Summary

- Phase3 Telecom's strongest economic claim is that aerial fibre on power transmission infrastructure can sell route diversity and repairable long-distance capacity to carriers, ISPs, enterprises and public institutions that cannot rely on a single ordinary ground route.

- The public evidence is meaningful but uneven: Phase3 describes 10,000 km of coverage, power-infrastructure right-of-way, NOC support, dark fibre, backhaul, dedicated internet, MPLS, IPLC and regional corridors, while public regulatory, concession and network records leave renewal, margin, SLA, MTTR and retention evidence incomplete.

- Licence rows, AS37248, AFRINIC allocations, PeeringDB and BGP pages are useful evidence of public network surface and legal/technical contactability; they do not by themselves prove internal quality, profitability, route construction, uptime or customer dependence.

The buyer is purchasing recoverable route diversity, not a slogan

Consider a Nigerian payment processor with offices in Lagos, Abuja and Kano. Its operations team already has a primary private line from a large mobile-network group. It can add a second terrestrial fibre circuit from another carrier, use microwave backhaul for selected sites, keep satellite for emergency continuity, fall back to mobile data during incidents, or postpone a regional expansion until connectivity is less fragile. The purchase decision is not "fibre or no fibre." It is whether the second path lowers the cost of failure enough to justify a wholesale or enterprise connectivity contract.

If the second path shares the same road trench, the same city works risk or the same downstream bottleneck as the first path, the buyer is paying twice for correlated failure. If the second path rides a different physical corridor, has a field team that can reach the fault, and has an operating right that survives regulatory and concession friction, the buyer is buying a serviceable insurance policy rather than just bandwidth.

That is the economic unit for Phase3 Telecom: a Nigerian wholesale and enterprise aerial-fibre connectivity contract. The unit may appear as domestic leased capacity, backhaul, dark fibre, dedicated internet, MPLS VPN, metro connectivity or an international private leased circuit, but the paid entity is more specific. A customer is buying a route, capacity on that route, monitoring, repair labour, power-line access, commercial assurance and a right to escalate when the route fails. Phase3's official site says the company is an independent aerial fibre optic network infrastructure and telecommunications provider incorporated in 2003 and licensed as a national long-distance operator to provide transmission services in 2006: https://www.phase3telecom.com/. Its about page adds POPs, colocation and NOCs in Nigeria and positions the company for dedicated internet access, MPLS VPN, metro ethernet and WAN services: https://www.phase3telecom.com/about-us/. Its corporate profile and "A Bold Intervention" page say coverage is "10,000km and counting" and that the company is licensed to run its network on Nigeria's power infrastructure using a unique right of way: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf and https://www.phase3telecom.com/bold-intervention/.

That unit has several billable layers. The first is physical path: which corridor the traffic follows, whether the circuit enters a distinct POP, whether the handoff can be kept away from the buyer's primary failure point, and whether the power-line route is actually useful for the customer's locations. The second is capacity: whether the buyer receives dedicated capacity, protected capacity, an optical handoff, dark fibre control or a managed IP service. The third is assurance: how the provider monitors alarms, dispatches field teams, communicates incidents and restores service.

The fourth is regulatory and site access: whether the provider has the right to operate on the route, enter the substation or pylon area, maintain shelters and keep power to active equipment. These layers are why a wholesale buyer can pay for a route even when cheaper bandwidth exists elsewhere. It is also why Phase3's public claims need to be read as a contract economics file, not only as marketing. A buyer is paying for a chain of obligations.

The first implication is that Phase3's price is not anchored only to megabits per second. A commodity access buyer can compare monthly bandwidth quotes, but a carrier, bank, cloud edge, public-sector network or regional ISP is also comparing avoided downtime, circuit diversity, procurement overhead, failover design, repair distance and the political risk of depending on one corridor. Phase3's domestic leased circuit page says its aerial right-of-way crosses Nigeria and the West African sub-region, refers to SDH/DWDM, NOC support and field-level maintenance teams, and markets aerial fibre as less susceptible to vandalization: https://www.phase3telecom.com/domestic-lease-circuit/. Its backhaul page sells service to LTE providers, mobile network operators, ISPs and enterprises from aggregation points to the core over fibre or microwave: https://www.phase3telecom.com/backhaul-services/. Those pages matter because they show the actual commercial surface: wholesale and enterprise buyers paying for paths, handoffs and operations, not retail broadband alone.

The second implication is that the direct substitute needs to stay visible. If the buyer can buy a second circuit from Bayobab, Airtel Telesonic, inq. Digital, Broadbased, Cyberspace, ipNX, MainOne-adjacent providers, a satellite operator or a microwave integrator, Phase3 needs its power-line route to change the failure pattern. NCC's public licence list shows several National Long Distance licensees and other infrastructure operators, including recent rows for Bayobab Nigeria Infra Private Limited, Broadbased Communications, Airtel Nigeria Telesonic and Galaxy Backbone: https://www.ncc.gov.ng/industry/licensing/list-licensees. The presence of alternatives does not weaken Phase3's case. It defines it. The company is valuable when its route is an economically distinct alternative to ordinary terrestrial backhaul or fragmented last-mile providers, not when it is merely one more name in a procurement spreadsheet.

Power-line right-of-way lowers one route problem and creates another

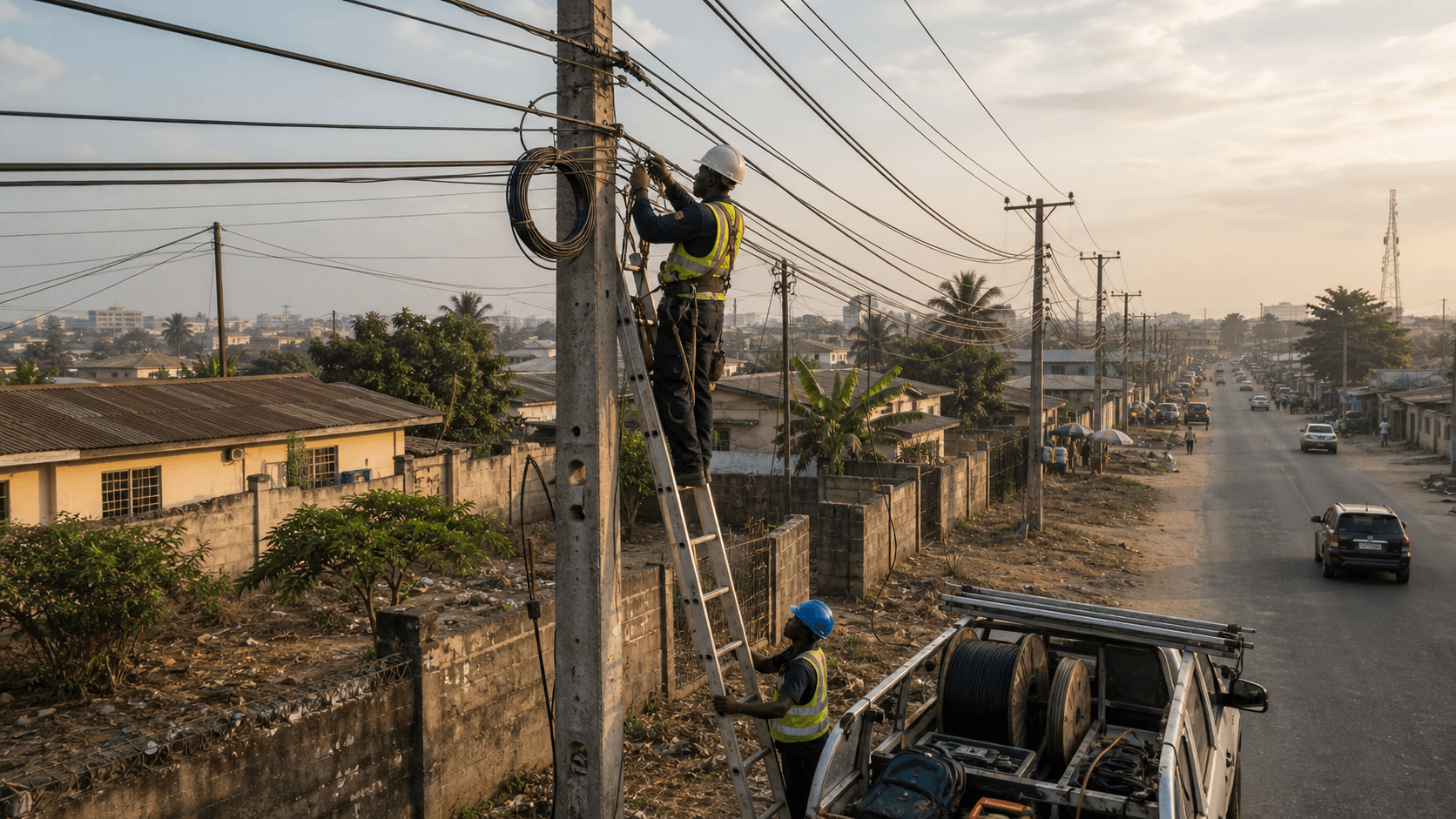

Nigeria's fibre economics are usually dominated by civil works, approvals, damage and repair. A buried route can require excavation, road cuts, state and local permissions, recurring right-of-way charges, coordination with contractors, and constant exposure to accidental cuts. An aerial route over transmission infrastructure changes that pattern. It can follow long-distance electrical corridors, use pylons and substations as route and access logic, and avoid part of the digging burden that makes ordinary fibre slow and expensive. Phase3's marketing leans directly into that advantage. The corporate profile says the company runs on Nigeria's power infrastructure, uses unique right-of-way, offers 24-hour proactive monitoring and support, and positions reliability around fewer fibre cuts: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. Its dedicated internet page says availability is delivered over a "100% fibre connection" through the aerial right of way and refers to 99.9 percent service availability, multiple traffic diversity, 1:1 contention and 24/7 customer support and network monitoring: https://www.phase3telecom.com/dedicated-internet-service-dis/.

That route model has a real economic logic. If the aerial corridor avoids road construction, vandalism around accessible ducts, and repeated municipal trenching disputes, a customer can buy diversity without paying for a new underground build from scratch. The path can also reach areas where commercial trenching would not be justified by immediate traffic volumes. That is why right-of-way, power-line reach and route repair should be treated as the mechanism, not background decoration.

A long-distance operator that can reuse an established utility corridor may lower the upfront cost of reaching thin or underserved geographies, then monetize the route through wholesale capacity, dark fibre, carrier backhaul, public-sector circuits and enterprise WANs. The economic value is strongest when the route is physically distinct from the customer's incumbent circuit and when a fault can be located and repaired before the avoided outage cost is lost.

The avoided cost is not only the cost of trenching. It is the cost of delay. A customer waiting for a buried fibre build can lose months to route survey, permits, road restoration, contractor mobilisation, wayleave negotiation and municipal approvals. A carrier that can use a power corridor can sometimes offer a route where the ground build is not available, or can offer a physically different protection path while the customer's main provider remains tied to roads and ducts. That does not mean aerial fibre is cheap. It means the capital and operating burden moves.

The company may spend less on trenching and more on concession fees, tower access, electrical-safety coordination, splicing labour, emergency travel, route monitoring and power-site relationships. The buyer's question becomes whether those shifted costs create a better continuity outcome than a buried fibre path, microwave chain, satellite backup or larger operator leased line.

The same model creates another cost problem. Phase3 does not own the electricity transmission system. Aerial fibre over high-voltage infrastructure depends on access to towers, substations, shelters, power supply, safety procedures, transmission-line maintenance windows, and the institutional relationship with the power transmission operator. The public record around the Transmission Company of Nigeria concession shows why that dependency is not theoretical. BusinessDay reported in July 2020 that TCN wrote to NCC to grant operational licence to Phase3 Telecoms and Alheri Engineering after an 18-month halt, granting access to POPs, concessioned fibre optic cable and power supply connectivity: https://businessday.ng/technology/article/tcn-clears-phase3-telecoms-for-operation-after-18-months-halt-in-business/. The same report recorded that the halt followed a dispute over concession fees, that Phase3 disputed the allegations, and that industry stakeholders wanted certainty over whether the fibre would be available at expected quality.

This is the heart of the article. Power-line reach is a shortcut only if access survives. It can lower the cost of one route problem: digging, road damage, duplicated civil works, and fragile ground corridors. It can raise another: the dependence on the utility asset owner, the concession contract, substation access, line crews, safety coordination and repair logistics along transmission infrastructure. Phase3's network management page says the company uses alarm monitoring systems on high-voltage pylons where it has fibre infrastructure and has a management system for fast response to emergency crisis: https://www.phase3telecom.com/network-management/. That is strong directional evidence that the company understands the aerial route's operating burden. It is not enough, by itself, to establish actual mean time to repair, restoration performance or SLA compliance.

The concession record is a strategic asset and a warning label

The concession history matters because Phase3's right-of-way economics are tied to public infrastructure. Guardian Nigeria published Phase3's 2018 response to allegations that it owed the federal government money over the TCN fibre optic agreement, reporting the company's statement that it did not owe NGN 27.18 billion, that it had paid undisputed concession, royalty and equipment-space rental amounts, and that the dispute concerned harmonisation of right-of-way charges for fibre on power lines: https://guardian.ng/business-services/phase-3-explains-concession-agreement-with-tcn/. Realnews carried a similar account, including Phase3's assertion that it inherited dilapidated fibre, deployed 2,000 km and invested more than USD 100 million in capital and operating expenditure on the project: https://realnewsmagazine.net/phase3-telecom-not-owe-fg-n27-2bn-fibre-optic-agreement/.

The counter-record is also visible. Proshare reproduced a ministerial letter saying NEPA entered concession agreements with Phase3 and Alheri in 2006, that TCN inherited those agreements, and that the concessions covered operation of TCN's fibre optic network along transmission lines, build-operate-transfer enhancements and third-party telecommunications services: https://www.proshare.co/articles/fashola-writes-president-buhari-on-tcns-recovery-of-government-assets?category=Power+%26+Energy&classification=Read&menu=Economy. The same account says the concession fee was not merely for right-of-way but also for use of TCN fibre built alongside transmission lines. Those statements are contested background, not current margin proof. Yet they show why Phase3's most distinctive asset can become a governance question: if the route depends on a power-sector concession, any dispute over fees, access or enhancement obligations can affect service availability and customer confidence.

The Infrastructure Concession Regulatory Commission's 2020 annual report is a better official anchor for where the dispute ended up. It lists mediation on the concession for TCN existing and proposed fibre optic network and states that the parties, TCN, Phase3 Limited and Alheri Limited, resolved their contractual disputes by drawing up an addendum to the contracts: https://www.icrc.gov.ng/wp-content/uploads/2021/07/Annual-report-2020-final.pdf. That public record is important because it moves the story from accusation and rebuttal toward contractual resolution. It does not publish the full addendum, the commercial terms, the repair obligations or the post-resolution performance record.

For a buyer, the right reading is neither panic nor comfort. The concession shows a privileged route surface that ordinary providers may not have. It also shows that route access has a public-contract dependency. A bank choosing a disaster-recovery link should not treat an aerial route as automatically safer. It should ask whether the aerial corridor is independent from its primary route, whether Phase3 can reach the fault, whether substation and tower access are contractually secure, and whether escalation paths work when the fault crosses power-sector boundaries. The buyer is not just buying glass.

It is buying enforceable operating coordination.

Licence evidence supports the national-transmission role, with a 2026 public-record gap

The national long-distance licence is part of the economic mechanism because it authorizes transmission services at national scale. Phase3's own public materials say the company was issued an NLDO licence by the Nigerian Communications Commission and licensed as a national long-distance operator to provide transmission services: https://www.phase3telecom.com/about-us/ and https://www.phase3telecom.com/. NCC's public list of licensees is the official place to check the market's licence surface: https://www.ncc.gov.ng/industry/licensing/list-licensees. The list also shows the competitive set around long-distance transmission, not only Phase3.

The record needs careful treatment in 2026. A searchable NCC listing has previously surfaced Phase 3 Telecom Limited as a National Long Distance licensee with a start date of 01/01/2006 and an end date of 31/12/2025, while the live NCC list visible in the research session emphasized other active National Long Distance rows and did not give a clean current Phase3 renewal row in the visible extract. That does not prove Phase3 lacks authority in 2026; the company remains publicly active, publishes current regional route announcements, and its official materials maintain the NLDO claim.

It does mean the public article should not pretend that renewal terms, licence refresh timing or current NCC row status are fully documented in open evidence. For procurement, the licence record is a due-diligence item, not a footnote.

NCC's 2024 year-end performance report also frames the wider market. It says mobile operators had 297,445.16 km of microwave radio links in December 2024, fixed telephony operators reported 11,743.67 km of on-land fibre, and "Other Operators" including long-distance service operators, interconnect exchange, metropolitan fibre and international data-access licensees reported 18,711 km of long-distance cable network unchanged from 2023: https://ncc.gov.ng/sites/default/files/2025-11/2024-Year-End-Performance-Report.pdf. The same report says ISP operating cost rose from NGN 96.8 billion in 2023 to NGN 196.3 billion in 2024, attributing the increase to high energy costs. That matters for Phase3 because it reinforces the buyer's substitute set. Microwave remains a massive operational layer. Fibre is valuable, but its economics are pressured by energy, repair and right-of-way cost. Aerial fibre earns a premium when it reduces correlated physical-failure exposure and repair friction, not just when it adds route kilometres.

Nigeria's public infrastructure agenda strengthens the background demand for backbones. The Federal Ministry of Communications, Innovation and Digital Economy describes Project BRIDGE as a PPP-backed SPV intended to deploy at least 90,000 km of fibre optic cables as core connectivity infrastructure and national backbone: https://fmcide.gov.ng/project-bridge/. The World Bank says BRIDGE would deploy more than 90,000 km and extend national backbone coverage from 35,000 km to 125,000 km: https://www.worldbank.org/en/news/press-release/2025/10/07/world-bank-approves-new-financing-to-enhance-nigeria-digital-infrastructure-and-health-security. EBRD's Nigeria Sovereign Fibre Project page describes a signed sovereign loan of up to USD 100 million for participation in an SPV for approximately 90,000 km of fibre-optic broadband infrastructure: https://www.ebrd.com/home/work-with-us/projects/psd/56618.html. These programmes are not Phase3 revenue. They are market signals that Nigeria wants a denser, more resilient backbone and that open, national-scale fibre is a policy priority.

The revenue case is a portfolio of contracts, not one product line

Phase3's public services are broad enough that the company should be read as a connectivity infrastructure portfolio. Domestic leased circuits target secure and reliable transmission for integrated data, voice and video: https://www.phase3telecom.com/domestic-lease-circuit/. Backhaul targets LTE providers, MNOs, ISPs and enterprises: https://www.phase3telecom.com/backhaul-services/. Dark fibre lets other networks configure components around their own requirements: https://www.phase3telecom.com/dark-fibre/. Dedicated internet offers 1:1 contention and public IPs: https://www.phase3telecom.com/dedicated-internet-service-dis/. IPLC offers dedicated international private-line service over a global optical footprint: https://www.phase3telecom.com/iplc/. The corporate profile adds MPLS, WAN, metro connectivity, managed services, data centre, satellite and sector-specific enterprise solutions: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf.

That breadth is useful if it converts aerial reach into repeatable account economics. A carrier may buy backhaul. An ISP may buy wholesale transport and route diversity. A bank may buy MPLS, dedicated internet and managed service. A government agency may buy secure continuity for public-sector applications. A cloud or content platform may buy low-latency regional access. A satellite customer may use Phase3's terrestrial network as part of distribution, while a remote customer may use satellite as the alternative when terrestrial infrastructure is not available. The point is not that every product has the same margin.

It is that the same long-distance infrastructure can support multiple paid units if customer acquisition, service assurance and repair costs stay below the account value.

The recent regional announcements show how Phase3 is trying to turn Nigerian power-line economics into West African corridor economics. In May 2025 Phase3 and CSquared, with Societe Beninoise d'Infrastructures Numeriques, announced a Lagos-to-Accra terrestrial fibre route, with the company saying the route provides capacity, speed and resilience for content delivery networks, hyperscalers, fintech platforms and digital-service providers: https://www.phase3telecom.com/phase3-csquared-and-sbin-commission-terrestrial-fibre-route-from-lagos-to-accra/. Also in May 2025 Phase3 and Sonatel announced a 3,500 km Lagos-to-Dakar terrestrial fibre route, positioned as a land-based alternative after 2024 subsea cable disruptions and described by Phase3 as reaching Benin, Togo, Ghana and Senegal: https://www.phase3telecom.com/phase3-and-sonatel-launch-lagos-dakar-terrestrial-fibre-route-to-power-west-africas-digital-future/. The Laser Light Africa partnership announcement describes an Infrastructure-as-a-Service offer across the Accra-Lagos corridor, planned micro data centres along the route, space-based redundancy, and use of electrical substations along Phase3's aerial fibre infrastructure: https://www.phase3telecom.com/phase3-and-laser-light-africa-to-deliver-infrastructure-as-a-service-across-the-accra-lagos-corridor/.

These announcements do not disclose take-up, prices, utilization or booked revenue. They do, however, show a coherent commercial direction. Phase3 is not trying to win only a local broadband household. It is trying to make the power-line corridor a wholesale and enterprise platform for regional resilience. The unit economics improve if one route can serve carriers, ISPs, public-sector workloads, enterprise networks, cloud access and regional redundancy. They weaken if the same route requires heavy bespoke support, repeated concession negotiation, expensive repairs, underused capacity or discounts to compensate for reliability uncertainty.

Route repair is the cost centre that decides the margin

Wholesale fibre contracts often look asset-heavy but labour-light from the outside. In practice, the repair organization can decide whether the contract is profitable. A fibre cut is not only a technical incident. It triggers fault localization, access permission, field dispatch, safety coordination, splicing work, customer communication, escalation credits and sometimes emergency rerouting. On an aerial network, the repair call may involve pylons, substations, electrical safety and remote routes. On an ordinary buried route, it may involve roads, construction crews and wayleave disputes.

Either way, the buyer values the circuit only if the provider can restore service faster and with less confusion than the substitute.

Phase3's own materials make repair a central claim. The domestic leased circuit page lists 24/7 NOC support, network management at equipment and network layer, field-level maintenance teams distributed across POPs, and dedicated connections with low latency and jitter: https://www.phase3telecom.com/domestic-lease-circuit/. The network management page says alarm monitoring systems are deployed on high-voltage pylons and that Phase3 has a management system for rapid emergency response: https://www.phase3telecom.com/network-management/. The corporate profile says managed service includes NOC management, technical support, field-level maintenance and change management, and refers to SLA terms around availability, reliability and MTTR: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. These claims align with the economics. Customers pay because repair capability can convert a distinct route into practical continuity.

The support page is more conservative. It gives public contact numbers, says general queries will be attended to within 48 hours, lists technical support hours of Monday to Friday 08:00 to 17:00 and Saturday 08:00 to 13:00, and says technical queries will be attended to within 72 hours: https://www.phase3telecom.com/contact-support/. That does not necessarily define enterprise SLA support; wholesale contracts may include different escalation terms. Still, the public support page is a useful friction marker. A buyer paying for route diversity should distinguish between marketing language, public support windows, contract-specific SLA commitments and actual outage restoration data.

Labour signals also point to repair as a burden. A 2025 LinkedIn job listing for a Network Operations and Maintenance Officer at Phase3 described experience in fibre maintenance and deployment, splicing machines, power meters, OTDR and network troubleshooting: https://ng.linkedin.com/jobs/view/network-operations-and-maintenance-officer-at-phase3-telecom-limited-at-phase3-telecom-4176818776. Indeed reviews are weak evidence, but they echo the field-work reality: one 2020 field-support technician review referred to distance from head office, while a 2015 field-support engineer review referred to troubleshooting network breakdown and restoration and sometimes working alone when more people were needed: https://ng.indeed.com/cmp/Phase3-Telecom/reviews. These are not verified operating metrics. They are market signals that the aerial-fibre model is labour-intensive and geographically distributed.

For margin, the key question is whether the incremental contract value pays for that labour. A carrier backhaul circuit with a strict SLA and high downtime penalty can support expensive maintenance if it avoids a larger failure cost for the customer. A low-price internet access circuit cannot. A dark-fibre lease may shift some network-control burden to the customer, but Phase3 still needs the route, access and physical restoration. An IPLC or regional corridor can command value if latency and diversity are distinctive. The repair cost centre is therefore not a back-office detail.

It is the place where Phase3 either turns right-of-way into margin or gives back the advantage in dispatch, coordination and credits.

A contract year is won or lost in small operating frictions

The aerial-fibre contract also has a renewal cycle. A buyer does not reprice the line only after a catastrophic outage. It reprices it after small incidents accumulate: unclear notifications, slow dispatch, repeated packet loss, confusing ownership between access and backbone segments, repair windows that collide with business hours, or site teams that cannot reach a fault because access approval is delayed. These frictions are economically important because the customer has substitutes. A bank can retain the circuit as a backup but reduce committed capacity. An ISP can move traffic to another upstream.

A mobile operator can keep microwave longer than planned. A public agency can delay additional sites. The route still exists, but the revenue mix deteriorates.

That is why the paid unit should be understood over a year, not at installation. Month one rewards route availability. Months two through twelve reward incident discipline. The provider has to keep a reliable inventory of spares, trained splicing teams, safety procedures, fuel or vehicle availability, customer escalation contacts, POP power arrangements and fault records. On an aerial system, the provider also has to coordinate around transmission-line safety and possibly utility maintenance.

A buried-fibre provider faces different repair constraints, but the economic principle is the same: a route with bad operating discipline becomes a discounted route.

Phase3's public materials show pieces of this operating stack. The corporate profile refers to NOC management, field-level maintenance, technical support management and change management: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. The domestic leased circuit page refers to field-level maintenance teams distributed across several POPs: https://www.phase3telecom.com/domestic-lease-circuit/. The support page gives public response targets for general and technical queries: https://www.phase3telecom.com/contact-support/. The missing link is not whether Phase3 has people and pages; it is whether the repair organization consistently turns incidents into short, well-communicated service events for high-value customers. That is the evidence a renewal decision would reward.

This also explains why customer mix matters. A carrier route with traffic diversity requirements and documented failover may pay for disciplined restoration. A small enterprise buying dedicated internet may care more about monthly price and support simplicity. A public-sector account may value continuity but impose procurement and payment friction. A regional cloud or content customer may value latency and route quality but demand demanding service reports. Phase3's portfolio can benefit from those multiple segments, yet each segment has a different tolerance for outage, price and contractual ambiguity.

A single physical corridor can therefore contain high-margin and low-margin contracts at the same time.

Technical records show public surface, not service quality

Phase3's network records are useful, but only within their lane. AFRINIC RDAP for AS37248 identifies "Phase3 Telecom Limited" as registrant and shows the autnum active: https://rdap.afrinic.net/rdap/autnum/37248. AFRINIC's IPv4 RDAP record for 41.87.64.0 to 41.87.95.255 shows a Phase3 Telecom Limited allocation in Nigeria: https://rdap.afrinic.net/rdap/ip/41.87.64.0/19. Its IPv6 RDAP record for 2c0f:fea8::/32 also lists Phase3 Telecom Limited in Nigeria: https://rdap.afrinic.net/rdap/ip/2c0f:fea8::/32. PeeringDB has a Phase3 Telecom network entity for ASN 37248 pointing to the Phase3 website: https://www.peeringdb.com/asn/37248. BGP.he.net lists AS37248 as Phase3 Telecom Limited and shows prefixes including 41.87.64.0/19 and 2c0f:fea8::/32, with route-validity indicators on specific prefixes: https://bgp.he.net/AS37248.

Those records support a limited conclusion. Phase3 has a public routed network surface, registry contactability and internet-number resources consistent with an operating telecom provider. They do not prove the fibre route is aerial, that the route follows a given transmission line, that a specific customer gets a diverse path, that a POP has power resilience, that internal monitoring works, that support is fast, or that the company is profitable. The assignment's boundary is important: ASNs, prefixes, route records and licence rows are evidence, not entities.

They are signal lights on the public network perimeter, not a map of internal operations.

The same boundary applies to BGP and PeeringDB in procurement. A buyer can use route records to check whether Phase3 announces prefixes, which upstreams or peers appear from third-party views, and whether public routing behaviour changes during an incident. But it cannot infer SLA compliance from a green route object. It needs contracted path diversity, route diagrams under NDA, POP handoff details, historical trouble tickets, restoration commitments, escalation contacts and evidence that the route does not collapse into the same physical corridor as the primary supplier.

Competition is not just another fibre operator

Phase3 competes with several kinds of substitutes. The simplest is another terrestrial fibre carrier. NCC's list of licensees shows a long-distance market with multiple operators, including large-group infrastructure providers and specialised carriers: https://www.ncc.gov.ng/industry/licensing/list-licensees. A customer may prefer the procurement comfort of a larger mobile group or an established enterprise carrier, especially if the account includes mobile, cloud, voice and managed services. In that case Phase3 needs the aerial route to provide a physical or commercial distinction that the larger operator does not.

The second substitute is microwave. NCC's 2024 performance report says mobile operators had 297,445.16 km of microwave radio links, a massive installed base that remains relevant for backhaul, redundancy and hard-to-reach sites: https://ncc.gov.ng/sites/default/files/2025-11/2024-Year-End-Performance-Report.pdf. Microwave is not a perfect substitute for fibre capacity, but it can be the practical alternative when a fibre route is expensive, slow or frequently cut. Phase3's backhaul page itself acknowledges fibre or microwave wireless network as backhaul media: https://www.phase3telecom.com/backhaul-services/. For some buyers, the trade-off is not best technology but least risky continuity.

The third substitute is satellite. Phase3 also sells satellite broadband through P3Tech, which complicates the competitive picture. The corporate profile says satellite can provide internet where terrestrial infrastructure is absent and is impervious to cable damage or infrastructure theft: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. For remote businesses, NGOs, mining operations or public-sector sites, satellite may be a backup to fibre, a temporary solution before fibre, or the primary service where fibre does not reach. This does not undercut the aerial-fibre thesis. It clarifies it. Phase3's fibre contract wins when capacity, latency and route economics beat satellite; satellite stays relevant where repair distance or fibre reach makes terrestrial service too uncertain.

The fourth substitute is delay. In markets with uncertain power, road works, foreign exchange pressure and public-contract complexity, a buyer can postpone an expansion, keep workloads in Lagos, rely on mobile data or reduce service quality in remote branches. Nigeria's Project BRIDGE and sovereign-fibre financing show the state wants the delay option to become less rational: https://fmcide.gov.ng/project-bridge/ and https://www.ebrd.com/home/work-with-us/projects/psd/56618.html. Phase3 benefits from that policy direction if its existing rights and regional routes let customers move before new public fibre arrives. It faces pressure if publicly financed fibre adds open-access competition on routes where Phase3 currently has scarcity value.

Regional routes make sense only if Nigerian continuity holds

The West African corridor strategy is commercially attractive because demand is no longer confined to national voice or internet transit. Content delivery, fintech, public-sector platforms, cloud access, remote work, digital identity, e-commerce and cross-border enterprise operations all require lower latency and better continuity. Phase3's Lagos-Accra and Lagos-Dakar announcements speak directly to that demand: https://www.phase3telecom.com/phase3-csquared-and-sbin-commission-terrestrial-fibre-route-from-lagos-to-accra/ and https://www.phase3telecom.com/phase3-and-sonatel-launch-lagos-dakar-terrestrial-fibre-route-to-power-west-africas-digital-future/. The older regional record is also relevant. Guardian reported in 2015 that Phase3 planned aerial fibre from Kano to Gazaoua in Niger, 228 km through Kano and Katsina, to let Niger leverage bandwidth from the Nigerian coast: https://guardian.ng/technology/phase3-telecom-expands-fibre-optic-cable-link-in-west-africa/. IT News Africa reported in 2012 that Phase3 had secured right-of-way from Communaute Electrique du Benin to use high-voltage lines in Benin and Togo: https://www.itnewsafrica.com/2012/02/nigerias-phase3-telecom-plotting-west-african-expansion/. Vanguard reported in 2009 that Phase3's aerial infrastructure in Nigeria was deployed on 330 kV and 132 kV high-voltage lines and in Togo and Benin on 161 kV high-voltage lines: https://www.vanguardngr.com/2009/09/phase3-telecom-extends-services-to-west-african-countries/.

The pattern is consistent: Phase3 uses power-line reach and partnerships to build cross-border terrestrial alternatives. The current economic question is whether those routes are sold as credible resilience in a region that has seen subsea cable vulnerability, terrestrial cuts, power outages and regulatory fragmentation. Phase3's Sonatel announcement explicitly referred to a land-based alternative after widespread subsea cable disruptions in 2024 and cited latency as low as 32 ms on the Lagos-Dakar route: https://www.phase3telecom.com/phase3-and-sonatel-launch-lagos-dakar-terrestrial-fibre-route-to-power-west-africas-digital-future/. That is a plausible demand case for hyperscalers, cloud providers, CDNs, financial services and public-sector applications. It is not a disclosed revenue case.

The Nigerian base remains decisive. If Phase3 cannot maintain Nigerian route continuity, then regional expansion carries the same fragility across more kilometres. If it can, the Nigerian aerial corridor becomes a platform for regional wholesale access. The Laser Light Africa announcement is notable because it connects the corridor to substations, micro data centres and space-based redundancy: https://www.phase3telecom.com/phase3-and-laser-light-africa-to-deliver-infrastructure-as-a-service-across-the-accra-lagos-corridor/. That mix of aerial fibre, power sites, compute and satellite redundancy is strategically coherent. Its value will depend on execution: site power, security, backhaul, cross-border permissions, customer contracts and the ability to repair along each segment.

Regionalisation also changes the buyer's avoided-cost calculation. A Lagos enterprise buying a local backup line can accept a narrow service area. A cloud platform, CDN or financial network serving Lagos, Accra and Dakar needs route continuity across jurisdictions. The price is then linked to fewer procurement relationships, fewer handoff disputes, more predictable latency and a clearer incident owner. Phase3's partnerships with Sonatel, CSquared, SBIN and Laser Light Africa are therefore commercially relevant even if they do not reveal revenue.

They show the company trying to make the aerial-corridor thesis travel beyond Nigeria, while using partners to cover territories, licences and customer relationships that Phase3 cannot credibly own alone.

The risk is that cross-border routes compound friction. Each border can introduce customs, tax, telecom licensing, security, currency, site-access and payment issues. Each partner adds an operational interface. A fault that begins in one country may affect a service sold in another. That is why regional routes usually command value only when the provider can offer clear service demarcation. A buyer should ask where Phase3's responsibility starts and ends, which partner owns each repair segment, how maintenance windows are communicated, which route alternatives exist when a border segment fails, and how commercial credits are handled.

These questions do not weaken the route case. They define the price a sophisticated buyer should be willing to pay.

Public-sector continuity is a customer need, not a guarantee

Phase3's public materials repeatedly mention government, schools, universities, hospitals, public-sector institutions and regional development. The corporate profile's e-government and e-voting sections say public authorities need secure access and operational continuity, and that Phase3's open-access network can support more efficient public processes: https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. The official narrative also emphasizes digital inclusion, public-private partnership and regional development. The profile of Stanley Jegede says Phase3 supports telecom operators, ISPs, financial institutions, governments, public-sector institutions and global technology platforms: https://www.phase3telecom.com/stanley-jegede-building-the-digital-backbone-of-west-africa/.

The public-sector angle matters because continuity failures have social cost beyond contract penalties. Education, health, identity systems, public procurement, elections, emergency services and government communications all become more expensive when connectivity is unreliable. Phase3's right-of-way model can be valuable if it gives public institutions a physically diverse path and a provider with field access outside the ordinary road trench. But public-sector continuity also raises the evidence standard.

Government buyers need transparent procurement, enforceable SLAs, route diversity, security controls and documented incident response. A public-sector claim in a brochure is not the same as a public-sector continuity record.

The same distinction applies to schools, hospitals and underserved areas. Phase3's Niger route and satellite materials address the digital-divide story: https://guardian.ng/technology/phase3-telecom-expands-fibre-optic-cable-link-in-west-africa/ and https://www.phase3telecom.com/wp-content/uploads/2024/01/Phase3-Corporate-Profile.pdf. Yet the economics of thin routes are hard. A low-income or remote area may need subsidy, anchor tenants, public-sector demand, wholesale aggregation or cross-border traffic to make capacity profitable. The aerial route can reduce civil-work cost, but it does not eliminate customer acquisition cost, repair distance, power dependence, customer equipment cost or the risk that traffic volumes lag the build.

Market signals point to a high-friction operating environment

Nigeria's network environment gives Phase3 both opportunity and pressure. TechAfrica News reported in May 2025 that fibre cuts, vandalism, power outages and infrastructure theft caused over 30 telecom disruptions in Nigeria, citing NCC's major outage reporting portal: https://techafricanews.com/2025/05/21/nigerias-telecom-networks-hit-by-over-30-outages-in-may-2025/ and https://uptime.com/statuspage/ncc?end=20250521&start=20250422. That is not Phase3-specific. It is a market-level signal that customers have real reasons to pay for diversity. It also implies that any provider promising continuity faces a severe operating environment.

NCC's 2024 report shows cost pressure in adjacent segments. ISP revenue rose sharply, but operating cost rose faster and was attributed to high energy costs: https://ncc.gov.ng/sites/default/files/2025-11/2024-Year-End-Performance-Report.pdf. Collocation and infrastructure-sharing operators also reported large operating-cost increases. Those figures do not disclose Phase3's own economics, but they reveal the cost climate in which Phase3 sells. Aerial fibre over power infrastructure may avoid some trenching costs, yet it cannot escape energy, security, personnel, equipment, foreign exchange, customer-support and repair exposure.

Unofficial signals are weaker but still useful if kept in their lane. Indeed reviews suggest Phase3 has had field technicians, support staff and geographically distributed repair work: https://ng.indeed.com/cmp/Phase3-Telecom/reviews. The LinkedIn maintenance role asks for hands-on fibre installation, maintenance, splicing and OTDR troubleshooting: https://ng.linkedin.com/jobs/view/network-operations-and-maintenance-officer-at-phase3-telecom-limited-at-phase3-telecom-4176818776. The public support page gives response-time language that may be slower than a carrier-grade SLA unless a separate enterprise contract applies: https://www.phase3telecom.com/contact-support/. None of these prove service quality. Together, they reinforce the practical point that the company's economics depend on field labour and support discipline as much as route rights.

The missing evidence falls into economics, reliability and retention

The public record leaves three evidence classes open. The economics class is the biggest. Phase3 is private, so the article cannot see route-level revenue, EBITDA, utilization, average revenue per wholesale customer, capitalized concession costs, repair cost per kilometre or price realization on dark fibre and backhaul. Phase3 says it has invested heavily and operates 10,000 km of coverage, but a buyer or investor would need current route utilization, contract duration and churn to know whether the asset is earning a return.

The reliability class is next. Phase3 publishes support claims, NOC claims, field-maintenance claims, aerial-fibre claims and availability language. The public record does not give audited uptime by route, MTTR by region, incident frequency, power-line access delays, customer credits, trouble-ticket closure times or independent latency history. The 2020 TCN access story and 2018 concession dispute make reliability evidence especially important because the route right is operational as well as legal.

The retention class is narrower but still material. Phase3 names broad customer categories, regional partners and use cases. It does not publish renewal rates, anchor customers by route, wholesale volume commitments, enterprise net revenue retention or public-sector contract continuity. Retention is where the buyer's failure cost becomes visible. If carriers and enterprises renew despite cheaper substitutes, the aerial route is likely solving a real continuity problem. If accounts churn after incidents or after publicly financed fibre expands, the route advantage is thinner.

Those gaps should be grouped, not exaggerated. Economics evidence would improve with utilisation by corridor, contract backlog and repair cost per kilometre. Reliability evidence would improve with route-level uptime, MTTR and incident-credit history. Retention evidence would improve with renewal rates and named anchor accounts where disclosure is possible. A long list of missing datapoints would make the company look unknowable, which is not fair. The public record is already enough to understand the business mechanism.

What remains missing is the private evidence that separates a plausible aerial-fibre story from a high-return route portfolio.

The judgement

Phase3 Telecom is most compelling when read as a right-of-way and repair company that happens to sell telecom services, not as a generic broadband provider. Its distinctiveness comes from the ability to use power transmission infrastructure for aerial fibre, translate that reach into wholesale and enterprise products, and offer customers a route that can differ physically from ordinary terrestrial fibre.

The evidence supports the existence of a serious operating platform: official service pages, a 10,000 km coverage claim, power-infrastructure right-of-way claims, NOC and field-maintenance claims, regional corridor announcements, NCC licensing context, ICRC concession-resolution context, AFRINIC records and AS37248 public routing evidence.

The caution is equally clear. Aerial fibre lowers some civil-work and route-cut risks while introducing dependency on power-line access, concession stability, substation coordination and field repair. The TCN dispute history is not an old footnote; it is the public demonstration that the company's most valuable route surface can become a governance and access issue. The 2026 public licence evidence also deserves clean renewal confirmation rather than assumption. Network records show public presence, not internal performance. Product pages show the menu, not margin. Announcements show strategy, not utilization.

For the opening buyer, the answer is therefore conditional. If the choice is between Phase3 and a second terrestrial circuit that follows the same road exposure, Phase3's aerial path can be economically attractive because it may reduce correlated failure and avoid part of the digging-right-of-way problem. If the choice is between Phase3 and microwave for a remote spur, satellite for emergency backup, or a private leased line from a larger operator, Phase3 wins only when its route diversity, latency, repair access and contract assurance lower the customer's total failure cost.

If route repair is slow, licence evidence is unclear, concession access becomes contested, or regional corridor demand does not fill capacity, the power-line advantage becomes a maintenance burden. Phase3's contract depends on power-line reach, but the margin depends on turning that reach into repairable continuity.