Summary

- Norlys-Fibernet Sinal A/S is best understood as a wholesale fibre infrastructure company whose open-access network can create visible retail choice while retaining a powerful role over the cost base beneath that choice.

- The most important tension is not whether Danish consumers see many broadband brands. It is whether wholesale charges, operational systems, service assurance and network consolidation leave those brands enough room to compete on lasting price and quality.

- Sinal's scale argument is credible: fibre rollout, platform migration, security investment and rural density economics require large fixed costs and steady take-up. The same scale also increases the need to test whether open access is producing infrastructure-level competition or a utility-backed toll collected through different retail fronts.

- The weakest evidence hinge is wholesale margin transparency. Public filings, regulator papers and retail-provider statements reveal the structure, but they do not fully show address-by-address access fees, provider margins, repair performance or churn economics.

The household sees brands, but the line owner sets the range

Start with a normal Danish household. The residents type an address into a broadband shop and see a set of retail names. One provider offers an introductory fibre price. Another offers a router, Wi-Fi support and a shorter binding period. A third says 5G will be enough. A fourth leans on television or streaming bundles. On the surface, this looks like ordinary consumer choice: pick a speed, pick a price, pick a service desk.

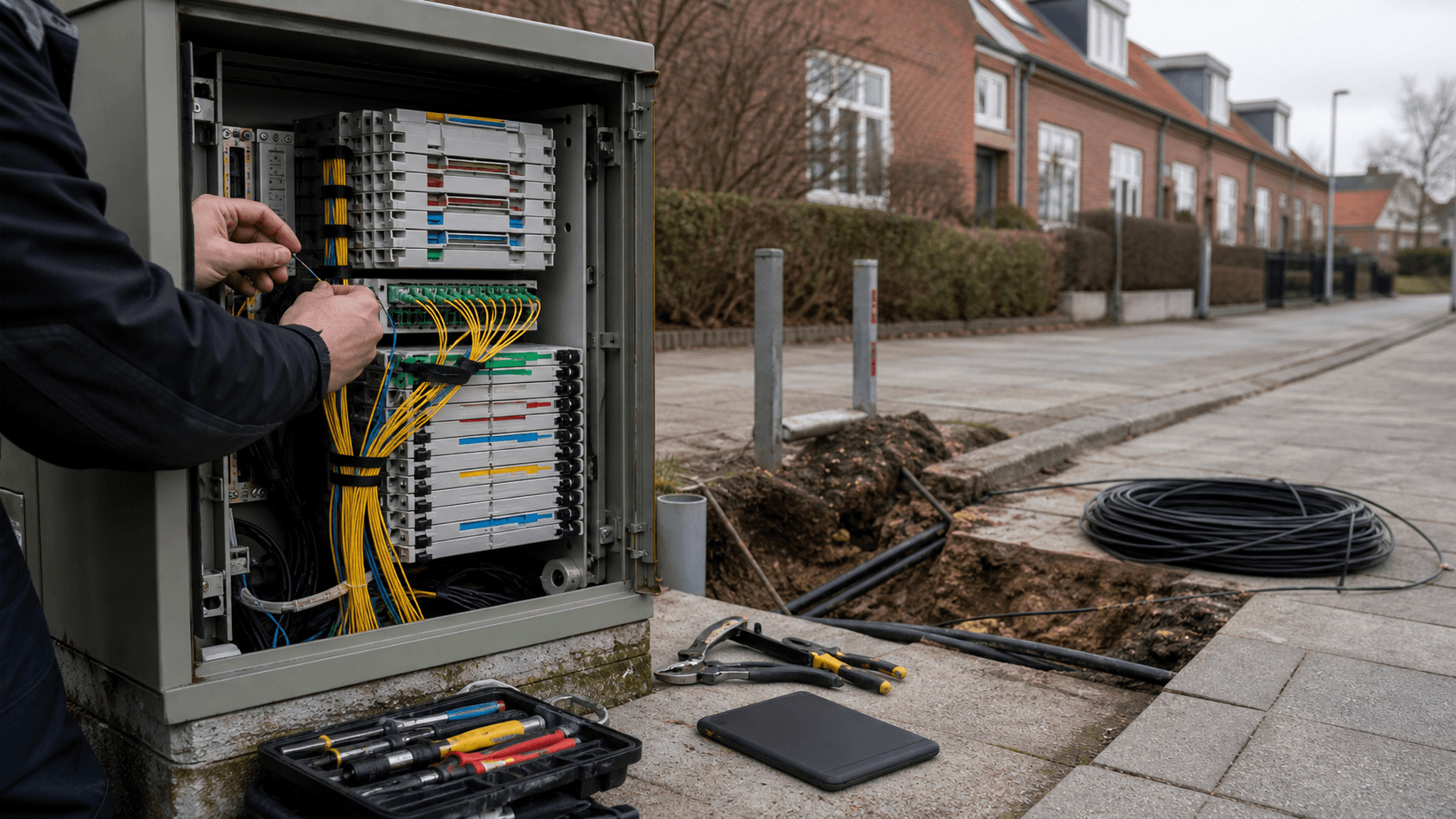

For Norlys-Fibernet Sinal A/S, the more revealing question is different. Which physical line reaches the wall? Which wholesale platform lets a retail provider activate service? Who repairs the line when a fibre box fails? Who decides the access product and price envelope that each retail provider must absorb before it can discount? That is where the retail shelf turns into a wholesale access economy.

Norlys says directly on its consumer open-choice page that Denmark's largest underground fibre cable network is owned by the group but made available to other internet and television providers. Its "Frit valg" page lists retail providers and tells households to choose among them after checking the address. That is the promise of the open-access model: one expensive fibre network can support many retail front ends, avoiding the waste of digging parallel networks down every rural road while still giving households more than one brand to call.

The promise is real, but it is incomplete. If one wholesale fibre owner carries the address and other providers pay to use that line, retail choice can still sit inside a narrow economic corridor. A provider may be able to market a cheaper first-month campaign, but not if the wholesale access charge leaves too little margin. It may be able to promise better customer service, but the repair path still depends on the wholesale line owner and the ordering systems that connect provider, platform and network.

It may be able to sell a 1 Gbit/s product, but the speed tier, fibre box, migration timing and service assurance are all shaped before the retail brand appears.

This is why Sinal matters. It is not just another Danish internet brand. It is the company that holds the wholesale fibre surface beneath a large part of Denmark's retail broadband choice. Sinal's own 2025 annual report says the company owns, expands, operates and maintains a fibre-based communication network, and develops, markets, sells and distributes fibre connectivity services to external service providers on a wholesale basis. It calls the network the largest and most densely deployed in Denmark and says it is open to multiple service providers through OpenNet. Those lines in the Sinal 2025 annual report are the analytical center of the company: the customer may buy from a retail provider, but the durable asset is the fibre access network.

The Sinal name exists because the old Norlys label blurred the market

The company's change from Norlys Fibernet to Sinal is not a cosmetic footnote. It is a market signal. In June 2025, Sinal said the new name was meant to make clearer which tasks are handled by the fibre network owner and which are handled by service providers. The announcement described the fibre company as the owner of Denmark's largest fibre network, with more than 900,000 addresses, and said the fibre company sells services on an open network to service providers for private and business customers. The same Sinal name-change announcement also acknowledged a source of confusion: Norlys both owned the network and operated on the network with internet, television and streaming, but through different companies.

That sentence is unusually important. It tells the reader why the name needed to change. In open-access fibre, separation is not just an org chart question. It is the foundation of trust. A wholesale network owner must persuade outside service providers that it will not quietly favour its related retail business. A retail customer must understand why a provider can offer service at an address but may not control the underlying installation or fault process. A regulator must decide whether a separated wholesale company is behaving like an open platform or like a gatekeeper.

The current ownership structure adds another layer. PGGM announced in 2022 that Norlys had agreed to sell a 35 percent stake in its wholesale fibre business to a consortium led by PGGM and including EDF Invest. PGGM framed the transaction as a large European fibre deal and a way to support continued development of the network. That PGGM announcement is useful because it separates two ideas that are often blended in consumer advertising: a member-owned Danish utility heritage on one side, and institutional infrastructure capital seeking long-term returns on the other.

Neither idea is automatically negative. Fibre networks require large upfront capital, long payback periods and a tolerance for slow rural economics. Institutional money can help finance that. But the ownership mix makes the wholesale toll more visible. If a fibre line is treated as long-life infrastructure, the investment case depends on stable cash flows from access. If the same line is sold to households through a shelf of retail brands, the question becomes who absorbs the cost of that stability: the retail provider, the final household, or both.

Sinal's 2025 filing shows the financial shape of that infrastructure business. Revenue rose to DKK 1.474 billion in 2025 from DKK 1.389 billion in 2024. Profit from primary operations improved to DKK 309 million, but net profit was still a loss of DKK 11 million after financial expenses and tax. The company reported DKK 666 million in property, plant and equipment investment in 2025 and a balance sheet total above DKK 10.8 billion. Those numbers do not describe a light reseller. They describe a capital-heavy owner of ducts, fibre plant, electronics, development projects and debt-funded network assets.

That is the reason the household's address check matters more than the advertising banner. The retail brand can change every six months. The line and the wholesale economics are slow-moving.

Open access reduces duplication while moving the competition fight into systems and terms

The open-access model is easy to praise at a high level. It can let one fibre owner achieve higher utilisation while retail providers reach more households without digging their own network. OpenNet presents exactly that logic: its homepage says it provides a cooperation model and IT platform for opening fibre networks, making it easier for network owners and service providers to work together, and it says its Danish platform covers more than 1.1 million addresses. The OpenNet homepage describes the value proposition as lower complexity, higher network utilisation, wider reach for providers and standardised platform processes.

OpenNet's own history page makes the same economic point more explicitly. It says the company was founded in 2017 to make it easy for network operators and service providers to collaborate through a standardised platform and equal terms, creating many-to-many relationships rather than a separate model and process for each partnership. By 2024, OpenNet said it had 26 partners and more than 1.1 million available addresses. That is the infrastructure-market dream: a provider does not have to negotiate one-off integrations for every local fibre owner, and a fibre owner can avoid the low utilisation that comes when a network is open only to its own retail arm.

But open access does not make the cost problem disappear. It moves the fight into product definitions, interfaces, access fees, repair workflows, service levels, data exchanges and migration systems. The household sees a shopping page. The service provider sees a wholesale order, an H1 product, a point of interconnect, a service-level commitment, a fault-reporting path and a bill from the access owner.

Norlys' own wholesale page lists standard products such as Wholesale Fiberaccess, dark fibre, mast positions and DWDM, and describes operator agreements that can include H1 standard fibre connections for private households, H2 fibre connections for larger businesses, H3 cable-TV products and POI connections between service provider and network owner. Those details on the Norlys wholesale page are not consumer marketing decoration. They are the anatomy of the market. They show that the retail experience is assembled out of wholesale access products and technical handoffs.

The role of software is just as important. In 2022, Cerillion said its BSS/OSS system helped Norlys expand through connectivity into the national open-access wholesale platform, automate service fulfilment for new fibre services and make the Norlys fibre network accessible to other Danish service providers through a standardised wholesale gateway. The Cerillion release also made the structural point that separating infrastructure owners from service providers had put Denmark near the front of fibre broadband models.

That sounds technical, but it is economics. If fulfilment is slow, providers bear customer-care cost. If address data is wrong, retail conversion suffers. If the wholesale platform is efficient, a provider can sign up a customer and switch service with fewer manual exceptions. If the platform is clumsy, retail competition looks broad in a list but narrow in practice. For Sinal, the operational system is part of the wholesale product.

Scale is Sinal's best defence and the source of the hardest scrutiny

Sinal's strongest argument is scale. Fibre rollout is not like adding a new phone plan. It requires civil works, permits, contractors, local coordination, electronics, customer premises equipment, maintenance crews, security work, power backup, software, network monitoring and support processes. Rural density makes the economics harsher because each metre of trenching may pass fewer paying households. A network that reaches scattered homes in Jutland needs high take-up, patient capital and an operating model that spreads fixed costs over many addresses.

Public data supports the idea that Denmark has largely moved into a fibre-and-gigabit era. The Danish digital authority's broadband mapping page says the annual mapping is collected from operators at address level and covers technically possible speeds, supplied speeds, technologies and provider availability. Its 2026 national background data show that 92.3 percent of homes and businesses had fibre access and 98.2 percent had access to 1 Gbit/s download speeds. For homes alone, the same workbook says 91.9 percent had fibre and 98.3 percent had access to 1 Gbit/s download speeds.

The subscription side points in the same direction. The 2025 telecom statistics workbook on the Danish telecom statistics page reports 2.409 million fixed internet subscriptions at year-end 2025. Fibre accounted for 1.448 million of them, compared with 643,378 cable-modem subscriptions and 119,052 xDSL subscriptions. The same data show fixed broadband median download capacity at 587.4 Mbit/s in 2025 and fibre median download capacity at 798.6 Mbit/s. Those are not early-adopter numbers. They describe a mass-market infrastructure transition.

If Sinal did not exist, Denmark would still need someone to bear the fixed cost of making that transition real in its geography. The company says the network reached more than 900,000 addresses before the EWII acquisition. Its 2025 annual report says it invested in security against physical intrusion, software and hardware replacement, energy-efficient solutions and upgrades that support speeds up to 6 Gbit/s. In January 2026, Sinal said the completed EWII deal would move it beyond one million addresses and give it scale to invest in a secure and stable network.

That January 2026 Sinal announcement is the cleanest version of the scale defence. It says the EWII network in the Triangle Region adds 135,000 addresses, lets customers choose among 18 internet and TV providers active on Sinal's network, and will involve migrating customers over the next few years to a newer platform with lower energy consumption, greater capacity and speeds up to 6 Gbit/s. It also says nearly 50 EWII Fibernet employees would join Sinal.

Scale, then, is not an empty slogan. It can reduce unit costs, support platform upgrades and maintain local operational knowledge. But scale also creates the need for scrutiny. If one network owner becomes the main wholesale access route over a region, then each price model, remedy, product definition and repair process carries more market weight. The same scale that helps Sinal finance future-proof fibre can also make retail providers dependent on its wholesale terms.

The retail shelf is real, but its prices are bounded from below

The retail shelf should not be dismissed. It is meaningful that households on Sinal's network can see multiple providers. Norlys' public page lists names such as Altibox, Bahnhof, EWII, Fastspeed, Hiper, Telenor, Waoo and YouSee. In 2024, Norlys welcomed Bahnhof and said households with Norlys fibre could choose broadband from the Swedish provider, increasing the count of active providers from 12 to 13. The Bahnhof announcement stressed that the deal came through OpenNet and that it was OpenNet's first foreign-provider onboarding to Danish fibre.

The retail shelf also has competitive language. Hiper advertises 1000 Mbit fibre from DKK 99 per month for the first six months on selected addresses, with a post-promotion price from DKK 319 per month. The Hiper page makes clear that the offer applies only to fibre at selected addresses. Telenor says fibre can deliver up to 1000 Mbit and tells households to check which solution is available at the address. The Telenor fibre page sells speed, router and support. EWII advertises fibre and cable internet, with fibre from DKK 339 per month and campaign terms that depend on where EWII can deliver. The EWII retail page is another reminder that consumer choice is address-based, not just brand-based.

Those retail pages prove that service providers can differentiate. They do not prove that the wholesale layer is disciplined. A provider can discount a first period to win a customer and then return to a normal price. It can bundle support or security. It can compete on cancellation terms. But its sustainable price floor is still shaped by wholesale access, customer acquisition cost, churn, support cost, bad debt, router cost, billing cost and the margin needed to survive.

That is why Fastspeed's 2026 move matters. Fastspeed, a retail provider known for competing across fibre networks, announced that it had stopped all new sales on Sinal's network with immediate effect. Its February 2026 statement said the decision followed announced price increases from July 2026 and a proposed commitment package under market testing, which Fastspeed said could raise the maximum fibre lease price for a 1000 Mbit product by up to DKK 200 excluding VAT compared with the current level. Fastspeed also argued that Norlys' related retail business would not face the same cost burden in practice.

Fastspeed is an interested party, and its claims should be read as a provider's argument in a live regulatory and commercial dispute rather than as neutral fact. Still, the signal is important because it comes from inside the open-access retail layer. A retail provider can complain loudly and still keep selling if margins are merely uncomfortable. Stopping new sales says the provider believes the future wholesale corridor is too risky for customer promises at that address set.

The wider customer-market chatter points in the same direction, with the usual caution that forum posts are anecdotal. In one Danish tech-support discussion, a user said they could switch providers every six months in search of better prices but could not access some attractive campaigns because their physical fibre was Norlys-based; replies focused on the buried infrastructure, not the router or retail logo. That Reddit thread is not evidence of wholesale pricing by itself. It is evidence of how consumers experience the market: the retail brand is visible, but the line owner is the constraint they learn to ask about.

The EWII remedy shows competition policy cares about infrastructure alternatives, not brand count alone

The most concrete public intervention around Sinal is the EWII acquisition. In August 2025, the Danish Competition Council approved Norlys Fibernet A/S, now Sinal A/S, acquiring EWII Fibernet A/S only subject to remedies. The English decision summary said the council could not approve the deal unconditionally because of a risk that the merger would reduce competition and lead customers to pay more for broadband and TV. The concern focused on around 135,000 end users in the EWII area, especially customers who could not opt out of Norlys because Norlys would own the fibre network and be the sole supplier to their antenna association.

That is a revealing competition theory. The authority did not say that a list of retail brands was enough. It looked at the alternatives available at the infrastructure and local-association level. In the Triangle Region, many households had access to EWII fibre and another high-capacity route through coaxial networks tied to antenna associations. If Norlys controlled both the fibre network and the retail/coax route in those local arrangements, the number of retail brands elsewhere would not answer the local problem.

The remedy required Norlys to ensure that seven antenna associations in the Triangle Region would get a different broadband and TV supplier than Norlys, and that Norlys would not achieve full or partial influence over those activities for a period. EWII's own August 2025 statement described the conditional approval and said EWII had spent nearly 20 years rolling out fibre to all addresses in the Triangle Region. Sinal's 2026 completion announcement then said the deal could proceed because Norlys had fulfilled the commitment related to those seven antenna associations.

This is the wholesale-versus-retail question in regulatory form. If open access always guaranteed competition, the authority would not have needed such a remedy. The concern was that infrastructure concentration and retail arrangements could reduce the practical alternatives for households. The solution was not to remove Sinal from the fibre market, but to protect a competing local route and separate Norlys' customer-facing activity from certain association supply.

For Sinal, the deal is strategically coherent. It adds a dense and economically important region around Vejle, Fredericia, Kolding, Middelfart and Vejen. It brings employees who know the network. It pushes the address footprint past one million and improves the business case for platform upgrades. For the market, the same deal raises the stakes of wholesale discipline. A larger Sinal can invest better, but it also becomes harder for retail providers to ignore.

Market-testing the wholesale toll is the real test of open access

The 2026 market-test process around fibre commitments makes the hidden toll explicit. In February 2026, the Competition and Consumer Authority said fibre companies with strong market positions were putting commitments into market testing. The authority's announcement said decisions are made in five-year periods, target areas where competition problems have been identified, and use a techno-economic model to calculate price caps for building and operating telecom networks in Denmark. It also said commitments sent to market testing are not legally binding at that stage and can be revised before a final decision.

Norlys Group's draft commitment for market testing is especially useful because it sets out the separation in formal terms. The Norlys Group draft commitment PDF says the group had structured its activities so that Sinal is the legal owner of fibre wholesale infrastructure, while the customer company Norlys is the legal owner of the retail business. It says Sinal and the customer company operate as separate companies with distinct business objectives, boards or management structures, employees, budgets and financial administration. It then defines Sinal's H1 fibre access product, service-provider access through a standardised platform and a point of interconnect.

That formal separation matters. It is what allows retail providers to say they are buying access from a wholesale company, not merely reselling a rival's retail product. But the same document also shows why the market test is hard. The H1 product is a mass-market fibre Ethernet layer-2 access product. Providers can use their own customer equipment, buy different speed tiers within Sinal's technical limits, receive access through saleable addresses and connect through central interconnect points. The product is not vague. It is built out of specific wholesale characteristics that can be priced, audited and disputed.

Fastspeed's objection lands exactly here. If the wholesale maximum price rises sharply, and if the related retail business is perceived as less exposed to the same effective burden, the public promise of separation is tested. Sinal can answer that price caps should reflect real costs, security investments, platform upgrades, debt service and the economics of a network that covers lower-density regions. Retail providers can answer that an open network is not meaningful if the toll consumes the competitive margin.

The available public record does not fully settle the dispute. The regulator's final decision, the detailed cost model, provider responses, actual wholesale invoices, retail gross margins and address-level performance data would be needed to prove who is right. But the dispute itself changes the analysis. It shows that the central commercial fight is no longer whether Sinal can attract retail names to a list. It is whether those names can compete through a full customer lifetime when wholesale terms change.

Operational labour is part of the product, not a back-office detail

Wholesale fibre economics often sound like finance and price caps, but the product is also labour. Someone has to survey the street, coordinate civil works, install or replace the fibre box, manage faults, answer retail-provider tickets, update address databases, keep electronics patched, secure physical sites, maintain power resilience and migrate customers from older platforms to newer ones. The labour is local, technical and recurring.

Sinal's own materials make this visible. Its January 2026 EWII completion announcement says nearly 50 EWII Fibernet employees would move to Sinal and that their knowledge would be important for migrating 135,000 addresses. Its 2025 annual report says the company invested in securing the fibre network against physical intrusion and in replacing and maintaining software and hardware. A separate SFC Energy announcement says SFC would supply hydrogen fuel-cell emergency power for point-of-presence stations in Norlys Fibernet's fibre optic broadband networks, with 235 kW of capacity installed between August and December 2025. That SFC Energy announcement is a niche source, but it points to a real cost category: critical access networks need power backup, not only marketing.

Operational scale also appears in network-resource evidence. PeeringDB lists Sinal's AS39642 as a regional cable/DSL/ISP network with substantial traffic levels and a record of public peering locations. That does not make an ASN or peering record into a company profile by itself, and it should not be overread as proof of retail competition. It is evidence that Sinal's footprint includes network operations beyond a static fibre map.

This labour dimension strengthens Sinal's case that wholesale access cannot be priced as if fibre were already paid for and maintenance-free. A household may think the line is "in the ground" and therefore cheap to use after installation. In practice, a wholesale fibre owner must keep the passive and active network working, integrate retail orders, dispatch technicians and invest in upgrades. The question is not whether Sinal should earn money from that work. It is whether the amount and structure of the wholesale toll allow independent retail pressure to survive.

That is where local support labour becomes a market issue. If retail providers depend on the wholesale owner for installation appointments, repair status and fibre-box replacement, then poor wholesale service can damage the retail provider's brand. If wholesale response is strong, a small provider can compete despite not owning the line. If wholesale response is weak or uneven, retail choice becomes more fragile because customers blame the brand they pay even when the fault path sits underneath it.

5G, cable and second fibre lines are outside checks, but not equal at every address

Sinal does not face a world with no substitutes. Danish households increasingly compare fibre with cable, 5G fixed wireless and, in some places, a second fibre line. Norlys itself sells 5G and cable products alongside fibre. Hiper advertises fibre and 5G. EWII sells fibre and cable. The telecom statistics show cable still had 643,378 subscriptions at year-end 2025, while fixed wireless and satellite were much smaller but visible categories. These technologies can cap the wholesale toll if customers can actually switch.

The problem is address specificity. A household in a dense town may have coax, fibre and 5G options. A rural household may have one high-quality fixed line and mobile broadband that is acceptable only in some conditions. The Danish broadband mapping tool is built around that reality: it is address-level rather than national-average. A national gigabit statistic does not tell a household whether two independent high-capacity networks reach the same wall.

The EWII remedy again matters because it treated high-capacity alternatives as local facts. The concern was not "Denmark has many providers." It was "these households may lose a meaningful alternative." That is the right way to read Sinal's competitive exposure. In some addresses, 5G or coax may discipline Sinal because a retail provider can move the customer to another access route. In others, the only realistic high-speed fixed path may be Sinal's fibre, and the wholesale terms become the main constraint.

This also explains why consumers in online discussions often talk about "whose fibre" rather than only "which provider." The market has taught them that campaigns can be address-limited. A provider that advertises a low introductory fibre price may not offer it on every wholesale network. A user who sees neighbours getting a lower campaign on another network does not experience Denmark as a single retail market; they experience it as an address market shaped by the buried line.

For Sinal, substitutes cut both ways. 5G competition can pressure the company to improve activation, customer journey and pricing. Its parent group has expanded into mobile, making fixed-mobile substitution a real strategic factor. But fixed wireless does not erase the fibre toll question because fibre remains the premium access product for symmetric capacity, low latency, high household data use and business reliability. The bigger data loads become, the more valuable a stable fibre line is. That can strengthen both the social case for fibre investment and the commercial power of the fibre owner.

The weakest evidence hinge is the margin between wholesale and retail

The hardest question is whether public wholesale offers, group reporting and regulator data reveal real infrastructure competition or simply a utility-backed fibre toll collected through different retail fronts. The honest answer is that the public evidence is strong enough to identify the risk but not strong enough to close the case.

We can see Sinal's role. Its filings state that it sells wholesale fibre connectivity to external service providers. We can see its scale. Its network passed more than 900,000 addresses before EWII, and more than one million after the completed acquisition. We can see its capital intensity. The company has a balance sheet above DKK 10.8 billion, large fibre assets, high depreciation and major investment. We can see formal separation. The market-test draft separates Sinal's wholesale infrastructure from Norlys' retail business. We can see retail choice.

The public provider list and Bahnhof onboarding show multiple brands on the network. We can see provider friction. Fastspeed's sales stop says at least one retail competitor believes the future wholesale price corridor could become untenable.

What we cannot see fully is the margin. Public filings do not show the average wholesale fee paid by each provider by product tier and address type. They do not show the effective discounting, installation charges, repair penalties, migration costs or service credits that shape provider economics. They do not show whether Norlys' related retail business bears the same effective cost, at the same timing, with the same working-capital burden and the same operational consequences as outside providers. They do not show customer lifetime value by wholesale network.

They do not show fault duration by provider in a way that would let outsiders test whether open access is operationally neutral.

Those are not minor gaps. They are the difference between open access as a competitive mechanism and open access as a branded reseller layer over a local toll road. The central tension cannot be resolved by counting retail logos. It has to be resolved by testing prices, service quality and provider outcomes over time.

The facts that would change the judgement are concrete. If final regulator decisions set price caps that leave efficient retail providers room to sell competitively, that would support Sinal's open-access claim. If independent providers keep entering the network, retain customers, publish competitive standard prices after promotions and avoid repeated margin disputes, that would support the same view. If Sinal publishes or makes available credible equivalent-input metrics showing equal terms, equal repair performance and equal wholesale treatment for related and unrelated providers, the separation case becomes stronger.

The opposite facts would point the other way. If multiple independent providers stop new sales on Sinal's network, if address-level campaigns disappear while related retail offers remain viable, if wholesale price increases outpace visible cost drivers, if repair or activation metrics favour the related retail arm, or if households in Sinal-heavy areas consistently face higher standard prices than similar households with alternative fibre or coax routes, the open-access model would look less like infrastructure competition and more like a toll collected through retail masks.

Sinal's market power is not a defect unless the toll becomes the product

The practical judgement is balanced but not neutral. Sinal is an important infrastructure company because it has built, bought and operated fibre in places where parallel networks may not be economically rational. Its scale helps Denmark sustain high fibre availability, migrate to higher speeds, improve resilience and let retail providers reach homes without duplicating civil works. The company should not be analysed as if it were merely a retail ISP with a big marketing budget. It is closer to a regional utility-fibre platform with telecom, software, finance and local labour inside it.

But that is exactly why the toll matters. A utility-fibre platform can enable competition only if its wholesale terms are disciplined enough for retail providers to win and keep customers on more than introductory loss leaders. If the toll rises too far, the retail shelf becomes less important. The household still sees multiple brands, but the brands all inherit the same expensive line. The price difference narrows, campaigns become address-limited, provider switching becomes less powerful and the final customer learns that the real choice was made when the fibre owner reached the wall.

Norlys-Fibernet Sinal A/S therefore sits at the most important point in Denmark's broadband market: between the promise of many retail providers and the fixed cost of one access line. Its public story is that separation, open access and scale let Denmark have both efficient infrastructure and consumer choice. The market's unresolved worry is that wholesale access can become a toll strong enough to decide what competition costs before the household ever sees a retail offer.

The Danish household at the beginning of this article may still be right to compare brands. Service, router quality, contract terms and first-year price all matter. But the more durable question is below the checkout page. The hidden fixed cost is the trench, the fibre, the platform, the service handoff, the repair crew, the power backup, the debt and the wholesale fee. Sinal's success should be measured not only by how many addresses it passes or how many providers appear on its list, but by whether those providers can keep turning the same fibre line into genuinely different and affordable choices.