Summary

- AX Internet qualifies for the regional ISP category because public evidence shows customer-facing fixed internet service under the Fibrazo brand, an Argentine VA-ISP licence, Corrientes coverage and plan pages, a customer contract, and current AS271949 route evidence.

- The interesting economic unit is not a normal monthly broadband subscription. It is a prepaid residential fibre account that can be recharged for 7, 15 or 30 days in Argentina, and in Colombia-facing Fibrazo material for periods as short as one day.

- The retention question is whether a household that buys access in small time blocks will keep treating the line as essential after installation, service faults, inflation, mobile substitutes, larger fixed providers and neighbourhood alternatives test the value of the connection.

The household decision

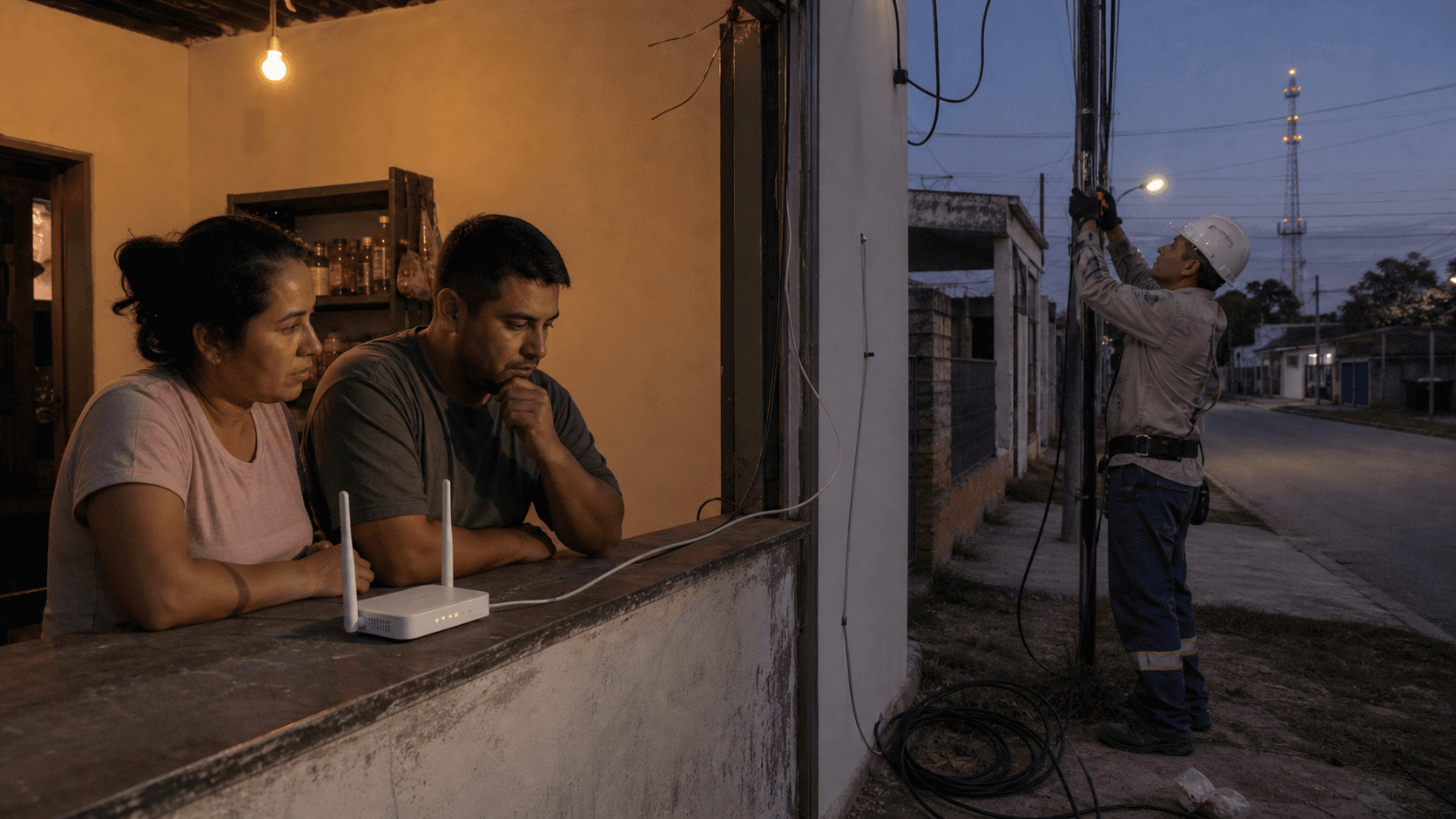

The relevant Fibrazo sale starts with a small domestic calculation. A household in Corrientes has a child who needs school access, an adult who sells through WhatsApp, a television that can stream only when the connection is stable, and an income rhythm that does not arrive neatly on the first day of the month. The household may be able to pay for internet this week but not want a permanent bill that turns into debt next month. A microbusiness faces a similar trade-off.

A kiosk, hairdresser, repair shop or home seller may need enough upload speed to answer customers and update catalogues, but may not trust a fixed contract if cash comes in daily.

AX Internet's Fibrazo brand is built around that hesitation. Its Argentine site describes itself as home internet paid by the day. The plan page offers recharges for 7, 15 and 30 days, presents a lower tier labelled 40MB and a higher Planazo tier labelled 300MB, and lists current Argentine peso prices for each validity period. The coverage page asks the user to choose Corrientes and directs uncovered users to a WhatsApp contact. The same site says there is no contract, no installation charge and no data running out.

Those claims are marketing claims, not measured network performance, but they define the product promise: an installed fixed connection with prepaid billing and household control over when to buy more days.

That promise is more subtle than cheap internet. A cheap monthly plan still asks for a monthly budget, a collection relationship and a penalty logic if the customer cannot pay. A mobile data package gives the user control over spend, but it usually turns the connection into a scarce resource. People ration video calls, uploads, homework and streaming because each gigabyte matters. Fibrazo is trying to combine the two behaviours: the fixed-line experience of a home connection with the spend control of prepaid mobile.

In low-income neighbourhoods, the difference can decide whether internet becomes a shared household utility or remains a phone-by-phone expense.

The retention test begins after the cable is installed. A pay-by-day account is easy to pause. That is attractive for a customer, but dangerous for the operator. If the customer does not see the connection as reliable, useful and easy to repair, the same flexibility that removes fear also removes lock-in. The company must earn repeated recharges without leaning on long contracts. Every outage, slow support response or awkward payment step can become a churn event. In a normal broadband account the operator may see churn when the customer formally cancels.

In Fibrazo's design, churn can look like silence: the customer simply stops recharging.

What AX Internet sells

The public record supports a real access business rather than a dormant registry footprint. AX Internet S.A. appears in ENACOM's licensee workbook as a VA-ISP, or value-added internet service provider, with CUIT 30-71695609-8, resolution 693 ENACOM/2021, and an address in Corrientes. The same CUIT and address appear in the public customer contract hosted on Fibrazo's Argentine website. The contract names AX Internet S.A.

as the provider of an internet access service and describes the service as prepaid packages of data used through equipment delivered in comodato, a loan-for-use arrangement common in telecom customer premises equipment.

The product surface is consistent across pages. The Argentine plan page advertises 7-day, 15-day and 30-day options. At the time reviewed, the lower tier showed ARS 5,227 for 7 days, ARS 11,200 for 15 days and ARS 22,400 for 30 days. The Planazo tier showed ARS 5,740, ARS 12,300 and ARS 24,600 for the same durations. The most important signal is not the absolute price, because Argentine prices move quickly. It is the shape of the price table: the customer is not being pushed into a single month. The account is deliberately sold in small blocks.

The contract is more formal than the homepage, and it gives a more useful view of operating risk. It says AX Internet may modify general conditions with 30 days' notice. It says customers must return loaned equipment after service ends or face billing for it. It says service at a new address depends on technical availability. It says the customer must allow identified personnel to access the location for inspection and maintenance when equipment is installed.

It also says the customer-service centre receives claims Monday to Friday from 9 to 18 and Saturday from 9 to 13 through the 3794662424 line, with target response times of three business days for service deficiencies or interruption, five business days for billing claims and ten business days for other claims.

Those terms show why prepaid fibre is not simply software-like recurring revenue. The operator still owns or controls physical equipment. It still needs field access. It still carries installation, maintenance, collection, customer education and regulatory obligations. The prepaid unit may reduce bad debt, because service can stop when the customer does not recharge, but it does not remove the need to build a local operating base. The company has to finance the customer connection before knowing whether that home will buy enough days to repay the installation, support and upstream costs.

There is one clear public inconsistency to watch. Fibrazo's Argentine marketing says installation is free, while the contract template says the customer will pay any connection charge described in the service request. The two statements can be reconciled if the current commercial offer waives the charge or if the contract preserves a right for other plans, but a reader should not assume that every customer in every period faces zero upfront installation cost. For a product built around distrust of contracts, the practical clarity of that point matters.

Why the prepaid unit matters

The daily or weekly unit changes the economics of trust. A fibre operator normally wants a stable monthly subscription because the access network has high fixed costs. A cable must pass the home. A drop must connect the home. Customer premises equipment must be installed, tracked and recovered. A support team must answer faults whether the customer is on day one or day twenty-nine. A prepaid account breaks the revenue into smaller pieces, so the operator needs frequent renewals and dense neighbourhood penetration to recover the same costs.

Fibrazo's investor descriptions explain why the company accepts that harder revenue pattern. Mercy Corps Ventures described Fibrazo as a startup focused on low-income urban settlements in Latin America, offering low-cost fibre internet through a pay-as-you-go design. The investor's write-up says Fibrazo identifies peripheral neighbourhoods without good fixed internet, works with internet companies to extend fibre to a point in the neighbourhood, then performs the last-mile connection and uses free trials to convert homes into paying customers.

New Ventures Capital similarly describes Fibrazo as providing last-mile fibre optic internet and infrastructure to underserved barrios in Argentina and Colombia.

That is a neighbourhood-density thesis. The company is not trying to win one apartment in a wealthy building where the incumbent can match price and bundle mobile, television and streaming. It is trying to find areas where conventional telecom operators have not liked the address quality, collection cost, installation friction or income volatility. If it can concentrate enough customers in a barrio, field labour becomes more efficient, local referrals matter, and the cash-collection behaviour becomes part of the brand.

If it cannot reach density, the same approach becomes expensive: many installations, many small payments, many local support visits and not enough recurring revenue to support the network.

The proposition also has a behavioural dimension. A family that has never had fixed broadband may not immediately trust the value of a home line. Mercy Corps Ventures says Fibrazo used a two-week free trial in its approach. The IEEE Connecting the Unconnected booklet for 2022 similarly described Fibrazo building last-mile fibre in two poor Corrientes neighbourhoods, going door to door, giving interested households a free trial, and then letting customers prepay days according to liquidity. That older programme evidence should not be read as a current subscriber count, but it explains the logic behind the current plan page.

The company is lowering the perceived risk of trying a fixed line.

In inflationary markets the unit also protects attention. If prices move often, a monthly customer may focus on the latest bill increase. A prepaid customer sees a posted recharge price and chooses a shorter or longer validity period. That does not remove inflation risk for the operator. Imported equipment, network electronics, customer premises devices, vehicles, fuel, labour and upstream transit may move with the exchange rate or with general prices. It changes how the risk is presented to the customer. Instead of "your bill increased," the product says "this is today's price for seven, fifteen or thirty days."

Network-resource evidence

AX Internet also has current network evidence. LACNIC RDAP lists AS271949 as an active direct allocation for AX Internet S.A., with registration in 2021 and Gustavo Lorenzo Brisco listed as legal representative. LACNIC RDAP also shows AX Internet S.A. as registrant for 190.122.90.0/24, 128.201.171.0/24 and 2803:5610::/32. RIPEstat's announced-prefixes data for AS271949 showed visible announcements in late June and early July 2026 for 190.122.90.0/24, 128.201.171.0/24, 38.191.40.0/24, and two IPv6 /48s under 2803:5610.

PeeringDB lists the network as AX INTERNET, also known as Fibrazo, with ASN 271949, network type Cable/DSL/ISP, regional geographic scope, open peering policy and traffic level in the 10-20Gbps range.

This combination is strong enough for the network-resource topic because it links the brand, the company and active routing. It is not just a business registration. It is not just an old IP block. It is also not proof of customer quality, uptime or geographic reach. BGP evidence shows that the network is announced to the global internet. It does not show how many homes are connected, how clean the access layer is, how often customers see speed degradation, or whether every marketing city has the same quality.

The 38.191.40.0/24 route should be treated cautiously. RIPEstat observed it being announced by AS271949 during the reviewed window, but ARIN's RDAP view of 38.191.40.0 points to Cogent's larger 38.0.0.0/8 allocation rather than to AX Internet as holder. That may simply reflect leased address space or upstream arrangements. It should not be described as an AX-owned block without more documentation. The safer resource story is AS271949 plus the LACNIC-registered AX Internet IPv4 and IPv6 resources.

BGP paths observed through RIPEstat also suggest dependence on upstream and transit relationships outside AX Internet's own access network. That is normal for a regional ISP. It means customer experience depends not only on the fibre drop in the neighbourhood but also on backhaul, transit, peering, route stability and upstream pricing. PeeringDB's open policy and traffic range suggest an operator that has moved beyond the smallest reseller state, but the public data do not show an extensive multi-city autonomous interconnection footprint comparable with national carriers.

For a pay-by-day product, that distinction matters. A conventional operator can sometimes absorb a poor experience because customers are tied to a billing cycle or bundle. Fibrazo's customer can stop recharging. The network proof therefore supports the existence and operating surface of the ISP, but it also sharpens the retention question. Current routes make Fibrazo visible as an internet operator; they do not by themselves prove that the household will come back after a fault.

Corrientes and the Argentine market

Corrientes is not a saturated Buenos Aires-style market in the ENACOM data. In ENACOM's fixed internet report for the second quarter of 2025, Argentina had about 12.25 million fixed internet accesses and 81.82 accesses per 100 households nationally. Corrientes had 171,724 fixed internet accesses and 55.98 accesses per 100 households. The same report put national fibre optic accesses at 5.32 million, close to cable modem's 5.46 million, while wireless, satellite and ADSL remained smaller categories.

It also showed Corrientes with an average fixed internet download speed of 132.98 Mbps, below the national average of 224.77 Mbps but within the broad middle of the provincial table.

Those numbers create a plausible opening for a regional fibre entrant. Corrientes is not unconnected, but its household penetration is far below the national figure. A company that can build in neighbourhoods where incumbents have left gaps can find demand without claiming that the entire province lacks fixed internet. The opportunity is selective: blocks, barrios and customer segments that need fixed access but have been unattractive to larger providers.

The competitive pressure is real. Telecom Argentina's 2025 SEC filing showed the scale of a national operator: millions of fixed internet accesses, mobile subscribers, pay TV subscribers, and broadband ARPU figures that indicate an established ability to bundle services and spend on networks. Telecom reported 4.0 million fixed internet subscribers excluding TMA in the first quarter of 2025 and said 90 percent of those accesses had service of 100 Mb or more. That is a different operating machine from a regional prepaid fibre account.

Fibrazo does not need to beat national operators everywhere. It needs to beat them where the household decision is shaped by distrust, address informality, irregular cash flow and the pain of mobile data rationing. But if a larger operator decides to target the same barrio with a discounted bundle, or if mobile data becomes cheap enough for a household's real usage, Fibrazo's advantage narrows. The product has to remain flexible without feeling second tier.

Neighbourhood wireless providers are another substitute. They may be informal, familiar, cheap and fast to install. A local wireless operator may know the streets, take cash and answer on a personal phone. Fibrazo's fibre should offer a stronger technical ceiling, especially for shared household use, uploads and streaming, but wireless can be good enough if the household's usage is light or if fibre installation is delayed. Satellite backup is a different competitor.

Low-earth-orbit satellite service can reach difficult areas and may be attractive to rural or remote users, but equipment cost, power, roof placement and monthly plan price make it a poor direct substitute for many low-income urban homes. For a microbusiness, satellite may be backup; for the family Fibrazo targets, it is usually not the first price comparison.

Mobile broadband remains the most important substitute because it is already in the customer's hand. It is also the behaviour Fibrazo is trying to displace. Mercy Corps Ventures argued that mobile packages can be expensive for heavy home use and cut service when the package expires. That investor argument matches common usage logic: a phone is flexible, but a household that studies, streams and works online can consume data quickly. Fibrazo's "no data running out" claim is aimed directly at that anxiety.

Colombia as proof and complication

The Fibrazo brand is not only Argentine in public evidence. The Colombian Fibrazo website uses the same promise of home internet paid by the day, says users can recharge from one day, and describes no permanence clauses, free installation, no fixed bill and payment through MiFibrazo, Nequi, SuperGIROS, Efecty, PSE and other channels. The Colombian terms name FIBRAZO S.A.S. as a Colombian telecommunications service provider and describe fibre internet by recharge, available only in certain cities and neighbourhoods.

They list Cartagena, Barranquilla, Santa Marta, Turbaco, Monteria and Sincelejo for fixed internet activation, targeted at strata 1 and 2 households.

That Colombia evidence strengthens the operating thesis but complicates the corporate read. The Argentine directory company is AX Internet S.A. The Colombian terms name FIBRAZO S.A.S. A reader should not collapse every Fibrazo-branded activity into AX Internet S.A. without a corporate chart. The better view is that AX Internet is the Argentine company behind Fibrazo's Corrientes record, while public investor pages and Fibrazo's own Colombian site show a brand and operating playbook being applied in both Argentina and Colombia.

The Colombia material is useful because it shows where the concept moves when the company tries to scale. The Colombian homepage explains recharge through local payment methods and support through WhatsApp. The terms set a maximum installation period after first recharge, explain refunds when installation is not technically viable, and describe customer complaint rights. The page also describes internet tiers with 400, 600 and 800 Mbps symmetrical speeds, optional or bundled television arrangements, and the use of an ONT and, for some products, a TV box. This is not merely an impact story.

It is a telecom retail operation with country-specific consumer rules.

The operating risk rises with each country. Argentina and Colombia have different regulators, customer-rights regimes, payment rails, tax rules, labour markets, import constraints and local competitive structures. The playbook may be similar, but the execution is local. A sales message that works in Corrientes might need a different support and installation discipline in Cartagena or Barranquilla. The more the company depends on trust in low-income neighbourhoods, the less it can rely on a central brand alone.

Support labour and the field cost

Fibrazo's public pages make support look simple: contact by WhatsApp, recharge online, call a local number, and use the customer service channel for claims. The contract reveals the heavier reality. The operator expects to deliver equipment, recover equipment, access the premises for inspection and maintenance, respond to faults, manage customer data, handle billing claims, and comply with quality indicators set by Argentine rules. That is local support labour.

The cost is not just wages. It is route planning, trucks or motorbikes, training, stock control, optical equipment, drop cable, connectors, customer premises devices, safety procedures, permissions to pass fibre through a building or street, and a local reputation strong enough that households allow technicians to enter. In neighbourhoods with informal addresses, customer acquisition may involve location pins, local references and repeated visits. The IEEE description of Fibrazo's early Corrientes deployment noted door-to-door outreach and a design aimed at customers who might lack formal address documents.

That kind of acquisition can solve a barrier, but it is labour intensive.

Field cost is also where the pay-by-day design meets reality. If installation is free and the customer buys only short validity periods, the payback period can be long. A 7-day plan creates low adoption friction, but a customer who buys one week and then disappears leaves the operator with sunk installation and equipment exposure. A customer who buys repeatedly becomes valuable because revenue recurs without the resentment of a long contract. The business therefore depends on a conversion from trial to habit.

The public customer testimonials on Fibrazo's Argentine site are useful as marketing signals. They name Corrientes neighbourhoods such as Serantes and Ongay, and one testimonial links the service to children's school needs. These are not independent satisfaction data. The same page chooses which comments to publish. Still, they show the company presenting itself through neighbourhood credibility rather than through enterprise features or generic national coverage.

Unofficial signals are mixed, which is normal for access networks. Public social and forum snippets include positive mentions, requests for contacts, and complaints about service quality or support responsiveness. A Reddit thread about fibre service in Corrientes includes a user recommending caution about Fibrazo because of Wi-Fi and claim-handling problems. A Facebook group snippet complains about bad service. These fragments are not statistically representative and cannot prove network performance.

They are valuable because they show the weak point the company must manage: in a flexible prepaid account, support frustration can immediately become non-recharge.

Investor expectations and impact framing

Fibrazo is framed by investors as both a telecom company and an inclusion company. New Ventures Capital describes it as connecting underserved barrios in Latin America, says it has reached neighbourhoods in Cartagena and Barranquilla as well as Argentina, and lists founders Gustavo Lorenzo Brisco as CEO and Emiliano Mroue as CFO. The page also reports 54 low-income schools connected and 43,958 students connected. The Fibrazo Argentine homepage contains similar school-connectivity language and the same 54-school figure appears in public impact material.

Impact framing can help a telecom company enter neighbourhoods where trust is thin. It tells customers, investors and partners that the operator is not merely selling bandwidth; it is solving a social access problem. But the framing can also obscure the hard commercial question. An impact thesis does not pay for truck rolls, upstream transit or customer premises equipment unless the unit economics work. If low-income households love the flexibility but recharge irregularly, the company must either find subsidies, reduce installation cost, increase density, add services, or accept lower returns.

The investor pages suggest the company believes density and local knowledge can solve that. Mercy Corps Ventures described a neglected Latin American market and argued that Fibrazo's plan is cheaper than heavy mobile data usage. New Ventures Capital said Fibrazo understands the internal dynamics of barrios and can reach penetration rates above market average. Those are investor claims, not audited operating results. The public article should treat them as explanation of strategy, not proof of profitability.

LinkedIn adds a labour-market signal. The Fibrazo company page lists the industry as telecommunications, company size as 201-500 employees, founded in 2020, and visible job posts in Colombia, including roles in Medellin and Cartagena. LinkedIn company pages are self-maintained and can be imprecise, but the hiring pattern supports an operating footprint beyond a small static website. It also shows that scaling the model requires functions such as NOC, purchasing, data, growth and sales leadership, not only fibre technicians.

The economics of trust

The strongest argument for AX Internet is that the product is shaped around a real pain point. In Latin American low-income urban neighbourhoods, the barrier is not only whether a fibre cable passes nearby. It is whether the provider will install in the home, whether the customer can commit to monthly payments, whether mobile data is too expensive for household use, whether the household trusts a contract, and whether service can be restored when it fails.

Fibrazo addresses those barriers directly in its public language: recharge when you can, know what you pay, no long contract, no data running out, WhatsApp support, and free installation as advertised.

The strongest argument against the company is that every one of those promises transfers risk back to the operator. No contract means less contractual lock-in. Free installation means more capital at risk before payback. Prepaid days mean more frequent renewal decisions. Low-income customer focus means greater exposure to income shocks. Neighbourhood expansion means local execution risk. Fibre quality expectations mean the company cannot hide behind "best effort" as easily as a casual Wi-Fi seller. The account is flexible for the household precisely because it is demanding for the ISP.

Inflation adds another layer. ENACOM's fixed-internet report showed a sharp rise in sector revenue and ARPU in Argentine pesos, reflecting the price environment. Telecom Argentina's filings also restated results for inflation and showed year-over-year inflation of 55.9 percent as of March 2025, down from much higher 2024 levels but still high enough to complicate pricing. A small ISP must keep recharges affordable while costs such as electronics, fuel, labour and upstream services move. Short validity periods help reprice faster, but customers notice price changes more often.

The product may also blur the line between household and microbusiness use. The public pages speak to homes, but the need is often economic. A family vendor, home repair worker or small shop may use the connection to communicate with clients, upload product photos or receive digital payments. That can strengthen retention because the line supports income, not only entertainment. It can also increase usage and support expectations. A microbusiness owner who loses connectivity during peak sales hours may be less patient than a household streaming at night.

Payment rails and the recharge habit

The payment rail is part of the product, not a back-office detail. A prepaid fibre account works only if the customer can recharge at the moment the connection matters. In Argentina, the public plan page points the user to WhatsApp contact rather than publishing a broad list of channels on the same page. In Colombia, Fibrazo's website is more explicit: it says customers can use MiFibrazo and payment options such as Nequi, SuperGIROS, Efecty and PSE. The Colombian terms also say the customer can consult balance and recharge through the self-service portal or WhatsApp.

That difference may reflect country maturity, local payment infrastructure or simply how much each site exposes. It still shows why Fibrazo's operating task is not only to build fibre. A weekly internet product needs a weekly payment habit. If the household runs out of days at night, on a weekend or before a school deadline, the next purchase must be easy enough that the customer does not fall back to mobile data. A long interruption between intent and recharge weakens the whole promise.

The recharge habit also changes how the customer compares price. A monthly plan asks, "Can I afford the bill?" A weekly plan asks, "Is this week's access worth this week's money?" That can help households with irregular income because they can buy a smaller block when cash is tight. It can hurt the operator because the value comparison happens many times per month. Each time, the customer may remember the last fault, the last support reply, the current mobile balance, or the fact that a neighbour has a different provider.

For a microbusiness, the payment rail must feel even more predictable. If the business owner depends on the connection to take orders, upload photos, receive wallet payments or answer suppliers, the recharge is not discretionary entertainment. It is working capital. But it remains small working capital. A prepaid fibre account that can be topped up for a short period is attractive precisely because the owner can match the internet spend to near-term revenue. Fibrazo's opportunity is to turn that small payment into a recurring routine. Its risk is that the account remains a patch, used only when the customer has no better option.

Repair economics after installation

Installation is the visible sales moment, but repair is the retention moment. A customer may accept a delayed installation if the first connection finally works. A customer who has already paid for a week may be less forgiving when the line fails. The Argentine contract's response targets give a formal structure, yet a three-business-day service-fault target sits awkwardly beside a seven-day recharge. If a customer loses half of a weekly validity period to a fault and waits for an answer, the compensation rule may matter less than the memory of being disconnected.

This is one reason local density matters so much. A dense cluster of customers lets the operator solve faults in one area, keep spare equipment nearby, and make field visits economically sensible. A thin scatter of customers turns each fault into travel time. The same network design that is efficient at neighbourhood scale can become fragile if expansion outruns the local service base. Public sources do not show Fibrazo's truck-roll cost, response compliance, repair backlog or neighbourhood-level density, so the article cannot score execution.

It can identify the variable that matters most: prepaid fibre must be repaired fast enough that customers keep recharging.

The access network also faces physical risks that are easy to underestimate. Fibre cuts, power outages, damaged drops, poorly protected indoor cabling, customer equipment faults, connector contamination and building-access problems can all produce downtime. The customer may experience them as one thing: "the internet does not work." A low-income household usually does not care whether the fault is in the upstream, the ONT, the Wi-Fi router, a power issue or a cut cable in the street. It cares whether someone explains the problem and restores service while the paid days still feel valuable.

AX Internet's contract tries to define the line between company responsibility and customer responsibility. It says the customer must maintain necessary personal equipment and allow identified personnel to access installed equipment. It also limits responsibility for interruptions caused by power failures or other external services. Those are normal legal protections. Commercially, however, the customer may not make those distinctions. If the family bought Fibrazo and the home is offline, the brand owns the frustration even when the legal cause is mixed.

Substitutes as retention tests

Each substitute tests a different part of the offer. A larger Argentine fixed provider tests speed, bundling and perceived reliability. It can offer mobile, television, streaming or wallet products around the broadband account. It can advertise a familiar national brand and sometimes discount aggressively. Fibrazo's response is not to be bigger; it is to be easier to start, easier to pause and better adapted to the neighbourhood. That response works only when the customer values flexibility more than bundle breadth.

Mobile broadband tests immediacy. No technician is needed. The customer already owns the phone. A prepaid mobile top-up can be bought in very small amounts and used instantly. Fibrazo must beat mobile on household economics: shared screens, schoolwork, uploads, streaming, stable video calls and the absence of constant data anxiety. If mobile prices fall or 5G fixed-wireless offers become more available, that comparison tightens. The company's investor story relies on the claim that mobile data is too costly for heavy home use. That is plausible, but it must be true in each neighbourhood and price period, not only in a regional average.

Neighbourhood wireless tests local familiarity. A wireless seller may be less formal but more personally known. The customer may be able to call someone nearby, pay in cash and get a practical answer. Fibrazo's fibre should have a technical advantage in capacity and consistency, but the advantage is wasted if installation or support feels distant. The best defence against a local wireless substitute is not only speed. It is the combination of speed, repair, clear recharge and enough community trust that the operator feels local rather than remote.

Satellite tests edge cases. It can reach places where terrestrial access is weak, and it may appeal to businesses that need backup. But for the urban-peripheral, low-income household Fibrazo describes, satellite's equipment, placement and monthly cost make it a different product. It is a reminder, though, that "unserved" is becoming more complicated. As satellite, fixed wireless and national fibre expand, Fibrazo cannot assume that absence of incumbent interest will last. It has to turn early neighbourhood entry into durable habit before substitutes become easier.

What the public record does not prove

The public record is good enough to classify AX Internet as a regional ISP, but it is not good enough to prove operational excellence. It does not disclose active subscribers, average revenue per connected home, collection loss, installation payback, support compliance, route diversity, last-mile fault rates or monthly retention. It does not disclose whether the school-connectivity numbers are current, cumulative, independently verified or tied to revenue. It does not disclose whether Colombian growth shares the same balance sheet as AX Internet S.A. in Argentina.

The record also does not prove that the public prices are stable. In Argentina, price lists can become stale quickly, and websites may lag commercial reality. The useful evidence is the recharge structure and customer promise, not a claim that a July 2026 reader will face exactly the same peso amounts. Any valuation or commissioning decision should refresh the live plan page and, ideally, test the WhatsApp sales path before relying on exact price comparisons.

Finally, the public record does not prove that the network is uniformly fibre-to-the-home in every covered pocket. Company and investor materials describe fibre and FTTH-style last-mile access, and the contract is for internet access using delivered equipment. The article therefore treats fibre as the offered access technology. But the exact architecture, split ratios, backhaul design, vendor equipment and customer Wi-Fi performance are not public. Those details decide whether the service behaves like a high-quality fixed connection after the sale.

Public evidence

The public record used for this article supports the thesis in layers. Fibrazo's Argentine homepage, https://www.fibrazo.com.ar/, supports the brand positioning, Corrientes testimonials, no-contract language, daily-payment message, school-connectivity programme and Latin America ambition. The Argentine plan page, https://www.fibrazo.com.ar/plan/, supports the 7-, 15- and 30-day recharge structure and the displayed Argentine prices. The coverage page, https://www.fibrazo.com.ar/cobertura/, supports current Corrientes-facing coverage language and WhatsApp-assisted availability checking. The customer contract at https://www.fibrazo.com.ar/wp-content/uploads/2024/10/Modelo-Contrato-AX-INTERNET.pdf supports the legal provider identity, prepaid service terms, equipment arrangement, support hours, claim-response targets and fault-compensation language.

The regulator and network records support the operating-surface claim. ENACOM's licensee workbook at https://www.enacom.gob.ar/multimedia/noticias/archivos/202506/archivo_20250605110854_212.xlsx lists AX Internet S.A. as a VA-ISP licensee in Corrientes. LACNIC's AS271949 RDAP record at https://rdap.lacnic.net/rdap/autnum/AS271949 supports the ASN registration to AX Internet S.A. LACNIC records for https://rdap.lacnic.net/rdap/ip/190.122.90.0/24, https://rdap.lacnic.net/rdap/ip/128.201.171.0/24 and https://rdap.lacnic.net/rdap/ip/2803:5610::/32 support registered AX Internet IP resources. RIPEstat's announced-prefixes view, https://stat.ripe.net/data/announced-prefixes/data.json?resource=AS271949, supports current route visibility. PeeringDB's network page, https://www.peeringdb.com/net/28522, supports the Fibrazo alias, ISP network type, ASN, traffic range and regional scope, with the caveat that PeeringDB is user-maintained.

Market and investor sources support context. Mercy Corps Ventures' article at https://medium.com/mercy-corps-social-venture-fund/closing-the-connectivity-gap-for-low-income-urban-populations-in-latin-america-df9b540e3fe2 explains the low-income Latin America pay-as-you-go thesis, free trial approach and mobile-data substitute argument. New Ventures Capital's portfolio page, https://nvcapital.vc/our-work/fibrazo/, supports the founder names, Argentina and Colombia footprint, last-mile fibre service description and school impact figures. The Colombian website, https://www.fibrazo.com.co/, and terms page, https://www.fibrazo.com.co/terminos-y-condiciones/, support Colombia-facing Fibrazo service claims, payment channels, cities, strata focus, one-day recharge language and installation/refund terms. The Fibrazo LinkedIn page, https://www.linkedin.com/company/fibrazo, supports the telecommunications industry label, 2020 founding claim, company-size range and recent Colombia hiring signals.

The sector backdrop comes from ENACOM's fixed internet report for the second quarter of 2025, https://indicadores.enacom.gob.ar/files/informes/nacionales/2025/T2/2025T2-03%20-%20Acceso%20a%20Internet%20Fija.pdf, which supports national and Corrientes fixed-internet penetration, fibre growth and average speed context. Telecom Argentina's SEC filing, https://www.sec.gov/Archives/edgar/data/932470/000110465925047387/tm2514765d1_6k.htm, supports the larger-provider comparison, including subscriber scale, broadband churn, ARPU and inflation-restated reporting. The IEEE Connecting the Unconnected 2022 booklet, https://ctu.ieee.org/wp-content/uploads/2025/06/IEEE-Connecting-the-Unconnected-Challenge_2022-booklet.pdf, supports historical description of Fibrazo's early Corrientes deployment and pay-per-period design. Public forum and social results, including https://www.reddit.com/r/AskArgentina/comments/1ce0j2f/servicio_de_fibra_%C3%B3ptica_en_corrientes_capital/, are used only as weak unofficial signals of customer discussion and complaint themes, not as proof of overall service quality.

What would change the judgement

The first fact that would change the view is verified customer retention by recharge cohort. The public story is persuasive because the product fits a real affordability problem. But the business becomes much stronger if 7-day buyers reliably graduate into repeated 15- or 30-day purchases, or if short-period buyers stay active over many months. Without that proof, the product can be loved at installation and weak at renewal.

The second fact is installation payback. If installation is truly free to the customer, the company needs enough lifetime revenue per connected home to recover labour, materials, customer premises equipment and support. Dense neighbourhood build-outs can make that work. Scattered addresses can break it. Public sources do not provide cost-per-home, gross margin, payback period or equipment recovery rates.

The third fact is fault performance. The contract gives response targets; it does not publish actual compliance. For a pay-by-day product, a three-business-day target for service interruption may be legally understandable but commercially painful if the household's current recharge window is only seven days. The customer's memory of a fault may matter more than the formal compensation rule.

The fourth fact is upstream resilience. AS271949 is visible and has registered resources, but public BGP records cannot fully reveal route diversity, backhaul bottlenecks or local access congestion. A regional ISP that depends heavily on one upstream path or one fragile local link may look healthy in registry evidence until a failure exposes concentration.

The fifth fact is corporate structure across Argentina and Colombia. Public pages show AX Internet S.A. in Argentina and Fibrazo S.A.S. in Colombia. Investor pages discuss Fibrazo across both countries. A clearer corporate map would help separate which assets, obligations, licences, liabilities and revenues belong to AX Internet and which belong to other Fibrazo operating companies.

Bottom line

AX Internet is a stronger case than a thin ASN profile because the evidence joins the retail offer, the licence, the contract and the network. The company sells a recognizable access service under the Fibrazo brand. It has public Argentine plans, Corrientes coverage language, an ENACOM VA-ISP row, a customer contract, current LACNIC resources and live AS271949 announcements. That is enough to treat it as a regional ISP with meaningful network-resource evidence.

The harder question is whether the prepaid fibre account can keep customers after the first installation. Fibrazo's promise is attractive because it removes the fear of a fixed monthly bill. The same design removes a portion of the operator's lock-in. The customer can buy a week, pause, complain, switch to mobile, wait for a larger provider, or ask a neighbourhood wireless seller. AX Internet's advantage must therefore be renewed in small decisions: the recharge price is clear, the connection works, the support channel answers, the technician arrives, the child can study, the seller can upload, and the household feels in control.

If those small decisions repeat, Fibrazo becomes more than affordable broadband. It becomes an access habit in places where conventional broadband has often failed to become one. If they do not repeat, the company will have proved that prepaid fibre can create trial, but not that it can create durable retention.