Summary

- Azimut-R Ltd.'s economic case rests on a narrow but real local bargain: the customer pays for a connection that can be installed, billed, repaired and explained by people close to the service area, while the operator absorbs the cost volatility of backhaul, field visits, compliance and customer loss.

- The visible network evidence points to a small Russian access provider with three originated IPv4 blocks, no visible IPv6 footprint in common routing datasets, and an upstream relationship that makes supplier dependence central to any judgment about resilience.

- The investable question is not whether Azimut-R can advertise faster tariffs, but whether its tariff ladder, support model and repair cadence can turn local trust into cash flow after equipment inflation, regulatory duties and competition from larger bundled providers.

The Incentive Before The Network

The useful way to read Azimut-R Ltd. is to start with the cash decision facing a household or small company in Pushkino: pay a local operator for a wire that should keep working, or take a substitute from a larger carrier, a mobile bundle, a building-level rival, or an older incumbent service. Reliability is not a slogan in that decision. It is a price paid every month in exchange for fewer interruptions, faster answers when the line fails, and a higher chance that the technician knows the road, cabinet, building manager, power issue or last repair that matters.

That gives Azimut-R a possible advantage, but also defines its ceiling. A local provider can be close to the customer, yet closeness is expensive. It needs office staff, support coverage, engineers who can travel, spares that sit on shelves, billing systems, abuse handling, regulatory compliance, optical equipment, routers, leases, poles, ducts, rooftops, power and upstream capacity. Every small outage is a service event; every truck roll can consume the margin from several low-priced subscribers. If the operator prices too high, customers compare it with national brands.

If it prices too low, it trains customers to expect a local repair service that the monthly fee cannot sustain.

The company therefore sits inside a classic access-network test: who pays, who benefits, and who carries downside? Customers benefit from a reachable local provider if service is actually maintained. The local economy benefits when homes, shops and offices have a functioning fixed connection. The upstream network benefits from aggregated local demand. Azimut-R carries the operational downside when a cable is cut, a settlement has low density, a supplier raises prices, equipment is hard to replace, or customers churn after a visible outage. Strategy without resource allocation would be marketing here.

The only strategy that matters is the one that decides where to build, where to repair, what speed to promise, what support hours to fund, and what price can pay for those choices.

Company Identity And Operating Boundary

The public record presents Azimut-R as a Russian limited liability company tied to Pushkino in Moscow Region. Its own company page says it was registered in January 2004, grew out of earlier activity under the Azimut name, became an operator after receiving communications licences, and provides internet access to individuals and legal entities. The same material places its service activity across more than ten localities in the Pushkinsky urban district.

That is a modest but meaningful boundary: it suggests a local access franchise rather than a national enterprise software firm, a cloud provider, a wholesale carrier, or a data-centre platform.

The company also appears in the RIPE NCC membership context as Azimut-R Ltd., with Russia listed as its service area and a Pushkino address. Its autonomous system is AS34975, commonly labelled AZIMUTR-AS. Routing datasets show a small routed footprint: three IPv4 prefixes and no visible IPv6 allocation in the datasets reviewed. The visible prefixes add up to 7,168 IPv4 addresses, or twenty-eight routed blocks at the common reporting unit.

That is enough address space for a local access provider, hosted customer devices, management ranges and legacy public addressing, but it is not evidence of a broad cloud, transit, hosting or registry business.

The operating boundary matters because it prevents exaggeration. Azimut-R may sell internet access, business connectivity and IP television-related services through its local site, but the available evidence does not support treating it as a carrier with large intercity reach or as an independent national backbone. Its public materials point to a local fixed-access provider with settlement-level commitments, customer support, payment points and service notices. That is still economically important. Local access networks are not glamorous assets, but they are the layer where broadband promises either meet a household wall socket or fail.

The directory evidence should therefore be read as number-resource and service-area evidence, not as proof of every possible product. RIPE membership and BGP origination show that Azimut-R holds or operates public number resources and participates in the routed internet. They do not prove how many active subscribers it has, how much of the network is fibre versus copper or wireless, how many kilometres of plant it controls, how many buildings are passed, how much traffic it carries at peak, or how its contracts allocate fault responsibility with suppliers and landlords. Those gaps are not minor.

They are the difference between a network that merely exists in registries and a business that can earn an acceptable return on local reliability.

What The Customer Is Buying

Azimut-R's site frames the offer around internet access, tariff plans, connection requests, support numbers, office payment options, personal-account payments and instructions for customer equipment. The customer-facing evidence is practical rather than visionary: how to connect, where to pay, how to configure PPPoE, how to use routers, how to reach support, and what the monthly plan costs. That practical tone is an asset if the customer problem is not discovery but continuity. Most households do not want a theory of broadband. They want the connection to work after a storm, a cable relocation, a billing issue or a router change.

The price list shows distinct economics for apartment households, private-sector households and business customers. For residents in multi-apartment buildings, the listed connection fee is zero and the consumer tariff ladder is low by international standards: 55 megabits for 500 rubles per month, 75 megabits for 600 rubles, and 100 megabits for 900 rubles. For private houses, the monthly prices are higher, with 40 megabits at 1,000 rubles, 60 megabits at 1,300 rubles and 100 megabits at 1,700 rubles. GPON plans for named cottage settlements run higher in speed and price, reaching one gigabit for 2,700 rubles.

For legal entities and individual entrepreneurs, the price step is much steeper, especially in standalone buildings, where the listed plans range from a low-speed business plan at 4,725 rubles including VAT to a 100 megabit plan at 26,250 rubles.

That tariff spread is the economic map of the business. Apartment customers are dense and price-sensitive. Private-sector customers require expensive last-mile work. GPON cottage customers may pay for speed and convenience if the build is already justified. Business customers may pay for uptime, support and documented service, but only if the provider can deliver a level of reliability that justifies the premium. The operator is not simply selling bandwidth. It is selling a different cost-to-serve proposition in each geography and customer class.

The details of connection pricing reinforce the point. A private house FTTH connection is listed at 5,000 rubles, while connection in apartment buildings is listed at zero. The difference is not a marketing oddity; it reflects the physical economics. Dense buildings allow the fixed cost of entry, cabling and switching to be shared across many potential subscribers. A private house connection can require a bespoke drop, field labour, site-specific obstacles and a longer payback. If the private-sector customer then churns quickly, the operator can be left with a stranded connection cost.

If the customer remains for years, the connection fee and higher monthly tariff may turn a difficult build into a reasonable local annuity.

Network-Resource Evidence And Its Limits

The routing evidence is compact. AS34975 is listed in public routing tools as active under RIPE, with three originated IPv4 prefixes: 95.129.56.0/21, 95.143.16.0/20 and 185.18.20.0/22. IPinfo, bgp.tools, BigDataCloud, IPIP and Hurricane Electric's BGP service broadly agree on the same shape: Azimut-R is a Russian ISP or eyeball network, originates a small number of IPv4 routes, and has no visible IPv6 footprint in those datasets. PeeringDB lists the network but does not show public exchange-point presence or disclosed traffic levels. IPinfo and other routing views show Flex Ltd. as the visible upstream relationship.

This evidence supports a local-access interpretation. An eyeball network with limited originated routes and one visible upstream is usually a business that aggregates end-user traffic and buys connectivity rather than a business that sells transit to many networks. The positive reading is that the operator has its own routing identity, public address space, route objects and operational continuity over many years. The cautious reading is that visible independence at the ASN level does not equal supplier diversity.

If Flex is the main upstream dependency, then reliability is partly a question of Flex's backhaul, peering, maintenance windows, commercial terms and incident response.

The absence of visible IPv6 matters as a strategic signal. A small provider can operate successfully with IPv4, NAT and customer equipment workarounds, especially in a market where legacy devices and tariffs remain common. But IPv6 absence reduces future flexibility. It can complicate customer-premise design, limit direct addressing, increase reliance on address sharing, and make the provider look less modern to technically sophisticated business customers. IPv6 is not automatically a revenue driver. It is closer to an option on future operating simplicity.

The longer a fixed-access provider delays it, the higher the later migration burden can become.

RPKI validity shown for the visible prefixes is a positive operational indicator, because route-origin validation reduces one class of routing error and can support cleaner interconnection. Yet RPKI is not the same as resilience. It tells us the route origin is authorised; it does not tell us whether local optical plant has redundancy, whether cabinets have backup power, whether the help desk answers at peak complaint hours, or whether the operator can source replacement hardware during sanctions pressure.

The net conclusion is narrow but useful: Azimut-R has enough public network evidence to be treated as a real local network operator, and too little evidence to be treated as a diversified infrastructure platform. For customers, that means the visible question is service continuity. For investors or strategic observers, it means the central variables are not address counts but churn, repair cost, supplier terms, capex discipline and price elasticity.

Revenue Growth Versus Value Creation

Revenue growth in this kind of business is not the same as value creation. A provider can raise revenue by adding low-margin customers in expensive-to-serve streets, discounting connection fees, selling higher headline speeds without upgrading congested links, or taking on business customers that demand costly service attention. Value is created only when the additional account earns a margin after install, support, upstream usage, equipment, billing, taxes, compliance, bad debt and future repair cost.

The official tariff table makes that distinction visible. A 500-ruble apartment plan can be attractive if the building is dense, the drop is short, the customer self-serves payment, and the network is not congested. The same price can be poor value for the operator if the customer requires repeated support, pays late, or sits behind a plant segment that needs heavy maintenance. A 26,250-ruble business plan looks far richer, but it may come with expectations for rapid repair, lower contention, dedicated routing help, contract paperwork and outage escalation. The headline price is only the starting point.

The published financial indicators available from Russian company-information services show a small business, not a high-margin software-like asset. Third-party business records point to annual revenue in the tens of millions of rubles, low reported net profit, modest headcount and a small-company status. These figures should be treated carefully because different aggregators may update at different times and may reflect official filings with a lag. Still, they are consistent with the economics of a local ISP: revenue can be stable, but net profit can be thin after payroll, repair, supplier costs and compliance.

The key pricing issue is whether Azimut-R can move customers up the tariff ladder without losing the very customers it needs for density. The market is saturated enough that most households already understand broadband as a commodity. Larger providers can bundle mobile, TV, streaming discounts or national-brand comfort. Local rivals can compete building by building. Mobile broadband can be a backup or substitute in some cases, although fixed access usually remains the better choice for heavy household use. That leaves Azimut-R with a value proposition based on locality, continuity and responsiveness.

It has to prove those benefits in service events, not in plan names.

This is why the company's news notices are economically important. Planned works on a central node, relocation of a trunk line, cable damage in Pravdinsky, office-schedule changes and support availability notices all show the underlying business reality: network reliability is produced by maintenance, not wished into being. Customers see the maintenance as inconvenience; the operator sees it as cost prevention. Good communication can reduce churn, but it cannot eliminate the cash cost of field work.

The Residential Price Floor

The residential price floor is the harshest part of the model. At 500 to 900 rubles per month for apartment plans, there is not much room for repeated service failure. Suppose a customer at the lower tariff pays 6,000 rubles a year. From that must come upstream capacity, local switching and optical depreciation, support, payment processing, taxes, bad debt, network operations, premises, staff and the occasional repair. One avoidable truck roll can consume a large share of annual gross contribution from that customer.

A building fault affecting dozens of customers can justify the visit, but a single-home complaint can be economically painful unless triage is strong.

Private-sector tariffs create a different calculation. The higher monthly prices and connection fee are necessary because the access line is less dense. But a higher price also invites comparison with mobile broadband, national fixed offers, or a neighbour's recommendation. For private houses, the customer is paying not just for speed but for the right to call someone local when a drop line, pole, optic, router or payment issue arises. If the repair experience is strong, the price can hold. If the repair experience is weak, the customer will treat the tariff as overpriced bandwidth.

The GPON tariff ladder for named cottage settlements suggests an attempt to create a higher-speed product where network design and customer density allow it. Gigabit marketing can be useful, but it also changes expectations. A customer paying for 300, 500 or 1,000 megabits will judge congestion, Wi-Fi guidance, router performance and content access differently from a customer on a 55 megabit plan. Some complaints that look like access-network faults are really home-router or Wi-Fi problems. A local provider still has to absorb the conversation. That raises support cost even when the network core is working.

The residential business therefore has one strategic job: preserve density while moving enough customers to higher contribution levels to fund maintenance. That can be done through speed upgrades, payment convenience, better fault communication, bundled IP television, business cross-sell, or improved service in private settlements. It cannot be done sustainably through discounts alone. A local ISP that competes only on cheap monthly price will eventually underfund the very repairs that made customers choose a local provider.

Business Customers And The Premium Test

Business access is where the economics should improve, but only if the provider can defend the premium. Azimut-R's listed business tariffs are much higher than residential tariffs, especially for standalone buildings. The implied logic is sound: business customers impose higher installation cost, value downtime differently, need invoices and predictable service, and may sit in locations where network entry is bespoke. A small shop, office, warehouse or institution does not buy broadband in the same way a household buys broadband. It buys a working day.

The difficulty is that business customers also have realistic substitutes. A national provider may offer a familiar contract and a clearer escalation path. A mobile operator may offer backup connectivity. A landlord may already have a preferred building provider. A systems integrator may bundle connectivity with equipment. The local provider can win when it has plant nearby, can install quickly, can explain the local constraints honestly, and can repair faster than a remote provider. It loses when the customer wants a national service-level brand, multi-site terms, cyber services, cloud bundles or procurement comfort.

For Azimut-R, the strongest business case is likely not pure speed. It is local accountability. A legal entity paying thousands of rubles per month needs to believe that the provider knows which cabinet, street and upstream matter. But accountability costs money. Business support cannot simply be the same queue as household support if the company wants premium pricing to hold. It needs a credible answer for outages, a method for prioritising business faults, and enough margin to fund spares and staff.

The published tariffs give the company room to earn better contribution from business customers, but the data available publicly does not show the mix between household and business revenue. That mix would change the judgment. A customer base dominated by low-priced residential plans creates one kind of risk. A customer base with a meaningful share of sticky small-business accounts creates another. The latter can fund resilience, but it also increases downside from outages because business customers are less forgiving when work stops.

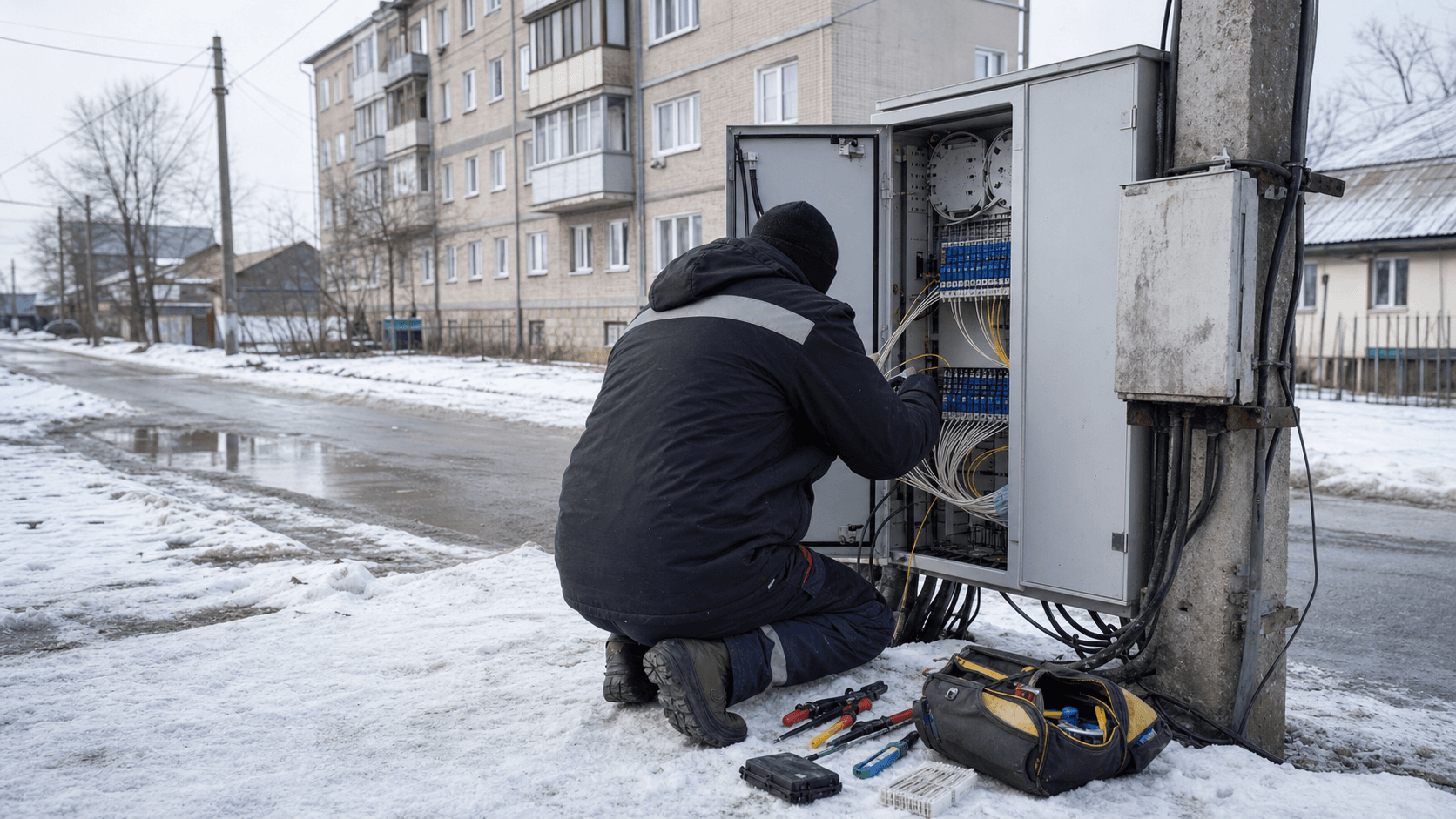

Capital Needs And Repair Reality

Azimut-R's public notices show a network that needs recurring work: planned activity at nodes, a trunk-line relocation in Tsernskoye, work at a central node in Pushkino, and a damaged trunk cable in Pravdinsky. That is not evidence of poor management by itself. All access networks need maintenance, and transparent notices can be a sign of an operator dealing with local physical reality. The business issue is whether those events are budgeted as normal cost or treated as occasional surprises.

Fixed access has a deceptively stable revenue line. Subscribers pay every month, and the network can run for long periods without dramatic change. But the cost base is lumpy. A cable cut, a failed active device, a power problem, a building access dispute, a tariff migration, or a supplier maintenance window can create sudden expense. If the provider underinvests, faults accumulate and churn rises. If it overbuilds, capital sits underused. If it upgrades too slowly, speed promises fall behind. If it upgrades too quickly, depreciation outruns revenue.

The best local ISPs manage capex with strong geographic discipline. They know which streets have enough demand, which buildings are worth entering, which private-house drops will pay back, and which settlements require a premium tariff. They avoid heroic expansion into areas where incumbents already have dense coverage and customers will not pay a local premium. They also maintain a clear replacement plan for ageing switching and optical gear. Sanctions and equipment availability make that discipline harder, because replacement cycles can lengthen, vendor options can narrow, and grey-market or unfamiliar equipment can increase support risk.

Azimut-R's tariff structure hints at that discipline by separating apartments, private houses, GPON cottage areas and business premises. But the public evidence cannot confirm whether actual capital allocation follows the same logic. The decisive evidence would be churn by area, fault rates by plant segment, payback on private-house installs, average revenue per account, and the proportion of support contacts solved without a field visit.

Supplier Dependence And The Flex Question

Supplier dependence is the strategic hinge. Azimut-R's own company history describes an early relationship with Flex, and routing datasets show Flex Ltd. as the visible upstream. If that relationship is stable, commercially fair and technically reliable, it may be a strength. A small operator does not necessarily need many upstreams if a regional partner provides good backhaul, peering and support. Concentration can reduce complexity and strengthen coordination.

But concentration also shifts bargaining power. If a local ISP depends heavily on one upstream for reachability, then its customer promise partly rests on another company's network, prices and maintenance decisions. The local customer may blame Azimut-R for a fault even when the upstream segment is at issue. The operator still owns the customer relationship. That means supplier resilience has to be bought, negotiated or engineered, not assumed.

The public routing view does not show meaningful upstream diversity. That does not prove there is no backup path at the physical or commercial level, but it does mean the conservative conclusion should treat upstream dependence as a material risk. It affects reliability, negotiation, capacity planning, outage attribution and strategic freedom. If Flex changes terms, suffers congestion, restructures routes, or prioritises its own retail economics, Azimut-R may have limited immediate alternatives unless it has prebuilt redundancy.

The Flex relationship may also shape capital choices. If Azimut-R can rely on Flex for backbone scale, it can concentrate on access, support and billing. That is a sensible division of labour for a local operator. The danger is that the company may then have too little independent leverage to capture the full value of customer loyalty. In a local ISP, the customer relationship is the scarce asset. If the upstream owns too much of the economics, the access provider becomes a service desk and last-mile maintenance arm with limited upside.

Competition And Substitutes

Pushkino is not an empty market. Local directories and provider listings identify multiple internet and telecom options, including local names such as Beirel Telecom, Pushkino-Telecom, Delta Svyaz Service and others, as well as larger national operators visible in consumer tariff aggregators. That matters because Azimut-R cannot set price as a monopolist across the area. It must compete street by street, building by building and settlement by settlement.

The substitutes are not identical. A national operator can bring brand recognition, bundle economics and potentially broader support systems. A local rival can bring similar proximity and perhaps stronger coverage in a specific neighbourhood. Cable television operators can use existing building relationships. Mobile operators can serve renters, temporary users and households that do not want a fixed install, although fixed access remains better for heavy video, gaming, remote work and multi-device households.

For some customers, the best substitute is not another provider but patience: delay switching because the current provider is familiar enough and changing is inconvenient.

Azimut-R's defensible position is therefore local trust plus acceptable price. Trust comes from answering phones, issuing timely notices, repairing faults, offering payment channels and not surprising customers. Price discipline comes from knowing where the company has a true service edge and where it is merely one provider among many. A 500-ruble apartment plan cannot carry a high-touch service model by itself. A higher private-sector or business plan can, but only when the customer values the service enough to stay.

The old forum and review signals show both sides of the market. Some customers complain about speed, support or outages. Others describe long tenure, acceptable reliability and quick repairs. That mix is normal for a local ISP and should not be overread as statistically representative. It is useful as a market signal: the brand is judged less by abstract capability than by whether it solves the last problem. A local provider can survive mixed reviews if its coverage area contains enough customers who believe the alternative is no better. It struggles when the alternative is clearly cheaper, faster and equally responsive.

Regulation, Data Duties And Geopolitical Cost

Russian telecom regulation adds another layer of cost and constraint. Communications providers operate under licences and must comply with data-retention, lawful-access and network-control obligations. Public legal and policy sources describe the burden of data storage, SORM-related duties, sovereign-internet technical requirements and the financial pressure these place on providers. The exact cost for Azimut-R is not visible, but the direction is clear: compliance is not optional and is not free.

For a large operator, compliance cost can be spread across millions of customers. For a small local access provider, the same category of obligation can be proportionally heavier. Hardware, storage, integration, reporting, legal administration and technical coordination all compete with spending on access upgrades and repair. Regulation can therefore favour scale even when customers prefer local support. It can make the market less friendly to small independent providers without formally banning them.

Geopolitics compounds the issue. Analyses of Russia's telecom equipment environment point to sanctions pressure, the departure of some Western vendors, substitution efforts, parallel supply routes and increased equipment cost. For a local ISP, this is not an abstract policy debate. It affects router availability, optical line terminal choices, spares, firmware confidence, warranty support and the price of contractor work. If equipment costs rise faster than household tariffs, the operator faces a squeeze. If it passes the cost through too quickly, customers compare offers. If it delays replacement, outage risk rises.

Regulation also changes customer expectations around data locality and service continuity. Households may not choose a local ISP for data-sovereignty reasons, but businesses may care that connectivity and billing sit within Russian operational constraints. At the same time, cross-border connectivity remains vital because much of the economic value of an internet connection comes from reaching services beyond the region. A local ISP must therefore satisfy domestic rules while preserving practical reach to global services. That balance is mostly invisible to the household until something breaks.

Market Context And The Broadband Ceiling

The broader Russian fixed-broadband market is mature enough that growth is harder than first connection. Government and market sources describe high broadband availability, a large fixed and mobile internet-access market, and continued investment needs for quality and resilience. MTS's public reporting for 2024 described a saturated fixed-broadband environment, rising fixed-line ARPU and ongoing cost pressure from sanctions, inflation, equipment and contractor services. BusinesStat reporting cited by RBC points to continued fixed-broadband market growth in value terms in 2025.

Those trends are helpful for revenue, but they do not guarantee margin.

For Azimut-R, market maturity means share-taking and upgrading matter more than basic adoption. Most households that want fixed internet likely already have some option. The company has to win a switch, defend an existing customer, connect a newly built home, or persuade a user that higher speed or better service justifies a higher monthly fee. Value creation becomes operational, not demographic.

The ceiling is also shaped by population density and local construction. Pushkino and the surrounding settlements include apartment buildings, private homes and cottage areas. Each format has a different payback. Apartment buildings reward penetration. Private homes reward careful route planning and connection fees. Cottage settlements can support GPON if take-up is high enough and the build is controlled. A local provider that mistakes one format for another destroys margin. It cannot price a sparse build like a dense building, and it cannot support a demanding business customer like a low-price household.

The opportunity is that remote work, streaming, cloud dependency, smart televisions and payment digitisation make fixed broadband more central to household life. Even when mobile data is good, a stable home connection has value. The risk is that the customer sees broadband as generic until it fails, then expects a local human response without wanting to pay the full local cost.

Unofficial Market Signals

Unofficial signals should be handled carefully. Customer reviews, local forum posts and consumer speed-test pages are not audited operating data. They can be biased, stale, emotional or unrepresentative. But they still reveal what customers notice. In Azimut-R's case, the public review mix includes complaints about weak speed or support, praise for long-term stability and quick equipment repair, and remarks that faults in private-sector networks can be typical but tolerable if fixed quickly. The old local forum material also shows that users historically compared Azimut-R with other Pushkino-area providers on speed, price and peering.

The economic meaning is not that every complaint is true. It is that the brand promise is tested at the exact point where the cost base hurts: outage response. A customer does not care whether a fault comes from a central node, a trunk cable, an upstream window, a router, a local drop or Wi-Fi inside the flat. The customer pays Azimut-R and wants an answer. The provider has to sort the fault at the lowest possible cost while preserving enough goodwill to keep the account.

The company's own notices provide a better-quality market signal than anonymous reviews because they show recurring operational communication. Notices about planned work, technical work, support availability and office hours show an operator that uses its site as a customer channel. That is valuable only if the notices are timely and matched by action. A notice without repair is just a complaint accelerant. A notice with a credible restoration window can reduce call volume and churn.

Unofficial signals also point to an old strength of local ISPs: community memory. Customers remember whether technicians came, whether the office solved a payment issue, whether a neighbour's connection improved, and whether the provider warned about works. National brands can advertise scale. Local providers trade on remembered incidents. That asset is fragile. It is built slowly and lost quickly.

What Would Change The Judgment

Several facts would materially change the view of Azimut-R. The first is subscriber mix. If the company has a large share of loyal business and high-speed private-sector accounts, its cash-flow quality is stronger than the low-end residential tariffs imply. If the base is dominated by low-price apartment accounts with high churn, the margin picture is weaker.

The second is network redundancy. Evidence of multiple upstreams, physically diverse backhaul, backup power at key nodes and a documented IPv6 plan would improve the resilience assessment. A single visible upstream does not doom the business, but diversity would make the local reliability promise more credible.

The third is fault economics. Public notices show maintenance events, but they do not show frequency per subscriber, mean time to repair, repeat faults, or how many support contacts are solved remotely. Those numbers determine whether local service is a margin advantage or a margin drain.

The fourth is capex discipline. A local provider can create value by building only where it can earn density or premium pricing. It can destroy value by chasing coverage vanity. Evidence of careful settlement-level expansion, measured take-up and targeted GPON deployment would support the business case.

The fifth is regulatory and equipment cost pass-through. If Azimut-R can raise tariffs gradually without elevated churn, it can preserve repair capacity. If customers resist increases, compliance and equipment inflation will pressure service quality. The January 2026 notice moving an older tariff into archive and raising the archived monthly fee is a small example of this broader need: old prices eventually have to meet current costs.

The sixth is customer concentration. A few business customers can improve revenue quality, but excessive dependence on one institution, landlord or settlement can increase risk. Local networks often appear diversified because they have many subscriber accounts, yet a single building manager, upstream contract or municipal works event can affect many accounts at once.

The Strategic Judgment

Azimut-R's strategic position is real but narrow. It appears to be a local access provider with a long operating history, a Pushkino-area service boundary, active public number resources and a practical tariff set. Its public materials show the ordinary machinery of a local ISP: connection requests, payment channels, support numbers, office hours, customer-equipment instructions, IP television features, tariff notices and service-work announcements. That machinery is exactly where value is made or lost.

The company should not be judged by the standards of a national carrier or cloud platform. It should be judged by whether it can convert local knowledge into lower churn and adequate margins. The strongest case is that Azimut-R knows its service area, has customers who value local support, can segment tariffs by build cost, and has operated long enough to maintain number resources and a recognisable brand. The weakest case is that the company is small, faces price pressure, appears dependent on a visible upstream, lacks a visible IPv6 posture, and must carry regulatory and equipment-cost burdens that favour larger operators.

The cash-flow test is therefore unforgiving. Reliability is valuable only if somebody pays for it. A household paying 500 rubles per month cannot finance unlimited field work. A private-house customer paying 1,700 rubles can finance more, but expects the difference to show up in service. A business customer paying many thousands can improve margin, but demands priority. The operator has to match service promise to tariff reality.

For Elias Ward's economic question, the answer is conditional. Azimut-R can sell reliability, local repair and reachable support at a price that covers transit, backhaul, field work, abuse handling and churn only where it keeps the build local, the customer mix disciplined and the support model efficient. It cannot rely on generic broadband demand to do that work. It has to earn the premium through visible maintenance, honest communication, supplier resilience and selective investment.

The strategic signal to watch is not a new slogan or a headline speed tier. It is whether the company keeps moving old tariffs toward current cost, expands only where the physical payback makes sense, adds resilience to the upstream and addressing posture, and uses local service events to prove that a smaller provider can be worth paying for. If those things happen, Azimut-R remains a durable local network business. If they do not, it becomes another small access operator squeezed between national bundles, supplier dependence and customers who want local accountability at commodity prices.