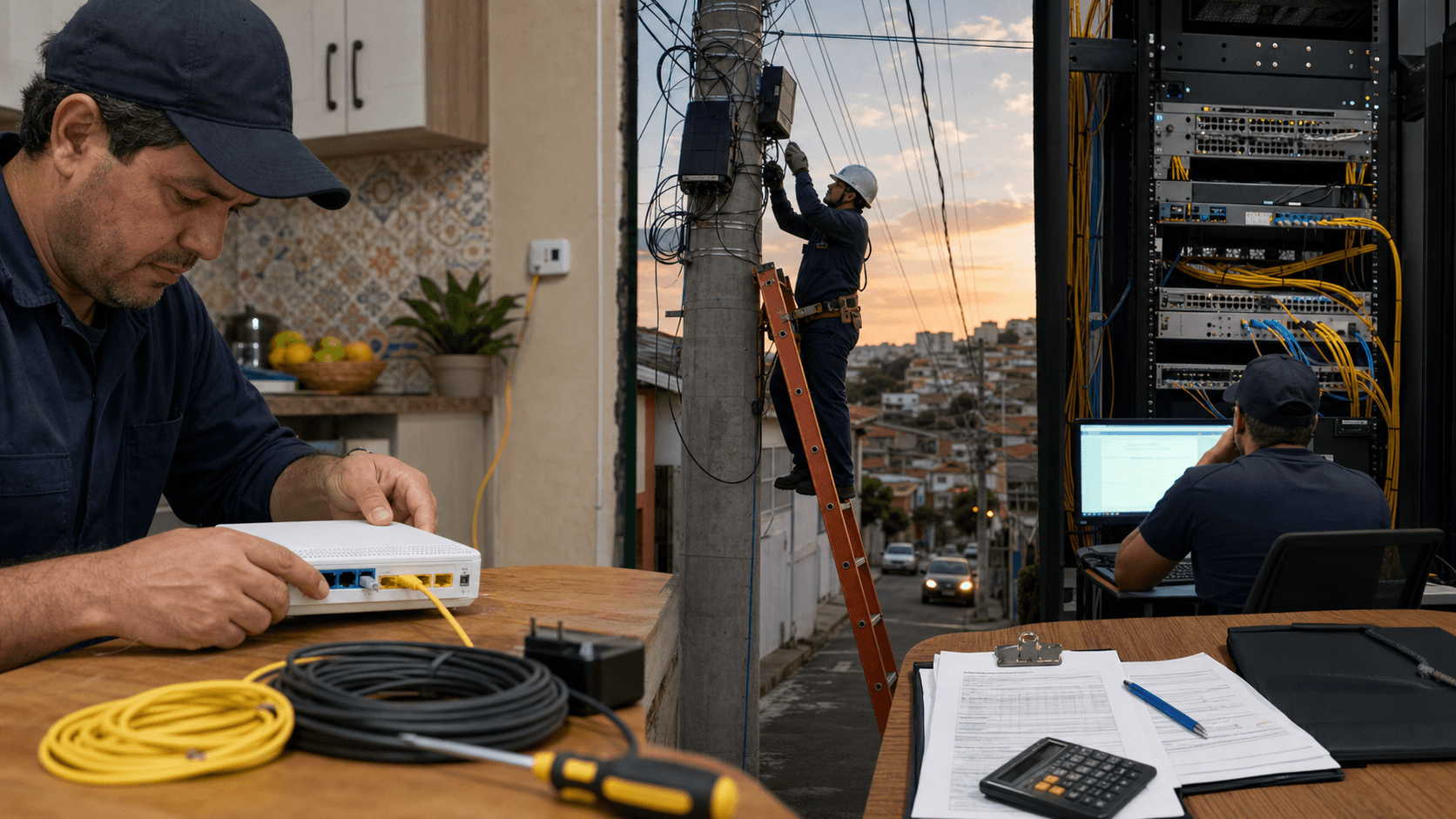

The second support visit is where the cheap-margin story in Brazilian connectivity starts to come apart. The first visit is the one everyone models: a cabinet is placed, a server is racked, a fibre cross-connect is patched, a private network is lit, a cloud tenant is moved out of a dollar-priced hyperscaler, or a streaming client is put on a higher-capacity server. The second visit is different. It happens when the customer has already signed, the monthly price has already been negotiated in reais, and the provider now has to send a technician, open a ticket, swap a disk, trace latency, prove that a packet loss complaint is upstream rather than local, explain a backup failure, or walk a customer through the difference between an application problem and an infrastructure problem. Under Servicos de Internet Ltda is interesting because its public evidence shows a company built around that second visit, not just the first sale: its site sells 24x7 support with first response in up to 15 minutes, certified data centers, 10Gbps server connectivity, real-denominated monthly billing, and managed infrastructure rather than a bare commodity link (https://under.com.br/).

That makes Under a better lens for the payback clock than a generic fibre-overbuild story. The public brand, Under, is not simply promising a home broadband line. It is selling enterprise infrastructure in Brazil: bare metal, public and private cloud, cloud database, colocation, storage, firewall, backup, secondary links, GPU servers, and managed services. Its product map is visible across the main site and service pages, and the company frames the economic proposition around high performance, support, local billing and operational control rather than a mass-market tariff (https://under.com.br/servidor-dedicado/). The reason this matters is that the network payback problem is the same in a different form. After a provider has paid for compute, racks, power, cooling, IP transit, IX capacity, hardware spares, software tooling, monitoring and human support, the margin depends on keeping repeat interventions low enough that monthly recurring revenue can amortize the installed base.

The company-specific evidence appears quickly. Registro.br RDAP lists AS28209 as a direct allocation in Brazil, links it to Under Servicos de Internet Ltda and CNPJ 05.501.732/0001-89, and shows related address blocks including 189.113.0.0/20, 177.70.0.0/19, 2804:1070::/32 and 179.127.0.0/19 (https://rdap.registro.br/autnum/28209). RIPEstat's routing status for AS28209 on 2026-07-04 shows the network visible to 325 of 325 IPv4 RIS peers and 320 of 321 IPv6 RIS peers, with 41 IPv4 prefixes, 20,736 IPv4 addresses, seven IPv6 prefixes and 31 observed neighbours (https://stat.ripe.net/data/routing-status/data.json?resource=AS28209). PeeringDB lists Under as an enterprise and content network with heavy outbound traffic, 100 IPv4 prefixes, 10 IPv6 prefixes, South America scope, open peering policy and a presence at IX.br Sao Paulo (https://www.peeringdb.com/net/5932). Those are not the signals of a marketing-only hoster. They are the signals of a real routing estate whose economics are shaped by interconnection, traffic mix and support quality.

The public peering picture sharpens the margin story. PeeringDB's API lists four operational IX.br Sao Paulo ports for AS28209: two 100Gbps entries and two 20Gbps entries, all with IPv4 and IPv6 addresses on IX.br's Sao Paulo exchange fabric (https://www.peeringdb.com/api/netixlan?asn=28209). Hurricane Electric's BGP page shows Under's aut-num as importing from large transit and content networks including AS174, AS3356, AS6939, Google, Microsoft, Meta, Amazon, Cloudflare, Akamai and others, and it adds a terse but revealing remark: "Bare Metal Cloud" (https://bgp.he.net/AS28209). BGP.Tools says AS28209 was registered on 8 May 2008 and identifies Under's website, prefixes and IX presence (https://bgp.tools/as/28209). The machine beneath the brand is therefore not a speculative assumption. It is the core of the business model: a Brazilian infrastructure provider using local data-center capacity, public internet-number resources, IX.br, transit and managed support to turn a fixed asset base into monthly recurring enterprise demand.

The opening economic judgment is that Under's upside comes from keeping customers close enough to price in service and latency, but standardized enough that every account does not become a bespoke engineering project. Under's own history page says it has more than 20 years of experience in data centers and cloud computing, two Tier 3 data centers in Sao Paulo state, minimum availability of 99.982%, N+1 redundancy for critical components, controlled 24-hour access, anti-fire protection, anti-DDoS, support within 15 minutes, payment in reais and service zones in Cotia and Barueri (https://under.com.br/sobre-a-under/). A third-party industry note from Abracloud says Under was founded in 2003, is based in Sao Paulo, has two Tier 3 certified data centers in the city area, and serves more than 750 companies and organizations across Brazil with dedicated servers, cloud servers and colocation (https://abracloud.com.br/under-investe-na-oferta-de-backup-da-nuvem-em-servidores-dedicados/). The revenue promise is not "we can install fibre cheaply." It is "we can absorb the second, third and tenth operational call at a price below the customer's alternative."

That promise is harder than it looks. Under's product pages sell a mix of fixed-capacity and managed-risk features: internal VLANs up to 10Gbps inside the same data center or up to 1Gbps between Under data centers, 10TB of free data transfer for interlinked services, hot-swap disks, remote KVM over IP, VPN out-of-band administration and monthly server prices in reais without exchange-rate variation (https://under.com.br/servidor-dedicado/). Its colocation page offers remote hands, installation and cabling by Under, NOC hardware monitoring without extra cost, redundant internet, 24x7 monitoring, 1Gbps anti-DDoS included and expandable to 10Gbps, redundant power and Tier 3 Brazilian data-center hosting (https://under.com.br/colocation/). The buyer hears reliability. The operator hears labor, replacement inventory, energy exposure, vendor dependence, ticket queues and the constant risk that a "managed" promise becomes an unpriced consulting retainer.

The first hard fact about Under, then, is identity. The public legal and internet-number evidence points to a Brazilian company whose CNPJ record has been visible since 2003 and whose principal activity is data processing, application service provision and internet hosting. CNPJ.biz lists Under Servicos de Internet Ltda under CNPJ 05.501.732/0001-89, founded on 28 January 2003, active, in Sao Paulo, with Receita Federal activity 63.11-9-00 for data processing, application service providers and internet hosting (https://cnpj.biz/05501732000189). Econodata's page for an older TeHospedo branch shows the same legal name and business line and records the TeHospedo trading name for a Sao Paulo branch that opened in 2007 and was later closed, while its branch table lists active related units in Sao Paulo, Barueri, Cotia and Porto Alegre (https://www.econodata.com.br/consulta-empresa/05501732000260-under-servicos-de-internet-ltda). The company itself says the business began in 2003 as a hosting company under TeHospedo and Revenderia, with servers abroad, before moving into the larger data-center and managed-hosting business now visible in its portfolio (https://under.com.br/sobre-a-under/).

The second hard fact is that Under has enough network surface to make routing and interconnection part of its economics. IPinfo lists AS28209 with address blocks including 177.70.0.0/19, 189.113.0.0/20 and multiple smaller routed networks, and identifies the autonomous system as Under Servicos de Internet Ltda in Brazil (https://ipinfo.io/AS28209). RIPEstat's announced-prefixes call shows many of those prefixes visible through June and early July 2026, including 177.70.0.0/19, 189.113.0.0/20, 2804:1070::/32 and multiple more-specific routes (https://stat.ripe.net/data/announced-prefixes/data.json?resource=AS28209). This matters commercially because a provider with its own ASN and address space is not merely reselling a server in someone else's cloud. It can engineer routes, peer locally, advertise customer or service networks, optimize traffic exchange and build a differentiated latency story for Brazilian workloads. It also carries the reputational cost of routing errors, abuse reports, traffic imbalances and customer-visible outages.

The third fact is that Under sits in a Brazilian broadband and infrastructure market whose economics reward regional operators but punish weak operations. Anatel's 2025 publication on small broadband providers says Prestadoras de Pequeno Porte, or PPPs, play a fundamental role in Brazil's fixed broadband market, with consolidated results close to or sometimes above incumbents in the fourth quarter of 2024 (https://www.gov.br/anatel/pt-br/assuntos/noticias/anatel-divulga-panorama-economico-financeiro-das-prestadoras-de-pequeno-porte-ppps-no-mercado-de-banda-larga). Teletime's report on the same Anatel balance says PPPs invested R$2.4 billion in broadband capex in the fourth quarter of 2024, versus R$1.2 billion by larger operators, representing 66% of broadband investment in that quarter (https://teletime.com.br/13/10/2025/ppps-investem-o-dobro-das-grandes-operadoras-em-banda-larga/). TeleSintese, citing Anatel, reported that Brazil ended 2025 with about 53.9 million fixed broadband accesses, fibre at about 79% of connections, and regional operators collectively above 56% of the market (https://telesintese.com.br/quem-lidera-a-banda-larga-no-brasil-segundo-a-anatel/). Under is not a classic neighbourhood FTTH roll-up in the public record, but it benefits from the same national pattern: demand has moved toward local fibre, local hosting, local service levels and regional alternatives to incumbents and dollar-priced global clouds.

Under's business model looks like a deliberate move up the value chain from access to controlled infrastructure. The company's home page sells "bare metal, cloud and colocation" to push businesses, not consumer broadband bundles (https://under.com.br/). Its managed colocation page says Under combines enterprise components and connectivity with major internet providers in Brazil, while supplying remote hands, monitoring and installation rather than leaving the customer alone with a rack contract (https://under.com.br/colocation/). Its cloud and storage pages add public cloud, private cloud, database, S3-compatible object storage, firewall, backup and secondary-link products (https://under.com.br/object-storage-por-capacidade/). That portfolio changes the payback math. A fibre ISP recovers a drop cable and ONU through monthly access fees. Under recovers racks, servers, storage arrays, network ports, people, vendor contracts and data-center capacity through layered revenue per customer.

The mechanism is visible in Under's customer cases. The Brasil Stream case says the customer used dedicated servers in Under's data centers to support streaming and CDN demand, moved from older foreign providers with narrower capacity and high latency, and scaled from 1Gbps with previous suppliers to 30Gbps with Under, using 10Gbps servers and 500TB of traffic (https://under.com.br/case-de-sucesso/brasil-stream/). The Vetor Inteligencia case says a backup-services customer moved infrastructure to Under, reducing infrastructure cost from 40% to less than 10% of revenue, gaining two Tier 3 data centers in Brazil, and targeting recovery of data in up to 15 minutes (https://under.com.br/case-de-sucesso/case-vetor-inteligencia/). The Todeschini case says Under hosts and secures institutional sites for a Brazilian furniture group (https://under.com.br/case-de-sucesso/todeschini/). The SQG case says performance, support and financial conditions were major differentiators, with backup added as another solution (https://under.com.br/case-de-sucesso/sqg-solucoes/). These are sales materials, so they are not neutral evidence of margin. They are useful because they reveal the product wedge: a local Brazilian infrastructure provider sells reduced latency, real-denominated cost visibility, managed support and enough network capacity to keep mid-market workloads off foreign or generic platforms.

The revenue logic is therefore more subtle than "more customers equals more profit." In infrastructure hosting, customers with steady workloads, predictable traffic and self-sufficient technical teams can be excellent annuity accounts. Customers that require constant intervention can destroy the economics even if monthly invoices look healthy. Under's own pages sell fast support, NOC monitoring, remote hands and managed operations; those features are necessary to win customers, but they make the second support visit a cost line rather than an exception (https://under.com.br/colocation/). A customer who buys a low-priced dedicated server and then opens repeated tickets for application tuning, spam complaints, disk usage, database locks, backup verification or firewall rules can consume the margin intended to amortize hardware. The company's challenge is to segment: sell enough management to command a premium, define enough responsibility boundaries to prevent unlimited labor leakage, and standardize enough service components that each account does not require a new architecture.

Under's pricing language shows one answer: make the local-currency guarantee a selling point. The dedicated-server page says customers hire servers with prices in reais, so the monthly payment does not change when the dollar moves and customers avoid foreign transaction taxes (https://under.com.br/servidor-dedicado/). A 2026 Under blog post makes the same argument more explicitly: local infrastructure can protect Brazilian IT budgets from dollar volatility, avoid variable egress and IOPS charges, and turn heavy capex into fixed monthly opex (https://under.com.br/dolar-alto-3-formas-de-proteger-seu-orcamento-de-ti-hoje/). This is a real commercial wedge in Brazil. A customer comparing Under with AWS, Azure or Google Cloud is not only comparing CPU and RAM. It is comparing exchange-rate risk, billing surprise, support language, data-residency comfort, latency to Brazilian users, and whether someone will pick up the phone when a service goes down.

But that same local-currency promise moves risk from the customer to the provider. Servers, network gear, optics, storage, GPUs, batteries, cooling hardware, many software licenses and spares are exposed directly or indirectly to global technology pricing. A provider that invoices in reais and promises no exchange-rate variation must either hedge, hold margin, buy inventory carefully or accept that hardware replacement cycles can squeeze returns. Under's product pages are heavy with hardware-dependent promises: hot-swap disks, Secure Console, VLANs, dedicated GPU servers, storage, cloud database, private cloud, and data-center redundancy (https://under.com.br/servidores-dedicados-gpu/). If replacement hardware becomes more expensive while contracts remain fixed, the payback clock lengthens. If equipment fails earlier than expected, the second support visit becomes a capital event as well as a labor event.

This is where Under's shift toward higher-value workloads may be rational. Its 2025 press item says CEO Roberto Berto wants Under to focus on infrastructure for artificial-intelligence workloads in Brazil, including dedicated GPU hardware, compliance-sensitive processing and advice on matching hardware to models and use cases (https://under.com.br/under-vai-se-dedicar-a-oferta-de-infraestrutura-para-ia-no-brasil/). That pitch is not simply fashionable. GPU and private-infrastructure workloads can carry higher revenue per rack unit than generic shared hosting if the provider can source hardware, cool it, power it and keep utilization high. The risk is also higher: GPUs are expensive, obsolescence is fast, energy density rises, and customers may want cloud-like flexibility without cloud-like pricing. If Under can sell dedicated inference and private infrastructure as a Brazilian compliance and budget-control product, the margin pool improves. If demand comes in bursts and hardware sits idle, the payback clock becomes harsher than in ordinary dedicated servers.

The cost base starts with data-center capacity. Under says it operates two Tier 3 data centers in Sao Paulo state, with Cotia and Barueri service zones, minimum 99.982% availability, N+1 redundancy for critical components, controlled 24-hour access, anti-fire protection and anti-DDoS (https://under.com.br/sobre-a-under/). Its status page publicly tracks components including interconnection between SP1 and SP2, Datacenter SP2, Datacenter SP1, ACS Apache CloudStack, telephone center, Freshservice tickets, Under Control and VPN management console, and at the time viewed showed those components operational with 100% availability over the previous seven days (https://status.under.com.br/). A status page does not prove long-term uptime, but it proves something about the operating model: the company is packaging infrastructure as a monitored service with customer-facing transparency. That transparency creates trust; it also creates a visible standard against which customers can judge every incident.

Power, cooling and property constraints matter because data centers are physical businesses pretending to be software businesses. The public sources do not disclose Under's energy contracts, rack utilization, power density, cooling architecture or capex by site. The observable product promises still let us infer the pressure points. Tier 3 redundancy means duplicated or standby components. Remote hands means labor. Anti-DDoS means mitigation capacity. Multi-data-center VLANs and secondary links mean transport capacity. Backup and object storage mean storage media, replication choices, retention rules and customer education. The entity-storage page prices a capacity product at R$0.05 per GB used, with a 2TB minimum, no additional charges for inbound and outbound requests, reading free up to one times stored volume, and replication charged at R$0.05 per GB (https://under.com.br/object-storage-por-capacidade/). That is a classic local-provider move: replace opaque global-cloud transaction billing with a simpler local unit price. It works if the shared platform is engineered for cold storage and customer behavior stays within assumptions.

Connectivity is the second big cost and differentiator. Under's PeeringDB record shows heavy outbound traffic and open peering, and its IX.br Sao Paulo entries imply serious local exchange commitment with aggregate listed port capacity of 240Gbps across two 100Gbps and two 20Gbps ports (https://www.peeringdb.com/api/netixlan?asn=28209). BGP.Tools and Hurricane Electric show the company speaking with transit and content networks; RIPEstat shows live routing visibility; and the Brasil Stream case says streaming demand moved toward Under because the customer needed wider links and lower latency (https://under.com.br/case-de-sucesso/brasil-stream/). The upside is that local peering can reduce transit cost and improve user experience. The downside is that heavy outbound traffic can require constant capacity planning. A streaming, backup, entity-storage or AI-data customer can change the traffic profile quickly. When traffic grows, the first cost is not only bandwidth. It is optics, ports, routers, IX fees, engineering time and sometimes data-center cross-connect constraints.

The supplier and upstream dependence is therefore not a weakness in itself; it is the working capital of the business. PeeringDB lists Under at IX.br Sao Paulo and at Cirion Sao Paulo SAO1 in Cotia (https://www.peeringdb.com/api/netfac?net_id=5932). Hurricane Electric's import list includes major global transit and content networks, including Level 3/Lumen-related AS3356, Cogent AS174, Hurricane Electric AS6939 and content networks such as Google, Microsoft, Meta, Amazon, Cloudflare and Akamai (https://bgp.he.net/AS28209). RIPEstat's asn-neighbours call shows observed neighbours including AS3356, AS6939 and several Brazilian or regional networks (https://stat.ripe.net/data/asn-neighbours/data.json?resource=AS28209). For a customer, that looks like resilience and route choice. For Under, it means vendor selection and peering discipline are central to gross margin. Buying too much transit wastes money. Buying too little causes quality problems. Peering too casually increases operational complexity. Not peering enough leaves avoidable traffic costs on the table.

Competition comes from three directions. The first is the global cloud stack, which offers product depth, procurement confidence and instant scale but exposes Brazilian customers to dollar billing, egress fees and sometimes latency or data-control anxieties. Under's own 2026 budget post explicitly attacks those weaknesses by arguing for billing in reais, fixed cost and avoidance of variable traffic and IOPS charges (https://under.com.br/dolar-alto-3-formas-de-proteger-seu-orcamento-de-ti-hoje/). The second is the Brazilian data-center and cloud peer group: local and regional providers that can also sell colocation, cloud, backup and managed hosting. The third is the broader ISP universe, because regional broadband operators are increasingly mature buyers and sellers of data-center, cloud and interconnection services. Anatel and industry coverage show the PPP segment investing heavily and holding a large share of broadband revenue and traffic (https://abrint.com.br/noticias/anatel-divulga-dados-setoriais-ppps-lideram-investimentos-e-se-destacam-em-receita/). Under's edge is not that nobody else can host servers. It is that it can combine Brazilian legal identity, local data centers, visible interconnection, customer support and product packaging into a credible mid-market alternative.

Local overbuild still matters, even when the company is not primarily a retail FTTH provider. In the access market, overbuild means two or three fibre operators stringing cable through the same neighbourhood and pushing prices down. In Under's market, overbuild means multiple Brazilian infrastructure providers chasing the same enterprise migration story: local cloud, backup, dedicated servers, GPU infrastructure, private cloud and predictable billing. TeleSintese's report that regional operators collectively exceed 56% of fixed broadband accesses signals both opportunity and crowding (https://telesintese.com.br/quem-lidera-a-banda-larga-no-brasil-segundo-a-anatel/). Customers have more local options; they also have more providers making similar claims. Under must therefore defend differentiation with proof: route performance, support speed, uptime, recoverability, cost control and credible customer references. Generic "Brazilian cloud" language will not be enough if customers can move among several local operators.

The pole-access question is less direct for Under than for a last-mile FTTH company, but it still belongs in the payback framework. Brazil's broadband expansion depends heavily on utility-pole sharing, and Anatel and Aneel have spent years trying to reset the rules. The 2014 joint resolution set R$3.19 as the reference price per fixing point for pole sharing in conflict resolution (https://informacoes.anatel.gov.br/legislacao/resolucoes/resolucoes-conjuntas/820-resolucaoconjunta-4). Aneel approved a proposed joint resolution in 2025 and sent it to Anatel for decision, while later Anatel commentary in 2026 still described the pole-sharing issue as moving toward a sustainable model (https://www.gov.br/aneel/pt-br/assuntos/noticias/2025/proposta-de-resolucao-conjunta-sobre-compartilhamento-de-postes-e-aprovada-pela-aneel-e-segue-para-decisao-da-anatel, https://www.gov.br/anatel/pt-br/assuntos/noticias/anatel-demonstra-otimismo-sobre-resolucao-do-impasse-dos-postes). For Under, the relevance is ecosystem cost. If regional access providers face higher or uncertain pole costs, they may delay network builds, consolidate, cut data-center spending, or demand sharper wholesale pricing. If pole rules stabilize, more fibre access can feed demand for local hosting, CDN, backup and interconnection.

Regulation also touches data centers and telecom equipment. The exact licensing profile of Under's service mix cannot be reconstructed from public pages alone, but the company lives at the edge of telecom, hosting, data protection, consumer/business contracts and cybersecurity. Its own 2025 artificial-intelligence infrastructure article leans on compliance, LGPD risk and local processing as reasons to avoid sending certain workloads abroad (https://under.com.br/under-vai-se-dedicar-a-oferta-de-infraestrutura-para-ia-no-brasil/). Its contract materials for cloud servers place duties on customers around backup agents, reporting backup failures via the Under panel, keeping independent offline copies and avoiding spam, phishing, malicious content or illegal uses (https://static.under.com.br/s/pdf/contrato_servidor_cloud.pdf). Those clauses point to a normal but important boundary: Under can sell managed infrastructure, but it still needs customers to own application hygiene, backup validation and legal use. The cleaner that boundary, the better the margin.

Unofficial market signals tell a mixed but useful story. Public court-index aggregators show Under appearing in service-contract and obligation disputes, including cases where Under is plaintiff and cases where it is defendant; Jusbrasil lists 135 process mentions and Escavador lists 176 process appearances, with many in Rio Grande do Sul and Sao Paulo (https://www.jusbrasil.com.br/processos/nome/246796675/under-servicos-de-internet-ltda, https://www.escavador.com/nomes/under-servicos-de-internet-ltda-17d51fc93d). The numbers should not be read as a finding of wrongdoing. They are a sign that Under has enough commercial volume and contractual friction to leave a public trace. In infrastructure services, disputes often cluster around unpaid invoices, service levels, termination, data recovery, migration expectations or disagreement over what was included. That is exactly where the second support visit becomes economic: a poorly bounded service promise can become a legal and collection cost long after the original installation revenue has been booked.

Consumer-review traces point to the same operating surface. Reclame Aqui pages for Under Servidores e Datacenters include complaint listings and individual negative complaints about support, bureaucracy or billing, alongside company responses on some pages (https://www.reclameaqui.com.br/empresa/under-servidores-e-datacenters/lista-reclamacoes/, https://www.reclameaqui.com.br/under-servidores-e-datacenters/maior-arrependimento-contratar-a-under_OJltnqaT16YHDFQM/). A serious reading does not treat a review portal as statistically representative. It treats it as field noise from the part of the business that sales decks cannot remove: customers judge infrastructure providers not only when systems work, but when something fails and the boundaries between provider, customer application and third-party software are contested. Under's status page, support promise and managed product language all make that noise relevant (https://status.under.com.br/).

The stronger unofficial signal is actually customer willingness to attach named operations to Under's cases. Brasil Stream, Vetor Inteligencia, SQG and Todeschini are not evidence of Under's full customer base, but they are examples of the kind of workloads Under wants associated with its brand: streaming, backup, enterprise sites, business intelligence and data protection (https://under.com.br/case-de-sucesso/brasil-stream/, https://under.com.br/case-de-sucesso/case-vetor-inteligencia/, https://under.com.br/case-de-sucesso/sqg-solucoes/, https://under.com.br/case-de-sucesso/todeschini/). Those workloads have a common trait: downtime is embarrassing, but total hyperscaler sophistication may be unnecessary or too expensive. This is the middle market that Brazilian infrastructure providers can serve well if they are disciplined. It is also the market where customers often need more handholding than they admit during procurement.

The quality of Under's network evidence raises the floor of the analysis. A shell company can build a website. It cannot easily fake AS28209's routing history, address blocks, IX.br ports and visible prefixes across RIPE RIS peers. Registro.br's RDAP data shows AS28209 registered on 8 May 2008, with Under as registrant and Roberto Berto as legal representative in the public record (https://rdap.registro.br/autnum/28209). RIPEstat says the first seen prefix-origin observation for AS28209 was 189.113.1.0/24 on 1 September 2009, and that the network remained visible on 4 July 2026 (https://stat.ripe.net/data/routing-status/data.json?resource=AS28209). PeeringDB's record was created in 2013 and updated in 2025, with open policy and IX.br Sao Paulo data (https://www.peeringdb.com/api/net?asn=28209). The business may still face margin pressure, but the underlying network is durable enough to merit analysis as an operating infrastructure company rather than a thin reseller.

The payment-discipline problem deserves its own place in the analysis because it is the unglamorous counterpart to network engineering. A provider can design a good server platform and still lose money if collections, disputes and service boundaries are weak. Infrastructure contracts are sticky when the service is running well; they are combustible when a customer is late, a backup restore is disputed, a migration is messy, or a termination clause is misunderstood. Public process aggregators show several Under matters involving service provision, rescission, default and civil obligations, including actions where Under appears as claimant in service disputes (https://www.jusbrasil.com.br/processos/nome/246796675/under-servicos-de-internet-ltda). That does not show abnormal legal risk by itself. It does show the commercial reality of this product category. A provider selling always-on infrastructure often becomes a creditor, a support desk and a migration partner at the same time. If customers delay payment after consuming support and capacity, the operator carries the working capital.

Under's own contract language, visible in its cloud-server agreement, suggests that the company understands the need to place responsibility on the customer side as well as the provider side. The document requires customers to notify Under through the Under panel when backup reports are missing or show a failure, says each report problem should be opened as an individual ticket, gives Under seven business days to correct errors in backup structure after the ticket, requires the customer to keep a complete copy outside the internet, and bars spam, phishing, malicious content and unlawful use (https://static.under.com.br/s/pdf/contrato_servidor_cloud.pdf). These clauses are not just legal furniture. They are margin protection. Backup is a product that customers often value only after the failure. Without a clear duty to review reports and maintain an independent copy, the provider can be pulled into open-ended liability for application-level or customer-side mistakes. With the duty stated, Under can sell managed infrastructure without accepting every operational risk in the customer's stack.

The same is true for equipment replacement. Under advertises hot-swap disks, secure console access, KVM over IP and remote administration because business buyers want a provider that can keep systems alive without a site visit by the customer (https://under.com.br/servidor-dedicado/). Those features improve conversion, but they also require the provider to hold spares, train technicians, document configurations and maintain enough monitoring to know when intervention is needed. A cheap server monthly fee can look profitable when modeled as hardware depreciation plus power plus bandwidth. It becomes less profitable when the same customer requires repeated disk checks, emergency access, backup explanation, security hardening, firewall adjustment and post-incident reassurance. Under's stated support response in up to 15 minutes is valuable precisely because human time is scarce (https://under.com.br/). The key economic question is whether support is attached to higher-priced managed tiers or diluted across low-priced accounts.

The role of Sao Paulo also needs a more precise reading. For Under, being in Sao Paulo state is not a generic headquarters fact; it is part of the product. Brazil's cloud and enterprise traffic gravitates toward Sao Paulo because the region concentrates customers, data centers, IX.br capacity, financial institutions, enterprise software buyers and national connectivity. Under says its service zones are Cotia and Barueri, and PeeringDB places a facility relationship at Cirion Sao Paulo - SAO1 in Cotia (https://under.com.br/sobre-a-under/, https://www.peeringdb.com/api/netfac?net_id=5932). That geography can lower latency and simplify procurement for Brazilian companies. It can also create concentration risk. If too much of a customer's stack, support dependency and redundancy story sits in one metro area, the provider must be precise about what "two data centers" solves and what it does not. Dual sites inside Sao Paulo state can reduce facility-specific risk; they do not by themselves create a national disaster-recovery footprint.

The status-page component list gives a clue to how Under packages that Sao Paulo concentration. It separates interconnection between SP1 and SP2, each data center, CloudStack, ticketing, telephone support, Under Control and VPN management (https://status.under.com.br/). That is useful because it shows the customer-facing service decomposition. If interconnection fails, the problem differs from a support-phone issue. If CloudStack has a problem, it differs from a physical-server management-console issue. This sort of decomposition is how infrastructure operators avoid turning every incident into a brand-level outage. It is also how sophisticated customers learn where their true dependencies sit. A customer buying redundancy should ask whether the application is replicated, whether backups are immutable, whether DNS and routing are diversified, whether the support channel is independent of the failing system, and whether the contract's recovery promise matches the architecture.

There is a second market in the background: Brazilian regional ISPs as potential customers, peers and competitors. Many access providers need data-center services, backup, colocation, CDN nodes, email, billing platforms, monitoring, voice platforms and wholesale IP resources. Some become sophisticated enough to build or rent their own infrastructure; others buy from providers like Under. Anatel's PPP research and industry coverage show that small and regional providers carry a large share of broadband investment, traffic and customer relationships (https://teletime.com.br/13/10/2025/ppps-investem-o-dobro-das-grandes-operadoras-em-banda-larga/). That makes Under's market larger than direct enterprise hosting. A growing ISP may need local data-center capacity, IX.br adjacency, private cloud and backup to professionalize its own service base. At the same time, large regional ISPs can internalize some of those functions and negotiate aggressively. Under's best customers may be the companies just below that internal-build threshold: large enough to value reliability, not large enough to run the stack alone.

That positioning also explains why service reputation can move revenue. Anatel's 2025 satisfaction coverage reported that regional providers led perceived-quality rankings in fixed broadband and that operational quality, fewer failures and lower need to contact operators were tied to satisfaction (https://teletime.com.br/23/03/2026/provedores-regionais-satisfacao/). The lesson applies to Under's infrastructure niche even though the customer is often a business rather than a household. The most profitable support call is the one avoided through better provisioning, monitoring and documentation. A provider that can reduce avoidable tickets protects margin and improves customer trust. A provider that wins customers with fast support but requires constant support to keep the product usable will struggle to turn service quality into economics. Under's challenge is to make its support promise a confidence signal, not a crutch for products that require too much manual care.

The cloud-substitution question is especially important for mid-market Brazilian companies. Global clouds sell breadth and automation, but their pricing can punish data-heavy workloads, backup restores, streaming, object storage reads and traffic-heavy applications. Under's entity-storage product emphasizes no per-request charges, free reads up to one times stored volume and a simple R$0.05 per GB price for cold storage, with replication charged separately (https://under.com.br/object-storage-por-capacidade/). That is a direct response to a common cloud-bill complaint. But simplicity can cut both ways. If a customer behaves like an archive customer, Under's unit economics may be attractive. If a customer uses a cold-storage product as a hot analytics platform, the shared infrastructure can face contention or hidden support costs. The provider must therefore educate customers at sale time, not after the workload has already distorted the platform.

The artificial-intelligence infrastructure pitch has the same constraint. Under argues that Brazilian companies may prefer local dedicated GPU infrastructure because public cloud inference can be expensive, compliance-sensitive and exposed to dollar costs (https://under.com.br/under-vai-se-dedicar-a-oferta-de-infraestrutura-para-ia-no-brasil/). The thesis is plausible. Data-heavy Brazilian firms may want local processing, predictable invoices and help choosing hardware. But the provider's exposure is unforgiving. GPUs require high upfront spending, stronger power and cooling planning, faster refresh assumptions and a sales force that can distinguish real production demand from experimentation. If Under sells GPU infrastructure as consultative managed service, it can create a higher-margin product. If it buys ahead of real demand, it can trap capital in hardware that ages quickly. The evidence to watch is not press language about demand; it is utilization, contract length, power availability and whether customers commit to dedicated capacity.

The strongest bear case is not that Under lacks evidence. It is that the evidence describes a business with many moving parts. A pure access ISP can be complicated, but the product is legible: connect premises, bill monthly, maintain the outside plant, manage churn. Under's mix is broader: routing, data centers, dedicated servers, private cloud, public cloud, backup, object storage, database, firewall, secondary links, remote hands and potential GPU infrastructure. Each product can raise account value; each also introduces a failure mode and a support boundary. Breadth is attractive when the customer wants a single Brazilian partner.

Breadth is dangerous when the provider underprices coordination. The commercial discipline is to package bundles around repeatable architectures, not custom exceptions.

The strongest bull case is that Under has already crossed the credibility threshold that many regional infrastructure brands never reach. A two-decade operating history, visible ASN, IX.br Sao Paulo ports, public customer cases, data-center claims, status page and local-currency value proposition give it a base from which to sell trust (https://under.com.br/sobre-a-under/, https://www.peeringdb.com/net/5932, https://status.under.com.br/). Trust is monetizable in enterprise infrastructure because migration is painful and outages are costly. A customer that has moved ERP, streaming, backup, institutional sites or private cloud into a provider's environment is less likely to churn over a small price difference if support, billing and performance are stable. That stickiness is the prize. The cost of earning it is the second support visit, repeated thousands of times without letting the exception become the operating model.

That durability does not answer the valuation question. It frames it. Under's business gets more attractive if three things are true. First, the company can keep utilization high across data-center, server and network assets. Second, it can sell managed services at prices that reflect the true cost of support, replacement, monitoring and customer education. Third, it can use local routing and real-denominated billing to capture customers who are not well served by either hyperscalers or small unmanaged hosts.

The company gets less attractive if competition compresses local cloud pricing, if support tickets rise faster than revenue, if GPU bets require heavy capex before demand is proven, if power and cooling constraints worsen, or if hardware replacement costs outrun reais-denominated contracts.

The facts that would change the judgment are specific. Evidence of sustained customer growth without an increase in support backlog would strengthen the view. So would disclosure of rack utilization, churn, average revenue per account, gross margin by product line, power costs, data-center expansion terms, GPU utilization and the share of revenue from recurring managed contracts rather than one-off projects. Additional IX capacity or new regional exchange locations would strengthen the latency and resilience case, especially if paired with customer wins in streaming, backup or enterprise software.

Conversely, rising complaint volume, repeated status incidents, court disputes centered on service failure rather than ordinary collection, or customer migration away from Under's platform would weaken the case. A visible move from commodity dedicated servers toward higher-margin managed private cloud and GPU infrastructure would be positive only if utilization and support discipline follow.

There is also a strategic question about whether Under wants to be a cloud company, a data-center operator, a managed-service provider, an ISP, or a Brazilian infrastructure integrator. The public portfolio says "all of the above" in a controlled mid-market way. That breadth can improve wallet share: a customer might buy dedicated servers, backup, firewall, storage, secondary links and cloud database from one provider. It can also blur responsibility.

When one company sells the compute, the network, the backup, the firewall and the support desk, customers may expect one throat to choke even when the actual fault is in application code, customer configuration or a third-party dependency. The best operators turn that expectation into premium managed contracts. The worst absorb it for free. Under's evidence suggests the company understands the premium-service side; the open question is how tightly it prices and enforces it.

On balance, Under looks like a credible Brazilian infrastructure provider whose economics depend less on first-build excitement than on disciplined aftercare. Its public record is stronger than most low-disclosure registry rows: there is a real ASN, visible IP space, IX.br Sao Paulo capacity, public service pages, customer cases, a status page, corporate records and market traces.

The company is exposed to the same forces that define Brazil's regional ISP and data-infrastructure market: fibre expansion, local peering, regional-provider strength, pole-policy friction, hyperscaler substitution, real-versus-dollar billing, and the need to make support costs visible in price. The attractive part is the moat created by local infrastructure, routing maturity and enterprise support. The risky part is that every promise that wins the account also creates work after the account is won.

The core thesis is therefore cautious but constructive. Under Internet's payback clock does not stop when the server is installed, the IP block is announced or the customer signs the monthly contract. It starts there. The second visit reveals whether the first sale was priced correctly. If Under can keep those visits short, standardized and premium-priced, its Sao Paulo data-center base and AS28209 network can compound into a durable local alternative to global cloud and unmanaged hosting.

If those visits become open-ended problem solving bundled into low fixed prices, the same evidence that makes Under credible also makes the cost risk visible. In Brazilian infrastructure, the winners will not be the operators that build once. They will be the operators that can afford to come back.