Summary

- EBTTIKAR TECHNOLOGY Company Ltd is most plausibly a Saudi enterprise technology service account, not a pure commodity hosting shop. Its own website presents managed services, cloud and infrastructure, cybersecurity, SOC and NOC, telecom services, consultancy, healthcare digitisation and technology partnerships as the commercial surface.

- Public registry evidence is real but narrow. RIPE records identify EBTTIKAR as ORG-ETCL2-RIPE, a Saudi LIR in Riyadh, and AS211226 as EBTTIKAR. RIPEstat showed AS211226 announced on 7 July 2026 with one visible IPv4 /24, 256 IPv4 addresses, one observed neighbour and no visible IPv6 routing.

- The paid account should be defined early: a buyer is paying for hosting, cloud or data-service continuity across systems, support response, monitoring, upstream coordination, localisation and migration avoidance. The substitute set is hyperscale cloud, another local host or managed-service provider, a reseller platform, an in-house server, a website builder, or delayed migration.

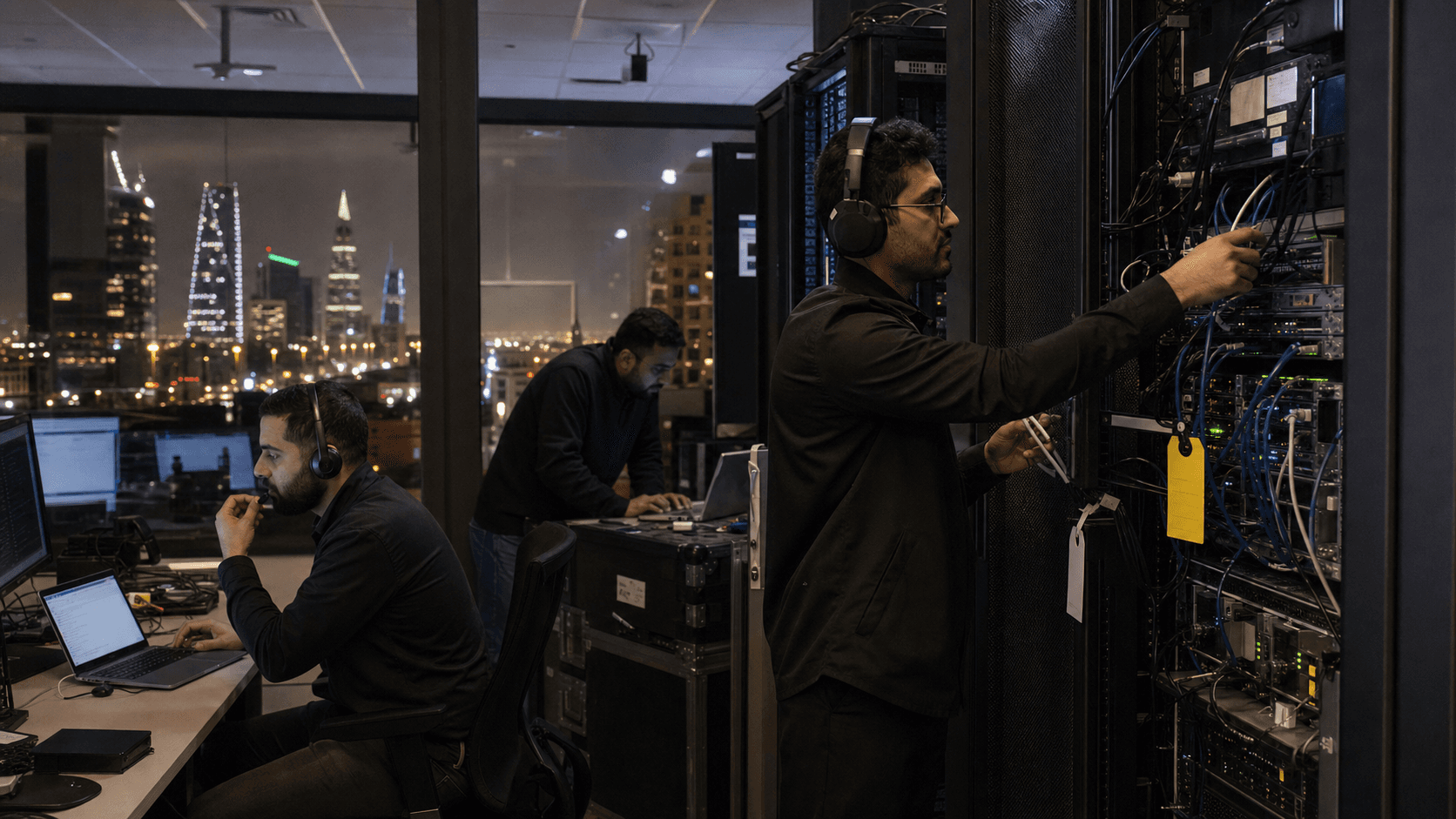

- The company's strongest public economic evidence is support labour and operational breadth. EBTTIKAR's public pages describe 24/7 SOC/NOC, managed services, IT service management, incident response, cloud and data-centre operations, telecom engineering, wireless networks, and project metrics such as staff counts and ticket volume. Those are company-published claims, not verified contracts.

- The public record leaves major limits: no audited revenue, no confirmed customer names, no verified facility ownership, no uptime history, no churn data, no supplier contracts, no margin disclosure and no independent contract evidence. Those limits are part of the economics because continuity businesses are valuable only if private renewal, support and reliability facts hold up.

The renewal begins with a continuity failure

The useful way to understand EBTTIKAR TECHNOLOGY Company Ltd is to begin with a buyer who has just learned that a system is more embedded than the procurement file suggested. A Riyadh operations manager sees a weekend failover test break because an application dependency, firewall rule, backup job or monitoring alert was known only to the incumbent support team. A finance manager then asks why the company should renew a broad technology services contract when cloud prices are visible and a cheaper provider is ready to bid. The technical team answers with the real cost: migration would not be a clean shopping exercise.

It would be an operating project.

That moment defines the economic unit. EBTTIKAR's relevant account is a hosting, cloud, managed infrastructure or data-service continuity account. The buyer pays for live systems to keep working, for support staff to know the environment, for local implementation labour to be available, for vendor products to be integrated, for cyber controls to be watched, for network dependencies to be managed, and for migration to be avoided until the business can handle it. Raw speed matters, but it is not the full product.

The substitute set is concrete. A buyer can move workloads to a hyperscale cloud, shift to another Saudi host or managed-service provider, use a reseller platform, rebuild on an in-house server, put a simpler public site on a website builder, or delay migration until a budget cycle or outage forces action. Each substitute has a different price. Hyperscale cloud can reduce infrastructure procurement and improve self-service. Another local provider can undercut labour rates or promise better service. A reseller can wrap global infrastructure in a local account relationship. An in-house setup can appeal to buyers who want control.

A website builder can remove the infrastructure question entirely for simple workloads. Delay is the cheapest choice until it is not.

The article's thesis is therefore not that EBTTIKAR is irreplaceable. It is that EBTTIKAR matters where a Saudi buyer pays for continuity across messy enterprise systems. The company's own home page at https://ebttikar.com/ presents it as an information technology services provider in Saudi Arabia, a subsidiary of N2V, and a business using digital transformation, managed services, infrastructure, cybersecurity, SOC and NOC, and physical security to help organisations streamline technology operations. That is a broad support account, not a narrow server-price list.

The public evidence needs discipline. EBTTIKAR's website is a company-owned source. RIPE and RIPEstat records are technical sources. Saudi regulatory pages are market context. None of them proves revenue, customer retention, margin, facility control or contract quality. Those gaps are not footnotes. They are central to pricing a continuity account, because the value of such a provider depends on things that are usually private: how quickly staff respond, whether monitoring catches incidents, whether backups restore, whether upstream suppliers cooperate, and whether buyers renew after stressful events.

What EBTTIKAR says it sells

EBTTIKAR's public service pages describe a firm built around enterprise IT operations rather than only around internet access. The about page at https://ebttikar.com/about-us/ says EBTTIKAR is headquartered in Riyadh, describes it as a leading IT solutions provider and subsidiary of N2V, and says it uses customer-centric delivery, strategic partnerships and innovation to provide cost-effective IT solutions. It also names artificial intelligence, data management and video analytics as areas of specialisation, while presenting partnerships with global technology vendors as part of the delivery model.

The cloud and infrastructure page at https://ebttikar.com/cloud-and-infrastructure/ is closer to the assignment's continuity theme. It says EBTTIKAR's cloud and infrastructure services simplify deployment, configuration, management and monitoring of data centres, and it lists IaaS, PaaS, SaaS, hybrid cloud, backup and disaster recovery, virtualisation, hyperconverged and converged systems, enterprise servers and storage, data protection, network automation, application delivery control, monitoring, Wi-Fi, collaboration and physical data-centre components. That does not prove EBTTIKAR owns a data centre. It proves the company wants to be paid for the operating layer around enterprise infrastructure.

The managed-services page at https://ebttikar.com/managed-services/ makes the labour component explicit. It says seamless IT operations are critical to business success, and describes end-to-end solutions for optimised, secure and continuously monitored technology infrastructure. It names IT service management, incident, problem, change, knowledge, asset and release management, CMDB and service catalogue, integration tools, self-service portals, endpoint management, network infrastructure, software and hardware asset management, SOC and NOC, service assessment, service design, service build, service run and service transformation.

That set of terms is economically important because it shows the product is not a box. It is a standing capability. The buyer is paying for people and process: asset records, escalation routines, knowledge bases, service catalogues, incident handling and change control. A server price can be compared in minutes. An operating relationship takes months to replace if the incumbent has built the runbook, knows the remote sites, understands the procurement preferences and remembers which exceptions were added after past incidents.

The consultancy page at https://ebttikar.com/consultancy-services/ adds another layer: assessment, testing, optimisation, consolidation, capacity planning, policy development, auditing, ITIL implementation, business continuity, disaster recovery, data-centre design and architecture, and IP and wireless services. Again, none of that proves customer success. It does define the account that EBTTIKAR is trying to sell: it is a services firm positioned to make technology decisions less disruptive for enterprise buyers.

The SOC and NOC page at https://ebttikar.com/soc-noc/ deepens the continuity argument. EBTTIKAR says it provides SOC-as-a-Service with round-the-clock monitoring, detection and response, and a NOC for monitoring, management and optimisation of IT infrastructure. It also names Cisco Managed XDR, Cisco Secure Endpoint, Umbrella, Email Security and Talos Threat Intelligence, plus SolarWinds and AppDynamics for network and application monitoring. That public wording points to a vendor-integrator model in which EBTTIKAR's value is partly the orchestration of upstream technology.

The cybersecurity page at https://ebttikar.com/cyber-security/ lists consultation, risk assessment, cyber-defence technologies, a cybersecurity centre in Saudi Arabia, essential cybersecurity controls, communication protection, NG-FW, NDR, ZTNA, DNS security, secure remote access, SASE, NAC, DDoS protection, endpoint protection, EDR, MDM, encryption, data classification, DLP, backup, secure email, web application and API protection, SIEM, SOAR, XDR, attack-surface management, breach and attack simulation, identity and access management, privilege access management, multi-factor authentication, GRC, threat intelligence, brand protection, vulnerability management, penetration testing, threat hunting and incident response. The breadth is attractive, but breadth also raises delivery risk. A company can list many controls; the economics turn on whether it has enough skilled labour and vendor backing to operate them under pressure.

The telecom-services page at https://ebttikar.com/telecom-services/ expands the company beyond conventional IT outsourcing. It describes wireless connectivity, partnerships with Rajant, Cambium Networks and Motorola Solutions, mission-critical communications, DMR, ATC and TETRA, camera and video-management systems, smart meeting rooms, wireless network expansion and managed services for network infrastructure. It also refers to certified engineers, end-to-end support, installation, maintenance and 24/7 monitoring. For a Saudi enterprise buyer, that matters because physical sites, wireless networks, cameras, branches and industrial environments can make IT continuity local and labour-heavy.

Taken together, the public pages point to a specific business model: EBTTIKAR sells operational continuity across enterprise technology stacks. The buyer does not simply buy hosting. The buyer buys a team that can design, implement, monitor, support, secure and change systems in Saudi operating conditions.

What public records prove

The strongest independent public evidence is not customer evidence. It is registry and routing evidence. RIPE's organisation entity at https://rest.db.ripe.net/ripe/organisation/ORG-ETCL2-RIPE.json identifies ORG-ETCL2-RIPE as EBTTIKAR TECHNOLOGY Company Ltd, organisation type LIR, country SA, registration number 1010183447, a Riyadh address on Prince Masaad bin AbdulAziz Street in Sulaymaniyah District, phone contact, admin and technical roles, an abuse contact and maintainer references. The entity was created on 14 April 2021 and last modified on 13 May 2026.

RIPE RDAP at https://rdap.db.ripe.net/entity/ORG-ETCL2-RIPE adds the linked resources. It ties the organisation to the IPv4 network 193.34.224.0 - 193.34.224.255, named SA-EBTTIKAR-20210416, with status active, and to AS211226, named EBTTIKAR. The RDAP record shows the network registration date as 16 April 2021 and the AS registration date as 3 June 2021. This is strong evidence that the company is a Saudi LIR and number-resource holder. It is not evidence of large hosting scale.

The aut-num record at https://rest.db.ripe.net/ripe/aut-num/AS211226.json identifies AS211226 as EBTTIKAR, links it to ORG-ETCL2-RIPE, lists status ASSIGNED, and records import/export policy entries with AS29690 and AS29684. Those two ASNs matter because they show the public routing relationship that EBTTIKAR represented in RIPE records. RIPEstat's overview at https://stat.ripe.net/data/as-overview/data.json?resource=AS211226 showed AS211226 announced on 7 July 2026, with holder "EBTTIKAR EBTTIKAR TECHNOLOGY Company Ltd."

The scale is small in the public routing view. RIPEstat's routing-status endpoint at https://stat.ripe.net/data/routing-status/data.json?resource=AS211226 showed one visible IPv4 prefix, 193.34.224.0/24, 256 IPv4 addresses, visibility from 324 of 325 RIS IPv4 full-feed peers, zero visible IPv6 space and one observed neighbour at the query time. The announced-prefixes endpoint at https://stat.ripe.net/data/announced-prefixes/data.json?resource=AS211226 listed 193.34.224.0/24 for the 23 June 2026 to 7 July 2026 interval.

That evidence should be read carefully. One /24 is enough to support real routing, management addresses, customer-facing services, VPN endpoints, monitoring systems, security platforms or internal continuity infrastructure. It is not enough to claim a broad independent hosting network. A company with one visible /24 can still be economically important as an integrator and managed-service provider, but the public network footprint does not support a story of large self-owned cloud capacity.

RIPEstat's ASN-neighbours endpoint at https://stat.ripe.net/data/asn-neighbours/data.json?resource=AS211226 showed one unique neighbour, AS29684, at the checked time. RIPEstat identifies AS29684 as "NOURNET-ASN Nour Internet Company for Communications and Information Technology Ltd." at https://stat.ripe.net/data/as-overview/data.json?resource=AS29684. RIPE's AS211226 aut-num also lists AS29690, which RIPEstat identifies as "ATHEER AI Jeraisy Electronic Services Company Ltd." at https://stat.ripe.net/data/as-overview/data.json?resource=AS29690. RIPEstat's routing-consistency endpoint at https://stat.ripe.net/data/as-routing-consistency/data.json?resource=AS211226 showed AS29684 present in both Whois and BGP, while AS29690 was present in Whois but not in the observed BGP path at that query time.

The upstream conclusion is precise. EBTTIKAR is visible as a Saudi number-resource holder with a routed /24 and an observed NourNet path. The record also contains a policy reference to Atheer/Al Jeraisy. The public data does not show commercial contracts, redundancy, physical links, service levels, route-security operations, or whether any customer workloads are on that space. The routing record supports operational substance; it also makes supplier dependence an explicit part of the analysis.

Route security is another public limit. RIPEstat's RPKI validation endpoint at https://stat.ripe.net/data/rpki-validation/data.json?resource=211226&prefix=193.34.224.0/24 returned status unknown with no validating ROAs for the visible prefix at the checked time. That is not proof of an incident, and many networks operate with uneven RPKI coverage. But for a provider selling continuity, route-origin authorisation is a diligence item. A buyer should ask whether the company plans to publish appropriate ROAs, how route changes are approved, and how quickly routing issues are escalated through upstream providers.

The paid account is continuity, not inventory

EBTTIKAR's economics make more sense when treated as a continuity account rather than inventory resale. If a customer only needs a public website and a few forms, a website builder can remove most infrastructure concerns. If a customer has a clean cloud-native application and an internal platform team, hyperscale cloud can be a strong substitute. If a customer needs cheap server capacity, another host or reseller can compete on price.

EBTTIKAR matters where the customer's environment is more complex: branches, cameras, endpoints, legacy applications, monitoring, help desk, cyber controls, wireless networks, data backup, application performance and local operating rules.

The account becomes sticky when the provider has the support memory. In a renewal meeting, the buyer may ask whether a lower-cost replacement can handle the same practical details: old equipment, procurement documents, Arabic and English working norms, vendor warranty procedures, urgent on-site work, incident communication, service-desk escalation, firewall policy, endpoint coverage, backup restoration and monitoring thresholds. If the answer is uncertain, the incumbent has renewal power.

This is why EBTTIKAR's public emphasis on IT service management matters. Incident, problem, change, knowledge, asset and release management are not decorative terms. They are the paperwork and habits that make continuity possible. A provider that maintains a CMDB, tracks assets, knows end-of-life equipment, documents recurring incidents and controls changes can make enterprise IT less fragile. A provider that merely sells hardware and reacts to tickets has less durable value.

The same logic applies to cloud and infrastructure. EBTTIKAR's cloud page uses terms such as hybrid cloud, backup and disaster recovery, data protection, software-defined data centre network, monitoring and management. Those categories are easy to list and hard to deliver. The valuable version is a service account that knows which workloads can move to cloud, which must remain on premises, which data must be backed up locally, which recovery target is acceptable, and which business unit will tolerate downtime.

The weaker version is product aggregation. If EBTTIKAR mainly resells vendor tools and relies on third parties for the critical parts of delivery, gross margin and control may be thin. Vendor access may still be valuable, especially in Saudi Arabia where localisation, Arabic support, procurement and site work matter. But a reseller-heavy model gives the buyer more reason to compare EBTTIKAR with another partner carrying similar upstream products.

The public record does not settle that distinction. EBTTIKAR's site lists many services, tools and partnerships. It also gives company-published project signals. But it does not publish audited utilisation, renewal rates, service-level penalties, product margin, labour margin, facility ownership, upstream contracts or verified customer statements. The fair conclusion is conditional: EBTTIKAR's public offer is designed around continuity; the strength of the business depends on private evidence of execution.

Saudi enterprise IT continuity is labour-heavy

The Saudi operating context makes local support labour more than a convenience. Enterprise IT projects often involve site access, procurement documentation, security review, bilingual or Arabic-first operational coordination, vendor certifications, government-aligned cyber controls, branch networks, physical security, wireless deployments, and continuity expectations around business-critical services. A global cloud console does not remove all of that work.

EBTTIKAR's public contact page at https://ebttikar.com/contact-us/ places the company at 8132 Prince Musaad Bin Abdulaziz Street, As Sulimaniyah, Riyadh 12232, with a Saudi phone and fax number. That address aligns closely with the RIPE organisation record's Riyadh/Sulaymaniyah information. The point is not that a contact page proves scale. It is that EBTTIKAR presents a local operating surface, and the RIPE record independently connects the same company name to Saudi number resources.

Localisation also appears in the service catalogue. The telecom page describes wireless and mission-critical communications for logistics, mining, public safety, smart cities, industrial sites and commercial facilities. The consultancy page mentions business continuity, disaster recovery, policy development, auditing and ITIL implementation. The SOC/NOC page promises round-the-clock support and monitoring. Those are labour products. They require certified engineers, support shifts, escalation procedures, vendor relationships and management discipline.

Support labour is expensive because it cannot be fully automated away. A monitoring tool can alert, but someone must decide whether the alert is noise, a customer incident, an upstream problem or a security event. A backup tool can schedule copies, but someone must test restoration and document recovery. A wireless vendor can sell hardware, but someone must survey sites, install, configure, maintain and troubleshoot. A cloud provider can supply infrastructure, but someone must build identity, network policy, logging, governance and cost controls.

The assignment's phrase "hosting continuity before raw speed" fits this labour reality. For EBTTIKAR, the continuity account is not simply a server staying online. It is the continuity of enterprise operations across cloud, on-premises equipment, branch networks, cyber monitoring and support response. A buyer pays because service interruption creates business disruption, not because the invoice line says "hosting."

The public limit is that labour capacity is mostly private. EBTTIKAR's site uses terms such as certified professionals, certified teams and certified engineers. It does not publish staff rosters, shift coverage, training records, ticket response distributions or engineer utilisation. The clients page gives project-style staff counts, but those are company-published claims.

A serious buyer should ask for the staffing plan behind any managed-service contract, the escalation process, named delivery roles, replacement coverage, language support, and evidence that the promised labour is not merely borrowed from vendors after a ticket is opened.

Public project signals without invented contracts

The most tempting EBTTIKAR page is the clients page at https://ebttikar.com/clients/. It says "Projects We're Proud Of" and lists metrics such as 157 staff for managed services for infrastructure and applications, SLA-based work, 20+ years partnership, 20,000 tickets monthly, 98% SLA, desktop, CCTV and network corrective and preventive maintenance, microwave and LTE or 4G/5G towers, NE/FE, 3,000 ATMs or branches, 4,200, 77 staff for IT operations managed services, 115 staff for managed services for infrastructure, 52 staff for SLA-based work, SAR 60 million managed services for infrastructure across headquarters, branches and offices, 220 staff, a proactive monitoring centre with 13 staff, managed services across 12 cities, 61+ hospitals and 150+ clinics, 250 staff for hybrid managed services for infrastructure and applications, 42 applications, Cisco frame infrastructure and cybersecurity across 30+ affiliates and 2,000+ devices, professional outsourcing with 34 staff, and smart labs for 70 schools.

Those data points are useful, but they must be bounded. The page does not name customers in the extracted public text, does not provide contract documents, does not show procurement award references and does not independently verify the metrics. It should therefore be treated as company-published market signal, not confirmed customer evidence. The economic value is still meaningful: the page shows that EBTTIKAR wants to be evaluated as a labour-intensive managed-service provider, not only as a hardware reseller.

The signal matches the service catalogue. Staff counts, tickets, SLA language, branches, hospitals, clinics, devices, applications, monitoring centres and outsourcing all describe continuity economics. The buyer is not paying for a static asset. The buyer is paying for people to keep systems working across many locations and exceptions. If those projects are active and accurately described, EBTTIKAR may have a real operating base in support labour. If they are old, overstated, thinly staffed or dependent on subcontractors, the public signal is weaker.

The lack of named customers is not unusual for enterprise IT services. Confidentiality, public-sector procurement rules, banking security, healthcare sensitivity and partner-channel arrangements can all limit public case studies. But the absence matters. It means outside readers cannot verify customer concentration, industry mix, renewal duration or satisfaction. A company can have large projects and still have weak margins if support scope is underpriced or if one large account consumes too much labour.

This is where public-record limits become economic facts. In a continuity business, proof of work is not enough; proof of profitable, renewable work is what matters. EBTTIKAR's public project signals suggest the type of account that could produce recurring revenue. They do not show whether the accounts renew, whether service credits are paid, whether margins cover labour, whether the customer base is diversified, or whether EBTTIKAR controls the critical tooling.

The right diligence question is not "Are the project metrics real?" as a yes-or-no public verdict. It is "What private evidence would let a buyer, lender or partner price the account?" Useful evidence would include signed scope summaries, anonymised renewal cohorts, service-level achievement logs, ticket aging, escalation times, gross margin after labour and vendor costs, customer concentration, account age, and reference calls. Without those, the public article can say EBTTIKAR has a credible continuity-market posture, not a proven revenue base.

Revenue logic without public revenue

No audited revenue, segment revenue, customer count, margin or order backlog was found in the public sources reviewed for this article. That limitation matters because EBTTIKAR's service catalogue could support several very different business models. It could be a profitable managed-services firm with recurring enterprise accounts. It could be a project-heavy systems integrator with uneven revenue. It could be a labour-outsourcing business with thin margins. It could be a vendor partner whose economics depend on product resale. It could be a combination of all four.

The revenue logic implied by the public pages is recurring plus project-based. Managed services, SOC/NOC, IT operations, monitoring, endpoint management, asset management and support desks lend themselves to monthly or multi-year service contracts. Cloud and infrastructure, data-centre design, wireless deployments, cybersecurity assessments, penetration testing, GRC projects and telecom installations can be project-based. Vendor partnerships can create resale or implementation margin. Outsourcing can produce staff-based revenue. The attractive version is a blended account in which project work leads to managed-service renewal.

Pricing should therefore be understood through avoided disruption. A buyer compares the renewal price with the cost of a migration project, the risk of downtime, the time to document the environment, the effort to replace vendor-specific skills, the cost of hiring internal support, the cyber review required for a new provider, the procurement delay of changing suppliers and the reputational cost of a failed transition. The invoice may look like cloud, monitoring, cybersecurity or managed services. The economic value is avoided interruption.

That value is highest when EBTTIKAR touches several layers at once. A customer that uses EBTTIKAR for wireless connectivity, branch support, managed infrastructure, SOC/NOC, backup and vendor implementation may face high switching costs. A customer that only bought a one-time hardware installation can replace the provider more easily. A customer that uses EBTTIKAR for a healthcare system, 24/7 monitoring or multi-site support has a different risk profile from a customer that only uses EBTTIKAR for advice.

Margin depends on the same layers. Support-heavy contracts can be sticky but labour-intensive. Cloud and security products can be profitable if the provider adds configuration, monitoring and response; they can be low-margin if the provider merely resells licences. Telecom deployments can generate project revenue but require certified engineers, spare parts, site access and maintenance. Data-centre design and backup work can be valuable but exposes the provider if recovery fails.

The public record does not show pricing. That is not a weakness by itself; enterprise services are often bespoke. But it makes comparison harder. Buyers should demand clarity about what is included, which hours are covered, which vendor subscriptions are passed through, what happens after scope changes, how renewals are priced, how service credits work, and what data or configuration the customer can take during exit. Continuity pricing works only when both sides understand the cost of keeping the environment stable.

How a buyer should price the account

The practical pricing exercise starts with a map of what breaks during exit. The buyer should separate portable items from sticky items. Portable items include commodity compute, standard email licences, ordinary laptops, basic firewall hardware, a public website and off-the-shelf software subscriptions. Sticky items include undocumented network exceptions, old branch equipment, camera systems, wireless backhaul, bespoke monitoring, backup routines, local support habits, vendor escalation paths, endpoint coverage, incident history and management reports that executives already use.

That distinction changes the renewal conversation. If most of the account is portable, EBTTIKAR faces direct price competition from cloud platforms, other local providers and resellers. If much of the account is sticky, the renewal price can be higher than a simple market quote and still be rational. The buyer is not only comparing monthly fees. It is comparing the cost of rebuilding operational memory.

Operational memory has several components. The first is configuration memory: who knows which systems exist, how they are connected, what exceptions were made, which passwords and admin roles are controlled, and which services depend on older equipment. The second is incident memory: who remembers recurring faults, past outages, vendor weaknesses, fragile sites and the real escalation path when ordinary support fails. The third is procurement memory: who can navigate the buyer's approvals, local paperwork, Arabic and English communication, site access and service reporting.

The fourth is vendor memory: who has the right contacts, certifications and support entitlements with upstream suppliers.

EBTTIKAR's public pages support the idea that it wants to sell these forms of memory. Managed services, consultancy, SOC/NOC, cyber controls, telecom engineering and cloud infrastructure all require retained knowledge. The company's clients page adds a labour-heavy signal with staff counts, ticket volumes and SLA language. The public record does not prove that this memory is well maintained. But if it is, the account is economically different from a commodity hosting account.

The buyer should also price the cost of doing nothing. Delayed migration is a real substitute because it preserves budget and avoids immediate risk. It can be rational when the current service works and the buyer lacks internal capacity to change. It becomes dangerous when delay hides technical debt: untested backups, unsupported hardware, stale firewall rules, weak endpoint coverage, unknown cloud spend, poor identity controls or undocumented branches. A continuity provider benefits from delay only if it uses the extra time to reduce risk. If it merely collects renewal fees while risk accumulates, the account becomes brittle.

The second pricing question is whether EBTTIKAR reduces supplier complexity or simply adds another layer. A good local integrator translates global technology into a manageable operating model. It consolidates support, gives the buyer one place to escalate, and coordinates cloud, hardware, monitoring, network and cyber suppliers. A weak integrator forces the buyer to pay an extra margin while still chasing the underlying vendor during incidents. The difference is visible only in service records, not in marketing language.

The third question is whether localisation is genuinely valuable for the buyer. Local Saudi support can matter for site access, language, branch work, government-facing documentation, cyber-control interpretation, physical installation and emergency coordination. But localisation is not automatic quality. A buyer should ask how EBTTIKAR staffs local support, which skills are in-house, which are subcontracted, which locations are covered, how urgent site visits are handled, and how after-hours work is paid.

The fourth question is whether the network-resource footprint is part of the account or only background. AS211226 and 193.34.224.0/24 give EBTTIKAR a visible internet-number surface. For some managed-service accounts that may matter little. For others, it may affect VPNs, monitoring, hosted services, security platforms, customer addresses, mail reputation or connectivity. Because the visible routed footprint is small, customers should not assume large hosting capacity. They should ask exactly where their systems run, who controls addresses, how routes are secured, and whether the resource footprint is used in their service.

The fifth question is whether the account can survive staff turnover. In labour-heavy IT services, continuity can collapse when a few engineers leave. The buyer should ask how EBTTIKAR preserves knowledge in tools, documentation and team process rather than in individual memory. This is especially important for long contracts with many sites or critical cyber responsibilities. A continuity account is valuable only if the provider can keep service quality stable even as people change.

These questions do not require the buyer to reject EBTTIKAR. They make the price visible. A renewal is strong if EBTTIKAR can show that it reduces outage risk, lowers internal workload, keeps vendor complexity under control, supports Saudi operating needs and gives the buyer a fair exit path. A renewal is weak if the account is mostly product resale, undocumented labour, fragile upstream dependence and inertia. The public record supports asking the question; it does not answer it completely.

Upstream technology dependence is part of the product

EBTTIKAR's own pages make upstream technology dependence visible. The home page names partnerships and awards involving Huawei, Dell Technologies, EdgeCortix, Cisco, Westcon-Comstor and other technology brands. The about page names Cisco, Huawei, HP, Dell EMC, Amazon, Nutanix and Symantec among global technology relationships. The alliances page at https://ebttikar.com/alliances/ says EBTTIKAR has more than 12 strategic partnerships and uses those relationships for access to technologies, support, training and product certification. The SOC/NOC page names Cisco, SolarWinds and AppDynamics. The telecom page names Rajant, Cambium Networks, Motorola Solutions, Hytera, Rohde & Schwarz and ZD Energy.

Those upstream relationships can be a strength. Saudi enterprise buyers may want local implementation teams for global products. Vendor access, certification, Arabic or local support, warranty handling, training and procurement familiarity can reduce friction. A buyer might prefer a Saudi partner that can coordinate products, site work and support rather than directly managing many vendors.

The same relationships are also a dependency. If EBTTIKAR's service promise relies on Cisco security products, SolarWinds monitoring, AppDynamics application visibility, Dell or Huawei infrastructure, wireless vendors, cloud platforms or distributor terms, then EBTTIKAR's control is partial. It must keep certifications current, maintain partner status, secure stock or licence access, pass vendor support through quickly, and avoid being squeezed by vendor pricing or policy changes. A continuity provider can fail even when its staff work hard if the upstream product or supplier path fails.

The network-resource evidence adds another supplier layer. AS211226 is a real autonomous system, but RIPEstat saw one neighbour, AS29684, at the checked time, while the RIPE policy record also named AS29690. EBTTIKAR's visible routing therefore depends on upstream networks. That is normal for a smaller enterprise IT provider. It is still economically material. A customer buying continuity should ask how many upstream paths are available, whether there is physical diversity, what maintenance notices look like, how DDoS events are handled, whether there are failover tests, and who has authority to change routing.

Cloud substitutes reinforce the dependence question. AWS's official global infrastructure page at https://aws.amazon.com/about-aws/global-infrastructure/ says the AWS Cloud spans 123 Availability Zones across 39 geographic regions and shows announced plans for a Kingdom of Saudi Arabia region, with edge locations including Jeddah and Riyadh. Microsoft's Azure geography page at https://azure.microsoft.com/en-us/explore/global-infrastructure/geographies/#overview says Azure is available or coming soon to Saudi Arabia and lists Saudi Arabia East among regions. Google's Dammam access document at https://cloud.google.com/docs/dammam-region-access points to local access arrangements around the Dammam region. Hyperscale platforms are therefore not distant abstractions for Saudi buyers; they are increasingly part of the local decision set.

That does not eliminate EBTTIKAR's role. Hyperscale cloud can make infrastructure easier to buy and harder to govern. Buyers still need identity, network design, migration planning, backup, cost control, security operations, monitoring, vendor management and local support. EBTTIKAR can be valuable if it turns upstream technology into reliable local operations. It is vulnerable if customers decide that upstream platforms plus another partner can provide the same continuity at lower risk.

Competition is six different exits

The first exit is hyperscale cloud. It is attractive for buyers that want elastic compute, managed databases, global tooling, strong documentation and vendor scale. It is less simple for buyers with legacy systems, branch networks, on-premises equipment, local support needs, complex procurement or limited internal engineering. EBTTIKAR's opportunity is to manage the messy transition, hybrid model or post-migration operating layer. Its risk is that cloud-native teams bypass local service accounts.

The second exit is another Saudi host, integrator or managed-service provider. This is the closest substitute because it can also offer local labour, Arabic or bilingual support, site work and vendor relationships. EBTTIKAR competes here on support depth, certifications, project history, relationship trust, price, responsiveness and ability to retain skilled staff. A buyer unhappy with service quality can move without adopting a radically different operating model.

The third exit is a reseller platform. A web agency, MSP or specialised partner can sit between the customer and larger infrastructure providers, giving the buyer a personal account relationship without the full cost of a broad systems integrator. This substitute is strong for smaller businesses and standard workloads. It is weaker when the customer needs branch telecom, physical security, healthcare systems, large support teams, SOC/NOC, wireless engineering or detailed enterprise governance.

The fourth exit is an in-house server or in-house IT team. Some buyers prefer direct control, especially when workloads are stable and budgets are tight. In-house control can reduce external invoices but increases responsibility for patching, security, power, backup, monitoring, staffing and incident response. EBTTIKAR wins if the buyer concludes that internal teams should focus on business operations rather than day-to-day infrastructure.

The fifth exit is a website builder or software-as-a-service product. For simple public sites, booking tools, forms, content and basic commerce, the smartest move may be to stop managing infrastructure. This is a serious threat at the low-complexity end of the market. EBTTIKAR has little defence if the workload can be simplified into a managed product. It matters where the customer needs systems integration, data flows, custom applications, local networks, security controls or enterprise support.

The sixth exit is delay. Many buyers renew because switching is annoying. Delay can look like loyalty, but it is weaker. A customer that renews only because migration is hard may leave after a bad outage, security incident, billing dispute or staff change. A continuity provider must convert friction into trust. The renewal must feel like a rational risk decision, not a trap.

These exits show why EBTTIKAR's strongest defence is not raw speed. It is operating knowledge. If EBTTIKAR knows the environment, maintains support quality, coordinates vendors, documents changes, and helps the buyer reduce risk, it can retain accounts even when cheaper options exist. If it underdelivers, the same embeddedness becomes a liability, and customers will use the next renewal or incident to exit.

Regulation and market context

Saudi cloud and cybersecurity rules shape the buyer's risk calculus. CST's cloud-computing regulations page at https://www.cst.gov.sa/en/regulations-and-licenses/regulations/Document-1550 says the update was issued to develop the communications and information technology sector, stimulate investment in cloud computing, enhance competition, raise service quality and empower cloud computing service providers, while addressing obligations and rights for providers, individual users and government and private sectors. That context supports demand for cloud and managed services, but also raises expectations.

NCA's regulatory-documents index at https://nca.gov.sa/en/regulatory-documents/ lists controls and standards such as Essential Cybersecurity Controls, Critical Systems Cybersecurity Controls, Operational Technology Cybersecurity Controls, National Cryptographic Standards, Cybersecurity Guidelines for e-Commerce and Data Cybersecurity Controls. This does not prove EBTTIKAR is compliant with every relevant control or certified for every buyer. It shows why Saudi customers may ask for documented security operations, controls mapping, logs, incident response, data protection and governance.

For EBTTIKAR, regulation is both demand and cost. It increases the need for local cybersecurity, monitoring, GRC, data protection, backup and incident response services. It also makes weak delivery riskier. A provider selling SOC-as-a-Service, NOC, GRC, vulnerability management and incident response must have credible processes. The customer's compliance exposure does not disappear because a provider's page lists services.

Operational risk is broader than regulation. EBTTIKAR depends on skilled labour, vendor certifications, upstream networks, equipment supply, software licences, customer trust, ticket discipline and site access. The public routing footprint is small, so route resilience should be checked. The public cloud and managed-service pages are broad, so delivery capacity should be checked. The clients page gives strong project-style metrics, so verification should be checked. The company claims awards and partnerships, so current partner status should be checked.

Geopolitical and supply-chain risk should be framed carefully. Saudi Arabia is a major and growing technology market, but enterprise IT providers still depend on imported hardware, global software licences, cloud platform availability, cross-border support channels and cyber-threat conditions. EBTTIKAR's public pages show reliance on global technology partners. That can improve capability and create upstream exposure at the same time.

The regulatory conclusion is balanced. Saudi market conditions can favour a local integrator with cybersecurity, cloud, managed services and telecom capability. They do not guarantee success. The providers that win must show evidence: service governance, trained staff, incident history, recovery testing, documented controls, customer references and contractual clarity.

What would change the judgement

The first fact that would improve confidence is verified renewal evidence. If EBTTIKAR can show that managed-service, SOC/NOC, cloud or infrastructure customers renew after service reviews and incidents, the continuity thesis becomes much stronger. If customers churn after projects complete, the thesis weakens.

The second fact is support performance. Ticket volume is useful only when paired with response time, resolution time, escalation rate, first-contact resolution, after-hours coverage, root-cause analysis and customer satisfaction. EBTTIKAR's public page mentions 20,000 monthly tickets and 98% SLA in a project context, but the public record does not show the underlying logs or customer verification.

The third fact is facility control. EBTTIKAR's cloud and infrastructure page refers to data-centre operations, design and architecture. It does not verify ownership of a data centre, leased capacity, certifications, power design, carrier list, remote-hands capability or physical security controls. Buyers should not infer facility ownership from service language.

The fourth fact is vendor dependence and partner currency. EBTTIKAR's pages name many global technology partners. Useful diligence would show current partner tiers, certification counts, support entitlements, renewal dates, distributor terms, escalation paths and whether customer contracts depend on a specific upstream vendor.

The fifth fact is network resilience. Public records show ORG-ETCL2-RIPE, AS211226, 193.34.224.0/24 and an observed AS29684 path. The private questions are transit diversity, physical path diversity, route-change controls, RPKI plans, DDoS response, monitoring, maintenance windows and who handles abuse or routing incidents.

The sixth fact is customer concentration. EBTTIKAR's clients page suggests sizeable managed-service projects but does not identify buyers. A provider with many diversified accounts is different from one that depends on a few large contracts. Concentration affects renewal risk, staffing risk and bargaining power.

The seventh fact is labour economics. A continuity provider must pay for skilled staff before an incident happens. The question is gross margin after salaries, subcontractors, vendor licences, training, support tooling, field travel and management overhead. Underpriced support can look like growth until the staff model breaks.

The eighth fact is exit fairness. Customers value continuity when the provider can help them leave cleanly if needed: documentation, data export, configuration handover, backup transfer, admin credential process and transition support. A provider that makes exit painful may retain short-term revenue but damage long-term trust.

The ninth fact is independent market evidence. Public customer case studies, procurement references, awards verified by third parties, regulator listings, support reviews, partner directories and audited statements would all improve confidence. Company-owned pages are useful but not sufficient.

The tenth fact is product focus. EBTTIKAR's public pages are broad. Breadth can win if the company has the staff, partners and governance to integrate services. Breadth can also dilute execution. A clearer public explanation of which accounts are core, where the company has repeatable delivery and where it uses partners would sharpen the investment view.

Final assessment

EBTTIKAR TECHNOLOGY Company Ltd matters because it sits in the practical middle of Saudi enterprise IT. It is not best understood as a pure host competing only on server speed. It is a local technology services account selling managed operations, cloud and infrastructure support, SOC/NOC, cybersecurity, telecom engineering, consulting, continuity planning and vendor-enabled implementation. The buyer pays for the fact that moving these functions is costly once they are connected to live business systems.

The public evidence is stronger on service positioning than on financial proof. EBTTIKAR's own site gives a rich picture of its intended market: enterprise IT services in Saudi Arabia, managed services, cloud and infrastructure, SOC/NOC, cyber and network security, telecom services, consultancy and technology partnerships. RIPE and RIPEstat confirm a real Saudi LIR and routed AS footprint, but the visible public network surface is small: one IPv4 /24, one observed neighbour and no visible IPv6 at the checked time.

That combination supports a cautious thesis. EBTTIKAR's value is not raw network scale. Its value, if durable, is support labour and continuity knowledge: knowing the customer's systems, integrating upstream technology, handling local implementation, monitoring operations, responding to incidents and reducing the risk of migration. This can be economically attractive in Saudi Arabia, where enterprise technology demand, cyber controls, localisation and cloud adoption create demand for trusted local operators.

The limits are just as important. Public sources do not verify revenue, churn, contracts, customer names, facility ownership, support headcount, uptime history, service credits, upstream commercial terms or margins. Company-published project metrics should be treated as market signals, not confirmed contracts. A buyer or partner should verify the private facts before treating EBTTIKAR as a high-confidence recurring-revenue business.

The final judgement is therefore conditional but substantive. EBTTIKAR sells hosting continuity before raw speed because its public offer is about keeping enterprise systems working, not simply providing a faster port. The company earns attention where Saudi buyers face migration friction, support labour scarcity, cybersecurity requirements, local procurement needs and upstream technology complexity. The question is not whether substitutes exist. They do. The question is whether EBTTIKAR's local service account lowers the risk and total cost of continuity enough for buyers to renew.