electronic security equipment. That description connects the website's marketing to a concrete industrial niche: alarm and service-centre technology.

The mobile app evidence reinforces the point. The OMS app listings describe an application for Siemens Netherlands users to view and operate alarm notifications through a secure connection to the Siemens Customer Service Center. The app is provided by E.N.A.I. Systems B.V. and has been present in app stores for years. That does not prove large revenue, but it shows ENAI sitting behind branded professional service workflows where another institution owns the customer relationship and ENAI supplies the enabling technology.

The company also appears in security-sector ecosystems. Security Delta and Security Insight profiles repeat the ENAI story around service-centre solutions and list the Capelle address. AddSecure's partner listing shows ENAI among security partners. Vanderbilt integration pages discuss the RX-8000 alarm receiver and its role for central monitoring stations, while older industry news and vendor releases describe ENAI integration with Texecom, Vanderbilt and Dialogic technologies. These sources are not financial statements, but they show that ENAI's products are recognised in the alarm-receiving and service-centre market.

The correct operating boundary is therefore narrower than "regional ISP" and broader than "software vendor." ENAI is a systems company using communications, network resources, apps and supplier integrations to support professional continuity services. The directory classification gives a useful monitoring lane because number resources and carrier dependence matter. It should not be read as proof that the company sells consumer internet access, IP transit, cloud infrastructure or registry services as its main business.

That distinction affects valuation. An access provider is judged on subscribers, average revenue per line, wholesale cost, churn, network capex and regulation. ENAI should be judged on recurring service contracts, support intensity, app and receiver maintenance, implementation backlog, supplier terms, incident performance, field-response load and whether its number resources improve customer retention or reduce supplier dependence.

What customers seem to buy

ENAI's public offer has four visible revenue shapes. The first is platform and product licensing around alarm and service-centre operations. Products named by the company include Facman, x-ALARM, x-HOME, RX-8000, Information Services, d-FENCE, Responsability and Comfortability. The names matter less than the architecture: they suggest a suite sold to professional organisations that need to receive, classify, monitor, communicate, bill and report around events.

The second revenue shape is integration. Alarm-centre systems are rarely isolated. They connect to receivers, sensors, customer databases, mobile apps, phone systems, video, access control, service desks and reporting. ENAI's public material repeatedly stresses combining its own building blocks with other suppliers. That is economically attractive when ENAI is paid for design authority and ongoing support. It is less attractive when integration becomes unpaid custom work needed to win a product sale.

The third shape is maintenance and continuity. The website says system failure can have a major impact on daily operations and that ENAI offers several service levels to guarantee effectiveness. For a customer buying alarm handling or secure service-centre tools, the support promise is central. A cheap monthly licence is not enough if no one responds to failures. The commercial unit is the whole service relationship: setup, monitoring, repair, updates, advice and accountable contact.

The fourth shape is digital-security monitoring. The d-FENCE site describes a digital alarm system for computers, networks, websites and online identity, with 24-hour monitoring and partner distribution. It advertises a low starting monthly price through a channel offer. That is a useful signal because it shows ENAI trying to convert safety-sector logic into cyber resilience: monitor the digital environment like a physical alarm installation. The risk is that low entry prices can be thin unless monitoring is automated, false positives are controlled and partners carry part of the customer-support burden.

These shapes have different margins. A receiver sold with installation may include third-party hardware and one-time project revenue. A mobile app tied to a service centre may require continuous development but can scale across accounts. A monitoring offer may have a low monthly entry point but high long-term value if it retains customers and attaches response services. Consultancy and knowledge sessions can be profitable when they lead to product adoption, but they are hard to scale if senior staff must deliver every engagement.

The market rewards ENAI when customers value operational accountability. A professional service provider does not want to assemble one alarm receiver, one app developer, one carrier, one hosting provider, one cyber-monitoring tool and one field support team. The buyer wants one party that understands the workflow and can make the whole system work. ENAI's public proposition is built around that convenience.

The same bundle creates a disclosure problem. Public evidence does not show how much revenue comes from product licences, hardware, apps, monitoring, maintenance, professional services or telecom inputs. It also does not show whether recurring revenue is growing faster than project work. Without those splits, investors and counterparties should assume that ENAI's economics depend on execution discipline rather than on a simple annuity.

Number resources show control options, not a retail footprint

The RIPE evidence is important because it gives ENAI a measurable place in internet number-resource governance. RIPE and routing records identify ORG-ESB3-RIPE for E.N.A.I. Systems B.V., an LIR designation, AS204456 named enai-systems, IPv4 allocation context around 185.222.232.0/22 and IPv6 allocation context around 2a0d:800::/29. The organisation record links the company to the Capelle aan den IJssel address and a network operations contact.

That evidence should be read carefully. An LIR and address allocation prove that ENAI has registry responsibilities and resource-holder context. They do not prove that the company sells broadband, operates a large autonomous network, hosts many domains or earns meaningful IP transit revenue. IPinfo and IPGeolocation views both indicate very limited or inactive routing directly under AS204456, while other route views show parts of ENAI-associated IPv4 space announced through larger Dutch networks.

The visible counterparties matter. The AS204456 registration contains routing-policy lines referencing Eurofiber Nederland and Odido Netherlands. BGP and geolocation views show 185.222.232.0/24 associated with Odido and the broader 185.222.232.0/22 context associated with Eurofiber in some views. BigDataCloud records the 185.222.234.0/23 block as reachable globally through Eurofiber. This pattern suggests ENAI is not trying to be a large independent transit network. It appears to use resource control alongside established carriers.

That may be economically rational. For a specialised alarm and service-centre systems company, buying carrier reach from Eurofiber or Odido can be smarter than building a full network. The company can preserve address continuity and registry control for its applications while avoiding the scale burden of operating a broad backbone. Customers care whether the service works; they do not necessarily care whether ENAI or a wholesale carrier lights the long-haul path.

The cost is dependence. If ENAI's services rely on one or two major network suppliers, resilience depends on contract terms, route diversity, last-mile options, service credits, maintenance windows and escalation relationships. The public record does not show whether ENAI has physically diverse paths, redundant carrier handoffs, backup sites, route-origin authorisations for every relevant prefix or documented failover tests. Those are the facts that turn resource evidence into reliability evidence.

There is also an abuse and governance cost. Address resources require operational contact, abuse handling and registry hygiene. An alarm-centre technology company may not want to run a retail ISP, but it still has to handle the obligations attached to its resources and any services reachable through them. If a customer system is misconfigured, compromised or used in a way that triggers complaints, ENAI may face operational work that a pure software vendor would avoid.

The address footprint therefore supports the business case only if it lowers customer friction or raises service quality. It can help ENAI offer stable addressing, controlled routing relationships, private integrations and local custody. It cannot by itself justify a premium. Customers pay for the outcome: a signal is received, a dashboard stays available, a support team responds, and the provider can explain why the service is resilient.

Pricing power has to come from accountability

ENAI does not publish a broad tariff book for every service. That absence is normal for a systems company selling to professional customers, but it makes the pricing test harder. We can still infer the logic. The company sells into markets where buyers have alternatives: large carriers for business internet, cloud providers for hosting, alarm receiving centres and security integrators for monitoring, software vendors for workflow systems, and internal IT teams for local operations.

Against those substitutes, ENAI's pricing power cannot come from generic bandwidth. The Netherlands has deep fibre, wholesale and enterprise connectivity markets. ACM's latest telecom monitor shows a fibre-rich broadband environment with dominant national players and strong fixed-mobile bundles. Odido's wholesale and business pages advertise broadband, Ethernet, internet, IP-VPN, cloud connect and national coverage. Eurofiber positions itself around business fibre, open infrastructure, cloud and data centres. A small specialist cannot out-scale those networks.

The premium has to come from context. ENAI understands alarm handling, service-centre workflow, sensor and receiver integrations, secure app access and the operational expectations of professional service providers. If a customer can call ENAI and get a person who understands the whole chain from alarm receiver to mobile workflow, the service has more value than a generic circuit with a support ticket. That is where local reliability becomes a product.

This type of pricing has a ceiling. Buyers still compare budgets. A service provider may value a complete alarm platform, but it can push back if hardware, app support, monitoring and connectivity are priced as separate surprises. ENAI needs packages that make the total cost visible while protecting margin for exceptional work. If the company underprices the base service and hopes to recover cost through ad hoc support, customers will resist the very charges that keep the service viable.

The OMS app illustrates both sides. It creates convenience for Siemens Netherlands service-centre users, presenting secure remote access and operation through a branded workflow. That can be valuable if it reduces calls, enables self-service and improves the service centre's customer relationship. But mobile apps require regular platform updates, privacy review, authentication maintenance, store compliance and support for login failures. An app that seems cheap at launch can become a recurring engineering obligation.

d-FENCE shows the same question in cyber monitoring. A low entry price can widen adoption through partners. Yet digital monitoring can generate alerts, triage work, customer questions and false-positive burden. The price must cover not only sensors but the human judgement around risk. If partners carry first-line service and ENAI supplies platform intelligence, margins can scale. If ENAI must handle every anxious customer directly, the economics are much thinner.

The strategic test is whether ENAI separates revenue growth from value creation. More customers are not automatically good if each new account adds custom support. More integrations are not automatically good if each vendor link creates a maintenance promise. Value appears when a new account can reuse the same platform, documentation, carrier relationships and support playbook while paying enough to fund its share of renewal capital.

The cost stack is heavier than the brand suggests

A safety-and-comfort brand can hide an industrial cost stack. ENAI's public offer rests on engineering labour, carrier services, vendor components, software maintenance, field coordination, physical office and workshop capacity, compliance work and 24-hour support. Each layer has to be paid before the company reaches profit.

Labour is the most important cost. Alarm-centre products, receiver integrations, secure apps and service-level promises require people who understand both safety workflows and communications technology. The Stagemarkt listing identifies ENAI as a recognised training company for ICT support and system-engineering paths, including infrastructure installation and management. That supports the view that ENAI needs practical technical capability, not only sales staff. Training is a strength, but it also signals dependence on scarce skills.

Carrier and hosting costs form the second layer. ENAI's number resources and public routing context point to reliance on established Dutch carriers. Those services have recurring fees, installation charges, service classes and upgrade cycles. A supplier maintenance event can become ENAI's customer problem if ENAI is the accountable service provider. Redundancy lowers outage risk but raises monthly cost.

Vendor components create the third layer. The RX-8000 receiver history references multiple infrastructures, including IP, GPRS, PSTN and ISDN, and integrations with protocols and equipment from other security vendors. Dialogic's release described ENAI using Diva media boards in RX-8000 alarm receiver contexts. Older Vanderbilt and Texecom material describes integrations into alarm communications. This supplier ecosystem gives ENAI credibility and compatibility, but it also means replacement parts, certification, firmware and support terms can affect ENAI's gross margin.

Application upkeep is the fourth layer. App-store records show OMS has had version updates over several years, with privacy disclosures around contact information and encrypted transit. Even stable apps need ongoing work as iOS, Android, authentication methods and enterprise security expectations change. If the app is tied to alarm operations, downtime or login failure is not a minor inconvenience.

Support and incident handling are the fifth layer. The company promises continuity and control. A customer does not buy that promise for ordinary days; it buys it for failures. A support team must diagnose whether a problem sits in a customer device, a receiver, an app session, an upstream carrier, DNS, an IP route, a server, a firewall, a vendor protocol or user error. That diagnostic burden is costly precisely because the product bundle is useful.

Capital renewal is the sixth layer. Receivers, servers, routers, firewalls, monitoring systems, app code, development environments and office infrastructure age. A company with 22 full-time-equivalent staff cannot fund renewal through scale alone. It needs disciplined recurring revenue, paid upgrades and product simplification. Otherwise technical debt consumes the same people who should be building the next customer feature.

The positive signal is that ENAI's public records show a long-lived company with positive equity and a focused sector. The caution is that longevity does not prove current return on capital. A business can survive for decades because it is trusted and useful, while still earning modest returns if customers resist the price of true resilience.

Suppliers and substitutes shape the margin

The Netherlands is a hard place to sell undifferentiated connectivity. It is also a good place to buy high-quality inputs. Eurofiber's public material describes a large open fibre network, Dutch data-centre assets and business infrastructure. Odido Wholesale offers national broadband access, mobile connectivity, Ethernet, internet, MVNO and IoT services for carriers and service providers. For ENAI, those firms can be suppliers, substitutes or both.

As suppliers, they let ENAI focus on its specialist layer. ENAI can use established wholesale and enterprise connectivity rather than building a network footprint it cannot fill. That reduces capital needs and improves reliability if the supplier service is strong. The tradeoff is that ENAI may have limited control over wholesale price, repair timing, physical path diversity and network changes.

As substitutes, those same firms can move up the stack. Odido Business sells business networks, IP-VPN, cloud connect, Ethernet connect, fixed internet, backup and DDoS protection. Eurofiber sells connectivity, cloud, colocation and infrastructure resilience. A customer that mainly wants secure connectivity can buy directly from a national provider. ENAI must prove that alarm workflow, service-centre knowledge and system integration justify staying in the middle.

Security-sector substitutes are also present. Large alarm-monitoring companies, system integrators and access-control vendors can provide platforms and service. App stores show ENAI's role in branded apps for professional customers, but brand-owner relationships can shift. A customer with scale can sponsor a new app, change receiver software or standardise on a different vendor suite if the economics make sense.

Cloud platforms are another substitute. Many service-centre functions can be delivered from public cloud or specialised SaaS. Cloud can lower upfront capital and speed deployment. It can also create new dependencies around data location, availability zones, identity, egress costs and third-party support. ENAI's opportunity is to help customers choose the right mix of local control and cloud convenience. Its risk is becoming a small maintainer of legacy equipment while newer buyers choose cloud-native tools.

The supplier dependence has a geopolitical dimension even inside the Netherlands. Telecommunications resilience is now tied to cybersecurity obligations, lawful access duties, foreign vendor restrictions, privacy expectations and critical-infrastructure policy. ENAI's customers may be in safety, care and public-service-adjacent settings. That makes vendor provenance, data handling and service continuity more than procurement details.

The company can defend its margin by making the bundle measurably better. That means documented service levels, clear responsibilities, tested failover, predictable support prices, transparent privacy handling and a narrow set of vendor integrations ENAI can maintain deeply. Strategy without resource allocation is marketing. If ENAI claims to sell continuity, capital and staff must be allocated to the parts of the system most likely to fail.

Customer concentration is the hidden risk

ENAI's public evidence points to professional and institutional customers, but it does not disclose revenue concentration. That is a major uncertainty. A small systems company can look diversified because it has many product names and partner references while still depending on a few major accounts for cash.

The app evidence shows one named branded workflow around Siemens Netherlands. Security-sector pages show ENAI in partner ecosystems. Industry material around RX-8000 points to central monitoring stations and security providers. Those are useful references because professional customers validate the technology. They also raise bargaining-power questions. If one large brand or service centre accounts for a significant share of app maintenance, receiver support or custom development, ENAI may have less pricing freedom than the product catalogue suggests.

Concentration can also hide in channels. d-FENCE describes partner and distributor routes. A channel strategy can scale sales while reducing direct support load. But if a few partners control most demand, ENAI's economics depend on partner incentives, training quality, churn and first-line service performance. The company may own the technology risk while the partner owns the customer relationship.

Support concentration is different from revenue concentration. A large account may pay well and require predictable work. A small account may pay little and generate many support requests. ENAI should measure contribution after support hours, not only invoice value. The same is true for custom integrations. A customer that demands unusual device support or bespoke reporting can consume engineering time out of proportion to contract value.

Public headcount makes this especially important. With a small workforce, a single demanding implementation can crowd out product development or delay lower-value customers. That may be rational if the account is profitable and strategic. It becomes dangerous if engineering work is given away to preserve a relationship.

The company profiles do not disclose backlog, recurring revenue share, renewal rate, average contract length, top-customer share or gross margin by product. They also do not show whether equity growth came from operating profitability, retained earnings, asset revaluations or group transactions. The article therefore cannot conclude that ENAI has high customer concentration. It can only say that concentration is the primary missing fact in a business of this size and shape.

What would a healthy pattern look like? No single customer should determine the support rota. The same core platform should serve multiple service providers. App and receiver maintenance should be covered by recurring fees. Partners should be trained well enough to reduce direct support burden. Custom work should be priced and documented, not absorbed as goodwill. Carrier costs should be matched to committed revenue, not held on speculation.

The weak pattern is the reverse: a few major accounts demanding custom work, several legacy products needing specialist knowledge, low monthly monitoring prices, carrier contracts sized for resilience but not fully recovered, and a public website that distracts from the core offer. The public evidence is not sufficient to place ENAI in either pattern. It is sufficient to make the question central.

Regulation makes reliability a duty, not only a feature

Dutch telecom rules matter even if ENAI is not primarily a public internet provider. Business.gov.nl explains that providers of public electronic communications networks or services in the Netherlands must register with ACM, keep networks and services functional and secure, report interruptions or security issues to the Dutch Authority for Digital Infrastructure, protect privacy, follow net-neutrality rules where relevant and support lawful information duties in defined cases. RDI guidance stresses direct reporting of security and continuity incidents.

The public evidence reviewed here does not establish that ENAI sells public internet access. The distinction is important. Internal corporate networks, private service-centre systems and alarm applications may sit outside some obligations that apply to public telecom providers. But ENAI's use of number resources, carrier relationships, secure signalling and professional communications means the company must still understand where the boundary sits. Misclassifying a service can turn a commercial product into a compliance exposure.

Privacy is also unavoidable. App-store disclosures for OMS refer to contact information and encrypted transit. Alarm and care workflows can involve sensitive operational data, locations, identities and incident records. The customer may be the data controller, ENAI may be a processor or service provider, and third-party vendors may sit under the stack. The commercial question is whether ENAI prices the work required for privacy review, retention rules, incident notification and secure development.

Cybersecurity regulation is both demand and cost. Customers in safety, care, telecom and digital services increasingly need stronger monitoring, audit trails, incident response and supplier assurance. ENAI can sell into that demand through digital-safety products and consultancy. At the same time, buyers may ask ENAI for evidence of its own controls: vulnerability management, access control, backup, disaster recovery, staff training, supplier oversight and documented incident response.

The public ENAI site itself creates an operating signal. Search results show irrelevant casino-style posts on the same domain in 2025, and one indexed page appears under a normal ENAI URL while containing unrelated gambling content. That does not prove a breach and should not be treated as evidence about production systems. It does show website governance weakness unless there is a benign explanation. For a company selling digital safety and continuity, public web hygiene is part of trust.

The regulatory risk is not only fines. It is sales friction. A buyer may choose ENAI because it wants a specialist that understands safety workflows. The same buyer will ask harder questions if public materials look stale, contaminated or thin. Better documentation can convert regulation into advantage. Poor documentation leaves ENAI competing on relationship and price.

The ideal posture is simple: define which services are public communications, which are private managed systems, which data ENAI processes, which suppliers touch customer data, which resources are covered by incident duties, and which service credits apply when failure occurs. The clearer the boundary, the easier it is to charge for real reliability.

Unofficial signals point to diligence questions

Unofficial market signals should not be treated as proof, but they can identify questions. App-store data show OMS has modest public visibility but a long maintenance history. Google Play records more than five thousand downloads, while Apple and app-tracking pages show version 1.2.3 and years of updates. That supports continuity, but not revenue scale. A professional app can be commercially important with few public reviews if it serves a defined customer base.

Partner pages and industry references show ENAI's products inside security-sector workflows. Vanderbilt, Dialogic, Dr. Pfau and DEMA references around RX-8000 and alarm-receiver interfaces suggest technical relevance beyond ENAI's own website. Again, this is not revenue proof. It is ecosystem evidence. The question is whether these references still drive current sales or mainly document a long-lived installed base.

The company-profile data show a small workforce and positive equity. Liza's profile presents 22 FTE for 2024 and equity above EUR 1.3 million. That suggests a real operating base, not a shell. It also means the company likely has limited spare capacity for many simultaneous custom projects. A lean team can be profitable if products are standardised. It can be fragile if customers expect bespoke attention.

Stagemarkt's recognition of ENAI as a training company is positive for talent development. It also tells us the company needs infrastructure and support skills enough to train ICT workers. In a tight labour market, training can reduce recruitment dependence and preserve institutional knowledge. The financial benefit appears only if trainees become productive and stay.

The old BeveiligingNieuws item about ENAI's move to Capelle aan den IJssel described the company as more than 65 years old in the safety sector and moving to a modern workplace in 2015. The fact is dated, but it reinforces continuity. Long history can support trust in conservative safety markets. It can also bring legacy systems and product obligations that newer competitors do not carry.

The weakest signal is the public website condition. The official site includes duplicated sections, placeholder-like footer material and indexed irrelevant posts. None of that proves operational failure. But it conflicts with a premium digital-safety image. Customers buying critical communications often infer discipline from public documentation. If the low-stakes website is untidy, the company should compensate with stronger customer-facing evidence around uptime, security controls and support process.

The most important unofficial signal is absence. There is little public evidence of customer count, traffic volume, uptime, churn, financial scale by segment or current contract wins. For a private small company, that is normal. For an outside economic judgement, it keeps confidence moderate. The evidence base supports an operating thesis, not a definitive margin conclusion.

What would change the judgment

The current judgement is cautious. ENAI appears to be a credible Dutch safety and service-centre systems company with real number-resource context and a long operating history. It has a plausible path to value if recurring service contracts pay for the full reliability burden. It has not publicly shown enough financial or operational detail to prove that the network-resource footprint and continuity promises produce attractive returns after labour, supplier costs and renewal capital.

The first fact that would change the judgement is recurring revenue share. If most revenue comes from multi-year software, monitoring, maintenance and support contracts with low churn, ENAI's small scale becomes less concerning. If most revenue comes from one-time equipment projects and custom integrations, the reliability story is weaker.

The second fact is contribution margin after support. ENAI should know gross margin by product after carrier fees, hosting, app maintenance, field work, first-line support, vendor licences and incident handling. Revenue growth without this view can mislead management. A low-price cyber-monitoring product or app relationship can look strategic while consuming scarce engineers.

The third fact is customer concentration. A top-five customer share, average contract length and channel concentration would show how much bargaining power sits outside the company. A few strong institutional relationships may be valuable, but only if contracts fund the work they require.

The fourth fact is network resilience. ENAI's RIPE resources and carrier counterparties are useful; the open question is physical and operational diversity. Valid route-origin authorisations, redundant upstream contracts, tested failover, separated power and hosting arrangements, documented incident history and clear abuse handling would convert registry evidence into reliability evidence.

The fifth fact is capital renewal. The public company profiles show equity and headcount, but not capex, depreciation, software-development capitalisation, lease commitments or maintenance backlog. A service-centre technology company can run profitably for years and then face a costly receiver, app, security or infrastructure refresh. Customers should be paying enough now for that next cycle.

The sixth fact is website and security governance. Removing irrelevant indexed posts, cleaning public copy, maintaining privacy and processor documents, and presenting current security controls would not transform the business model. It would reduce avoidable doubt. In this market, trust is a commercial asset.

The seventh fact is partner economics. If partners and professional service providers handle sales and first-line support while ENAI supplies a robust platform, the model can scale. If partners generate fragmented demands without absorbing service cost, channel growth can erode margin.

The answer to the core economic question is therefore conditional. ENAI can sell reliability, local repair and reachable support at a price that covers the cost stack if it prices the whole accountable service and limits custom drift. It probably cannot win by looking like a small carrier. Its advantage is the operating context around alarms, service centres and safety workflows. The network resources are valuable when they strengthen that context. They are not the business by themselves.