Summary

- Arnouk and Lady Partner Company Microsolutions is publicly evidenced as a RIPE NCC Local Internet Registry in Syria with one IPv4 provider-aggregatable allocation and one IPv6 allocation, but that evidence proves resource-holder status rather than a full independent retail network.

- The cash-flow test is whether a narrow account base can pay for upstream dependence, local support, regulatory compliance, RIPE fees, replacement equipment, billing losses, and working capital in a low-income, low-resilience market.

- Routing evidence points to Syrian Telecom as the key carriage layer for the IPv4 block, which can lower build cost but also narrows operational independence and supplier leverage.

- The judgment should change only if current production evidence shows active customers, published tariffs, staffed service channels, audited revenue, route diversity, current licensing, and customer retention strong enough to cover renewal capital.

One paying account is the whole test

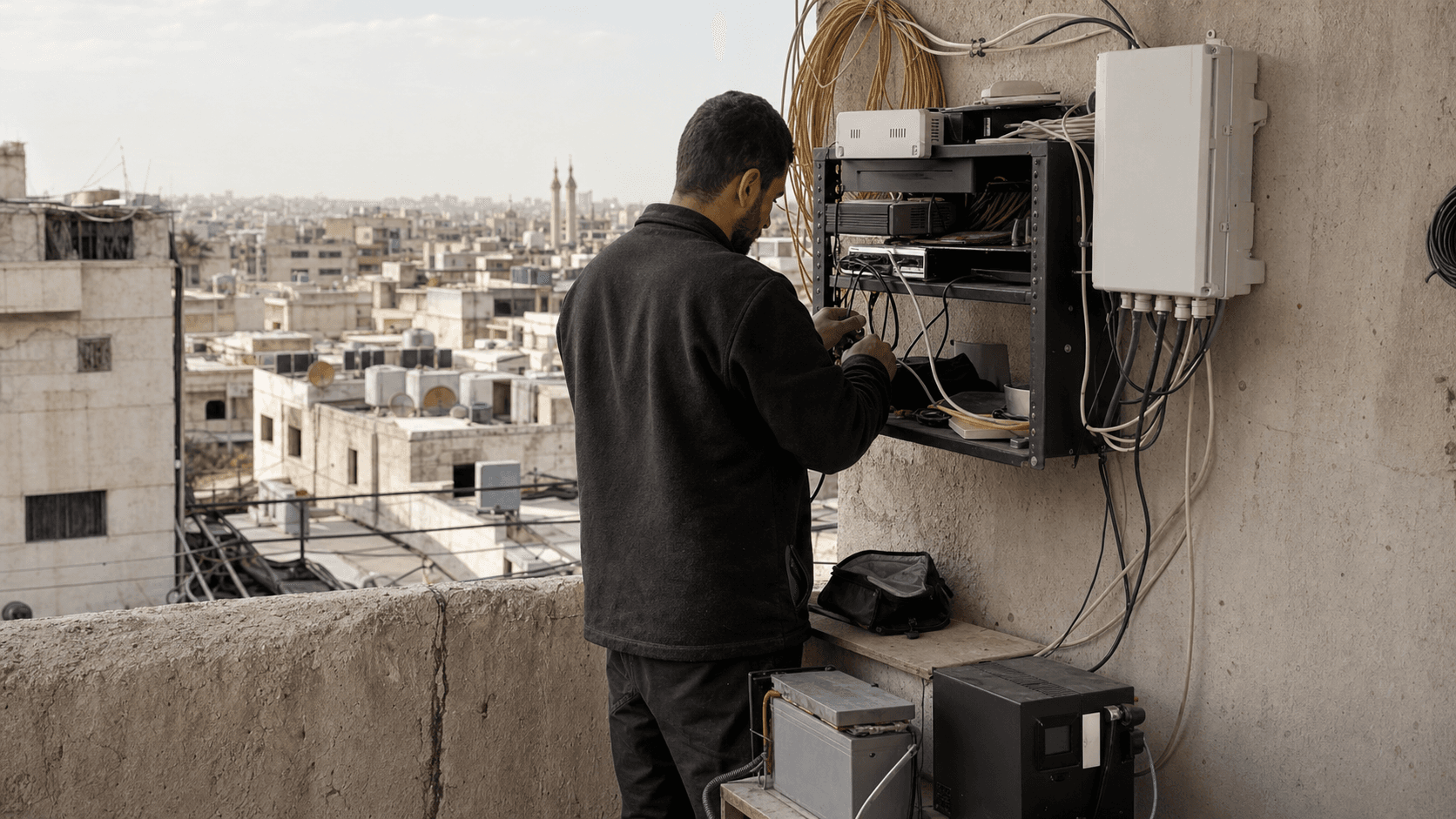

Start with one paying account: a shop, office, clinic, private school, small software firm, or apartment building that buys local connectivity because it needs a stable route to email, payments, cloud tools, voice calls, remote family, and public services. Its monthly fee is not just revenue. It has to carry every cost that sits behind the plug. It has to pay for upstream access, civil works already sunk into the access path, a router or radio that fails at inconvenient times, a person who answers when the service drops, billing and collection friction, compliance work, and the annual cost of staying recognized in the number-resource system.

If that one account pays late, discounts hard, or churns to a mobile bundle, the network does not become cheaper in proportion. The supplier still wants payment, the registry still expects renewal, the technician still needs wages, and the next spare part still has to be bought in hard currency or through an import chain.

That is why Arnouk and Lady Partner Company Microsolutions should not be read as merely a name in a registry. A registry entry is the opening of the question, not the answer. It tells us there is a formal identity associated with Internet number resources in Syria. It does not tell us how many people pay the company, whether the company sells fixed wireless access, leased lines, managed connectivity, wholesale address space, hosting support, or only holds resources in a broader commercial arrangement. The economics have to be tested from the outside with disciplined restraint.

A small allocation can support a useful business if the customers are dense, loyal, and willing to pay for reliability. The same allocation can also be a thin administrative footprint sitting behind a stronger carrier, reseller, or local partner.

The article therefore treats the company as a cash-flow problem. A reliable local connection in Syria is not created by address space alone. It is created by the capacity to convert fees into maintenance, permissions, power, transit, routing administration, customer care, and reinvestment. The buyer wants a working service. The seller needs enough gross margin to absorb outages, fuel or power instability, foreign exchange movements, sanctions compliance friction, and hardware scarcity. The public record proves a number-resource footprint.

The commercial question is whether the footprint is attached to a customer engine strong enough to keep the service standing when costs arrive before collections.

What the public record proves

The public record proves four core facts. First, Arnouk and Lady Partner Company Microsolutions appears in RIPE NCC material as a Local Internet Registry with a Syrian service area. Second, the RIPE-linked company listing gives a Damascus-area address and contact details, and the country listed is the Syrian Arab Republic. Third, public allocation summaries identify the LIR code associated with the company and show a provider-aggregatable IPv4 block dated April 2016. Fourth, the same allocation summaries show an IPv6 allocation dated October 2021. Those facts are meaningful.

They show that the company has been visible to the regional number-resource system for years, not just as a newly minted marketing page.

The specific IPv4 footprint is small in global terms: one block of 1,024 addresses. In a mature fixed-broadband market that would not support a large retail operator by itself unless address sharing, carrier-grade translation, business services, or non-address revenue carried the model. In a constrained market, however, a small block can still matter. It can support local access customers, business links, management addresses, or a narrow service domain if the operator has upstream carriage and disciplined address use.

The IPv6 footprint is more expansive in address count, as IPv6 allocations usually are, but the Syrian market context matters. National IPv6 user adoption remains very low by international comparison, so the business value of IPv6 is more strategic than immediately monetized. It can signal readiness, reduce future scarcity pressure, and support modern network design, but it does not automatically produce cash.

The public record also links the IPv4 allocation to Syrian Telecom autonomous-system evidence. Third-party network data and route records show the Arnouk block appearing under Syrian Telecom origin data, and older route records also show another Syrian origin path. That matters because it points to a resource holder whose reachability may depend on a national carrier layer rather than on a fully independent autonomous-system posture. The economic implication is double-edged. Dependence on an incumbent carrier can reduce capital intensity, because the smaller entity does not have to build every interconnection and international path.

It also weakens bargaining power, because the customer-facing promise depends on upstream terms, restoration priorities, route policy, and technical responsiveness outside the smaller entity's direct control.

The public record does not prove active tariff plans, active customer numbers, audited revenue, licensing status for every service line, ownership, direct peering, current help-desk staffing, or service-level performance. That absence is not a negative finding by itself. Small operators in difficult markets often leave a thin public trail. But for an economics-first judgment, the absence of public commercial data is itself part of the risk profile. The evidence supports tracking the company as a resource holder and possible local connectivity entity.

It does not support treating it as a scaled, independently monetized ISP without further proof.

What the record does not prove

The most important discipline is to separate registry status from commercial service. RIPE membership and allocations are evidence of a relationship with the number-resource system. They do not prove that Arnouk and Lady Partner Company Microsolutions sells broadband directly to households. They do not prove cloud hosting, managed security, IP transit, data-center operation, domain-registration service, enterprise connectivity, or wholesale resale. Those may exist, but they must be evidenced separately. This distinction is not pedantic.

In telecom economics, the difference between a resource holder and a revenue-generating operator is the difference between a file and a business.

The record also does not prove that the company controls the underlying physical access network. The customer may see a local brand or contact, but the expensive parts of connectivity can sit elsewhere: incumbent backbone, wireless access equipment, tower sites, poles, ducts, leased transmission, shared offices, outsourced support, or reseller agreements. A small company can add real value at the last mile even when it buys the heavy network inputs from someone else. It can know the neighborhood, collect from customers, install radios, maintain routers, and solve problems faster than a central carrier.

But its profit pool is then the spread between what customers pay and what suppliers charge. That spread can be thin in a market where affordability is low and customers treat connectivity as necessary but price-sensitive.

Nor does the record prove that every domain, contact, or LazerNet reference is owned by the same legal person. Public network data ties the Arnouk allocation to a LazerNet-branded domain and shows a separate Lazer Net Ltd footprint in the same national context. The right conclusion is not to merge identities casually. The safer conclusion is that there are contact-domain and routing-context overlaps that deserve attention, while legal and operational control still require confirmation. This matters because related branding can produce false confidence.

A customer may care only that the service works, but an analyst has to know who carries the obligation, who pays the supplier, who can renew the registry account, and who can respond when a compliance inquiry or abuse complaint arrives.

The record is also quiet on ownership and financing. That is a material gap. In a fragile network market, a small operator's resilience often depends less on technical skill than on who can provide working capital. Hardware has to be imported or sourced through constrained channels. Spare radios, routers, optical modules, batteries, and power gear may be priced in dollars or linked to foreign exchange. If collections are in local currency and supplier costs reprice faster than customer fees, the company can be operationally competent and still financially squeezed. Public registry evidence cannot answer that question.

It can only show the base on which a deeper operating review should begin.

The resource footprint as an economic clue

The IPv4 block associated with Arnouk and Lady Partner Company Microsolutions is a small but real asset in a world where IPv4 scarcity still shapes network design. A 1,024-address allocation can be useful for a local access network, business customers, infrastructure nodes, and address pools behind translation. But it also imposes discipline. If the company serves many retail users, it cannot hand out plentiful public addresses without charging for them or rationing them. If it serves fewer higher-value accounts, the address pool can support more stable customer relationships, but the account concentration risk rises.

The block therefore tells us both that the company has something valuable and that the scale ceiling is visible unless revenue comes from services beyond raw addressing.

IPv6 changes the technical ceiling but not necessarily the near-term revenue ceiling. A large IPv6 allocation gives design room, cleaner end-to-end addressing, and a better future posture. Yet the market evidence for Syria points to low IPv6 adoption among users. That means IPv6 readiness may help with enterprise credibility or future migration, but most immediate customer value still runs through IPv4 reachability, mobile access, local caching, and the reliability of ordinary web and application traffic. An operator cannot pay wages with unused address capacity.

It has to convert technical optionality into customer retention, lower support cost, or better supplier terms.

The allocation dates are also informative. An IPv4 allocation in 2016 places the company in a period when small regional resource footprints were still being formalized across parts of the Middle East. The IPv6 allocation in 2021 suggests the account did not vanish after the initial registration. It remained visible enough to take or hold next-generation resources. That continuity is a positive indicator. It does not show profitability, but it lowers the probability that the entry is a one-off artifact.

A company that maintains number-resource status across years has at least some administrative continuity, or it is part of a wider arrangement where continuity is worth preserving.

Still, the market value of the footprint depends on route quality. An address block that is theoretically assigned but poorly routed is not useful to customers. The public route evidence shows the IPv4 space tied to Syrian Telecom origin data. That is a viable path if Syrian Telecom supplies stable national and international reach. It is a constraint if the smaller company has no route diversity, no direct upstream choice, and no practical way to reroute during congestion or outage. The allocation is therefore best understood as a governed resource sitting inside a broader Syrian carriage environment.

It has value, but the value is mediated by supplier dependence and by the country's wider network resilience.

Supplier dependence is the hidden balance sheet

For a small connectivity company, suppliers are the hidden balance sheet. The public accounts may be unavailable, but the operating dependencies can still be read. Upstream bandwidth, route origination, last-mile inputs, power continuity, equipment supply, premises, billing systems, and registry fees all arrive as obligations before the customer sees a clean connection. If the company buys key inputs from Syrian Telecom or relies on Syrian Telecom for route visibility, then the economics are shaped by that relationship. The company may be closer to a local access and customer-service layer than to an independent network owner.

That model can work. In many markets, small providers survive precisely because they do not own the whole stack. They know local customers, install quickly, accept smaller accounts, and provide human support in places where a national operator is slow. Their capital lightness is a strength when demand is uncertain. But the tradeoff is that the upstream supplier can capture much of the margin. If wholesale bandwidth prices rise, if payment terms tighten, or if the supplier prioritizes its own retail products, the small provider has little room to maneuver.

It can either raise prices, accept lower margins, reduce service quality, or lose customers.

The Syrian context makes supplier dependence more serious. National infrastructure has been affected by years of conflict, sanctions, currency stress, and investment gaps. Even after sanctions relief in some jurisdictions, telecom equipment and finance do not normalize overnight. Banks remain cautious. Vendors scrutinize counterparties. Import chains carry delay and compliance cost. A small provider must hold enough cash or supplier trust to bridge these frictions. Otherwise, ordinary network maintenance becomes a liquidity event. A failed router is not just a technical fault; it is a working-capital test.

Supplier dependence also shapes customer promises. If the company markets reliability but cannot influence upstream congestion or national outages, it risks selling a service-level expectation it cannot enforce. Better operators handle this by being explicit with customers, pricing realistically, and investing in the parts they can control: local access quality, faster field response, careful address management, backup power, spare equipment, and clear outage communication. The public record does not show whether Arnouk does that. The economic point is that its registry footprint is too narrow to carry a broad reliability claim on its own.

Reliability would have to come from disciplined supplier management and localized execution.

Revenue quality matters more than nominal subscriber count

The central revenue question is not how many possible users exist in Syria. It is how many paying accounts the company can keep at prices that cover real costs. A low-income connectivity market can have high need and weak monetization at the same time. Customers need Internet access for education, work, remittances, messaging, commerce, and public information. But need does not equal pricing power. When household income is tight, users downgrade, share connections, switch to prepaid mobile bundles, tolerate lower speeds, or delay payment. A provider that grows by adding fragile accounts may increase support load faster than gross profit.

Revenue quality is best judged through account type. A business customer with a point-of-sale system, cloud accounting, remote staff, or a branch office may pay more reliably than a household, but it will demand faster repair. A residential cluster may produce more accounts per street, but collections can be labor intensive. A school, clinic, NGO office, or local government site may value uptime but introduce procurement delays. A reseller or building operator can aggregate demand, but that creates concentration risk.

Without public customer data, the safe assumption is that any small provider must balance these segments carefully or be exposed to one dominant buyer.

Pricing power also depends on substitutes. In Syria, substitutes include mobile data, incumbent fixed services, other local wireless providers, business links from better-known operators, satellite in some contexts, shared Wi-Fi, and informal resale. If a customer's alternative is poor, the local provider can charge for reliability. If the alternative is "good enough" and easier to buy, the provider becomes a price taker.

The public evidence on market competitiveness is mixed in a way that matters: the national market looks constrained and resilience is low, yet the presence of many listed LIRs and local wireless licensing activity means customers may still face several imperfect alternatives in dense areas.

The strongest business would not be a volume story. It would be a quality-of-revenue story: a compact group of customers who pay on time because downtime is costly to them, with contracts or social proximity that reduce churn, and with enough margin to fund repair. The weakest business would be a thin pool of low-price users behind a supplier contract the company cannot renegotiate. Registry evidence cannot distinguish between those cases. That is why published tariffs, customer references, active service channels, and evidence of current installations would be decisive.

The cost base is unforgiving

The cost base for a small network entity has fixed and semi-fixed layers. RIPE membership and number-resource administration are small compared with a national carrier's budget, but they are not zero. Upstream service is recurring. Equipment depreciation continues whether customers are happy or not. Support labor is lumpy: a provider can run lean until outages cluster, at which point customers expect simultaneous attention. Power backup is also lumpy. Batteries, generators, inverters, fuel, and replacements create costs that customers rarely see but immediately punish when absent.

Currency risk can be more damaging than the nominal cost list suggests. Customer collections may be in local currency, while equipment, software, international connectivity inputs, and even some compliance services are linked to foreign currency. If the local currency weakens and contracts cannot be repriced quickly, the provider's margin compresses. A small operator with limited cash cannot always buy spare parts in advance. It may defer replacement, reuse equipment, or accept longer restoration times. Those choices preserve cash in the short term and damage reputation in the long term.

Compliance is another cost that looks administrative until it becomes commercial. Maintaining accurate registry records, abuse contacts, billing contacts, and route objects is part of being a serious number-resource holder. In a market with sanctions history, counterparties may ask more questions than they would in a low-risk jurisdiction. A supplier, bank, domain provider, or equipment vendor may require screening and documentation. Even when broad sanctions relief applies, targeted measures remain, and international institutions often move more slowly than formal policy. The cost is not only legal advice.

It is delay, uncertainty, and the need to maintain clean records.

The repair burden should not be underestimated. A local provider's reputation depends on what happens when a connection fails. Field visits, replacement radios, roof access, customer premises wiring, configuration errors, malware complaints, and power faults all consume time. A provider with too few technicians can sell more accounts than it can support. A provider with too many technicians loses money unless revenue density is high. The optimal staffing level is hard to find in a volatile market. That is why the first paying account matters: each fee must contribute to a repair machine that is mostly invisible until the day it is needed.

Competition and substitutes are imperfect but real

Syria's connectivity market is not a clean textbook market. Public data points to low resilience, limited competition for many users, low fixed speeds, and a heavy role for incumbent infrastructure. At the same time, the list of Syrian RIPE members, local wireless licensing activity, mobile reform, and the entry of new mobile investment all show that Arnouk does not operate in a vacuum. The customer has alternatives, even if those alternatives are uneven. The relevant competitive set is not just other companies with similar registry entries. It includes every way a user can get enough connectivity to avoid paying Arnouk's price.

Mobile is the obvious substitute for many households and small businesses. If mobile data becomes cheaper or more reliable after new investment, some fixed wireless or small local access accounts will weaken. Mobile will not replace every business link, and it may be inferior for stable office use, shared premises, or predictable monthly data needs. But it sets a psychological price ceiling. A customer who can buy a prepaid bundle and tether devices will resist a local provider's higher fee unless the local provider offers materially better reliability, latency, support, or data allowance.

The incumbent fixed layer is another substitute and supplier at the same time. Syrian Telecom can be a wholesale enabler, a route origin, and a retail alternative. That creates a familiar small-provider problem: the company may depend on a stronger player that can also compete for the same end customer. The small provider's defense is local execution. It must solve issues faster, understand neighborhood constraints, extend service where the incumbent does not prioritize, or bundle support in a way a larger operator will not. If it cannot do that, it is merely reselling exposure to the same underlying network with an extra margin layer.

Informal and semi-formal access also matters. Shared connections, building-level Wi-Fi, small wireless networks, and local resellers can pressure formal providers. Regulation may push public Internet provision toward licensed companies, but enforcement is uneven in many recovering markets. A licensed provider can benefit if authorities clamp down on unlicensed service, yet it can also lose accounts to cheaper gray-market alternatives if enforcement is weak. The company's competitive position therefore depends partly on policy consistency.

A rule that requires licenses is valuable only if customers and venues believe noncompliance will actually matter.

Regulation and geopolitics set the risk premium

Syria's telecom sector is being repositioned after years of political and economic stress. Public official sources point to mobile licensing reform, a settlement around a departing international operator, and a major new mobile license awarded to Zain. Those developments may improve the investment climate and create demand for supporting connectivity, enterprise links, and local service partners. They may also raise expectations. If national mobile networks modernize and attract large capital, small fixed or wireless providers will need a sharper reason to exist.

Sanctions are no longer the same constraint they were before 2025, but the risk premium remains. The United States moved to remove broad Syria sanctions while retaining targeted restrictions against former regime-linked actors, human rights abusers, drug traffickers, terrorism-linked parties, and other designated groups. The European Union also eased broad economic sanctions while maintaining targeted measures against former regime-linked individuals and entities. In practical commercial life, that means Syria can become easier to finance without becoming ordinary.

Banks, vendors, and registries still care about screening, ownership, end use, and payment flows. A small telecom-linked company has to operate inside that caution.

Regulatory risk also sits closer to the ground. Public reporting from Syria's telecommunications regulator emphasizes licensing for providers of public Internet access and restrictions on unlicensed provision in public venues. That can help formal providers by reducing informal competition. It can hurt them if compliance costs rise or if permits are required for service models that were previously informal. The company needs current licenses, clear service scope, and a clean relationship with the regulator if it sells to the public. A RIPE allocation alone does not answer that.

Geopolitical risk enters through procurement. Telecom networks use hardware, software, firmware, cryptography, monitoring tools, and sometimes cloud management systems. Vendors may be reluctant to supply, may demand prepayment, or may route sales through intermediaries. Each intermediary adds cost and uncertainty. If the company depends on imported equipment but earns in a weak local market, the replacement cycle can become the binding constraint on reliability. The customer experiences that as slow repair or inconsistent performance. The operator experiences it as a margin squeeze that cannot be solved merely by holding IP addresses.

Unofficial signals should be used cautiously

Unofficial market signals around the Arnouk address space are thin and should be treated cautiously. Abuse-report databases show scattered reports on individual addresses in the allocation, with low confidence scores in some cases and a small number of reports. That does not prove a bad network. Any access provider can receive abuse complaints from infected customer devices, web crawlers, open proxies, misconfigured equipment, or hostile users. In fact, a small number of low-confidence reports may simply indicate that the address space is in use somewhere.

The right question is whether the provider maintains a responsive abuse contact and can identify and control offending customers.

Domain and IP reputation sources also point to a LazerNet-branded context around related Syrian address space. This is useful but not conclusive. It suggests a local Internet services environment and offers clues about nameservers, mail hosts, and site presence. It does not prove that Arnouk and Lazer Net Ltd are legally the same entity. It also does not prove customer scale. Public website ranking estimates are especially noisy in Syria, where access patterns, caching, local language use, and intermittent availability can distort third-party measurements. They should be used as clues, not as valuation inputs.

Network tools show that Syrian Telecom is the larger routing context. This is a stronger signal than reputation chatter because BGP data is closer to how the Internet actually reaches the address block. But even BGP evidence needs care. A route origin can show who announces reachability without showing the private commercial agreement behind it. The smaller company may be a customer, partner, affiliated service, local brand, or resource holder whose block is carried by the incumbent. Each relationship has different economics. Only contracts, invoices, or direct operating evidence would settle it.

The absence of social chatter is also ambiguous. A consumer ISP with poor service often leaves complaints; a small business-focused operator may leave almost none. A company operating through local relationships may have limited public footprint. In Syria, public criticism and commercial disclosure may be muted by political, security, language, and platform factors. Therefore, the article does not penalize the company for lacking a large review trail. It does, however, treat the absence of public customer proof as a reason to keep the confidence level moderate rather than high.

Who pays, who benefits, who carries downside

The paying customer funds the whole chain. The customer pays because connectivity is valuable, but the fee is split among many claimants before any profit remains. Upstream carriers, access-site owners, equipment vendors, technicians, registry obligations, tax or license costs, payment intermediaries, and bad-debt losses all stand ahead of equity return. The customer benefits if the provider is close enough to fix local problems faster than a larger operator. The provider benefits if it can buy wholesale inputs at predictable prices and sell a differentiated service.

The supplier benefits if small providers extend demand without requiring the supplier to manage every end user.

The downside risk is less evenly distributed. Customers carry the immediate cost of outages: lost sales, missed messages, failed calls, interrupted learning, and wasted time. The provider carries churn and reputation loss, but only after customers have suffered. Suppliers may still collect fixed fees even when local service quality is poor. The registry system continues to require accurate records and fees regardless of retail demand. This distribution matters because it explains why small providers can look stable until a shock arrives. The pain first appears at the customer edge and only later becomes a financial problem for the operator.

If Arnouk has concentrated customers, downside risk becomes sharper. Losing one school, business complex, reseller, or public-sector account could remove a large share of cash flow. If it has many low-paying households, collection and repair costs may eat the margin. If it relies heavily on one supplier, a price change or service dispute can reset the economics overnight. The public record is not rich enough to identify the dominant risk, but all three are plausible for a narrow resource holder in this market.

The healthiest version of the business would align incentives clearly. Customers would pay for a defined service, not vague reliability. The company would maintain realistic contention, spare equipment, and honest outage communication. Suppliers would have contracts that allow restoration and predictable capacity. The regulator would provide clear licensing. In that version, even a small provider can be socially useful and financially durable. The weakest version is a thin reseller with limited control, weak collections, no route diversity, and customers who leave as soon as mobile or incumbent alternatives improve.

The cash-flow test

The cash-flow test has five parts. First, does recurring revenue cover recurring supplier cost before any growth spending? If the answer is no, the company is subsidizing customers or consuming past capital. Second, does gross margin cover support labor and spares? If the answer is no, reliability will decline when equipment ages. Third, can prices be adjusted when foreign-linked costs rise? If the answer is no, inflation and currency movement transfer value from the provider to customers until the provider cuts quality. Fourth, does the company have enough customer diversity to survive the loss of one large account?

If the answer is no, the network may be financially brittle even if it is technically sound. Fifth, does the company have a current regulatory and supplier position that lets it keep operating without interruption? If the answer is no, every customer promise is conditional.

On available evidence, only part of this test can be answered. The company has a public number-resource footprint. It has a Syrian service-area record. It has address space that can support real network use. It appears in a routing context tied to a national incumbent. Those are prerequisites, not proof of cash generation. No public material reviewed for this assignment shows current tariffs, customer contracts, audited accounts, traffic volumes, network maps, repair metrics, or renewal-capital reserves.

Therefore, the prudent judgment is that the company is trackable and potentially operationally relevant, but not yet investable or competitively classifiable on public evidence alone.

This is not a criticism of the company. Many small operators in difficult jurisdictions have better operating reality than public documentation suggests. A local provider may be known to customers through phone calls, installers, shops, and neighborhood reputation rather than polished websites. But an external research judgment must price uncertainty. If the public record does not show revenue quality, the analysis cannot assign it. If route data shows upstream dependence, the analysis cannot assume independence. If allocation data shows a small footprint, the analysis cannot infer large scale.

The cash-flow test is also useful because it avoids a common error in telecom analysis: mistaking scarcity for profitability. IPv4 addresses are scarce, Syrian connectivity is difficult, and reliable service is valuable. None of that guarantees margin. Profit appears only when the provider controls enough of the value chain, charges enough for the reliability customers need, and keeps costs from outrunning collections. That is the unresolved question for Arnouk and Lady Partner Company Microsolutions.

What would change the judgment

The judgment would improve with current evidence of active service and pricing. A live service page, current tariff sheet, verified customer service channel, active installation footprint, or recent customer references would show that the registry footprint is attached to market demand. Evidence of business customers would matter more than generic consumer claims because business accounts are likelier to pay for reliability. Evidence of low churn, prepaid discipline, or multi-month contracts would matter more than raw subscriber count.

The judgment would improve further with network-control evidence. A current autonomous-system relationship, route diversity beyond a single national path, documented upstream contracts, RPKI status for the block, active monitoring, and clear abuse-handling procedures would reduce the supplier-dependence discount. So would evidence that the IPv6 allocation is not merely held but deployed for customers or infrastructure. In a low-IPv6 country, deployment would signal operational seriousness even if immediate revenue remains IPv4-led.

The judgment would also improve with licensing and compliance evidence. A current public Internet service license, if applicable to the company's actual service line, would reduce regulatory risk. Clean billing contacts and registry contacts reduce administrative risk. Evidence that the company can source equipment lawfully under the post-2025 sanctions environment would reduce replacement risk. A current ownership disclosure, even if private, would help counterparties understand sanctions and credit exposure.

The judgment would worsen if the resource records become stale, if the allocation stops being visible in BGP, if contact details fail, if abuse reports rise without response, if the company is shown to depend on a single troubled reseller, or if customers publicly report chronic non-repair. It would also worsen if mobile reform quickly improves consumer alternatives while the company lacks business accounts that value fixed or managed reliability. In that case, the small resource footprint becomes less a defensible niche and more a stranded administrative position.

For now, the most defensible conclusion is moderate and specific. Arnouk and Lady Partner Company Microsolutions is a Syrian RIPE NCC resource-holder with a small but meaningful number-resource footprint and evidence of routing through the national telecom environment. That makes it relevant to local network reliability analysis. It does not prove a scaled retail ISP, independent infrastructure owner, cloud provider, or financially strong operator.

The cash-flow test remains open: can enough paying accounts fund supplier costs, support labor, compliance, and renewal capital in a market where connectivity is essential but purchasing power and resilience are weak? Until that answer is documented, the company should be tracked as a useful but uncertain local network entity rather than treated as a settled commercial winner.