Summary

- The paid unit that matters is a backbone connectivity, transit and enterprise network account: internet access, IP/MPLS VPN, leased capacity, Ethernet transport, route engineering, service operations, and account support across Russian regional corridors.

- TransTeleCom's public materials support a serious route-reach claim. Its corporate site at https://company.ttk.ru/ says the company operates and maintains more than 100,000 km of fibre-optic lines with more than 6 Tbit/s of capacity, serves customers across Russia, and connects to neighbouring-country networks through its EurasiaHighway.

- The hard public anchor is AS20485. Public BGP resources such as https://bgp.tools/as/20485 and https://bgp.he.net/AS20485 identify TransTeleCom's autonomous system, its RIPE allocation status, originated prefixes and upstream relationships. That evidence shows public routing surface and dependencies; it does not prove internal architecture, resilience, customer uptime or route quality.

- The account is expensive because a Russian backbone provider must pay for fibre corridors, rail-adjacent access, backbone nodes, peering and transit, network-operations labour, service-level commitments, equipment replacement, sanctions-constrained procurement and enterprise support in regions where cheaper access products may not solve continuity.

- The substitute set is real: Rostelecom's national backbone and MPLS network, mobile operator enterprise services from providers such as MTS, local fibre providers, cloud direct-connect or colocated alternatives, and the option to delay a route upgrade until demand or budget is clearer.

- Missing proof sits in three buckets: economics, reliability and retention. Public sources do not disclose product-level margins, private renewal rates, outage history, SLA credits, equipment inventory age, or how often customers choose TransTeleCom over cheaper domestic alternatives after testing continuity in the field.

A continuity buyer starts with a route problem

Imagine a Russian industrial group with plants in the Urals, a distribution centre near Moscow, a data workload in a domestic cloud, a warehouse in Siberia and a procurement office that still needs predictable access to counterparties outside Russia. The company already has local internet links. Some are cheap. Some are bundled with mobile services. One regional facility can buy fibre from a city provider at a price the finance department likes. Another can wait for the landlord's next building upgrade. The CIO is not looking for a slogan about digital transformation.

The question on the table is narrower: should the enterprise pay TransTeleCom for a backbone account because a rail-adjacent route gives better continuity than cheaper domestic substitutes?

That question is where Joint Stock Company TransTeleCom matters. The company is not just a household broadband name. It is the Russian Railways-linked operator whose public corporate page at https://company.ttk.ru/ describes more than 100,000 km of optical lines, more than 6 Tbit/s of network capacity, operations across eight federal districts and a data-transit role between East and West. The same page says TransTeleCom provides backbone services to operators and large Russian corporations, while its business site at https://b2b.ttk.ru/ presents internet access, corporate VPN, Ethernet, trunk digital channels, international channels, SD-WAN, DDoS protection, cloud and integration offers. The buyer therefore prices a route through a bundle of physical reach, public routing, enterprise service management and institutional proximity to rail infrastructure.

The enterprise's alternative is not no connectivity. It can buy Rostelecom, which describes a 500,000 km national backbone at https://www.company.rt.ru/en/about/net/magistr/ and an IP/MPLS network at https://www.company.rt.ru/en/about/net/mpls/ with hub-level nodes, regional distribution nodes, access points, international exchange presence and stated MPLS capacity. It can buy mobile operator business services: MTS Business at https://business.mts.ru/moskva markets mobile staff tariffs, office internet, VPN, static IP, DDoS protection and corporate support. It can use a local fibre provider where the route is confined to one city. It can move a workload closer to a cloud provider or data centre and buy a cloud connection rather than a long private path. It can also delay a route upgrade and carry more operational risk for another budget cycle.

The price decision therefore begins with continuity, not bandwidth. A cheap link is attractive when a warehouse uses cloud email and standard browsing. It becomes less attractive when a plant needs a predictable ERP path, a railway-adjacent site needs low interruption during field work, a bank or energy customer asks about stable routing, or a regional office must keep voice, video and operational telemetry moving through periods of local disruption. TransTeleCom's account is valuable only if it reduces the practical cost of those failures.

Public evidence can show that the company has a large network surface and products built for enterprise traffic. It cannot show that a given customer path will stay up during the next fibre cut, maintenance window, traffic-engineering event or sanctions-driven equipment shortage.

That boundary is important. The public internet can show the outline of AS20485, official product claims and competitor offers. It cannot inspect a customer's SLA negotiations or internal route diversity. The economic test is not whether TransTeleCom owns or operates impressive fibre. It is whether paying for a backbone account buys a better risk-adjusted result than Rostelecom, a mobile operator enterprise product, a local fibre supplier, cloud direct connectivity or a delayed upgrade.

What the customer actually buys

The account has several layers. The simplest layer is internet access for organizations. TransTeleCom's business page at https://b2b.ttk.ru/dostup_v_internet/ says it connects companies through its own backbone channel, offers stable routing, dedicated IP addresses, reverse DNS options and availability in more than 1,000 cities and settlements. It highlights backbone redundancy, public IP management and connection by dedicated channel to a port on the IP network. For a small office, this can look like ordinary business internet. For a distributed enterprise, those details become the first sign that the provider is selling a managed edge into a larger national route system.

The second layer is private connectivity. The corporate IP VPN page at https://b2b.ttk.ru/korporativnaya_set_vpn/ describes a closed network over TransTeleCom's IP MPLS backbone, logically separated from the public internet, with QoS classes for data, voice and video, full-mesh exchange, expansion to new points and service operation as the company grows. The language is familiar to enterprise telecom buyers, but its economics are specific. A VPN account prices design labour, site survey, topological choices, traffic classes, access ports, customer-premises equipment, testing, change management and ongoing fault handling. The customer buys one accountable network for offices, warehouses, stores, remote sites and critical applications rather than a collection of unrelated commodity access lines.

The third layer is point-to-point capacity. The operator page for backbone digital channels at https://b2b.ttk.ru/operators/mck says TransTeleCom offers channels between two points on its backbone nodes in Russia, with capacities from 64 Kbit/s to 10 Gbit/s and use cases covering voice, data and video for commercial organizations, government institutions, telecom operators, mobile operators and internet providers. The virtual Ethernet page at https://b2b.ttk.ru/operators/vke says it provides Ethernet over MPLS between two points on IP nodes of the backbone network, with VLAN and port modes for linking logical network segments, online databases, video conferencing and voice. Those pages show a product stack aimed at buyers who want circuit-like predictability without building the underlying long-haul network themselves.

The fourth layer is operator-facing reach. The operator section at https://b2b.ttk.ru/operators/ positions TransTeleCom for other telecom companies and lists international channels, synchronization, Ethernet, VPN and backbone digital channels. The business home page says international channels can range from 64 Kbit/s to 10 Gbit/s and are used for links with other operator networks, corporate networks and global information resources. That operator-facing surface matters because an enterprise may not buy TransTeleCom directly at every site. It may encounter TransTeleCom as an upstream route, a leased path, a wholesale component, a data-centre interconnect or a backup path embedded in another provider's service.

The fifth layer is managed modernization. The SD-WAN page at https://b2b.ttk.ru/sd-wan/ frames TransTeleCom's offer as a turn-key service with one communications contract, a cross-service SLA, service-model economics instead of upfront capex, a geographically reserved platform on backbone IP/MPLS nodes and Russian software and platform components. SD-WAN is not a magic substitute for physical reach; it still needs underlay links. But it changes the account discussion because the buyer can ask TransTeleCom to manage policy, failover and traffic steering across more than one access path. In a sanctions-constrained environment where old hardware may be hard to replace with the same Western vendor, a managed SD-WAN package can be sold as operational insurance as much as network optimization.

Those layers define the paid unit. The buyer is not simply paying for "internet". It is paying for a route account that blends access, private transport, public routing, SLA language, NOC availability, field support, equipment and change control. The question is whether the customer's operational dependence is high enough to make that bundle cheaper than failure.

Rail-adjacent reach is a real advantage, but it is not free

TransTeleCom's network identity is inseparable from Russian rail infrastructure. The corporate site says the company is involved in transport and logistics digital transformation, provides communications services to transport enterprises, and develops and operates infrastructure for communications and transport security systems. It says the optical line system exceeds 100,000 km and that EurasiaHighway connects with neighbouring-country networks including China, Japan, Mongolia, North Korea, Finland, the Baltic states and CIS countries. That is a distinct footprint.

Rail corridors pass through industrial regions, freight nodes, energy geographies and cities that matter to enterprise buyers.

Rail-adjacent reach has economic value because rights of way are hard to replicate. A provider with access along transport corridors can be useful where a city fibre provider stops at a commercial district, where a mobile operator's enterprise offer still depends on backhaul, or where a new customer site sits closer to a railway corridor than to a competitive metropolitan ring. A company moving goods, monitoring field equipment, operating warehouses or linking regional production sites may care less about consumer broadband coverage and more about whether a provider can bring a path near the operational corridor.

But the same advantage creates cost. Fibre corridors must be maintained across distance, climate, permissions, repair windows, physical-security constraints and coordination with transport infrastructure. The buyer sees a monthly account; the operator sees ducts, optical cable, regeneration or amplification, backbone nodes, power, spares, field technicians, planned maintenance, emergency restoration, customer notification and safety procedures. A rail-adjacent path can be valuable precisely because it is not a cheap urban fibre drop. The account must recover the cost of long assets that customers may use only when something breaks elsewhere.

That is why TransTeleCom's pricing cannot be evaluated only by comparing megabits. A local provider may offer a lower per-megabit quote inside one city. A mobile operator may bundle mobile staff lines, office internet and fixed-wireless fallback with less procurement friction. Rostelecom may offer broader incumbent reach and a larger published backbone. The TransTeleCom case has to be more specific: route diversity, rail-corridor proximity, enterprise continuity, cross-border transit options, and operational support for sites where the cheaper offer does not remove the failure mode.

Public evidence supports the route-reach claim but not the route-quality claim. The official corporate page and service pages show scale, target markets and product architecture. They do not publish fibre maps precise enough for a customer to infer path diversity. They do not disclose restoration intervals by corridor. They do not show whether a customer's primary and backup routes share a bridge, duct, power source or maintenance contractor. Those details belong in a technical proposal and SLA negotiation.

A serious buyer should treat rail-adjacent reach as a reason to ask harder route-diversity questions, not as automatic proof of resilience.

AS20485 is a useful public anchor, not an x-ray

The hard comparative anchor for TransTeleCom's public internet surface is AS20485. BGP Tools at https://bgp.tools/as/20485 identifies "TransTeleCom JSC" as AS20485, registered in September 2002, active and allocated under RIPE, with originated IPv4 and IPv6 prefixes and visible upstreams including Arelion, Tata Communications, PCCW Global, Telecom Italia Sparkle, MegaFon and ER-Telecom at the time of access. Hurricane Electric's BGP Toolkit at https://bgp.he.net/AS20485 provides another public view of the same autonomous system. RIPEstat at https://stat.ripe.net/AS20485 offers a route-statistics surface for the AS.

This evidence matters because it demonstrates that TransTeleCom is not merely a marketing label for enterprise access. It has a visible autonomous-system presence and publicly observable routing relationships. For a backbone or transit buyer, that is relevant. Public BGP data helps answer basic questions: does the company announce routes, what upstreams are visible, what AS number will appear in public path data, and which public internet dependencies can be observed from outside? A customer comparing TransTeleCom with a local fibre reseller should care about that difference.

The same evidence must be bounded. AS20485 does not prove a customer's private MPLS path. It does not show internal topology, NOC staffing, equipment age, dark-fibre ownership, precise route diversity, congestion management, traffic prioritization inside private services, or outage history. It does not show whether a particular enterprise VPN has redundant access in both directions. It does not show whether a backbone path was engineered to avoid a specific region. BGP visibility is a public surface. It is useful because it can falsify weak claims and reveal dependencies. It is dangerous when treated as proof of service quality.

For a buyer, the public network evidence is most useful as an economic clue. The visible upstream mix suggests that even a large domestic backbone account still exists inside a web of external transit and peering relationships. International route economics do not stop at Russia's border. If a customer needs traffic paths to Europe, Asia, global cloud providers or foreign counterparties, TransTeleCom must buy, peer, exchange or otherwise manage relationships beyond its own fibre. Those relationships can add resilience, but they also add cost and political exposure.

Sanctions, supplier exits, routing policy changes, cable incidents and commercial disputes can all affect the menu of reachable paths.

The buyer should therefore ask two different questions. First: what does AS20485's public surface say about TransTeleCom's role in the internet ecosystem? It says there is a serious public network with observable routes and dependencies. Second: does that prove the proposed enterprise route is worth the price? No. That depends on contracted design, route separation, access diversity, change handling, monitoring, support escalation and how the provider responds when a real incident crosses the boundary between public internet, private transport and customer equipment.

The account carries state-linked customer gravity

TransTeleCom's economics are shaped by its Russian Railways context and by its customer categories. Its official materials say the company serves private individuals, state customers and business clients across Russia. The business site lists industry solutions for banks and financial organizations, transport and logistics, industrial and manufacturing enterprises, fuel and energy, retail and distributed service networks, government sector and state corporations, healthcare, education and IT, digital, media, data-centre and service-provider markets.

The service pages mention commercial organizations, government institutions, telecom operators, mobile operators and internet providers as users of backbone channels.

This matters for route-risk pricing because state-linked and infrastructure customers buy differently from small offices. They may value procurement continuity, domestic legal compatibility, Russian support, familiar documentation, local account teams and the ability to align connectivity with transport infrastructure or national programmes. They may be less willing to depend on a foreign cloud path, a consumer-grade access product or a provider with no regional restoration capability.

A railway-linked operator can have credibility in that market because it already speaks the language of regulated operations, field infrastructure and national-scale service.

State-linked gravity also cuts both ways. Large public-sector and infrastructure customers can make a provider more stable, but they can also constrain it. Procurement cycles may be slow. Tender terms may compress margins. Compliance obligations may require domestic equipment, domestic cryptography, reporting, lawful-intercept readiness, data localization support or security controls that add cost. Customers may demand service levels without accepting the full price of physical diversity. The provider's sales team must convert institutional trust into profitable accounts rather than low-margin obligations.

The business pages show this tension. TransTeleCom sells not only connectivity but DDoS protection, information security, video analytics, transport digital services, Bank of Russia transport gateway services, cloud infrastructure, telecom integration and outsourcing. A customer who buys a backbone account may also be buying a domestic technology posture. That can help retention because the relationship becomes broader than one route. It can also make substitution harder because the customer must replace several services at once. But it increases delivery burden.

When a provider becomes the communications wrapper for transport, government, industrial and energy processes, a failed handoff can become an operational complaint rather than a simple internet ticket.

The article's thesis sits inside that burden. TransTeleCom matters when a customer prices backbone connectivity through route reach, rail-adjacent infrastructure, enterprise continuity, peering, sanctions-constrained equipment and alternatives. It does not matter as much when the workload is generic, the site is metropolitan, the cloud provider is nearby, and a cheaper access product can meet the same practical risk threshold.

Sanctions and equipment replacement move the price

The sanctions issue is not that every TransTeleCom router or optical system is publicly known to be unavailable. Public evidence does not allow that claim. The issue is broader and more economic: Russian telecom operators operate in an environment where Western export controls, supplier exits, payment constraints, software-support limits and replacement uncertainty raise the cost of maintaining and modernizing networks. U.S. technology-sector sanctions and export-control coverage were reported early in the war by outlets such as Axios at https://www.axios.com/2022/03/31/us-new-sanctions-russian-technology-sector and semiconductor-control risks were signalled before the invasion at https://www.axios.com/2022/02/02/chip-blockade-russia-sanctions-biden. The Bureau of Industry and Security site at https://www.bis.gov/ is the official public home for U.S. export-control administration. Those sources do not name TransTeleCom as uniquely affected; they show the operating environment for Russian high-technology procurement.

TransTeleCom's own product pages respond to that environment indirectly. The SD-WAN page emphasizes Russian software and platform components. The business site lists import substitution of information-security tools as a product area. The cloud page at https://cloud.ttk.ru/ markets protected Russian cloud infrastructure, monitoring, administration, backup, anti-virus, firewalls, DDoS protection and GOST encryption. These offers are commercial, but they also reflect buyer anxiety. Enterprises want continuity, but they also want confidence that a provider can maintain the service without waiting for unavailable parts, unsupported firmware or blocked vendor relationships.

Equipment replacement is a hidden cost in the backbone account. Optical transport, routers, switches, customer-premises equipment, security appliances, synchronization systems, management software and monitoring tools all age. A sanctions-constrained market can lengthen procurement cycles, encourage use of alternative suppliers, require additional testing, force mixed-vendor operations, increase inventory buffers, and shift more labour onto internal engineering teams. If a provider promises an SLA, it must carry enough spare capacity and human expertise to make the promise credible.

A cheap competitor may avoid those costs by limiting the service, quoting best-effort access or relying on customer-owned equipment.

The economic question for the buyer is not whether sanctions automatically make TransTeleCom unreliable. That would be too crude. The better question is whether the provider has turned sanctions pressure into a managed operating model. Does it have replacement plans for access and backbone equipment? Does the enterprise account include supported CPE or only network-side commitments? What happens when a router model reaches end of support? How are security updates handled? Which components are domestic, which are foreign, and which are covered by tested alternatives?

How much of the SLA depends on hardware the provider can actually replace inside Russia?

Public sources cannot answer those questions. They do, however, explain why price comparisons have to include more than the monthly line rate. A backbone account in 2026 Russia prices procurement risk. Customers may pay more for a provider that can absorb those risks, but they should demand evidence of inventory, support process and migration practice rather than accepting "import substitution" as a blanket answer.

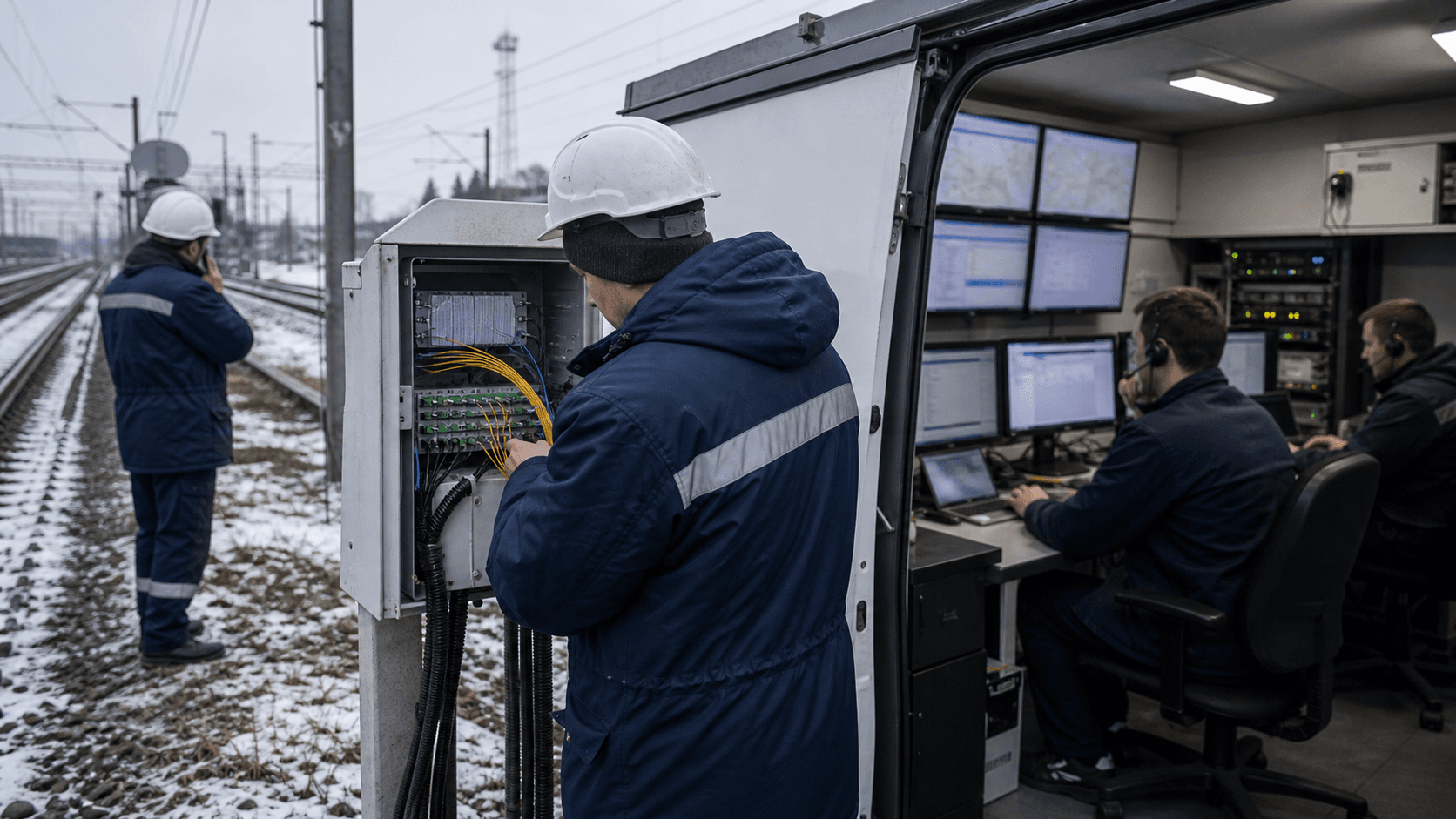

NOC labour is part of the product

Backbone continuity is labour-intensive. The network operations centre, field engineering, provisioning, incident management, route engineering, customer support and account management all sit behind the invoice. TransTeleCom's operator page says it offers 24x7 support. The business home page points different phone lines at small and medium business customers, large business and government customers, and current clients of different group entities.

The internet page describes steps from address and requirements collection to technical feasibility, scheme proposal, dedicated-channel connection, route configuration and handover into operation. The VPN page describes requirement gathering, topology design, QoS classes, point connection, equipment configuration, testing and ongoing operation.

That process is the service. A backbone account is not valuable only when packets move. It is valuable when a customer opens a ticket at 02:00, when a new warehouse needs a route in three weeks, when a video application performs badly, when a route must be changed without breaking a call centre, when a DDoS event hits a public application, or when a customer needs evidence for an internal post-incident review. The NOC must know whether the problem is customer LAN equipment, access fibre, backbone transport, IP routing, a remote peer, an upstream transit issue, DNS, DDoS mitigation, CPE failure or planned maintenance.

That diagnostic labour has a real cost.

Service-level agreements price that labour. A customer may think it is buying a percentage availability figure, but the provider is pricing mean time to detect, mean time to repair, escalation paths, spare equipment, route alternatives, monitoring tools, documentation and customer communication. An SLA without field capacity is only a promise. Field capacity without route design is only a truck. Route design without customer communication is still a business failure if the enterprise cannot plan around the outage.

TransTeleCom can defend a higher account price when it can bring NOC labour close to the customer's operational problem. For example, an energy distributor connecting regional control centres may value a provider that understands protected channels, private addressing, failover and regulated documentation. A retailer with hundreds of points of sale may value one provider for VPN, internet, DDoS and voice. A logistics company may value rail-corridor familiarity and support for distributed sites. A data-centre or service-provider customer may value backbone channels and public routing visibility.

The risk is commoditization. If the customer's workload can tolerate interruption, if the local provider has adequate support, or if cloud applications reduce dependence on private site-to-site networking, then the NOC labour premium may look like overhead. The provider must then prove that its managed account prevents enough operational pain to justify the price. Public webpages cannot prove that. They can only show that the product is designed around those service tasks.

Rostelecom sets the national benchmark

Every TransTeleCom account has to be priced against Rostelecom. Rostelecom's official backbone page says its digital backbone runs 500,000 km and is built on fibre using SDH and DWDM technology, with more than 350 access points, participation in 17 international cable systems, direct connections with 190 networks in 70 countries, contractual arrangements with more than 2,300 national and international fixed and mobile operators, and geographically widespread route protection.

Its IP/MPLS page says the network covers all regions of the Russian Federation with 24 hub-level nodes and 110 regional distribution nodes, more than 350 access points, 7.8 Tbit/s MPLS IP throughput capacity, foreign access points including Stockholm, London, Hong Kong, Frankfurt and Amsterdam, and presence at Russian and international exchange points.

That is the hard incumbent comparison. TransTeleCom's official claim of more than 100,000 km is large, but Rostelecom's published backbone is larger. Rostelecom's role as the national incumbent gives it a wide service catalogue, procurement familiarity, public-sector reach and data-centre and cloud assets. A buyer who only needs the largest published national footprint may start there. A buyer who wants a single supplier for telecom, cloud, cybersecurity, digital-region services and incumbent access may also start there.

TransTeleCom's counter-position is not simply "larger". It is rail-adjacent and transit-specific. The official TTK page says the company is number one in East-West data transit and attributes 40 percent of traffic transit through Russia to TransTeleCom. The business page repeats a market position in traffic transit through Russia and China-Europe data transfer. Those are company claims, not independent audited market proof in the public pages. But they explain the commercial story. TransTeleCom wants to be evaluated on backbone corridor economics, not only on mass-market telecom scale.

The enterprise buyer should therefore avoid a false binary. Rostelecom may be the correct answer for a broad incumbent account, especially where the customer's sites align with its access network, public-sector procurement, cloud products or local operating teams. TransTeleCom may be the correct answer where route diversity from the incumbent matters, where rail-adjacent corridors solve a regional problem, where East-West transit is relevant, where the customer needs a second national provider, or where TTK's specific product/account team performs better in the target geography.

The price of TransTeleCom's account is partly the price of not being fully dependent on Rostelecom. That may sound abstract until a customer experiences a regional outage, a procurement dispute, a maintenance window or a path-quality issue that makes a second national route valuable. The premium is rational only if the route is genuinely diverse and operationally supported. It is wasted if it runs through the same vulnerable local access, the same building riser, the same power dependency or the same upstream bottleneck.

Mobile operators and local fibre compress the lower end

The cheaper end of the substitute set is more dangerous for TransTeleCom than it may appear. MTS Business at https://business.mts.ru/moskva does not present itself as a backbone specialist on the page accessed for this research, but it markets a broad business portfolio: mobile communications for employees, office internet, business VPN, static IP, DDoS protection, APN protected data transfer, M2M, NB-IoT, support, billing documents and a 24/7 business account interface. Similar mobile operator enterprise portfolios are common in Russia. They are not always substitutes for a national private backbone, but they can be enough for many distributed customers.

Mobile operator offers compress the price because they bundle what many customers already buy. If a company has hundreds of staff SIMs, vehicle trackers, store tablets, point-of-sale backups, IoT sensors and call-centre numbers, the mobile operator can make connectivity feel administratively simple. A store or small warehouse may accept fixed-mobile fallback rather than a second fibre path. An office may buy business internet and VPN from the same mobile group because billing and support are easy. A company with seasonal sites may use LTE or 5G routers until the business case for fibre is proven.

Local fibre providers compress the price in another way. In a metropolitan area, local access may be cheap, fast and good enough. A city fibre provider may have better building access, faster installation and lower cost for one office. A commercial real-estate site may already have a preferred provider. A data-centre campus may offer cross-connects and carrier choice that make a national provider less central. If a workload is mostly cloud-based and not latency-critical across Russia, the buyer may prefer local internet plus cloud security controls rather than a private national route.

Cloud direct-connect options also change the account. TransTeleCom's own cloud page recognizes that customers are comparing provider-managed infrastructure with their own servers, technical teams, administrative staff, installation and certification costs. But if the customer's application centre of gravity moves into a domestic cloud or data centre, the enterprise may buy a high-quality cloud connection for one region instead of upgrading every branch through a national backbone. The route account then has to defend its value as a branch-to-cloud and branch-to-branch continuity layer.

Delayed upgrades are the final substitute. In uncertain economic conditions, a customer may simply defer. It may keep two imperfect links, accept manual workarounds, reduce video usage, move batch jobs overnight, or wait for a facility lease decision before buying a managed backbone account. That delay is a competitor because continuity budgets are discretionary until a failure becomes expensive enough to change the board's tolerance.

TransTeleCom wins against these substitutes when it can connect the failure cost to the route design. The argument must be concrete: a plant outage costs X, a logistics interruption affects Y, a regulated workflow requires Z, and the proposed TransTeleCom route removes a specific dependency cheaper alternatives leave in place. Without that evidence, the cheaper substitute has the advantage.

Peering and transit are economic levers, not magic

Peering and transit are central to TransTeleCom's story because the company is not only an access provider. Its public materials emphasize data transit through Russia and East-West routes. Public BGP evidence shows AS20485 with visible upstreams and a long-standing autonomous system. The official corporate site highlights EurasiaHighway and neighbouring-country connections. The business page reports traffic-transit and China-Europe transfer market positions. These pieces create a clear commercial thesis: TransTeleCom sells paths, not only ports.

The economic value of a path depends on what the customer is trying to avoid. A content provider may care about reachability and latency to Russian access networks. A cloud customer may care about predictable paths to domestic data centres. An operator may care about international channels, IP transit, synchronization and wholesale capacity. A bank or logistics company may care about stable routing and regional private paths more than global internet transit. A manufacturer may care about branch continuity and application response time. The same backbone can be valuable in different ways, but each use case needs a different proof.

Public peering and BGP data can help a customer ask the right questions. If AS20485 is visible with multiple upstreams, the customer can ask which upstreams affect its destination set, whether the proposed product uses public internet or private transport, whether traffic is engineered through specific cities, how rerouting works, which exchange points matter, and whether route changes are monitored. If a provider claims international reach, the customer can ask whether reach is direct, through partners, through purchased transit, through settlement-free peering or through a wholesale channel.

Each answer has different economic and risk implications.

But peering and transit should not be oversold. A visible upstream list does not prove low latency. A route object does not prove congestion-free performance. A peering relationship does not prove that traffic for a private enterprise VPN will use that path. A route map does not prove resilience during fibre cuts. An AS path seen from one vantage point may not represent a customer's traffic during an incident. The public internet is dynamic, and private enterprise services can be engineered separately from public route announcements.

That boundary matters because network records can tempt buyers into over-reading what they show. ASN, prefixes, route objects and datasets are evidence. They are not people or companies. They should not be treated as durable actors. For TransTeleCom, AS20485 helps identify public surface and dependencies. It does not tell the enterprise whether the proposed backbone account will outperform a Rostelecom VPN, an MTS business VPN, a local fibre pair, or a cloud direct connect. That answer comes from route design, contract terms and operational history.

Enterprise SLAs convert uncertainty into a bill

An enterprise SLA is a financial instrument disguised as a service promise. It converts uncertain outage risk into a predictable bill and a limited remedy. TransTeleCom's pages use the language of reliability, redundancy, QoS, support and one-provider responsibility. The SD-WAN page explicitly mentions a cross-service SLA. The VPN page describes traffic classes and stable service for voice, video and business applications. The internet page points to backbone redundancy. The operator page emphasizes 24x7 support. These are the ingredients of an SLA sale.

The value of that sale depends on the customer's failure math. For a warehouse, an hour of connectivity failure may delay scanning, inventory visibility and transport dispatch. For a bank office, it may interrupt customer service, compliance access and branch operations. For an energy or utility customer, it may affect monitoring, maintenance coordination and safety workflows. For a service provider, it may affect downstream customers and brand trust. If the cost of failure is high, the backbone account can be cheap even at a higher monthly price. If the cost of failure is low, the same account can be over-specified.

SLA credits are not the same as resilience. A customer rarely wants a small credit after an outage. It wants the outage avoided or shortened. A serious buyer therefore needs to inspect the service design behind the SLA: access diversity, power diversity, route diversity, repair commitments, monitoring, ticket escalation, maintenance notification, customer-side demarcation, equipment replacement and reporting. The contract should specify what is actually measured. Is availability measured at the provider port, the customer CPE, the application layer, or a private route endpoint? Are planned works excluded?

How are regional force majeure events treated? Are DDoS events, upstream failures and customer-equipment failures excluded?

TransTeleCom's public service descriptions show that it has products capable of carrying SLA expectations. They do not disclose SLA outcomes. They do not show how many customers received credits, how often restoration targets were missed, or whether particular corridors underperform. That is missing reliability proof. It is not a criticism unique to TransTeleCom; most telecom providers do not publish that level of account data. But it is central to the price decision because the premium account exists to reduce failure, not to produce glossy service categories.

The enterprise should also ask whether the SLA prices sanctions-era repair. If a CPE fails and the original model is no longer easy to source, what replacement is used? If an optical component must be substituted, how is compatibility tested? If a software platform is domestic, what security assurance and update process applies? If a route depends on a foreign interconnect, what contingency exists if commercial conditions change? These questions turn sanctions risk into operational due diligence.

The regional route problem is usually at the edge

Backbone providers often market the long-haul network because it is impressive. Customers often suffer at the edge because that is where the office, plant, warehouse or station meets the provider. TransTeleCom's 100,000 km claim matters, but the regional economics of an account may be decided by last-mile access, building entry, local fibre path, power, CPE, permissions and field labour. A national route is only as resilient as the weakest segment the customer's traffic must traverse.

The official internet page's workflow recognizes this. It asks for address and requirements, checks technical feasibility, proposes a scheme, connects by dedicated channel to a port on the IP network, configures routing and hands the service into operation. That process is routine, but it is where the practical risk sits. A cheap quote may depend on a single building entry. A backup path may share a duct with the primary path. A warehouse may have mobile signal good enough for casual browsing but not for failover under load. A plant may require trenching, landlord permission or coordination with other infrastructure work.

A remote site may have long repair times because field access is hard.

Rail-adjacent infrastructure can help at the edge if the customer's site aligns with it. It can be less helpful if the final connection from railway corridor to facility is expensive, slow or physically vulnerable. A buyer should therefore ask not only whether TransTeleCom has a backbone near the region but how the actual access segment reaches the facility. The price of the account may include construction, leased local access, customer equipment, installation and testing. Those costs can make the first-year economics look worse than a cheaper provider's quote.

They may still be rational if they remove a failure mode the cheaper quote leaves untouched.

Regional reach also affects retention. Once a provider has built or coordinated a difficult access path, the customer may be less likely to churn. That can be good for TransTeleCom's margins if the service performs. It can be bad for the customer if it becomes locked into a provider without periodic proof of value. Smart buyers separate sunk construction cost from renewal value. They ask whether the route is still needed, whether substitutes have improved, and whether the provider's performance justifies continuation.

The missing retention proof is important. Public sources do not show how sticky TransTeleCom's enterprise accounts are, how many customers renew after installation, how much churn comes from local substitutes, or how often customers keep TTK as a secondary path while buying primary service elsewhere. Without that data, the article can explain the retention mechanism but not quantify it.

Cloud direct connect changes the geography of the account

The cloud comparison is not external to TransTeleCom; the company markets cloud infrastructure itself at https://cloud.ttk.ru/. The cloud page presents infrastructure rental, virtual workstations, dedicated servers, equipment rental, data-centre services, managed Kubernetes, databases, compute services, monitoring, administration, security, storage, backup, migration help, 24/7 monitoring, stable connection, GOST encryption and Russian cloud use cases for state institutions, healthcare, banking, education and business. It also contrasts cloud rental with owning servers, technical teams, administrative staff, installation and certification.

That matters because enterprise connectivity used to be centred on office-to-office networking. Increasingly, the decisive route is branch-to-cloud, branch-to-data-centre or site-to-application. A company may not need every facility to talk to every other facility at high quality. It may need every facility to reach a domestic ERP environment, a warehouse management system, a monitoring platform, a voice service, a backup repository or a data-exchange gateway. If those systems move into a cloud or data centre, the backbone account can be redesigned around application paths rather than old office topology.

This can help TransTeleCom if it sells connectivity and cloud together. One provider can potentially manage the customer's access, private network, security service and cloud infrastructure. The account becomes harder to displace because the customer must compare a combined operational model, not a single line. It can also help with sanctions and compliance concerns because the provider can position domestic cloud, Russian cryptography options and local support as part of the continuity story.

But cloud can also hurt the backbone premium. If a customer moves workloads into a provider-neutral data centre with many carriers, it may buy cross-connects and local internet diversity instead of a national private route. If a SaaS application works over ordinary internet with strong application-layer security, the private VPN may be less critical. If a cloud provider offers direct connectivity through a partner ecosystem, the customer may not need TransTeleCom at every site. The route account must adapt to the new geography: fewer point-to-point lines, more branch-to-cloud design, more security, more monitoring and more policy control.

The public sources do not show whether TransTeleCom's cloud business materially improves backbone account retention. They do show that the company understands the bundle. For customers, the practical issue is whether one provider can reduce operational complexity without creating a single point of commercial and technical dependence. The best account may combine TransTeleCom for one path, Rostelecom or a mobile operator for another, and cloud connectivity designed so that application access survives a single provider incident.

Why the route can be worth paying for

TransTeleCom is worth paying for when the customer can name the failure that cheaper substitutes do not solve. The strongest case is a distributed enterprise with regional sites near rail or industrial corridors, a need for private traffic classes, a requirement for route diversity from the incumbent, and enough operational cost in outages to justify a managed account. In that case, the account buys more than bandwidth. It buys a route design, an operational escalation path and a provider whose public surface supports a national backbone role.

A second strong case is an operator or service-provider customer. The operator pages for backbone digital channels, virtual Ethernet, international channels and synchronization show that TransTeleCom serves wholesale and inter-operator needs. A regional ISP, mobile operator, data-centre provider or digital service company may need capacity between nodes, access to Russian and international routes, or a second provider for resilience. For those customers, AS20485's public BGP surface and TransTeleCom's corridor story are directly relevant. The customer still needs private terms, but the public evidence aligns with the product.

A third case is a customer exposed to transport, logistics, energy, state or industrial requirements. TransTeleCom's rail-adjacent identity and official focus on transport digital services can matter when the customer needs a provider familiar with distributed physical infrastructure. A generic cloud connectivity offer may not be enough for a site that needs field coordination, private transport and regulated documentation.

A fourth case is sanctions-era continuity. If a customer believes cheap providers will struggle to replace equipment, support security tools or maintain route diversity, it may pay a premium for a provider that can demonstrate inventory, domestic alternatives, tested migration paths and support depth. The key word is demonstrate. Public marketing around Russian components and import substitution is a starting point, not proof.

The weak case is a simple metropolitan office, a non-critical workload, a site well served by multiple local fibres, or a company whose applications tolerate ordinary internet paths. For those customers, TransTeleCom's backbone story may be excessive. Rostelecom, MTS Business, another mobile operator, a local ISP or a cloud-first design may produce the same business outcome at lower cost. The buyer should not subsidize national backbone economics unless its own continuity problem requires them.

Missing proof: economics, reliability and retention

The public record leaves three missing-proof buckets. The first is economics. TransTeleCom's public pages make scale and market-position claims, but they do not disclose product-level revenue, margins, capex by network segment, cost per corridor, wholesale transit costs, SLA-credit expense, equipment replacement cost, or how much of the backbone account is profitable after field labour and procurement constraints. Without that data, outsiders cannot know whether the account is a high-margin enterprise product, a defensive wholesale product, or a strategic service priced partly by institutional relationships.

The second is reliability. Official pages mention redundancy, QoS, support and backbone scale. Public BGP pages show AS surface. None of that reveals outage rates, repair intervals, packet loss, latency distributions, route-convergence behaviour, customer trouble-ticket volumes, incident root causes or performance against SLA. It also does not show route diversity at the customer edge. A buyer should request path diagrams, diversity statements, maintenance history, incident reporting templates and references for similar regional routes. Public evidence supports due diligence; it does not replace it.

The third is retention. TransTeleCom's account value depends on whether customers stay because the service performs, not because switching is inconvenient. Public sources do not reveal renewal rates, churn reasons, win/loss against Rostelecom, mobile operator bundles, local fibre or cloud direct-connect alternatives, or how often customers downgrade from private routes to cheaper internet plus SD-WAN. Retention is the best test of whether the route premium is perceived as worth paying after the first contract period. It is also the least visible from outside.

There are also proof gaps around sanctions. Public export-control sources explain the environment, but they do not show TransTeleCom's inventory, vendor exposure, procurement channels or replacement backlog. Public service pages mention Russian components in some areas, but they do not show test results, failure rates or migration costs. The provider may be managing the issue well; the public record simply cannot prove it.

These gaps do not make the account unattractive. They define the buyer's negotiation. A serious enterprise should ask TransTeleCom to price the specific continuity problem, not sell generic backbone prestige. It should compare the offer with Rostelecom's national backbone, MTS or other mobile operator enterprise services, local fibre, cloud connection options and delayed upgrade economics. It should demand evidence at the route level, not only at the company level.

The backbone account carries Russian route risk

TransTeleCom's public story is strong enough to matter. A company with more than 100,000 km of optical lines, a rail-adjacent history, a visible AS20485 public network surface, operator-facing products, enterprise IP/MPLS services, SD-WAN, cloud infrastructure and a stated East-West transit role deserves attention in any Russian backbone procurement. It is not a generic reseller at the edge of the market.

The same facts make the account risky. Long corridors are expensive. Rail-adjacent reach is valuable only when it matches the customer's sites. Public BGP visibility shows dependencies as well as scale. Sanctions pressure can raise equipment and support costs. State-linked and infrastructure customers can create sticky demand but also heavy obligations. Rostelecom sets a larger national benchmark. Mobile operator business portfolios and local fibre compress the lower end. Cloud direct-connect designs can move the customer's continuity problem away from traditional private routes.

The enterprise should therefore price TransTeleCom as an option on continuity. If the route reduces a named operational failure, if access diversity is real, if SLA design matches the application, if equipment replacement is credible, if NOC labour is visible, and if the account gives a better risk-adjusted path than Rostelecom, mobile operators, local fibre or cloud alternatives, the premium can be rational. If the provider cannot demonstrate those points, the backbone label becomes a costly abstraction.

The public evidence proves surface, not outcome. It proves that TransTeleCom markets and operates a national-scale backbone and enterprise-connectivity portfolio. It proves AS20485 has a visible public internet footprint. It proves competitors offer serious alternatives. It proves the sanctions environment makes equipment and compliance part of the price. It does not prove that any specific route will outperform a cheaper domestic substitute. That proof must be won in the proposal, the contract and the first incident after go-live.