Summary

- BELBIM is most useful to analyze through the record discipline behind Istanbulkart: stored value, card linkage, QR travel, subscription loading, top-up state, verified wallet accounts, support history and public-service continuity.

- Public app-store evidence from İstanbulkart Mobil shows a finance app operated by Belbim with QR public-transport use, Turkish-lira top-ups, subscription-pass loading, automatic top-up, emergency-limit features, card-to-card transfers, verified-account IBAN access, FAST transfers and İstanbulkart Plus payment use.

- The regulatory context is electronic money and payment services rather than ordinary consumer-app convenience; the Central Bank of the Republic of Turkiye maintains the electronic-money institution framework, while app-store records identify the seller as BELBIM ELEKTRONIK PARA VE ODEME HIZ.A.S.

- The unresolved questions are operational: whether account and transaction state stays synchronized across cards, mobile wallet, transport gates, banking rails, support channels and recovery processes, and whether storage, compute, migration and data-quality labor justify the stack over time.

The company boundary is a municipal payment record, not a generic wallet label

BELBIM ELEKTRONIK PARA VE ODEME HIZMETLERI AS sits in a different risk class from an ordinary city app. The existing BTW company page identifies the assigned entity as BELBIM ELEKTRONIK PARA VE ODEME HIZMETLERI AS and links it to the Istanbul mobility and payments context. The public evidence inspected for this article is narrow enough to be handled carefully: it supports BELBIM as the operator behind the İstanbulkart mobile account surface, but it does not expose the private databases, settlement engines, gate integrations, customer-support tools or recovery runbooks that would prove how the service behaves under every repeated journey.

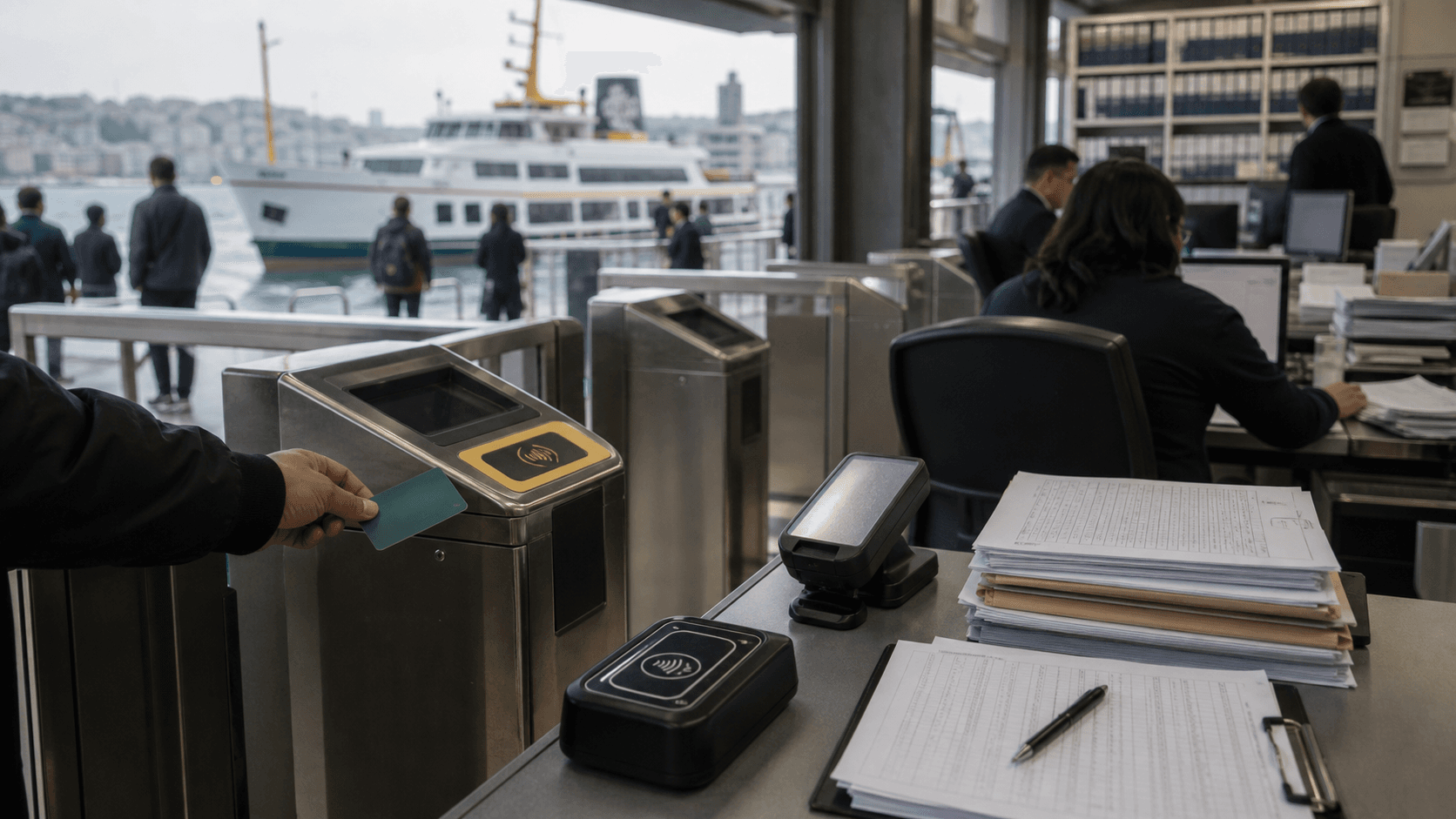

That distinction matters because Istanbulkart is not just a card-shaped convenience. The public app listing for İstanbulkart - Dijital Hesabım presents the service as a smart wallet tied to transportation in Istanbul. The same listing identifies the artist as Belbim and the seller as BELBIM ELEKTRONIK PARA VE ODEME HIZ.A.S. Its description says users can use QR codes for public transport rides, top up İstanbulkart with Turkish lira, load a subscription pass, configure automatic top-ups, activate an emergency-limit feature, transfer money between their own cards and cards of people close to them, upgrade to a verified account, receive an IBAN, make 24/7 FAST transfers, and use a digital account and Virtual İstanbulkart Plus for online shopping and transport payments. Those claims are enough to define the operating surface: account state, value state, card state, transport entitlement, bank-transfer capability, wallet capability and support state all have to meet in one record.

The Central Bank of the Republic of Turkiye's electronic-money institution page supplies the relevant regulatory frame. It is a page about electronic-money institutions, not a marketing page about transit convenience. That frame changes the interpretation of İstanbulkart Mobil. If the app were only a journey-planning tool, a poor interface would be frustrating but limited. If the app is also the account front end for electronic money, stored value, verified identity, card recovery, bank transfers and transport access, record accuracy becomes the product.

The core technical question is therefore not whether BELBIM has a recognizable brand. It is whether the system keeps data fresh, governed, queryable and recoverable under repeated use. Fresh means the customer, card, balance, pass, transfer and gate-use records do not drift from each other. Governed means there are clear rules for identity, access, privacy, retention, settlement, dispute handling and support actions. Queryable means support staff and operational teams can reconstruct what happened when a card, account, top-up or journey goes wrong.

Recoverable means a lost phone, changed device, failed top-up, disputed settlement or temporary outage does not leave the rider without a practical path back to service.

The public evidence can show why this is the right test. It cannot prove the private answer. No public source inspected here exposes BELBIM's data model, card-account matching logic, reconciliation jobs, settlement timing, uptime history, queue depth, app telemetry, incident logs, disaster recovery test results or customer-remediation metrics. A serious analysis should not invent those things. It should instead examine the records the public can see and ask what kind of operating system would be required for those records to behave consistently in the real city.

Istanbulkart turns a fare card into an account-state problem

The important shift in İstanbulkart Mobil is that transportation access is no longer only a physical card balance. The app-store description turns the card into an account graph. A user may have a physical İstanbulkart, a digital account, a Virtual İstanbulkart Plus, a verified status, one or more linked cards, automatic top-up rules, a subscription pass, an emergency-limit rule, an IBAN, bank-transfer capability and shopping use outside transit. Each of those features is public-facing. Each creates a private record that has to remain synchronized.

This is where municipal payment technology becomes harder than consumer wallet advertising suggests. A rider approaches a gate or validator expecting the system to know whether the card, QR code or digital wallet can pay. The answer may depend on a stored-value balance, subscription entitlement, account status, product type, age or eligibility category, device state, offline device behavior, pending top-up, chargeback, fraud rule or support action. The rider experiences the result as yes or no. The operator sees a chain of records that has to settle into a reliable truth.

Top-up is a good example. The app description says users can top up İstanbulkart with Turkish lira and load a subscription pass. A top-up is not complete merely because a payment attempt begins. The system has to receive the payment result, associate it with the correct account or card, update the available value, handle any delayed posting path, preserve an audit trail, expose the new state to the user, and make the result usable at the transport edge. A subscription-pass load has similar complexity.

The pass must attach to the correct product and account, start and expire under defined rules, interact with validators, and remain visible to support teams if a rider challenges a failed use.

QR public-transport use adds another layer. QR access makes the mobile account itself a travel credential. That raises the stakes for device changes, app login, connectivity, clock tolerance, session state, fraud controls and recovery. A plastic card can still be carried when a phone fails. A mobile QR journey depends on the account, app, device, credential generation and validator acceptance. If the QR layer works well, it reduces friction. If it fails during commute hours, the rider's problem is immediate and public.

Automatic top-up and emergency-limit features show that BELBIM is trying to reduce the classic public-transport failure of limited public evidence balance. That is a useful automation goal, but it also creates a more complex rule engine. The system has to know the threshold, funding source, card or account target, authorization result, timing, retry behavior, user notification and dispute path. Emergency-limit use also needs record discipline because it effectively moves a user through a transport moment when normal balance would otherwise be limited public evidence.

The public description does not disclose how the feature is implemented, so it should not be treated as proof of resilience. It is better treated as evidence that the operating problem is known: a city fare system must survive small balance failures without turning every ride into a support case.

Transfers between a user's own cards and the cards of people close to them widen the account graph again. A family or care relationship may rely on one person topping up another person's card. That sounds simple, but it requires clear ownership, authorization, anti-fraud controls, reversal rules and support evidence. If a transfer is sent to the wrong card, posted late, duplicated, blocked or misunderstood, the system needs a queryable event record. The article cannot establish how often that happens. It can establish that the feature creates a need for reliable record lineage.

The verified-account and IBAN claims are the strongest signs that İstanbulkart Mobil is not just fare media. The app listing says a verified account can obtain an IBAN and make 24/7 FAST transfers to any bank. That pushes the service into the territory of identity, regulated payments, bank-transfer reconciliation and customer due diligence. A transport pass can be anonymous or low-friction in some settings. A verified account with an IBAN cannot be treated that way. It must link user identity, wallet status, transfer eligibility, limits, transaction history, suspicious-activity controls, complaint handling and regulatory evidence.

That is why BELBIM should not be evaluated as if the only question were whether the app looks modern. The real system is a set of operating records behind repeated city movement. Cards, QR codes, top-ups, passes, bank transfers and support cases are all records. If they are accurate, the city experiences a smooth payment layer. If they drift, the failure lands at a gate, a call center, a service desk, a bank statement or a public complaint channel.

Electronic money changes the duty of care

The words in the company name are not decorative. BELBIM ELEKTRONIK PARA VE ODEME HIZMETLERI AS is explicitly an electronic money and payment services company. The app-store seller name reinforces that boundary. The Central Bank's electronic-money institution framework provides the proper regulatory context. That means the public technology question should include stored value, payment service continuity, customer identity, transaction records, safeguarding, dispute handling and privacy, not only app features.

Electronic money is operationally unforgiving because users treat value as a fact. A rider who tops up a card expects the balance to be available. A user who receives or sends value expects the account record to match the transaction record. A verified account holder expects identity and access controls to protect the account while still allowing legitimate recovery. A merchant or transport operator expects settlement evidence. A regulator expects the institution to explain what happened when a disputed transaction, outage, security event or customer complaint arises.

Those expectations all depend on data quality. A payment system can tolerate neither casual duplication nor casual disappearance. Every top-up, pass load, QR validation, card transfer, FAST transfer and wallet purchase needs enough event history to reconstruct its path. The event history has to distinguish pending from complete, authorized from settled, visible from usable, reversed from failed, and support-adjusted from system-generated. If the same rider sees one balance in the app and another at the transport edge, the issue is not only user experience. It is a state-consistency problem.

Public evidence does not show whether BELBIM's systems are event-sourced, batch-reconciled, real-time replicated, regionally distributed, outsourced, cloud-hosted, locally hosted or hybrid. It does not show transaction-processing latency, database technology, settlement windows, backup recovery time, incident response or fraud controls. Those limits are important. A public article should not pretend to inspect private architecture.

The right conclusion is more disciplined: the public product claims require a strong architecture, and the public sources available here do not let outsiders verify whether that architecture meets the stress of repeated use.

The most sensitive stress is the intersection of transport and money. A payment app can delay a user from online shopping and still be inconvenient. A transport payment record can delay movement through a station, bus, ferry or tram. That is why municipal service continuity has a different public meaning from ordinary finance-app reliability. Istanbul's transport system is a daily utility.

If account recovery slows down, if top-ups post late, if QR credentials fail, if subscription-pass state is wrong, if a device change blocks access, or if support cannot find the event record, the failure becomes part of the city's mobility friction.

That is also why electronic-money governance and public-sector continuity should be read together. BELBIM's operating burden is not only to make payments work in a commercial sense. It is to make a city service legible when payments do not work. A citizen or visitor needs to know where to go, which account is affected, whether a card can be recovered, whether a top-up is pending, what proof is needed, how a device can be re-linked, and how disputed value will be handled. Those are not marketing features. They are continuity features.

Market signals show where record drift becomes visible

The public market evidence is uneven but useful if handled with caution. The Apple lookup record for İstanbulkart Mobil showed version 6.1.0 with a current version release date of June 22, 2026, finance categorization, English and Turkish language support, and an average user rating of about 2.93 from 17,739 ratings at the time inspected. The Google Play page for com.belbim.istanbulkart exposed public review text and developer responses. Reviews are not a scientific outage sample and should not be treated as platform-wide measurements. They are still useful because they reveal the kinds of failures users notice when payment records meet support reality.

The repeated themes in the visible Google Play review material were registration difficulty, phone-number and identity constraints, device-change friction, card or top-up visibility problems, app crashes or blank states, bank-card confusion, and the need to contact ALO 153 for resolution. One visible developer response said a device-matching error required security verification and asked the user to call ALO 153 and follow IVR steps to update device information. Other responses directed users to ALO 153 or city support channels.

Those responses show a sensible security posture in one respect: device changes and account recovery should not be frictionless for a payment account. They also reveal the operational cost: if the recovery path is slow, unclear or call-center dependent, the burden moves from automation back to support labor.

The complaints from foreign visitors about phone-number or identification requirements are especially important because they show a product-boundary problem rather than just a bug report. A verified account with payment and bank-transfer functions needs stronger identity rules. A transport product used by visitors benefits from low-friction access. Those two requirements can conflict. If BELBIM optimizes for regulated account control, some casual users may find onboarding restrictive. If it optimizes for visitor convenience, it may weaken payment-account controls.

The public evidence does not show BELBIM's policy reasoning, but the market signal shows the tension that any city wallet has to manage.

Top-up and card-state complaints are even closer to the core thesis. A user who says money left a bank account but did not appear on a transport card may be describing a misunderstanding, a delayed posting path, a bank authorization hold, a failed reconciliation, an app display problem, or a genuine transaction failure. The public review alone cannot determine which. Yet the complaint category is exactly what a municipal payment operator must be ready to resolve quickly. The support team needs a trace that connects bank-card action, wallet account, card target, posting time, status, reversal path and user communication.

Without that trace, the user experiences a state mismatch and the operator experiences a manual investigation.

Blank screens, missing button text and registration loops are less directly about payment settlement, but they still matter because the app is the account front end. If a rider cannot register, cannot see the phone-number selector, cannot proceed after a device change, or cannot complete identity verification, the technical failure may block access to value management. In a simple content app, a blank screen is an interface defect. In a city payment wallet, it may become account-recovery friction.

The safest interpretation is that the app-store market evidence validates the known failure modes without quantifying their frequency. It supports concern about transaction-state mismatch, account-recovery delays, support bottlenecks, privacy and compliance burden, and public-service dependency. It does not establish outage rates, refund rates, failure rates, fraud levels or customer-service performance. A fair article should use reviews as directional evidence of where users feel pain, not as proof that the system fails at scale.

The same caution applies to ratings. A 2.93 average rating on Apple's record is a market signal, not an engineering measurement. It can reflect app stability, user expectations, tourist restrictions, language issues, identity rules, support frustration, old versions, recent updates or unrelated complaints. It cannot be converted into transaction reliability. Still, a low-to-moderate rating for a service tied to public mobility is operationally relevant because perception affects adoption.

If users do not trust the mobile account, they may stay with physical cards, kiosk top-ups or other workarounds, increasing the complexity of the overall payment environment.

Public-service continuity is the hard product

Municipal mobility payments have a continuity standard that ordinary commercial apps rarely face. A rider usually does not choose the payment system at the moment of use. The city has selected the fare medium, the transport operators have deployed the validators, and the public has built routines around the card or account. That means BELBIM's product is not only "payments." It is the payment continuity layer for repeated public movement.

Continuity has several dimensions. The first is validator continuity: gates, buses, metro stations, ferries and other transport points need to accept the correct credential. The second is account continuity: the user needs to access the correct card, digital account, pass and balance. The third is funding continuity: top-ups, automatic rules, emergency limits and transfers must behave predictably. The fourth is support continuity: a rider must have a path when the system says no.

The fifth is evidence continuity: BELBIM and public stakeholders need records that explain what happened without relying only on memory, screenshots or call-center improvisation.

The public app description is enough to show why this continuity burden is significant. QR public-transport use puts the phone into the ride path. Turkish-lira top-ups and subscription-pass loading place funding and entitlement management in the app. Verified accounts and IBAN/FAST capability create stronger identity and financial-service expectations. İstanbulkart Plus extends the payment surface beyond transit. Each feature may be rational on its own. Together they form a platform where a failure in one layer can spill into another.

An outage spillover can be subtle. A mobile login problem may not stop a physical card already loaded with value, but it can stop a user from topping up, seeing a balance, activating a subscription or recovering an account. A bank-transfer delay may not stop a ride immediately, but it can produce a support dispute. A validator issue may not be caused by the wallet but still land on the wallet brand. A device-matching rule may protect accounts but still strand a user who changed phones before commuting. Continuity analysis has to account for these indirect paths.

Public evidence does not disclose BELBIM's failover design, offline validator behavior, incident escalation process, customer-notification channels, support staffing, backup frequency, recovery objectives or settlement reconciliation windows. Without those details, it would be wrong to claim that BELBIM meets or misses a specific resilience threshold. What can be said is that the product surface demands resilience. The more account and payment features the app carries, the more continuity depends on accurate state transitions rather than merely available screens.

The strongest operational discipline is usually invisible to users. A well-designed system will preserve an event trail, reconcile with payment rails, expose a simple status to the user, give support staff a clear timeline, and prevent duplicate or contradictory corrections. It will also separate high-risk account changes from low-risk convenience actions. A device relink, verified-account recovery or IBAN-related issue should not be handled like a cosmetic preference. A basic balance display bug should not require the same identity burden as a regulated account recovery.

The public material does not show whether BELBIM makes those distinctions well. The distinctions are nevertheless the right way to judge the stack.

Public-sector continuity also includes communication. Users need plain explanations when a top-up is pending, a card is blocked, a device is unmatched, a phone number cannot be accepted, a verified-account step is required or a transport credential cannot be generated. A payment-record system can be technically accurate and still fail if the user cannot understand the status. The app-store review material suggests that some users experienced opaque errors or unclear registration paths. That does not prove systemic failure, but it shows why readable state is part of the product.

Data locality and governance are not side issues

Data-sovereignty and locality matter because BELBIM operates in a Turkish municipal and payment context. The service appears to handle personal account data, transport-use state, stored value, verification status, contact information, device state, bank-transfer capability and support interactions. Public evidence does not show where every dataset is hosted or how each processor relationship is structured. It does show that the service is not merely a static information page. It is a record-keeping environment tied to people, movement and money.

Data locality has two practical meanings here. The first is legal and regulatory: electronic-money and payment-service records need to remain available to the institution, regulator and customer under local requirements. The second is operational: records that drive city movement should be close enough, resilient enough and governable enough to support repeated use. A transit payment credential that depends on remote, opaque or poorly governed state can become fragile at the moment of need.

The public evidence does not justify a claim that BELBIM uses or avoids any specific cloud vendor, database platform or hosting architecture. That silence should be respected. The commercial question is still valid: do the storage, compute, migration, lock-in and data-quality costs beat the current stack? For a city payment operator, the answer cannot be based only on infrastructure price. It must include uptime, reconciliation, support load, regulatory evidence, privacy controls, auditability, data retention, disaster recovery and the cost of changing systems without corrupting account history.

Migration risk is especially high in a payment-record system. Moving from one stack to another may require preserving card identifiers, wallet accounts, transaction histories, subscription rules, support cases, device links, identity-verification records, bank-transfer references and dispute evidence. A migration that preserves balances but loses support lineage is not complete. A migration that preserves account login but breaks validator synchronization is not complete. A migration that lowers compute cost but increases manual reconciliation may be commercially worse.

Lock-in is also complicated. A regulated payment service may accept some lock-in if it gains reliability, security and supportability. It may reject a nominally flexible architecture if the practical burden of operating it is too high. The right metric is not ideology. It is whether BELBIM can keep records fresh and recoverable at city scale while maintaining compliance and controlling support workload. Public sources do not let outsiders calculate that cost. They do let outsiders identify the cost categories.

Privacy and compliance are part of the same equation. A verified wallet, IBAN access and FAST transfer capability mean that some users pass through stronger identity and financial-service flows. A city mobility product also touches location-adjacent behavior, even if the public evidence here does not expose detailed journey logs. Good governance has to manage who can see what, for what purpose, for how long, and under which support or legal process. The article cannot audit those controls. It can say that the service surface requires them.

What public evidence can and cannot establish

The public evidence can establish a clear product boundary. The Apple app record identifies İstanbulkart Mobil as a Belbim finance app and names BELBIM ELEKTRONIK PARA VE ODEME HIZ.A.S. as seller. It describes QR public-transport use, Turkish-lira top-ups, subscription-pass loading, automatic top-up, emergency limit, card-to-card transfers, verified accounts, IBAN issuance, 24/7 FAST transfers, a digital account, Virtual İstanbulkart Plus and broader shopping payment use. The Central Bank page establishes that electronic-money institutions are a regulated category in Turkiye. The BTW directory page supplies the assigned company identity.

The Google Play page and visible review material provide market-signal evidence about registration, support, device matching and top-up-state pain points.

The public evidence can also establish that direct product-performance testing is not available from these sources. The app-store descriptions do not disclose transaction success rates, settlement timing, uptime, support response, fraud controls, database design, validator integration, backup recovery, disaster drills, incident postmortems, queue volumes, refund rates or data-processing maps. The reviews do not prove platform-wide reliability. The regulator page does not reveal BELBIM's private operating metrics. The directory page is a boundary, not an audit.

That evidence limit is not a weakness in the article; it is the main analytical result. BELBIM's most consequential technology is precisely the part the public cannot directly inspect: the event history behind card/account/payment state. A reader can see the app promises. A user can see some support pain in reviews. A regulator can define the category. But the real discipline is the ability to answer, quickly and accurately, what happened to a given top-up, pass load, QR use, card transfer, verified-account change, device relink or disputed transaction.

The article therefore avoids claiming that BELBIM has or lacks a specific architecture. It does not claim a measured outage rate, app crash rate, fraud rate, customer count, transaction volume, validator latency, support response time or settlement speed. It also does not claim that app-store complaints represent all users. The fair conclusion is more modest and more useful: public evidence shows a system whose risk is record synchronization, and the public record is not deep enough to verify the private controls that would reduce that risk.

The commercial question is whether record quality pays for itself

The assigned commercial question asks whether storage, compute, migration, lock-in and data-quality labor beat the current stack. For BELBIM, that question should be translated into operational terms. The value of the stack is not only the cost per transaction or the price of compute. It is the cost of making a disputed city payment explainable. It is the cost of keeping top-ups, passes, QR credentials, wallet balances, bank transfers and support actions in one coherent record.

A cheaper stack that increases state mismatch can become expensive quickly. Every mismatch creates support work, public frustration and potential regulatory exposure. A user whose top-up is delayed may contact support. A user whose device cannot be relinked may call ALO 153. A user whose card transfer is unclear may need manual investigation. A visitor who cannot register may abandon the app and use a physical workaround. A support team that cannot query a complete event trail spends time reconstructing basic facts. That labor is part of the technology cost.

The reverse is also true. A stronger stack can be overbuilt if it adds complexity without reducing operational friction. If a migration creates vendor lock-in, opaque troubleshooting, slow change cycles or high specialist dependency, it may reduce infrastructure risk while increasing operating risk. BELBIM's optimal stack is therefore the one that makes the city payment record easier to trust and easier to repair, not necessarily the newest or most centralized stack.

The strongest commercial metric would be the cost per resolved state question. How much does it cost to prove whether a top-up posted, a pass loaded, a QR ride was accepted, a card transfer reached the target, a verified account was relinked correctly, or a disputed transaction was reversed? Public sources do not provide that metric. But it is the right metric because it joins technology and service continuity. Storage, compute and support labor are not separate categories in this system. They meet inside the evidence trail.

Data quality labor is sometimes treated as back-office drag. In a municipal payment system, it is public-service infrastructure. A clean card-account relation lowers recovery cost. A clean transaction history lowers dispute cost. A clean device-link history lowers fraud and lockout risk. A clean support timeline lowers repeat calls. A clean settlement record lowers reconciliation risk. If BELBIM can automate these records without losing traceability, the commercial case strengthens. If automation creates opaque states that require manual repair, the case weakens.

The operating standard is boring consistency

The practical standard for BELBIM is not a spectacular feature launch. It is boring consistency across repeated city use. A rider should not have to understand whether the relevant record is a wallet balance, a card balance, a pass entitlement, a payment authorization, a bank-transfer status, a device link or a support adjustment. The system should expose the correct next action and preserve enough evidence for the operator to explain the result. That is the difference between a payment app that looks modern and a payment record that can carry public mobility.

Boring consistency has to cover edge cases, not only normal use. A user may change phones, lose a card, top up just before a journey, try to help a family member, use a subscription product, attempt QR access with a weak connection, encounter a validator problem, or contest a bank-card charge. None of those cases is exotic in a large city. The visible app-store complaints show why these edge cases matter: registration, device matching, top-up visibility and identity constraints are exactly the points where the public can feel record uncertainty. The article does not treat those complaints as a measured failure rate.

It treats them as a map of where system design must be legible.

The best evidence design would give each actor a different but consistent view of the same event. The rider sees a clear status and next step. The support agent sees a timeline, not a guess. The payment team sees authorization, settlement and reversal state. The transport operator sees whether a ride credential was valid. The compliance team sees the identity and rule basis for a restricted action. The engineering team sees whether the problem is app display, account state, payment rail, card synchronization, validator acceptance or delayed posting. Public evidence does not show whether BELBIM has that design.

But the product surface requires something like it.

This is also why continuity cannot be separated from language, error design and customer communication. A technically correct state that is described poorly will still create support load. A device-security rule that protects an account but gives the user no usable recovery path will still feel like service failure. A delayed top-up that is eventually reconciled but invisible in the meantime will still damage trust. Payment-record quality therefore includes user-readable status, not only database accuracy.

For BELBIM, the strongest future signal would be more public evidence about recovery and explainability: clearer status language, explicit handling of pending top-ups, transparent device-change flows, accessible visitor options where regulation permits, and published service information that helps users understand when a payment record is pending, failed, posted or under review. Those would not reveal sensitive architecture. They would show that the operator understands the public-service burden of its own record system.

How to judge BELBIM

BELBIM should be judged through the discipline of the payment record. The public sources show a company and app surface that connect transport access, stored value, mobile wallet use, verified financial accounts, bank transfers, card transfers and support recovery. That is a significant technology role in Istanbul's mobility system. It is also a role where small state errors can become visible public-service failures.

The strongest public evidence is product-boundary evidence. The app-store record confirms the Belbim seller, the finance category and the feature set. The Central Bank page confirms the electronic-money institution context in Turkiye. The Google Play page supplies market signals about the kinds of user pain that arise when registration, device matching, top-up visibility or account recovery become difficult. The BTW directory page anchors the assigned company identity. Together, these sources support an analysis of BELBIM as a municipal payment-record operator rather than a generic payment-technology label.

The public evidence does not prove private reliability. It does not show transaction success rates, outage history, settlement design, card-gate synchronization, customer support speed, data-locality architecture, backup recovery or security controls. That gap should keep the analysis sober. A reader can say BELBIM's public product requires serious record discipline. A reader cannot say from public sources alone that every private workflow meets the standard.

The right watch points are clear: transaction-state mismatch, outage spillover, account-recovery delays, privacy and compliance burden, settlement disputes, support bottlenecks and public-service dependency. These are not abstract risks. They follow directly from the feature set. QR transit, automatic top-up, subscription passes, verified accounts, IBAN access, FAST transfers and İstanbulkart Plus all increase the number of records that must stay aligned.

BELBIM's future credibility will depend on whether it can make that alignment boring. The best city payment system is not the one that draws attention to itself. It is the one where a rider can move, top up, recover, transfer, verify and dispute without discovering the seams between card, account, bank rail, validator and support queue. Public evidence shows why that standard matters. The remaining question is whether BELBIM's private operating record meets it every day.