Summary

- Foxtel s.r.l. is a Viterbo-based Italian telecoms and broadcast-technology company whose aFibra AntennADSL access business sells a mixed fixed-wireless and FTTH proposition across parts of Lazio, Tuscany and Umbria.

- The strongest evidence for the company as a regional ISP is current and operating: aFibra publishes FWA and FTTH access offers, coverage and support channels, tariff and technical transparency documents, reseller and installer information, and live network records for AS56754.

- The economic question is whether a local radio grid with more than 60 claimed sites can keep enough scattered customers online at EUR 25.90 to EUR 29.90 per month while fibre, national FWA, mobile broadband and satellite keep lowering the outside option.

- The evidence supports the topics Regional ISP economics, Local support labour and Network-resource evidence, but it does not prove address eligibility, delivered speed, congestion, repair time, customer churn or unit margins.

A household at the edge of the map

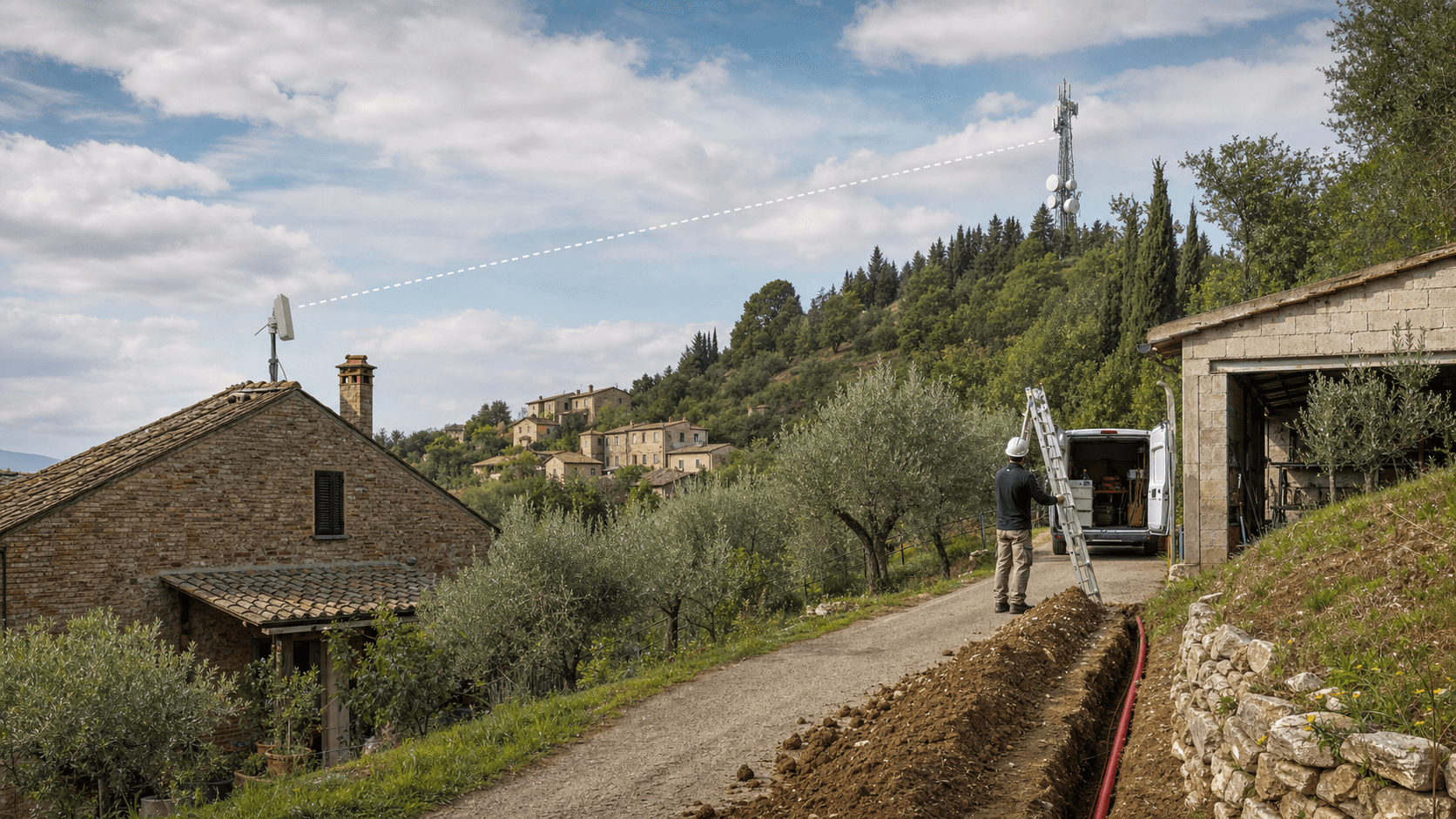

The customer this company is built around is not the apartment in central Rome that can choose among a dozen national FTTH retailers. It is a household in a frazione, a farmhouse near a ridge, a small agriturismo with cameras and booking systems, or a local professional office whose broadband choice is still constrained by distance from a cabinet, civil works, and the timetable of fibre deployment. The customer asks a practical question: can this line be installed soon, can it carry video calls and streaming at night, and can someone nearby fix it when weather, trees or equipment get in the way?

aFibra answers that question with a hybrid offer. On its home page, the brand says it has provided FWA service since 2010 to more than 3,000 customers in Lazio, Umbria and Tuscany, with telephone and chat support in real time. The same page advertises two paths: FTTH for addresses that can use fibre, and Fibra-Radio FWA for places without fibre. Its coverage page claims a proprietary network with more than 60 locations across Lazio, Tuscany and Umbria, using 5 GHz and 60 GHz rather than mobile 4G or 5G frequencies. Those claims do not prove capacity at any given house. They do define the business model: a local operator tries to make roof equipment, nearby radio sites and local support compete against the slow, expensive geometry of fibre trenches in low-density places.

The company boundary is important. Foxtel s.r.l. is the legal entity. aFibra AntennADSL is the customer-facing internet access brand. The article is about that company and that access business, not about the Australian pay-TV company with a similar name and not about turning every network artifact into a separate business actor. AS numbers, prefixes, IX ports and route records are evidence of an operating network. They are not customers, products or independent economic units.

What Foxtel sells: a local access account, not a slogan

The clearest paid unit is the monthly access subscription. aFibra's residential Fibra-Radio 100 page advertises up to 100 Mbps down and 30 Mbps up, unlimited traffic, a minimum guaranteed bandwidth of 5 Mbps, no fixed phone-line requirement, free antenna loan, promotional free activation and standard installation, and a EUR 25.90 monthly charge with bimonthly advance billing. The same page lists optional add-ons: a public static IP at EUR 5.00 per month, router rental at EUR 1.50 per month, on-site antenna assistance from EUR 50.00 depending on geography, and VoIP number portability with a EUR 59 adapter.

The business Fibra-Radio 100 offer is similar but aimed at VAT-number customers. It prices the base plan at EUR 25.90 plus VAT, keeps the 100/30 Mbps headline, and adds business-relevant options such as speed upgrades up to 2 Gbps symmetric by quotation, public static IP, hotspot service, and VoIP. The dedicated Ponte Radio FWA page extends the same radio idea to events, building sites, photovoltaic monitoring, video broadcast and alarm or CCTV systems, with up to 2 Gbps symmetric by quotation and minimum guaranteed bandwidth to be agreed.

The FTTH side is not a separate thesis. It is the hedge. The FTTH page says aFibra has an Open Stream arrangement with Open Fiber and offers up to 1 Gbps down and 300 Mbps up, unlimited use, a EUR 29.90 monthly charge, promotional free activation instead of EUR 59, a Wi-Fi 6 router in free loan, and a free FWA backup service with a one-time backup installation cost unless the customer is already an AntennADSL customer. That bundle changes the economics of the local ISP. Where fibre reaches the premise, the company can keep a customer by reselling or integrating FTTH instead of defending radio as the only answer. Where fibre does not reach, radio remains the main product.

The regulatory documents make the public offer more concrete than a marketing page alone. The tariff transparency page points to current AGCOM-format offer sheets. The 2025 New Fibra-Radio 100 sheet identifies Foxtel SRL as the operator, marks the offer as subscribable from 1 July 2025, lists FWA as the technology, states the geographic reference as Lazio provinces VT, RI and RM, Tuscany province GR, and Umbria provinces PG and TR, and records a EUR 25.90 monthly flat charge with a 24-month minimum term and EUR 119 deactivation cost. The FTTH 1 Giga Promo sheet lists the same regional scope, FTTH technology, 1000/300 Mbps speeds, EUR 29.90 monthly flat charge, and the same 24-month minimum term and deactivation charge.

That is enough to treat Foxtel as an operating regional ISP. It is not enough to infer profitability. A EUR 25.90 FWA household account has to pay for base-station sites, spectrum-compatible equipment, backhaul, power, monitoring, installers, customer support, replacement antennas, billing, payment costs and upstream internet. A EUR 29.90 FTTH account has a different cost stack: wholesale access, customer acquisition, router support, fault handling and churn against larger retail brands. The public evidence tells us the product exists and is currently marketed.

It does not disclose take-up by commune, utilization by site, wholesale terms, churn, gross margin or average repair cost.

Why sixty radio sites can be cheaper than one fibre trench

The radio proposition is easiest to understand by looking at what it avoids. A fibre line to a remote premise often requires civil works, ducts, permits, subcontractor scheduling and a network owner willing to invest before the household has proven it will subscribe. The more scattered the homes, the weaker the trench economics become. A radio network can use one elevated site to reach many premises that have line of sight. A customer installation becomes a roof or balcony antenna, a cable run and a router, rather than a civil-work project.

aFibra states on its FWA pages that standard installation includes mounting an antenna in free loan, using a balcony or pre-existing pole on the roof, up to 20 metres of cable with an airborne route to the router, and a maximum two-hour work time. The fine print matters. Extra cable, brackets, antenna poles, wall drilling or cable ducting can raise the price. The FAQ says coverage checks through maps are approximate; obstacles such as a neighbour's tree may prevent installation, and the contract is signed only after a successful installation.

That is a more honest description of FWA economics than a simple "available everywhere" claim. The radio network lowers the probability that every customer requires trenching, but it replaces trench risk with line-of-sight risk and field-labour risk.

The margin map begins with the first visit. A national fibre order can be expensive to provision, but once a line is lit the operator's incremental support problem is often a router, an optical network terminal, a wholesale ticket or a billing issue. A WISP has a different first-cost profile. The customer premise equipment must be mounted and aligned. The installer must assess line of sight, roof safety, cable route, customer Wi-Fi placement and whether a neighbour's roof, tree or hill blocks the signal. If the install fails, the company may have spent staff time without creating a paying line.

If the install succeeds but later needs re-aiming after wind, vegetation growth or building work, the account can require more field attention than a fibre line at the same price.

That does not make the model unattractive. It means density has to be understood differently. Fibre density is about premises per metre of civil works, cabinets, ducts and splitter reach. FWA density is about usable premises per radio site, spectrum reuse, clear paths, sector loading, backhaul capacity, technician travel routes and the share of customers that can be installed under the standard two-hour assumption. A site that covers many visible roofs can be powerful. A site that sees mostly trees, valleys and low-demand second homes may create a wider marketing footprint than paying capacity.

The more than 60-site claim is therefore strategically meaningful but economically incomplete. It suggests a real attempt to move the radio network closer to customers. It does not disclose whether each site is a high-yield node, a coverage filler, a backhaul relay or a maintenance liability.

The cost base also changes by customer type. A household that only needs streaming, schoolwork and basic remote work may tolerate normally available FWA speeds if the line is stable and the support channel answers quickly. A small business with payment terminals, cloud accounting, CCTV, booking systems or VoIP may care less about a low headline price and more about predictable upload, public IP, backup and fault response. The business pages leave room for quoted upgrades, static IP and hotspot services, which can lift average revenue if sold carefully. The same extras can also raise support complexity.

A static IP customer may run services that expose routing or firewall questions. A hotspot customer may need log retention and access-point support. A video-surveillance or photovoltaic-monitoring customer may care about low-data but high-continuity operation. Each extra product can improve margin only if the operator can standardise delivery and avoid bespoke support swallowing the premium.

Power and backhaul are quiet but central. The public pages make the radio access layer visible, while the economics depend on what sits behind each mast. A base station needs site rights, equipment, power, protection from weather, monitoring, and enough backhaul to avoid moving congestion from the last mile to the upstream link. The presence of AS56754 and the Namex Rome port shows Foxtel has an internet-routing footprint, but it does not map the private transport network from each radio site to the internet edge. For a regional ISP, that hidden middle mile is often where economics are made or lost.

Good sites need affordable backhaul; weak sites need too much maintenance per subscriber; oversold sites create support calls; underused sites trap capital.

This is why aFibra's mixed radio and fibre strategy is more credible than a pure anti-fibre posture. If fibre arrives in the dense part of a town, the local operator can use FTTH to keep or win accounts there, while preserving radio for scattered premises, temporary sites, farms, edge businesses and backup. If it defended radio against fibre in every case, it would risk becoming the slower option as soon as wholesale FTTH became orderable. If it abandoned radio for resale fibre, it would lose the local differentiator that originally solved the address gap.

The economic discipline is to place each technology where it has the best cost-to-service fit.

The technical page also shows why the article should not treat "up to 100 Mbps" as a delivered-speed guarantee. aFibra's technical transparency page links to the Fibra-Radio 100 fixed-service quality sheet. That sheet lists FWA as the access technology, minimum speeds of 5 Mbps down and 1 Mbps up, normally available speeds of 30 Mbps down and 15 Mbps up, advertised speeds of 100 Mbps down and 30 Mbps up, maximum packet loss of 2 percent, and no IPv6 service. It also directs customers to AGCOM's Ne.Me.Sys measurement process. The headline plan is therefore not a symmetrical fibre product. It is an access service whose performance depends on radio quality, site load, backhaul, local installation quality and customer equipment.

The company's own FAQ names the risk. It says effective speed depends on factors such as distance from the antenna. It says slowdowns can come from user traffic congestion and from weather conditions such as heavy rain, snow, dense low cloud and wind-driven antenna movement. It also says a remote-control system notifies the company when a customer loses the radio link. That mix is important: radio gives the operator faster coverage and lower civil-work exposure, but it creates a support promise that has to be met premise by premise.

This is why local support labour is not a soft topic. It is part of the product. aFibra's contact page gives email, phone and WhatsApp channels for technical or commercial questions. The reseller page lists Foxtel in Viterbo plus partner locations in Rome, Vetralla, Campagnano, Ronciglione, Massa Martana, Castiglione in Teverina, Orte, Narni and Viterbo, and says the partner network includes resellers and certified installers across Lazio, Umbria and Tuscany. The partner recruitment page seeks commercial consultants, resellers and installer technicians. The jobs page lists roles such as RF planning and technician installer. For a national ISP those details would be small. For a WISP, they are the operating surface.

Network-resource evidence: real, current, but not a speed test

Foxtel's public network evidence is stronger than a directory listing or stale IP allocation. RIPE identifies AS56754 as FoxtelAS for Foxtel Srl, with the organisation record ORG-FS47-RIPE carrying the company's Italian registration number and Viterbo address. RIPEstat's announced-prefixes call on 10 July 2026 showed six visible IPv4 prefixes announced by AS56754 for the 26 June to 10 July window: 91.227.109.0/24, 94.176.184.0/23, 185.139.104.0/22, and 185.246.92.0/24 through 185.246.94.0/24. RIPEstat's route-consistency data also showed those prefixes in BGP and in Whois, while an IPv6 allocation was in Whois but not visible in BGP.

PeeringDB adds an interconnection layer. The Foxtel s.r.l. network page lists AS56754 as a Cable/DSL/ISP network with traffic of 5-10 Gbps, balanced traffic ratios, European scope, open peering policy and a public exchange point at Namex Rome. The PeeringDB API for the netixlan record shows an operational 10G Namex Rome VLAN peering port with IPv4 address 193.201.28.135 and IPv6 address 2001:7f8:10::5:6754. Independent BGP views such as bgp.tools also describe AS56754 as active, show originated IPv4 prefixes, and identify Fastweb as an upstream.

This is current operating evidence. It supports the Network-resource evidence topic because the ISP offer is tied to visible routing and interconnection. But it should be read with the right limit. BGP proves that Foxtel operates or controls routed internet resources visible to the global table. It does not prove which customer is behind a particular antenna, whether a given customer receives 30 Mbps at peak time, whether the 60-site coverage claim is enough in a storm, or whether there is spare backhaul capacity on a specific hilltop. Network-resource evidence is a floor for credibility, not a customer-outcome audit.

The AS56754 profile does, however, reveal strategic dependence. If the route data and bgp.tools view identify a narrow upstream set, the company must keep upstream and IX economics stable while selling cheap local access. If it uses Open Fiber for FTTH, it must also manage another dependency: the wholesale access network. Its own FTTH technical documentation links to Open Fiber's Open Internet parameters, which list Open Fiber reference values such as 980/280 Mbps maximum for 1 Gbps profiles, 600/100 Mbps normally available, 100/12 Mbps minimum, 50 ms maximum delay, 0.1 percent packet loss, private dynamic IPv4 with CGNAT or static public IPv4, and globally routable IPv6 prefix delegation. That is a different operating model from radio. Foxtel can control the local customer relationship, but it cannot make Open Fiber's civil works, provisioning or wholesale fault handling disappear.

The price umbrella is narrow

aFibra's base residential FWA price, EUR 25.90 per month, is not an obvious premium product. It sits in a crowded Italian price band. TIM's current WiFi Casa page advertises fibre up to 2.5 Gbps and modem with a headline EUR 29.90 monthly price, or EUR 24.90 for TIM mobile customers under a promotion, with coverage and technical limits. Fastweb's home internet page lists Casa Start from EUR 27.95 per month, discounted to EUR 23.95 for mobile customers, and FWA Light from EUR 25.95. Vodafone's home page shows a fixed-plus-mobile bundle at EUR 23.95 per month for the fixed component when a SIM is also activated, with free activation and no permanence bond. WINDTRE's Super Fibra sits in the same national discounting environment.

EOLO is the most direct FWA benchmark because it is a national rural wireless specialist. Its EOLO Casa page describes FWA up to 100 Mbps down and 20 Mbps up, router included, a promotional EUR 19.90 for the first 12 months and then EUR 24.90. Its Viterbo coverage page shows the same base plan and also offers higher FWA profiles and FTTH products where available. EOLO's brand, scale and support hours give it a national alternative-network profile that a local WISP has to answer with proximity and address-specific knowledge.

Mobile broadband and 5G FWA add another substitute. TIM's page includes a 5G FWA waiting or second-address product and says it uses fibre to the radio base station with the final segment on the 5G network. Vodafone and Fastweb also market wireless or backup variants. Starlink adds a satellite outside option for remote houses that can accept hardware, sky-view and latency tradeoffs; current non-affiliated price trackers such as Starlink Prices list Italy at around EUR 40 per month with a hardware kit price, while older industry reporting from thinkbroadband described a lower deprioritised plan. Because Starlink checkout prices and plan names change, the safe conclusion is not a precise price point. It is that satellite now sits close enough to rural fixed broadband to discipline weak local offers in some homes.

The national policy environment narrows the window further. AGCOM's Osservatorio sulle comunicazioni n.1-2026 says Italian fixed accesses were around 20.53 million at December 2025, FTTH represented 34.1 percent of total fixed access, FWA reached around 2.68 million accesses, and smaller operators represented around 9.8 percent of broadband and ultrabroadband lines. It also says the share of lines marketed at 100 Mbps or more rose from 61.7 percent in December 2021 to 83.9 percent in December 2025, while lines marketed at 1 Gbps or more rose from 12.6 percent to 35.9 percent. The European Commission's Italy digital connectivity page describes Italy's 1 Giga plan and the 2023-2026 ultra-broadband strategy, including the objective of 1 Gbps fixed coverage for all civic numbers and FWA coverage of at least 100 Mbps in the most remote areas.

That makes aFibra's problem more precise. The company is not selling "internet where nobody else will ever go." It is selling a practical local answer during a transition in which Open Fiber, FiberCop, EOLO, mobile operators and satellite are all expanding address eligibility. The defensible account is one where the customer values local installation, quick coverage checks, radio knowledge, continuity, optional FTTH migration, static IP, VoIP, and a person who understands why the roof line matters.

FTTH resale changes the WISP story

The old WISP story was simple: radio exists because fibre does not. aFibra's current posture is less simple and more realistic. It advertises radio and fibre side by side. Open Fiber's mission page describes a wholesale-only FTTH model designed to give operators equal access and expand choice. Open Fiber's home page says, with data updated 30 April 2026, that its network served 4.28 million customers, covered 6.34 thousand FTTH municipalities, reached 17.428 million connected property units, and spanned 168.037 thousand kilometres of infrastructure. aFibra's FTTH page places the local brand on that wholesale network.

For Foxtel, this can be defensive and offensive at the same time. Defensive, because the company can keep a customer whose address finally becomes FTTH eligible instead of watching the household leave for a national retailer. Offensive, because a local ISP can use existing customer trust and installer presence to sell fibre where national brands feel impersonal. The backup-FWA line on the FTTH offer is especially revealing. It tells a customer that radio is not obsolete just because fibre arrives. It can become redundancy, continuity or a second path for a customer that needs uptime more than a single headline speed.

The risk is that the economics are thinner. FTTH resale through a wholesale network rarely gives a small retailer the same infrastructure leverage it has on its own radio grid. The customer pays a national-market price. The operator has to pay wholesale fees, support the router, manage billing, handle faults, and compete with national promotional bundles. The margin may be acceptable when it protects an existing customer or gives aFibra a broader local bundle. It is less obvious that FTTH resale alone can fund the radio network.

The more likely model is a portfolio: radio where address density and line of sight fit, FTTH where wholesale access exists, and higher-touch business or event radio where customers pay for speed of activation and support.

The operating surface: weather, congestion, field work and expectations

The company's public documents point to the risks an investor or competitor should watch. The first is coverage versus capacity. A coverage page and 60-plus structures do not show how many customers can be served at peak time, how much spectrum reuse is available, how each site is backhauled, or how many premises are blocked by terrain and vegetation. aFibra's own FAQ says slowdowns can come from congestion and weather, and its FWA offer says effective speed is tied to capacity and congestion. That candour is useful, but it also prevents overclaiming.

The second risk is installation variance. Standard installation is narrow: antenna, pre-existing mounting point, up to 20 metres of cable, and no more than two hours. Rural houses often have non-standard roofs, longer cable paths, trees, stone walls, protected facades and neighbour permissions. Trustpilot's small review set is positive overall, with 19 reviews and a 4.6 score, but Trustpilot itself says the company has not sent recent review invitations and reviews may not be representative. The reviews are useful as market signals around support and installation, not as proof of service quality across the footprint.

The third risk is support cost. A national fibre retailer can spread call-centre and truck-roll systems across millions of lines. A local WISP's promise is that it knows the hill, the installer and the customer. That can win accounts, but it can also raise cost when storms, power, trees, antenna alignment or customer Wi-Fi problems trigger field response. aFibra's optional on-site assistance pricing, partner pages and installer recruitment all point to the same truth: support is labour, and labour has geography.

The fourth risk is technology substitution. 60 GHz links can offer high throughput but are sensitive to line of sight and atmospheric attenuation; 5 GHz can reach farther but is more exposed to interference and contention. National 5G FWA uses licensed mobile spectrum and large balance sheets, but it may be less customised at a specific rural premise. Fibre is more durable once installed, but address availability and civil works can lag. Satellite can bypass terrain but adds hardware, sky view and network-capacity constraints.

aFibra's best account is the one where those tradeoffs are explained clearly before installation, not discovered only after a customer has churned.

The fifth risk is customer expectation. The gap between advertised maximum speed and normally available speed is public in the technical sheet. For a family moving from unstable ADSL, 30 Mbps normally available can be a large improvement. For a business comparing against symmetric fibre or a 5G FWA marketing claim, the same number can feel weak. The company has to segment. A low-price household FWA account, a VAT-number business account, a quoted dedicated radio bridge, a VoIP line, and an FTTH account should not be judged by the same service promise.

Why this company remains worth watching

Foxtel s.r.l. is small enough that it can be missed in national broadband narratives and visible enough in network data to be tested. Its website footer gives the Viterbo address, VAT number 01985290566 and ROC number 30270. RIPE records connect the company to AS56754 and current route objects. PeeringDB shows an operational Namex Rome presence. The aFibra pages show the paid access account, the local installation process, and the support channels. Company and LinkedIn pages add another dimension: Foxtel's broadcast-equipment and R&D profile is not the same as a pure reseller.

It has a technical identity that plausibly matters in radio planning and field equipment, even though public sources do not let us measure how much of that engineering translates into ISP margin.

The judgement is therefore balanced. aFibra is not a speculative shell built on a stale ASN. It is an operating local access provider with current offers, current network evidence and a clear geographic thesis. It also is not proven to have fibre-like capacity across its whole stated footprint. The 60-site claim matters because it tells us the company has tried to densify radio coverage in central Italy. It does not tell us whether a particular household in Tuscia, the Maremma edge or inland Umbria can get the plan, whether evening throughput is stable, or whether the price covers the full cost of maintenance.

What would change the judgement

Several facts would strengthen the case materially. The first would be address-level availability evidence from multiple points across the claimed footprint, especially in the provinces named in the tariff sheets. A coverage form is necessary, but a research judgement improves when a sample of real addresses shows which technology is offered, whether installation dates are near term, and whether the customer is steered to radio, FTTH or no service. That would separate the marketed footprint from the economically serviceable footprint.

The second would be time-series network evidence. A single RIPEstat window shows current announcements; it does not show how stable the route origin, upstream mix, packet loss or IX reachability has been across seasons. For an FWA operator, seasonality matters because vegetation, storms, holiday-home usage and summer tourism can change both radio paths and demand. Repeated views of prefix visibility, latency from Italian probes, route changes and Namex utilisation would not prove customer experience, but they would make the network-resource evidence more operational.

The third would be clearer business mix. The public pages show residential, VAT-number, dedicated radio, FTTH and VoIP products. They do not reveal whether most revenue comes from low-price households, business accounts, custom links, broadcast technology, public-sector work, reseller commissions or a mixture. That matters because each line has different resilience. A base of low-price households is sensitive to national promotional offers. A base of businesses paying for static IP, backup, hotspot or monitoring can support more local labour.

Broadcast-equipment revenue could fund technical capability, but it may also distract from access-network scale. Public accounts, tender records or management disclosures would help, but absent those records the article keeps the economic judgement bounded.

The fourth would be fault-response evidence. aFibra's public and LinkedIn pages suggest local support, fast activation and short fault-response aspirations. Trustpilot comments and embedded Google-style review snippets are encouraging but small and self-selecting. A stronger proof would be published service-quality indicators, complaint rates, average repair time, or a transparent customer-support report. That is especially important because local support is part of the competitive thesis.

If the local operator answers quickly and fixes roof-radio problems faster than a national provider can schedule a technician, the support premium is real. If support quality is uneven, the local brand loses one of its main reasons to exist.

The fifth would be fibre-transition evidence. The long-term question is not whether aFibra can install radio in places without fibre. The harder question is whether it can retain customers as FTTH expands. Evidence of successful migration from radio to aFibra FTTH, take-up of FWA backup on fibre accounts, or bundled business continuity packages would show that the company is managing technology substitution rather than being eroded by it. Without that evidence, the safer view is that FTTH resale is a credible hedge but not a proven growth engine.

Facts could also weaken the judgement. If route visibility deteriorated, if the PeeringDB profile became stale or the Namex port disappeared, network-resource confidence would fall. If tariff documents stopped being updated or support pages went quiet, current operating evidence would need to be downgraded. If customer reviews began consistently naming congestion, missed appointments or unresolved faults, the local-support thesis would weaken.

If Open Fiber and national retailers reached most of the same addresses with cheaper or faster service, aFibra's radio footprint would have to shift toward niche backup, temporary links and hard-to-serve premises rather than broad household access.

For readers, the most useful way to understand the company is to follow the paid unit: a monthly household or business access account that may start as FWA, move to FTTH, add VoIP, need a static IP, or require a dedicated radio bridge. The account is valuable when it solves a real local constraint faster than a national fibre order and with more accountability than a mobile or satellite substitute. The account is fragile when national networks become available at the same address with better speed, lower support cost and similar price.

The practical buyer test is therefore simple but strict. Ask whether the address can be served today, which technology will be installed, what the normally available speed is, what the total installation path requires, who owns the customer equipment, what happens if line of sight fails, what the exit cost is, whether a public IP or VoIP line is needed, and how support is reached when the problem is on the roof rather than inside the router. Those questions turn a marketing claim into an operating account.

They also show why local providers survive even while national fibre expands: some addresses still need someone who can judge the actual place, not only the database record.

That is why the headline is deliberately about competition with the fibre trench, not victory over it. Foxtel's aFibra brand does not have to beat FTTH everywhere to remain relevant. It has to win enough addresses where trench density is poor, installer knowledge is valuable, local support reduces downtime, and the customer's real choice is not "gigabit fibre versus radio" but "which operator can make this specific place work this month?" In central Italy, that is still a real market.