Summary

- CAGHET-PLUS SRL looks like a small local broadband and cable television operator in Taraclia, not a national infrastructure owner. Its own public material says it has operated since 2000, serves cable television and high-speed broadband in Taraclia, began replacing cable with fiber in 2013, and now advertises a 190 lei internet and television bundle with speeds up to 150 Mbps.

- The economic case is fragile but not trivial. The company has a formal number-resource footprint through AS43783 and four IPv4 routes, yet the retail value proposition depends less on routing scale than on whether local support, repair speed and customer familiarity can defend cash flow against Moldovan market pressure where fiber penetration is high, bundles are common and larger providers advertise much faster service near the same monthly price.

The paying account buys local certainty

The economic incentive starts with one account, not with an autonomous system number. A household in Taraclia does not buy "connectivity" in the abstract. It buys the expectation that the video call works when a relative is abroad, the payment terminal in a small shop can settle, a school assignment can be uploaded, a television package can replace a separate entertainment bill, and someone reachable will answer when the line goes down. The bill has to be small enough for a local household budget, but high enough to carry costs that are not small at all.

That is the tension behind CAGHET-PLUS SRL. Its own public pages place the company in Taraclia and describe services of cable multi-channel television and high-speed broadband. The site says the business has been in the market since 2000 and that it began modernising the cable network by replacing it with fiber in autumn 2013. Those facts establish a local operating history and a retail service frame. They do not prove national scale, large enterprise capability or a high-margin wholesale business. They show a company whose primary claim to value is probably practical availability in a specific place.

For the customer, the first substitute is not a perfect technical comparison. It is the option that seems good enough at an acceptable monthly price. A larger Moldovan operator may offer faster headline speeds, a bundled mobile discount, a router promotion or a television package with more channels. Another local provider may know the same buildings and streets. Mobile broadband may be enough for a household that mostly streams on phones.

The only reason a smaller local operator can hold the account is if the customer believes the service is reliable enough, the support path is less remote, the repair routine is familiar and the total bill is understandable.

That is why revenue growth and value creation have to be separated. Adding accounts at a discounted price can lift revenue while weakening the business if each new connection requires a long drop, a router subsidy, content cost, help-desk time and future repair visits. Raising prices can improve reported revenue but destroy value if customers can switch to a faster alternative. Selling reliability is valuable only when the customer pays for it and when the provider has the operating discipline to deliver it without letting field work consume the margin.

The downside bearer is also clear. If the line fails, the customer loses access. If transit or backhaul cost rises, the provider carries it unless the bill can be repriced. If a storm, cable cut or power problem causes repeated visits, the repair burden sits with the operator. If abuse complaints, payment collection or television carriage terms become more complex, a small staff must absorb work that a larger carrier can spread across a bigger base. Strategy without resource allocation would be marketing here. The real strategy is whether the monthly account can fund the boring work of staying reachable.

The business boundary is local and specific

CAGHET-PLUS SRL should be read first as a Taraclia service business. The company site lists contact details in Taraclia, including an office location, working hours and local phone numbers. Its service page lists cable television and internet. It shows a television subscription at 50 lei and an internet plus television plan at 190 lei with speed up to 150 Mbps, a 36-month term and a connection fee. The page also says cable television is provided free when the internet plan is connected. This is a retail bundle, not a claim of broad telecom infrastructure.

The official self-description is useful because it narrows the boundary. The company says it is one of the operators in Moldova providing cable multi-channel television and high-speed broadband in Taraclia. That wording matters. It is not a national data-centre story, a cloud platform story or a carrier-neutral exchange story. It is a small access-network and television story in a city whose 2024 census population is reported at roughly ten thousand people. The addressable market is therefore limited even before competition, household income and migration are considered.

The operating boundary is also shaped by the local economy. A small city can be attractive for a local provider because reputation travels quickly and customers may value proximity. The same feature limits upside. There are only so many households, shops, schools, cafes and offices to connect. Once the main streets and apartment blocks are wired, incremental growth becomes harder. Expansion into nearby localities may require more plant, longer repair routes, new permissions and lower density. Staying only in the core area protects service response but caps scale.

Third-party company information adds a financial caution. A public commercial registry page identifies the legal company, registration date, address, ownership and administrator, and shows visible historical financial signals for 2023: sales income of about 590.58 thousand lei, a net loss of about 116.55 thousand lei, negative equity and six employees. That page is not a full audited telecom operating model, and several fields are masked or subscription-limited. Still, the visible figures are consistent with a very small enterprise. If they are directionally accurate, the company has little room for expensive mistakes.

The company therefore has to make local focus do economic work. A small operator cannot assume that scale will rescue an undisciplined cost base. It cannot carry many unprofitable accounts for long. It cannot keep matching every national promotion if the national player is using mobile, television, device financing and a broader brand to spread acquisition cost. CAGHET-PLUS must be valuable for reasons a bigger provider may not reproduce cheaply in Taraclia: local knowledge, fast practical response, personal collection discipline, existing cable or fiber routes, and customer trust built over time.

This does not make the business weak by definition. Small local access providers can survive when their plant is paid down, their support costs are controlled and customers value direct service. But the boundary needs to be honest. CAGHET-PLUS is not being judged as if it were Moldtelecom, Orange or StarNet. It is being judged on whether a narrow local footprint can produce enough cash to maintain a modern service promise.

Number resources prove responsibility, not market power

The routing record is important, but it has to be kept in proportion. CAGHET-PLUS appears in RIPE NCC membership and routing evidence as a Moldovan member and resource holder. AS43783 is associated with CAGHETPLUS-AS and CAGHET-PLUS SRL. Public routing pages show four IPv4 routes, each a /24, for a total of 1,024 IPv4 addresses, and no visible IPv6 routes in the third-party summaries reviewed. Some records also mark the advertised IPv4 space as valid under routing-security checks.

That evidence says the company is not merely a reseller name on a bill. It has a formal footprint in the number-resource system and appears to originate its own address space. For a small local provider, that matters. It can support more direct control over routing policy, abuse contact handling, address assignment, provider changes and service continuity. It may also signal that the operator has invested in technical administration beyond a simple downstream retail arrangement.

But the record should not be inflated. A RIPE membership and an autonomous system do not prove that the company sells IP transit, cloud hosting, managed network services or wholesale connectivity at meaningful scale. The address space is small by carrier standards. The public summaries identify four IPv4 routes rather than a broad portfolio of allocations. The absence of visible IPv6 routing in common public summaries is a strategic weakness if it reflects actual customer service, because modern access networks increasingly need IPv6 readiness as address scarcity and application behaviour evolve.

The routing relationships also point to dependence. Public routing summaries and database records show import and export relationships involving Moldovan and regional networks, with Moldtelecom appearing in peer or upstream summaries. That is normal for a small operator. It still means the company does not control the whole chain between a Taraclia customer and the global internet. Transit, backhaul, regional handoff, equipment configuration and route stability all sit between the retail promise and the user experience.

Cloudflare Radar has estimated the customer population behind AS43783 in the low thousands in recent snapshots. That is a measurement estimate, not a subscriber count. It should not be treated as a financial disclosure. It does, however, fit the small-footprint picture. If the user base is indeed measured in a few thousand people rather than tens of thousands of accounts, the business has limited purchasing leverage and limited tolerance for duplicated cost.

The right conclusion is balanced. Number-resource evidence increases confidence that CAGHET-PLUS has real network-operating responsibility. It also reinforces the cash-flow test. Owning routing responsibility creates recurring duties: registry fees, contact accuracy, abuse response, routing-security hygiene, equipment maintenance, supplier negotiation and technical competence. Those duties are valuable only if the customer base pays enough for them. A small autonomous system can support local reliability. It cannot, by itself, create pricing power.

Price is a promise to absorb several costs

The visible retail price is the centre of the business model. CAGHET-PLUS advertises an internet plus television plan at 190 lei per month with speed up to 150 Mbps and a connection fee of 150 lei under a 36-month subscription term. It also lists a standard television subscription at 50 lei. The bundle says cable television is provided free when internet is connected. That reads like a household-retention offer: keep the account inside one local bill, avoid a separate television decision, and use the bundle to reduce churn.

The problem is that 190 lei has to pay for more than bandwidth. It has to cover transit and backhaul. It has to cover the access plant in streets and buildings. It has to cover customer-premises equipment, installation labour, repairs, power, office work, billing, payment fees, tax, bank handling, network monitoring, television rights or carriage arrangements, support calls, abuse complaints and bad debt. It has to leave enough surplus to replace equipment before failure forces emergency spending. If the company finances growth by long contracts and modest connection fees, the monthly account must still carry the future capital cycle.

The 36-month term is therefore not incidental. A long term can protect the provider from the installation-cost payback problem. If a new connection needs a field visit, cable, connectors, a router and administration, the operator cannot recover that cost from a small connection fee alone. A multi-year subscription gives the operator time to earn back the outlay. The customer, however, accepts that term only if the service remains competitive. A 150 Mbps maximum can be adequate for many households, but the Moldovan market has moved toward much higher advertised speeds.

Larger competitors make the price test harder. Orange advertises fiber plans where 500 Mbps and 940 Mbps options sit around the same broad price band, with promotional discounts. StarNet advertises 300 Mbps, 500 Mbps and 1,000 Mbps fiber options, with promotional monthly prices starting below or near CAGHET-PLUS's bundle level. Moldtelecom has promoted 300 Mbps, 500 Mbps and 1,000 Mbps options with aggressive first-year discounts and router inclusions. Coverage and availability vary, so these are not always direct local substitutes for every Taraclia address. But they shape expectations.

The customer learns that 150 Mbps is not premium in Moldova. The defence cannot simply be speed. It has to be the full promise: the connection works, television is included, the bill is predictable, local repair is faster, and the provider is known. If that promise holds, 190 lei may be reasonable. If repair response slips or support feels distant, the customer will compare the offer against faster national branding and ask why the local provider is not cheaper.

This is where revenue and value creation diverge. A bundle can hold revenue by keeping accounts attached. It creates value only if the additional television element reduces churn more than it increases content and support cost. Free television in a bundle is not free to the provider if it adds carriage obligations, equipment complexity or service complaints. The bundle is rational if it raises lifetime value. It is destructive if it hides margin erosion.

Reliability is a labour budget before it is a slogan

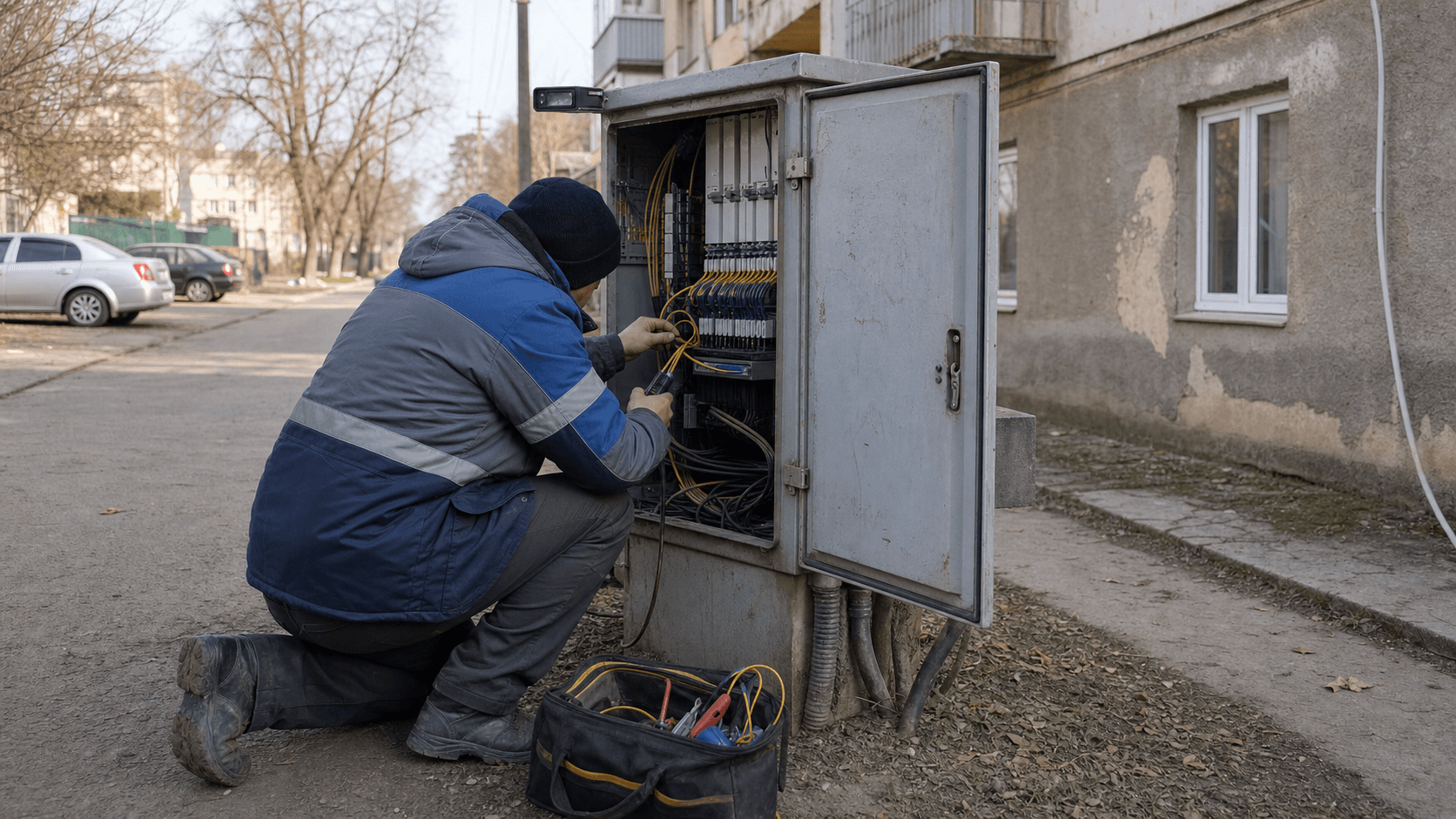

Reliability in a local access network is physical. It is not only latency, packet loss and routing tables. It is whether the drop cable is intact, whether connectors are sealed, whether power events are handled, whether a router replacement is available, whether a technician can reach a building, whether the office records the fault correctly, and whether repeat issues are fixed rather than postponed. For a small operator, reliability is a labour budget.

CAGHET-PLUS's own history mentions a cable-network modernisation toward fiber beginning in 2013. That was the right direction. Fiber is usually more future-proof than old coaxial plant, especially as streaming, video calls, cloud storage and multi-device households increase demand. But modernising once does not end the capital burden. Fiber networks still need splicing, cabinets, splitters, optical line terminals, power, route protection, testing tools and skilled repair. Customer routers age quickly. Wi-Fi complaints are often blamed on the provider even when the access line is sound.

The economics are awkward because the customer pays a flat monthly fee while usage grows. A household that streamed occasional video ten years ago may now have several devices, cloud backups, remote work, gaming and smart televisions. The access provider must add capacity in aggregation, backhaul and support even if the headline price does not rise. If usage growth is not matched by ARPU growth or lower unit cost, reliability becomes less profitable over time.

Small scale makes this harder. A large operator can operate a call centre, field-dispatch system, spare-device stock and monitoring team across hundreds of thousands of customers. A local operator may depend on a small team where the same people install, repair, answer calls and handle administration. That can be a strength when staff know the streets and customers. It is a weakness if illness, departure or overload removes key knowledge.

The visible third-party financial signals reinforce this point. A six-employee local operator cannot afford a deep bench. If sales income is around the scale shown on the commercial registry page, every technician hour matters. A truck roll to fix a low-priced account can consume a meaningful portion of monthly margin. A repeated fault in one building can turn a nominally profitable cluster into a drain. Abuse complaints, malware-infected customer devices or payment disputes are not glamorous, but they use staff time.

The test is whether the company has designed the offer around its labour reality. Long contracts help if they lower churn. Local office hours help if they route problems efficiently. A simple two-product offer helps if it reduces billing confusion. But the company still needs enough repair capacity to make the local-service promise credible. Customers forgive one outage more easily than repeated uncertainty. A local provider that cannot answer promptly loses the one advantage it has over a larger brand.

Moldova's market raises the performance floor

The broader Moldovan market is no longer an underbuilt broadband environment where any fixed line commands loyalty. Regulator data for 2025 reported 962.2 thousand fixed internet connections, up 7 percent, and fixed-internet household penetration of 83.6 percent. FTTx connections accounted for 97.3 percent of total fixed internet access connections. Paid television subscriptions were also close to 696.9 thousand. Total electronic communications revenue was reported at 6.64 billion lei, with sector investment of 1.48 billion lei.

Those numbers are good for demand but difficult for small operators. They show that fixed broadband is mainstream, fiber is the norm, and customers are used to bundles. The market is not waiting for a basic provider to introduce connectivity. It is comparing offers. In the first quarter of 2025, regulator data showed the largest fixed-broadband speed category as 100 to 500 Mbps, with a further large share in the 500 Mbps to 1 Gbps range. Connections below 30 Mbps had shrunk sharply. That raises the minimum acceptable experience for every operator.

The bundle context matters as well. Regulator data showed that most fixed-internet subscriptions included additional services, and that fixed internet plus IPTV was the most popular bundled pattern. CAGHET-PLUS's internet plus television offer fits this national behaviour. The bundle is not an oddity. It is a defensive requirement in a market where customers expect one provider to carry entertainment and access.

The danger is that the national market makes local offers look slow. A 150 Mbps plan can still meet many household needs, especially if actual performance is stable and upload is adequate. But customers increasingly evaluate value through advertised speed, router quality, television interface and promotional gifts. If larger providers keep marketing 500 Mbps or 1 Gbps near the same price band, local operators must either upgrade, discount or emphasize service. Each option has a cost.

Geography cuts both ways. Taraclia is not Chisinau. A national provider's headline offer may not be available at every address, and local plant may matter more than national advertising. The National Bureau of Statistics describes Taraclia district as relatively low density, while Taraclia city itself is modest in population. Low density reduces the attractiveness of overbuilding by multiple large players, but it also reduces the revenue base for the incumbent local operator.

The market therefore gives CAGHET-PLUS a narrow lane. It can survive if it is the practical provider for a defined local customer base and if its network quality is good enough that customers do not feel under-served. It will struggle if customers begin to view the offer as slower but not meaningfully cheaper, or local but not meaningfully more responsive. In a high-fiber market, nostalgia is not a strategy. The company has to convert local familiarity into measurable retention and lower support friction.

Supplier dependence is the hidden balance sheet

The customer sees one bill. The operator sees a chain of suppliers. Transit and upstream connectivity are the obvious ones. Public routing records show that CAGHET-PLUS sits behind other networks for reachability to the wider internet. That is normal. It also means supplier price, route quality, outage handling and commercial terms flow into the retail promise. If the upstream provider has an issue, the local customer still blames the local provider.

Backhaul is the next dependence. A Taraclia access operator needs capacity from the local network to regional or national points of interconnection. If it leases backhaul, it pays recurring fees and depends on another operator's repair priority. If it owns more of the path, it carries maintenance and capital cost. Either way, the price of reliability is not limited to the access line in the customer's building.

Television adds a different supplier risk. A cable or television bundle requires content, channel lineup management, equipment compatibility and customer support for a service whose perceived value can shift quickly. Streaming services and online video reduce the willingness to pay for traditional television, yet older or family households may still value a familiar package. The bundle can lower churn, but the operator must avoid letting television complexity eat the margin that internet access provides.

Customer equipment is another hidden balance-sheet item. Router expectations have risen. Customers now ask about whole-home Wi-Fi, multiple rooms, video stability and device compatibility. Larger operators advertise Wi-Fi 6, mesh devices or smart television promotions. A small provider can keep offers simple, but it cannot ignore in-home performance. Even when the problem is a cheap client device or thick wall, the complaint becomes a service issue.

Payment methods and collection also matter. CAGHET-PLUS's site points customers toward bank payment options. That lowers office cash handling but may add fees and reconciliation work. A small operator's cash flow can be sensitive to delays, missed payments and administrative effort. Long subscription terms help only if customers keep paying and if enforcement does not damage reputation.

Registry and technical governance are supplier-like obligations even when they are not ordinary suppliers. Maintaining number resources, routing records, abuse contacts and operational competence costs money and attention. If a small operator lets those tasks drift, it risks deliverability, security reputation, route acceptance and customer trust. If it keeps them current, it absorbs a fixed cost that must be spread over a small base.

This is why the cash-flow test is more demanding than a simple price comparison. A 190 lei account is not a gross margin line until supplier dependence is paid for. The company that understands this will price cautiously, upgrade selectively and avoid growth that adds fragile routes or distant customers without enough density. The company that treats every new account as pure revenue will eventually discover that support, suppliers and renewal capital have first claim on the cash.

Customer concentration is geographic before it is contractual

There is no public evidence that CAGHET-PLUS depends on one named enterprise customer, and the retail offer points toward households and small local accounts. Yet concentration risk can exist without a single large contract. In a small city, the customer base is geographically concentrated. A few apartment blocks, streets or neighbourhood clusters may carry a large share of revenue. A local competitor's upgrade in one area, a building access dispute or a cable cut can therefore affect a disproportionate part of the business.

Geographic concentration can be useful when the network is dense. If many customers sit on the same local plant, installation and repair cost per account can be low. A technician can handle multiple visits in one area. Word of mouth can reduce sales cost. Existing ducts, poles or building routes become valuable. But the same density creates vulnerability if plant quality is uneven or if a rival overbuilds the best clusters.

The customer mix also matters. A household account has different economics from a small business, public institution or hospitality location. Businesses may value uptime more and may accept a higher price for support, but they also need faster repair commitments and may switch if reliability affects revenue. Households are price sensitive but can be sticky if the service is familiar. Public institutions may require formal procurement and documentation that small teams find burdensome.

The company needs enough higher-value accounts to support the network, but not so much exposure to any one relationship that a lost account damages the cost base.

Churn is the silent metric. A long contract can delay churn, but it cannot remove dissatisfaction. If customers reach the end of a term and see faster alternatives, the provider must have given them reasons to stay. Local repair, predictable billing, a television bundle, personal familiarity and adequate speed can all help. But if the customer experience has been mediocre, the long term becomes a reason to leave at the first clean exit.

The company also faces demographic pressure. Taraclia city and district are not high-growth metropolitan markets. The 2024 census data show a small city and a national population context shaped by decline and migration. A local broadband operator cannot rely on a flood of new households. It has to increase value per account, defend share or expand carefully into nearby demand. That makes retention more important than headline subscriber wins.

The hardest accounts are those at the edge of the footprint. They may want service, but they require longer lines and more repair time. Serving them can be socially valuable and reputationally attractive, yet economically weak if pricing is the same as for dense urban clusters. A disciplined operator will know which extensions create durable cash flow and which are vanity. The public material does not reveal that internal map, so the outside judgment must remain conditional.

Competition is local, national and mobile

The competitive set has three layers. The first is local. Kompass listings for Taraclia show other communications-related providers in or near the area, including names associated with cable television and internet access. Such listings are not a complete competitive map, but they indicate that CAGHET-PLUS is not the only local connectivity option. Local rivals may have similar repair advantages and similar relationships with buildings.

The second layer is national fixed broadband. Moldtelecom, Orange and StarNet shape customer expectations even where coverage differs by address. Their advertised speeds and promotional bundles set the reference price. If a customer sees 300 Mbps, 500 Mbps or 1 Gbps marketed at or near 190 lei, a 150 Mbps local plan has to win on something other than raw speed. That could be availability, installation simplicity, bundled television, service response or trust. But the burden of proof sits with the smaller provider.

The third layer is mobile. Mobile data traffic has grown strongly in Moldova, and mobile offers can substitute for fixed service in some households. Mobile broadband is not a perfect replacement for a stable fixed line, especially for heavy streaming, remote work, gaming or multiple users. Still, a household under budget pressure may rely on smartphones if the fixed bill feels optional. That makes fixed broadband providers defend not only against each other but against the customer's decision to simplify spending.

Large providers have structural advantages. They can buy equipment at scale, spread marketing cost, absorb promotions, bundle mobile and fixed services, offer modern routers and support national advertising. They also have weaknesses. Their call centres can feel distant, local repair may be slower, and coverage may not reach every building with equal quality. A small provider's opportunity is to exploit those weaknesses, not to imitate every national promotion.

CAGHET-PLUS's 190 lei internet and television bundle therefore has to be read as a local competitive instrument. It is not the cheapest visible offer in the national market, nor the fastest. Its logic is a simple household package from a local provider. If the customer values a television add-on, local office familiarity and practical repair, the bundle can hold. If the customer values maximum speed and device promotions, the bundle is exposed.

The company should avoid a race it cannot win. Matching every speed tier from national providers would require capital and supplier capacity that may not earn back in a small base. Cutting price too far would weaken repair capacity and service quality. The better route is segmented discipline: keep a credible baseline offer, identify customers willing to pay for better reliability or business support, upgrade congested areas before they become churn centres, and make local service visibly superior.

Regulation and abuse handling consume scarce attention

Small size does not exempt an operator from sector obligations. Moldovan regulator pages describe statistical reporting duties for providers of public electronic communications networks and services. Separate regulator pages list providers that submitted quality-parameter reports in earlier periods, and CAGHET-PLUS appears in several historical lists. Those appearances do not prove present service quality by themselves, but they show the company was visible in the regulated reporting environment.

Reporting is not just paperwork. It requires accurate customer, service, technical and quality information. It also means someone inside the company has to understand deadlines, formats and regulator expectations. In a six-person business, that work competes with installations, repairs and customer support. A larger carrier spreads compliance over specialist teams; a local operator often relies on a small number of people.

Access rules, consumer-protection expectations and service-quality norms also influence the economics. Customers expect functioning service, transparent tariffs and complaint handling. A local provider that mishandles complaints can lose reputation quickly. A provider that over-serves every complaint without triage can lose margin. The balance is operationally hard: answer fast, diagnose well, avoid unnecessary visits, and still make the customer feel heard.

Abuse handling is another underpriced duty. Any access provider can receive reports tied to spam, malware, compromised devices, copyright complaints, scanning or other unwanted traffic. Even if the underlying issue sits with a customer's infected device, the operator must receive, triage and respond. The routing record and abuse contact make the company reachable to external parties. That is good governance, but it is also work.

Data locality and sovereignty enter the story through practical dependence rather than grand claims. A local access provider carries Moldovan customer traffic to global services that may host data abroad. Customers rely on cloud applications, messaging, video platforms, banking services and remote work systems. The operator does not control those services, but its reliability becomes the local access layer for them. If access fails, the customer's cloud dependency becomes a local network complaint.

Geopolitical and operational risk sit in the background. Moldova's connectivity depends on regional routes, supplier relationships, energy resilience and cross-border internet paths. A small Taraclia provider cannot diversify like a large carrier, but it can maintain sound routing, supplier options where feasible, spare equipment, power planning and clear customer communication. These are not glamorous investments. They decide whether the operator can keep trust during disruptions.

The regulatory and abuse burden supports the same conclusion as the cost analysis. A small operator needs enough gross margin to pay for non-revenue work. If pricing is too thin, compliance and abuse handling become deferred tasks. Deferred tasks eventually become service, reputation or regulatory risk. The customer may think the bill pays for speed. The operator knows it also pays for order.

Unofficial market signals have limited weight

Unofficial signals can help frame questions, but they should not be mistaken for proof. Proxy-list pages sometimes show individual IP addresses in CAGHET-PLUS space. Third-party routing pages estimate users, peers, routes or upstreams. Business directories classify the company and list services. Search results place the company alongside other local providers. These signals are useful because small operators often leave a light public footprint. They are not a substitute for audited accounts, subscriber disclosures, network maps or current regulator filings.

The proxy-list signal is especially limited. If an IP address from a provider appears in a proxy list, it may indicate a customer device, a misconfigured service, a resale arrangement or a transient measurement. It does not prove that the operator sells proxy services. It does not prove a security failure by the network. It does, however, remind investors that abuse handling is real. Small access networks are exposed to whatever customers connect behind them.

Commercial registry information is also a signal, not a full economic model. Visible data showing low sales, a net loss and a small staff for 2023 is important, but it may lag current performance and may not break out telecom-specific economics. The registered activity labels on such pages can be broad or stale. The right use is to ask whether the company has enough financial capacity to maintain network quality, not to treat one third-party page as the whole business.

Routing tools need similar caution. IPIP, IPGeolocation, IPinfo, CIDR Report and Cloudflare Radar each observe or present network facts from different methods. When they agree that AS43783 is small, Moldovan and IPv4-only in visible route summaries, that convergence is useful. When one estimates three thousand users and another older result suggests four thousand, the exact number should not be overread. The range tells us scale is modest.

Kompass and similar directories help identify local competitive texture, but they are not live coverage maps. A provider listed in Taraclia may not serve the same buildings or packages. A national tariff page may not apply to every local address. Therefore the fair competitive statement is not that every customer can instantly switch to every advertised plan. It is that advertised national offers shape what customers believe a fair broadband price should buy.

This restraint matters because the article's thesis is economic, not accusatory. The evidence does not support a claim that CAGHET-PLUS is failing, nor does it support a claim that it is a hidden high-growth asset. It supports a sharper question: can a small local operator turn proximity and responsibility into a durable enough cash margin in a market where the technical floor keeps rising?

Capital needs are not optional

The hardest fact about access networks is that yesterday's upgrade becomes today's baseline. CAGHET-PLUS's move toward fiber in 2013 may have been a material improvement at the time. More than a decade later, the market has shifted. A 100 Mbps improvement once looked modern; now regulator and provider data show Moldovan customers moving into 100 to 500 Mbps and 500 Mbps to 1 Gbps tiers. The investment cycle keeps moving.

Capital needs appear in three places. The first is access capacity: optical equipment, split ratios, distribution points, drops and customer devices. The second is aggregation and backhaul: the capacity between local customers and upstream handoff. The third is service systems: monitoring, billing, customer records, security, support tools and device replacement. A small operator can defer some spending for a while, especially if customers are tolerant, but congestion eventually becomes visible.

The temptation is to upgrade only when customers complain. That conserves cash in the short run and destroys trust in the long run. The better discipline is to identify where usage growth threatens service quality before customers churn. That does not require matching a national gigabit offer everywhere. It requires knowing which clusters need more capacity, which routers cause complaints, which upstream terms are too fragile and which customers would pay for a higher tier.

The company also has to consider IPv6. Public route summaries reviewed show no IPv6 routes for AS43783. If that reflects current service reality, it is not an immediate death sentence; many access networks still use IPv4 with translation or limited address strategies. But it is a future constraint. IPv4 scarcity, application behaviour and customer device growth make IPv6 readiness part of long-term network hygiene. A local operator that never invests in it may face avoidable complexity and reputational cost.

Capital allocation should therefore be conservative and visible in service results. Spend where it reduces repair visits, raises actual throughput, improves resilience or protects higher-value accounts. Avoid spending merely to advertise a headline speed that the revenue base cannot support. A small company can win by being dependable, but dependability needs renewed plant and working equipment.

This is also why a weak balance sheet would matter. If negative equity and losses persisted after 2023, renewal capital could be constrained. The company might then rely on supplier credit, customer prepayment, owner support or deferred maintenance. None of those is necessarily fatal, but each changes risk. The facts that would most improve confidence are recent financial statements showing positive operating cash flow, controlled debt, a clear upgrade plan and churn low enough to fund reinvestment.

What would change the judgment

The current judgment is conditional because several decisive facts are not public. The first is subscriber count by service. A few thousand users behind the network does not translate directly into paying accounts. The business case would look different if CAGHET-PLUS has a dense base of contracted households with low churn than if the active account base is small, aging or concentrated in low-margin television.

The second is current ARPU and gross margin. The visible 190 lei bundle is useful, but it does not reveal discounts, bad debt, content cost, supplier fees, router subsidies or support expense. A local provider can look cheap or expensive from the outside while earning a very different margin after all costs. The critical question is contribution per connected account after direct network, content and support costs.

The third is network quality. The public record shows service claims and historical reporting appearances, not current outage rates, latency, packet loss, repair times or customer satisfaction. Reliability is the product. Evidence of consistently fast repairs, low repeated faults and stable throughput would materially improve the view. Evidence of congestion, slow response or repeated service complaints would weaken it quickly.

The fourth is supplier diversification. If the company has one practical upstream and limited backhaul alternatives, reliability depends heavily on a supplier it does not control. If it has multiple upstream options, spare capacity and clear failover plans, its local promise is stronger. The public routing record hints at relationships but not commercial resilience.

The fifth is capital runway. A credible plan for speed upgrades, router replacement, IPv6, power resilience and monitoring would show that the operator understands where the market is going. A static 150 Mbps offer with no visible upgrade path would become less defensible each year as larger operators push higher speeds and better equipment.

The sixth is customer segmentation. If CAGHET-PLUS has local business customers, schools, shops or institutions paying for better service, the economics could be stronger than a pure household bundle suggests. If almost all accounts are low-priced residential bundles, the business is more exposed to promotion and churn. The article cannot assume either without evidence.

The final fact is owner commitment. Small operators often survive because owners accept modest returns, reinvest patiently and preserve local reputation. That can be an advantage over distant corporate decision-making. It can also hide underinvestment if the owner lacks capital. The difference shows up in network quality and renewal spending, not in slogans.

The judgment: local trust has to beat speed inflation

CAGHET-PLUS SRL is not a scale story. It is a local cash-flow story with a technical footprint. The company has public evidence of long operating history in Taraclia, a retail internet and television bundle, local contact points, historical regulator visibility, RIPE membership and AS43783 routing responsibility. Those facts support a real operating presence. They do not support claims of broad market power or national infrastructure depth.

The strongest argument for the company is proximity. In a small city, a provider that knows the buildings, answers locally and repairs quickly can hold accounts even when a national competitor advertises a faster plan. Customers do not live in tariff tables. They live with the actual connection in their flat, shop or office. If CAGHET-PLUS delivers stable service and practical support, its value can exceed its speed headline.

The weakest argument is the market's rising floor. Moldova's fixed broadband market is heavily fiber-based, bundled and increasingly oriented toward much higher speeds. Larger operators advertise routers, television, discounts and speeds that make a 150 Mbps bundle look ordinary. Customer expectations will not move backward. A local operator can avoid a reckless speed race, but it cannot ignore the direction of travel.

The investment view is therefore disciplined but cautious. CAGHET-PLUS can create value if it keeps its network dense, prices enough to fund repair and renewal, upgrades selectively, handles abuse and reporting competently, and turns local service into lower churn. It destroys value if it chases unprofitable growth, gives away television or installation without payback, underinvests in capacity, or lets supplier dependence define the customer experience.

The core economic question has a narrow answer. Yes, CAGHET-PLUS may be able to sell reliability, local repair and reachable support at a viable price, but only if customers in Taraclia experience those advantages clearly enough to accept a speed and brand trade-off. At 190 lei, there is not much room for waste. Every avoidable truck roll, every unpaid bill, every weak supplier term and every postponed upgrade competes with future reliability.

That makes the company worth tracking as a local network-economics case rather than a hidden national champion. The proof will not be a larger routing table or a louder advertisement. It will be recurring cash flow after support labour, supplier bills, repair work, compliance, abuse handling and renewal capital have all been paid. If the account still produces surplus after those costs, local trust has economic value. If it does not, the promise of reliability becomes a subsidy the company cannot afford.